Embed Size (px)

Citation preview

CREDIT RISK ANALYSISCASE STUDY

Get Homework/Assignment Done Homeworkping.comHomework Help https://www.homeworkping.com/

Research Paper helphttps://www.homeworkping.com/

Online Tutoringhttps://www.homeworkping.com/

click here for freelancing tutoring sites

ORION INDUSTRIES

CASE HISTORYIntroduction

This case study is a multi-part exercise that illustrates various elements of the credit process. Your study of the Orion case begins with issues pertaining to target marketing and qualitative analysis. As the case develops, you will be introduced to the entire gamut of the credit process, including additional data gathering activities, further qualitative analysis, financial analysis, credit structuring, approval, administration, and account management.

In the first part of the case, you will be introduced to the potential customer and the bank, the need that brings them together, and important background information regarding the country’s macroeconomic scenario and the customer’s operations.

The second part of the case, also in this unit, takes you on a plant visit where you will gather additional qualitative information.

Subsequent parts of the case, covered in Units Three, Four, and Five deal with financial (quantitative) analysis and then credit structuring, approval, documentation, and administration.

Now begin Part One of the case study and then complete the exercises that follow.

i

CREDIT RISK ANALYSISCASE STUDY

Part 1

First Customer-Banker Meeting

Leo Aries, a senior account executive with the Libra Bank, located in the Pegasus region of Andromeda, was catching up on paperwork. His secretary advised him that a Mr. Scorpio from Orion Industries was in the office and wished to speak with him about possible financing.

Aries was surprised because a screening process within the unit’s target market definition first identified most potential customers, and there was very little walk-in business. Also, he knew most of the companies in the region but had only vaguely heard of Orion. Nevertheless, he instructed the secretary to show Mr. Scorpio into one of the conference rooms.

Mr. Bruno Scorpio, the general manger of Orion and in his early forties, introduced himself. “Your friend George Virgo from the Running Club gave me your name as a reference. We just had lunch nearby, so I look the liberty of dropping in.” On two previous occasions, Virgo had recommended that people talk with Aries, mostly for financial advice. Both times Aries had quickly determined over the phone that the potential customers did not fit into the unit’s target market definition.

Aries was interested in developing business with medium to large industrial enterprises that had good growth potential. He actually preferred the smaller companies within this range, firms, which could grow along with the bank but were not first tier enterprises that could demand premium pricing and a lot of favors.

Economic/Political Background

Andromeda is a medium sized, quiet, democratic country with a population of about 29 million people. Historically, the economy had been based on agriculture, but a significant industrial infrastructure has developed in the past 15 years. This development was part of an economic plan for employment generation and business sector diversification. As a result of an economic slowdown in the early and mid 1980s, the country’s economic development in recent years has been directed more towards the export sector, particularly those exports that provide a high product integration percentage (value added content). There is significant potential for maximizing the yield of exports due to the country’s considerable deposits of basic raw materials.

The gross domestic product (GDP) of Andromeda is about US$ 62 billion resulting from positive but modest levels of growth during the early and mid 1980s. More recently, GDP growth rates have been in the range of 4% to 5%, and one of the more dynamic sectors of the economy has been manufacturing, with growth in the 6% to 7% range over the past two years.

ii

CREDIT RISK ANALYSISCASE STUDY

Monetary and fiscal policy in Andromeda has been fairly stable. Relatively small deficits in government expenditures have been financed internally, but these deficits and the recent rapid growth in several economic sectors have resulted in moderate but persistent annual inflation in the 15% to 18% range.

The monetary unit of Andromeda is the Lcy, currently valued at Lcy 40/1 US$. During the past three years the Lcy has devalued at the rate of about 10% to 12% per year, which is consistent with the inflation differential between Andromeda and the hard currency countries with which it trades.Libra Bank and the Pegasus RegionAndromeda has 24 commercial banks and several specialized agrarian and development banks. The commercial banks are permitted nationwide banking, although only the top six banks maintain a truly national presence. A second tier of eight regional banks maintains an influential position in important but geographically limited regions of the country.

Libra Bank is one of these regional banks, located in the Pegasus region about 300 km from the capital. Pegasus has traditionally been an agricultural region, but in recent years has sustained considerable growth in the industrial sector. This region is home to a major automobile manufacturing and assembly operation established eight years ago by a well-known multinational auto producer. This car plant has spawned numerous parts manufacturers that supply the assembly plant, many of which are partially owned or affiliated with foreign car parts makers.

Libra Bank is a full service bank with about Lcy 10 billion in assets. It has contributed to the industrial growth of the region by financing several major manufacturing projects and by offering extensive short term financing facilities and other traditional banking services. The industrial sector represents about 40% of the Libra loan portfolio as a result of marketing efforts in the last several years to capture major segments of this sector around Pegasus.

Orion Industries and Mr. Bruno Scorpio

“Mr. Aries, thank you for seeing me on such short notice. Please let me tell you about Orion Industries. We are medium sized metal works with annual sales of about Lcy 250 million. We have been in business for 24 years in Perseus (bout 60 km away), manufacturing different types of high precision metal products. During the past few years we have produced a variety of products. Our main product has been axle and transmission assemblies for tractors, working as a subcontractor to Andromeda Tractor Works. More recently we have been producing universal assemblies and rear axles for the Pegasus Automobile Plant. This is just the beginning of our involvement with the car sector, which we believe has a very high potential within the country.”

Scorpio explained the company’s history. Two brothers who immigrated to Andromeda thirty years ago started Orion. The Taurus brothers, excellent craftsmen and honest entrepreneurs, successfully managed the firm for many years. Eventually, the scope of

iii

CREDIT RISK ANALYSISCASE STUDY

operations became more than a large family business could handle and profits started to slip. Even though they took on extra business, training more people and purchasing more equipment, profits stayed at the same level as when they were half the size.

Three years ago, the Taurus brothers were introduced to Scorpio. He had a degree in mechanical engineering from a good university (the University of Andromeda) and had spent many years working with a large Andromeda company in the metal products sector. Over the years he had built up expertise in administration, especially in the area of cost control for manufacturing operations. He saw a good opportunity at Orion because of the high-quality products and the business potential in the nearby Pegasus region. Scorpio invested some of the personal savings in Orion and became the general manager and one-third shareholder, with an option to purchase a majority position.

The two brothers, now in their late fifties, are still active in the company on the production side. Scorpio has streamlined operations by eliminating some marginal products with small profit margins and emphasizing the tractor subcontracting work and the diversification into the auto sector. Orion has been delivering for three months under its contract with the Pegasus Automobile Plant, achieving good quality and a strong on-time production record.

Financing Request

“The reason for my visit, Mr. Aries, is that we are looking for new banking relationship. Currently, we are working mostly with the local branch of the Gemini Bank and they provide adequate services for payrolls and a limited amount of lending. However, they do not have the expertise or resources to deal with our projected future needs. We are looking for a long-term relationship with a large regional full service bank such as yours. Our mutual friend, George Virgo, mentioned your name and your bank, so here I am.

“We would like to establish a short-term facility for Lcy 40 million (equivalent to US$ 1,000,000). We would want periodic drawdowns for working capital purposes, mostly to help us finance receivables or to stock up on raw materials for particular jobs. Although I have made every effort to even out the workflow at the plant, some degree of seasonality is unavoidable. The credit line will help us here.

“We anticipate future capital needs for upgrading or relocating the plant, but that’s still a long way off. We would, however, like to establish financial relationships now so that when these futures needs arrive, we can count on the necessary financing. We have a couple of other prospective banks, but have come here first because of your bank’s reputation for thoroughness and imaginative financing.”

Invitation to Visit“We would like to invite you for a visit to our factory, at your earliest convenience, so that you can meet our people and judge Orion Industries for yourself. Our external

iv

CREDIT RISK ANALYSISCASE STUDY

auditor, the well-known firm of Capricorn & Centauri, will have our annual report finished in about two weeks and I will instruct them to send it to you as soon as it is ready. I would prefer to have you visit us before then so we can get the ball rolling as soon as possible. We anticipate some short term financing needs in about six to eight weeks, and if your bank is not interested, we would have to pursue other avenues.”

Aries and Scorpio said good-bye. “An interesting meeting,” thought Aries, “he seems to know what he’s talking about.” Aries liked Scorpio for his easy, open, and unpretentious manner.

Aries wasn’t sure what to make of this customer falling into his lap, but thought that pursing the opportunity would be worthwhile. All he had to lose at this point was a little time, and, in any event, it would be interesting to visit the customer’s factory. That way he could identify the qualitative parameters of a potential banking arrangement to decide whether or not to continue with a complete risk analysis.

The banker had to organize the information he gained from the initial interview with the potential client and decides what information he should get during his visit to the plant.

ORION INDUSTRIES – Part 2Introduction

In Part One of the Orion case we were introduced to the banker, the potential customer, and the economic setting of the case. We saw that although the bank did not have a precise definition of its target market, the potential customer apparently fit within the broad parameters established by the bank, and within the country’s macroeconomic situation.

Aries was intrigued enough to see a prospective deal, and schedule a plant visit. Through the questions in the Progress Check you saw how he should organize his data and plan what he would accomplish during his upcoming plant visit.

In Part Two of the Orion case, Aries displays resourcefulness in obtaining some valuable references. He then proceeds with the plant visit where he gathers a great deal of qualitative information. He tries to organize the information using the bank’s standard qualitative data forms.

Apparently satisfied that Orion Industries still represents potential business for the bank, Aries starts to think about the next two steps in the credit process. These include (1) the financial analysis of the Orion statements when they arrive, and (2) the formal credit and risk analysis to structure a deal and frame a potential credit recommendation.CheckingsBefore driving out to the Orion factory, Aries decided to call Aurora Borealis, a banker at Gemini Bank whom he had met in a credit course they both attended last year. Aurora confirmed that her bank had been dealing with Orion for many years, and the relationship was generally positive. Some credits had been renegotiated over the years,

v

CREDIT RISK ANALYSISCASE STUDY

but this was normal for a company like Orion that was continually taking on different jobs.

Aurora mentioned that Gemini Bank wished to maintain its relationship with Orion by continuing to offer current account and payroll services – and by maintaining its exposure levels at about the present level. But due to Gemini’s small size, it was already near the legal lending limit and could not meet all of Orion’s lending need. Another bank would have to finance Orion’s proposed growth.

Aries also contacted Libra Bank’s own account officer for the Andromeda Tractor Works (ATW) and asked him to track down information on Orion’s reputation for quality and timely delivery of the axle and transmission assemblies. After a couple of phone calls, the ATW account officer advised that the tractor producer was happy with the Orion relationship. The quality of work was excellent and reliability of delivery had improved considerably over the past year. Apparently, Orion had experienced some difficulties in the past that resulted in late deliveries, but this problem had now been solved.

Libra Bank did not have a banking relationship with the Pegasus Auto Plant since the auto producer dealt only with four top-tier Andromeda banks. Nevertheless, Aries wanted to get some feedback from the auto producer as to Orion’s product quality and reliability. Aries assumed that the reference would be a good one, but he wanted to make sure. He decided to leave this matter for later.Visit to the Orion FactoryPlant and EquipmentA few days later, Leo Aries drove to Perseus to visit the Orion plant. He found that the concrete block plant building was old but in fairly good condition, owned by the company, and free of liens. It was located in an old area that had good access to the highway connecting it to the heart of the Pegasus region. However, the location was slightly off the beaten track and far from the newer industrial areas that had developed near the Pegasus Automobile Plant. Electricity and water supplies in the area were adequate.

Inside, the plant was clean and well lighted, but quite crowded with numerous large machines. The machines though not new, appeared to be well maintained and were logically positioned to handle the workflows. They were all imported and looked expensive. Aries was informed that some of the machines collateralized existing long-term debt with the Gemini Bank and other long-term sources, but outstandings were low compared to the replacement market value of the machines. The machines were insured at their present market value, which was net of depreciation.

There were several warehouse areas within the building for storing raw materials, but these areas were randomly placed due to the cramped conditions inside the plant where every inch of space was utilized. Controls over inventories appeared to be adequate with locked wire mesh compartments.

vi

CREDIT RISK ANALYSISCASE STUDY

The administrative area was quite austere, with old furniture, wooden floors, and old photographs on the wall. There was no formality here; the administrative staff was friendly and comfortably dressed (no ties), and odors from the kitchen could be detected throughout the offices. Aries was informed that the company subsidized the workers’ lunches, with the workers paying only a normal price.

SAlmost all of Orion’s raw materials were sourced domestically from the few Andromedan steel mills and foundries (Andromeda Steel Works, Andromeda Mining and Metals), and the quality of these products was good. Purchase terms for Orion were the standard 30 to 60 days. A few specialized products such as drill bits and other tools were imported due to the inferior quality of local products. These purchases were relatively minor and were made on a cash basis using foreign exchange bought on the free market.

