Embed Size (px)

Citation preview

A MINOR PROJECT REPORT

ON

“A STUDY ON ADVERTISING STRATEGY ON MAX NEW YORK LIFE

INSURANCE COMPANY”

SUBMITTED IN THE PARTIAL FULFILLMENT FOR THE AWARD OF

THE DEGREE OF BACHELOR IN BUSINESS ADMINISTRATION

UNDER THE GUIDANCE OF:

Ms. Seema Wadhawan

SUBMITTED BY:

Aashiya Siddiqui

Enrollment No. – 05980301713

BBA, Semester – III

Batch 2013- 2016

RUKMINI DEVI INSTITUTE OF ADVANCED STUDIES

NAAC Accredited ‘A’ Grade

Category ‘A++’ Institute

High grading 81.7% by joint assessment

An ISO 9001:2008 Certified Institute

(Approved by AICTE, HRD Ministry, Govt. of India)

Affiliated to Guru Gobind Singh Indraprastha University, Delhi

2A & 2B, Madhuban Chowk, Outer Ring Road, Phase-1, Delhi-110085

Table of Content

S.No Particular Page No.

1 Chapter- 1

1.1 Advertising strategy

1.1.1 Developing the strategy

1.1.2 Insurance – introduction

1.2 Objective of the Study

1.3 Literature Review

2 Chapter-2

2.1 Company profile

2.2 History

3 Chapter-3

3.1 Research Methodology

3.1.1 research: meaning

3.1.2 Types of Research

4 Chapter-4

Data analysis & Interpretation

5 Chapter -5 findings & conclusion

5.1 Findings of the study

5.2 Conclusion

6 Chapter-6 Suggestions & Bibliography

6.1 Suggestions

6.2 Bibliography

7 Annexure

STUDENT DECLARATION

This is to certify that I have completed this project title “ADVERTISING STRATERGIES OF

MAX NEW YORK LIFE INSURANCE CO. LTD.” In partial fulfillment of the requirement for

the award of degree of bachelor of business administration at RUKMINI DEVI INSTITUTE OF

ADVANCED STUDIES; ROHINI.

I hereby certify that all the endeavor put in the task are genuine and original my knowledge and I

have not submitted it earlier elsewhere.

Signature

AASHIYA SIDDIQUI

BBA 2nd shift 3rd

CERTIFICATE

TO WHOM SO EVER IT MAY CONCERN

This is to certify that Aashiya Siddiqui has completed the project work “ADVERTISING

STRATEGY OF MAX NEW YORK LIFE INSURANCE CO. LTD .” Made by Bba(E),

05980301713 from Rukmini Devi Institute Of Advanced Studies affiliated to Guru Gobind Singh

Indraprastha university, Delhi under my guidance and his work is original.

PROJECT SUPERVISOR

SINGNATURE

Name: Ms. SEEMA WADHAWAN

ACKNOWLEDGEMENT

There is always a sense of gratitude which one express to other for the helpful so needy services

they render during all phases of life. I would like to express my gratitude towards all those who

have been helpful to me in getting this mighty task of training to a successful end. First of all, i

consider it a pleasant duty to express my heart felt appreciation, gratitude and indebtedness to

MS. SEEMA WADHAWAN (MY PROJECT GUIDE) for her keen interest, invaluable pain

taking & excellent guidance, patience, endurance, encouragement & thoughtful advice

throughout the project work duration. I would also like to be thankful to all my friends who gave

me constant & continuous inspiration to complete this project.

SIGNATURE

AASHIYA SIDDIQUI

BBA GENERAL

3RD SEMEMTER (05980301713)

EXECUTIVE SUMMARY

The Indian Insurance Industry is broadly segmented into public and privateinsurance companies.

Before year 2000, only public sector insurance companies were allowed to do business in India.

But after year 2000, insurance sector was thrown open for private insurance companies as well.

But as of now there now around 19 private life insurance companies and around 9 private

non-life insurance companies doing business in India.

This report is prepared with an aim to provide an overview of present India Insurance Industry.

Also with LIC, heading the public life insurance companies and Max New york life heading the

private life insurance players, this report also provides a comparative analysis of Life policies.

Based on this report, the prospecting insurance customers would get help in choosing the right

insurance products for themselves.

CHAPTER 1

PLAN OF THE STUDY

1.1ADVERTISING STRATEGY

Meaning

Advertising is a single component of the marketing process. It's the part that involves getting the

word out concerning your business, product, or the services you are offering. It involves the

process of developing strategies such as ad placement, frequency, etc. Advertising includes the

placement of an ad in such mediums as newspapers, direct mail, billboards, television, radio, and

of course the Internet. Advertising is the largest expense of most marketing plans, with public

relations following in a close second and market research not falling far behind.

The best way to distinguish between advertising and marketing is to think of marketing as a pie,

inside that pie you have slices of advertising, market research, media planning, public relations,

product pricing, distribution, customer support, sales strategy, and community involvement.

Advertising only equals one piece of the pie in the strategy. All of these elements must not only

work independently but they also must work together towards the bigger goal.

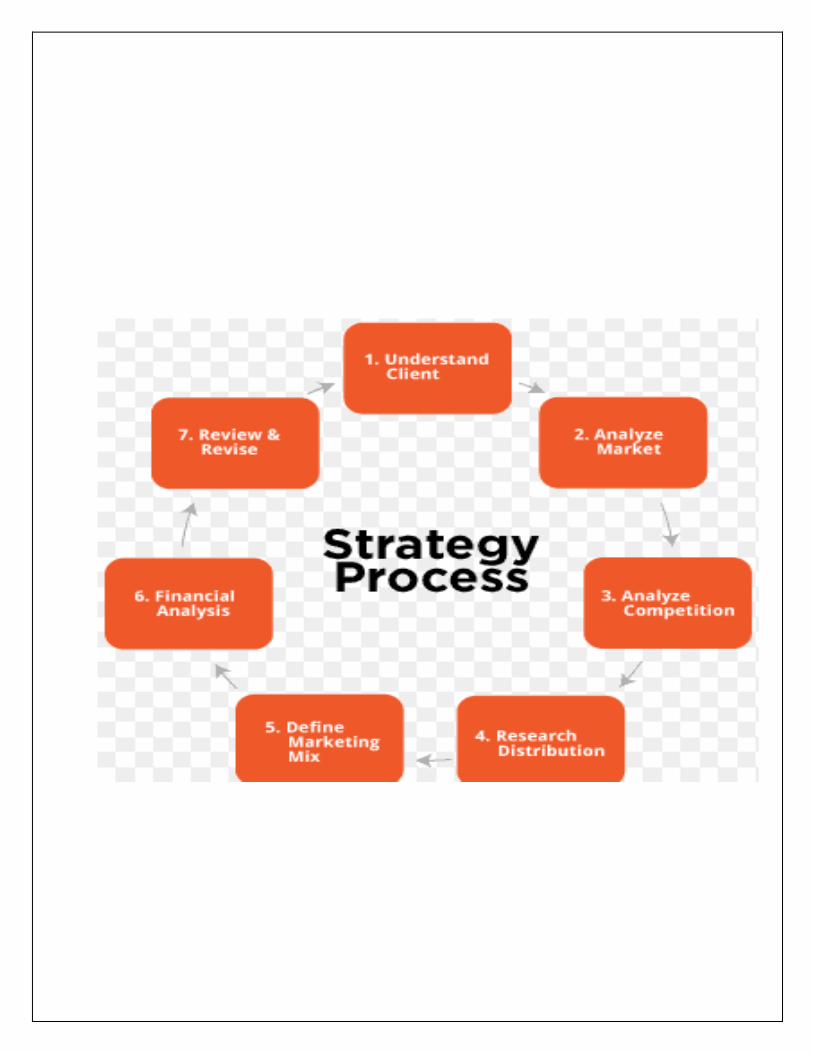

1.1.1 DEVELOPING THE STRATEGY

Positioning Statement

Formal advertising strategies are based on a "positioning statement," a technical term the meaning

of which, simply, is what the company's product or service is, how it is differentiated from

competing products and services, and by which means it will reach the customer. The positioning

statement covers the first two items in the listing above.

Implicit in a good positioning statement is what the industry calls the product concept, namely a

cluster of values that the product or service represents and the associational frameworks in which it

fits. A hunting knife will thus have a very different product concept than a pair of pink silk slippers

that glow in the dark. The product concept will later guide the choice of copy, images, and message

content to be used in actual ads (the "copy platform"). The positioning statement must also

implicitly include the profile of the targeted customer and the reasons why he or she would buy

this product or this service. At a later stage, more data on the "target consumer" is then developed

as the strategy is fleshed out.

Target Consumer

The target consumer is a complex combination of persons. First of all, it includes the person who

ultimately buys the product. Next it includes those who, in certain circumstances, decide what

product will be bought (but do not physically buy it). Finally, it includes those who influence

product purchases (children, spouse, and friends). In practice the small business owner, being close

to his or her customers, probably knows exactly how to advise the advertising agency on the target

consumer.

Communication Media

Once the product and its environment are understood and the target consumer has been specified,

the routes of reaching the consumer must be assessed—the media of communication. Five major

channels are available to the business owner:

Print—Primarily newspapers (both weekly and daily) and magazines.

Audio—FM and AM radio.

Video—Promotional videos, infomercials.

World Wide Web.

Direct mail.

Outdoor advertising—Billboards, advertisements on public transportation (cabs, buses).

Each of the channels available has its advantages, disadvantages, and cost patterns. A crucial stage

in developing the advertising strategy, therefore, is the fourth point made at the outset: how to

choose the optimum means, given budgetary constraints, to reach the largest number of target

consumers with the appropriately formulated message.

Implementation

The advertising campaign itself is distinct from the strategy, but the strategy is meant to guide

implementation. Therefore across-the-board consistency is highly desirable. Copy, artwork,

images, music—indeed all aspects of the campaign—should reflect the strategy throughout. This is

especially important when multiple channels are used: print, television, and direct mail, for

instance. To achieve a maximum coherence, many effective advertisers develop a unifying

thematic expressed as an image, a slogan, or a combination which is central to all the elements that

ultimately reach the consumer.

