Embed Size (px)

Citation preview

Budget and Budgetary Control

Budget

CIMA, London has defined budget as “a financial and/or quantitative statement, prepared prior to a defined period of time, of the policy to be pursued during that period for the purpose of attaining a given objective.”

It may include income, expenditure and employment of capital.

BudgetAccording to Gorden Shillinglaw, A budget is ‘ a

predetermined detailed plan of action developed and distributed as a guide to current operations and as a partial basis for the subsequent evaluation of performance’.

Following are the essentials of a budget: It is prepared in advance and is based on a

future plan of action. It relates to a future period and is based on

objectives to be attained. It is a statement expressed in monetary and/or

physical units prepared for the implementation of policy formulated by the management.

Characteristics of budget

• A budget is primarily a planning device but it also serves as a basis for performance evaluation and control

• A budget is prepared either in money terms or in quantitative terms or in both

• A budget is prepared for a definite future period• Purpose of budget is to implement the policies

formulated by the management for attaining the given objectives

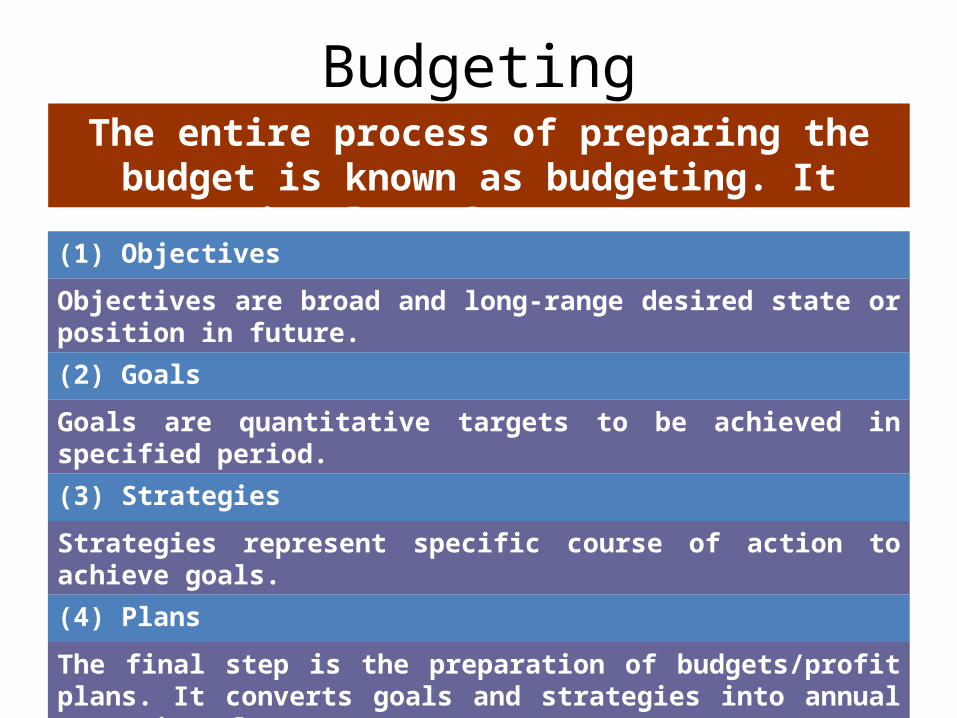

BudgetingThe entire process of preparing the budget is known

as budgeting. It involves four steps:

(1) Objectives

Objectives are broad and long-range desired state or position in future.

(2) Goals

Goals are quantitative targets to be achieved in specified period.

(3) Strategies

Strategies represent specific course of action to achieve goals.

(4) Plans

The final step is the preparation of budgets/profit plans. It converts goals and strategies into annual operating plans..

