Embed Size (px)

Citation preview

Cross-Screen Impact of

Free-to-Play

Peter Warman | CEO Newzoo | [email protected] Offenbach, November 2012

Let’s lean back for a moment.

© 2012 Newzoo www.newzoo.com

US EU* UK GER FR IT ES BE NL RU BR PL TR AUS JP CN

Newzoo research portfolio

Newzoo | The Total Picture Consumer, Transactional & Financial Data

© 2012 Newzoo 4

Several US clients cannot be

disclosed.

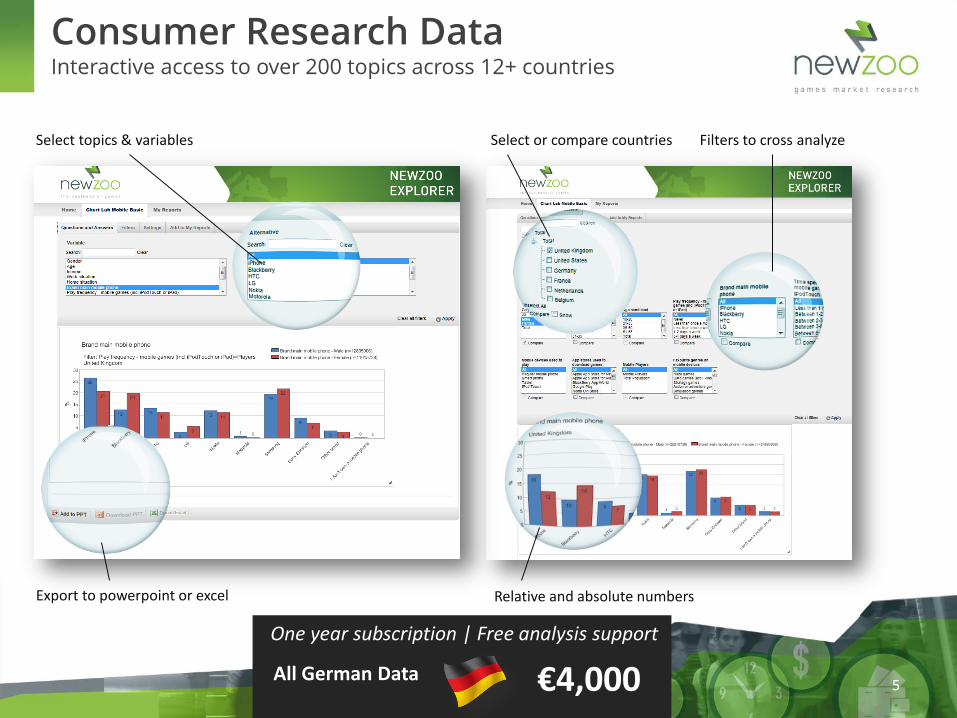

Consumer Research Data Interactive access to over 200 topics across 12+ countries

Export to powerpoint or excel

Select topics & variables Select or compare countries Filters to cross analyze

Relative and absolute numbers

5

One year subscription | Free analysis support

€4,000 All German Data

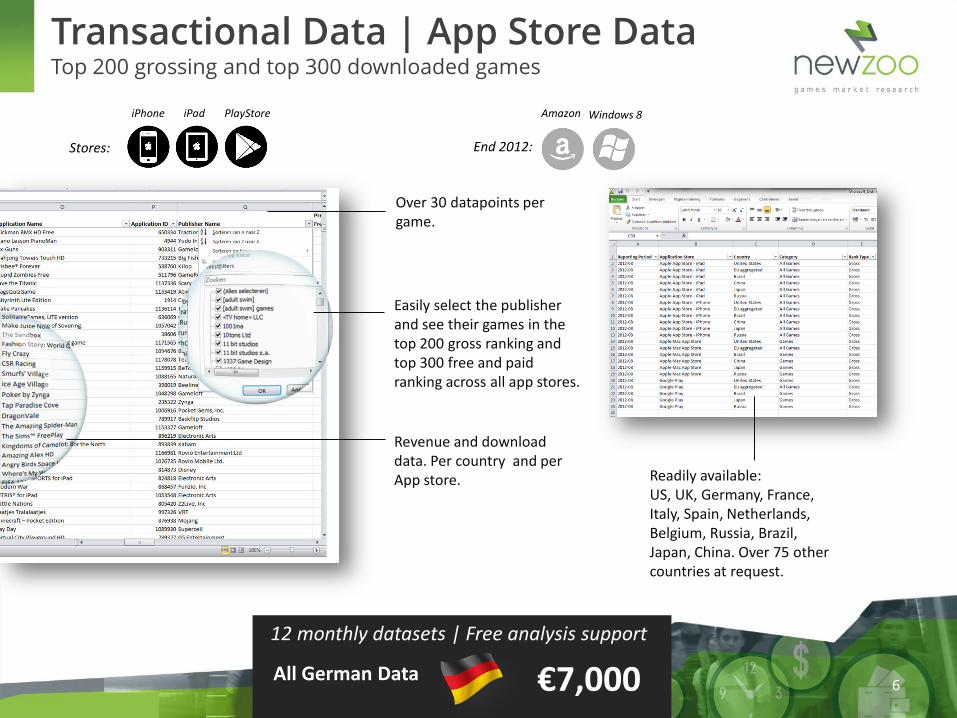

Transactional Data | App Store Data Top 200 grossing and top 300 downloaded games

Easily select the publisher and see their games in the top 200 gross ranking and top 300 free and paid ranking across all app stores.

Revenue and download data. Per country and per App store.

Over 30 datapoints per game.

Stores:

iPhone iPad PlayStore Amazon Windows 8

End 2012:

6

Readily available: US, UK, Germany, France, Italy, Spain, Netherlands, Belgium, Russia, Brazil, Japan, China. Over 75 other countries at request.

12 monthly datasets | Free analysis support

€7,000 All German Data

investors

“social gaming is dead” “social gaming was a bubble. Its gone now.”

Social Gaming vs Social Network Gaming The real world, The cloud & Social Networks connect all screens & games

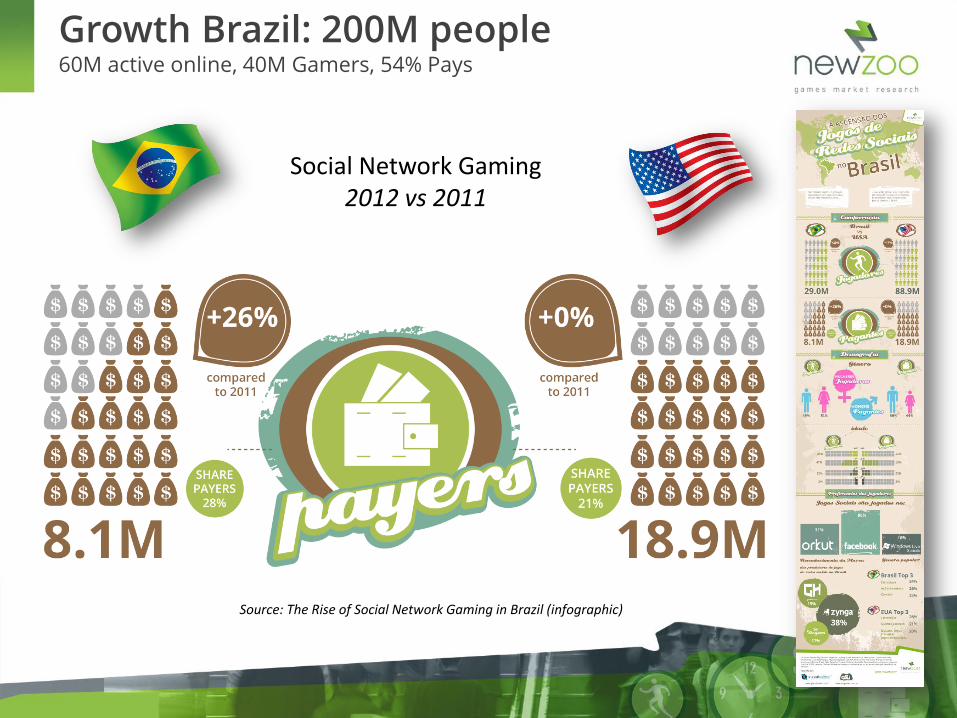

Growth Brazil: 200M people 60M active online, 40M Gamers, 54% Pays

Social Network Gaming 2012 vs 2011

Source: The Rise of Social Network Gaming in Brazil (infographic)

10

Growth Market Turkey: 78M people 30M active online, 21.8M Gamers, 52% Pays

Top 20 Mobile Publishers August 2012 Based on total iOS revenues in 9 countries across the globe

Based on total iOS (iPad/iPhone) revenues in the following countries

© 2

01

2 N

ewzo

o/D

istimo

11

Top 20 Mobile Games August 2012 Based on total iOS revenues in 9 countries across the globe

Based on total iOS (iPad/iPhone) revenues in the following countries

© 2

01

2 N

ewzo

o/D

istimo

12

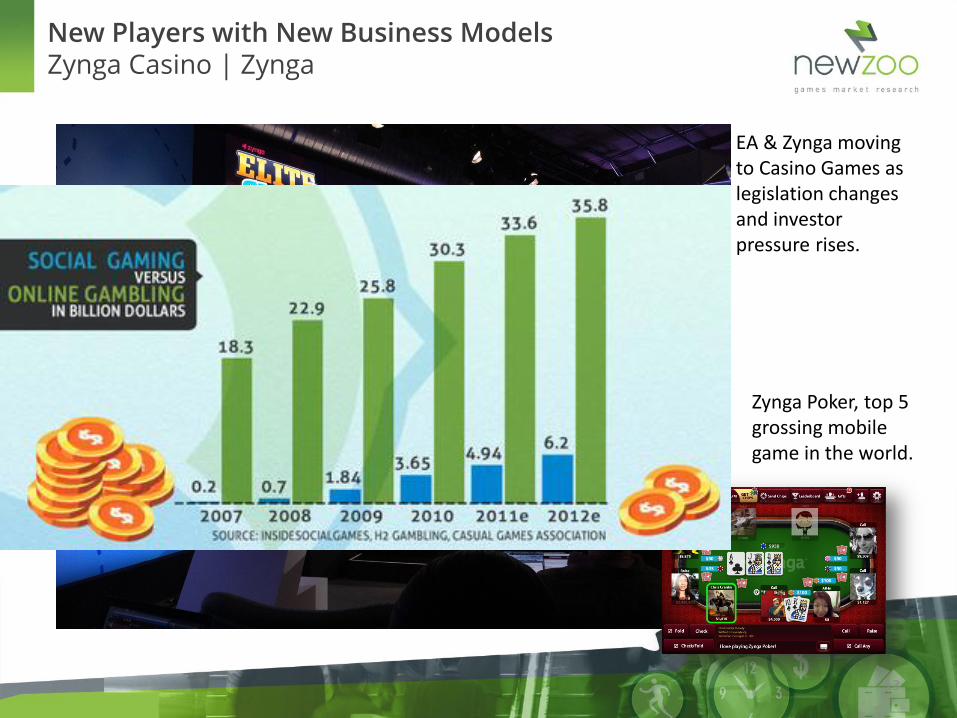

EA & Zynga moving to Casino Games as legislation changes and investor pressure rises.

Zynga Poker, top 5 grossing mobile game in the world.