1.1.2 INSURANCE – AN INTRODUCTION

Insurance may be described as a social device to ensure protection of economic value of life and

other assets. under the plan of insurance, a large number of people associate themselves by

sharing risks attached to individuals. the risks, which can be insured against, include fire, the

perils of sea, death and accidents and burglary. any risk contingent upon these, may be insured

against at a premium commensurate with the risk involved. thus collective bearing of risk is

insurance. insurance is a contract whereby, in return for the payment of premium by the insured,

the insurers pay the financial losses suffered by the insured as a result of the occurrence of

unforeseen events. the term "risk" is used to describe the possibility of adverse results flowing

from any occurrence or the accidental happenings, which produce a monetary loss. insurance is

a pool in which a large number of people exposed to a similar risk make contributions to a

common fund out of which the losses suffered by the unfortunate few, due to accidental events,

are made good. the sharing of risk among large groups of people is the basis of insurance. the

losses of an individual are distributed over a group of individuals.

DEFINITIONS

General definition:

In the words of John Magee, “Insurance is a plan by themselves which large number of people

associate and transfer to the shoulders of all, risks that attach to individuals.”

Fundamental definition:

In the words of D.S. Hansell, “Insurance accumulated contributions of all parties participating in

the scheme.”

Contractual definition:

In the words of justice Tindal, “Insurance is a contract in which a sum of money is paid to the

assured as consideration of insurer’ incurring the risk of paying a large sum upon a given

contingency.”

CHARACTERISTICS OF INSURANCE

•Sharing of risks

•Cooperative device

•Evaluation of risk

•Payment on happening of a special event

•The amount of payment depends on the nature of losses incurred.

•The success of insurance business depends on the large number of people insured against

similar risk.

•Insurance is a plan, which spreads the risk and losses of few people among a large number of

people.

•The insurance is a plan in which the insured transfers his risk on the insurer.

•Insurance is a legal contract which is based upon certain principles of insurance which includes

utmost good faith, insurable interest, contribution, indemnity, causes proxima, subrogation, etc.

•The scope of insurance is much wider and extensive.

FUNCTIONS OF INSURANCE:

Primary functions:

1. Provide protection: Insurance cannot check the happening of the risk, but can provide for the losses of

risk.

2. Collective bearing of risk: - Insurance is a device to share the financial losses of few among many others.

3. Assessment of risk: - Insurance determines the probable volume of risk by evaluating various factors that

give rise to risk.

4. .Provide certainty: - Insurance is a device, which helps to change from uncertainty to certainty.

Secondary functions:

1. Prevention of losses: - Insurance cautions businessman and individuals to adopt suitable device to prevent

unfortunate consequences of risk by observing safety instructions.

2. Small capital to cover large risks: - Insurance relives the businessman from security investment, by paying

small amount of insurance against larger risks and uncertainty.

3. Contributes towards development of larger industries.

Other Function:

Means of savings and investment:

Insurance companies are business houses. The product they sell is financial protection. To succeed and survive,

they must cover their costs, which include payments to cover the losses of policyholders, as well as sales and

administrative expenses, taxes and dividends.

Insurance companies have two sources of income for covering these costs:

Premiums and investment income. The premiums are collected on a regular basis and invested in Government

Bonds, Gilt, stocks, mutual funds, real estates and other conservative avenues. However, investment income

depends on market conditions, interest rates, economy etc. and varies from year to year. Because of the uncertainty

associated with the investment income, insurance companies must generate enough income from premiums to

cover the bulk of their expenses.

The risk becomes insurable if the following requirements are complied with:

1. The insured must suffer financial loss if the risk operates.

2. The loss must be measurable in money,

3. The object of the insurance contract must be legal.

4. The insurer should have sufficient knowledge about the risks he accepts.

Fundamentals of Insurance

The fundamental Principles of the Insurance are as follows:

INSURABLE INTEREST:

Insurable interest means the legal right to insure. Insurable Interest is a must and only then the

insurance contract is enforceable at law. This principle differentiates a Contract of insurance

from wager. Lack of insurable interest renders the contract null and void. For Insurable Interest

to exist there must be Property, Rights, Interest, Life or Liability; this must be insured and the

Insured should have a legally recognizable relationship thereto. The Insured should be benefited

by the safety of the property or is prejudiced by its loss. Insurable Interest may arise in the

following manner:

Ownership:

Absolute ownership entitles the owner to insure the property. This is the commonest

method whereby Insurable Interest arises.

Partial Interest

I s a lso insurab le e . g. a mortgagee . A c red ito r cans a lso insure the life of his

debtor but only to the extent of his loan.

Administrators and executors

I.e. officials appointed by a court of law to take care of a property may also insure the

property

Relationship

Does not automatically constitute insurable interest. The only relationship recognized by

law for this purpose is the one between a husband and wife.

An employer

Can insure his employee under a Personal Accident Policy a she has insurable interest in them.

1. PROXIMATE CAUSE:

Generally, the claims are payable under insurance policies if they arise out of events which

are proximately caused by the insured perils. In other words, the proximate cause of the

event has to be peril covered by the policy, so as to constitute a valid claim.

2. Contribution:

An insured may have several insurance on the same subject matter. If he recovers his loss under

all these insurance, he will obviously make a profit out of loss. This will be an infringement of

the principle of indemnity. Common Law has, therefore, evolved the doctrine of contribution

whereby the insured is prevented from recovering more than his loss, despite his

having several insurance on the subject matter.

3. Subrogation:

The principle of indemnity seeks to prevent the insured from making profit out of loss. However,

it may so happen that that the insured may recover his loss under his policy and he may also have

rights against third parties. If, after the insurance claim is settled, the insured is allowed to

enforce is rights against third parties and to retain whatever damages he receives from them, he

will certainly make a profit and the principle of indemnity will be infringed. Common Law has

therefore, evolved the doctrine of subrogation as corollary to the principle of indemnity.

Subrogation may be defined as the transfer of rights and remedies of the insured to the insurers

who have indemnified the insured in respect of the loss. The Common Law right of subrogation

is implied an all contracts on indemnity, as it arises only after payment of loss.

4. Utmost Good Faith:

In all General Insurance contracts we know that a property or interest or liability or life is offered

for insurance and the insured as to take decisions on the acceptance of the proposal. If he decides

to accept the proposal a premium commensurate with the risk has to be charged. To enable him

to take necessary decision in this regard, the insurer must have certain facts about the risk

offered. These facts influence the judgment of the insurer in deciding about the acceptance or

otherwise of the risk and the rate of premium to be charged, if accepted. Such facts are known as

material facts.

NATURE OF INSURANCE CONTRACTS

When the insured pays the premium and the insurers accept the risks, the contract of insurance is

concluded. The policy issued by the insurers is the evidence of the contract. The contract of

insurance, like any other contract, for example a contract for the sale of goods, is subject to the

general law of contract as embodied in the Indian Contract Act, 1872.

According to this Act, a contract must have certain essential features in order to

Make it legally valid and enforceable. The following are the essential elements:

Offer and acceptance: Usually, the offer is made by the proposer, and acceptance made

by the insurer.

Consideration: This means that the contract must involve some mutual benefit to the

parties. The premium is the consideration from the insured and the promise to indemnity

is the consideration from the insurers.

Agreement between the parties: Both the parties should agree to the same thing in the

same sense.

Capacity of the parties: Both the parties to the contract must legally competent to enter

into the contract. For example, minors cannot enter into insurance contracts.

Legality: The object of the contract must be legal and the contract should not violate any

legal requirements. E.g. no insurance can be had for smuggled goods.

Risk Reasonable or not, risks are inescapable in business. Every business ventures is

something of a gamble, because the possibility of loss is as real as the prospects for

profits. And even though managers do everything possible to ensure that their business

succeeds, they cannot guard against every conceivable form of risk.

Pure Risk versus Speculative Risk

Pure Risk: Events representing the kind of risk that no business can predict or escape,

known as Pure Risk, it is the threat of a loss without the possibility of gain. In other

words, a disaster such as avalanche or fire is costly for the business it strikes, but the fact

that no disaster occurs contributes nothing to a firm's profit.

Speculative Risk: It is the type of risk that offers the prospect of making profit -and

prompts people to go into business in the first place. Every business accepts the

possibility of losing money in order to make money. Approaches to Risk Management

Risk Management is the process of reducing the threat of loss due to uncontrollable

events.

Steps in selecting a risk management approach:

Avoiding the Risk:

When a company avoids risk, it eliminates the possibility that a particular event will occur. To

avoid the possibility of a suit, for example, not to produce any products -which would, of course,

eliminate both the threats of lawsuit and the opportunity to profit. With rare exceptions, avoiding

risk entirely is extremely difficult.

Reducing the Risk:

A more practical approach is to reduce the risk by taking precautions. Risk reduction is an

important element in most companies' approach to risk management. Typical precautions include

putting safety locks on doors to prevent robberies, installing overhead sprinklers to minimize fire

damage, and periodic checking motor vehicles to prevent accidents.

Assuming risk:

Many companies draw on current revenues or set aside a "Contingency Fund" to cover

unexpected losses. Setting aside money on regular basis could be cheaper than purchasing

insurance. Moreover, the company can earn interest on the reserved cash. Such assumption of

risk is also called self-insurance or risk retention.

Transferring the risk:

Most companies still rely on outside insurance firms for financial protection against catastrophic

losses. In buying insurance, companies transfer the risk of loss to an insurance firm, which

agrees to pay for certain types of losses. In exchange, the insurance firm collects a fee known as

a premium.