Regarding inventory levels, Scorpio figured he would have to maintain present levels of between three and four months. “I wish our production schedule was more consistent from month to month, but we must adapt to our buyers and, unfortunately, this means some fluctuation in production volumes. We have to keep greater stocks of raw material on hand to enable production flexibility. Over the next year, however, we hope to reduce our average inventory to between two and three months.

“I’m sure you will have more questions on the financial side once you get our figures,” continued Scorpio. “You’ll see that, financially speaking, we have improved the quality of our income stream by eliminating some unprofitable operations and focusing on our more lucrative product lines. You should have the numbers next week so you can see for yourself.”

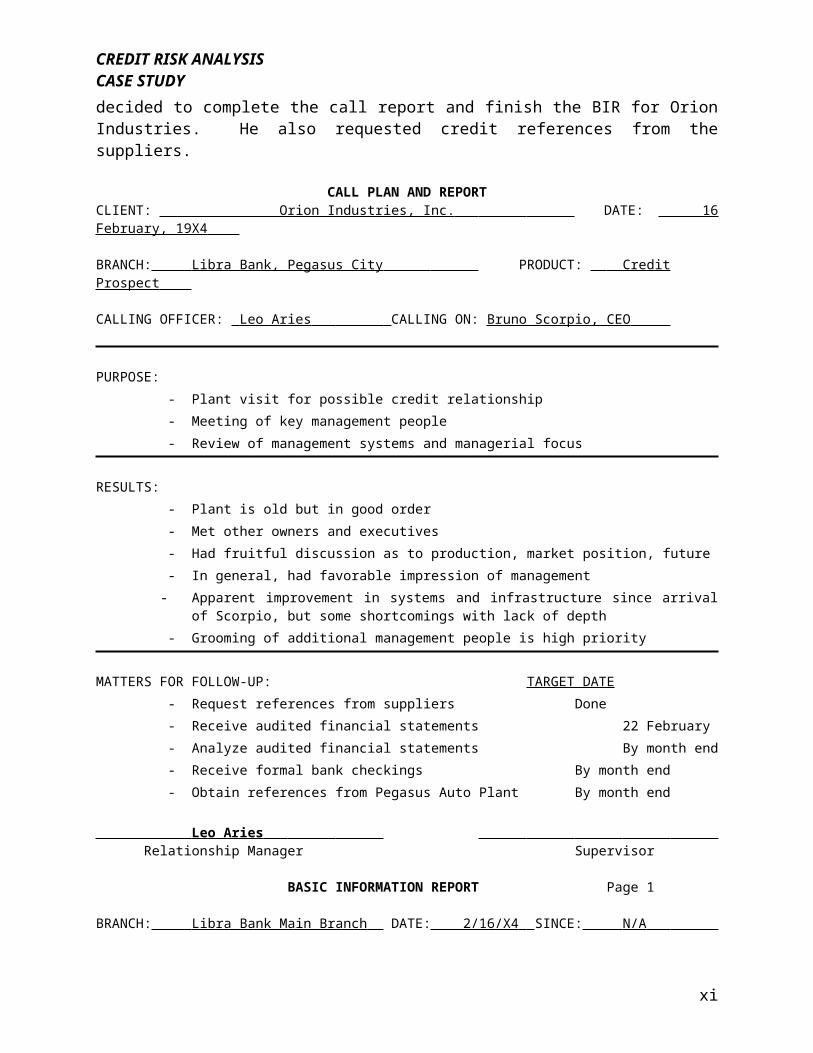

Aries returned to the bank to consider what he had learned about Orion Industries. “An interesting opportunity,” he thought. So far he had a positive feeling for the potential relationship and for Scorpio. Aries admired entrepreneurs who were willing to invest their own capital in an enterprise. Apparently, Scorpio had been successful at turning a relatively unsophisticated operation into a more modern and efficient company with prospects for considerable growth. “On the other, perhaps Scorpio was being too ambitious,” mused Aries. “But he has demonstrated drive and determination which, let’s face it, most people never attain.”Call ReportAries was anxious to get the financial statements to complement his analysis so far and provide a more comprehensive perspective of the situation. He figured that the numbers, once available, would reflect an improving picture over the last couple of years. In the meantime, and while the visit was fresh in his mind, Aries decided to complete the call report and finish the BIR for Orion Industries. He also requested credit references from the suppliers.

CALL PLAN AND REPORTCLIENT: Orion Industries, Inc. DATE: 16 February, 19X4

BRANCH: Libra Bank, Pegasus City PRODUCT: Credit Prospect

CALLING OFFICER: Leo Aries CALLING ON: Bruno Scorpio, CEO

PURPOSE:

vii

CREDIT RISK ANALYSISCASE STUDY

- Plant visit for possible credit relationship- Meeting of key management people- Review of management systems and managerial focus

RESULTS:- Plant is old but in good order- Met other owners and executives- Had fruitful discussion as to production, market position, future - In general, had favorable impression of management

- Apparent improvement in systems and infrastructure since arrival of Scorpio, but some shortcomings with lack of depth

- Grooming of additional management people is high priority

MATTERS FOR FOLLOW-UP: TARGET DATE- Request references from suppliers Done- Receive audited financial statements 22 February- Analyze audited financial statements By month end- Receive formal bank checkings By month end- Obtain references from Pegasus Auto Plant By month end

Leo Aries Relationship Manager Supervisor

BASIC INFORMATION REPORT Page 1

BRANCH: Libra Bank Main Branch DATE: 2/16/X4 SINCE: N/A

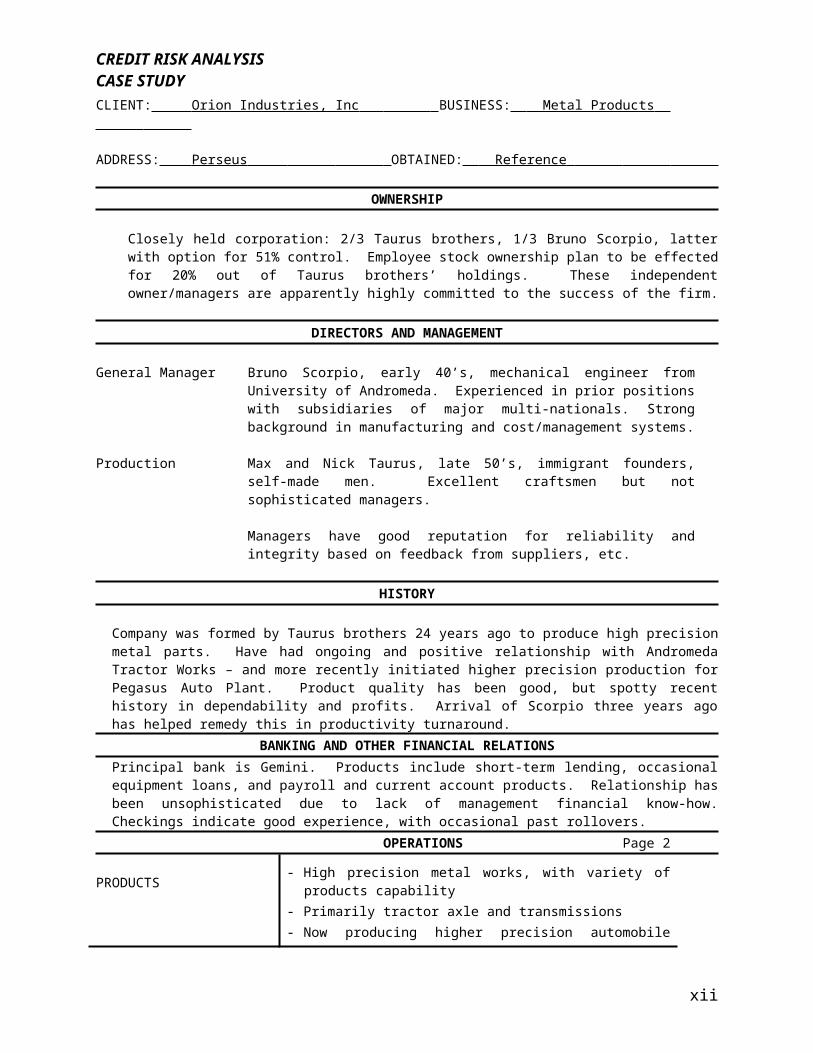

CLIENT: Orion Industries, Inc BUSINESS: Metal Products

ADDRESS: Perseus OBTAINED: Reference

OWNERSHIP

Closely held corporation: 2/3 Taurus brothers, 1/3 Bruno Scorpio, latter with option for 51% control. Employee stock ownership plan to be effected for 20% out of Taurus brothers’ holdings. These independent owner/managers are apparently highly committed to the success of the firm.

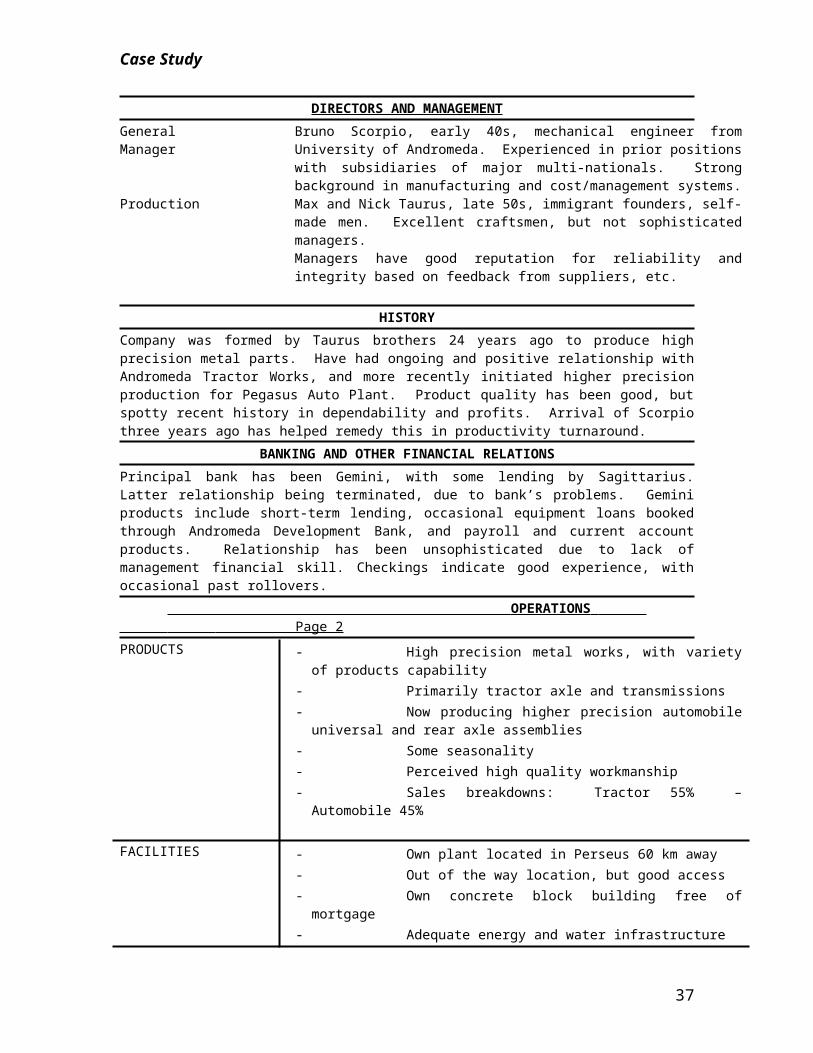

DIRECTORS AND MANAGEMENT

General Manager Bruno Scorpio, early 40’s, mechanical engineer from University of Andromeda. Experienced in prior positions with subsidiaries of major multi-nationals. Strong background in manufacturing and cost/management systems.

Production Max and Nick Taurus, late 50’s, immigrant founders, self-made men. Excellent craftsmen but not sophisticated managers.

Managers have good reputation for reliability and integrity based on feedback from suppliers, etc.

viii

CREDIT RISK ANALYSISCASE STUDY

HISTORY

Company was formed by Taurus brothers 24 years ago to produce high precision metal parts. Have had ongoing and positive relationship with Andromeda Tractor Works – and more recently initiated higher precision production for Pegasus Auto Plant. Product quality has been good, but spotty recent history in dependability and profits. Arrival of Scorpio three years ago has helped remedy this in productivity turnaround.

BANKING AND OTHER FINANCIAL RELATIONSPrincipal bank is Gemini. Products include short-term lending, occasional equipment loans, and payroll and current account products. Relationship has been unsophisticated due to lack of management financial know-how. Checkings indicate good experience, with occasional past rollovers.