New Players with New Business Models Zynga Casino | Zynga

13

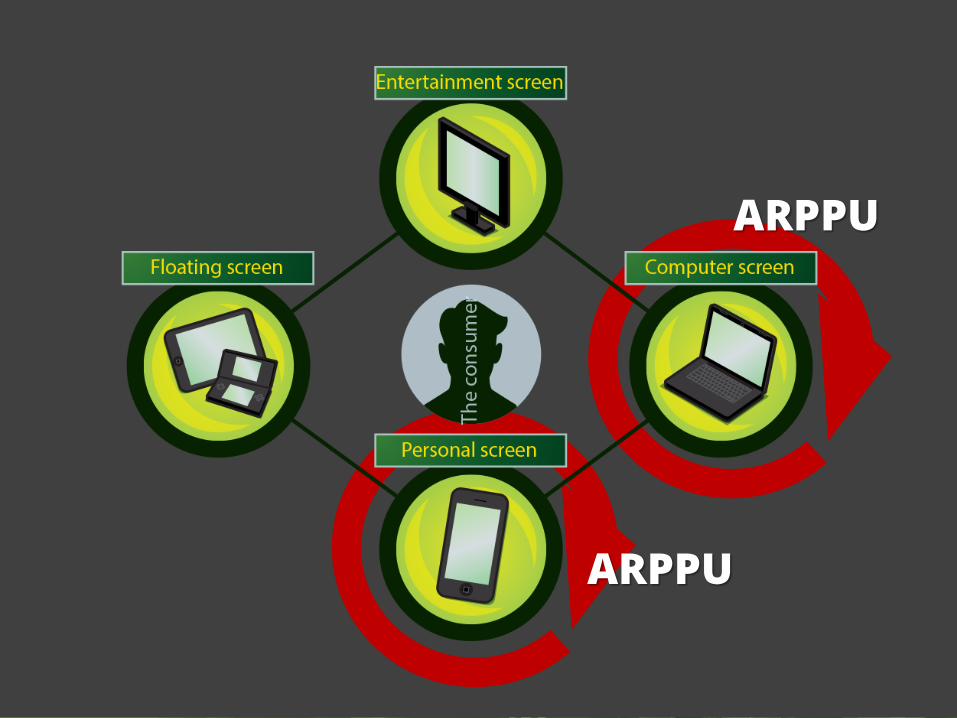

I promised that we would... Lean back

Games as Product

Games as Service

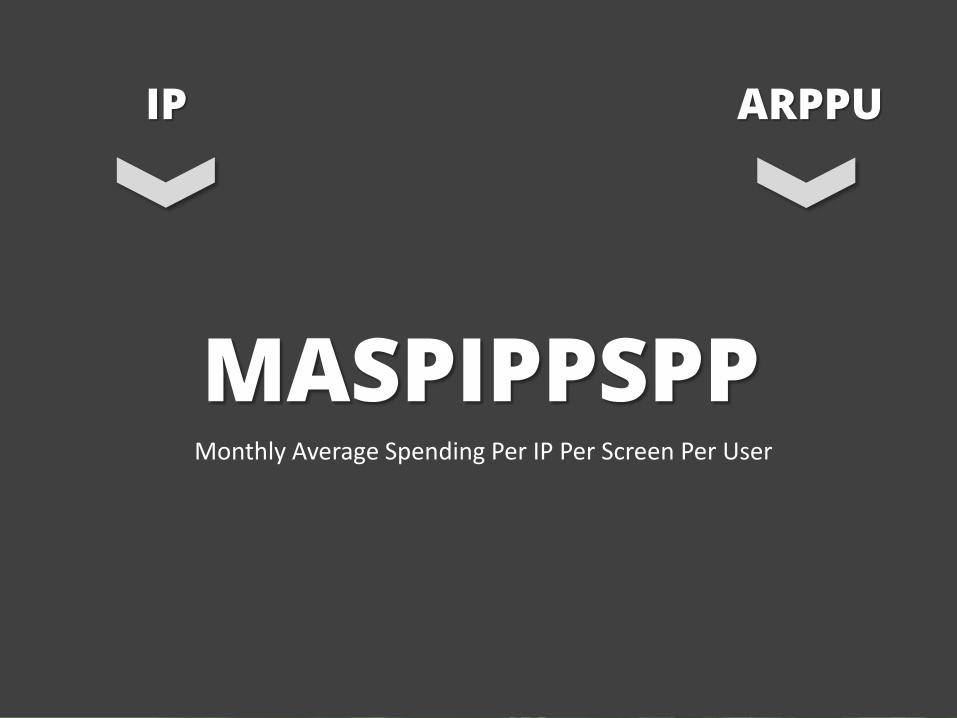

IP ARPPU

US EUROPE ASIA

TREND 2012

Games as Product

Games as Service

IP ARPPU

US EUROPE ASIA

TREND 2013

ARPPU

ARPPU

ARPPU

ARPPU

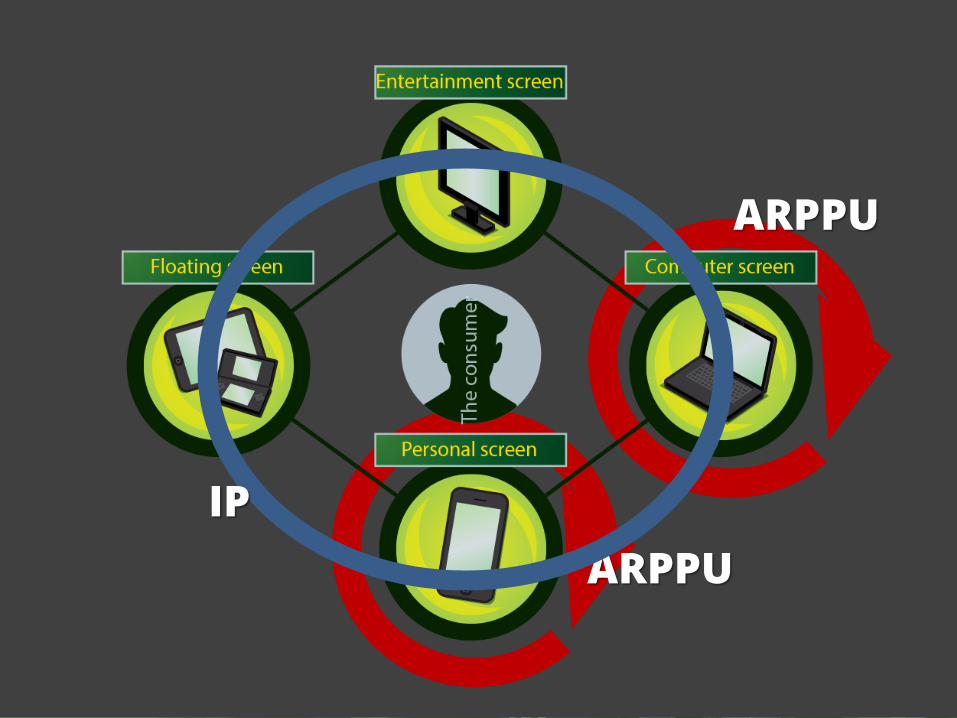

IP

IP ARPPU

MASPIPPSPP Monthly Average Spending Per IP Per Screen Per User

Lean back and….. Look at the Global/Total Picture

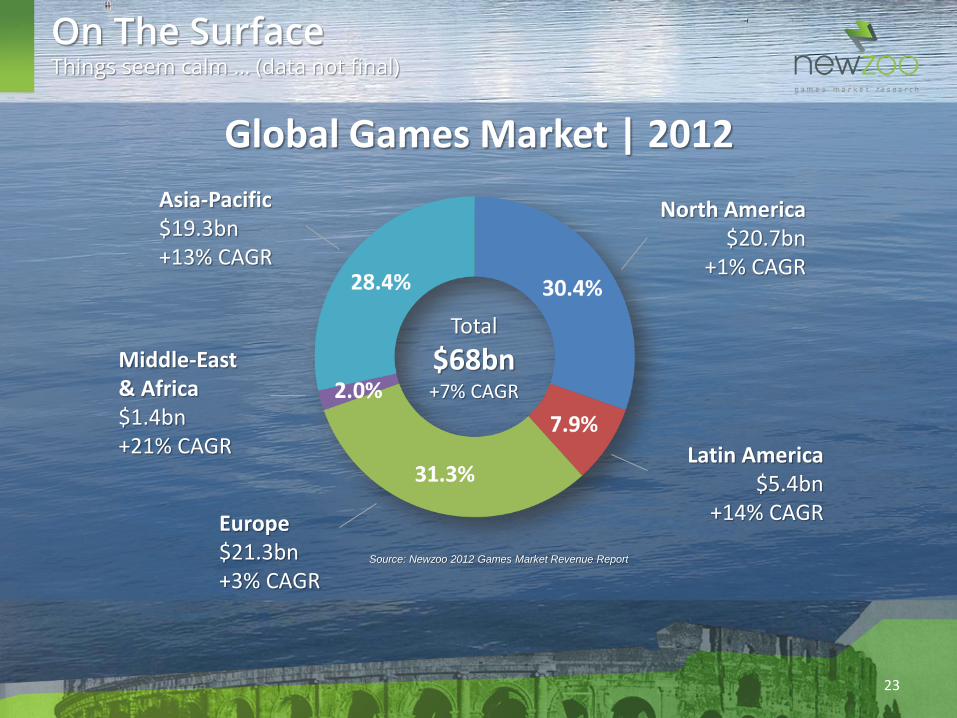

On The Surface Things seem calm … (data not final)

North America $20.7bn

+1% CAGR

Europe $21.3bn +3% CAGR

Latin America $5.4bn

+14% CAGR

Middle-East & Africa $1.4bn +21% CAGR

Asia-Pacific $19.3bn +13% CAGR

Total

$68bn +7% CAGR

Source: Newzoo 2012 Games Market Revenue Report

Global Games Market | 2012

23

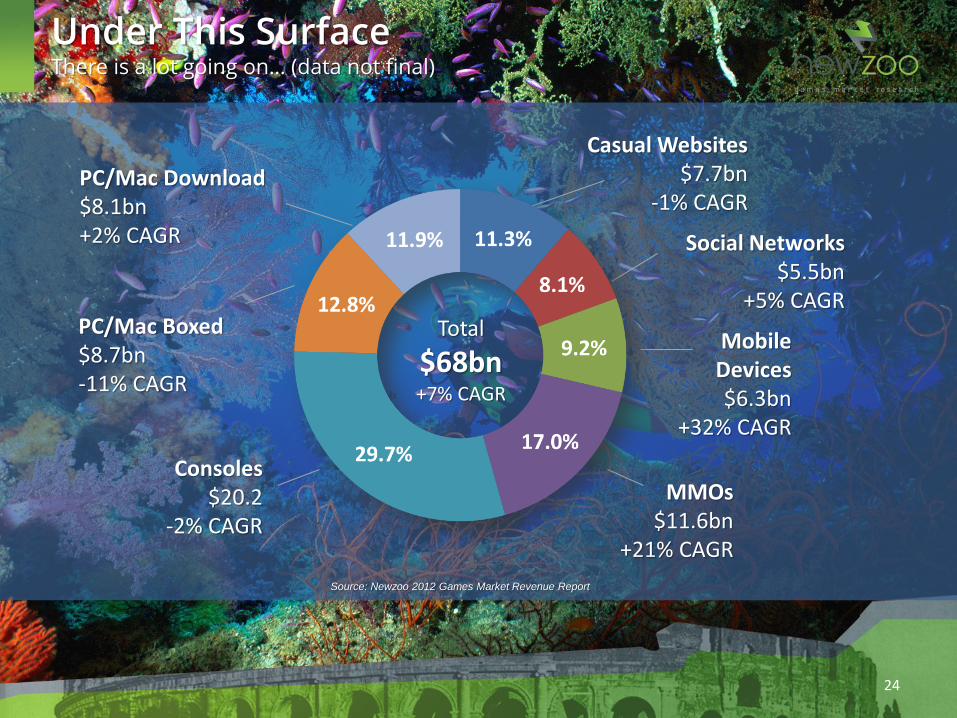

Under This Surface There is a lot going on… (data not final)