INSURABLE AND NON-INSURABLE RISKS

Insurable risks:

An insurable risk - one that an insurable company will cover-Generally meets the following

requirements. The peril insured against must not be under the control of the Insured. This means,

of course that insurer do not pay for losses that are intentionally caused by an insured, caused at

the Insured's direction, or caused with the insured's collusion. For example, a fire insurance

policy excludes loss caused by the Insured’s own arson. It does, however, include loss caused by

an employee's arson. Losses must be calculable, and the cost of insuring must be economically

feasible. To operate profitably, insurance companies must have data on the frequency of losses

caused by a given peril. If this information covers a long period of time and is based on a large

number of cases, Insurance companies can usually predict quite accurately how many losses will

occur in the future. For example, the insurance companies to fix up the rate of premium of

Personal Accident Insurance may use the information of the number of people who will die each

year in India in accidents. The peril must be unlikely to affect all insured simultaneously. Unless

an insurance company spreads its coverage over large geographic areas or a broad population

base or different classes of Insurance, a single disaster might force it to pay out all its policies at

once. The possible loss must be financially serious to the Insured. An Insurance company could

not afford the paperwork involved in handling numerous small claims of a few Rupees each. As

a result, many policies have a clause specifying that the insurance company will pay only that

part of a loss greater than an amount - the deductible or excess-stated in the policy. The excess

represents small losses that the Insured has to absorb.

1.2OBJECTIVE

Advertising Is The Best Way To Communicate To The Customers.

Advertising Helps Informs The Customers About The Brands Available In The Market .

Advertising Is For Everybody Including Kids, Young And Old. It Is Done Using Various

Media Types, With Different Techniques And Methods Most Suited.

To Become one Of The Top Quartile Life Insurance Companies In India.

Be The Brand Of The First Choice. Be The Employes Of The Choice. Become Principal

Choice For Agent.

1.3Literature Review

The company was incorporated on 24th February, and the certificate of commencement of

business was obtained on 21st March. The company was engaged in the manufacture of Bi-

axially oriented polypropylene (BOPP) films. The company was promoted in joint sector by

Max India Ltd.,Ranbaxy Laboratories Ltd., Montari Industries Ltd. and Punjab State

Industrial Development Corporation Ltd.

- The Company undertook to set up a project for the manufacture of 2,000 tonne’s per annum of

BOPP film.

-Following amalgamation, the Company organised its business and designated them under four

groups as follows: Max Pharm, Max Electronics, Maxxon BOPP Films, Max Telecom.

- The Max-GB Ltd. is a 50:50 joint venture formed with Gist-Brocades International BV of the

Netherlands. It manufactures and markets

Penicillin based drug intermediates (6-APA and 7-ADCA) and bulk drugs (Ampicillin,

Amoxicillin and Cephalexin).

- The Company undertook to set up a state-of-the-art bulk drugs and Intermediates facility at a

50 acre green field site at Nanjangud near Mysore in Karnataka. The bulk drugs range would

include Anti-epileptic and anti-histaminic drugs.1989

- During January, the Company issued

14,50,000-12% secured convertible debentures of Rs100 each as follows: (i) 2,90,000 debentures

to the resident and non-resident shareholders of the promoter companies(all were taken up). (ii)

72,500 debentures to employees (only 4,950 debentures taken up). The remaining 10,87,500

debentures, along with

67,550 debentures not taken by employees, were offered to the public.

All were taken up.

- The erstwhile Max India Ltd., expanded into pharmaceutical formulation at an existing

manufacturing facility at Okhla, New Delhi.

- New products such as Maxmox, a formulation of Amoxycillin, Cefamax, a formulation of

Cephalexin, Floxip and an innovative product Rejoor Were introduced.

Max Life Insurance, one of the leading life insurers, is a joint venture between Max India Ltd.

and Mitsui Sumitomo Insurance Co. Ltd. Max India is a leading Indian multi-business corporate,

while Mitsui Sumitomo Insurance is a member of MS&AD Insurance Group, which is amongst

the top general insurers in the world. Max Life Insurance offers comprehensive life insurance

and retirement solutions for long-term savings and protection to more than thirty lakh customers.

It has a country-wide diversified distribution model including the country's leading agent

advisors, exclusive arrangement with Axis Bank and several other partners. Max Life Insurance

is a quality business focused on delivering excellence to customers through advice based sale

process, customer centric approach to business, financial stability & investment expertise and

strong human capital.

Max Life Insurance has positioned itself on the quality platform. In line with its vision to be the

most admired life insurance company by securing the financial future of its customers, has

developed a strong corporate governance model based on the core values of caring, credibility,

collaborative and excellence.

Max Life Insurance offers comprehensive life insurance and retirement solutions for long-term

savings and protection to over thirty two lakh customers. It has a country-wide diversified

distribution model including the country's leading agent advisors, exclusive arrangement with

Axis Bank and several other partners. Max Life Insurance is a quality business focused on

delivering excellence to customers through advice based sale process, customer centric approach

to business, financial stability & investment expertise and strong human capital.

In the financial year 2013-14 Max Life Insurance ranked fourth among private life insurers with

a market share of 10.3%. The Company has been one of the fastest growing life insurance

companies with Gross Written Premium of Rs.7, 279 crore and Shareholders Profit after Tax of

Rs.43 crore for the Financial Year 2013-14. The Company's share capital of Rs.2,127 crore with

a solvency margin of 485% is indicative of its financial strength and stability. As on 31st March

2014,

Max Life Insurance had assets under management of Rs.24, 716 crore.

Max Life Insurance has a diversified distribution network spread across more than 750 cities.

The distribution is based on three pillars – agency distribution, banc assurance and partnership

distribution. Agency distribution forms its core distribution channels with advice based sales

process through its well trained and knowledgeable agent advisors. These agent advisors are

equipped to engage with prospective customers and offer customized solutions for their life stage

needs.

In banc assurance, the Company has a strong relationship with Axis Bank which in a short span

has become the largest non-captive banc assurance relationship in India with its network of over

2000 branches providing life insurance solutions to its customers. Partnership Distribution, the

third pillar of Max Life Insurance's distribution model is equally important and successful with

long standing relationship with large distributors of financial products such as Assure and

Peerless. These three key distribution channels are complemented by Group Insurance and

Customer Advocacy teams.

Max Life Insurance offers a comprehensive suite of Long Term Savings and Protection oriented

products. It currently has 12 products covering and 3 riders that can be customized to suit every

life stage need of the customer. Besides this, the company offers 3 products and 1 rider in group

insurance business.

CHAPTER 2

COMPANY PROFILE

2.1 COMPANY PROFILE

Max New York Life Insurance Company Limited is a joint venture between Max India Limited,

which is a one of India's leading multi-business corporate, and New York Life International,

which is a Fortune 100 company & global expert in life insurance. Max New York Life

Insurance started its commercial operations in India in 2001. It is the first life insurance company

in India to be awarded the IS0 9001:2000 certification. The company has around 133 offices all

over.

Max New York Life offers a variety of flexible products covering both life and health insurance

including 8 riders that can be customized to over 800 combinations which enable the customers

to choose the policy that suits their needs. Max New York Life also offers 6 products and 7

riders in group insurance business. The company has a plan for every need, designed as to meet

your long term financial goals & aspirations. They help you fulfilling your dreams &

commitments. The list of few plans provided by Max New York Life Insurance Company

Limited is given below:

Max India Limited (MIL) a multi-business corporate was incorporated in 24th February of the

year 1988. Focused on Knowledge, People and Service oriented of Healthcare (Max Healthcare),

Life Insurance (Max New York Life Insurance), Clinical Research (Neeman Medical

International) and also Max maintains interests in Specialty Plastic Products for the packaging

industry (Max Speciality Products) and Healthcare Staffing (Max HealthStaff). Max had

expanded its presents into pharmaceutical formulation at an existing manufacturing facility at

Okhla, New Delhi in the year 1994. Also in the same year, new products such as Maxmox, a

formulation of Amoxycillin, Cefamax, a formulation of Cephalexin, Floxip and an innovative

product Rejoor were introduced. In the year1992, a joint venture company was set up in

collaboration with Hutchison Telecom under the name of Hutchison Max Telecom Pvt. Ltd to

offer value added telecom services. MIL had entered into memorandum of understanding with

Comsat Corporation USA for a joint venture to address the needs of VSAT communication

services via satellite. Maxxon India, promoted by MIL, was merged with the company in the

year 1993. During the year 1994, an innovative new product for leather industry was introduced

under the name of Maxfoil and also in the same year the company commissioned the cellular,

paging and VSAT Satellite Communication networks. The joint venture between Max-GB Ltd.

and Hindustan Antibiotics Ltd for manufacture of Penicillin G was inaugurated at Pimpri on 8th

October of the year 1995. Forays were made into the banking and financial sectors and also into

distribution and manufacturing sectors. In March of the year 1996, a joint venture was formed

with Atotech BV of the Netherlands for PCB plating and general metal finishing chemicals. A

range of Upjohn products manufactured under licence in a new sterile facility were launched. In

April of the same year, the unit commissioned at its films metallising plant and launched its

metallised BOPP films branded Maxmet'. Max Corporation, a wholly owned subsidiary of the

Company has been amalgamated with the company in the year 1999. MCL stood dissolved

without winding up, and all assets and liabilities of MCL were transferred and vested with the

Company effective from 14th January of the year 2000. During the year 2000, the company had

acquired a majority interest in HealthScribe India Pvt. Ltd. a 100 per cent Indian subsidiary of

HealthScribe Inc., one of the World's leading medical transcription companies. MIL sold its 24

per cent stake in the 50:50 penicillin-based bulk pharmaceutical joint venture of Max GB to its

foreign partner, the Dutch DSM, for Rs. 26 crores. In the year 2001, Max healthcare, a division

of Max India Ltd., has opened two primary (Dr Max) and a secondary (Max Medcentre)

healthcare centres in New Delhi. During the identical year of 2001, the company entered into

insurance business, Max New York Life the joint venture between Max India and New York

Life. Max India became the first private player to shows interest in Health Insurance sector

during the year 2002 and also in the year, the company sold its pharmaceutical division to

Jubilant Organosys for the consideration of Rs. 62.7 crs. During 2002-03, the company had

entered into the healthcare staffing resources business through a 50% investment in a new

Company, Max HealthStaff International Ltd. During the year 2003, Max India closed down the

Max Ateev and Alta Cast, the software development and IT enabled business taking a big hit of

Rs.65 crs. During 2004-05, the company divested its equity stake in Comsat Max in favour of

Bharti Infotel Ltd, for a cash deal of Rs.33 crores. During 2005, the company decided to

amalgamate its wholly owned subsidiaries namely, Max Telecom Ventures Ltd and Max Asia-

Pacific Ltd Honkong with the company. In June of the year 2005, the company acquired

19,72,500 equity shares of Max HealthStaff for a consideration of Rs.2.51 Crores, thereby

making it a wholly owned subsidiary of the company. Max Super Speciality Hospital (MSSH)

was commenced its operations in May of the year 2006. Neeman Medical International (NMI)

had established preferred provider relationship with 5 Pharma major in the year 2006-07. Max

Speciality Products (MSP) commissioned a new state-of-the-art-speed BOPP film production

line with a capacity of 20000 tonnes per annum in March of the year 2007. The Company to

invests Rs 10 billion additionally in Max New York Life, the board decided in September of the

year 2007. The Company bagged an Express Healthcare Excellence Awards for the year 2007-

08. Max made a Joint venture with BUPA Finance Plc., UK (world leader of highest pedigree in

this space) in the year 2008.

