Embed Size (px)

Citation preview

Chapter 1Introduction

1

1.0 Introduction

1.1 Rational of the study: The internship report is an integral part of the BBA program

of every university. So it is compulsory to take such task by the students who to complete and

successfully end-up their BBA degree. It is also an opportunity for the students to minimize

the gap of their theoretical and practical knowledge. Students are required to work on a

specific topic based on their theoretical and practical knowledge acquired during the period

of the internship program and then submit it to the teacher. That is why I have prepared this

report.

1.2 Background of the organization: Southeast Bank Limited is a desires private

commercial bank in Bangladesh. Southeast Bank Ltd is a second-generation bank that was

established in 1995 with a dream and a vision to become a pioneer banking institution of the

country and contribute significantly to the growth of the national economy. The Bank’s

journey began when it was incorporated as a Public Limited Company on March 12. 1995.

The Registrar of Joint Stock Companies and Firms issued the Certificate of Commencement

of Business of the Bank on the same date. The Southeast Bank received its Banking License

from the Bangladesh Bank on March 23, 1995. The Bank’s first branch was opened by Late

M. Saifur Rahman, the then Honorable Finance Minister of the Government of the People’s

Republic of Bangladesh as the Chief Guest at the commercial hub of the country at 1,

Dilkusha Commercial Area, Dhaka on May 25, 1995.

The Bank s philosophy- “A Bank with Vision” has been preciously the essence of the legend

of its success. Within this very short period of time it has been able to create an image for

itself and has earned significant reputation in the country's banking sector as a Bank with

vision. Presently it has 98 branches in operation. Southeast Bank received “The Highest

Remittance Collection Bank Award 2012” arranged by the weekly Industry.

Company Vision:

To be a premier banking institution in Bangladesh and contribute significantly to the national

economy.

Company Missions:

High Quality financial services with state of the art technology

2

Fast customer services

Sustainable growth strategy

High ethical standards in business

Steady return on shareholders’ equity

Innovative banking at a competitive price

Attraction and retention of quality human resource

Commitment to Corporate Social Responsibility

Core Values:

Integrity

Respect

Team Spirit

Courtesy

Commitment

Service Excellence

Business Ethics

Core Strengths:

Professionally strong Board of Directors

Strong Capital base

Transparent and Quick Decision Making

Satisfied Customers

Skilled Risk Management

Diversification

Strong asset base

Core Competencies:

Knowledge

Experience and Expertise

Customer orientation/ Focus

Pursuit of Disciplined Growth Strategies

Reliability

Business Objective:

Make sound investments

3

Meet capital adequacy requirement at all the time

Ensure a satisfied work force

Ensure 100% recovery of all advances

Focus on fee-based income

Commitments to Clients:

Provide service with high degree of professionalism and use of modern technology

Create long term relationship based on mutual trust

Respond to customer needs with speed and accuracy

Share their values and beliefs

Provide products and services at competitive pricing

Ensure safety and security of customers’ valuable in trust with us

Operational Areas:

Southeast Bank Limited Operations consist of:

Real Time on line banking

Credit and Debit Card

ATM

Commercial Banking

Retail Banking

Investment Banking

Syndication and Mortgage Loan

Foreign Remittance

Departments:

There are five types of departments into the southeast Bank Ltd. Such as-

General Banking department

Remittance department

Foreign Exchange department

Credit department

Cash department

Organizational Structure of Southeast Bank Ltd:

4

There are 14 levels in the bank which is classified into 3 parts. These are Top Management,

Mid level Management and Lower level Management. The organizational structure is

furnished below:

1.3 Objectives:

5

Managing Director (MD)

Deputy Managing Director (DMD)

Senior Executive Vice President (SEVP)

Executive Vice President (EVP)

Senior Vice President (SVP)

Vice President (VP)

Assistant Vice President (AVP)

Senior Executive Officer (SEO)

Executive Officer (EO)

Senior Officer (SO)

Management Trainee (MT)

Junior Officer (JO)

Trainee Assistant (TA)

Top Management

Mid Level Management

Lower Level Management

1.3.1 Board Objective:

To analysis the policies and practices of credit management of the Southeast Bank Ltd.

