Embed Size (px)

DESCRIPTION

Citation preview

Things That Every CPA Need To Know About IFRS

Peter A. Margaritis, CPA, CGMA, MAccPeter A. Margaritis, LLC

October 16, 2012

IFRS are an existing set of “high-quality, country-neutral” accounting standards that continue to evolve.

Economic benefits:• Greater transparency and comparability• Facilitate cross-boarder filings • Access to capital • Lower cost of capital• Improve investor confidence• Reduce costs

IFRSIFRSIFRSIFRS

2011

2013

2016

2005

2012

2010

2012

2005

2014

2013

2005

IFRS: 120+ Countries Permit/RequireIFRS: 120+ Countries Permit/RequireIFRS: 120+ Countries Permit/RequireIFRS: 120+ Countries Permit/Require

Source:: PwC IFRS Readiness Series

Impact on Taxes

6

Principles vs. RulesPrinciples vs. RulesPrinciples vs. RulesPrinciples vs. Rules

Abbott and Costello

Transaction Analysis

AccountingResearch

DecisionMaking

US GAAP

Transaction Analysis

AccountingResearch

DecisionMaking

IFRS

Putting Principles Into ActionPutting Principles Into ActionPutting Principles Into ActionPutting Principles Into Action

United States UpdateUnited States Update

2012

Leases Re-expose (Q1) - 2013

Revenue Recognition Redeliberations (Q3-Q4)

IFRS (H1 2013)

FI: Impairment Re-expose (Q4)

FI: Classification & Measurement Exposure Draft (Q4)

FI: General Hedging IFRS (Q4)

FI: Macro Hedging Exposure Draft (Q3/Q4)

Insurance Contracts Re-expose (Q3/Q4)

Convergence – 10/01/12

IASB/FASB Completed MoU Projects

Share-based payments Business Combinations

Segment reporting Derecognition

Research Costs Consolidation

Borrowing costs Disclosures of Interest in Other Entities

Fair ValueEmployee Benefits (post employment benefits improvement)

Joint VenturesPresentation of Financial Statements (presentation of OCI improvement)

1. Sufficient Development and Application of IFRS for the U.S. Domestic Reporting System

2. The Independence of Standard Setting for the Benefit of Investors

3. Investor Understanding and Education Regarding IFRS

4. Examination of the U.S. Regulatory Environment that Would Be Affected by a Change in Accounting Standards

5. The Impact on Issuers, Both Large and Small, Including Changes to Accounting Systems, Changes to Contractual Arrangements, Corporate Governance Considerations, and Litigation Contingencies

6. Human Capital Readiness

SEC Workplan Update

The International The International Accounting Standards Accounting Standards

Board (IASB) Board (IASB)

An independent standard setter based in London, UK (British spelling)

IASB is the successor (2001) to the IASC which was founded in 1973

The IASB is appointed and overseen by a geographically and professionally diverse group of 22 Trustees of the IFRS Foundation

There is a 15 member IASB board that is the body that sets accounting standards using a formalized due process procedure.

IASBIASBIASBIASB

Source: Guide to IASC Foundation and IASB

IASB StructureIASB StructureIASB StructureIASB Structure

Who Funds The IASB ($33M Budget - US$)

$9 million

$2.6 million

$800K

$2.6 million

$1.2 million

$400K

$1 million

$11 million

Source: IASB Foundation Annual Report (2011)

$360K

$100K

$100K

Reference Type of Pronouncement

IAS International Accounting Standard (28)

IFRS International Financial Reporting Standard (13)

IFRIC Interpretation of the International Financial Reporting Interpretations Committee (16)

SIC Interpretation of the Standing Interpretations Committee (8)

Types of PronouncementsTypes of PronouncementsTypes of PronouncementsTypes of Pronouncements

• IFRS 10 Consolidated Financial Statements – 2013

• IFRS 11 Joint Arrangements - 2013

• IFRS 12 Disclosure of Interests in Other Entities - 2013

• IFRS 13 Fair Value Measurement - 2013

• IAS 19 Employee Benefits - 2013

• IAS 27 Separate Financial Statements - 2013

• IAS 28 Investments in Associates and Joint Ventures - 2013

• IAS 32 Offsetting Financial Assets and Liabilities - 2013

• IFRS 7 Disclosures: Offsetting Financial Assets and Financial Liabilities - 2014 w/ early adoption