Mobile Devices $6.3bn

+32% CAGR

MMOs $11.6bn

+21% CAGR

Consoles $20.2

-2% CAGR

PC/Mac Download $8.1bn +2% CAGR

Casual Websites $7.7bn

-1% CAGR

PC/Mac Boxed $8.7bn -11% CAGR

Social Networks $5.5bn

+5% CAGR Total

$68bn +7% CAGR

Source: Newzoo 2012 Games Market Revenue Report

24

Lean back and….. Think about how to monitor change

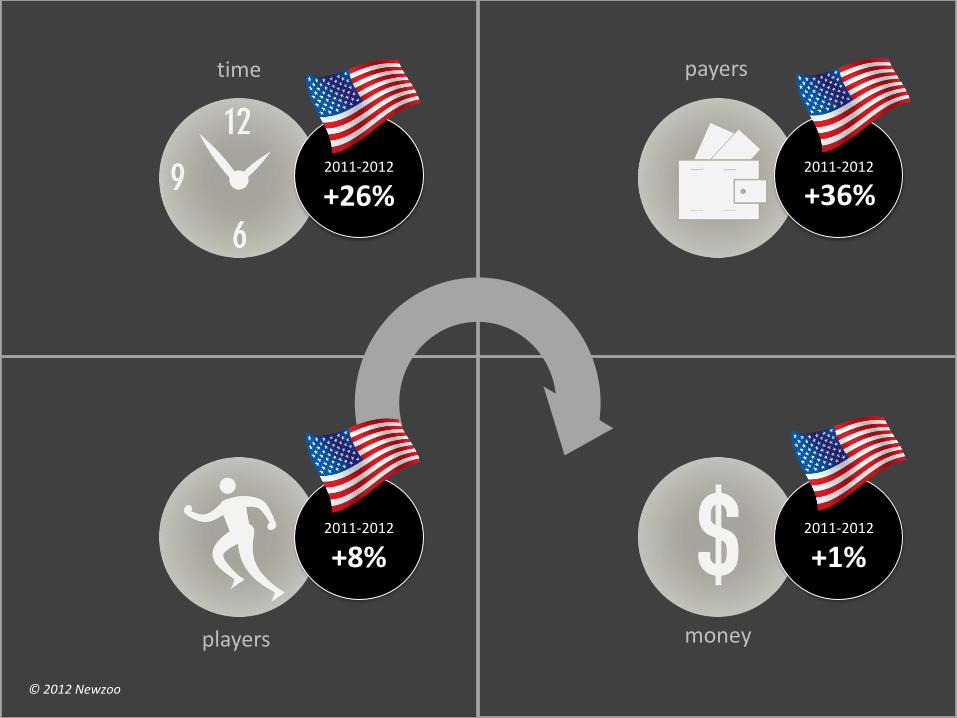

Monitoring Change | KPIs To size and seize future growth opportunities

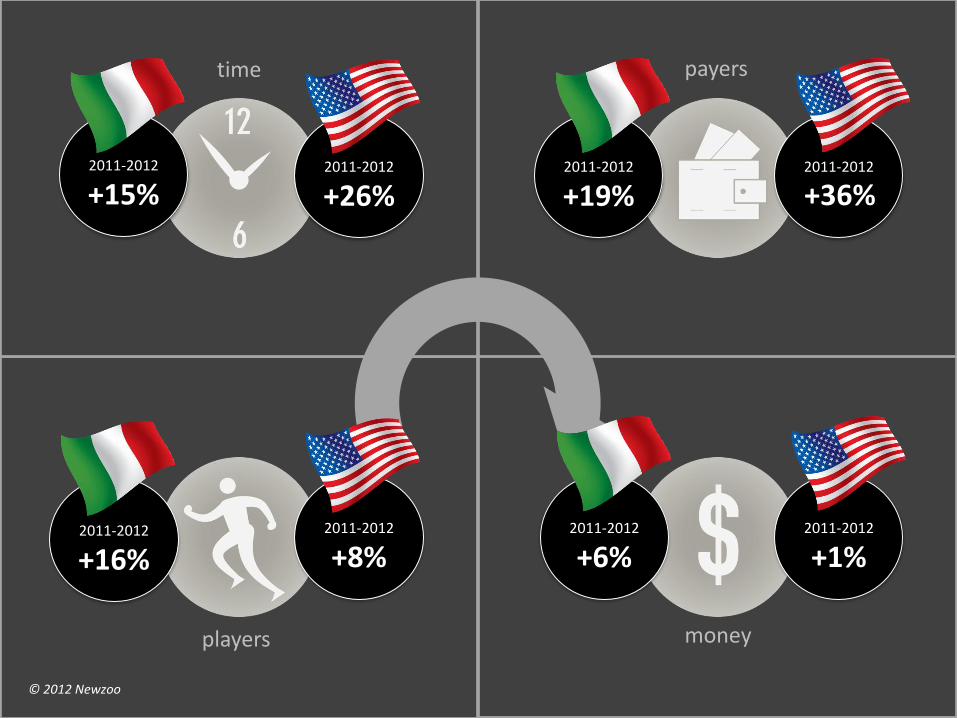

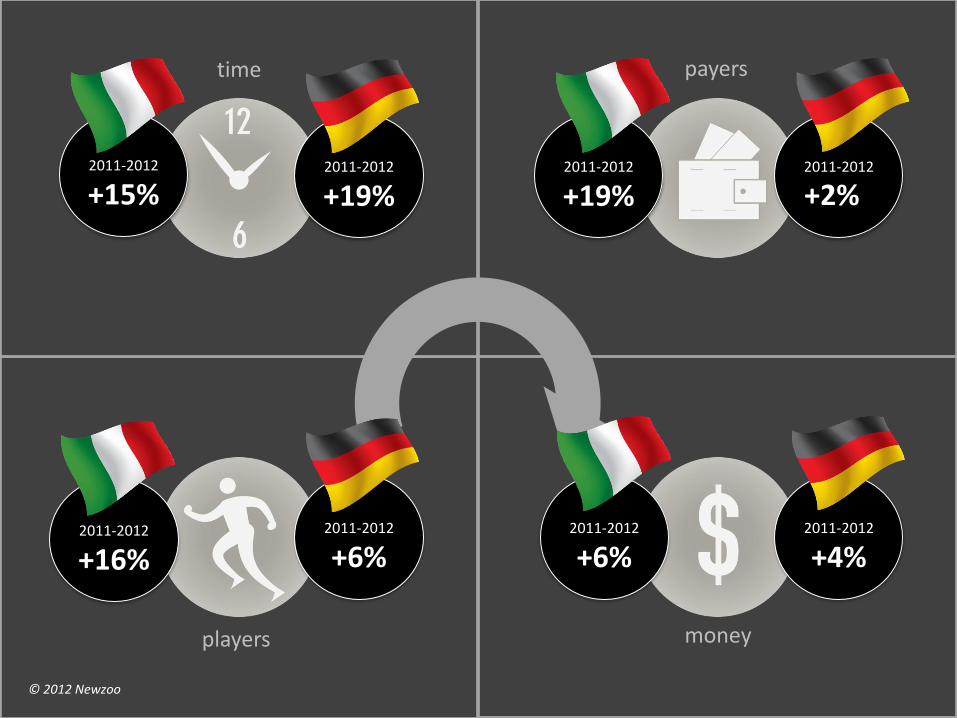

Games Market Growth

Most reports on the games market focus on number of players and/or money. To monitor and understand the changes in the games market this is not enough, especially now free-to-play business models are becoming so dominant. We always also report on Time and number of Paying Gamers (Payers) to provide more perspective.

27

players

time payers

money

© 2012 Newzoo 28

Key Growth Indicators | With Key Trends In Between

29

players

time payers

money

© 2012 Newzoo

2011-2012

+8%

2011-2012

+26%

2011-2012

+1%

2011-2012

+36%

Key Growth Indicators | With Key Trends In Between

30

players

time payers

money

© 2012 Newzoo

2011-2012

+8%

2011-2012

+26%

2011-2012

+1%

2011-2012

2011-2012

+15%

2011-2012

+16%

2011-2012

+19%

2011-2012

+6%

+36%

Key Growth Indicators | With Key Trends In Between

31

players

time payers

money

© 2012 Newzoo

2011-2012

+6%

2011-2012

+19%

2011-2012

+4%

2011-2012

2011-2012

+15%

2011-2012

+16%

2011-2012

+19%

2011-2012

+6%

+2%

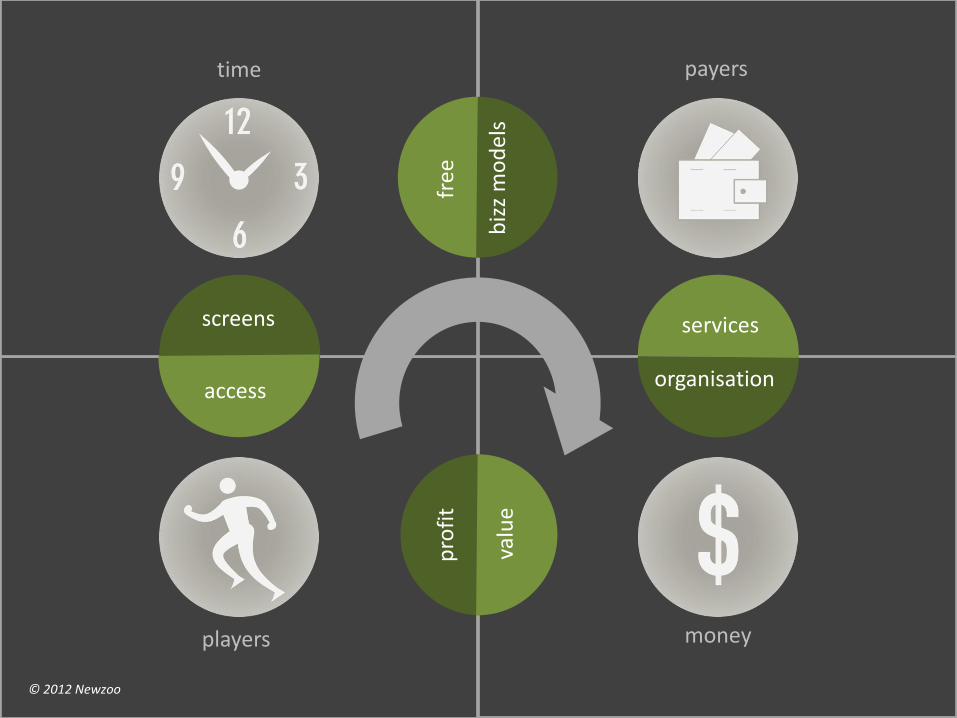

Lean back and….. Try to understand change

Key Growth Indicators | With Key Trends In Between

33

players

time payers

money

© 2012 Newzoo

access

screens

free

biz

z m

od

els

organisation

services

pro

fit

valu

e

34

Luxembourg, here we are This place is about more than money….