1.3.2 Specific Objective:

To evaluate the credit management system of Southeast Bank Ltd.

To identify the potential problem of credit department of Southeast Bank Ltd.

To provide some recommendation to improve credit management practices of

Southeast Bank Ltd.

6

Chapter 2Activities Undertaken

2.0 Activities Undertaken

7

2.1 Work Related:

I started my internship program in Southeast Bank Ltd, Kakrail Branch on 2nd February,

2014. At first I worked in the general banking section and here my supervisor was Shamima

Nasrin (JO) who gave me an introduction on the account opening process. As my topic of

internship report is “Policies and Practices of Credit Management of the Southeast Bank

Ltd” and here my supervisor was Mohammad Khairuzzaman (EO). Although three

months is not a very long period to learn the whole thing that usually occurs in an

organization but I had plenty of opportunity to work and understand the sectors of credit

department. Now I am describing the activity of general banking and credit departments that I

worked during my internship period in the following:

1. General Banking Department

Account opening specially savings and current account

Pay Order (PO) FDR and DPS issue

Issuance and Provide Cheque book

2. Credit department

Prepare internal memo

Bank authorization letter

Loan expand letter

Register book entry

Check CIB (credit information bureau) report

2.2 Organization Wide:

Credit Department:

A bank’s main earning source is credit. If bank’s credit management is not good then the

bank will never ever achieve its proper goals. Question may arise what are the proper

goals for the bank? The proper goals for the banks are profit maximization and

shareholder’s wealth maximization. The fundamental nature of credit is that an element of

trust exists between buyer and seller whether of good or money. The main use of bank

fund is to collect money from surplus unit and lend it to deficit economic unit.

8

Categories of Loans and Advances:

Continues Loan:

Certain credit limit

Contains expiry date for full adjustment

No particular repayment schedule

CC (Hypothecation & Pledge), OD etc.

Demand Loan:

Repayable on demand by the bank

Contingent or any other liability is converted to compulsory or forced loan without

any prior approval as regular loan.