• IFRS 9 Classification and Measurement of Financial Assets - 2015 w/ early adoption

New Standards and Modifications Effective 2013 and Beyond

Conceptual FrameworkConceptual Framework

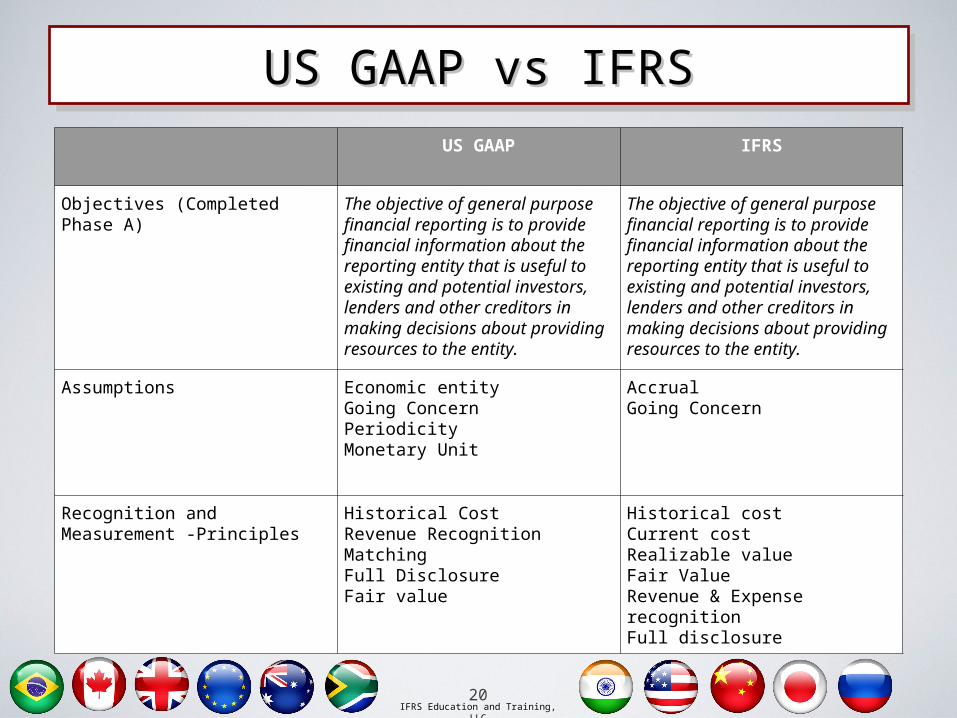

IFRS Education and Training, LLCIFRS Education and Training, LLC20

US GAAP IFRS

Objectives (Completed Phase A) The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity.

The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity.

Assumptions Economic entityGoing ConcernPeriodicityMonetary Unit

Accrual Going Concern

Recognition and Measurement -Principles

Historical CostRevenue RecognitionMatchingFull DisclosureFair value

Historical costCurrent costRealizable valueFair ValueRevenue & Expense recognitionFull disclosure

US GAAP vs IFRSUS GAAP vs IFRSUS GAAP vs IFRSUS GAAP vs IFRS

IFRS Education and Training, LLCIFRS Education and Training, LLC21

US GAAP IFRS

Qualitative Characteristics:

Fundamental and Enhancing Characteristics

Pervasive constraint

Completed Phase A

Relevance (FC) •predictive value•confirmatory value•materiality

Faithful representation (FC)•complete•neutral•free of error

Comparability (EC)Verifiability (EC)Timeliness (EC)Understandability (EC)

Cost (PC)

Relevance (FC) •predictive value•confirmatory value•materiality

Faithful representation (FC)•complete•neutral•free of error

Comparability (EC)Verifiability (EC)Timeliness (EC)Understandability (EC)

Cost (PC)

US GAAP vs IFRSUS GAAP vs IFRSUS GAAP vs IFRSUS GAAP vs IFRS

IFRS Education and Training, LLCIFRS Education and Training, LLC22

US GAAP IFRS

Elements of Financial Statements

AssetsLiabilitiesEquityInvestment by ownersDistribution to ownersRevenuesExpensesGainsLossesComprehensive Income

AssetsLiabilitiesEquity

Capital maintenance (revaluation of assets)