Max Life Insurance Company Limited provides life insurance products in India. The company

offers a range of participating, non-participating, and linked products covering life insurance,

pension, and health benefits. The company provides individual and group life insurance products

consisting of protection, child, retirement, growth, savings, health, and group plans Max Life

Insurance Company Limited distributes its products primarily through individual agents,

corporate agents, banks, and brokers. The company was formerly known as Max New York Life

Insurance Company Limited and changed its name to Max Life Insurance Company Limited in

July 2012. The company was incorporated in 2000 and is based in New Delhi, India. Max New

York Life Insurance Company Limited is a subsidiary of Max India Limited.

Max Life Insurance Company Limited has pulled out of the bid to acquire Aviva Life Insurance

Company India Pvt. Ltd. A source close to the development told Financial Chronicle that the two

private life insurance players, HDFC Standard Life Insurance Co., Ltd. and Birla Sun Life

Insurance Company Limited, have entered a non-binding agreement with Aviva plc (LSE:AV.) a

few weeks back. “We did not see value in the deal,” said a source in Max Life Insurance.

According to a person close to the development, Aviva Life is looking at a valuation of INR 50

billion, while its embedded value is estimated to be around INR 18 billion. “Aviva has a good

back-book and a strong franchise in the south besides a robust distribution strength comprising

agency, online and corporate relationship tie-ups. But they are asking for too much,” said an

official with one of the bidders. A mail sent to Aviva Life director Mohit Burman, who

represents Dabur, did not elicit any response. Top officials of Aviva Life, HDFC Life and Birla

Sun Life refused to comment.

2.2 HISTORY:

The company was founded in 1845 as the Nautilus Insurance Company in New York City, with

assets of just $17,000. It was renamed the New York Life Insurance Company in 1849. Its first

headquarters were at 112-114 Broadway; the first president was James DePeyster Ogden. The

current New York Life headquarters was designed by architectCass Gilbert and completed in

1928. The New York Life Building, at 51 Madison Avenue, was constructed during the

presidency of Darwin P. Kingsley. As with other early insurance companies in the U.S., in its

early years the company insured the lives of slaves for their owners. In response to bills passed

in California in 2001 and in Illinoisin 2003, the company reported that Nautilus sold 485

slaveholder life insurance policies during a two-year period in the 1840s; they added that their

trustees voted to end the sale of such policies 15 years before the Emancipation Proclamation.[3]

In 1860, before state laws required it, New York Life developed the non-forfeiture option, the

predecessor to the guaranteed cash values of modern policies, under which a policy remains in

force even if a premium payment is missed. It was also the first American life insurance

company to pay a cash dividend to policyholders, and the first U.S. company to issue policies to

women at the same rates as men. Susan B. Anthonywas one of their first female policy holders,

and her father worked for NYLIC.[4] In 1896, New York Life became the first company to insure

people with disabilities and the first to issue a policy with a disability benefit that presumes total

disability to be permanent after a predetermined period.

In the late 1990s New York Life was one of several large mutual life insurers to back a bill that

would allow demutualizationinto a structure known as a mutual holding company (MHC).

CEO Sy Sternberg himself argued strongly in favor of the bill,[5]which was ultimately defeated.

The NYLIC board of directors subsequently reversed course, with the company strongly and

publicly embracing their mutual nature in a series of advertisements.

Financial crisis of early 21st Century

According to their Report to Policyholders 2007, in early 2007 the company's managers became

concerned about the state of credit markets, so in February 2007 "based on our belief that the

markets were acting irrationally" New York Life decided to move much of its cash flow into

safer investments such as US Treasury bonds. "By August 2007, the credit market problems we

had feared were front page news," the Report notes.

In November 2008, the company announced it will not participate in the Troubled Asset Relief

Program. "The company can meet all of its strategic objectives without government capital, its

businesses are strong and profitable, and it is committed to remaining a mutual company

operating for the sole benefit of its policyholders," states a company press release.[6]

Theodore "Ted" Mathas, president and CEO in 2008, said at the time of the financial crisis that

New York Life is "built for times like these." This phrase became the title for the 2008 report to

policyholders. Ted Mathas becomes the company chairman on June 1, 2009.[7]

New York Life maintains "superior" financial ratings from A.M.

Best, Fitch, Moody's and Standard and Poor's, all of which have reaffirmed the ratings during the

financial crisis of autumn 2008.

Max Life Insurance Co. Ltd.

Max Life Insurance, one of the leading life insurers, is a joint venture between Max India Ltd.

and Mitsui Sumitomo Insurance Co. Ltd. Max India is a leading Indian multi-business corporate,

while Mitsui Sumitomo Insurance is a member of MS&AD Insurance Group, which is amongst

the top general insurers in the world. Max Life Insurance offers comprehensive life insurance

and retirement solutions for long-term savings and protection to more than thirty lakh customers.

It has a country-wide diversified distribution model including the country's leading agent

advisors, exclusive arrangement with Axis Bank and several other partners. Max Life Insurance

is a quality business focused on delivering excellence to customers through advice based sale

process, customer centric approach to business, financial stability & investment expertise and

strong human capital.

Max Life Insurance has positioned itself on the quality platform. In line with its vision to be the

most admired life insurance company by securing the financial future of its customers, has

developed a strong corporate governance model based on the core values of caring, credibility,

collaborative and excellence.

Max Life Insurance offers comprehensive life insurance and retirement solutions for long-term

savings and protection to over thirty two lakh customers. It has a country-wide diversified

distribution model including the country's leading agent advisors, exclusive arrangement with

Axis Bank and several other partners. Max Life Insurance is a quality business focused on

delivering excellence to customers through advice based sale process, customer centric approach

to business, financial stability & investment expertise and strong human capital.

In the financial year 2013-14 Max Life Insurance ranked fourth among private life insurers with

a market share of 10.3%. The Company has been one of the fastest growing life insurance

companies with Gross Written Premium of Rs. 7,279 crore and Shareholders Profit After Tax

of Rs. 436 crore for the Financial Year 2013-14. The Company's share capital of Rs. 2,127 crore

with a solvency margin of 485% is indicative of its financial strength and stability. As on 31st

March 2014, Max Life Insurance had assets under management of Rs. 24,716 crore.

Max Life Insurance has a diversified distribution network spread across more than 750 cities.

The distribution is based on three pillars – agency distribution, bancassurance and partnership

distribution. Agency distribution forms its core distribution channels with advice based sales

process through its well trained and knowledgeable agent advisors. These agent advisors are

equipped to engage with prospective customers and offer customized solutions for their life stage

needs.

In bancassurance, the Company has a strong relationship with Axis Bank which in a short span

has become the largest non-captive bancassurance relationship in India with its network of over

2000 branches providing life insurance solutions to its customers. Partnership Distribution, the

third pillar of Max Life Insurance's distribution model is equally important and successful with

long standing relationship with large distributors of financial products such as Amsure and

Peerless. These three key distribution channels are compelmented by Group Insurance and

Customer Advocacy teams.

Max Life Insurance offers a comprehensive suite of Long Term Savings and Protection oriented

products. It currently has 12 products covering and 3 riders that can be customized to suit every

life stage need of the customer. Besides this, the company offers 3 products and 1 rider in group

insurance business.

At Max Life Insurance, providing a superior customer experience is central to its vision and the

Company is committed to provide superior service experience to the customer. As a proactive

step towards service excellence, Max Life Insurance has launched the "Treating Customer

Fairly" (TCF) policy. The TCF policy aims to raise standards in the way the Company interacts

with customers at every touch point right from the pre-sales engagement to the payment of

benefits.

Max Life Insurance follows a prudent investment philosophy to optimize risk management in its

bid to provide maximize returns to policyholders. Investments are in instruments which are safe

and provide good returns in the long run.

The company values human capital and considers it to be its competitive advantage. Max Life

Insurance believes that people are its biggest organizational assets and hence lays a strong

emphasis on employee friendly practices leading to high levels of employee engagement and

motivation. This is reflected in the recognition that the company received from the Great Places

To Work Institute, India, as one of the best workplaces in the industry.

Max Life insurance works closely with Max India Foundation, an independent social service

organization of the Max India Group for all its CSR activities. The company has taken up

immunization programme as a societal agenda to ensure protection against major ailments for the

next generation of the country. The programme covers vaccines like BCG, Hepatitis B vaccine,

Polio drops, DPT, D Tap, Measles vaccine, MMR, Typhoid, dT and TT.

Max Life Insurance has always believed in setting new benchmarks in quality of service and

product offerings to its stakeholders and its efforts have been duly recognized over the years.