Forced LIM, FBP, IBP etc

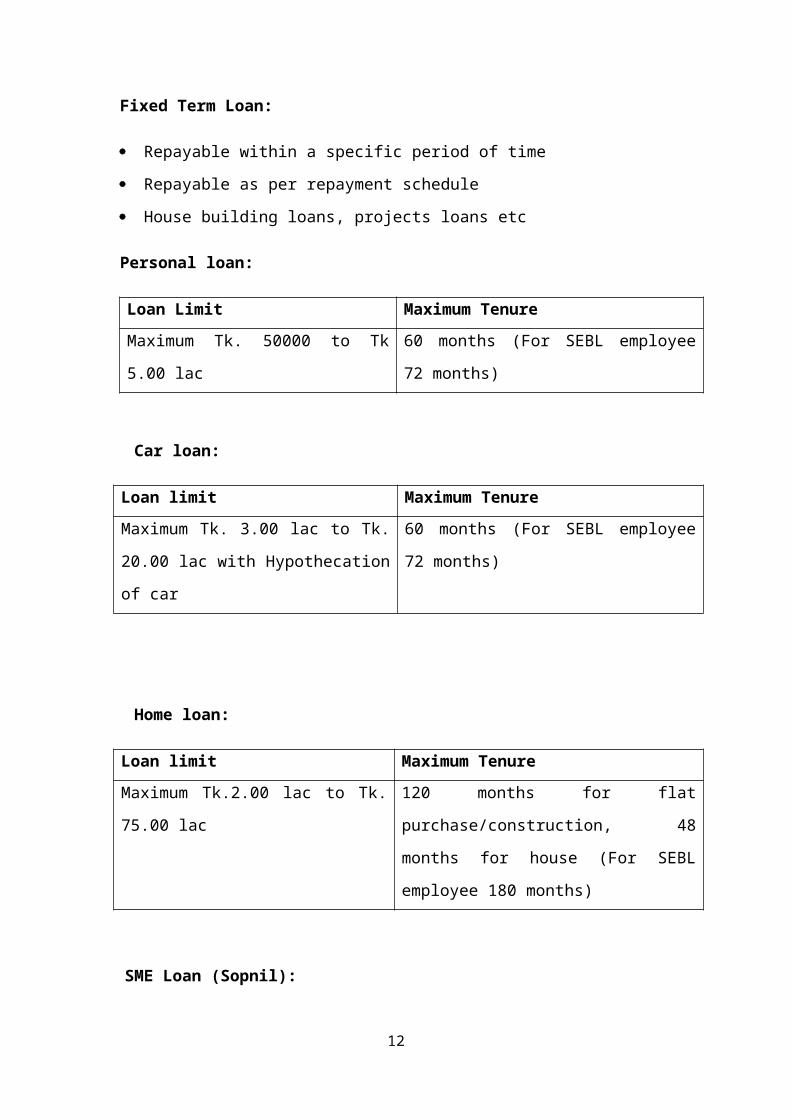

Fixed Term Loan:

Repayable within a specific period of time

Repayable as per repayment schedule

House building loans, projects loans etc

Personal loan:

Loan Limit Maximum Tenure

Maximum Tk. 50000 to Tk 5.00 lac 60 months (For SEBL employee 72 months)

Car loan:

Loan limit Maximum Tenure

Maximum Tk. 3.00 lac to Tk. 20.00 lac

with Hypothecation of car

60 months (For SEBL employee 72 months)

Home loan:

Loan limit Maximum Tenure

9

Maximum Tk.2.00 lac to Tk. 75.00 lac 120 months for flat purchase/construction, 48

months for house (For SEBL employee 180

months)

SME Loan (Sopnil):

Loan limit Maximum Tenure

Max Tk. 5.00 lac to Tk. 25.00 lac 48 months

Lending Guidelines:

A prudent banker should always adhere to the following general principles of lending funds

to these customers.

Background, Character and ability of the borrowers

Purpose of the facility

Term of facility

Safety

Security

Profitability

Sources of repayment

Diversity

Credit Control Policy of Bangladesh Bank

The Lending Process:

The lending procedure starts with building up of relationship with customer through account

opening. The stages of credit approval are done both at the branches and at the Head Office

levels. The lending procedure as observed in Southeast Bank Ltd is described below in

sequential order.

Applications from the Credit Applicant:

10

A loan procedure formally starts with a loan application from a client who must have

an account with the Bank. At first it starts from the branch level. Branch receives

application from client for a loan facility. In the application client mentions what

type of credit facility he/she wants from the bank including his/her personal

information & 3rd business information. Branch Manager or the Officer-in-charge of

the credit department conducts the initial interview with the customer.

Credit proposal:

The branch starts processing the loan at this stage. Based on the analysis (credit

analysis) done by the branch, the branch prepares a loan proposal. The proposal

contains following important and relevant information:

Name of the borrower(s)

Nature of credit

Purpose of credit

Extent of credit

Collateral Margin

Rate of interest

Repayment schedule

Validity etc.

Collection of Documents:

Document is a written statement of facts and a proof or evidence in respect to a

particular transaction between parties. If Bangladesh Bank sends positive CIB report

on that particular borrower and if the Bank thinks the prospective borrower to be a

good one, then the bank scrutinizes the documents.

Required documents are:

Title deed

Via deed

Financial documents of the company for the last three to five years.

Mutation certificate

Personal net worth of the borrower(s).

11

Duplicate carbon receipt

Khatians

Ground rent payment receipt

Holding tax payment receipt

Utility bills

Importance of documentation:

To protect the interest of the bank from any distress situation

To take legal action against the borrower in case of default

For safety and liquidity of depositors money

To create charge of the asset of the borrower to recover loan in case of need

Steps of documentation:

Obtaining the instruments

Stamping

Execution

Witnessing

Registration

Preservation

Kinds of Stamps:

Judicial

Adhesive

Non Judicial

Adhesive

Revenue stamp

Embossed/Engrossed stamp

Obtaining CIB Report:

After receiving the loan application from the client, the bank sends a letter to Credit

Information Bureau of Bangladesh Bank for obtaining a credit inquiry report of the

customer. This report is called CIB (Credit information Bureau) report. This report is

usually collected if the loan amount exceeds any amount. The purpose of this report

is to be informed whether or not the borrower has taken loans and advances from any

12

other banks and if so, what the status of those loans and advances is i.e., whether

those loans are classified or not.