Income (Revenues & gains)

Expenses (expenses & losses)

US GAAP vs IFRSUS GAAP vs IFRSUS GAAP vs IFRSUS GAAP vs IFRS

Financial Statement PresentationFinancial Statement PresentationIAS 1 IAS 1

1. Statement of Financial Position

2. Statement of Comprehensive Income

3. Statement of Changes in Equity

4. Statement of Cash Flows

5. Notes to the Financial Statements

Complete Set of Financial StatementsComplete Set of Financial StatementsComplete Set of Financial StatementsComplete Set of Financial Statements

IAS 1 requires an entity to present a statement of financial position as at the beginning of the earliest comparative period in a complete set of financial statements when the entity applies an accounting policy retrospectively or makes a retrospective restatement, as defined in IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors, or when the entity reclassifies items in the financial statements.

IAS 1: Presentation of Financial Statements

US GAAP IFRS

Financial Periods Required

No requirement. Public companies follow SEC rules.

Comparative information must be disclosed

Layout of Balance Sheet and Income Statement

No general requirement in accordance with specific layout. Public companies follow Regulation S-X

IAS 1 Presentation of Financial Statements does not prescribe but lists a minimum items

Presentation of debt as current vs. non-current in the balance sheet

Debt for which there is a covenant violation MAY be presented as non-current

Debt for which there is a covenant violation MUST be presented as current

DifferencesDifferencesDifferencesDifferences

US GAAP IFRS

Deferred Taxes

Deferred taxes are presented as current or non-current based on the nature of the related asset or liability

Deferred taxes are reported as non-current

Expense classificationSEC registrants are required to present based on function.

Entities may present expenses based on either function or nature

Extraordinary ItemsRestricted to items that are both unusual and infrequent

Prohibited

Differences from US GAAPDifferences from US GAAPDifferences from US GAAPDifferences from US GAAP

IFRS are more prescriptive in terms of the specific line items, headings, and subtotals that must be presented.

IFRS requires the presentation of a classified balance sheet, with separate sections for current and non-current assets as well as current and non-current liabilities.

Under IFRS, presentation in order of increasing liquidity and decreasing liquidity are both common in practice.

Statement of Financial PositionStatement of Financial PositionStatement of Financial PositionStatement of Financial Position

An entity shall present all items of income and expense recognised in a period:

• In a single statement of comprehensive income, or

• In two statements: a statement displaying components of profit or loss and a second statement beginning with profit or loss and displaying components of other comprehensive)

Statement of Comprehensive IncomeStatement of Comprehensive IncomeStatement of Comprehensive IncomeStatement of Comprehensive Income

Revenue XCost of sales (X)Gross profit XOther income XDistribution costs (X)Administrative expenses (X)Other expenses (X)Profit before tax X

Function of ExpenseFunction of ExpenseFunction of ExpenseFunction of Expense

Revenue XOther income XChanges in inventories of FG & WIP XRaw materials and consumables used X

Employee benefits expense XDepreciation and amortization expense X

Other expenses XTotal expenses (X)Profit before tax X

Nature of ExpenseNature of ExpenseNature of ExpenseNature of Expense

• Published in June 2011 and effective for reporting years beginning on or after July 1, 2012

• Retrospective application

• Statement of Profit and Loss and Other Comprehensive Income - not mandatory

• OCI section to present items classified and grouped by nature

• Must disclose income tax pending on each item

IAS 1: Presentation of OCI

• Individual IFRSs specify which gains and losses must be reported in OCI and whether these items must be reclassified.

• Reclassification - when gains or losses is recognized in one period and then recognized again in profit and loss in a later period.

• Some IFRS require reclassification from OCI (IAS 21 & IAS 39)

• Others prohibit reclassification from OCI (IAS 16, IAS 19, IFRS 9)

IAS 1: Presentation of OCI

Profit for the year x

Other Comprehensive Income

Items that will not be reclassified to P&L

Actuarial loss on defined benefit plan (X)

Income tax X (X)

Items that may be reclassified subsequently to to P&L

Cash flow hedges (X)

AVS financial assets X

Income tax (X) X

OCI for the year, net of tax X

Total OCI for the year X

Statement of P&L and OCI (example)

Statement of Changes in EquityStatement of Changes in EquityStatement of Changes in EquityStatement of Changes in Equity

Statement of Cash FlowsStatement of Cash FlowsStatement of Cash FlowsStatement of Cash Flows

Present information about the basis of preparation of the financial statements and the specific accounting policies used

Provide information that is not presented elsewhere in the financial statements, but is relevant to an understanding of any item.