Some of the awards and accolades won by Max Life Insurance in the recent year are as follows:

Recognized as a 'Superbrand of the Year' 2013-14

Ranked 8th amongst the Most Trusted Life Insurance companies in Brand Equity (The

Economic Times) survey

Golden Mikes 2014, the most coveted Indian Radio awards, for Max Life Insurance i-

genius

Amongst the top 100 'Great Place to Work'- 3rd year in a row

Awarded 'Celent Model Insurer Asia - Distribution Agent Channel' for New Work

System

'BIG Data & Business Analytics Award' for Business Analytics and Performance

Management Leadership

Project Unnati recognized at the ASQ World Conference 2013

CHAPTER 3

RESEARCH METHOLOGY

3.1RESEARCH METHODOLOGY

3.1.1 RESEARCH: meaning and concept

Research refers to any original and systematic investigation undertaken in order to increase

knowledge and to establish facts and principles. It is an organized and systematic activity and

may lead to new and improved insights, development of new products and processes. Thus

research is an µorganized and µsystematic way of finding answers to questions or finding

solutions to problems. Research is said to be systematic because, it involves the following of

definite set of steps in order to arrive at some conclusion.

Also it is said to be organized, as it is a planned procedure which is focused and having a well

defined scope, i.e. it has a structure and method. Research is aimed at finding answers ± maybe

to simple questions or for some hypothesis. It is said to be successful when answers are found.

Lastly, questions constitute the main component of research because if there is no question, then,

it follows that there can be no research. This is so, since the dynamics of research invariably

involves the process of focusing on relevant, useful and important questions. The questions for

the same may originate from management dilemma.

Fact-finding enquiries of different kinds. The major purpose of descriptive research is

description of the state of an affair, as it exists at present. Research methodology refers to the

tools and methods used for obtaining information for the purpose of the subject under

study. The methodology followed for the purpose of finding customers response will be

Random sample survey.

3.1.2 Types of Research

1. Descriptive

It includes surveys and fact finding enquires. Main aim is to describe the state of affair as

it is exists at present. The researchers have no control over variable. They can report what

has happened or what is happening. It is also known as Ex Post Facto.

2. Analytical

In this research, researcher has to use facts or information already available and analyzed

it to make a critical evaluation.

3. Applied

Aims at finding a solution for immediate problem faced. It applies theories and models

already developed to the actual solution of the problem.

Aim is not to develop theories but to test the theories in actual situation.

4. Fundamental

It is a formal and systematic process which aims to develop theories or model.

All important variables are identified in fundamental research. It involves selecting

appropriate sample so that generalization can be done.

5. Quantitative

It is based on the measurement of quantity or amount. It can be applied to these concepts

which can be expressed in terms of quantity.

6. Qualitative

It is concerned with the qualitative aspects.

7. Conceptual

It is related to some abstract ideas or theories. Generally used by philosophers or thinkers

to develop new concepts.

3.2 DATA COLLECTION

Data base helps your team to assess the health of your process. To do so, you

must identify the key quality characteristics you will measure, how you will measure them, and

what you will do with the data you collect.

Data base is nothing more than planning for and obtaining useful information on key quality

characteristics produced by your process. However, simply collecting data does not ensure that

you will obtain relevant or specific enough data to tell you what is occurring in the process.

3.2.1Primary data

Primary research consists of a collection of original primary data collected by the

researcher. It is often undertaken after the researcher has gained some insight into the

issue by reviewing secondary research or by analyzing previously collected primary

data.[clarification needed] It can be accomplished through various methods, including

questionnaires and telephone interviews in market research, or experiments and direct

observations in the physical sciences, amongst others.

3.2.2Secondary data

Secondary source of information was internet and various other articles in magazines, pamphlets

etc.These was some of the sources through which up-to-date and relevant data was collected. It is

one of the best methods to collect data because of economy in terms of time and money. The tool

used for data collection in this project is SECONDARY DATA:

The secondary data tools used in the project are books and internet. I refused to various articles

and data on internet. The founding’s of other people were also used to achieve appropriate data.

The secondary data thus collected helped to get refined and reliable data.This Project report is

made on the basis of secondary data.

3.3TOOLS ANALYSIS

Observation and descriptive survey methods used to collect the data about the features,

expectations, satisfaction, problems etc. the customers.

3.4SAMPLING DESIGN

Data was collected through questionnaires

Sample Size :- 100

Sample Area :- New Delhi

Sample Method :- Random sampling method

A survey was conducted in which 100 people were asked to fill the questionnaire. I will be using

statistical method for sample size determination.

CHAPTER 4

DATA ANALYSIS

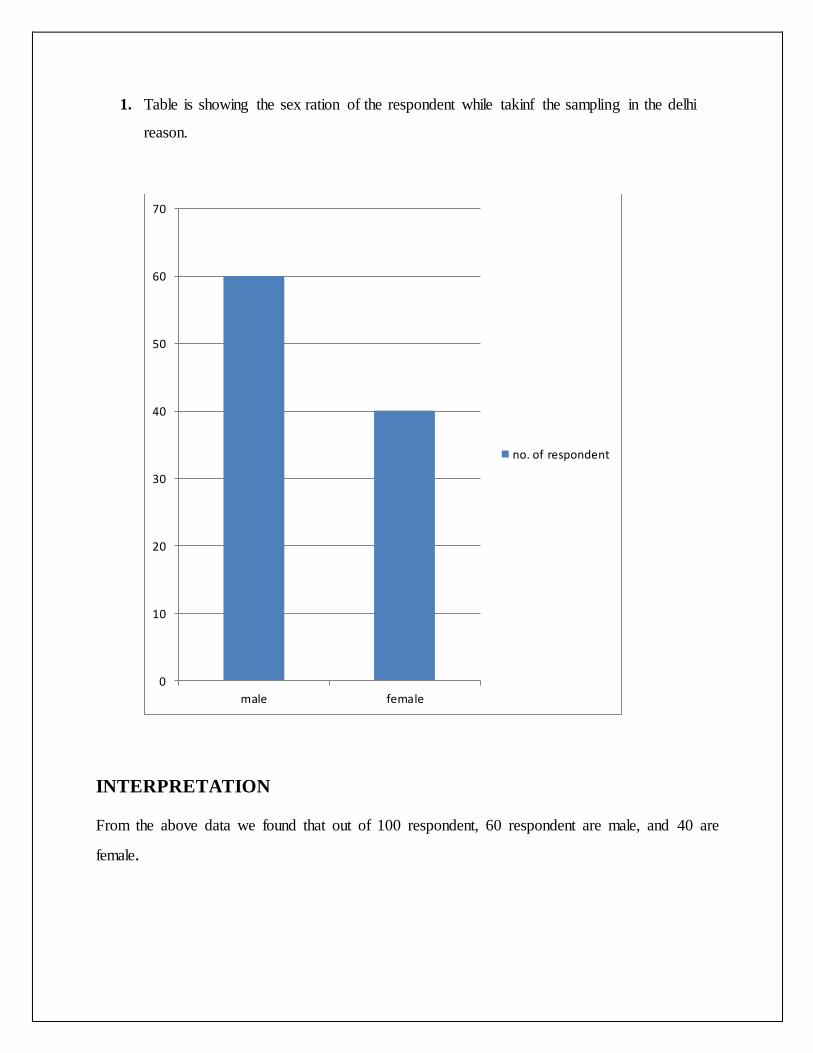

1. Table is showing the sex ration of the respondent while takinf the sampling in the delhi

reason.

INTERPRETATION

From the above data we found that out of 100 respondent, 60 respondent are male, and 40 are

female.

0

10

20

30

40

50

60

70

male female

no. of respondent

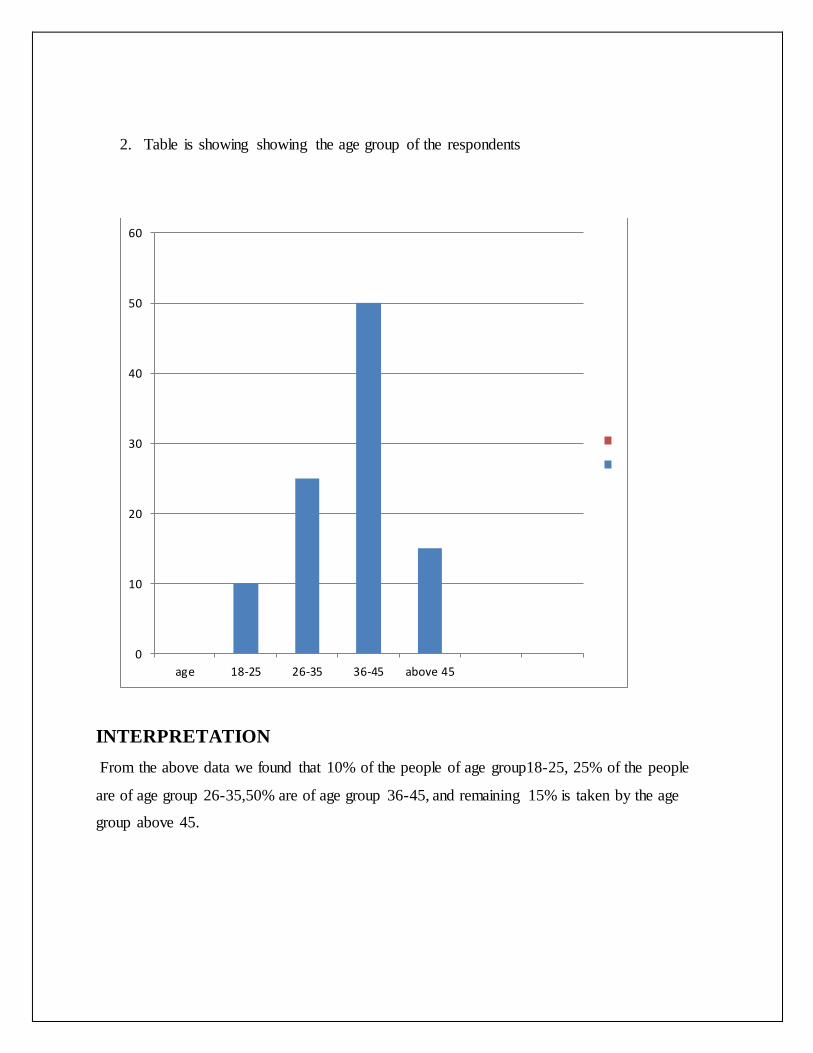

2. Table is showing showing the age group of the respondents

INTERPRETATION

From the above data we found that 10% of the people of age group18-25, 25% of the people

are of age group 26-35,50% are of age group 36-45, and remaining 15% is taken by the age

group above 45.

