Embed Size (px)

DESCRIPTION

Become a mortgage broker Pty Ltd. provides specialist training to assist new Mortgage brokers in the industry. Our different tailored courses make you enable to accredited Certificate IV and diploma mortgage broker programs. If you are interested in becoming a mortgage broker with our company, please contact us.

Citation preview

BAMB250113 Page 1

Business Opportunity

Copyright © Become A Mortgage Broker Pty Ltd

BAMB250113 Page 2

Welcome

Become A Mortgage Broker can offer you the opportunity to train in a fantastic

new career as a mortgage broker. We were formed to fill a void in the

mortgage and finance industry. There are many companies providing specific

training but Become A Mortgage Broker takes you a few steps further. We

assist you all the way by co‐ordinating all your training to become an

accredited mortgage broker, mentor you and provide you with all the training,

assistance and supporting tools to prepare and submit loan applications to the

banks for as long as you wish. If you have been searching for a specialist training provider that delivers

results, then you’ve found the right place.

We would be delighted to hear from you, so we can contribute to your future

success!

BAMB250113 Page 3

About Become a Mortgage Broker Pty Ltd

Become A Mortgage Broker Pty Ltd was established to assist new entrants into

the mortgage industry and to facilitate ongoing training.

Our experienced staff will explain to you the rules and the process required to

be a mortgage broker and guide you through the whole process from obtaining

Certificate IV in Financial Services to obtaining accreditation with numerous

banks and other lending institutions.

In addition, we will appoint a mentor who holds an Australian Credit Licence

issued by the Australian Securities and Investment Commission to provide

continuous training and assistance for the mandatory 2 years and beyond.

Through the mentor’s company, you will operate as an Australian Credit

Representative. Members have access to a broad range of lenders and their

products. Through our partners and alliances, we supply the technology,

lender access, training and support that enable members to service their

clients in the most professional and efficient way possible.

If you’re interested in becoming a mortgage broker with our company, please

Contact Us.

Website: www.become‐a‐mortgage‐broker.com.au

Email: info@become‐a‐mortgage‐broker.com.au

BAMB250113 Page 4

Become a Mortgage Broker

Consumers, now more than ever, recognise the importance of seeking expert

advice on something as important as their mortgage. As a consequence of this,

more and more people are turning to the professional service that a mortgage

broker provides.

Becoming a mortgage broker is relatively easy when compared with other

professional roles such as becoming a financial planner, accountant or solicitor.

No tertiary education is required and industry experience is not essential to

success.

Industry Partners:

BAMB25

Acc

The fin

Our ex

and da

occupi

loans,

50113

cess to

nance mar

xtensive le

ad applica

ied or inve

commerc

o ove

rket is ver

ending pan

nts to the

estment p

cial, prope

r 30 L

y diverse

nel of 30 l

e self‐emp

property. I

rty develo

Lende

with ever

enders ca

ployed who

n addition

opment, b

ers

y borrowe

aters for a

o wish to

n, it caters

business a

er having

ll needs fr

purchase

s for non‐c

nd insuran

unique ne

rom the m

an owner

conformin

nce

Page 5

eeds.

mum

r

ng

BAMB250113 Page 6

Benefits

Low start‐up costs and relatively low on‐going costs.

High earning capacity as well as the ability to earn passive income

through trailing commissions.

Ability to work from home.

Flexible working hours allowing you to take control of your life, and not

have an employer (other than you) controlling you!

A mortgage broking business is a saleable asset. Not only will you have

the potential to earn a great income, but you can sell your business in

the future should you choose.

Become your own boss… and potentially someone else’s!

The mortgage broking industry is a safe and stable industry… this is not a

fad that will fade with time.

Happiness – A recent study found that the group of people who seemed

to be the happiest and most content in their lives were those who

worked for themselves!

Deal with an established and reputable company.

We will guide you and assist you with all accreditation requirements.

We will arrange training with banks and other lenders.

Ongoing mentoring.

Customer Relationship Management System.

Marketing tools.

Online access to customer records and supporting documents.

Access to numerous industry calculators.

Up‐to‐date lender application forms.

Up‐to‐date lender policies.

BAMB250113 Page 7

Up‐to‐date lender products.