Disclose the information required by IFRSs that is not presented elsewhere in the financial statements; and

• measurement basis used• management’s judgments and

assumptions

Notes to the Financial StatementsNotes to the Financial StatementsNotes to the Financial StatementsNotes to the Financial Statements

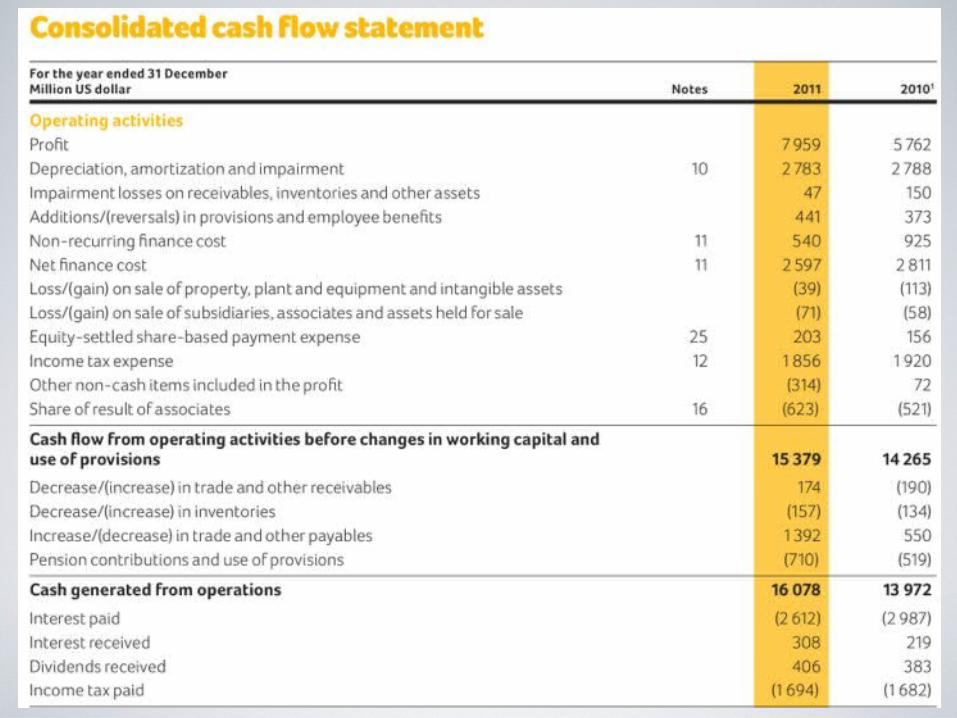

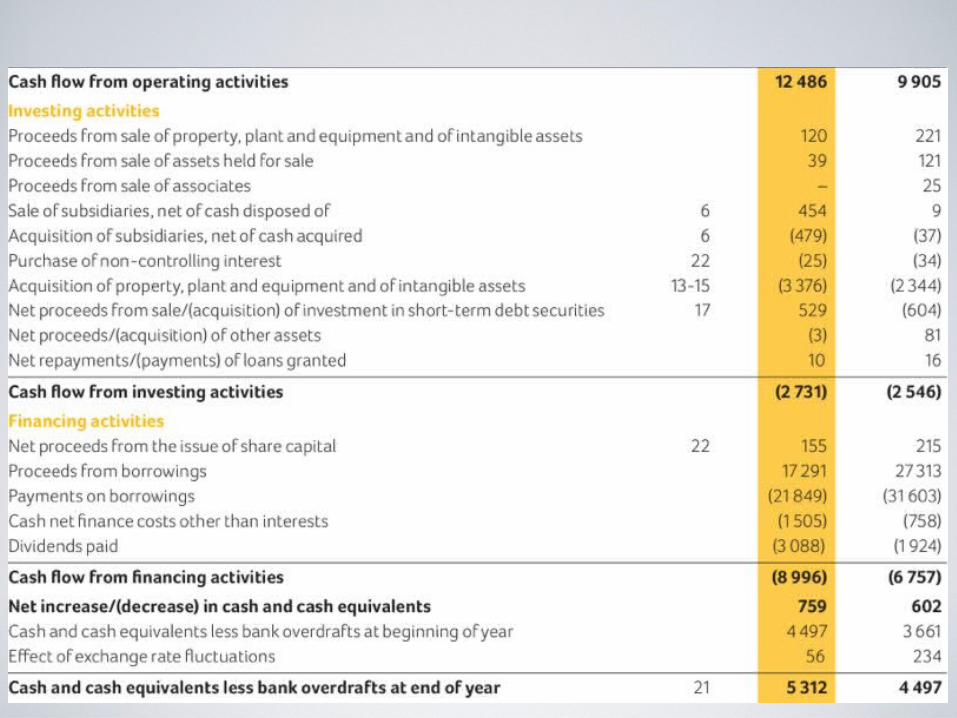

Heineken slide

Impairment Impairment IAS 36IAS 36

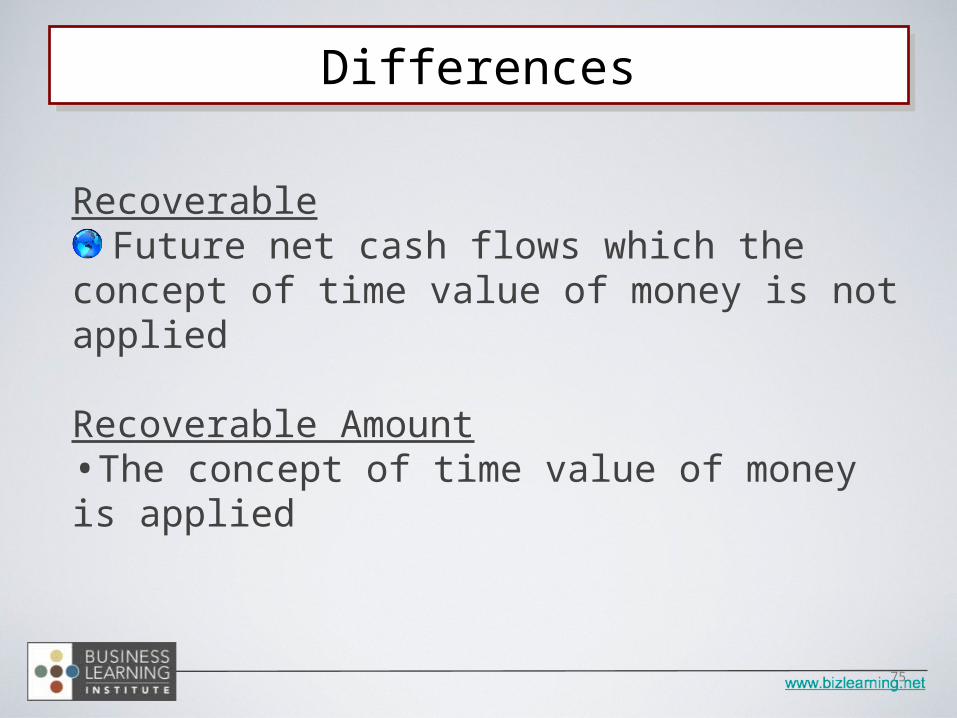

75

RecoverableFuture net cash flows which the concept of time

value of money is not applied

Recoverable Amount•The concept of time value of money is applied

DifferencesDifferences

Source: IFRS Partners

CA > RA Impairment

VIU FV - CS

Impairment TestingImpairment Testing

The carrying amount of a parcel of land is $1,400,000. The appraised fair value is $1,300,000. Costs to sell the asset would be 10% of the FV of the asset. The value in use (PV of discounted future cash flows) (VIU) was determined to be $1,250,000.

Fair Value $1,300,000Less: Costs to Sell 130,000 FV - Costs to Sell (a) $1,170,000Value in Use (b) $1,250,000

Recoverable Amount Higher or (a or b) $1,250,000

Carrying Amount (CA) $1,400,000Recoverable Amount (RA) $1,250,000Impairment (CA - RA) $150,000

Impairment ExampleImpairment Example

External sources of information•Asset’s market value has declined significantly.

•Significant changes with an adverse effect on the entity

•Market interest rates or other market rates of return on investments have increased during the period

•The carrying amount of the net assets of the entity is more than its market capitalisation.