0

10

20

30

40

50

60

age 18-25 26-35 36-45 above 45

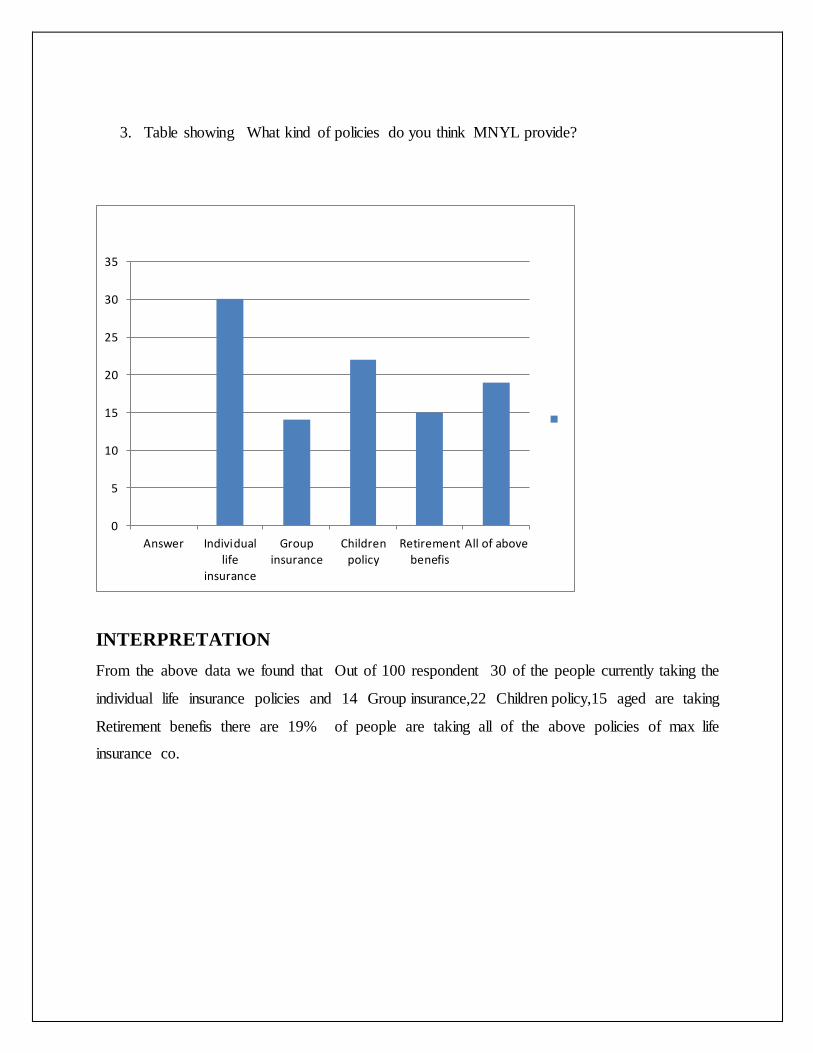

3. Table showing What kind of policies do you think MNYL provide?

INTERPRETATION

From the above data we found that Out of 100 respondent 30 of the people currently taking the

individual life insurance policies and 14 Group insurance,22 Children policy,15 aged are taking

Retirement benefis there are 19% of people are taking all of the above policies of max life

insurance co.

0

5

10

15

20

25

30

35

Answer Individual

life

insurance

Group

insuranceChildren

policyRetirement

benefisAll of above

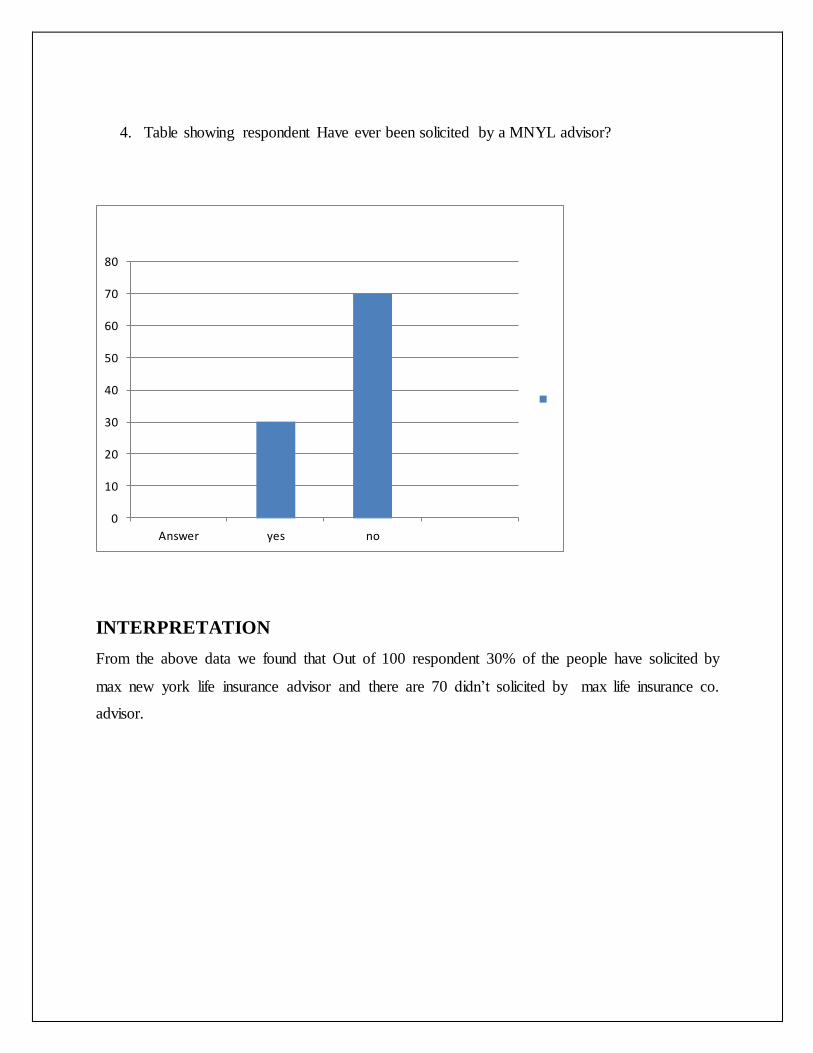

4. Table showing respondent Have ever been solicited by a MNYL advisor?

INTERPRETATION

From the above data we found that Out of 100 respondent 30% of the people have solicited by

max new york life insurance advisor and there are 70 didn’t solicited by max life insurance co.

advisor.

0

10

20

30

40

50

60

70

80

Answer yes no

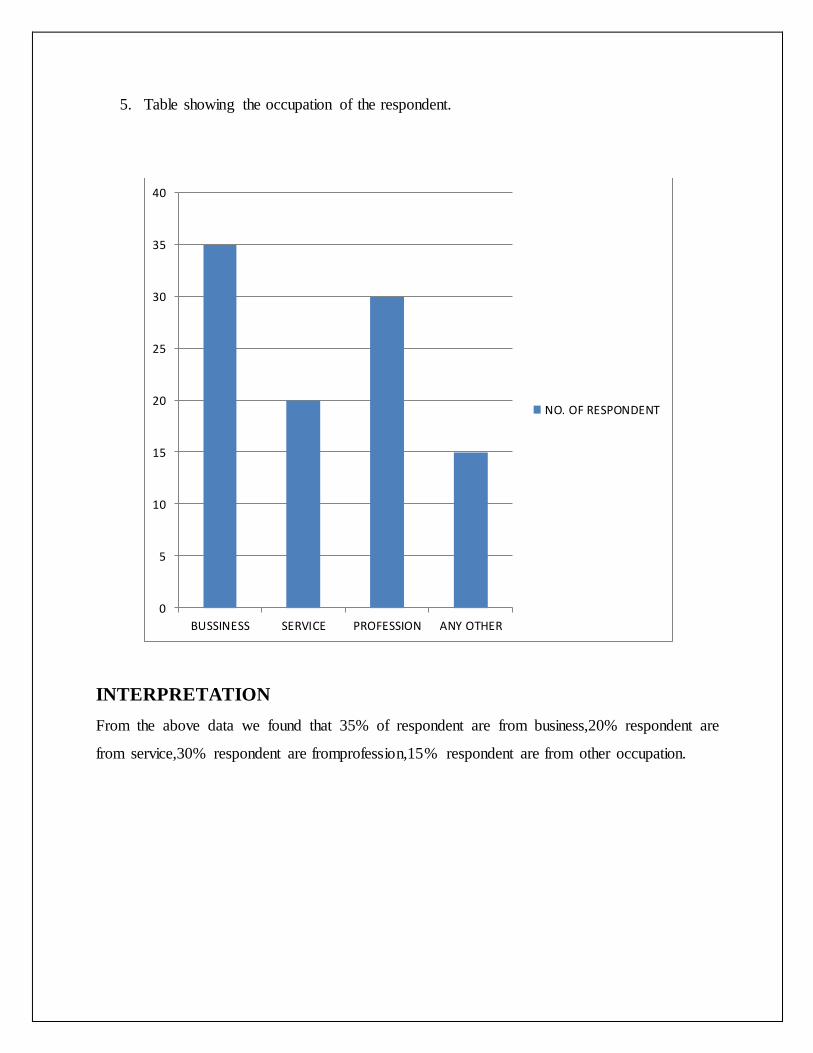

5. Table showing the occupation of the respondent.

INTERPRETATION

From the above data we found that 35% of respondent are from business,20% respondent are

from service,30% respondent are fromprofession,15% respondent are from other occupation.