© 2012 Newzoo

screens

access

bizz models

free

organisation

service

profit

value

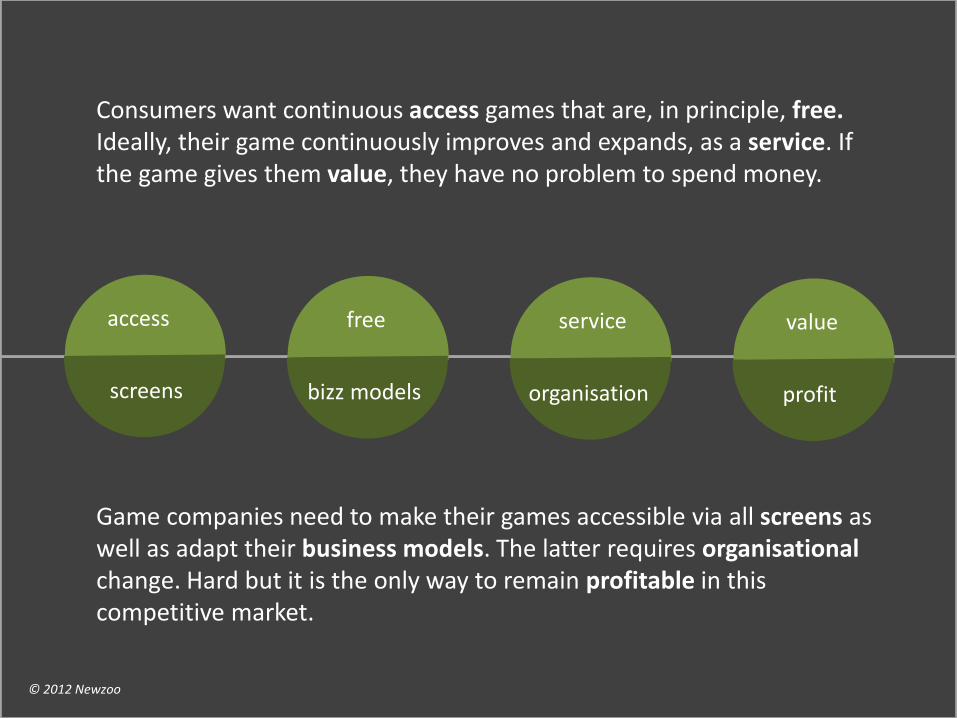

Consumers want continuous access games that are, in principle, free. Ideally, their game continuously improves and expands, as a service. If the game gives them value, they have no problem to spend money.

Game companies need to make their games accessible via all screens as well as adapt their business models. The latter requires organisational change. Hard but it is the only way to remain profitable in this competitive market.

New Players with New Business Models World of Tanks | Wargaming.net

Free-to-play MMO surpasses $100M revenues in 2012

Retail: Free-to-play boxed MMOs

35

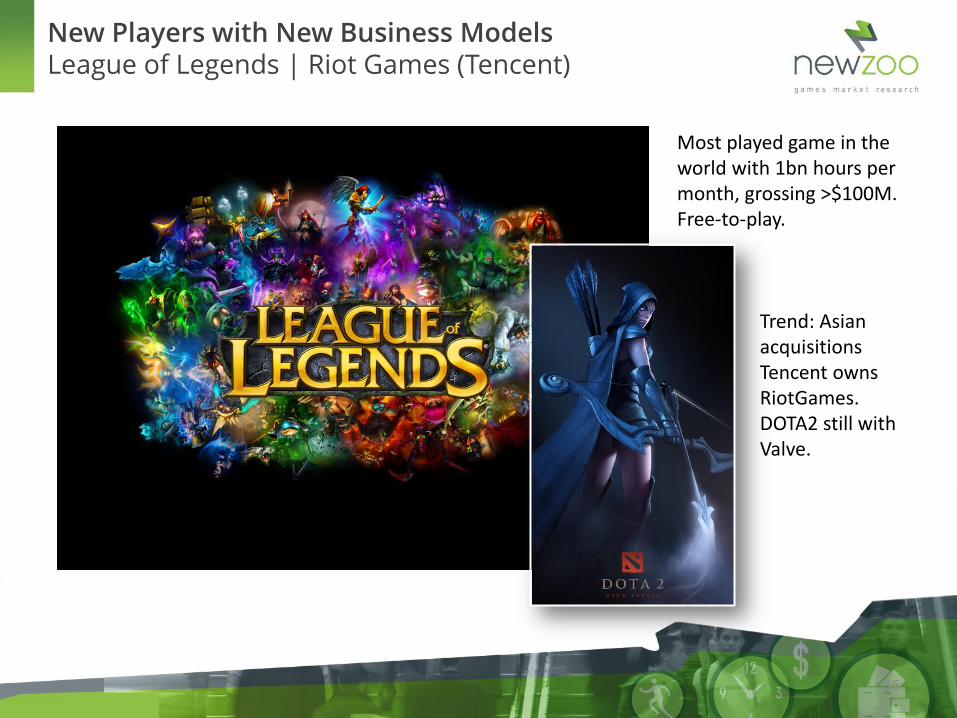

Most played game in the world with 1bn hours per month, grossing >$100M. Free-to-play.

Trend: Asian acquisitions Tencent owns RiotGames. DOTA2 still with Valve.

New Players with New Business Models League of Legends | Riot Games (Tencent)

36

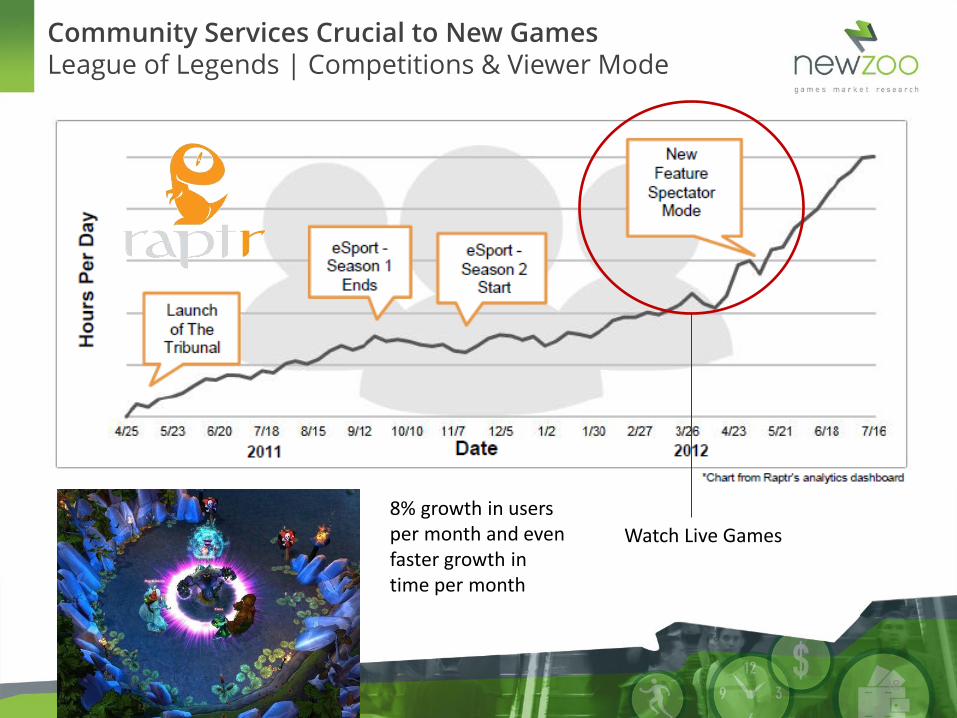

Community Services Crucial to New Games League of Legends | Competitions & Viewer Mode

37

38

8% growth in users per month and even faster growth in time per month

Community Services Crucial to New Games League of Legends | Competitions & Viewer Mode

Watch Live Games

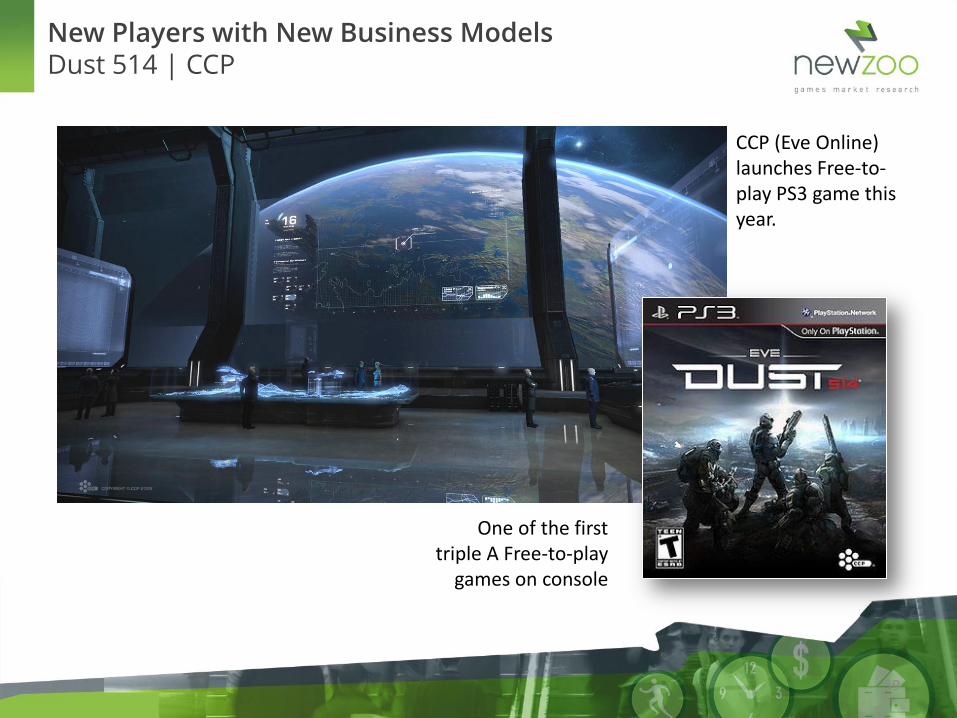

CCP (Eve Online) launches Free-to-play PS3 game this year.

One of the first triple A Free-to-play

games on console

New Players with New Business Models Dust 514 | CCP

39

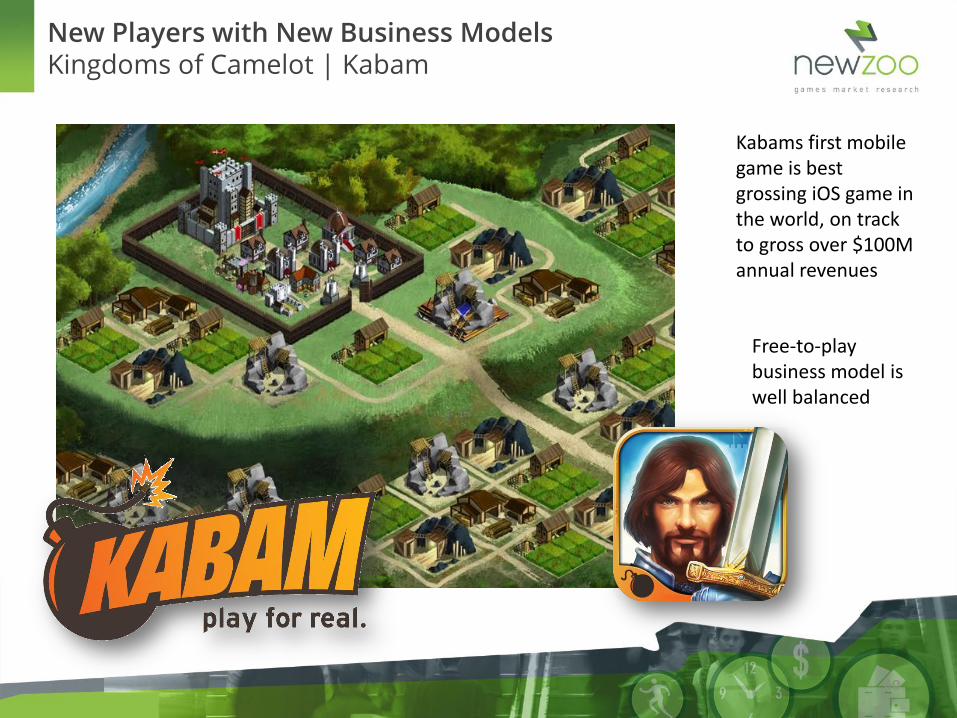

Kabams first mobile game is best grossing iOS game in the world, on track to gross over $100M annual revenues