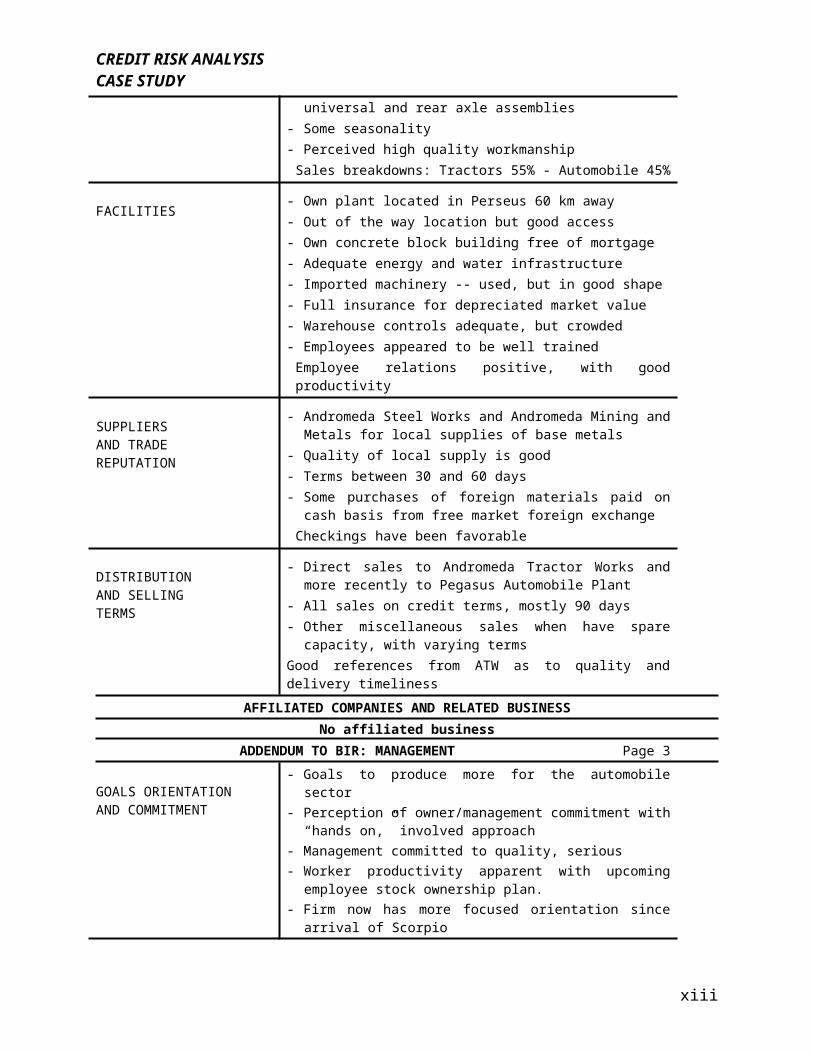

OPERATIONS Page 2

PRODUCTS - High precision metal works, with variety of products capability- Primarily tractor axle and transmissions- Now producing higher precision automobile universal and rear

axle assemblies - Some seasonality- Perceived high quality workmanship

Sales breakdowns: Tractors 55% - Automobile 45%

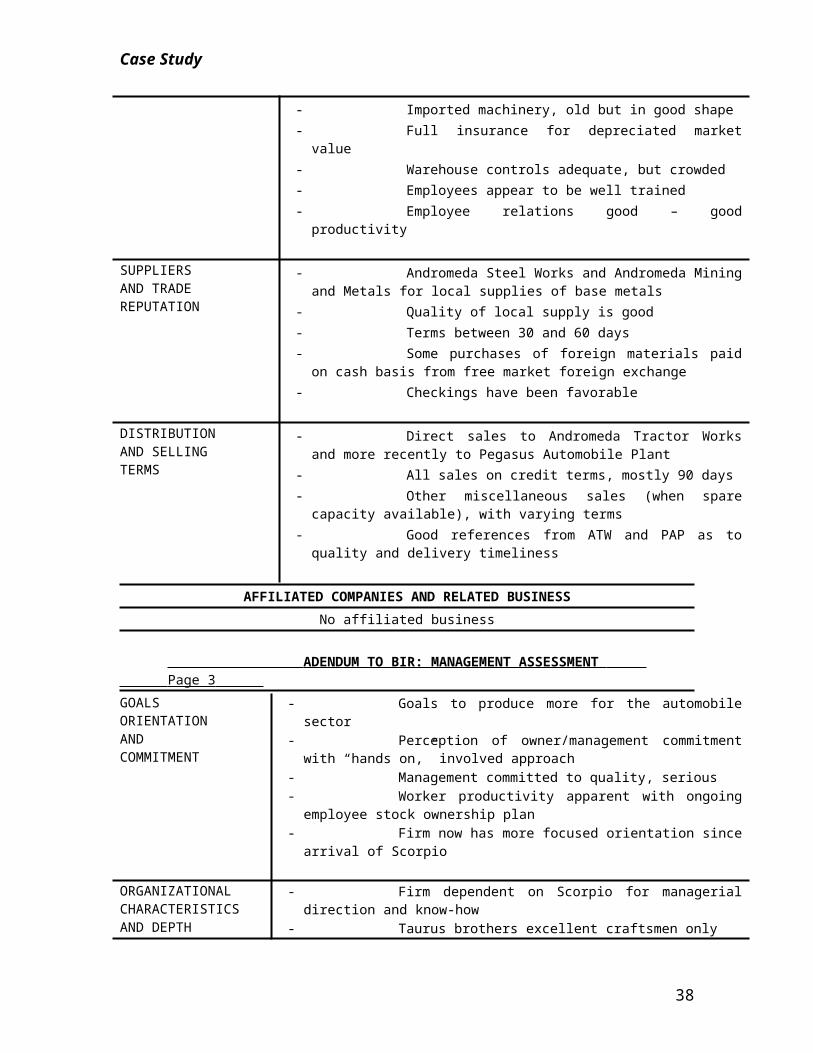

FACILITIES - Own plant located in Perseus 60 km away- Out of the way location but good access - Own concrete block building free of mortgage- Adequate energy and water infrastructure- Imported machinery -- used, but in good shape- Full insurance for depreciated market value- Warehouse controls adequate, but crowded- Employees appeared to be well trained

Employee relations positive, with good productivity

SUPPLIERSAND TRADEREPUTATION

- Andromeda Steel Works and Andromeda Mining and Metals for local supplies of base metals

- Quality of local supply is good - Terms between 30 and 60 days- Some purchases of foreign materials paid on cash basis from

free market foreign exchangeCheckings have been favorable

DISTRIBUTIONAND SELLINGTERMS

- Direct sales to Andromeda Tractor Works and more recently to Pegasus Automobile Plant

- All sales on credit terms, mostly 90 days- Other miscellaneous sales when have spare capacity, with

varying termsGood references from ATW as to quality and delivery timeliness

AFFILIATED COMPANIES AND RELATED BUSINESSNo affiliated business

ADDENDUM TO BIR: MANAGEMENT Page 3

GOALS ORIENTATIONAND COMMITMENT

- Goals to produce more for the automobile sector- Perception of owner/management commitment with “hands

ix

CREDIT RISK ANALYSISCASE STUDY

on,” involved approach- Management committed to quality, serious- Worker productivity apparent with upcoming employee stock

ownership plan.- Firm now has more focused orientation since arrival of

Scorpio

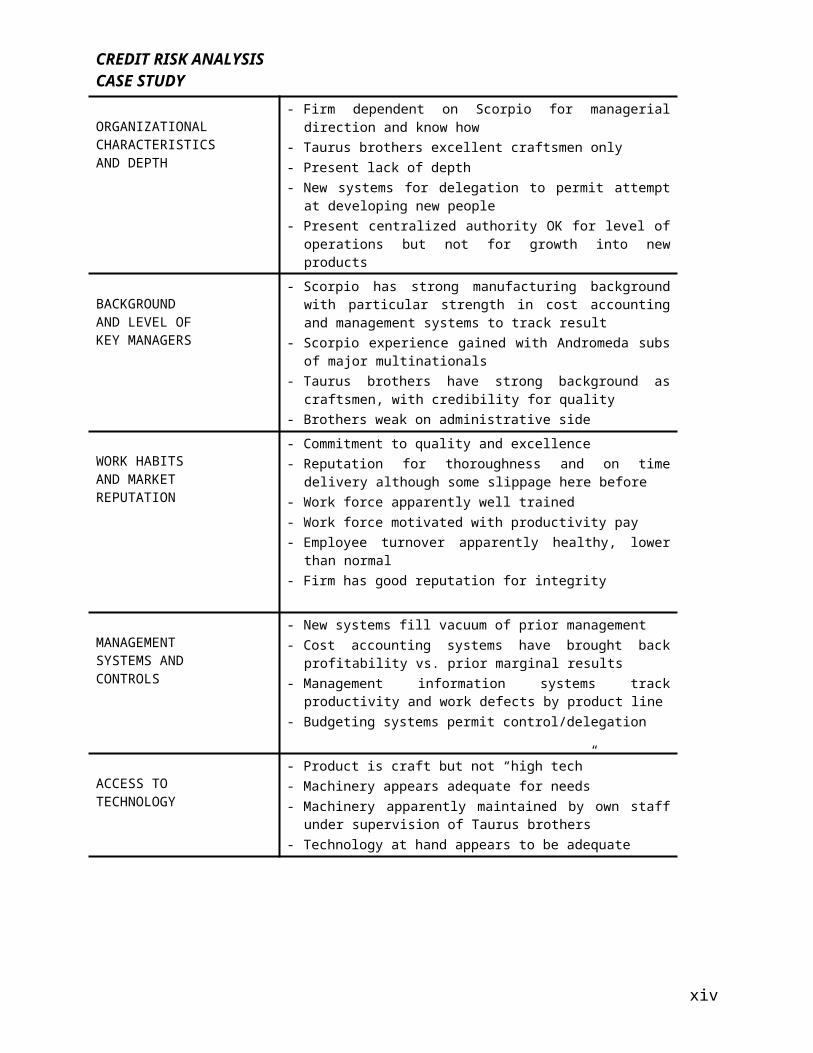

ORGANIZATIONAL CHARACTERISTICSAND DEPTH

- Firm dependent on Scorpio for managerial direction and know how

- Taurus brothers excellent craftsmen only- Present lack of depth- New systems for delegation to permit attempt at developing

new people- Present centralized authority OK for level of operations but not

for growth into new products

BACKGROUNDAND LEVEL OF KEY MANAGERS

- Scorpio has strong manufacturing background with particular strength in cost accounting and management systems to track result

- Scorpio experience gained with Andromeda subs of major multinationals

- Taurus brothers have strong background as craftsmen, with credibility for quality

- Brothers weak on administrative side

WORK HABITSAND MARKETREPUTATION

- Commitment to quality and excellence- Reputation for thoroughness and on time delivery although

some slippage here before- Work force apparently well trained- Work force motivated with productivity pay- Employee turnover apparently healthy, lower than normal- Firm has good reputation for integrity

MANAGEMENT SYSTEMS ANDCONTROLS

- New systems fill vacuum of prior management - Cost accounting systems have brought back profitability vs.

prior marginal results- Management information systems track productivity and work

defects by product line- Budgeting systems permit control/delegation

ACCESS TO TECHNOLOGY

- Product is craft but not “high tech”- Machinery appears adequate for needs- Machinery apparently maintained by own staff under

supervision of Taurus brothers- Technology at hand appears to be adequate

x

Case Study

ORION INDUSTRIES Introduction

We now return to the Orion Industries case, which was introduced in Unit One. In Part One we were given some background on the economic and political situation in the Third World country of Andromeda and the Pegasus region of the country. We were introduced to Orion Industries and Bruno Scorpio and witnessed the origination of a potential credit relationship with Leo Aries of Libra Bank.

In Part Two of the case, the banker obtained some additional information from third parties and visited the Orion plant. At the plant he met the rest of the Orion team and gathered a considerable amount of qualitative data about the company, how it operated, and its people. The banker then organized this information in anticipation of receiving the financial statements.

In Part Three of the case history, the financial numbers are put into a spreadsheet format. The banker must analyze the financial statements of the Orion Company to:

determine the financial soundness of the firm and measure historical cash generation capacity.

The analysis allows him to draw some conclusions about the relative risk and creditworthiness of Orion as a potential borrower. It also raises some additional questions about what can be reasonably anticipated in the future.

COMPARATIVE STATEMENTS OF FINANCIAL CONDITION ENCLOSED

11

Case Study

ORION INDUSTRIES – Looking to the Future

At Orion, Scorpio has come in to “clean house” financially, and has reduced both the scope of operations and the size of the balance sheet. The banker must ask how far this “downsizing” will go, and what will happen in the future.

The financial statements will probably level off soon and perhaps start to grow again, which could mean additional external financing needs for the firm. This is the reason Scorpio came to the bank in the first place. It is likely that some of the historical figures (such as reduction of current assets) are not indicative of near term future operations of the firm. But other figures, such as profitability and efficiency ratios, probably are indicative of future results under the present management.

The anticipated future financial growth is now a more pressing concern for the banker. The statements that are being analyzed, while indispensable for the financial and overall credit analysis of the firm, are history – yet any extension of credit will be for the future.