Up‐to‐date lender interest rates and fees.

Government documents such as First Home Owners Grants.

National Consumer Credit Policy documentation.

Online training videos and material.

Friendly ongoing support.

Assistance with loan scenarios.

Assistance with loan structuring.

Cross selling opportunities.

We will assess, submit and manage applications to the Lenders on your

behalf.

Ability to work and track progress via internet anywhere in the world.

Commissions itemised and paid monthly.

Your mentors have combined industry experience of over 45 years.

No fixed length contracts, just 30 days exit notice.

…..and much more.

BAMB25

Lea

Our so

Symm

from s

Sales R

50113

ding

oftware Sy

etry has e

sales throu

Results

Edge

ymmetry,

extensive f

ugh to ma

Mort

sets the b

functional

nagemen

tgage

benchmark

lity to cate

t.

Softw

k for loan

er to every

ware

originatio

y part of y

on systems

your busin

Page 8

s.

ness,

BAMB25

Admin

Manag

50113

nistration e

gement de

efficiencie

ecisions

es

Page 9

BAMB25

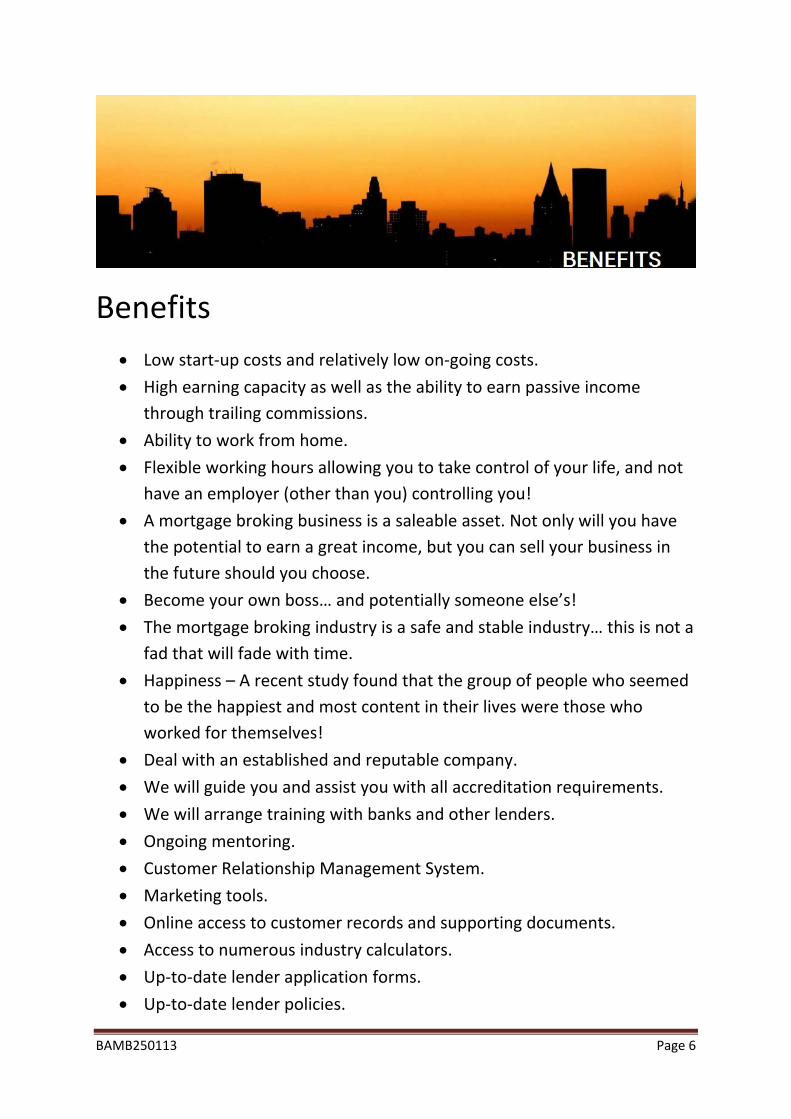

Minim

Calcula

50113

mise your IT

ate and qu

T costs

ualify

Page 10

BAMB25

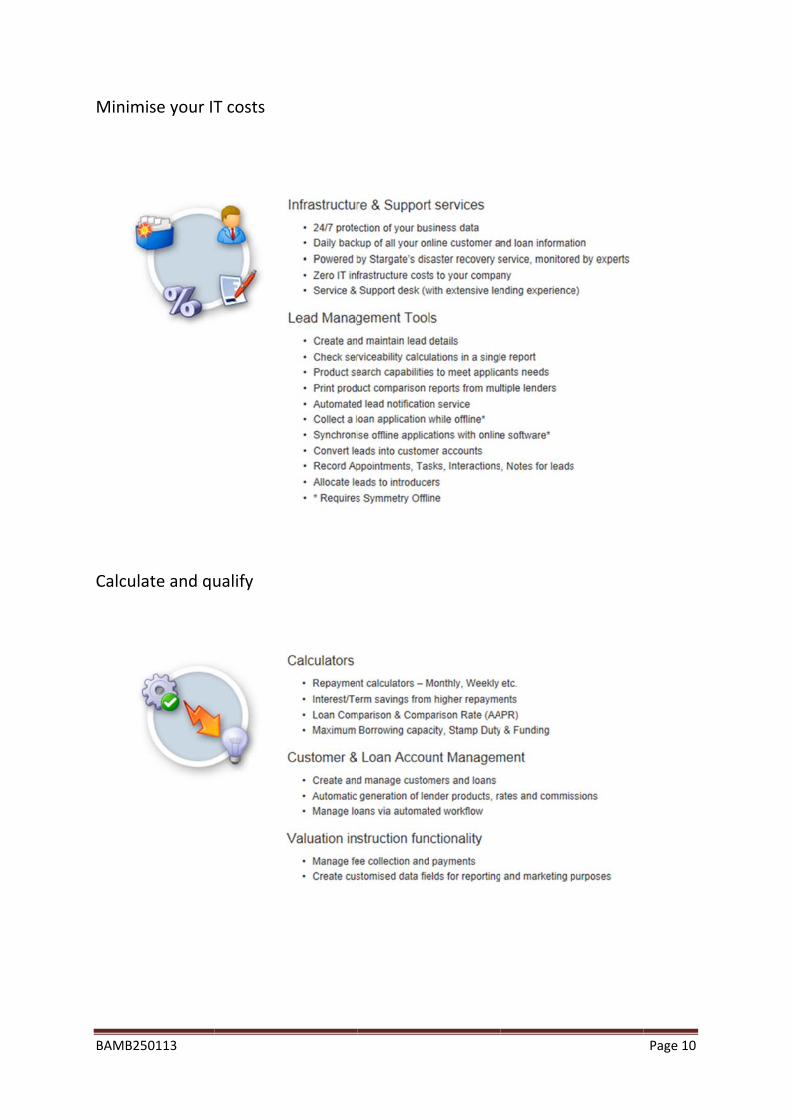