Free-to-play business model is well balanced

New Players with New Business Models Kingdoms of Camelot | Kabam

40

© 2012 Newzoo/Distimo

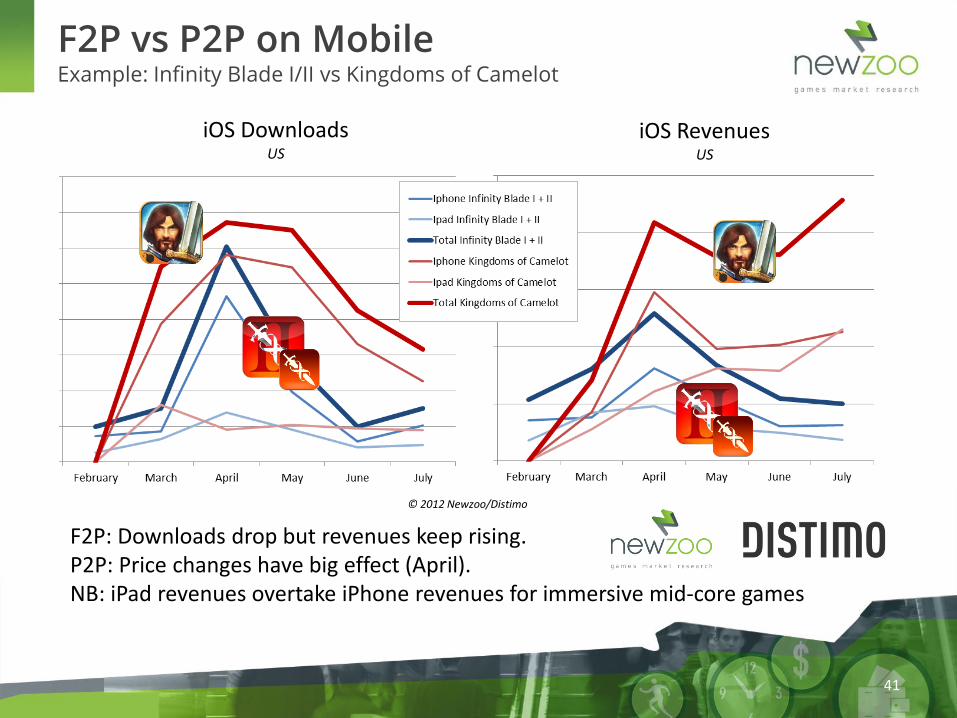

F2P vs P2P on Mobile Example: Infinity Blade I/II vs Kingdoms of Camelot

iOS Downloads US

iOS Revenues US

41

F2P: Downloads drop but revenues keep rising. P2P: Price changes have big effect (April). NB: iPad revenues overtake iPhone revenues for immersive mid-core games

Lean back and….. Think about what free-to-play means

“free-to-play is not a business model but a way

to run your business” - Peter Warman, CEO Newzoo

Quote of the month Why big publishers struggle amidst all the change

Just check out how Star Wars the Old Republic was launched compared to League of Legends (Wikipedia)

43

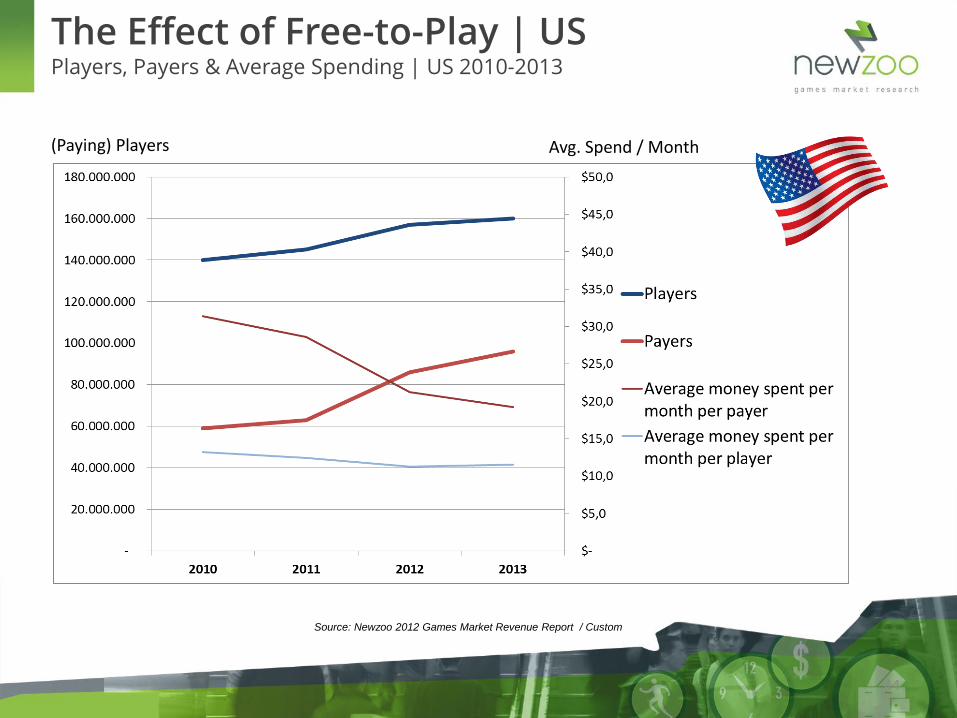

Source: Newzoo 2012 Games Market Revenue Report / Custom

(Paying) Players Avg. Spend / Month

The Effect of Free-to-Play | US Players, Payers & Average Spending | US 2010-2013

44

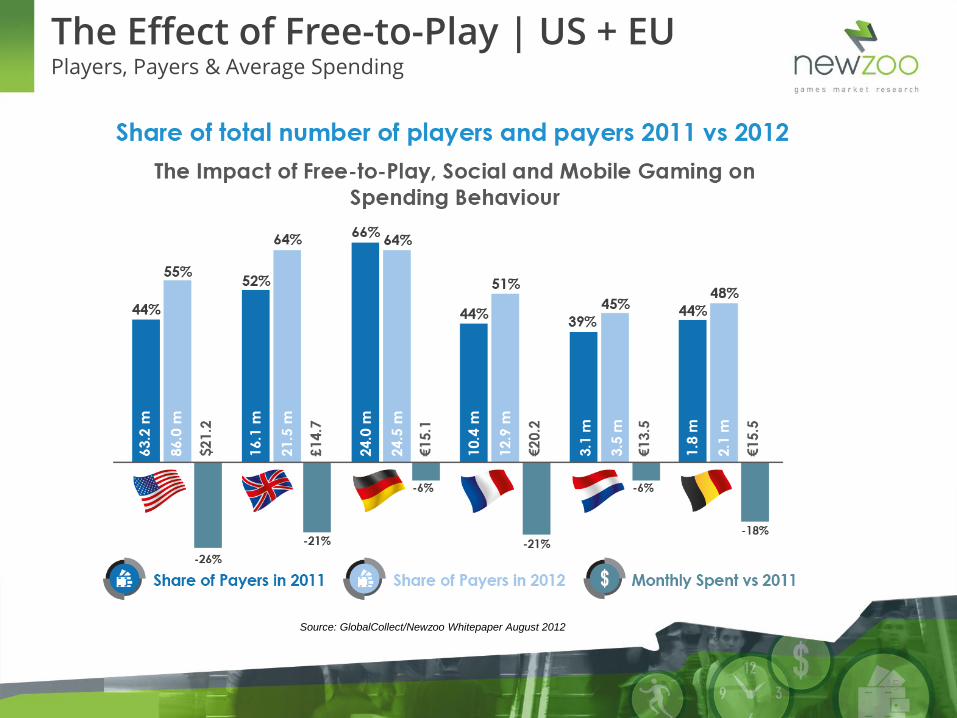

Source: GlobalCollect/Newzoo Whitepaper August 2012

The Effect of Free-to-Play | US + EU Players, Payers & Average Spending

45

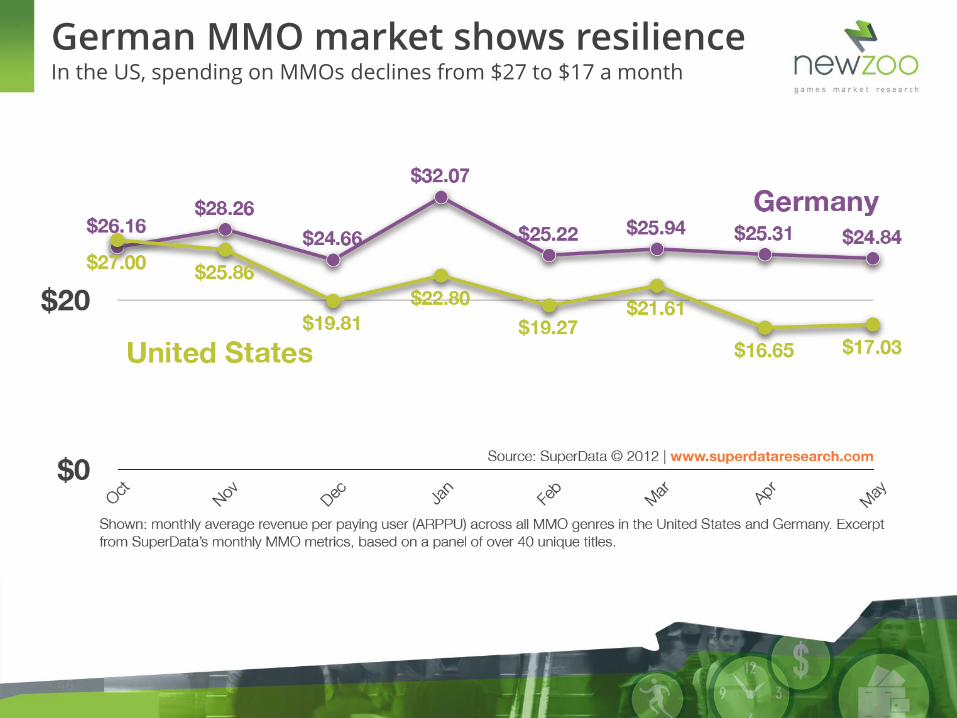

German MMO market shows resilience In the US, spending on MMOs declines from $27 to $17 a month

