Embed Size (px)

Citation preview

ClassClass BBA (A)BBA (A)

Group memberGroup member Muhammad Ishfaq 83Muhammad Ishfaq 83 Asim Javed 04Asim Javed 04Abdus Samad Hashmi 93Abdus Samad Hashmi 93 Zahid Iqbal 84Zahid Iqbal 84Arshia Abbas 89Arshia Abbas 89 Muniba Gul 94Muniba Gul 94Sana Tariq 47Sana Tariq 47

Assignment

On

AccOunting

Bad Debts Bad Debts

Definition:The amount, which cannot be

recovered from the debtors are called bad debts

Debts that come from credit customers who do not pay their bills

Affects a company’s credit policy

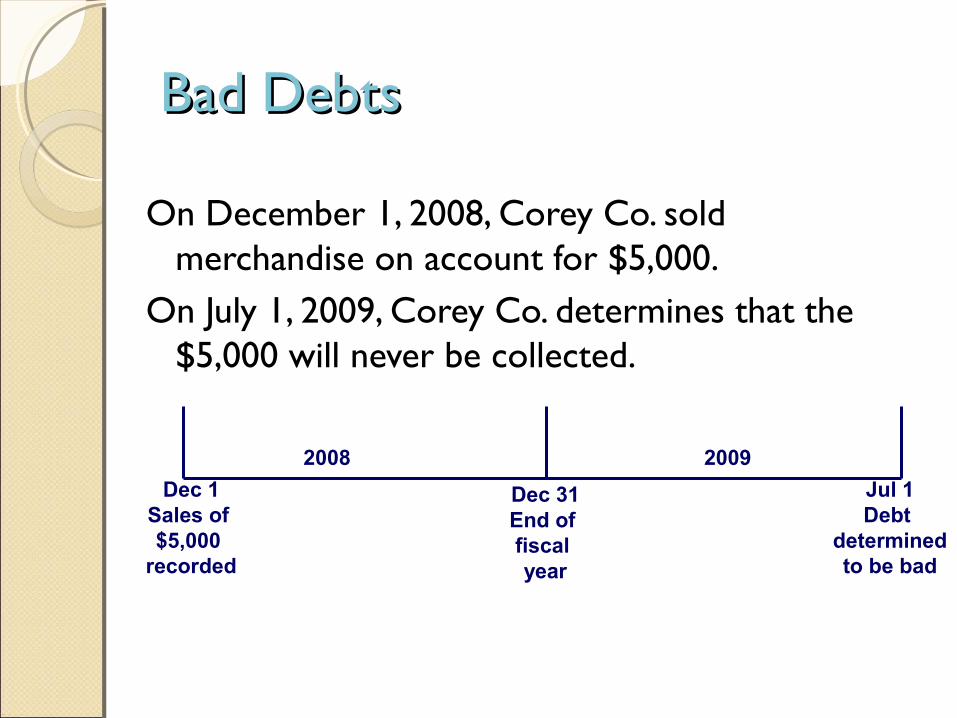

Bad DebtsBad Debts

On December 1, 2008, Corey Co. sold merchandise on account for $5,000.

On July 1, 2009, Corey Co. determines that the $5,000 will never be collected.