0

5

10

15

20

25

30

35

40

BUSSINESS SERVICE PROFESSION ANY OTHER

NO. OF RESPONDENT

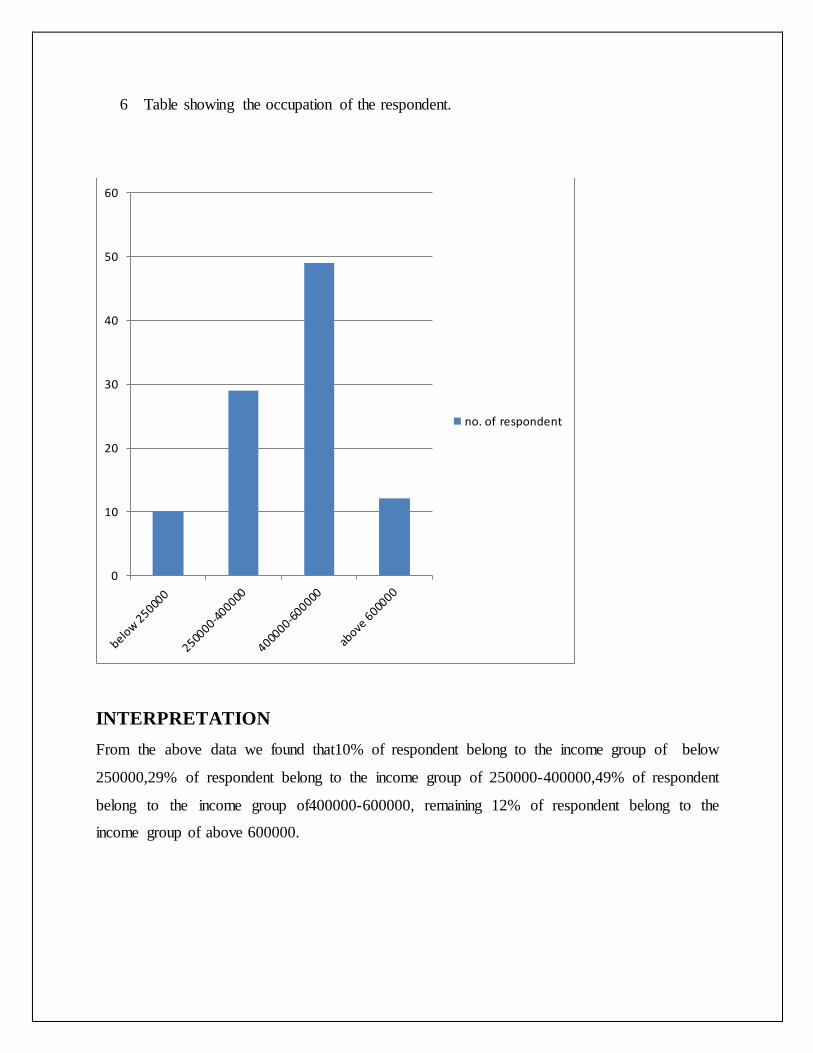

6 Table showing the occupation of the respondent.

INTERPRETATION

From the above data we found that10% of respondent belong to the income group of below

250000,29% of respondent belong to the income group of 250000-400000,49% of respondent

belong to the income group of400000-600000, remaining 12% of respondent belong to the

income group of above 600000.

0

10

20

30

40

50

60

no. of respondent

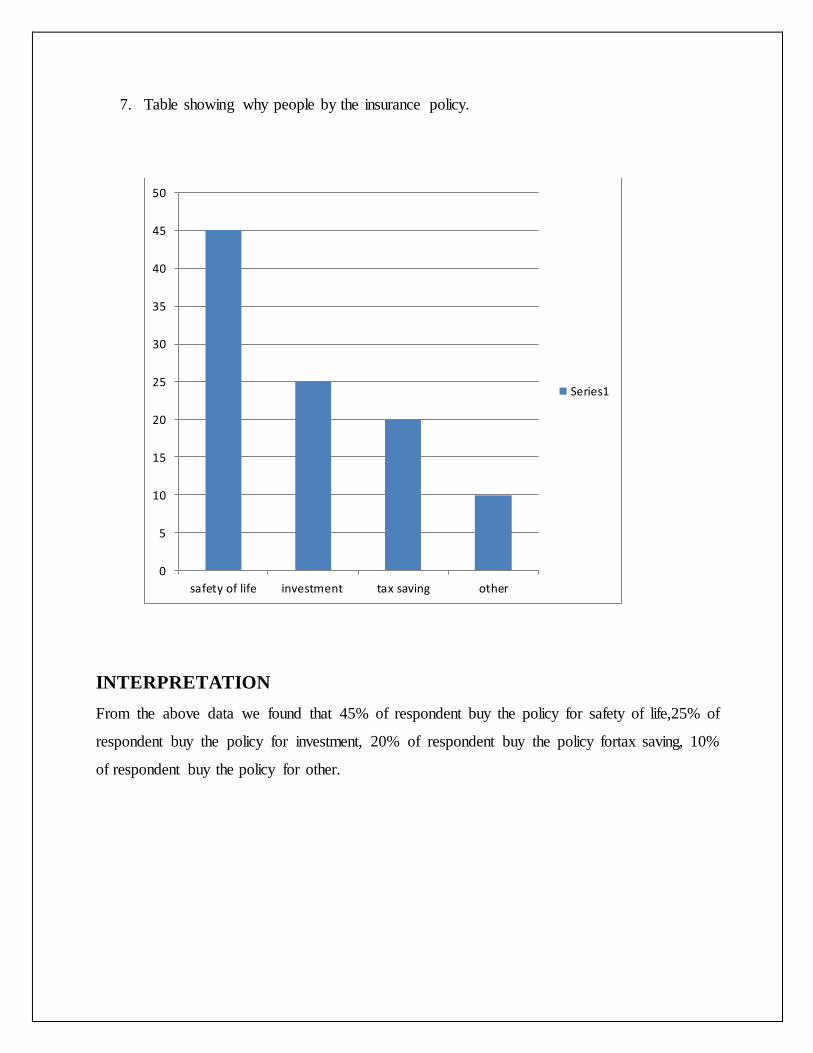

7. Table showing why people by the insurance policy.

INTERPRETATION

From the above data we found that 45% of respondent buy the policy for safety of life,25% of

respondent buy the policy for investment, 20% of respondent buy the policy fortax saving, 10%

of respondent buy the policy for other.

0

5

10

15

20

25

30

35

40

45

50

safety of life investment tax saving other

Series1

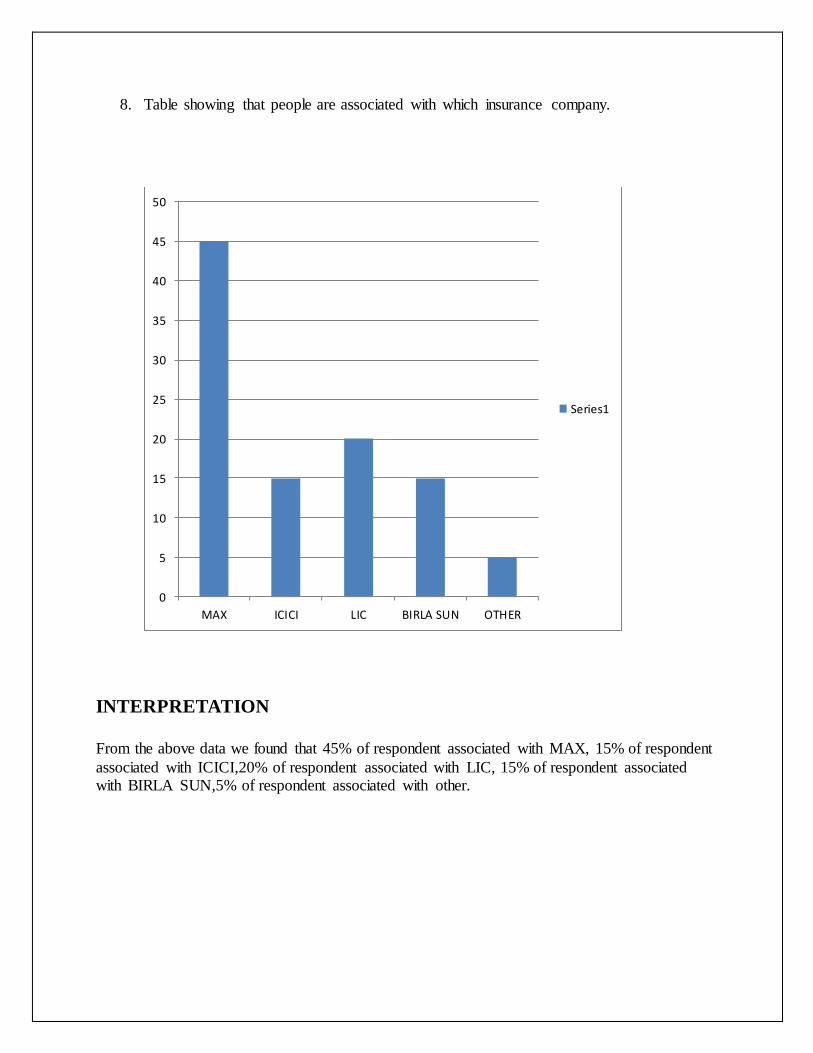

8. Table showing that people are associated with which insurance company.

INTERPRETATION

From the above data we found that 45% of respondent associated with MAX, 15% of respondent

associated with ICICI,20% of respondent associated with LIC, 15% of respondent associated with BIRLA SUN,5% of respondent associated with other.