46

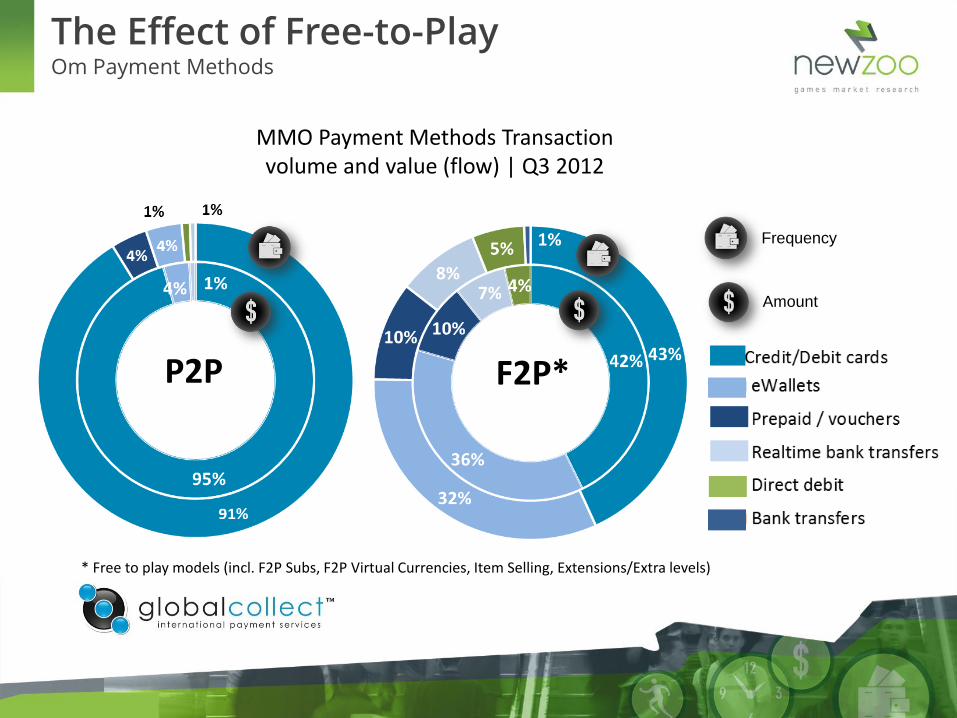

P2P F2P*

MMO Payment Methods Transaction volume and value (flow) | Q3 2012

Frequency

Amount

* Free to play models (incl. F2P Subs, F2P Virtual Currencies, Item Selling, Extensions/Extra levels)

The Effect of Free-to-Play Om Payment Methods

Lean back and….. Think about Amazon

49

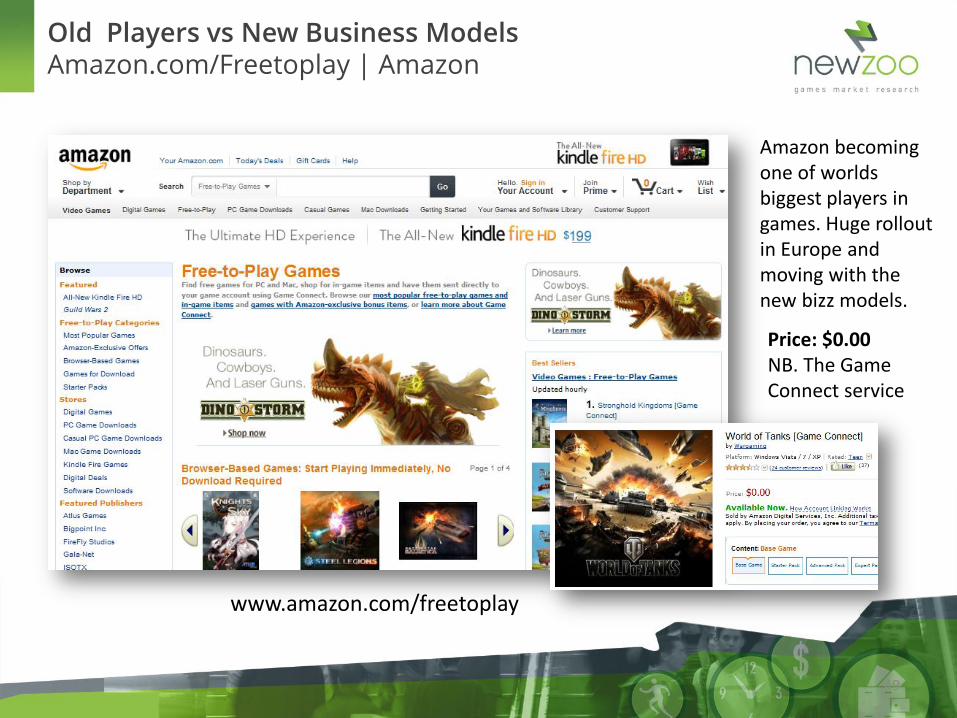

www.amazon.com/freetoplay

Amazon becoming one of worlds biggest players in games. Huge rollout in Europe and moving with the new bizz models.

Price: $0.00 NB. The Game Connect service

Old Players vs New Business Models Amazon.com/Freetoplay | Amazon

Old Players vs New Business Models Amazon.com/Freetoplay | Amazon

Lean back and….. Think how we can predict, size and seize future opportunities

52

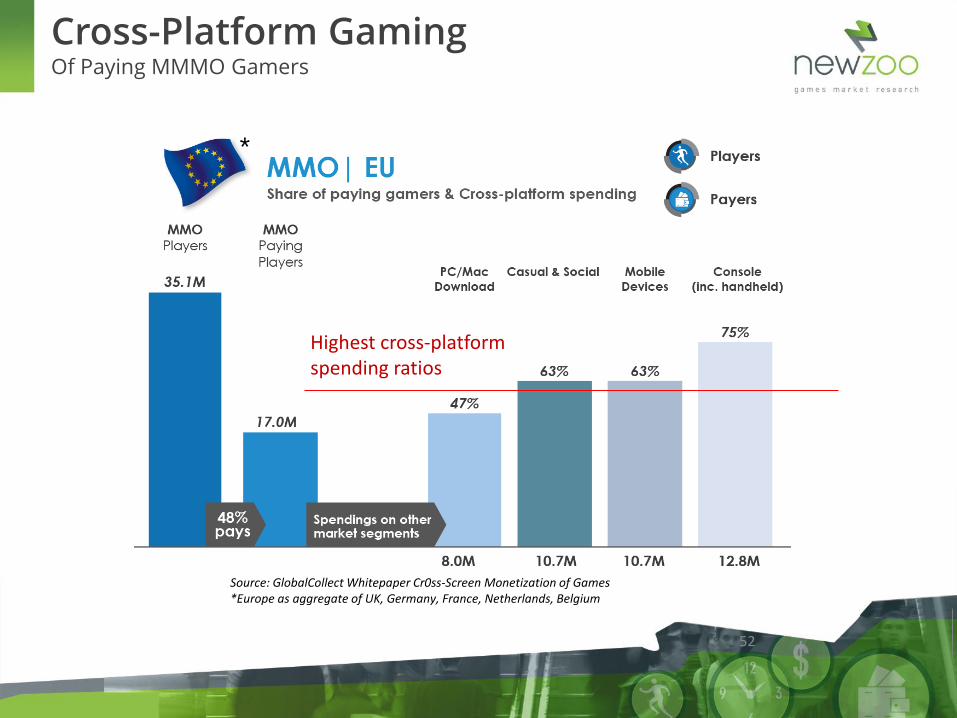

*

Source: GlobalCollect Whitepaper Cr0ss-Screen Monetization of Games *Europe as aggregate of UK, Germany, France, Netherlands, Belgium

Highest cross-platform spending ratios

Cross-Platform Gaming Of Paying MMMO Gamers

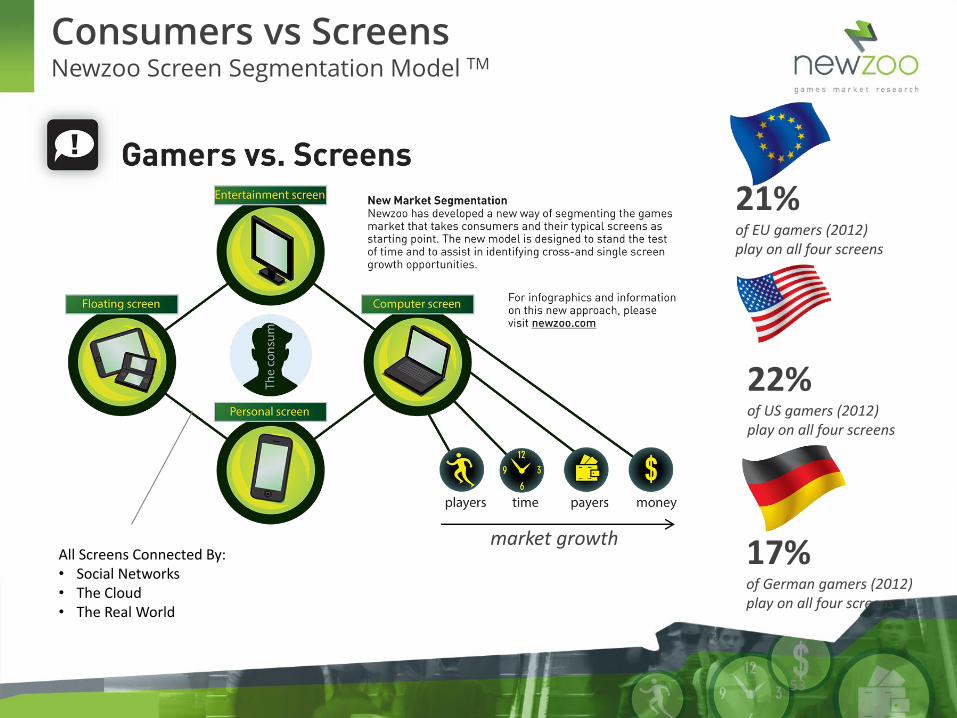

Consumers vs Screens Newzoo Screen Segmentation Model TM

22% of US gamers (2012) play on all four screens

21% of EU gamers (2012) play on all four screens

market growth All Screens Connected By: • Social Networks • The Cloud • The Real World