Dec 1Sales of $5,000

recorded

2008 2009

Dec 31End of fiscal year

Jul 1Debt

determinedto be bad

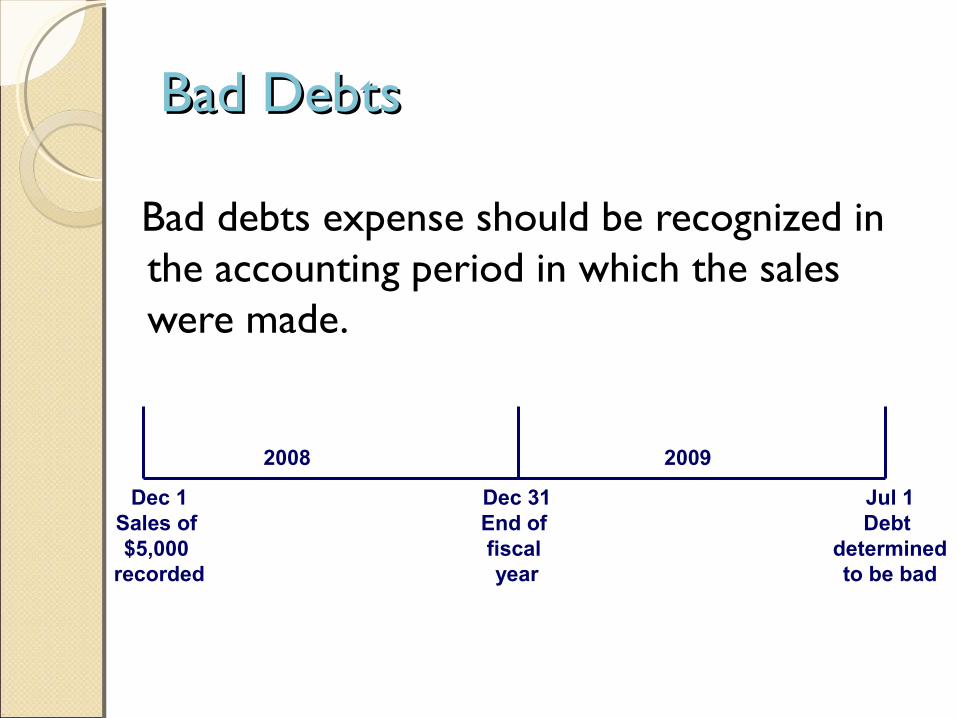

Bad DebtsBad Debts

Bad debts expense should be recognized in the accounting period in which the sales were made.