Manag

CRM a

50113

gement at

and more

t a touch

Page 11

BAMB25

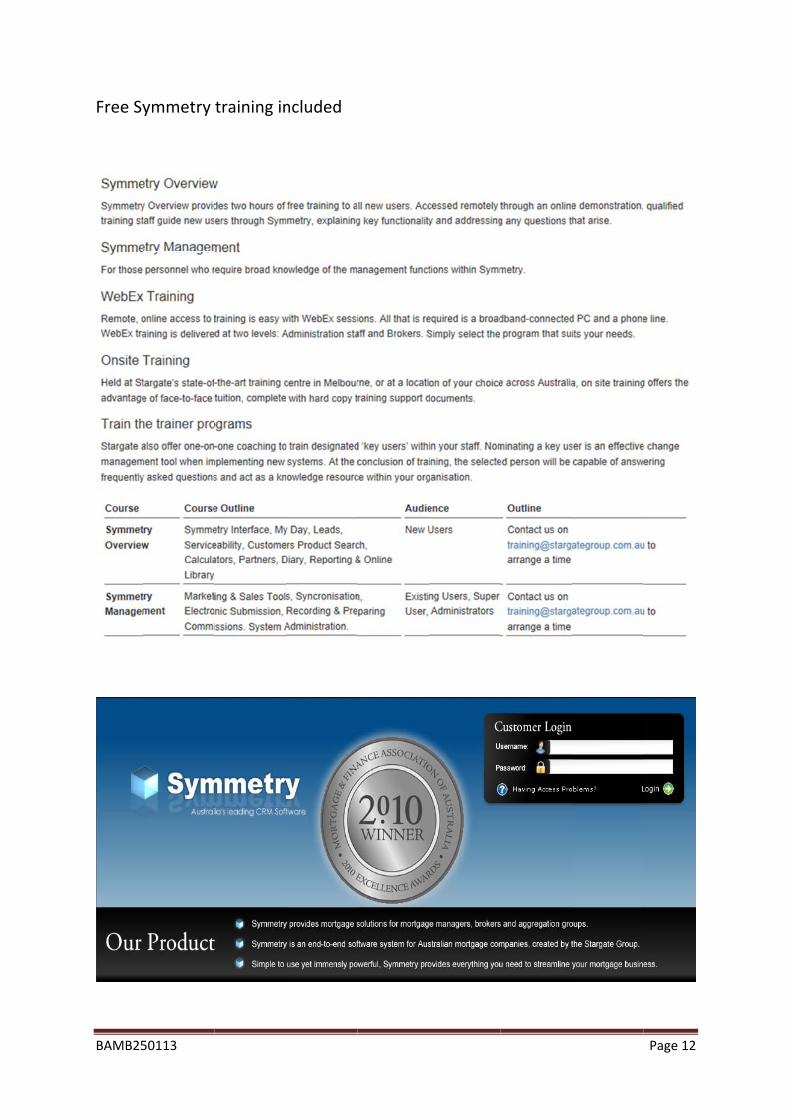

Free Sy

50113

ymmetry training inncluded

Page 12

BAMB25

Pot

Your e

comm

Upfron

betwe

comm

lender

receive

Trail co

the loa

Theref

Aggreg

on ave

We ha

broker

calcula

Comm

25%.

The an

Comm

first ye

50113

entia

earnings ar

ission.

nt commis

en panel

ission is c

r pays the

e on avera

ommissio

an for the

fore, on a

gator $62.

erage 75%

ave prepar

r settles o

ation is als

mission of 0

nnual Upfr

mission com

ear to $61

l Earn

re derived

ssion is pa

lenders an

urrently 0

Aggregato

age 75% o

n is paid m

month. O

$500,000

.50 per mo

% of that in

red a table

n average

so based o

0.15% pa.

ront Comm

mpounds

1,476 in th

ning C

d from two

ayable whe

nd is a one

0.6%, there

or $3,000

of that inco

monthly o

On average

0 loan on a

onth and

ncome or $

e on the P

e $1,000,0

on an aver

It is also b

mission of

each year

e fifth yea

Capac

o sources.

en a loan

e‐off paym

efore, if y

and after

ome or $2

n the life

e trail com

an interest

after they

$46.88 pe

Potential E

000 per mo

rage Upfro

based on

f $54,000

r as the po

ar.

ity

. Upfront

settles. Th

ment. On a

ou settle a

r they ded

2,250.

of the loa

mmission i

t only bas

y deduct t

er month.

Earning Ca

onth for th

ont Comm

an averag

does not v

ortfolio gro

commissio

he amoun

average u

a $500,00

uct their f

n based o

s currentl

is, the len

heir fees y

pacity if a

he first 5 y

mission of

ge Aggrega

vary but t

ows from

on and tra

nt varies

pfront

00 loan, th

fees you w

on the bala

y 0.15% p

nder pays t

you will re

a mortgag

years. The

0.6% and

ation Fee

the Trail

$7,332 fo

Page 13

ail

e

will

ance of

p.a.

the

eceive

e

e

Trail

of

or the

BAMB250113 Page 14

Potential Earning Capacity Calculator

By consistently settling on average $1,000,000 per annum or about 3 loans per

month, your income increases from $61,332 for the first year to $115,476 for

the fifth year.

The calculation does not include loans that may close, loans in arrears or

principal reductions.

Your annual Trail Commission is the value of your business and you can sell it

at a multiple of 1.5 to 3 times depending on the quality of the portfolio. As an

example, if you sell your loan book after year 5, the value could be as high as

$184,428 ($61,476 x 3).