17% of German gamers (2012) play on all four screens

53

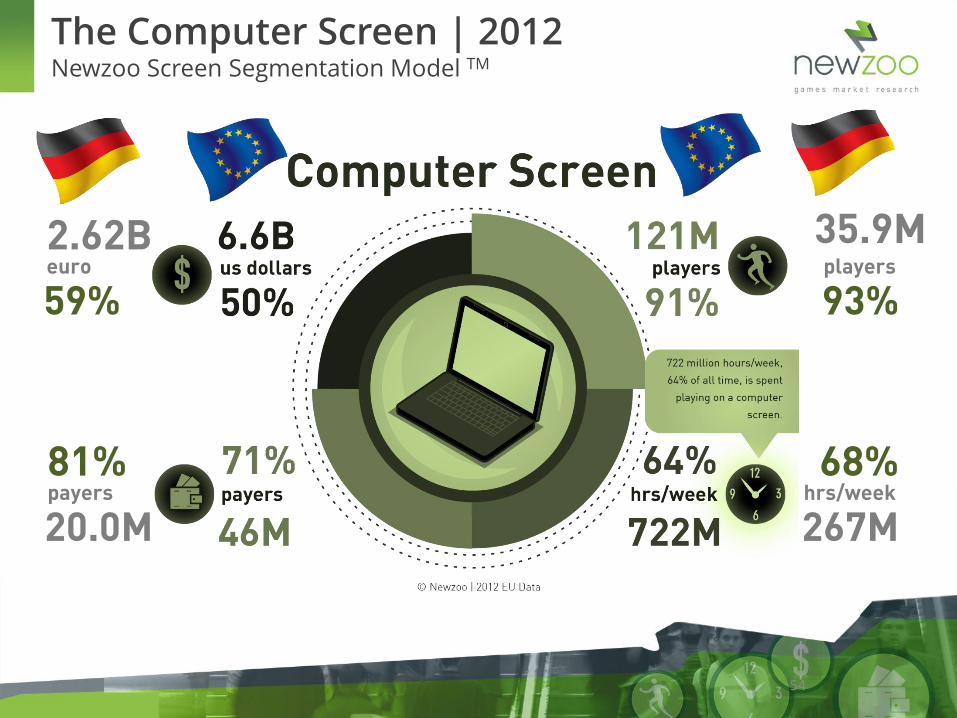

2.62B euro

59%

81% payers

20.0M

35.9M players

93%

68% hrs/week

267M

The Computer Screen | 2012 Newzoo Screen Segmentation Model TM

54

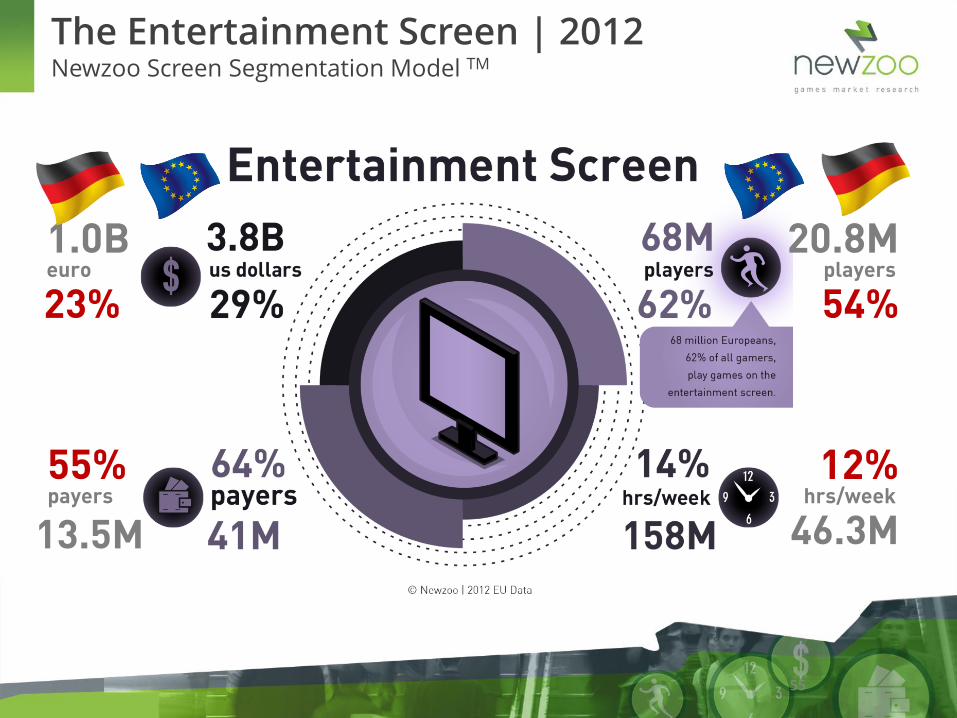

1.0B euro

23%

55% payers

13.5M

20.8M players

54%

12% hrs/week

46.3M

The Entertainment Screen | 2012 Newzoo Screen Segmentation Model TM

55

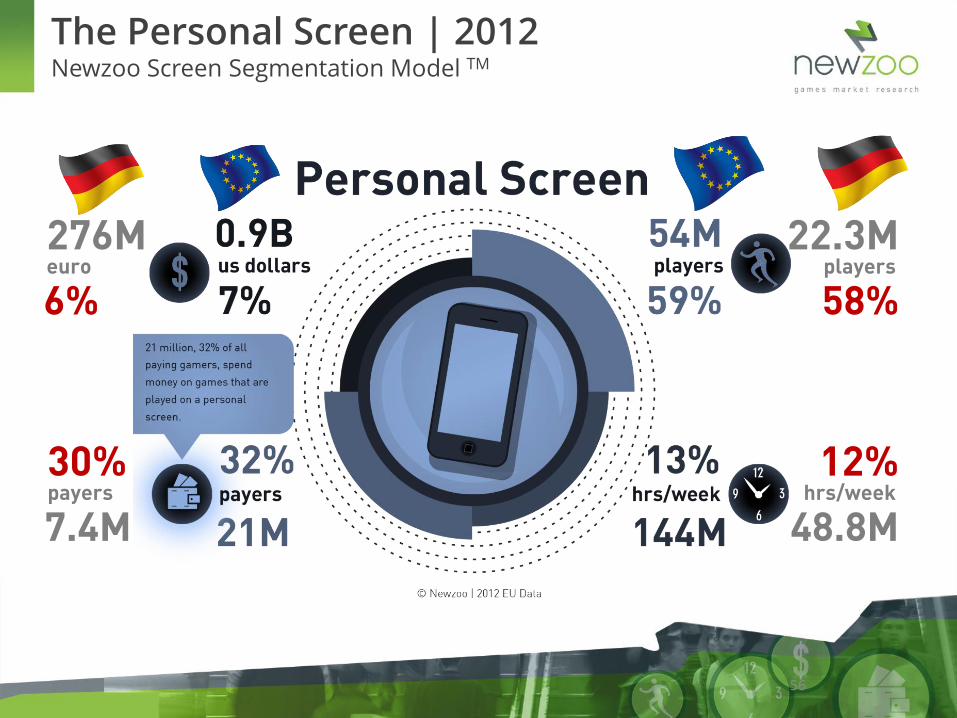

276M euro

6%

30% payers

7.4M

22.3M players

58%

12% hrs/week

48.8M

The Personal Screen | 2012 Newzoo Screen Segmentation Model TM

56

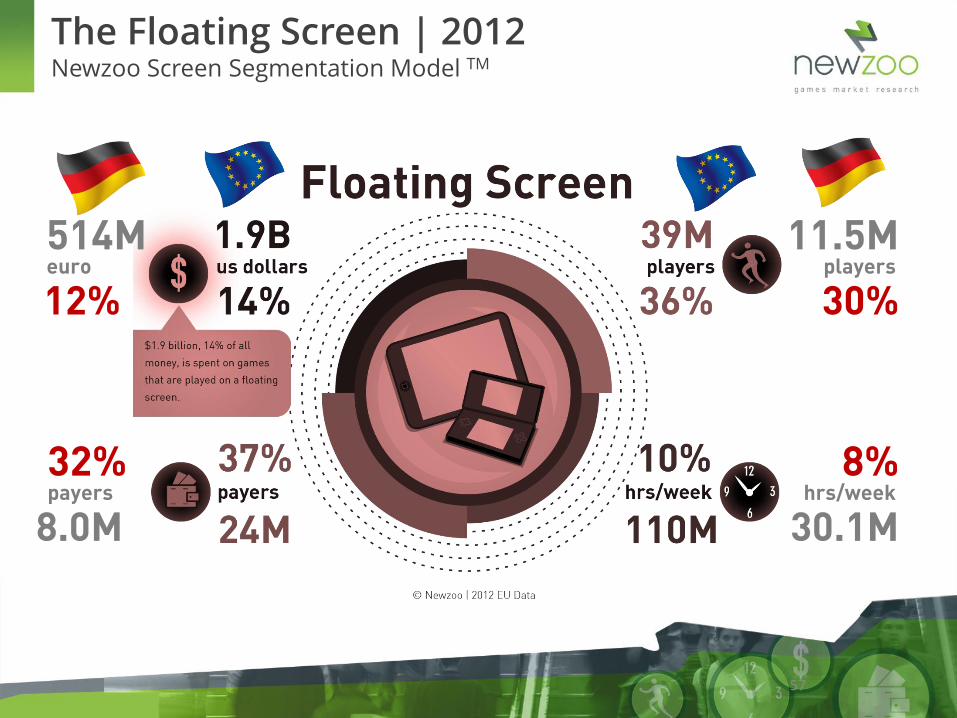

514M euro

12%

32% payers

8.0M

11.5M players

30%

8% hrs/week

30.1M

The Floating Screen | 2012 Newzoo Screen Segmentation Model TM

57

Lean back and….. Compare two similar games

World of Tanks Bubble Shooter

US UK GER FR IT ES BE NL RU BR PL TR AUS

Cross-Screen Spending Of (paying) players per IP

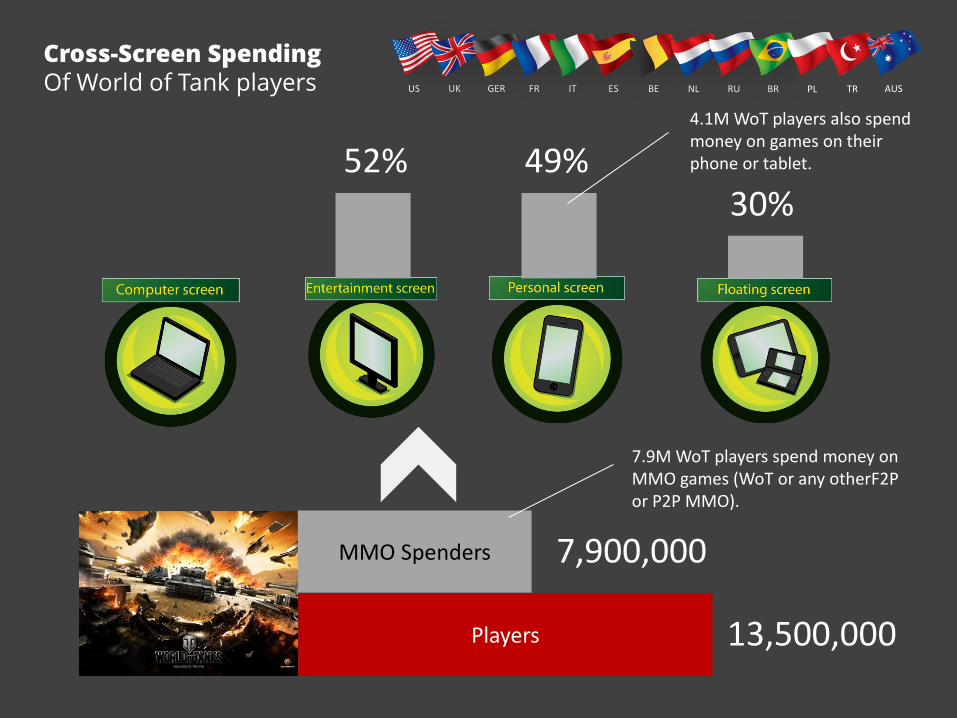

Players

MMO Spenders

US UK GER FR IT ES BE NL RU BR PL TR AUS

13,500,000

7,900,000

52% 49% 30%

Cross-Screen Spending Of World of Tank players

4.1M WoT players also spend money on games on their phone or tablet.

7.9M WoT players spend money on MMO games (WoT or any otherF2P or P2P MMO).

Players

Online Casual Spenders

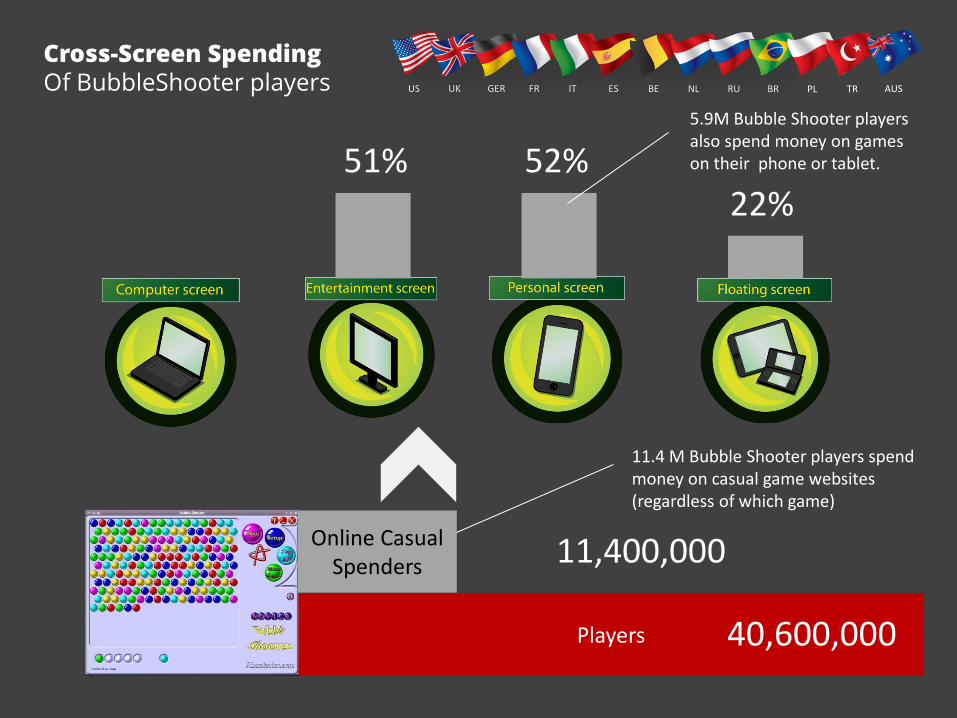

US UK GER FR IT ES BE NL RU BR PL TR AUS

40,600,000

11,400,000

51% 52% 22%

Cross-Screen Spending Of BubbleShooter players

5.9M Bubble Shooter players also spend money on games on their phone or tablet.

