Embed Size (px)

Citation preview

When is it time to consider

bankruptcy?

Here’s what you need to know.

Being in debt can feel like drowning.

It’s normal to wonder if bankruptcy is right. The idea of financial freedom is compelling! But is bankruptcy the right decision? Does it make you a bad person? Are there other options? Is it wrong to even consider it?

Here are some questions to ask yourHere are some questions to ask your-self before making the decsion.

Questions

1. How much do you owe?

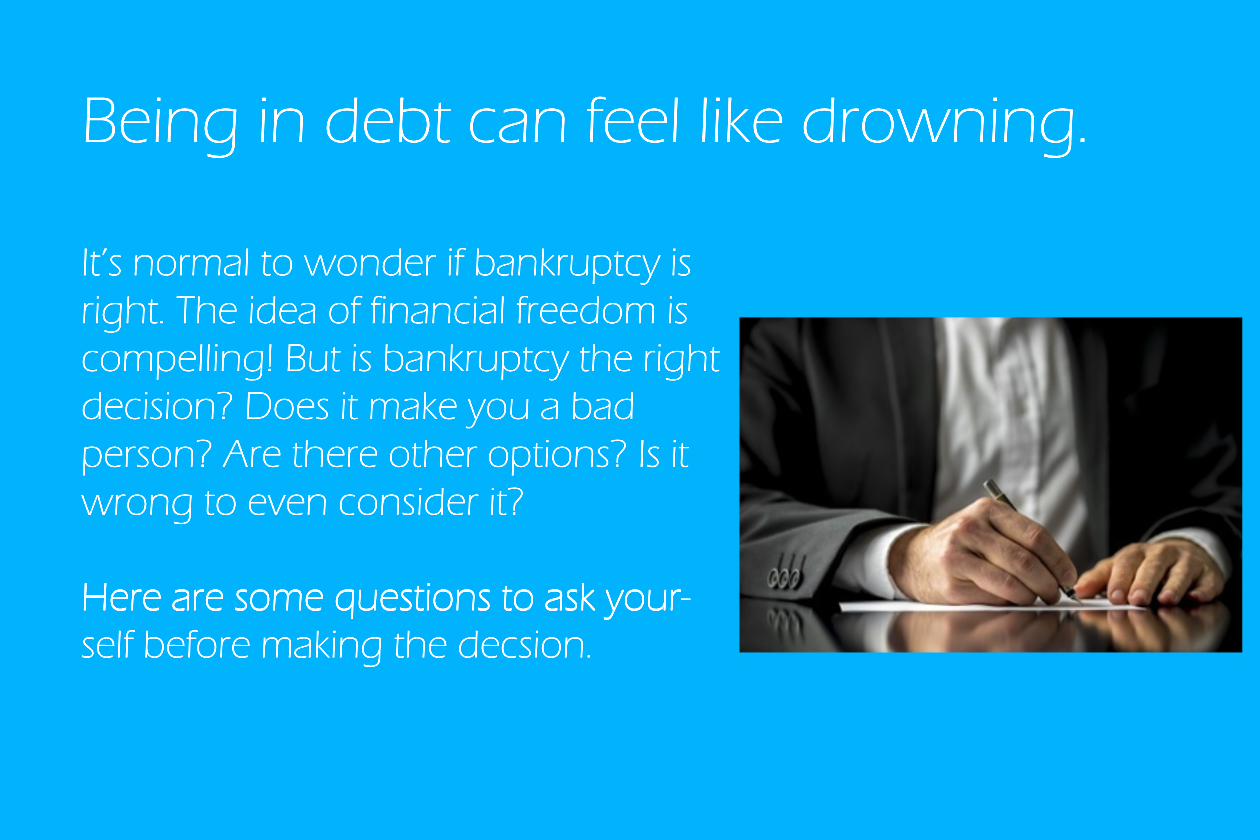

2. Is your debt “dischargable?”

3. Is bad credit going to bite you?

4. Are your problems temporary?

5. Are there other options?

6. Are you being too hard on yourself?

1. How much do you owe?Sometimes, when you sit down and do the math, you find that the amount you owe isn’t insur-mountable. A careful look at your budget might help you dis-cover a way to make your own repayment plan.

Filing for bankruptcy can cost as much as 2000 dollars, so if your debt isn’t much more than that, it might not make sense to file.

Is your debt “dischargable?”

Some kinds of debt never really go away, even in bankruptcy.

If you owe money in student loans or taxes, you probably won’t get relief. However, debt to credit card companies or payday loan companies is usually dischargable.

Be warned: if you’ve been using credit cards Be warned: if you’ve been using credit cards a lot, bankruptcy courts are going to be sus-picious and wonder why you decided to add to your debt just before declaring bankrupt-cy

Is bad credit going to be a problem?

Declaring bankruptcy means your credit score will suffer. Buying a new car, new home, or getting any type of loan will be more ex-pensive, if not impossible, in the future. It’s not a permanent prob-lem, but be aware that it can affect you for years. Do you have the discipline to operate without loans? Can you start saving money now for your next big pur-chase instead of getting a loan?

Are your problems temporary?

Did you lose your job? Is there a good chance that once you get a job you’ll be able to pay back your debts? If so, bankruptcy may not be your best option.

If you have experienced a permanent If you have experienced a permanent change in your life, such as disability, or if your debt payments are more than you’ll ever be able to afford even with a second job, then maybe bank-ruptcy could help.

Are there other options?

Can you go to credit counseling?

Can you get another job?

Have you made a budget?

Are there friends or family who can help?

Are you being too hard on yourself?

If you’ve done what you can, and the debts are only mounting and there’s no chance for escape, are you being too hard on yourself for considering bankruptcy? It exists for a reason, and good people use bankruptcy law every day. CLICK HERE to read one such story.

Find a good attorney who will talk with you frankly about your opFind a good attorney who will talk with you frankly about your op-tions. Not somebody who wants to just make money off of you - somebody who will discuss your needs and goals, and who will tell you about the pros and cons of bankruptcy.

Take care of yourself, and good luck.