0

5

10

15

20

25

30

35

40

45

50

MAX ICICI LIC BIRLA SUN OTHER

Series1

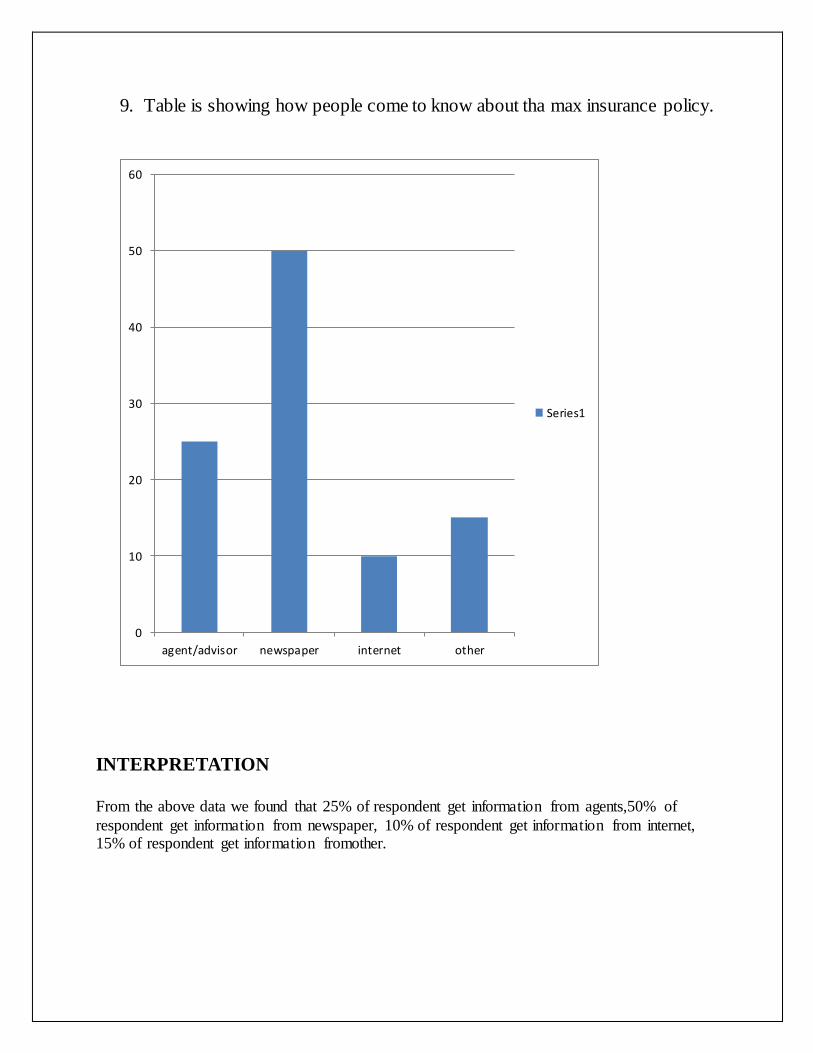

9. Table is showing how people come to know about tha max insurance policy.

INTERPRETATION

From the above data we found that 25% of respondent get information from agents,50% of

respondent get information from newspaper, 10% of respondent get information from internet, 15% of respondent get information fromother.

0

10

20

30

40

50

60

agent/advisor newspaper internet other

Series1

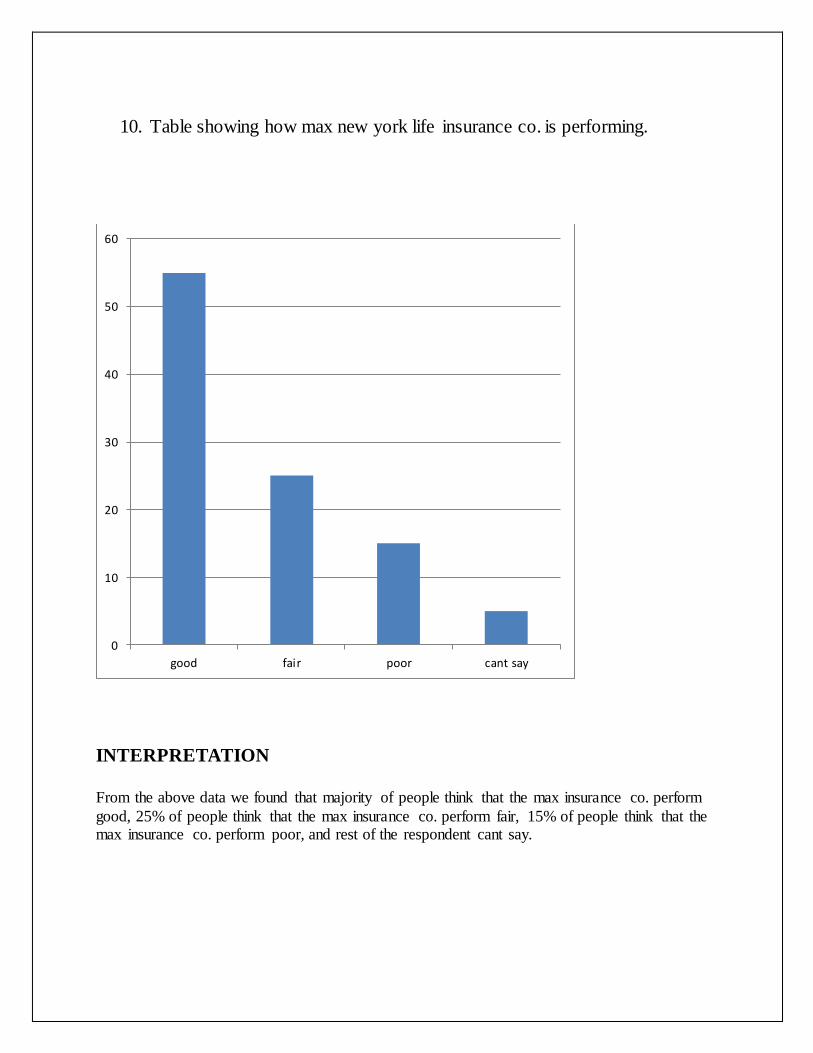

10. Table showing how max new york life insurance co. is performing.

INTERPRETATION

From the above data we found that majority of people think that the max insurance co. perform

good, 25% of people think that the max insurance co. perform fair, 15% of people think that the max insurance co. perform poor, and rest of the respondent cant say.

0

10

20

30

40

50

60

good fair poor cant say

CHAPTER 5

FINDING AND

CONCLUSION

5.1 FINDING OF THE STUDY

From the questionnaire it was found out that mainly people take policy of MNYL insurance co.

and most of them visited for solicited by a MNYL advisor.

The general awareness about the policy is very good and people like to coming here

as they find that MNYL better as compared to other insurances company.

Few years back MNYL is not common among the customer. But now alomost people

take MYNL policy.

Mostly the consumers are satisfied with the services provided by the MNYL.

Maximum numbers of consumer are loyal to there particular service providers and

they were using there policies since 1 to2 years.

5.2 CONCLUSION

MAX NEW YORK LIFE ENTERS “THE GUINNESS BOOK OFWORLD RECORDS”

Creates world record for the world’s largest umbrella Our exhaustive research in the field of Life

Insurance threw up some interesting trends, which can be seen in the above analysis. A general

impression that we gathered during Data collection was the immense awareness and knowledge

among people about various companies and their insurance products. People are beginning to look

beyond LIC for their insurance needs and are willing to trust private players with their hard earned

money. People in general have been impressed by the marketing and advertising campaigns of

insurance companies. A high penetration of print, radio and Television Ad campaigns over the

years is beginning to have its impact now .Another heartening trend was in terms of people

viewing insurance as a tax saving and investment instruments as much as a protective one. A very

high number of respondents have opted for insurance for such purposes and it shows how

insurance companies have been successful to attract public money in recent times. The general

satisfaction levels among public with regards to policy and agents still requires improvement. But

therein lies the opportunity for are native player like Max New York Life. LIC has never been

known for prompt service or customer oriented methods and Max New York Life can build on

these factors.

CHAPTER – 6

SUGGESTIONS/

RECOMMENDATIONS

6.1 SUGGESTION

1. As the people think that insurance is a tool to protect their family & a tax saving device. They

areaware of the fact & realizing its, importance. There is a large potential for insurance in India.

2. The entrance of private players will increase the competition and it would be a tough task to

securea good position in market.

3. Since Max New York Life Insurance is leading with several companies’ policies it should be

easyfor them to penetrate into the market and secure a good position if they pay

greater attention to theservice part provided to their customer and thereby forming a long and

trusted relationship.

4. As seen from the survey that at present 70% of the customer are having insurance

policy out of which 87.5% of the customer are planning for new investments. So it can be a

good potential for thecompany and they should make an attempt to trap these customers.

5. As 43% of the customers are even ready to go for insurance if a service provider away from

their city is providing it. But inturn they should provide good products and services. The

company shouldtry to convince these customers and get them in its favor.

6.2 BIBLIOGRAPHY

WEBSITE REFFERED

www.Max newyorklife.com

www.indraindia.com

www.hindubusinessline.com

QUESTIONNAIRE

Table is showing the sex ration of the respondent while taking the sampling in the Delhi region

NAME

:_________________________

ADDRESS

:______________________ ______________________________

OCCUPATION:

___________________

1. The Sex Ration Of The Respondent While Taking The Sampling In The Delhi region.

Male

Female

2. The Age Group Of The Respondents.

18-25

26-35

36-45

Above 45

3. What Kind Of Policies Do You Think

Individual Life Insurance

Group Insurance

Children Policy

Retirement Benefit

All Of The Above

4. Respondent Have Ever Been Solicited By A MNYL Advisor?

Yes

No

5. The Occupation Of The Respondent.

Business

Service

Profession

Any Other

6. The Occupation Of The Respondent.

Below 250000

250000-400000

400000-600000

Above 600000

7. Why People By The Insurance Policy.

Safety For Life

Investment

Tax Saving

Other

9. People Are Associated With Which Insurance Company.

MAXC

ICICI

LIC

BIRLA SUN

OTHER

10. How Max New York Life Insurance Co. Is Performing.

GOOD

FAIR

POOR

CANT SAY