11.4 M Bubble Shooter players spend money on casual game websites (regardless of which game)

“your paying players spend a maximum of 30%

of their budget on your single screen game”

- Peter Warman, CEO Newzoo

Key Take-Away Paying players spend money across screens

62

Lean back and….. Think about mobile….

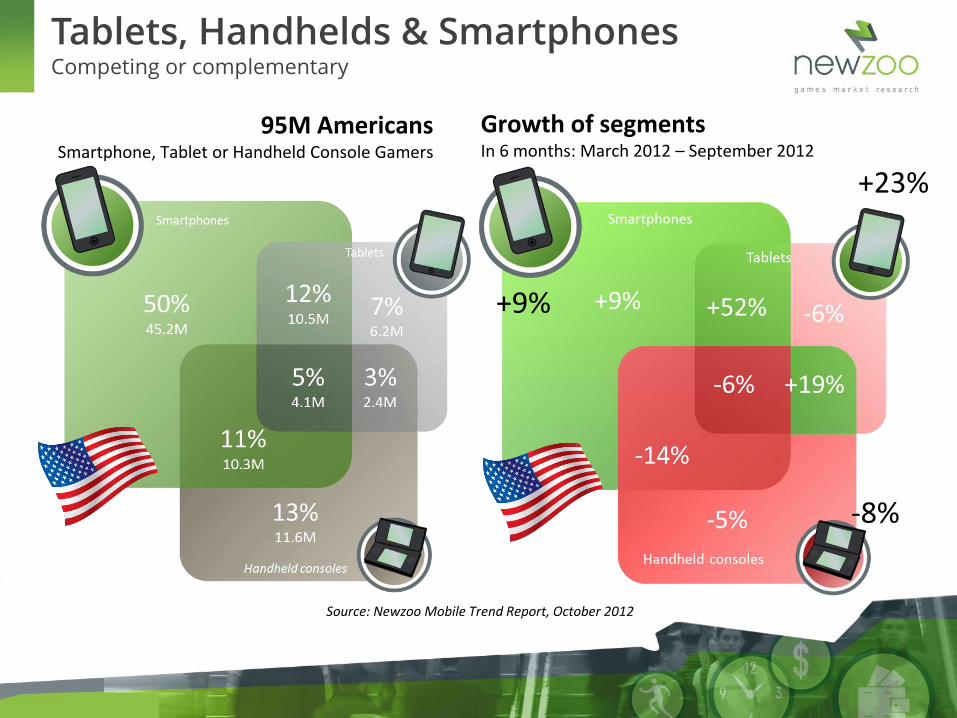

Tablets, Handhelds & Smartphones Competing or complementary

64

Source: Newzoo Mobile Trend Report, October 2012

95M Americans Smartphone, Tablet or Handheld Console Gamers

Growth of segments In 6 months: March 2012 – September 2012

+9%

+23%

-8%

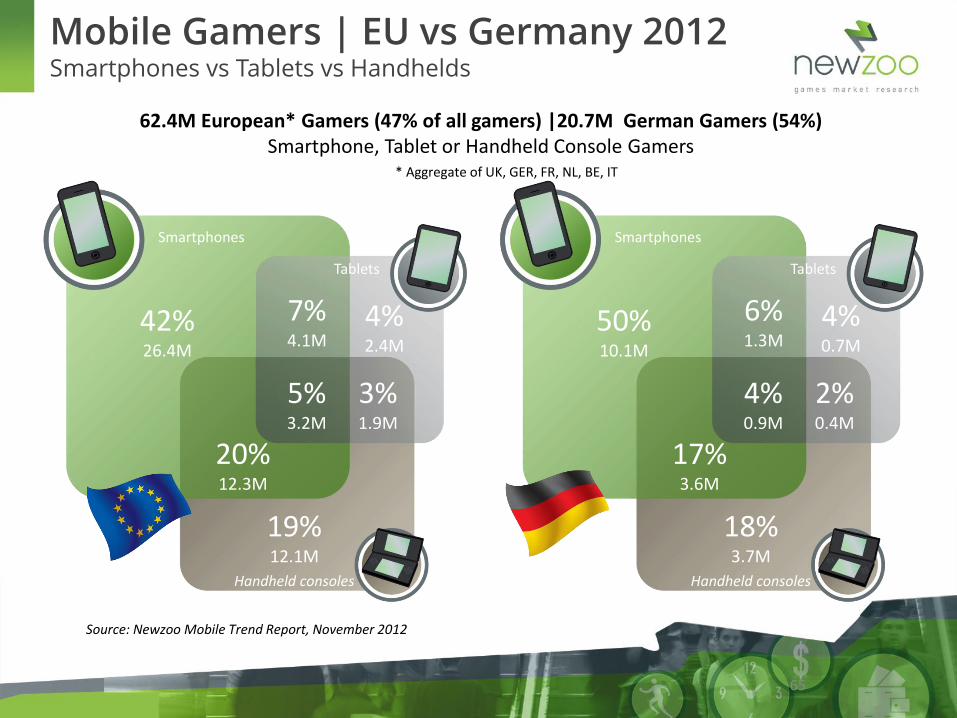

Mobile Gamers | EU vs Germany 2012 Smartphones vs Tablets vs Handhelds

Source: Newzoo Mobile Trend Report, November 2012

62.4M European* Gamers (47% of all gamers) |20.7M German Gamers (54%) Smartphone, Tablet or Handheld Console Gamers

Smartphones

Tablets

Handheld consoles

50% 10.1M

18% 3.7M

4% 0.7M

6% 1.3M

2% 0.4M

17% 3.6M

4% 0.9M

Smartphones

Tablets

Handheld consoles

42% 26.4M

19% 12.1M

4% 2.4M

7% 4.1M

3% 1.9M

20% 12.3M

5% 3.2M

65

* Aggregate of UK, GER, FR, NL, BE, IT

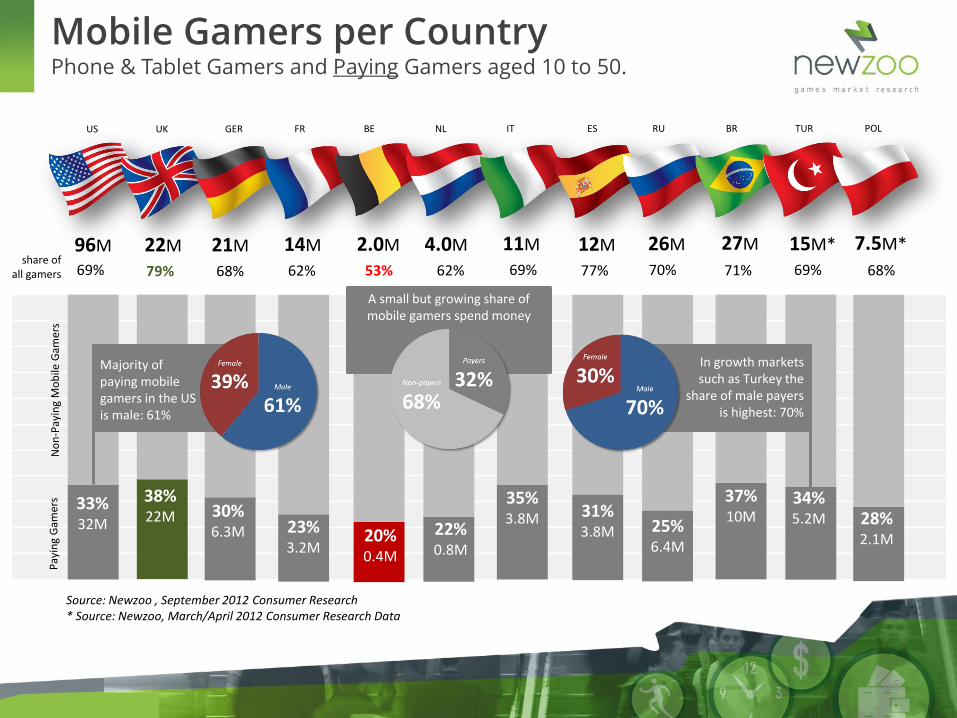

27M

Mobile Gamers per Country Phone & Tablet Gamers and Paying Gamers aged 10 to 50.

96M

Pay

ing

Gam

ers

22M 21M 14M 2.0M 4.0M 11M 12M 26M

79% 68% 62% 53% 62% 69% 77% 70% 71%

66

Source: Newzoo , September 2012 Consumer Research * Source: Newzoo, March/April 2012 Consumer Research Data

33% 32M

15M* 7.5M*

69% 68%

38% 22M 30%

6.3M 23% 3.2M

20% 0.4M

22% 0.8M

35% 3.8M 31%

3.8M 25% 6.4M

37% 10M 28%

2.1M

69%

34% 5.2M

No

n-P

ayin

g M

ob

ile G

amer

s

share of all gamers

Majority of paying mobile gamers in the US is male: 61%

In growth markets such as Turkey the

share of male payers is highest: 70%

A small but growing share of mobile gamers spend money

US UK GER FR BE NL IT ES RU BR TUR POL

Rank Game Last Month Publisher

1 The Simpsons™: Tapped Out 1 Electronic Arts

2 Clash of Clans 15 Supercell

3 Hay Day 9 SuperCell

4 Poker by Zynga 5 Zynga

5 Lords & Knights - Medieval Strategy MMO 4 XYRALITY GmbH

Top 5 Games Germany September 2012 Based on total iPad, iPhone and Google Play store revenues

Rank Game Last Month Publisher

1 Clash of Clans 10 Supercell

2 The Simpsons™: Tapped Out 1 Electronic Arts

3 Hay Day 5 SuperCell

4 Lords & Knights - Medieval Strategy MMO 4 XYRALITY GmbH

5 Ice Age Village 2 Gameloft

Rank Game Last Month Publisher

1 Rage of Bahamut 2 Mobage

2 Ice Age Village 1 Gameloft

3 Arcane Empires 584 Kabam

4 Airport City 3 Game Insight International

5 Zynga Poker 4 Zynga

Lean back and….. Think how we can help each other

my wish is

Come visit our new office (when its done)

And lean back for a monent (with coffee or beer)

We need each other (to make sure these guys understand our stuff)

Cross-Screen Impact of

Free-to-Play

Peter Warman | CEO Newzoo | [email protected] Offenbach, November 2012

Lean forward vs lean back

© 2012 Newzoo www.newzoo.com