Evaluation of CIB Report:

Bangladesh Bank provides Credit Information Bureau (CIB) Report to banks and

other financial institutions. This report is about borrowers having outstanding loan

balance of Tk. 1.00 ac and above with scheduled banks and non-bank financial

institutions. It contains the following information:

Debtor/borrower information (outstanding loan balance and loan classification

status) Owner information

Group/related business information

Credit Exposure Matrix/financial information

Third party guarantors information

Southeast Bank uses CIB Report as part of its credit appraisal procedure. It serves as

a useful tool to assess borrower’s credit standing and loan repayment behavior.

Head Office Management Committee:

Head office processes the credit proposal and afterwards puts forward an office note

if the loan is within the discretionary power of the Head Office Management

Committee or a memo to the Board/Executive Committee if the loan requires

approval from the Board of Directors

Sanction Advice:

If Head Office Management Committee or the Board, as the case may be, approves

the credit line, an approval letter is sent to the branch. The branch then issues a

sanction letter to the borrower with a Duplicate Copy. The duplicate copy duly

signed by the borrower is returned to the branch of the bank. This duplicate copy

returned by the applicant proves that the borrower agrees with the terms and

conditions of the credit line offered by the bank.

Collection of Charge Documents:

13

After issuing the sanction advice, the bank collects necessary charge documents.

Charge documents vary on the basis of types of facility, types of collateral etc.

Sanctioning of Credit at Branch level:

If the proposal meets SEBL lending criteria and is within the manager’s

discretionary power, the credit line is approved. The manager and the

sponsoring officer sign the credit line proposal and issue a sanction letter to

the client.

If the value of the credit line is above the branch manager’s limit then it is

send to Head Office for final approval with detailed information regarding the

client(s), credit analysis and security papers.

Disbursement Loan:

Finally loan is disbursed by the branch through a loan account in the name of the

borrower and monitoring of the loan starts formally.

The entire process can be shown in the following flow chart:

Security:

14

Loan disbursement

Branch sanction

Collect client documents

Send proposal to Head

office

Sanction to credit committee &

board meetting

Send request letter to client Check CIB report

Security means acquiring a claimed on an asset so that if repayment is not made as per

schedule the assets taken as security can be used to obtain repayment. Security are considered

as insurance against emergency.

Types of securities

Immovable properties

Movable properties

Creation of charge on security:

Pledge: When goods are delivered by a borrower to a banker as security for debt the delivery

is termed as a pledge.

Hypothecation: In hypothecation goods remain in possession of the borrower. But the

hypothecation deed provides the banker the power to take the goods in possession if needed.

In case the banker exercises such power the hypothecation will take the form of a pledge.

Mortgage: Mortgage is created by a registered deed and gives the mortgage the right of sale

in case of default.

Lien: Right to retain the goods of the borrower until the debts are repaid but not the power to

sell unless there is a written right to sell the goods.

Credit risk management:

In 2003 Bangladesh Bank a project to review the best practices in different risk areas in

banking industry of Bangladesh. Credit is one of the important risks. Credit risk grading is

the basic module for developing a credit risk management system.

Credit risk grading:

Credit risk grading is an important tool for credit risk management as it helps the bank &

financial institutions to under various dimensions of risk involved in different credit

transaction.