Signs of ImpairmentSigns of Impairment

Internal sources of information•Evidence is available of obsolescence or physical damage of an asset.

•Significant changes with an adverse effect on the entity have taken place during the period

•Evidence is available from internal reporting that indicates that the economic performance of an asset is, or will be, worse than expected.

Signs of ImpairmentSigns of Impairment

Inventory Inventory IAS 2IAS 2

GAAP and IFRS are both based on the principle that the primary basis of accounting for inventory is cost.

“Assets held for sale in the ordinary course of business, in the process of production of such sale, or to be consumed in the production of goods and services.”

The cost of inventory includes all direct expenses in order to ready the inventory for sale.

Specific Identification, FIFO, Weighted Average, and the Retail Method are similar under both standards.

SimilaritiesSimilarities

US GAAP IFRS

LIFO is acceptable method LIFO is prohibited

Inventory is carried at LCM. Market is defined as current replacement cost as long as the market is not > NRV (ceiling) and is not less than net realizable value reduced by a normal sales margin (floor)

Inventory is carried at the lower of cost and net realizable value. (NRV = estimated selling price less estimated costs to complete and sell)

Any write-downs of inventory to LCM creates a new cost basis that can not be reversed.

Previously recognized impairment losses are reversed, up to the amount of the original impairment loss when the reason for the impairment no longer exists.

DifferencesDifferences

Tin Cup, Inc. sells only one product and the cost of the product is $5 per unit.

Example 1:NRV = $4.50Replacement Cost = $4.65NRV minus normal profit margin = $4.10Inventory would be valued at $4.50 under both US GAAP and IFRS

Example 2:NRV = $4.50Replacement Cost = $4.35NRV minus normal profit margin = $4.10

US GAAP = $4.35IFRS = $4.50

LCM vs. Lower of Cost and NRVLCM vs. Lower of Cost and NRV

The amount of any write-down of inventories to NRV and all losses of inventories shall be recognised as an expense

The amount of any reversal of any write-down of inventories, arising from an increase NRV, shall be recognised as a reduction COGS.

Inventory MeasurementInventory Measurement

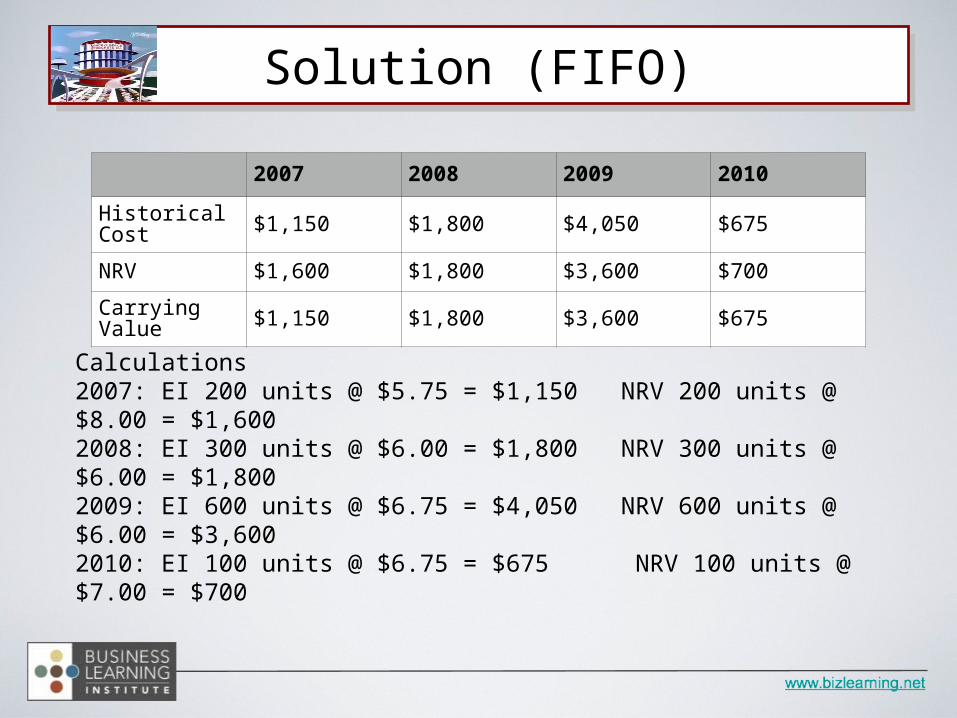

Spacely Space Sprockets, Inc. (SSSI) starts with no inventory in 20X7. The following occur:

2007, purchases 1,000 units for $5.75 and sells 800 units.2008, purchases 900 units for $6.00 and sells 800 units. 2009, purchases 1,100 units for $6.75 and sells 800 units2010, no purchases, sells 500 units

$ per unit at year end 2007 2008 2009 2010

Est. Selling $ $9.00 $7.00 $7.00 $8.00

Est. Cost to Complete and Sell

$1.00 $1.00 $1.00 $1.00

NRV $8.00 $6.00 $6.00 $7.00

ExampleExample

2007 2008 2009 2010

Historical Cost $1,150 $1,800 $4,050 $675

NRV $1,600 $1,800 $3,600 $700

Carrying Value $1,150 $1,800 $3,600 $675

Calculations2007: EI 200 units @ $5.75 = $1,150 NRV 200 units @ $8.00 = $1,6002008: EI 300 units @ $6.00 = $1,800 NRV 300 units @ $6.00 = $1,8002009: EI 600 units @ $6.75 = $4,050 NRV 600 units @ $6.00 = $3,6002010: EI 100 units @ $6.75 = $675 NRV 100 units @ $7.00 = $700

Solution (FIFO)Solution (FIFO)

InventoryInventory

5,750 4,600

1,1505,400 4,750

1,8007,425 5,175

4,050 4503,6000

600 75

675

EI 2007

EI 2008

EI 2009ADJEI 2009

ADJEI 2010

T-AccountT-Account

3,000

Property, Plant, and Property, Plant, and EquipmentEquipment

IAS 16IAS 16

“Tangible assets held for use that are expected to be used for more than one accounting period.”

The cost of the asset includes all costs incurred in order to get the asset ready for use – historical cost

Both methods do not allow the capitalization of start-up costs, G&A and overhead costs, or regular maintenance.

Depreciation of PP&E is required

Requires interest costs to be capitalized as part of the cost of the qualifying asset. (IAS 23 Revised in 2009)

SimilaritiesSimilarities

US GAAP IFRS

No annual review of the depreciation method required.

The depreciation method applied to an asset shall be reviewed at least at each financial year-end

Component depreciation is permitted but not common

Component depreciation is required if components of an asset have differing patterns of benefit

Revaluation is not permitted

Revaluation is a permitted alternative accounting election for an entire class of assets, requiring revaluation to fair value on a regular basis.

DifferencesDifferences

“An entity shall choose either the cost model or the revaluation model as its accounting policy and shall apply that policy to an entire class of property,

plant and equipment.”

Measurement After RecognitionMeasurement After Recognition

After recognition as an asset, an item of property, plant and equipment shall be

carried at its cost less any accumulated depreciation and any accumulated impairment losses.

Cost ModelCost Model

Fair Value

Revaluations shall be made with sufficient regularitysufficient regularity to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the end of the reporting period.“

Revaluation ModelRevaluation Model

The following are examples of separate classes:

LandLand and buildingsMachineryShipsAircraftMotor vehiclesFurniture and fixturesOffice equipment

Class of PPEClass of PPE

Revaluation Increases

Revaluation Decreases

0

Decreases > RSA 0 Balance = Loss on P&L

Revaluation Increase or DecreaseRevaluation Increase or Decrease

In 2011, ACME, Inc. purchased a parcel of land that is uses as a parking lot for its employees. ACME purchased this land for $1,200,000.

Land $1,200,000Cash $1,200,000

Revaluation ExampleRevaluation Example

In 2013, ACME decided to revalue its land in accordance with IAS 16. The company hired an appraiser who determined that the land had a fair market value of $1,300,000.