Dec 1Sales of $5,000

recorded

2008 2009

Dec 31End of fiscal year

Jul 1Debt

determinedto be bad

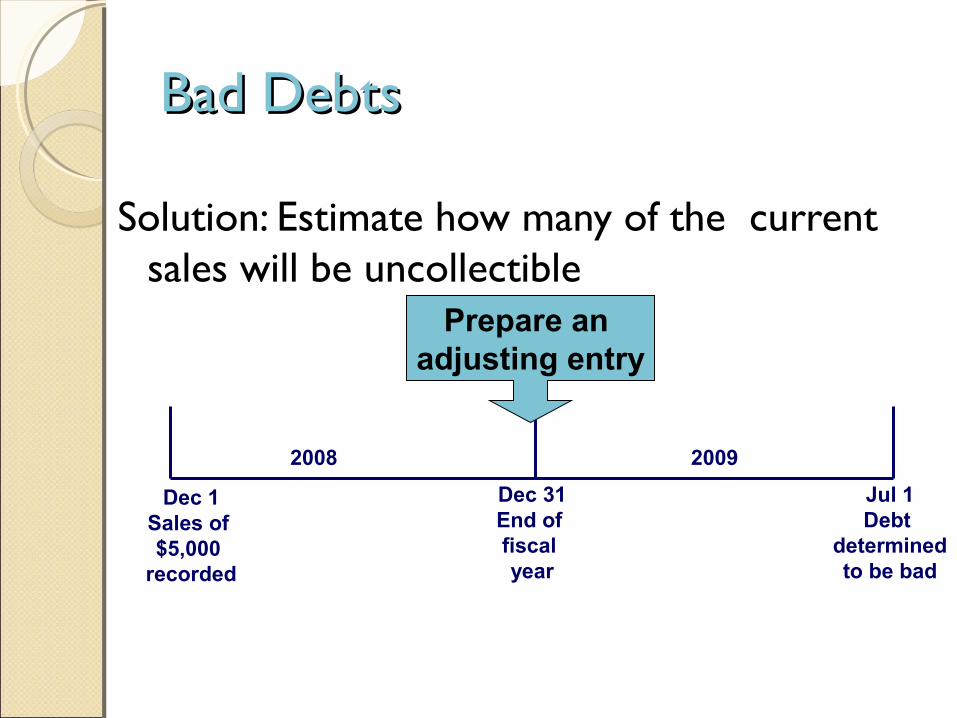

Bad DebtsBad Debts

Solution: Estimate how many of the current sales will be uncollectible

Dec 1Sales of $5,000

recorded

2008 2009

Dec 31End of fiscal year

Jul 1Debt

determinedto be bad

Prepare an adjusting entry

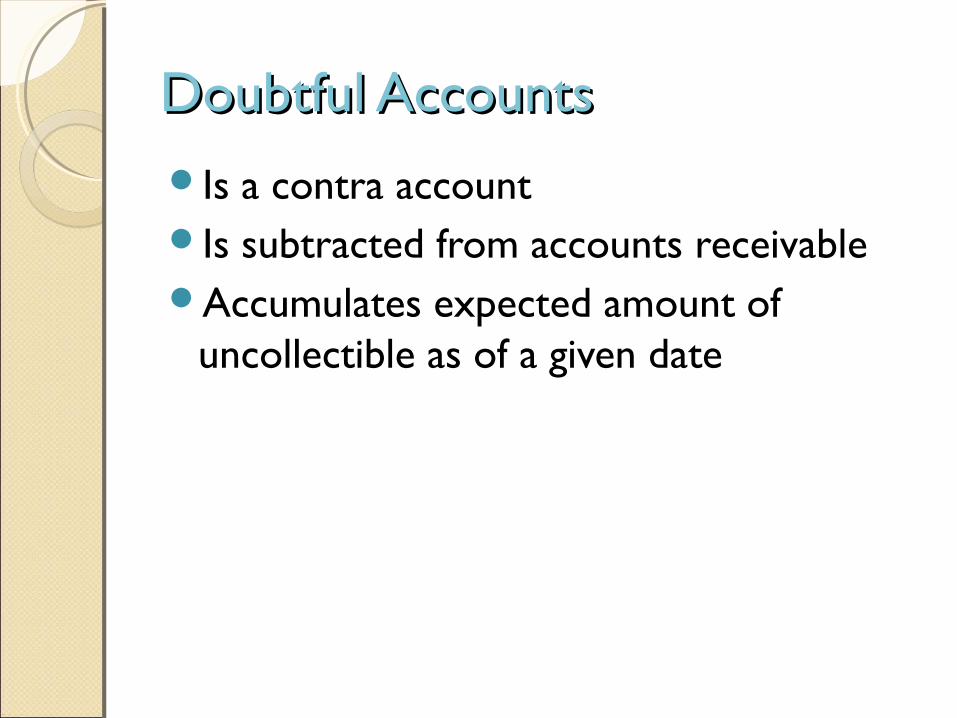

Doubtful AccountsDoubtful AccountsIs a contra accountIs subtracted from accounts receivableAccumulates expected amount of

uncollectible as of a given date

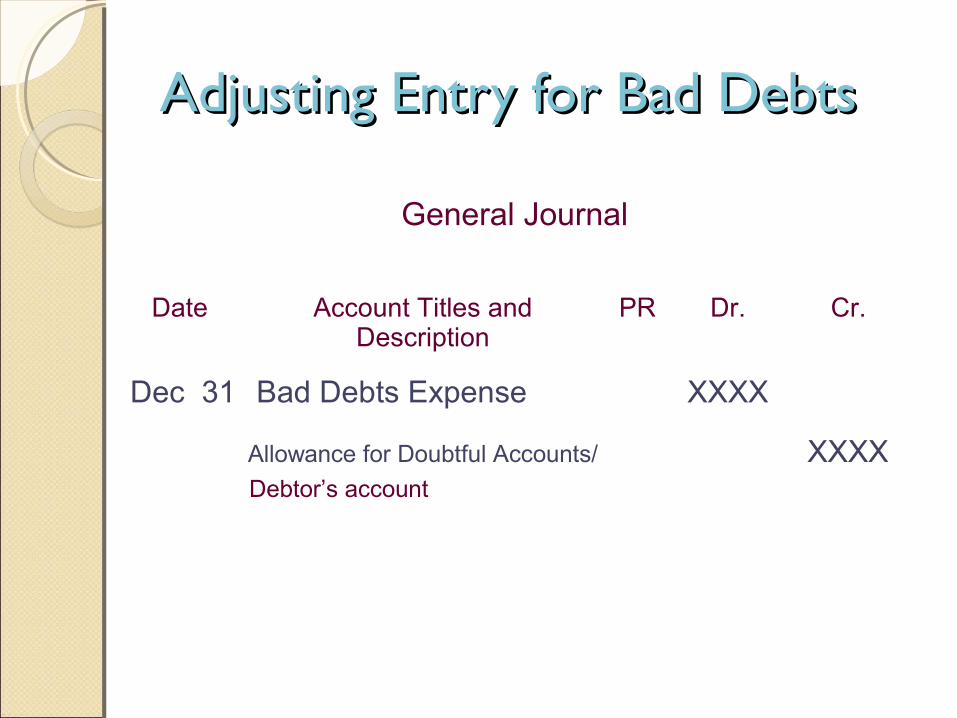

Adjusting Entry for Bad DebtsAdjusting Entry for Bad Debts

General Journal

Date Account Titles and

DescriptionPR Dr. Cr.