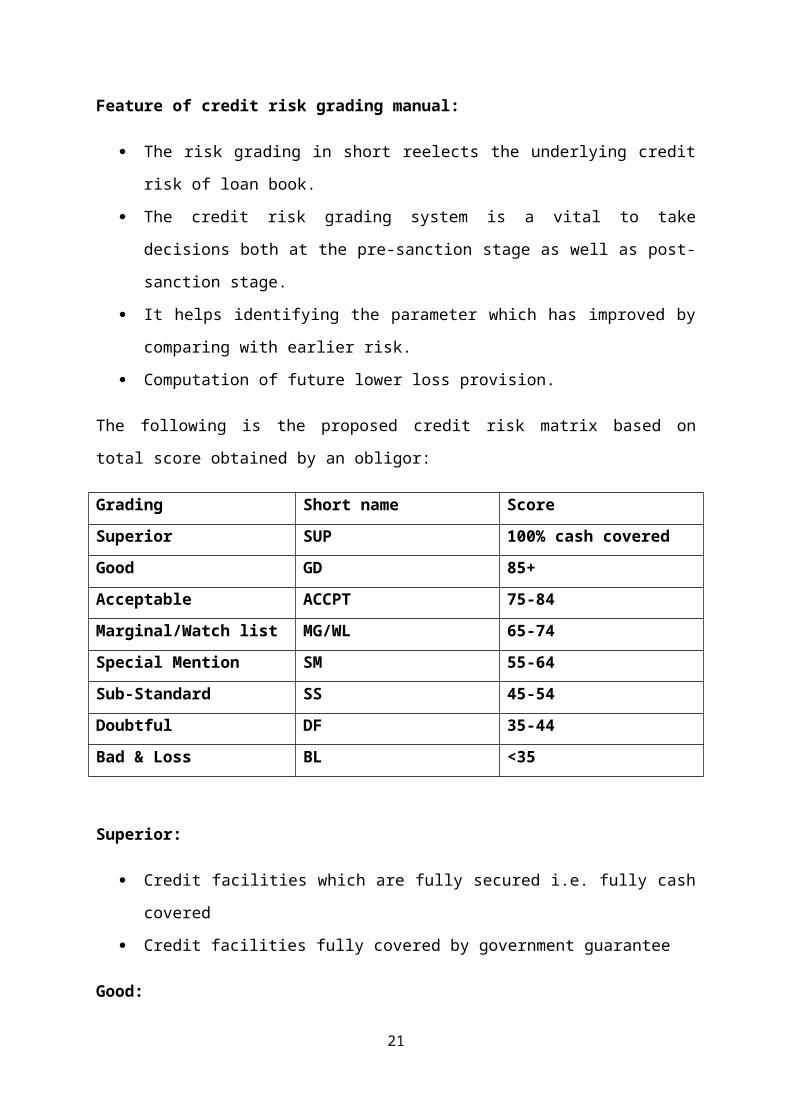

Feature of credit risk grading manual:

15

The risk grading in short reelects the underlying credit risk of loan book.

The credit risk grading system is a vital to take decisions both at the pre-sanction

stage as well as post-sanction stage.

It helps identifying the parameter which has improved by comparing with earlier risk.

Computation of future lower loss provision.

The following is the proposed credit risk matrix based on total score obtained by an obligor:

Grading Short name Score

Superior SUP 100% cash covered

Good GD 85+

Acceptable ACCPT 75-84

Marginal/Watch list MG/WL 65-74

Special Mention SM 55-64

Sub-Standard SS 45-54

Doubtful DF 35-44

Bad & Loss BL <35

Superior:

Credit facilities which are fully secured i.e. fully cash covered

Credit facilities fully covered by government guarantee

Good:

Strong repayment capacity of borrower

The borrower has excellent liquidity and low leverage

Aggregate score of 85

Acceptable:

Borrowers have adequate liquidity, cash flow and earning

Aggregate score of 75-84

Marginal/Watch list:

16

Borrowers have an above average risk due to strained liquidity.

Account conduct is poor

Special Mention:

This grade has potential weakness that deserve managements close attention

Severe management problems exist.

Sub Standard:

Financial condition is weak

These weaknesses jeopardize the full settlement of loans

Doubtful:

Full repayment of principal and interest is unlikely and the possibility of loss is

extremely high

Bad & Loss:

Credit of this grade has long outstanding with no progress in obtaining repayment.