The banker must, therefore, have an idea of the likely near-term financial development of the firm. He has to calculate the situation under a growth profile with a heavier debt load, anticipating takedowns under an assumed new line of credit with Libra Bank. To do this, the banker should prepare some projections to compare with the company’s forecasts.

This can be done informally, projecting out key balance sheet accounts for one year to measure increased funding needs and the effect on the balance sheet ratios. The banker should, therefore, obtain from Scorpio sufficient information to build these informal projections. Specifically, he needs to know:

anticipated sales growth; cgs/sales and other key margins; reasonable assumptions for –

- days receivable,- days inventory,- days payable, and- other current assets and other current liabilities;

anticipated capital expenditure levels; payment terms for existing long-term debt; dividend policies; and any anticipated other new external funding.

12

Case Study

Let’s continue to Part Four of the case and find out how Aries gets the needed information and performs the projection exercise.

PART-4

Follow-up Discussion with Scorpio Regarding Historical Figures

The banker called Bruno Scorpio to schedule a meeting. The purpose of the meeting was to discuss some questions about the Orion financial statements, future goals, and assumptions for this year’s financial operations. Aries asked Scorpio to provide a copy of the receivables aging report.

At the meeting, Aries quickly reviewed the aging report with Scorpio and concluded that the information did not indicate any problems with stale receivables. “We did experience some problems in 19X1 and had to write off some uncollectibles for two small jobs we did,” said Scorpio. “This write-off affected earnings in that year, which you can see on our financial statements.

“It was this type of experience that drove us away from many of the smaller jobs,” continued Scorpio in response to the banker’s questions. “The margins may be better, but they involve a lot of headaches with retooling, cost accounting for specific jobs, and working with some difficult customers. That is why we are presently dealing only with the Andromeda Tractor Works (ATW) and the Pegasus Auto Plant (PAP). Even though we have no collectibility problems, the market strength of these two companies forces us to grant longer credit terms than we would prefer. We’re working on this and hope to negotiate something better this year, but we’re not counting on it.

“We realize that limiting ourselves to two basic clients for now perhaps does not diversify us as much as we would like. However, these are the types of relationships we hope to build for the future. Although the net income per unit sold is not great, the volume of work is attractive and we can gradually improve profits by reducing unit costs. The work provides stability over the longer term, which is also quite attractive to us. We hope to enter into even longer term contracts when the present twelve-month deals we have signed over the past two years with PAP expire.”

In response to questions about the reduction in days payable, Scorpio indicated that in earlier years the firm bought from a greater number of suppliers. Some of them offered longer terms, probably because the quality of their product was inferior. “In fact,” said Scorpio, “this was one of our problems. The mixed quality of raw materials affected our own product quality. We are now purchasing from three prime suppliers that have the best quality materials, but they are more demanding in terms of timely payment. Our days payable have been reduced from prior years because we are not a big enough customer for them to grant concessions on trade terms. Although we had hoped to limit our need for other working capital financing by relying on trade credit, we have been unable to do so.”

13

Case Study

Information on Other Credit Relationships

Aries also inquired about some of the other creditors that appeared in the notes appended to the audited statements, specifically about Sagittarius Bank and the Andromeda Development Bank. Scorpio informed Aries that the relationship with Sagittarius Bank was being liquidated by paying down the long-term equipment loan as it came due. This was also part of the reason why Scorpio had approached Libra in the first place.

The reason for terminating the relationship was because Sagittarius Bank had recently experienced financial difficulties. “Our relationship with them has been cordial and proper,” said Scorpio, “but we don’t feel we can count on them in the future for new short-term takedowns.” Aries accepted this explanation since he knew about the situation with Sagittarius. In fact, several other Sagittarius clients had recently requested significant credit increases at Libra. Nevertheless, Scorpio made a mental note to request checkings from Sagittarius.

Several years ago, the Taurus brothers had approached the Aquarius Financial Company during a cash crunch, and some loans had been hastily arranged with cash collateral provided by the Taurus brothers. Although the finance company was owned by acquaintances of the brothers, it charged high spreads for these loans since it normally did not provide financing to the industrial sector. Because of their inconvenient terms, these loans were also among the first to be put on a liquidation basis after the arrival of Scorpio.

The credit with the Andromeda Development Bank (ADB) had been arranged by Gemini under a line of credit available to local banks to finance the purchase of some German equipment under a German export promotion program. “Part of the loan was financed in local currency and part in German Marks,” said Scorpio. “When I came to the company, one of the first uses we made of current asset reductions was to eliminate the cross-currency exposure by prepaying the German Mark portion of the loans. The local currency portion is being paid down as due, with about three years left on the loan.” This explanation confirmed what Aries had figured when he saw the ADB listed as a creditor in the notes attached to the audited financial statements.Discussion Pertaining to Goals and Future PlansIn response to the banker’s questions about return on equity (ROE) and goals in this area, the customer responded: “The receivables writeoffs I mentioned earlier caused the overall ROE for the year 19X1 to be about 2%. You can see from our statements that our ROE has improved considerably during the past two years.”

“In the past two years we have spent some money installing some new machines and our new accounting and management information systems. These expenses have reduced our profits from what they could have been, but, with these systems in place, we figure that our net margin can now be improved by about 2%, which translates to an ROE of about 22%.”

14

Case Study

“We ultimately would like to improve beyond this to achieve an ROE of about 25%, which would be about 10% above inflation. We are being selective with any potential new contract, requiring that it contribute to achieving this goal within our own projections.

We are rejecting those contracts that could become a drag on earnings. Having put our house in order, we must avoid tying up our resources in marginal or underproductive deals as we have done in the past. We believe that our current product quality puts us in an advantageous position, and the time for pricing concessions is past.”Specific Short-term Goals Aries then asked questions about projected numbers. “Now that we have information on Orion’s operations and financial numbers for the past three years, we would like to have some figures on financial goals for the rest of this year. What are you budgeting for sales, net income, current account levels, capital expenditures, dividends, etc.?”

“For this year, we anticipate renewed growth, but only in our current product line. We have cut the scope of operations over the past two years about as far as we want to go, which has restored strength to our balance sheet,” said Scorpio. “With the contracts we already have, we are budgeting annual sales of Lcy 290 million which would be about a 19% sales increase. This figure is quite firm, and it will go up if we can negotiate a production increase in our contract with the Pegasus Auto Plant.”Scorpio continued. “We have been discussing this with Pegasus for a couple of weeks. If we agree on terms soon, beginning around May or June our production could build incrementally up to about a 25% increase in volume by December. This would mean an average sales increase of about 35% for the year, instead of the 19% we are projecting now. Even if we don’t get the increase with PAP, we should be able to take on another job, perhaps as a subcontractor. This should enable us to reach an overall 25% sales growth even under the most conservative circumstances.“In terms of net income, we’re shooting for a return on sales (ROS) of 8% based on a decrease to 71% in the CGS/Sales margin and to 11.5% in selling, general, and administrative expenses/sales. This will be achieved through cost cutting and increased efficiency. Although we expect some increases in short-term borrowings, the reduction of our term debt will keep interest expense at about the same level as last year. We also anticipate lowering our effective tax rate to 30% due to certain tax credits from recent investments in fixed assets. For these reasons, we believe our 8% ROS goal is quite achievable.

“On the balance sheet, we anticipate about the same relative levels in current assets, days receivable, and days payable. We may increase inventory slightly if we take on the additional work with the PAP.

15

Case Study

“As to non-operating cash needs,” continued Scorpio, “we’ll be paying a level of about 5 million in dividends since this is the main source of the shareholder funds for making payments under the stock purchase plans. We’ll also need about 5 million more for capital expenditures to replace some aging fixed assets. Because of these equipment acquisitions and those of recent years, we expect annual depreciation to climb to about 7 million.”Longer-term GoalsThe banker asked Scorpio about long-term goals. He replied that over the long term, he hoped to position Orion as one of the larger and more significant component producers in the country. “We see a strong future for the automobile sector in Andromeda, not only for the domestic market but for exports as well, and we anticipate being an important part of this development. This would mean building a new plant in the not-too-distant future since our present facilities, while adequate now and for the next couple of years, are not enough to become large producers within our market.”

“The export market is especially interesting to us. In order for major multinational car producers, such as those in the USA, to maintain the viability of their domestically produced cars, they will have to maintain or lower costs by outsourcing many of the parts. This is where we come in. We feel our quality is now approaching theirs, but our prices in dollars are cheaper.”

“We see global markets as the future for industry in Andromeda. This is what successful Asian countries have done, and I don’t see why we can’t do the same in Andromeda – produce a high quality medium tech product for global companies.”

“The difficulty is getting our foot in the door. Our relationship with the Pegasus Auto Plant is extremely valuable because the major U.S. multinational owner of PAP has its own needs in the USA. Over the long term, we hope to build a relationship with this multinational that will permit us to grow outside of Andromeda and insulate our business from the domestic economic situation. We realize, however, that this is a long way off and we don’t expect to get there tomorrow.”

The meeting ended and Scorpio left the banker’s office. Aries thought about the conversation. “Scorpio has a great deal of drive and ambition,” he thought. “He’s an impressive guy, seems to know what he’s talking about, and has the company financial numbers to give him credibility. I think we can work with him, but just the same, we had better keep a close watch on Orion to make sure they don’t get too far ahead of us, or themselves.”

Before turning to other matters, Aries asked the administrative assistant to request routine bank checkings on Orion from the Sagittarius Bank and from the Andromeda Development Bank. “A few more numbers, and we should be about ready to put a credit proposal package together,” thought Aries.

16

Case Study

Financial ProjectionsAries immediately looked at the numbers he had written down in the meeting. With these he would put together some quick, informal one-year projections to see what the situation would look like as of 12/31/X4 under Scorpio’s assumptions. To be conservative, he also wanted to project out some more pessimistic figures to gauge the sensitivity of the numbers.

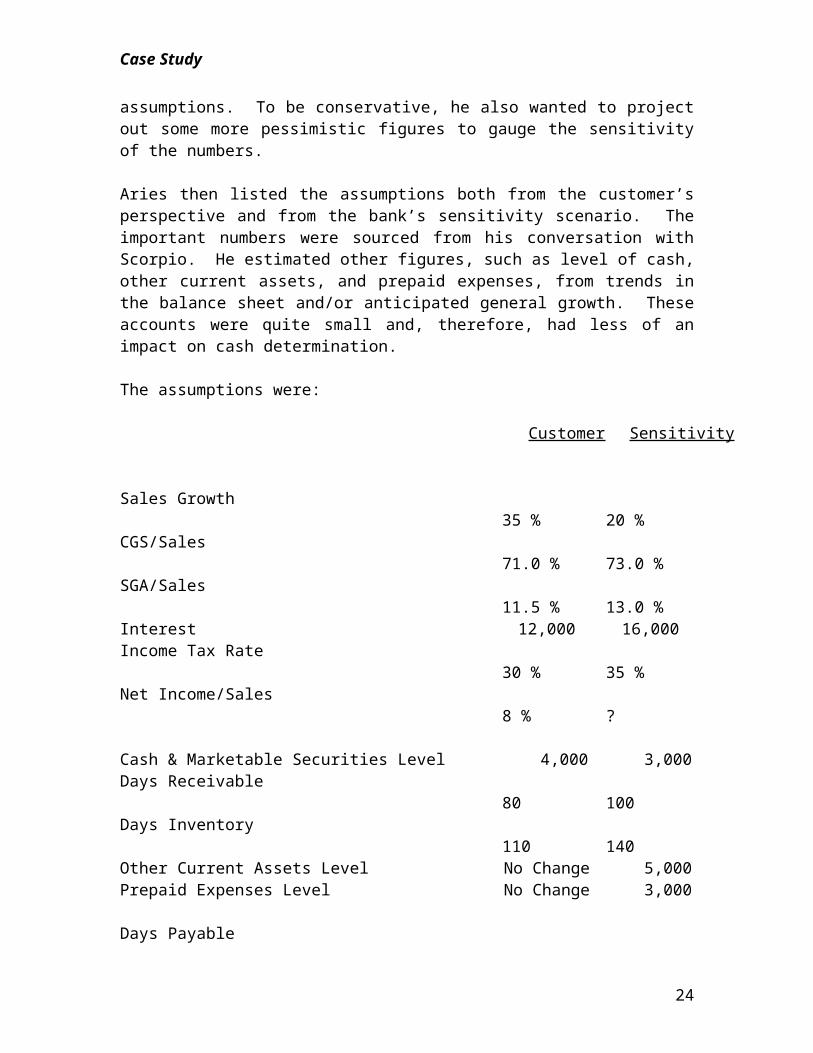

Aries then listed the assumptions both from the customer’s perspective and from the bank’s sensitivity scenario. The important numbers were sourced from his conversation with Scorpio. He estimated other figures, such as level of cash, other current assets, and prepaid expenses, from trends in the balance sheet and/or anticipated general growth. These accounts were quite small and, therefore, had less of an impact on cash determination.