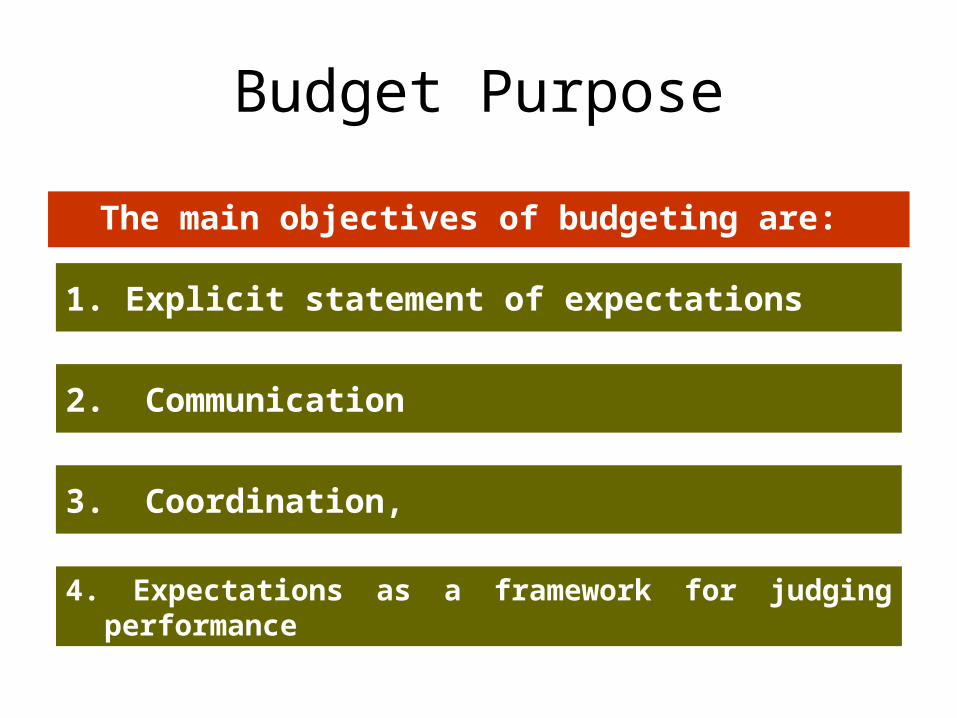

Budget Purpose

The main objectives of budgeting are:

1. Explicit statement of expectations

2. Communication

3. Coordination,

4. Expectations as a framework for judging performance

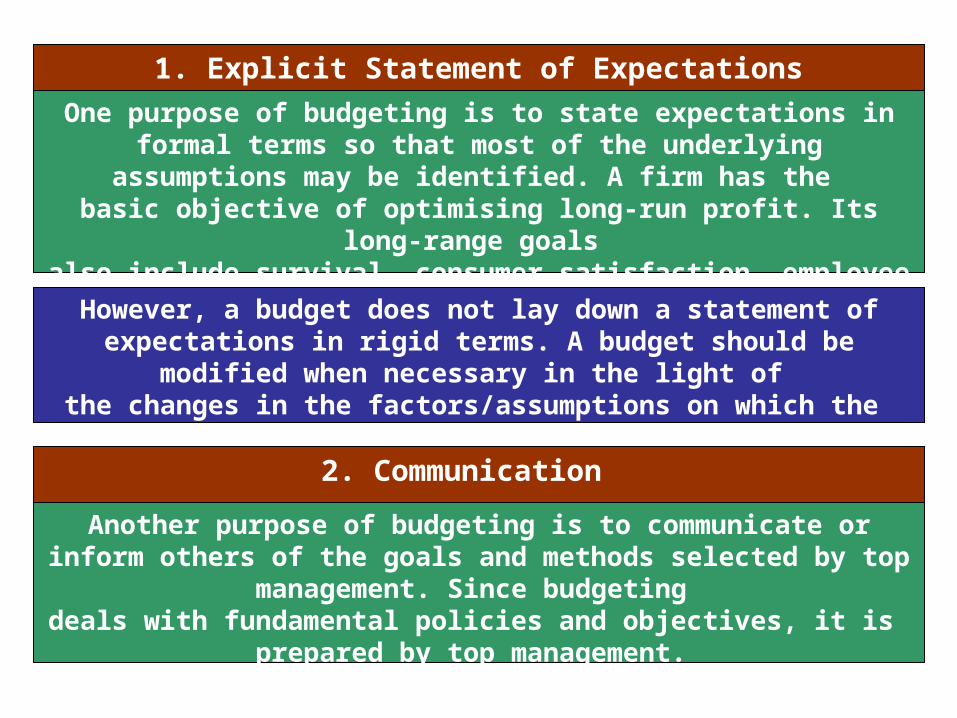

One purpose of budgeting is to state expectations in formal terms so that most of the underlying assumptions may be identified. A firm has the

basic objective of optimising long-run profit. Its long-range goals also include survival, consumer satisfaction, employee

welfare, personal power and prestige, and so on.

Another purpose of budgeting is to communicate or inform others of the goals and methods selected by top management. Since budgeting

deals with fundamental policies and objectives, it is prepared by top management.