Credit Risk

Financial

Risk (50%)

Business

Risk

(18%)

Management

Risk (12%)

Security

Risk

(10%)

Relationship

Risk (10%)

Lever

age (15%)

Liquid

ity (15%)

Profit

ability

(15%)

Cover

age (5%)

Siz

e of

Busines

s (5%)

Age

of

busines

s (3%)

Bus

iness

outlook

Exper

ience

(5%)

Succe

ssion

(4%)

Team

work

(3%)

Security

coverag

e (4%)

Collater

al

coverag

e (4%)

Support

(2%)

Account

conduct

(5%)

Utilizatio

n

Of limit

(2%)

Complian

ce of

condition

(2%)

17

(3%)

Ind

ustry

growth

(3%)

Mar

ket

compet

ition

(2%)

Bar

riers to

busines

s (2%)

Personal

deposits

(1%)

Credit risk solution:

Rating of corporate clients

Client selection procedure and strong monitoring

Taking higher collaterals and margin to reduce the credit risk

Properly select borrower category and exposure

Limits for SME and RT clients should be given on the basis of cost benefit

relationship

Timely reporting

18

Chapter 3 Challenges and

recommendations for improvement

19

3.0 Constraints/Challenges and Proposed Course of Action for

Improvement

While doing internship in SEBL I faced a newer kind of experience. This acted as a barrier to

conduct the program. The limitations were:-

3.1 Organizational Constraints: In general banking system they follow the traditional banking system.

In case of online banking service SEBL Bank is clearly in down position like the other

commercial bank. Because, people are not familiar with this system.

According to some clients’ opinion, introducer is one of the problems to open an

account. If a person who is new of the city wants to open account, it is a problem

for him/her to arrange an introducer of SB or CD accounts holder.

They can’t provide loan on the basis of customers demand for the lake of enough

deposits.

There are several weak points in the existing loan appraisal system of Southeast

Bank ltd. The CIB report from Bangladesh Bank does help a bit, particularly

with information on outstanding loan. But it does not help the bank to make a

comprehensive judgment on the borrower’s credit standing.

The average loan processing time is relatively long. This is particularly true for

project loan, which usually takes over one month to complete the processing. .

Bangladesh Bank exercises strict control credit activities in local banks. Sometimes the

restriction imposed, can create barrier in the normal operations and policies of the bank.

Sometimes the bank changes their pricing policies, in due time customers may not aware

about it.

3.2 Academic Preparation:Before internship I don’t have any practical experience in corporate side. For this reason

while I am working in SEBL, I have learnt various types of work which I mentioned in

chapter- 2. Besides that I found some mismatch while working in the organization like,

Sometimes I was assigned to do some jobs without explaining why this work is to be done.

This situation has created a lot of problems to understand why a specific function is being

performed. I am from Accounting and finance department. So, relevance of the academic

20

major I found some difference between assigned tasks and academic major. Like, most of the

assigned tasks are not practically done before during different semester.

3.3 Missing knowledge and skills that need to be learned:

In many cases, I have experienced mismatch with my academic courses while I was doing

internship program. This is because the university does not always provide the practical

knowledge and I found a few courses those focus on banking activities solely. In my BBA

course I had to gain knowledge in various broader aspects including finance, accounting,

capital budgeting, taxation, where very few of them deeply focuses on banking activities.

Also, the university always gives emphasis on the theoretical knowledge and I did not much

scope for gaining practical knowledge on banking activities. There is some knowledge that

needs to be learned in the university which is actually relevant to the organizational culture.

Like-

Beside bookish knowledge university should go for field visit for practical example

during different semester.

University could start different workshop or seminar program. They should call

different company employees to take different seminar or classes. In that case they

can share their corporate experience and knowledge. This is actually very helpful for

the students.

University should give some challenges work to understand the situation and also give

some practical knowledge to handle these situation.

21

Chapter 4Lessons Learned from

the Internship Program

22

4.0 Lessons Learned From The Internship Program:

4.1 Implications to organization/company:

Multi-dimensional Task Accomplishment:

It is required that an intern will deal with various sectors and departments of an organization.