Debtor’s account

Dec 31 Bad Debts Expense XXXX

Allowance for Doubtful Accounts/ XXXX

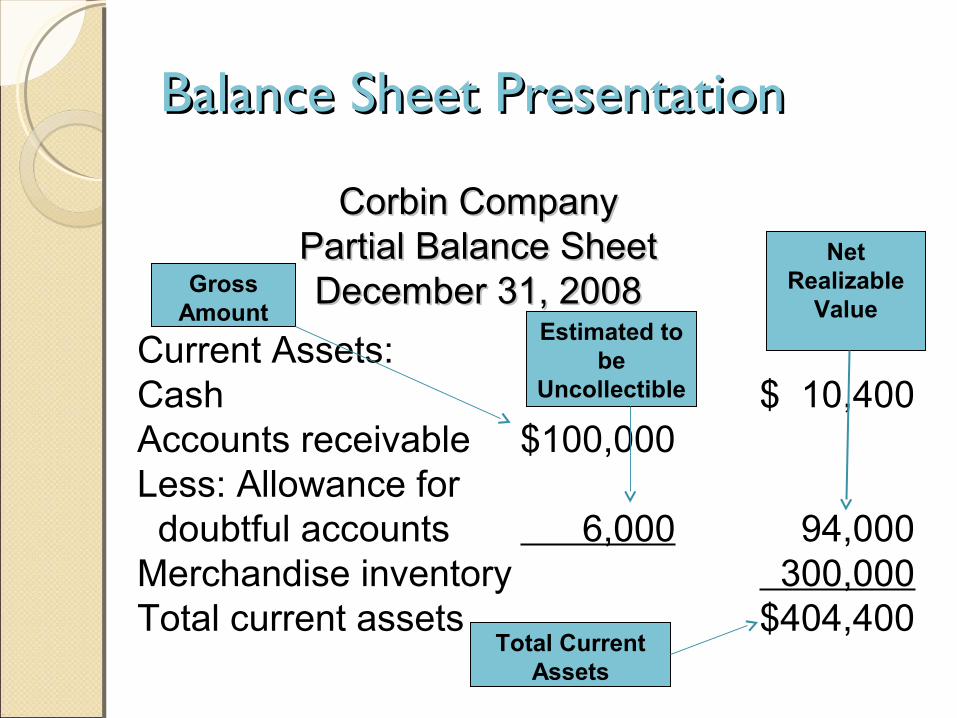

Balance Sheet PresentationBalance Sheet Presentation

Current Assets:Cash $ 10,400Accounts receivable $100,000Less: Allowance for doubtful accounts 6,000 94,000Merchandise inventory 300,000Total current assets $404,400

Corbin CompanyCorbin CompanyPartial Balance SheetPartial Balance SheetDecember 31, 2008December 31, 2008Gross

AmountEstimated to

beUncollectible

Net Realizable

Value

Total Current Assets

Net Realizable ValueNet Realizable Value• The amount of Accounts Receivable that

is expected to be collected• Calculated by subtracting Allowance for

Doubtful Accounts from Accounts Receivable

Income Statement ApproachIncome Statement Approach

Using the income statement approach and the balance sheet approach to estimate the amount of Bad Debts Expense