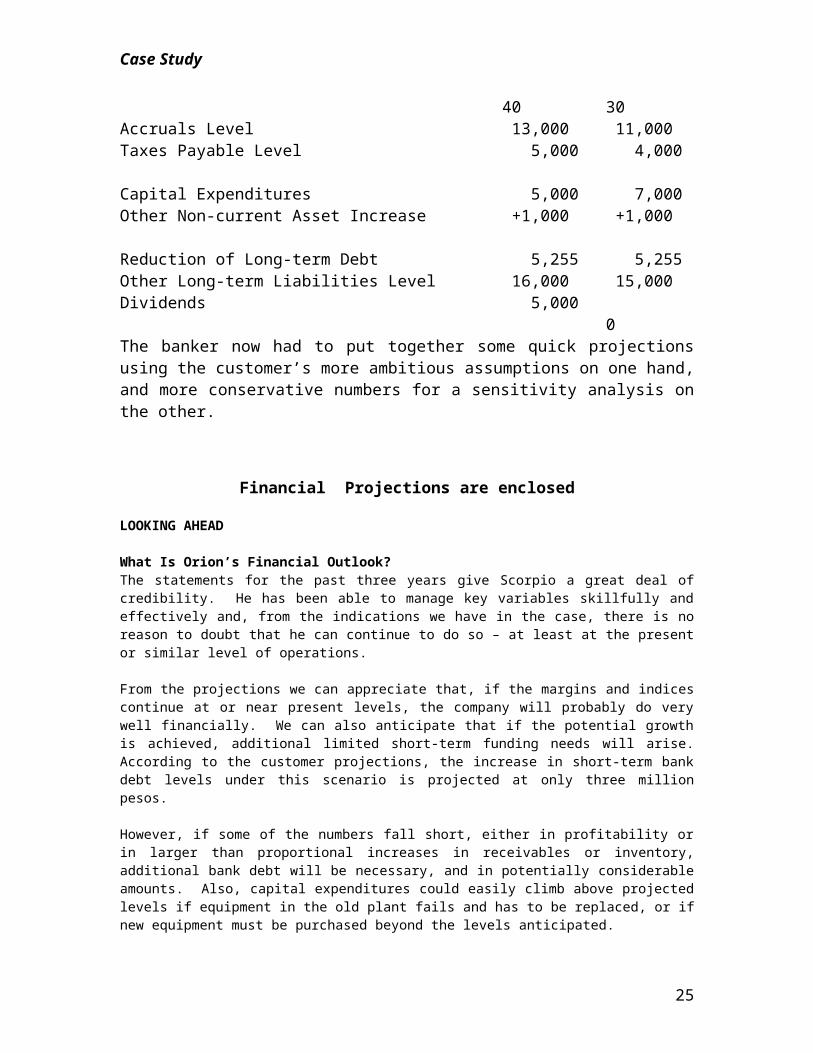

The assumptions were:

Customer Sensitivity

Sales Growth 35 % 20 %CGS/Sales 71.0 % 73.0 %SGA/Sales 11.5 % 13.0 %Interest 12,000 16,000Income Tax Rate 30 % 35 %Net Income/Sales 8 % ?

Cash & Marketable Securities Level 4,000 3,000Days Receivable 80 100Days Inventory 110 140Other Current Assets Level No Change 5,000Prepaid Expenses Level No Change 3,000

Days Payable 40 30Accruals Level 13,000 11,000Taxes Payable Level 5,000 4,000

Capital Expenditures 5,000 7,000Other Non-current Asset Increase +1,000 +1,000

Reduction of Long-term Debt 5,255 5,255Other Long-term Liabilities Level 16,000 15,000Dividends 5,000 0The banker now had to put together some quick projections using the customer’s more ambitious assumptions on one hand, and more conservative numbers for a sensitivity analysis on the other.

17

Case Study

Financial Projections are enclosed

LOOKING AHEAD

What Is Orion’s Financial Outlook?The statements for the past three years give Scorpio a great deal of credibility. He has been able to manage key variables skillfully and effectively and, from the indications we have in the case, there is no reason to doubt that he can continue to do so – at least at the present or similar level of operations.

From the projections we can appreciate that, if the margins and indices continue at or near present levels, the company will probably do very well financially. We can also anticipate that if the potential growth is achieved, additional limited short-term funding needs will arise. According to the customer projections, the increase in short-term bank debt levels under this scenario is projected at only three million pesos.

However, if some of the numbers fall short, either in profitability or in larger than proportional increases in receivables or inventory, additional bank debt will be necessary, and in potentially considerable amounts. Also, capital expenditures could easily climb above projected levels if equipment in the old plant fails and has to be replaced, or if new equipment must be purchased beyond the levels anticipated.

Because of Orion’s present strong capitalization, the firm has a great deal of creditworthiness to bank on. They should easily be able to obtain funds from a bank, be it Libra or another. In the pessimistic sensitivity scenario, the leverage ratio increases to only 1.25, which is well below historical levels.What Is the Next Step for Leo Aries? The banker has been gathering a great deal of credit information about Orion Industries, both qualitative and quantitative. He has also been analyzing this information in order to draw conclusions about the merits of a credit with Orion – the desirability of initiating a banking relationship with the company and what the terms of the relationship should be.Up to this point, Aries has been acting essentially under his own initiative. Since he cannot act alone to approve a credit facility for Orion, now is the time to decide if he wishes to promote the potential credit within the bank and, if so, to put together a credit proposal package. This will involve structuring a deal and compiling a credit recommendation for the consideration of the credit committee. We will see how this is done in the units that follow.

ORION INDUSTRIES

Introduction

In Part Five of the Orion Case Study, the banker must decide whether to proceed with a formal credit recommendation for Orion. He obtains additional financial information to construct a cash inflow/outflow budget in order to structure a potential deal.Orion Cash Inflow / OutflowA few days after putting together the Orion customer and sensitivity projections for 19X4, Aries felt he needed one last piece of financial information to prepare a cash inflow/outflow budget for Orion. Aries knew that the projections he had made, although extremely useful, provided a projection of average figures. But this did not account for the seasonality of the business, which Scorpio had mentioned on couple of occasions. The cash flow budget would help define the structuring for the potential new facility. It would provide a more detailed picture of the cash flows during the year in addition to the situation at the end of the year.

Besides, Aries was a computer buff and could utilize the cash inflow/outflow model that he had just finished devising on his personal computer. The model was similar to that used by other banks, with a couple of features that Aries had added. With the model, it would take no more than a few minutes to compile the data and print it out.

18

Case Study

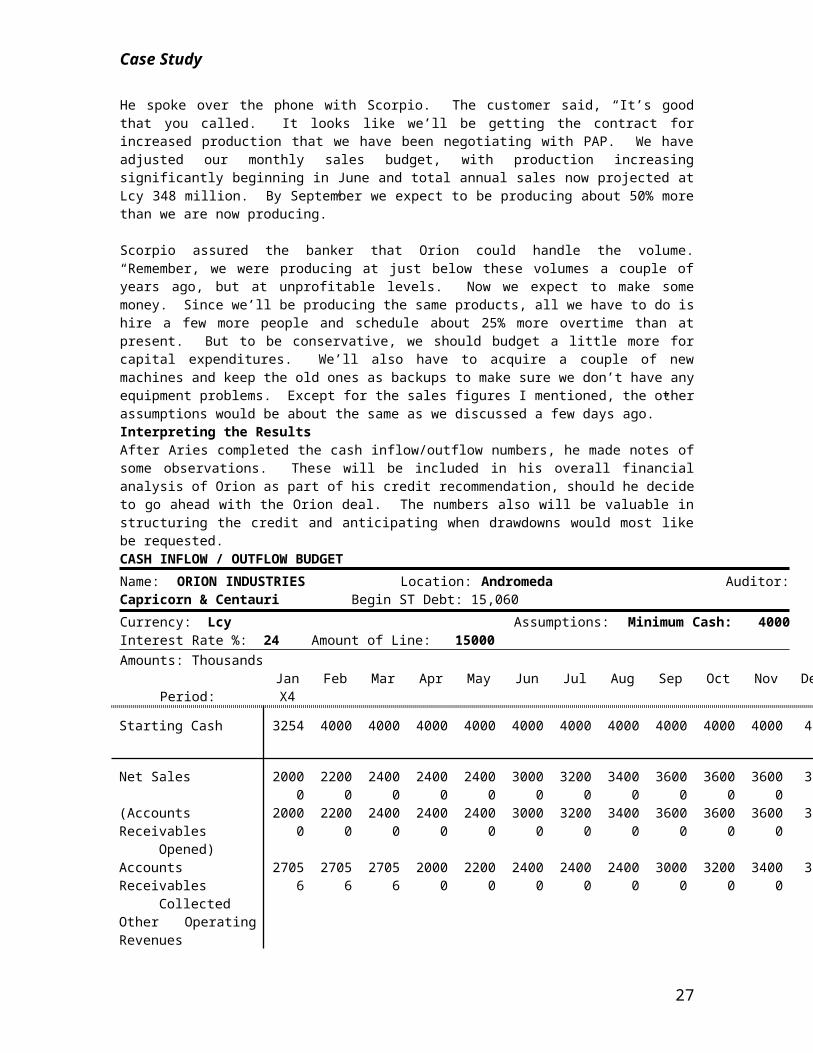

He spoke over the phone with Scorpio. The customer said, “It’s good that you called. It looks like we’ll be getting the contract for increased production that we have been negotiating with PAP. We have adjusted our monthly sales budget, with production increasing significantly beginning in June and total annual sales now projected at Lcy 348 million. By September we expect to be producing about 50% more than we are now producing.”

Scorpio assured the banker that Orion could handle the volume. “Remember, we were producing at just below these volumes a couple of years ago, but at unprofitable levels. Now we expect to make some money. Since we’ll be producing the same products, all we have to do is hire a few more people and schedule about 25% more overtime than at present. But to be conservative, we should budget a little more for capital expenditures. We’ll also have to acquire a couple of new machines and keep the old ones as backups to make sure we don’t have any equipment problems. Except for the sales figures I mentioned, the other assumptions would be about the same as we discussed a few days ago.”Interpreting the ResultsAfter Aries completed the cash inflow/outflow numbers, he made notes of some observations. These will be included in his overall financial analysis of Orion as part of his credit recommendation, should he decide to go ahead with the Orion deal. The numbers also will be valuable in structuring the credit and anticipating when drawdowns would most like be requested.CASH INFLOW / OUTFLOW BUDGETName: ORION INDUSTRIES Location: Andromeda Auditor: Capricorn & Centauri Begin ST Debt: 15,060Currency: Lcy Assumptions: Minimum Cash: 4000 Interest Rate %: 24 Amount of Line:

15000Amounts: Thousands

Period: Jan X4

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Starting Cash 3254 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000

Net Sales 20000 22000 24000 24000 24000 30000 32000 34000 36000 36000 36000 3000

(Accounts Receivables Opened)

20000 22000 24000 24000 24000 30000 32000 34000 36000 36000 36000 3000

Accounts Receivables Collected

27056 27056 27056 20000 22000 24000 24000 24000 30000 32000 34000 3600

Other Operating Revenues

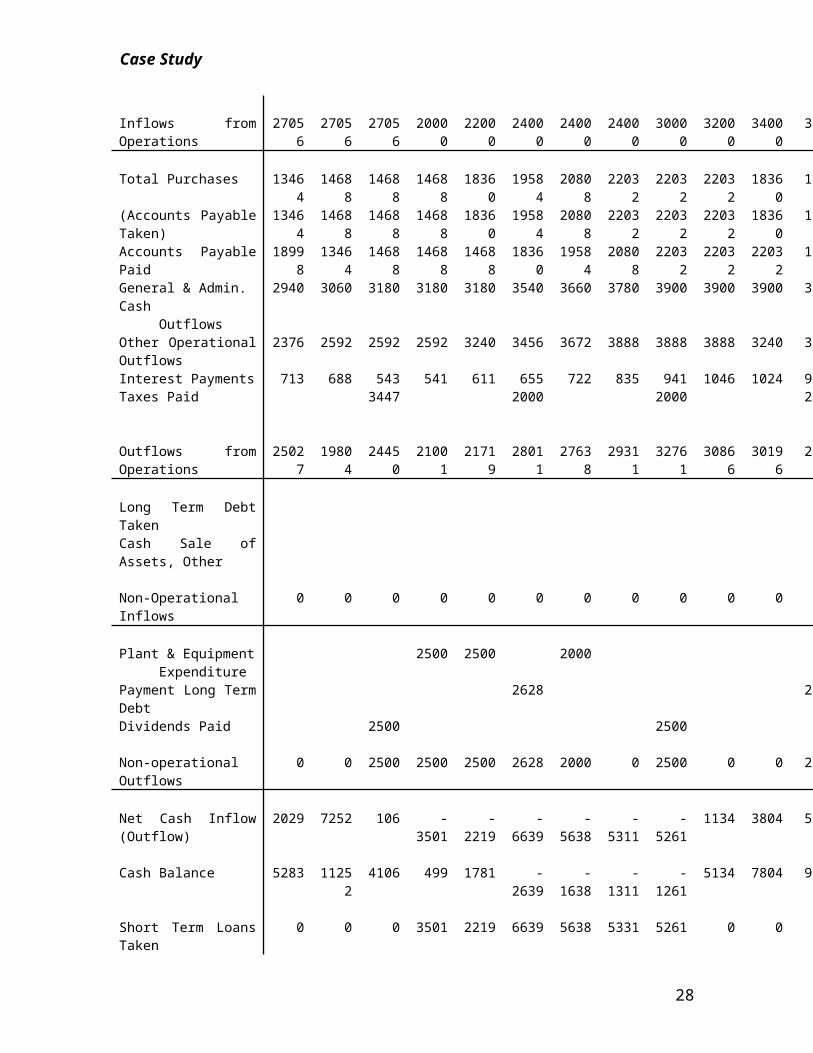

Inflows from Operations 27056 27056 27056 20000 22000 24000 24000 24000 30000 32000 34000 3600