Disclaimer: The above table is for illustration purpose only and subject to individual

agreements with your Aggregator and/or your Credit Licensee and should not be construed

as a guarantee or warranty of income. Factors such as experience, personal objectives,

location and skills will vary from broker to broker, therefore individual results will vary. The

table is for example purposes only. Every effort has been made to accurately present the

above figures and their potential. Earning potential is entirely dependent on the broker’s

ability and the Lenders commission rates and fees which are subject to change from time to

time.

BAMB250113 Page 15

Frequently Asked Questions

What Brokers Do?

Brokers work with clients to determine their borrowing needs and capacity,

select a loan that suits the borrower’s aims and objectives and manage the

process through to settlement. Brokers need strong financial literacy skills,

excellent people and customer service skills and the ability to really listen to

clients’ needs.

What is the difference between using a mortgage broker instead of going

directly to a bank?

A mortgage broker has access to most products offered by most banks, non‐

banks and financial institutions. They know how to structure transactions to

meet the clients’ requirements and the lender’s policies.

Other benefits in dealing with a broker are:

• Convenience;

• Mobile and usually are available outside bank trading hours;

• More personalised service;

• Greater expertise as they focus on loans only; and

• Unbiased opinions.

BAMB250113 Page 16

Is there a demand for brokers?

The demand for qualified and ethical mortgage and financial professionals is

growing, as more and more consumers turn to brokers as a trusted source for

housing and/or business finance.

Are there fees involved to become a mortgage broker?

Just like any start up business, there are fees involved but these fees are

minimal.

Can I be a part‐time broker?

Yes you can. Hours of work for a self‐ employed mortgage brokers is very

flexible.

We have mortgage brokers who have full time jobs and manage to have a

successful home loans business as well. Obviously input reflects output.

Can I make money whilst I am learning the business?

With our business, you can ‐ You can start generating commissions

immediately.

You will be able to start marketing and networking well before you have

completed the accreditation process. When you identify a prospective client

for a home loan you notify your Mentor, who will guide you through the

process.

What is a Mentor?

Industry membership requires that an applicant with less than 2 years’

experience (over the past five years) in mortgage lending, mortgage broking or

finance broking must be nominated for membership by another member (or

member’s representative) who undertakes to mentor (or ensure the mentoring

of) the applicant (mentee) until they have at least 2 years’ experience.

Where do the clients come from?

You will learn several proven marketing strategies that you could implement to

become visible to your marketplace.

BAMB250113 Page 17

Without doubt, the most effective method of having a continuous flow of

clients is referrals from strategic alliances or partnerships that you form.

These could be with Real Estate agents (or real estate salespeople),

Accountants, Lawyers, Insurance Agents and many other types of businesses.

These alliance partnerships might require you to remunerate your partner (not

in all circumstances) from the commissions that the referral has generated.

Think about this, if you were prepared to offer 50% of all upfront commissions,

would you agree that many partnership possibilities could result?

50% is very generous and unheard of but it will serve as an example.

This would be especially appealing to Real Estate sales people fighting for

market share. If the referral leads they give you result in 2 – 3 loans per month,

and you paid them 50% / 50% of upfront commission, they could earn an extra

$2,000 to $3,000 per month by simply passing on the leads and opportunities

to you… and you do all the work!

Do I need an ABN (Australian Business Number) and pay GST?

Yes! ‐ You will be paid your commissions with GST. You are a contractor /

service provider and therefore attract GST. Everything (business related) that

you pay GST on can be credited against the GST you get paid. NB GST is not

compulsory until you generate $75,000 p.a. income

What type of loans do brokers do?

Brokers can specialise in areas such as:

• Residential Loans

• Reverse Mortgages/Equity Release

• Equipment Leasing

• Chattel Finance

• Car and Personal Loans

• Business Loans

BAMB250113 Page 18

• Debtor Finance

• Commercial Property Finance

Many brokers are gaining additional skills and qualifications to expand their

client services into areas such as general insurance and financial planning.

How can I write loans with different Lenders?

A broker has to obtain accreditation with lenders in order to sell their

product/s. Most brokers will become accredited with a number of lenders –

called a ‘panel of lenders’. Brokers are only able to sell products from lenders

on their panel. The requirements for accreditation vary from lender to lender,

as too does the size of each broker's panel. Some lenders have minimum

volume loan requirements in order to achieve and maintain accreditation.