However, a budget does not lay down a statement of expectations in rigid terms. A budget should be modified when necessary in the light of

the changes in the factors/assumptions on which the original estimates were based.

1. Explicit Statement of Expectations

2. Communication

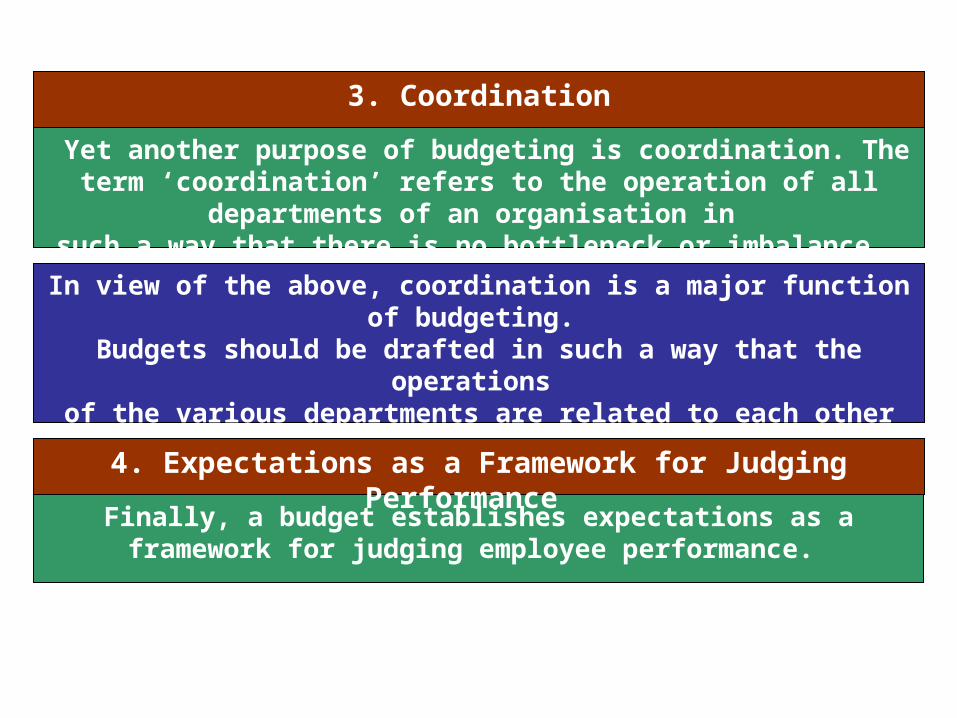

Yet another purpose of budgeting is coordination. The term ‘coordination’ refers to the operation of all departments of an organisation in

such a way that there is no bottleneck or imbalance.

Finally, a budget establishes expectations as a framework for judging employee performance.

In view of the above, coordination is a major function of budgeting. Budgets should be drafted in such a way that the operations

of the various departments are related to each other for the achievement of the overall goal.

3. Coordination

4. Expectations as a Framework for Judging Performance

9

Budgetary ControlIt is the system of management control and

accounting in which all operations are forecasted and so far as possible planned ahead, and the actual results compared with the forecasted and planned ones. Thus, budgetary control involves :

Establishment of budgets. Continuous comparison of actual with

budgets for target achievement and variance analysis.

Revision of budgets in the light of changed circumstances.

Characteristics of budgetary control• Establishment of budgets for each

function/department of the organisation• Comparison of actual performance with the

budgets on a continuous basis• Analysis of variations of actual performance

from that the budgeted performance to know the reasons thereof

• Taking remedial actions, where necessary• Revision of budgets in view of changes in

conditions

• The difference between, budgets, budgeting and budgetary control has been stated as , ‘Budgets are the individual objectives of a department etc., where as budgeting may be said to be the act of building budgets. Budgetary control embraces all and in addition includes the science of planning the budgets themselves and the utilization of such budgets to effect an overall management tool for the business planning and control.’

Objectives of budgetary control

• Planning• Co-ordination• Communication• Motivation• Control• Performance evaluation

13

Budgetary Control As A Management ToolAdvantages of Budgetary Control : Budgeting compels managers to think ahead – to

anticipate and preparing for future conditions. Budgeting coordinates the coordinates the activities

of various departments and functions of the business Increases production efficiency, eliminates waste and

control the cost. It pinpoints efficiency or lack of it It aims at maximisation of profit through careful

planning and control It provides a yardstick against which actual results can

be compared

Advantages of Budgetary Control :

• It shows management where action is needed to remedy a situation

• It directs capital expenditure in most profitable direction• It instills into all levels of management a timely, careful

and adequate consideration of all factors before reaching important decisions

• A budget motivates the executives to attain given goals• Budgeting also aids in obtaining bank credit• A budgetary control system assists in delegation of

authority and assignment of responsibility

15

Classification of Budgets

According to time: Long term Budget: Designed for a long period, generally 5

to 10 yrs. Concerned with the planning of the operations of a firm over a considerably long period of time.