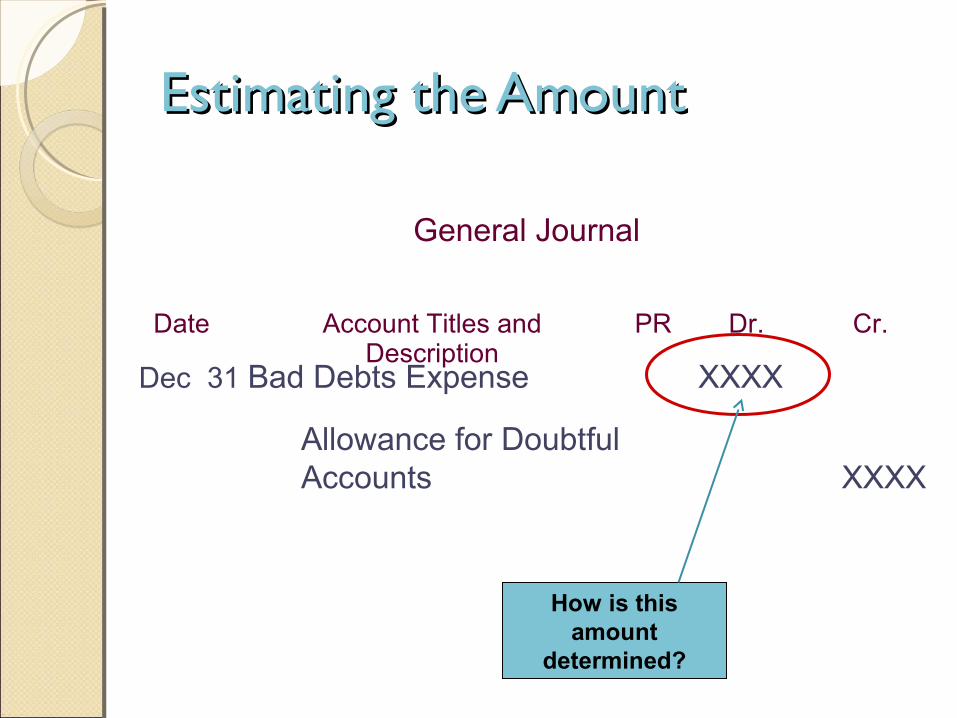

Estimating the AmountEstimating the Amount

General Journal

Date Account Titles and

DescriptionPR Dr. Cr.

Dec 31 Bad Debts Expense XXXX

Allowance for DoubtfulAccounts XXXX

How is this amount

determined?