Total Purchases 13464 14688 14688 14688 18360 19584 20808 22032 22032 22032 18360 1836

(Accounts Payable Taken)

13464 14688 14688 14688 18360 19584 20808 22032 22032 22032 18360 1836

Accounts Payable Paid 18998 13464 14688 14688 14688 18360 19584 20808 22032 22032 22032 1836

General & Admin. Cash Outflows

2940 3060 3180 3180 3180 3540 3660 3780 3900 3900 3900 3540

Other Operational Outflows

2376 2592 2592 2592 3240 3456 3672 3888 3888 3888 3240 3240

Interest Payments 713 688 543 541 611 655 722 835 941 1046 1024 947Taxes Paid 3447 2000 2000 2000

Outflows from 25027 19804 24450 21001 21719 28011 27638 29311 32761 30866 30196 2808

19

Case Study

Operations

Long Term Debt TakenCash Sale of Assets, Other

Non-Operational Inflows 0 0 0 0 0 0 0 0 0 0 0

Plant & Equipment 2500 2500 2000 ExpenditurePayment Long Term Debt

2628 2628

Dividends Paid 2500 2500

Non-operational Outflows

0 0 2500 2500 2500 2628 2000 0 2500 0 0 2628

Net Cash Inflow (Outflow)

2029 7252 106 -3501 -2219 -6639 -5638 -5311 -5261 1134 3804 5285

Cash Balance 5283 11252 4106 499 1781 -2639 -1638 -1311 -1261 5134 7804 9285

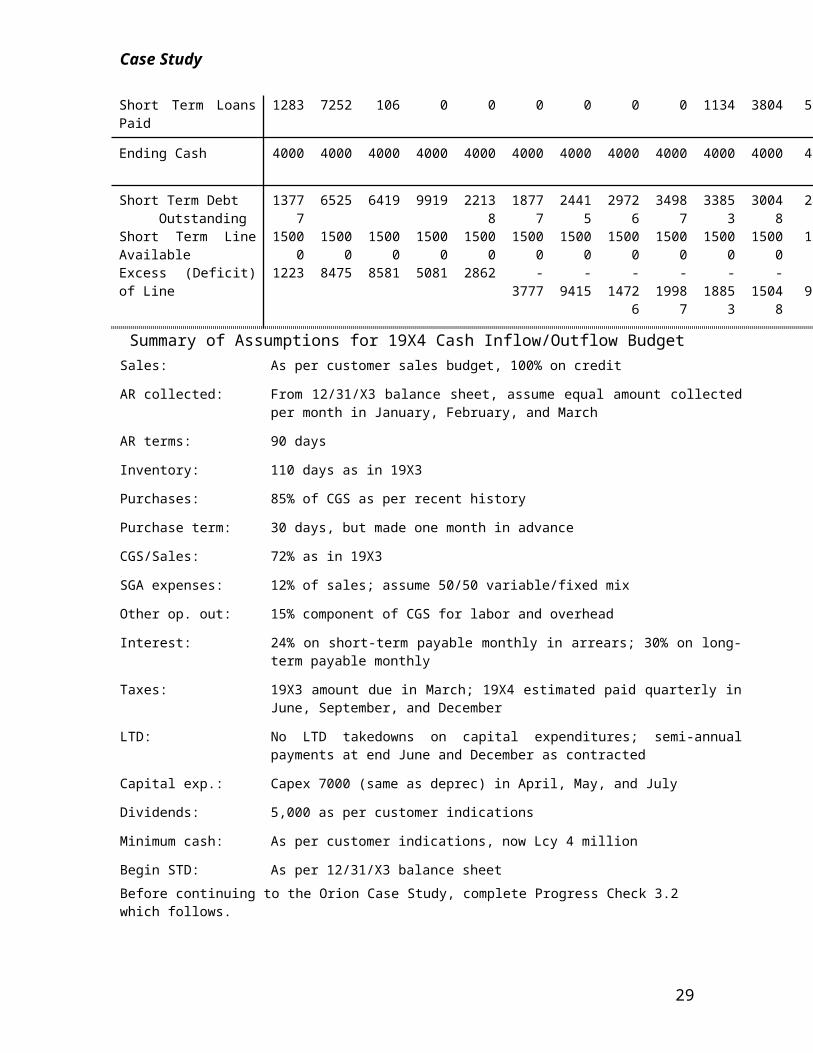

Short Term Loans Taken 0 0 0 3501 2219 6639 5638 5331 5261 0 0Short Term Loans Paid 1283 7252 106 0 0 0 0 0 0 1134 3804 5285

Ending Cash 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000

Short Term Debt Outstanding

13777 6525 6419 9919 22138 18777 24415 29726 34987 33853 30048 2476

Short Term Line Available

15000 15000 15000 15000 15000 15000 15000 15000 15000 15000 15000 1500

Excess (Deficit) of Line 1223 8475 8581 5081 2862 -3777 -9415 -14726

-19987

-18853

-15048 9764

Summary of Assumptions for 19X4 Cash Inflow/Outflow BudgetSales: As per customer sales budget, 100% on credit

AR collected: From 12/31/X3 balance sheet, assume equal amount collected per month in January, February, and March

AR terms: 90 days

Inventory: 110 days as in 19X3

Purchases: 85% of CGS as per recent history

Purchase term: 30 days, but made one month in advance

CGS/Sales: 72% as in 19X3

SGA expenses: 12% of sales; assume 50/50 variable/fixed mix

Other op. out: 15% component of CGS for labor and overhead

Interest: 24% on short-term payable monthly in arrears; 30% on long-term payable monthly

Taxes: 19X3 amount due in March; 19X4 estimated paid quarterly in June, September,

20

Case Study

and December

LTD: No LTD takedowns on capital expenditures; semi-annual payments at end June and December as contracted

Capital exp.: Capex 7000 (same as deprec) in April, May, and July

Dividends: 5,000 as per customer indications

Minimum cash: As per customer indications, now Lcy 4 million

Begin STD: As per 12/31/X3 balance sheetBefore continuing to the Orion Case Study, complete Progress Check 3.2 which follows.

ORION INDUSTRIES

In Part Six of the case study, Aries ties up some loose ends and analyzes the potential risks associated with this credit. He weighs the risk against the opportunity and decides to recommend the credit. Finally , he decides on terms and conditions and structures the potential credit.

Loose Ends

Checkings from Sagittarius BankAt about the time that Aries was completing his numbers analysis, Libra Bank received favorable checkings from Sagittarius Bank. The report confirmed that Orion had been a customer for several years and had a record for punctual payment. Sagittarius was satisfied with the relationship, but Aries knew that this bank had serious liquidity problems and couldn’t sustain the account. “Their loss is our gain,” thought Aries.Quality Confirmation from PAPAries was also able to obtain some information over the telephone from the Pegasus Automobile Plant’s procurement manager concerning the quality of Orion’s products and the company’s reliability for timely delivery. The procurement manager reported, “We are pleased with the Orion relationship. Their product is top quality and management is serious about on-time delivery, which helps us reduce our own inventory requirements. Orion continues to be one of our smaller suppliers, but we are pleased that they have agreed to increase their volume with us. We intend to limit our suppliers to those that can best integrate their operations with ours.”Aries noted the gist of the conversation in the reference section of the credit file. Although this was a strong reference, Aries was now thinking about the possible risks with the potential credit – risks which must be considered along with the many positive factors for structuring a credit for Orion.Credit RisksSmall Customer BaseWhile the PAP procurement manager gave a good recommendation regarding quality and timeliness, he flagged a potential risk that Aries had not yet considered. The risk was that in an economic downturn, PAP might view Orion as a marginal producer and eliminate the company as a supplier. However, the strong economic situation, the growing market demand, and the increased contract with PAP seemed to neutralize this risk for the short term. Also, Orion’s production quality was some insurance against loss of the relationship with PAP or with the Tractor Works.While Orion presently produced for these two principal customers, there were other possibilities as well. Most of the less profitable relationships had been terminated by Scorpio over the past two years in order to focus on the more profitable clients. But Scorpio had indicated that one of their major thrusts during the next two years was to diversify even more and search out new buyers, particularly in the export market. While the current lack of a diversified customer base was a situation to keep an eye on, Aries decided that it was an acceptable risk.

21

Case Study

Insufficient Management DepthAnother credit risk appeared to be Scorpio’s overall importance to Orion and, ironically, his grasp of the company’s situation. Scorpio tended to dominate the firm’s decision making to the point where it could be considered a “one man show.” Administrative management was stretched thin. The Taurus brothers were important on the operational side, but did not have the skills or interest to manage effectively.Aries had discussed this with Scorpio and learned that two key people had been trained to maintain the integrity of the cost accounting and management information systems, which were so crucial to the success of the firm. In addition, a new administrative manager would be hired when operations started to expand. The risk of insufficient management personnel appeared to be diminishing, but it was something else to keep an eye on.Overly Ambitious GoalsAries also considered the related risk that perhaps Scorpio’s goals were overly ambitious and he was trying to achieve too much, too soon. It was possible he was overextending the company and himself. Aries had jokingly brought up the subject with Scorpio on one occasion. The customer responded, “Perhaps, but our track record over the past two years shows that although our balance sheet has shrunk rather than grown, our profitability has grown tremendously. This should give us some credibility on that score.”Age of the PlantThe age of the plant could also be considered a risk, especially considering the emphasis on quality and timely delivery of Orion products. Aries had discussed this with Scorpio, who assured him that, with the addition of a few new machines, the plant was capable of producing under their contracted obligations. But Scorpio did acknowledge that within a couple of years a new plant with greater capacity would probably be necessary, especially if additional contracts could be obtained. This would either involve expansion or relocation.Other RisksThere were other risks, such as potential problems with availability of raw materials (most were produced domestically) and qualified labor, but these risks were shared by practically all industrial producers and had never hampered Orion in the past. World petroleum prices were relatively low at this time, and were expected to remain low for the foreseeable future. Therefore, fuel prices were not expected to negatively impact domestic or international demand for automobiles, at least for the next several years.Since Orion no longer had any foreign currency debt, devaluation was not a risk, and the mini-devaluations even helped Andromedan exports remain competitive. Auto production costs in Andromeda were lower than in developed countries. Export of automobiles and parts had become a major potential source of foreign currency earnings, and devaluation would probably make these exports even more competitive – particularly since a major portion of the components was sourced domestically.Balancing Opportunities with RisksGrowing CompanyLeo Aries felt quite strongly that he had a solid potential credit. He liked Orion Industries because it was a growing middle-size enterprise with a quality product in an improving market. The company matched well with his unit’s target market definition and appeared to be a company with continually growing needs. The situation was favorable for the bank to develop a mutually beneficial, solid relationship.Professional, Experienced PersonnelThe management personnel at Orion were professional and experienced. They had a practical focus, high standards of quality and the ability to maximize their operation without frills or excessive investment in plant and buildings. Their plans indicated an excellent potential opportunity for the bank to finance the future plant relocation and/or expansion, and to provide letters of credit or other trade services for exports.Quality ProductAries also thought about Orion’s product. There was a strong demand for parts in Andromeda’s rapidly expanding automotive sector. In addition, Orion was able to produce other products, including the existing line of tractor parts. The tractor market was not growing as fast as the automotive sector, but continued to offer an attractive, consistent demand for metal products.

22

Case Study

Orion’s products had a strong reputation for quality and, because of this, the company should be able to withstand an economic downturn.Strong Financial SituationThe financial situation of the company was quite strong. The statements clearly reflected how Scorpio reduced the size of operations and made more efficient use of his assets. The company became more profitable because margins were improved and interest expense was reduced by the prepayment of long-term debt. The overall reduction in liabilities was accomplished by reducing current assets and not by investing in new fixed assets. The balance sheet was quite strong with a leverage of only 0.87 on 12/31/X3, reduced by more than half in only two years. However, borrowing would reverse that.Strong LeadershipIn particular, Aries admired Scorpio. The potential customer was an impressive person, soft-spoken but commanding of respect. He was a good manager with strong credibility established by his impressive turnaround of the Orion financial situation. He was a rare combination of a numbers and operations man, with a strong grasp and attention to detail. He was a man that Aries felt he could trust and work with comfortably.