The variety of task I have performed in the Branch was not of the same taste; however, I felt

that I have achieved some more dimensions while I was studying on the various sectors of the

organization. These multi-dimensional pieces of work could be valuable for my career ahead

of me.

Taking Responsibilities:

To take responsibilities and to give a positive result end of the day is itself a big

challenge. SEBL has provided me a vast knowledge of this. Here I have personally seen

corporate people with their responsibilities every day. My confidence level has gone higher

than I expected by spending this short period of time at SEBL.

Experience Gain:

I worked at SEBL as an intern for 3 months and I feel very lucky that my step is right and

perfect. This company has enough individual corners from where I feel experience is a must

thing to gain here. Seniors at this place has always been very helpful to provide enough

guidance to gain experience. With the help of my education and presence at SEBL has given

some idea about overall banking operation.

Discipline:

Discipline maintaining at SEBL corporate offices is a key thing. Besides hard working

capability this company highlights every individual’s discipline level separately. So far I

have maintained myself well here, for example – I always maintain my office timing.

Enhancement of Communication Skill:

As a fully customer oriented organization, the SEBL operates great customer service where

the communication skill is one of the fundamental factors. Treating every customer in bank’s

customized unique way is a challenging thing as I observed while working with the staffs of

23

the branch. I have achieved significant amount of knowledge about customer service and I

have realized that great communication skill is the fundamental requirement of serving the

customers with great service.

Familiarization with Corporate Culture:

I have also observed the customers from different cultures are being served by the bank and

gained the skill of maintaining a unique culture regardless possessing different cultural

backgrounds by the people. Additionally, the corporate culture of the SEBL was really

friendly and cooperative for me during my whole internship program.

Adjustment with the Work Place and Socialization:

Organizational socialization means the adjustment of the skill, academic knowledge and

behavior with the working environment in the working place. While I was performing my

internship program within the bank, I was being treated as an employee like others in the

organization. I got sufficient assistance from the working people in terms of acquiring enough

idea about their working strategy. This enhanced my knowledge, skill and the power of

implementing of my academic knowledge in a workplace. I believe this is much quite

important and also the whole program made me ready for starting my professional career in

the same environment.

Initiative:

SEBL always appreciate take initiative for work challenge & help those with all

resources for achieving their goals. I have learned way of working from my seniors

and now I have confident enough to take initiatives before others.

Customer secrecy:

The bank always tries to keep the customer secrecy. The Bank never discloses one client’s

information to other clients. For example, husband’s cheque book or ATM pin is not given to

wife for safety. Before doing majority of tasks the bank at first go for verification like

informing balance information, providing statement, fund transfer issuance of cheque book

etc.

24

4.2 Implications to University’s Internship Program:

This internship is a part of our BBA program. AIUB has given us this opportunity to have a

practical job experience before getting into a permanent job as a full time employee.

Definitely this internship program will help us a lot in job sectors. Internship helps us to learn

lots of things which will be very effective for the near future.

From university’s internship program I have learned-

The main point I have learnt from internship is that the difference between academic

knowledge and professional work.

I learnt how to follow my supervisor instruction and his valuable suggestion.

University helps me to improve my presentation skill during different semester which

is actually helps me a lot when I am face to face a customer in the organization.

Co education in the university helps me to be communicative and friendly.

How to give a company’s portfolio in the report.

How to present work experience in the repor.t

Cooperative education experience.

Concern for integrating experiences and external experiences.

4.3 Others:

While doing this internship I have learned lots of new things, which was totally unknown for

me. Besides learning from the organization and the university I have also learned some other

things which are very essential for me.