Income Statement ApproachIncome Statement Approach

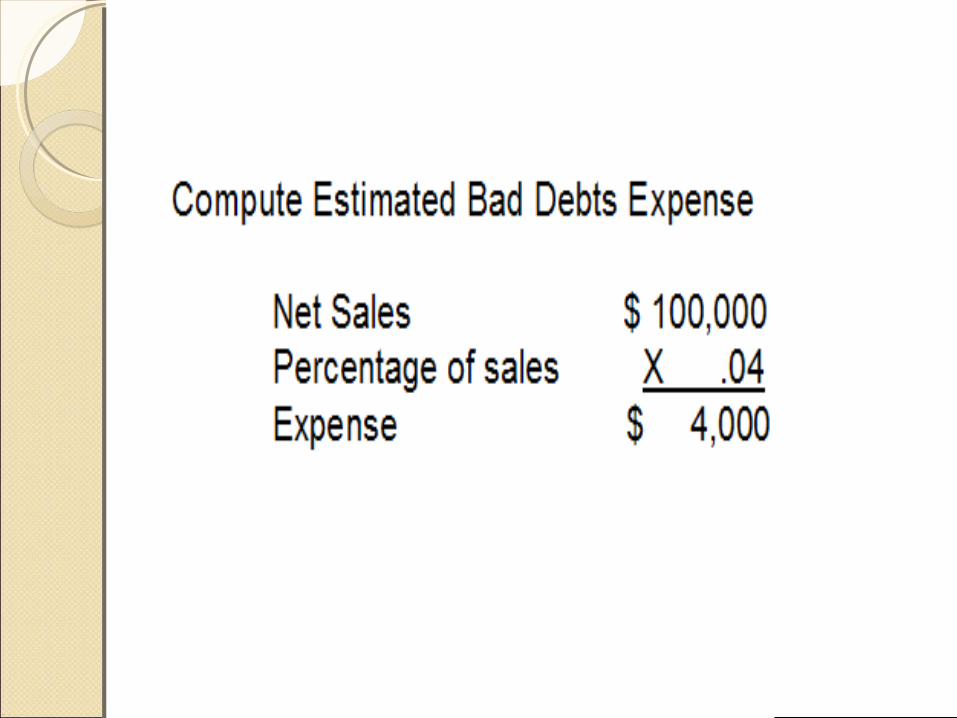

Bad Debts Expense = Percentage of net credit sales

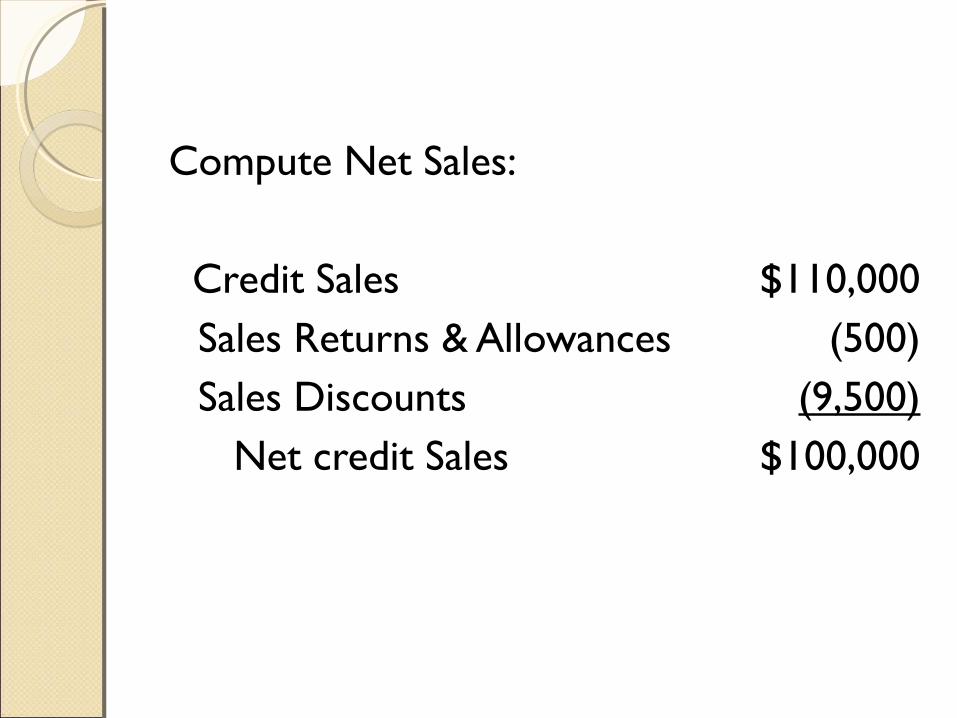

Compute Net Sales: Credit Sales $110,000

Sales Returns & Allowances (500)Sales Discounts (9,500) Net credit Sales $100,000