What are Aggregators & Franchise Groups?

Many brokers join an aggregator or franchise group to access the group's wide

panel of lenders. These groups provide many additional services to brokers

such as software and technology, training, general business support and back

office administration.

How do I obtain Lender Accreditation?

A broker/brokerage has to obtain accreditation with lenders in order to sell

their product/s. Most brokers will become accredited with a number of lenders

– called a ‘panel of lenders’. Brokers are only able to sell products from lenders

on their panel. The requirements for accreditation vary from lender to lender,

as too does the size of each broker's panel. Some lenders have minimum

volume loan requirements in order to achieve and maintain accreditation.

What is Professional Indemnity Insurance?

Like many other businesses, brokers also need to maintain professional

indemnity insurance.

It is an ASIC requirement for brokers to be covered by or personally have in

place, PI Insurance for no less than $2 million for any one claim and $2 million

in the aggregate and minimum Run‐Off cover.

BAMB250113 Page 19

What is Membership of the Credit Ombudsman?

Many businesses are joining an external dispute resolution (EDR) scheme as

part of their consumer complaints handing processes. The industry's EDR is the

Credit Ombudsman (COSL).

ASIC requires brokers to hold membership of COSL (or another ASIC approved

EDR) or be covered by a COSL membership.

What are the Pay Levels?

Brokers are remunerated by the lender and receive an upfront commission and

a trailing commission on the loans they settle. It is not standard industry

practice for a broker to charge a customer for their service due to this

arrangement although, the changes required by the new Credit Legislation may

mean some brokers will charge a fee and receive a commission. Consumers

should be encouraged to ensure that a broker provides them with this

information before they engage his or her services

What is AML/CTF?

The obligation referred to is the Anti‐Money laundering and Counter‐

Terrorism Financing Act 2006.

It is to update and eventually supersede the Financial Transaction Reports Act

1988 that gave rise to what is currently the 100 Points ID check, suspicious and

other transaction reporting. The ultimate purpose is to upgrade Australia's

money laundering defenses to prevent the proceeds of crime and other illegal

activity entering or being passed through the financial system. Brokers will be

impacted either directly by providing what is described in the 2006 Act as a

"designated service" or by holding an AFSL and indirectly through the AML

compliance requirements of lenders or other providers of "designated

services" for which the broker is an agent.

Only businesses that are a "reporting entity" and thus covered by the 2006 Act

are required to be legally compliant and will be regulated by AUSTRAC.

However, agents such as brokers acting for principals that provide designated

services will be required by their principal through contract to also be

compliant.

BAMB250113 Page 20

Understanding the accreditation process

1. Upon your initial enquiry we will send you a Registration Form and

Information Pack which will provide you with details you need to get the

process going. Upon receipt of your application and joining fee, we will

send you out enrolment forms for your Certificate IV in Finance and

Mortgage Broking, Anti‐Money Laundering and Counter‐Terrorism

Financing Act 2006 (AML/CTF) course, application forms for National

Police Check, Introducer Accreditation and Symmetry CRM and

membership forms for the Credit Ombudsman Service Limited (COSL)

and Finance Brokers Association of Australia (FBAA).

2. Once you have completed and received your Certificate IV and AML/CTF

certificates, forward to us together with all other application and

membership forms and a copy of your resume, photo identification and

two business or character references. We will then conduct a Credit

Check and apply for the National Police Check. This should take one to

two weeks to complete.

3. On receipt of a clear National Police Check and Credit Check, we will

apply for your Professional Indemnity Insurance and apply to ASIC for

your Credit Representative number. We will forward to you an

appointment agreement as our Credit Representative. We will also apply

for your COSL and FBAA memberships. This should take approximately 4

to 6 weeks.

BAMB25

4.

5.

6.