Increased trust, confidence and professionalism

Improved subject area and discipline knowledge

Increasing sophistication

Developing skills and competencies

25

Chapter 5Concluding Statement

5.0 Concluding Statement

5.1 Summary:

26

As an intern student at Southeast Bank Limited at Kakrail Branch, Dhaka, I have truly

enjoyed my internship from the learning and experience viewpoint. I am confident that 3

months internship program at SEBL to meet the requirement of the course outline as well

as to comprehend the application of the theoretical knowledge in the practical fields.My

internship report on the topic, “A Study on Practices & Policies of Credit Management of

Southeast Bank Limited, Kakrail Branch.” The main point of this report was to identify

the activities of credit department.

During the course of my practical orientation I have tried to learn the practical banking

activities to realize my theoretical knowledge, what I have gathered and going to acquire

from various courses. It is great pleasure for me to have practical exposure of Southeast

Bank Limited, because without practical exposure it couldn’t be possible for me to

compare the theory with practice.

So in conclusion it can be said that every organization has its positive as well as negatives

and in case of Southeast Bank Limited existence of the later one is less than the earlier

one and as the management is determined to reach the pick of success it seems that in

near future the negatives will be eliminated. The performance of the bank has been

evaluated with respect to different performance dimensions and with their able leaders

Southeast Bank will reach the highest level of success very shortly. I wish the bank all

success prosperity in their field.

5.2 Recommendations for Future Strategic Actions (Organization

Perspective):

27

In such competitive modern days in Banking, Bank as Southeast bank is also facing some

recognizable challenges. SEBL has to take necessary steps to meet the challenges with

appropriate efforts. Here suggestions that I have for this course of action.

The Bank should increase its ATM booth in different locations and improve its

facility throughout the country.

Although every table of every section of SEBL is capable of supplying the various

information about bank but this task is generally performed by the front desk or

account opening section. However this section is found always busy. Therefore, if

bank wants to perform this task in more efficiently the branch should keep a

Reception Section.

SEBL could arrange the monthly seminar or workshop on the vast area of Credit

Management and its contemporary issues for the branch’s offices, certainly this

workshop will motivate them.

For customer’s convenience in Credit Department of Southeast Bank Ltd should

provide more personnel to deliver faster services to their customer.

They should also focus on the marketing aspects to let customers know about their

products and offerings and more promotion should be given to attract new customer.

Southeast Bank Ltd should provide an effective training program for the junior level

officers as though they can perform their task efficiently.

They should provide prayer facilities for female employee.

5.3 Recommendations for Future Strategic Actions (University

Perspective):

The communication between the intern and the supervisor should be quite clear and

on the regular basis so that the intern has the total understanding and control over the

entire internship program.

The university sometimes could take initiative for the students who often fail to get

offer from the companies for internship. The university could make some reference

lists with big companies and make them offer its students for internship.

The interns could get highly motivated by the supervisors while they will be

performing the internship program in some particular companies. This motivation will

drive the interns to get jobs.

28

29

30

Chapter 6Suggestions for Improvement or Course of Action

6.0 Suggestions for Improvement or Course of Action:

31

Improve office atmosphere to give customers better feeling.

They should introduce new products and services.

Southeast Bank Ltd should establish and adhere to adequate of loan provision and reserve.

Southeast Bank should always monitor the performance of its competitors in the field of

Credit management.

To ensure timely repayment of loan installments, banks need to have well-

coordinated supervision and monitoring programs.

Use of effective management information systems.

SEBL should focus on their promotional activities.

SEBL has to follow safety lending strategy carefully and corporate governance.

Up to date banking software should be use to give better service to the customers.

Manpower should be increase in Credit section.

References

32

Southeast Bank Ltd Annual Report from 2004 to 2012.

Memorandum and Articles of Southeast Bank Ltd.

Records & files used in official correspondence for day to day operation.

www.Southeastbanklimited.com

Face to face conversation with the section Credit In-charge of Southeast Bank

Limited, Kakrail Branch.

Discuss with the senior officers of Southeast Bank Limited, Kakrail Branch.

Appendices

33

CV

34

![[6]Report Body](https://img.pdfslide.us/doc/110x75/577d295b1a28ab4e1ea690c4/6report-body.jpg)

![Marketing Report [Body]](https://img.pdfslide.us/doc/110x75/577d379f1a28ab3a6b960854/marketing-report-body.jpg)