Structuring the Credit

Aries felt that Scorpio’s request for a short-term line of credit, with drawdowns up to a maximum Lcy 40 million, was the appropriate structure. The amount seemed high in relation to projected needs, especially considering that Gemini Bank currently offered about Lcy 15 million in short-term facilities. But Aries was willing to go with the amount in order to compete favorably with Gemini for the business, and also to maintain a strong cushion of availability in case of unexpected additional needs.The bank operated under this mode with many other industrial enterprises, and the structuring worked quite well. The facility would permit the borrower to draw down as needed for a determined period up to 180 days, or to discount receivables. The company to its own cash flow cycle could adjust that way the borrowing.

ORION INDUSTRIESFinishing Touches

Aries discussed the structure (proposed in Part Six) with Scorpio to confirm his agreement on the details. In general, the customer was in agreement. “Although much of the time we’ll be discounting receivables, we prefer the flexibility of short-term loan availability as well. This will see us through just fine,” said Scorpio.Scorpio balked at the 3% spread and 1% commission as a negotiating tactic; but, knowing this was the market rate, he finally accepted the terms. “Next year we’ll be back asking you to reduce the spread, after you see how strong our balance sheet comes out,” said Scorpio. Aries said, “I think we can work on this basis and I’ll start the approval machinery moving right away, Of course, you realize this is not our final position until all approvals are obtained up the line.” The banker had to cover himself since credit seniors might make some changes or additions to conditions on approval, although he thought any changes would be minor. Aries felt confident that this credit request would sail through the approval chain because it was a strong credit and consistent with the type of client the bank wanted.As the meeting between Scorpio and Aries ended, the client mentioned his concern about how much longer this approval process would take. “It’s already been about four weeks,” he said, “and, now that we have the contract for increased production for PAP, we’ll need funds availability soon. Can we have a commitment from your bank in one week’s time?”Aries answered that this should be sufficient time. He knew that Scorpio must be thinking in terms of obtaining financial backstop availability very soon. If something went wrong with the Libra Bank negotiations now, Scorpio would have very little time to patch something together with another bank. But these were just hypothetical problems, figured Aries. “Nothing will go wrong.”

23

Case Study

Credit PackageAries had all of the elements of the credit package ready except for the credit memo, which he stayed late that night to finish. Given the amount of exposure recommended for Orion, Aries knew that the credit would have to be approved by his department head and the Senior Credit Officer of the Libra Bank, who was at the second highest level, below the Board of Directors.When he had finished, Aries left the credit package, along with the credit file, on the department head’s desk. Aries had kept his credit supervisor informed of the progress with the potential credit, so the supervisor was familiar with the situation and was able to sign off on the credit application quickly. The credit supervisor had provided some valuable thoughts during the analysis phase, and had participated in a couple of meetings with Scorpio.The credit package was then routed to the Senior Credit Officer (SCO) of the Libra Bank. Aries had met with the SCO on two or three occasions and had been impressed with the depth of the SCO’s credit knowledge, which Aries thought fully justified the SCO’s strong reputation.Review of the Credit PackageThe SCO’s policy was to read the material carefully once and make a quick decision one way or the other. If there were any loose ends to tie up, he would discuss them with the author in person and ask the credit officer to quickly adjust them. If he agreed with the credit proposal, he would sign the Credit Proposal/Approval form when this was done. If there were fundamental problems, he would discuss them immediately with the author and see if a cure could be found. If not, the credit would be disapproved.On the following pages, you will see a reproduction of the Orion credit package. It includes:

Credit Proposal/Approval Form, Basic Information Report (BIR), Addendum to BIR – Management Assessment, Comparative Statement of Financial Condition (spreads), Customer and Sensitivity Projections, Cash Inflow/Outflow Budget, Summary of Assumptions for 19X4 Inflow/Outflow Budget,

and Credit Memo.

Most of this material has been developed in earlier parts of the Orion Case and is presented again to demonstrate what a credit package looks like. Carefully read the Credit Memo on page 4-24 to understand the style and methodology of the credit presentation and to be prepared to answer subsequent questions for analysis.

24

Case Study

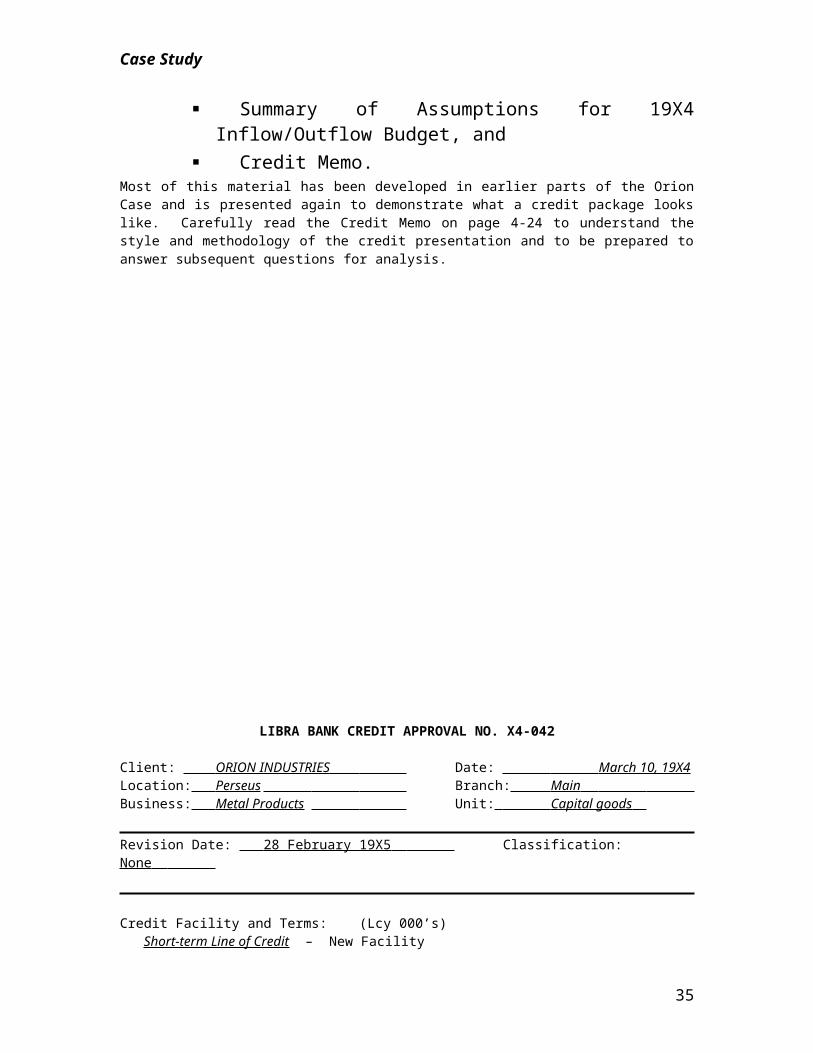

LIBRA BANK CREDIT APPROVAL NO. X4-042

Client: ORION INDUSTRIES Date: March 10, 19X4 Location: Perseus Branch: Main Business: Metal Products Unit: Capital goods

Revision Date: 28 February 19X5 Classification: None

Credit Facility and Terms: (Lcy 000’s)Short-term Line of Credit – New Facility

Amount: Lcy 40,000 Purpose: Short-term loans, or discount of trade bills with recourse Payments: In full at maturity, or as collected for trade bills Tenor: Up to 180 days Interest: Base rate or discount rate + 3% p.a. Commission: 1% flat on opening Commitment Fee: .25% p.a. on undrawn facility Support: 1) Lien on trade receivables for 120% of outstandings for loans

2) Personal guarantee of B. Scorpio and M. and N. Taurus for full amount of facility

3) Life insurance policy in name of B. Scorpio endorsed to bankExisting Aggregate Facilities: (Lcy 000’s) Approved

None

Security/Support: Pledge receivables from PAP and ATW for 120% of outstandings duly

endorsed to bank (on loans) Continuing Letter of Guarantee (CLG) signed by Orion to evidence

recourse on discounted trade bills CLG signed by B. Scorpio and M. and N. Taurus for full amount of facility.

Approved Amount: Lcy 40,000,000

Credit Committee: Area Head: Seniors: Board:

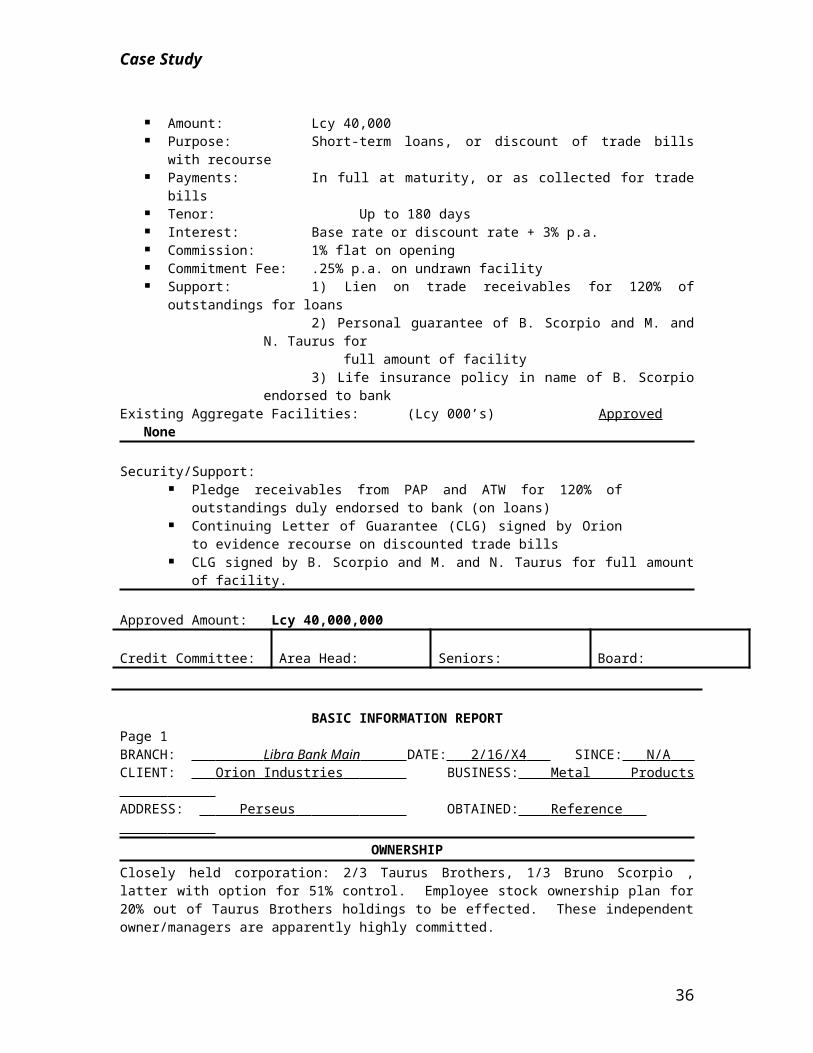

BASIC INFORMATION REPORT Page 1BRANCH: Libra Bank Main DATE: 2/16/X4 SINCE: N/A CLIENT: Orion Industries BUSINESS: Metal Products ADDRESS: Perseus OBTAINED: Reference

25

Case Study

OWNERSHIPClosely held corporation: 2/3 Taurus Brothers, 1/3 Bruno Scorpio , latter with option for 51% control. Employee stock ownership plan for 20% out of Taurus Brothers holdings to be effected. These independent owner/managers are apparently highly committed.

DIRECTORS AND MANAGEMENTGeneral Manager

Bruno Scorpio, early 40s, mechanical engineer from University of Andromeda. Experienced in prior positions with subsidiaries of major multi-nationals. Strong background in manufacturing and cost/management systems.

Production Max and Nick Taurus, late 50s, immigrant founders, self-made men. Excellent craftsmen, but not sophisticated managers.Managers have good reputation for reliability and integrity based on feedback from suppliers, etc.

HISTORYCompany was formed by Taurus brothers 24 years ago to produce high precision metal parts. Have had ongoing and positive relationship with Andromeda Tractor Works, and more recently initiated higher precision production for Pegasus Auto Plant. Product quality has been good, but spotty recent history in dependability and profits. Arrival of Scorpio three years ago has helped remedy this in productivity turnaround.

BANKING AND OTHER FINANCIAL RELATIONSPrincipal bank has been Gemini, with some lending by Sagittarius. Latter relationship being terminated, due to bank’s problems. Gemini products include short-term lending, occasional equipment loans booked through Andromeda Development Bank, and payroll and current account products. Relationship has been unsophisticated due to lack of management financial skill. Checkings indicate good experience, with occasional past rollovers.