The wh

return

to the

50113

On receip

accreditat

completio

directly to

approxim

Upon app

Agreemen

commissi

Induction

Once you

accreditat

hole proce

all the fo

time you

pt of your

tion with v

on and ret

o arrange

ately one

proval by t

nt setting

on structu

training.

have com

tion numb

ess depen

rms. On a

start writ

members

various le

turn and w

training a

week but

the Aggreg

out our te

ure and ar

Allow one

mpleted yo

bers, you w

nds on how

verage, it

ing loans.

hips, we w

nders and

will arrang

and accred

t will vary

gator, we

erms of en

rrange for

e day.

our lender

will be elig

w quickly y

t takes 10

will forwar

d the aggr

ge for the

ditation. T

from lend

will send

ngagemen

your Sym

r accredita

gible to st

you comp

weeks fro

rd to you

egator for

lenders to

his should

der to lend

you the In

nt includin

mmetry CR

ations and

tart writing

plete your

om the tim

applicatio

r your

o contact y

d take

der.

ntroducer

ng the

RM and

d received

g loans.

training a

me you en

Page 21

ons for

you

r

d your

and

quire

BAMB25

FeeTo pro

payabl

Certific

Compl

Nation

COSL

Veda C

FBAA M

PI Insu

ACR An

Symm

Symm

Trainin

Total

Sign N

Fee Pa

Conditio

* All fee

50113

es* oceed to th

le:

cate IV

liance Cer

nal Police C

Check

Membersh

urance

nnual Fee

etry Set‐U

etry First

ng

Now Disco

ayable

ons:

es are inclusi

he training

tificate (A

Check

hip

e

Up Fee

Monthly F

unt

ive of GST.

g and accr

AML/CTF)

Fee

reditation

Accred

3 mont

may ap

, the follo

itation mus

ths. After 3

ply. No refu

owing is a

$ 695

$ 275

$ 42

$ 125

$ 22

$ 410

$ 715

$ 660

$ 324

$ 181

$ 880

$4,330

$1,566

$2,764

t be comple

months add

unds.

list of all f

5.00

5.00

2.00

5.00

2.00

0.00

5.00

0.00

4.50

1.50

0.00

0.00

6.00

4.00

eted within

ditional fee

Page 22

fees

s

BAMB25

Wh

If you w

Registr

an inte

If you

Fax:

Webs

50113

at to

would like

ration for

erview.

have any

1300

site: www

: info@

do ne

e to progr

m and em

questions

798 696

w.become

@become

ext

ess to the

mail or fax

s, please c

‐a‐mortga

‐a‐mortga

e next stag

to us and

all us or v

age‐broke

age‐broke

ge, please

we will ar

visit our we

er.com.au

er.com.au

complete

rrange a s

ebsite:

e our

suitable tim

Page 23

me for

BAMB250113 Page 24

Registration

Name:

Address:

Phone: F Fax: Mob:

Email: A.B.N.: A.B.N.:

Have you ever been declared bankrupt, or subject to control under the Bankruptcy Act 1966? YES NO

Is there anything else we need to know as we consider your application e.g. bankruptcy, poor credit

history, AVO, health issues, driving restrictions or criminal convictions. YES NO

Have you ever had an application for the grant or renewal of a finance brokers licence or for YES NO

Registration to act as a finance broker refused?

Have you ever had a Lender or Industry Association decline or withdraw your accreditation? YES NO

DECLARATION BY APPLICANT: I, Authorise Become A Mortgage Broker Pty Ltd ABN 46 159 787 149 and Vault Mortgage Corporation Pty Ltd ABN 17 120 182 765 (Group) to carry out reference checks or make any other enquiries they feel necessary in assessing this application for accreditation. I confirm, agree, understand, acknowledge, represent and warrant that: a) Accreditation with the Group is at the absolute discretion of the Group.

b) To the best of my knowledge and belief, all the information given in this application is

true and correct.

Signature:

Date:

/ /

BAMB250113 Page 25

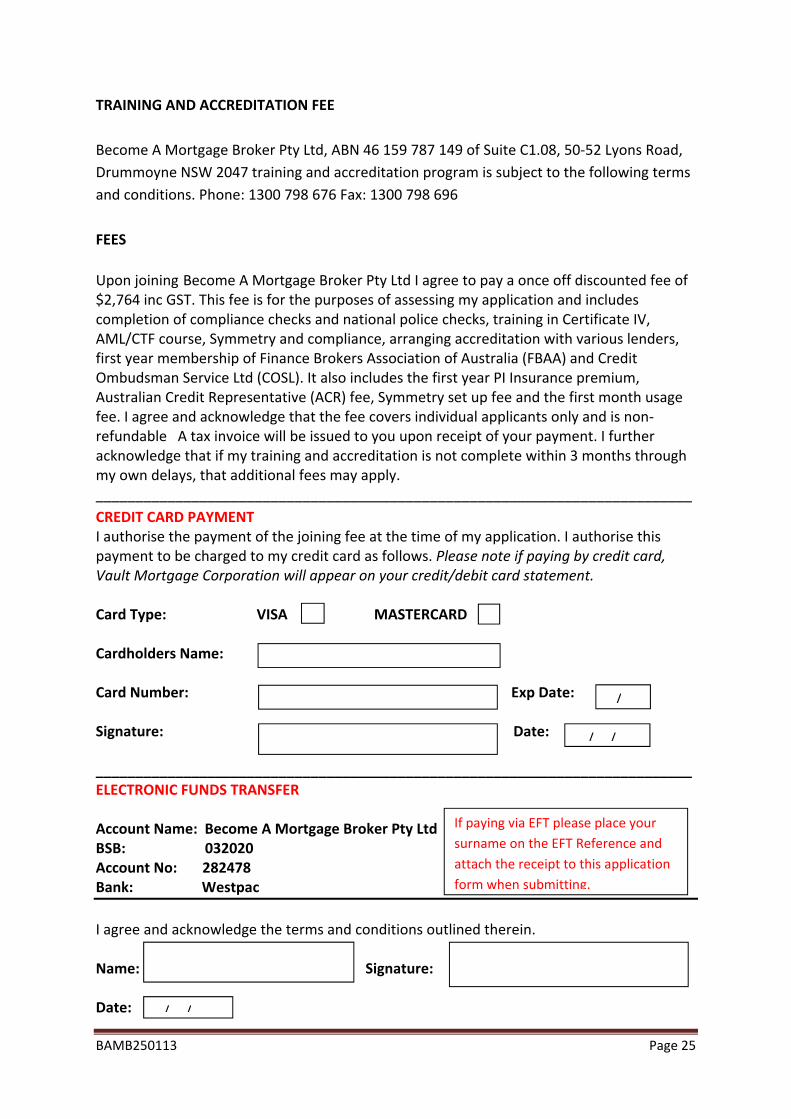

TRAINING AND ACCREDITATION FEE

Become A Mortgage Broker Pty Ltd, ABN 46 159 787 149 of Suite C1.08, 50‐52 Lyons Road,

Drummoyne NSW 2047 training and accreditation program is subject to the following terms

and conditions. Phone: 1300 798 676 Fax: 1300 798 696

FEES

Upon joining Become A Mortgage Broker Pty Ltd I agree to pay a once off discounted fee of $2,764 inc GST. This fee is for the purposes of assessing my application and includes completion of compliance checks and national police checks, training in Certificate IV, AML/CTF course, Symmetry and compliance, arranging accreditation with various lenders, first year membership of Finance Brokers Association of Australia (FBAA) and Credit Ombudsman Service Ltd (COSL). It also includes the first year PI Insurance premium, Australian Credit Representative (ACR) fee, Symmetry set up fee and the first month usage fee. I agree and acknowledge that the fee covers individual applicants only and is non‐refundable A tax invoice will be issued to you upon receipt of your payment. I further acknowledge that if my training and accreditation is not complete within 3 months through my own delays, that additional fees may apply. ___________________________________________________________________________

CREDIT CARD PAYMENT I authorise the payment of the joining fee at the time of my application. I authorise this payment to be charged to my credit card as follows. Please note if paying by credit card, Vault Mortgage Corporation will appear on your credit/debit card statement. Card Type: VISA MASTERCARD Cardholders Name: Card Number: Exp Date: Signature: Date: ___________________________________________________________________________ ELECTRONIC FUNDS TRANSFER Account Name: Become A Mortgage Broker Pty Ltd BSB: 032020 Account No: 282478 Bank: Westpac

I agree and acknowledge the terms and conditions outlined therein. Name: Signature: Date:

/

/ /

If paying via EFT please place your

surname on the EFT Reference and

attach the receipt to this application

form when submitting.

/ /