Short term Budget : Designed for a period generally not exceeding 5 yrs.

Current budgets: Cover a very short period, say a month or a quarter. They are essentially short term budgets adjusted to current conditions.

Rolling Budgets: A new budget is prepared at the end of each month or quarter for a full year ahead. The figures for the month or quarter which has rolled down, are dropped and the figures for the next month or quarter are added.

16

Classification of Budgets ( Contd )According to function: Sales Budget: It is a forecast of sales to be achieved in a budget period.

The sales budget can be prepared to show sales classified according to products, salesmen, customers, territories and periods etc. Factors to be considered while preparation of sales budget include past sales figures and trends, Salesmen’s estimates, Plant capacity, Orders in hand, Seasonal fluctuations, Potential market etc.

Production Budget: Provides an estimate of the total volume of production

product-wise, with the scheduling of operations by days, weeks and months and a forecast of the closing finished product inventory. The key considerations involved in budgeting production are:

Sales Budget, Inventory policy which depends upon factors like storage facility, perishability of the product, risk of price changes etc., Production capacity, management policy.

Production cost budget: It shows the estimated cost of production. The quantities of production budget are expressed in terms of cost in detail with respect to elements of cost.

Purchase Budget: Forecasts the quantity and value of purchases required for production. It indicates the quantities of each type of raw material and other items to be purchased and the timing of purchases. This budget also depends upon many factors like Opening, closing stock, maximum and minimum stock quantities, EOQs,

Capital Expenditure Budget : Forecasts the amount of capital that may be required

for procurement of capital assets like new building, machinery, land and intangible items like patents etc. during the budget period.

• Labour budget: It represents the forecast of labour requirements during the budget period. This budget may be linked with production budget and production cost budget. Its purpose includes:

a) To estimate the labour cost of productionb) To determine the direct labour required in terms of

labour hours and hence the number and grade of workers to meet production requirement

c) To provide the personnel department with personnel requirement

d) To determine cash requirement for payment of wages and salaries

e) To provide data for managerial control of labour cost

Similarly we have, Production overhead budgetSelling and Distribution cost budgetAdministration cost budget

20

Classification of Budgets ( Contd ) Cash Budget: Forecasts the estimated amount of cash receipts and

payments and the likely cash balance in hand at the end of different periods. A cash budget helps the management in

i) Determining the future cash needs of the firm.ii) Planning for financing of those needsiii) Exercising control over cash and liquidity of the firm. A Cash budget can be prepared in any of the following

three ways:i. Receipts and Payments Method : Cash receipts and

payments from various sources are estimated and a budget is prepared using the estimates.

ii. Adjusted Profit & Loss Account Method: Cash budget is prepared on the basis of opening cash and bank balances,

21

Classification of Budgets ( Contd ) projected profit and loss account and the balance of various

assets and liabilities. iii. Balance Sheet Method: Under this method, at the end of

each period a projected balance sheet is drawn up listing various assets and liabilities except cash and bank balances. The balancing figure is taken as the closing cash/ bank balance.

Master Budget : It is a summary budget incorporating all functional budgets in capsule form.

It has two parts i) Operating budget i.e. budgeted profit & loss account and ii) Financial budget i.e. budgeted balance sheet.

22

Classification of Budgets ( Contd )According to Flexibility:Fixed Budget : According to CIMA London, ‘ a fixed budget is a

budget which is designed to remain unchanged irrespective of the level of activity actually attained’. Hence it is unrealistic yardstick incase the level of activity actually attained does not conform to the one assumed for budgeting purposes.

Flexible Budget : According to CIMA London, a flexible budget is , ‘ a budget designed to change in accordance to the level of activity actually attained’. Thus a budget can be prepared for various level of activities say 70%, 80%, 90%, 100% capacity utilisation. Then whatever the output is achieved it can be compared with an appropriate level.

It is used on companies where it is extremely difficult to forecast output and sales with accuracy like luxury prodcuts, fashion products, export products etc.