OPERATIONS Page 2 PRODUCTS - High precision metal works, with variety of products

capability- Primarily tractor axle and transmissions- Now producing higher precision automobile universal

and rear axle assemblies- Some seasonality- Perceived high quality workmanship- Sales breakdowns: Tractor 55% – Automobile 45%

FACILITIES - Own plant located in Perseus 60 km away- Out of the way location, but good access- Own concrete block building free of mortgage- Adequate energy and water infrastructure- Imported machinery, old but in good shape- Full insurance for depreciated market value- Warehouse controls adequate, but crowded- Employees appear to be well trained- Employee relations good – good productivity

SUPPLIERSAND TRADEREPUTATION

- Andromeda Steel Works and Andromeda Mining and Metals for local supplies of base metals

- Quality of local supply is good

26

Case Study

- Terms between 30 and 60 days- Some purchases of foreign materials paid on cash basis

from free market foreign exchange- Checkings have been favorable

DISTRIBUTION AND SELLING TERMS

- Direct sales to Andromeda Tractor Works and more recently to Pegasus Automobile Plant

- All sales on credit terms, mostly 90 days- Other miscellaneous sales (when spare capacity

available), with varying terms- Good references from ATW and PAP as to quality and

delivery timeliness

AFFILIATED COMPANIES AND RELATED BUSINESSNo affiliated business

ADENDUM TO BIR: MANAGEMENT ASSESSMENT Page 3 GOALSORIENTATIONAND COMMITMENT

- Goals to produce more for the automobile sector- Perception of owner/management commitment with

“hands on,” involved approach- Management committed to quality, serious- Worker productivity apparent with ongoing employee

stock ownership plan- Firm now has more focused orientation since arrival of

Scorpio

ORGANIZATIONAL CHARACTERISTICS AND DEPTH

- Firm dependent on Scorpio for managerial direction and know-how

- Taurus brothers excellent craftsmen only- Present lack of depth- New delegation system to develop new people- Present centralized authority OK for level of operations,

but not for growth into new products

BACKGROUND AND LEVEL OF KEY MANAGERS

- Scorpio has strong manufacturing background, with particular strength in cost accounting and management systems for tracking results

- Scorpio experience gained with Andromeda subs of major multinationals

- Taurus brothers have strong background as craftsmen, with credibility for quality

- Brothers weak on administrative side

WORK HABITS AND MARKET REPUTATON

- Commitment to quality and excellence- Reputation for thoroughness and on-time delivery,

although previously some problems- Work force apparently well trained- Work force motivated with productivity pay- Employee turnover apparently healthy, lower than normal- Firm has good reputation for integrity

27

Case Study

MANAGEMENT SYSTEMS AND CONTROLS

- New systems fill vacuum of prior management- Cost accounting systems have brought back profitability

vs. prior marginal results- Management information systems track productivity and

work defects by product line- Budgeting systems permit control/delegation

ACCESS TO TECHNOLOGY

- Product is craft but not “high tech”- Machinery appears adequate for needs- Machinery apparently maintained by own staff under

supervision of Taurus brothers- Technology appears to be adequate

COMPARATIVE STATEMENT OF FINANCIAL CONDITIONName: ORION INDUSTRIES Location: ANDORMEDA

Currency: LCY IN THOUSANDS Auditor: CAPRICORN & CENTAURI

Date: 12/31/X1 12/31/X2 12/31/X3Number of Months 12 12 12

Sales on Credit % 100 100 100

BALANCE SHEET Actual Actual Actual

ASSETSCash 1,997 1,792 1,854Marketable Securities 2,000 2,000 1,400Accounts Receivable 67,350 61,872 54,114Inventory 74,720 56,972 53,468Other Current Assets 5,476 2,650 4,126Prepaid Expenses 3,015 2,651 2,455 0 Current Assets 154,558 127,937 117,417Net Fixed Assets 44,762 41,127 38,406Investments 0 0 0Other Non-current Assets 2,986 5,242 6,107Intangibles 0 0 0 0 Total Non-current Assets 47,748 46,369 44,513 0

Total Assets 202,306 174,306 161,930 0

LIABILITIES & EQUITYDue Banks, Short-term 39,615 35,542 15.060Accounts Payable 26,720 20,468 18,998Accruals 10,429 8,072 8,388Taxes Payable 230 2,116 3,447Other Current LiabilitiesCurrent Portion L T Debt 7,120 5,433 5,255 0 Current Liabilities 84,114 68,631 51,148Long-term Debt 33,247 16,452 11,232Other Liabilities, Long-term 19,794 12,732 12,970 0 Long-term Liabilities 53,041 29,184 24,202 0

28

Case Study

Total Liabilities 137,155 97,815 75,350Common Stock 33,000 30,000 30,000Surplus & Reserves 24,000 24,481 25,080Retained Earnings 11,151 22,010 31,500 0 Total Net Worth 65,151 76,491 86,580 0

Liabilities & Net Worth 202,306 174,306 161,930 0

29

Case Study

Name: ORION INDUSTRIESDate: 12/31/X1 12/31/X2 12/31/X3

INCOME STATEMENT Actual Actual ActualNet Sales 277,867 270,238 243,504Cost of Goods Sold 213,306 202,528 175,310 % of Sales 76.8 74.9 72.0Selling, General, Admin. Expense 38,972 32,566 30,896 % of Sales 14.0 12.1 12.7 0

Gross Margin 25,589 35,144 37,298 % of Sales 9.2 13.0 15.3Depreciation 5,121 5,374 6,539Interest Expense 18,862 13,327 10,760Other Income/(Expenses), Net -67 -144 -98 0

Earnings Before Taxes 1,539 16,299 19,901 0 % of Sales 0.6 6.0 8.2Income Taxes 304 4,959 6,866Extraordinary Items 0 0 0 0

Net Income 1,235 11,340 13,035 % of Sales 0.4 4.2 5.4 0

RATIOS (Annualized)

Sales Growth Rate % -2.7 -9.9Net Income/Average Net Worth % 1.9 16.0 16.0Net Income/Average Assets % 0.6 6.0 7.8Sales/Average Assets 1.37 1.44 1.45 0

Current Ratio 1.8 1.9 2.3Quick Asset Ratio 0.8 1.0 1.1Days Receivables 87 82 80Days Inventory 126 101 110Days Payable 45 36 39 9

Leverage (Debt/Equity) 2.11 1.28 0.87Long-term Leverage 0.81 0.38 0.28 4

RECONCILIATIONS

Net WorthBeginning Net Worth N/A 65,151 76,491Plus: Net Income 1,235 11,340 13,035Plus: Fresh Capital 0 0Total Increase 11,340 13,035Less: Dividends, Other 0 2,946Increase/Decrease in NW 11,340 10,089Ending Net Worth 65,151 76,491 86,580 0

Fixed AssetsBeginning Fixed Assets N/A 44,762 41,127Less: Depreciation 5,121 5,374 6,539Subtotal 39,388 34,588Ending Fixed Assets 44,762 41,127 38,406Capital Expenditure . 1,739 3,818 8

Name: ORION INDUSTRIES

30

Case Study

Date: 12/31/X1 12/31/X2 12/31/X3Number of Months 12 12 12

CASH GENERATION Actual Actual Actual

Net Income 1,235 11,340 13,035Depreciation 5,121 5,374 6,539Other Non-Cash Charges N/A 0 0Gross Operating Funds Generation 6,356 16,714 19,574

Increase in Cash & Market Securities -205 -538Increase in Accounts Receivable -5,478 -7,758Increase in Inventory -17,748 -3,504Increase Other Current Assets -2,826 1,476Increase Prepaid Expenses . -364 -196

Total Operating Needs . -26,621 -10,520

Increase in Accounts Payable -6,252 -1,470Increase in Accruals -2,357 316Increase Taxes Payable 1,886 1,331Increase Other Current Liabilities . 0 0

Total Operating Sources . -6,723 177

Net Operating Cash Generation . 36,612 30,271

Capital Expenditures 1,739 3,818Dividends 0 2,946Increase in Investments 0 0Increase Other Non-Current Assets 2,256 865Increase in Intangibles 0 0Reduction Short-term Bank Debt 7,073 17,482Reduction Long-term Debt . 18,482 5,398

Total Non-Operating Needs . 29,550 30,509

Fresh Capital/Other NW Increase 0 0Increase Other Long-term Liabilities -7,062 238Increase Short-term Bank Debt 0 0Increase Long-term Debt . 0 0

Total Non-Operating Sources . -7,062 238

* Check (NOCG – TNON + TNOS) . 0 0

* Check (Net Operating Cash Generation – Total Non-operating Needs + Total Non-operating Sources)

Name: ORION INDUSTRIES

Date: 12/31/X1 12/31/X2 12/31/X3Number of Months 12 12 12

SUPPLEMENTARY INFORMATION

Net Fixed Assets Breakdown

31

Case Study

Land 6,721 6,721 6,721Buildings 21,520 21,520 24,036Machinery & Equipment 41,387 43,522 44,567Vehicles 1,767 1,371 1,628Subtotal 71,395 73,134 76,952Less: Accumulated Depreciation 26,633 32,007 38,546Net Fixed Assets 44,762 41,127 38,406

Due Banks, Short-termGemini Bank 13,947 17,440 15,060Sagittarius Bank 14,571 9,655 0Acquarius Financial 11,097 5,447 0

39,615 32,542 15,060

Long-term DebtGemini Bank 6,422 5,276 4,130Sagittarius Bank 9,827 6,344 3,151Andromeda Develop Bank 24,118 10,265 9,206

40,367 21,885 16,487Less: Current Portion 7,120 5,433 5,255

33,247 16,452 11,232

InventoryFinished Goods 23,630 16,032 19,377Work in Process 4,423 2,461 3,855Raw Material 46,667 38,479 30,236

74,720 56,972 53,468

32

Case Study

CLIENT AND SENSITIVITY PROJECTIONS

ORION INDUSTRIES

12 month Actual

12 month Customer

12 month Sensitivity

Thousands of Lcy 12/31/X3 Projection Projection

BALANCE SHEET

Cash & Marketable Securities 3,254 4,000 3,000Accounts Receivable 54,114 73,051 81,168Inventory 53,468 71,316 82,954Other Current Assets 4,126 4,126 5,000Prepaid Expenses 2,455 2,455 3,000Current Assets 117,417 154,948 175,121

Net Fixed Assets 38,406 36,406 38,406Investments 0 0 0Other Non-current Assets 6,107 7,107 7,107Intangibles 0 0 0Non-current Assets 44,513 43,513 45,513

TOTAL ASSETS 161,930 198,461 220,635

Bank Debt, Short-term 15,060 18,747 63,406Accounts Payable 18,998 25,933 17,776Accruals 8,388 13,000 11,000Taxes Payable 3,447 5,000 4,000Other Current Liabilities 0 0 0Current Portion L T Debt 5,255 5,255 5,255Current Liabilities 51,148 67,935 101,437

Long-term Debt 11,232 5,977 5,977Other Long-term Liabilities 12,970 16,000 15,000TOTAL LIABILITIES 75,350 89,912 122,414

Common Stock 30,000 30,000 30,000Surplus and Reserves 25,080 25,680 25,680Retained Earnings 31,500 52,869 42,541

TOTAL NET WORTH 86,580 108,549 98,221

LIABILITIES & NET WORTH 161,930 198,461 220,63512/31/X3 Customer Sensitivity

INCOME STATEMENT

Net Sales 243,504 328,730 292,205Cost of Goods Sold 175,310 233,399 213,310 % of Sales 72.0 % 71.0 % 73.0 %Selling, General, Admin. Expenses 30,896 37,804 37,987 % of Sales 12.7 % 11.5 % 13.0 %

33

Case Study

Gross Margin 37,298 57,528 40,909 % of Sales 15.3 % 17.5 % 14.0 %Depreciation 6,539 7,000 7,000Interest Expense 10,760 12000 16,000Other Income, Net -98 0 0 Earnings Before Taxes 19,901 38,528 17,909 % of Sales 8.2 % 11.7 % 6.1 %Income Taxes 6,866 11,558 6,268 Net Income 13,035 26,969 11,641 % of Sales 5.4 % 8.2 % 4.0 %

RATIOS (Annualized)

Sales Growth Rate % -9.9 % 35.0 % 20.0 %Net Income/Average Net Worth % 16.0 % 27.6 % 12.06 %Net Income/Average Assets % 7.8 % 15.0 % 6.1 %Sales/Average Assets 1.4 1.8 1.5

Current Ratio 2.3 2.3 1.7Quick Asset Ratio 1.1 1.1 .8Days Receivables 80 80 100Days Inventory 110 110 140Days Payable 39 40 30

Leverage 0.87 0.83 1.25Long-term Leverage 0.28 0.20 0.21