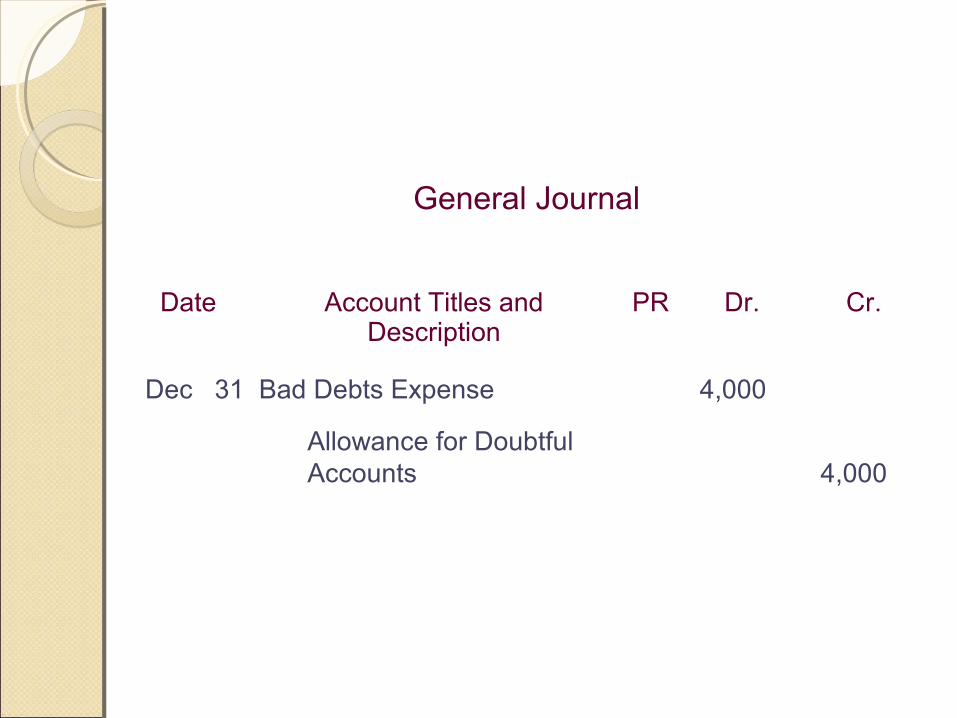

General Journal

Date Account Titles and Description

PR Dr. Cr.

Dec 31 Bad Debts Expense 4,000

Allowance for DoubtfulAccounts 4,000

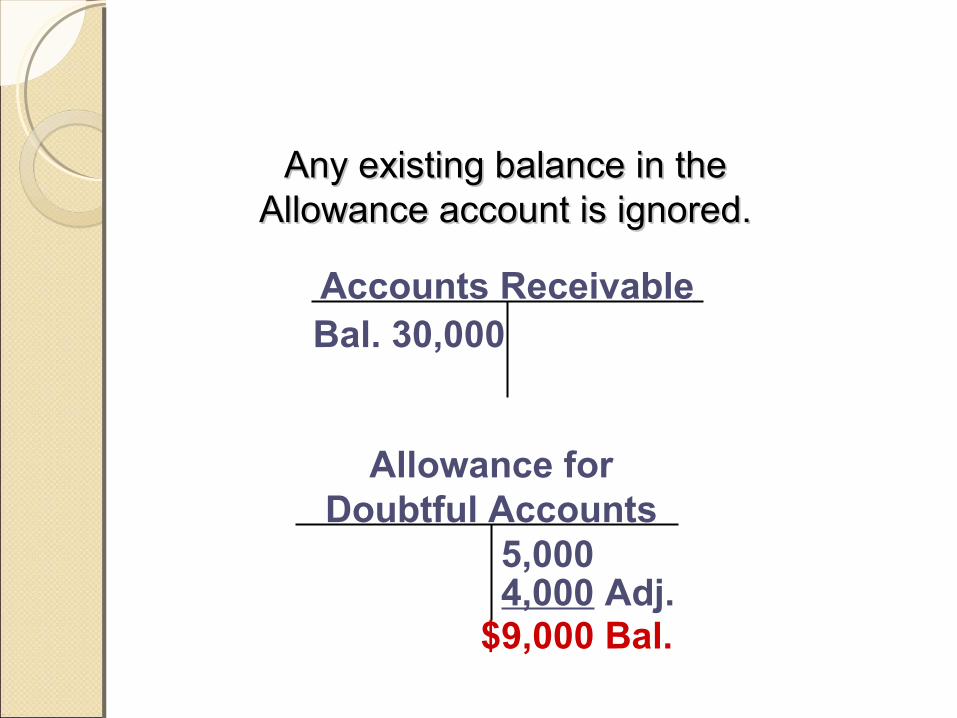

Accounts ReceivableBal. 30,000

Allowance forDoubtful Accounts

5,0004,000 Adj.

$9,000 Bal.

Any existing balance in theAny existing balance in theAllowance account is ignored.Allowance account is ignored.

Balance Sheet ApproachBalance Sheet Approach

Bad debts is based on the Accounts Receivable amount.

Balance Sheet ApproachBalance Sheet ApproachNet realizable value - The amount (accounts receivable

– Allowance for doubtful accounts) that is expected to be collected.

Focus is on determining the net realizable value of Accounts Receivable, which is reported on Balance Sheet

Thank you!

![Anil Kumar Jaiswal (MBA Dissertation/Project) - 2010 [Bad Debts Reduction in EBU Segment]](https://img.pdfslide.us/doc/110x75/5527bc65497959ec0f8b4ac8/anil-kumar-jaiswal-mba-dissertationproject-2010-bad-debts-reduction-in-ebu-segment.jpg)