Land $100,000Revaluation Reserve (OCI) $100,000

Revaluation ExampleRevaluation Example

In 2015, ACME the market value of the land decreased by 15% $1,105,000 (FV $1,300,000 – $195,000)

Revaluation Reserve $100,000Revaluation Loss $95,000Land $195,000

LandLand

$1,200,000$1,200,000

$100,000$100,000

$1,300,000$1,300,000 $195,000$195,000

$1,105,000$1,105,000

Revaluation ReserveRevaluation Reserve

$100,000$100,000

$100,000$100,000

Revaluation ExampleRevaluation Example

Accumulated Depreciation for a Revalued Asset can either be:

Restated proportionally so that the carrying amount of the revalued asset equals it revalued amount, OR

•Eliminated against the gross carrying amount (net method)

Accumulated DepreciationAccumulated Depreciation

Scooby Doo, Inc. (SDI) purchased a building for $300,000 in January 2003. The building was being depreciated at $10,000 per year (S/L for 30 yrs). December 2007, SDI had recorded $50,000 of accumulated depreciation on the building and the book value of the building is $250,000. SDI, decided to revalue it assets and receive a fair value appraisal of $375,000 on the building as of January 1, 2008.

ExampleExample

Appraised value suggests a 50% increase over the historical cost book value.

The gross asset and accumulated depreciation should both be written up by that proportion.

Building ($300,000 X 50%) $150,000Accumulated Depreciation ($50,000 X 50%) $25,000Revaluation Surplus $125,000

Before AfterBuilding $300,000 $450,000A/D ($50,000) ($75,000)BV $250,000 $375,000

Proportional Method ExampleProportional Method Example

The accumulated depreciation account will be reduced to zero and the building will reflect the entire FMV appraisal

Building $75,000Accumulated Depreciation $50,000Revaluation Surplus $125,000

Before AfterBuilding $300,000 $375,000A/D $50,000 ($0)BV $250,000 $375,000

Net Method ExampleNet Method Example

LeasesLeasesIAS 17IAS 17

Recognition as either a finance lease or an operating lease.

The party that bears substantially all the risks and rewards of ownership of the leased property to recognize the leased asset and corresponding liability.

Measured at the lower of the PV of the minimum lease payments or the fair value of the asset.

Criteria to help make the determination between a finance lease and an operating lease.

Lease contains a bargain purchase option.

The lease transfers ownership of the property to the lessee by the end of the lease term

LeasesLeases

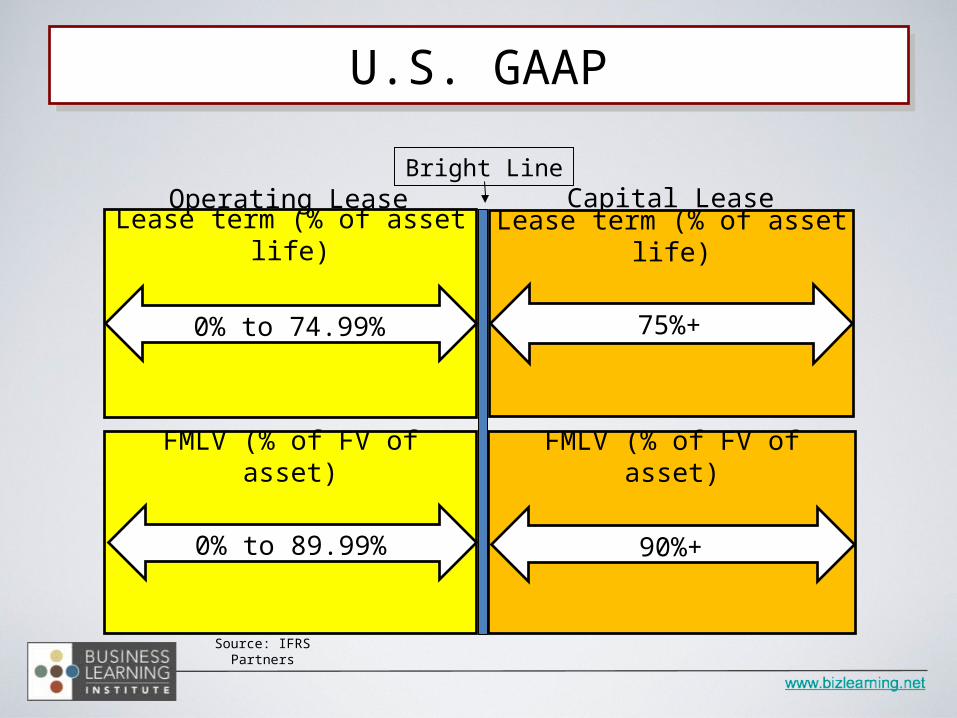

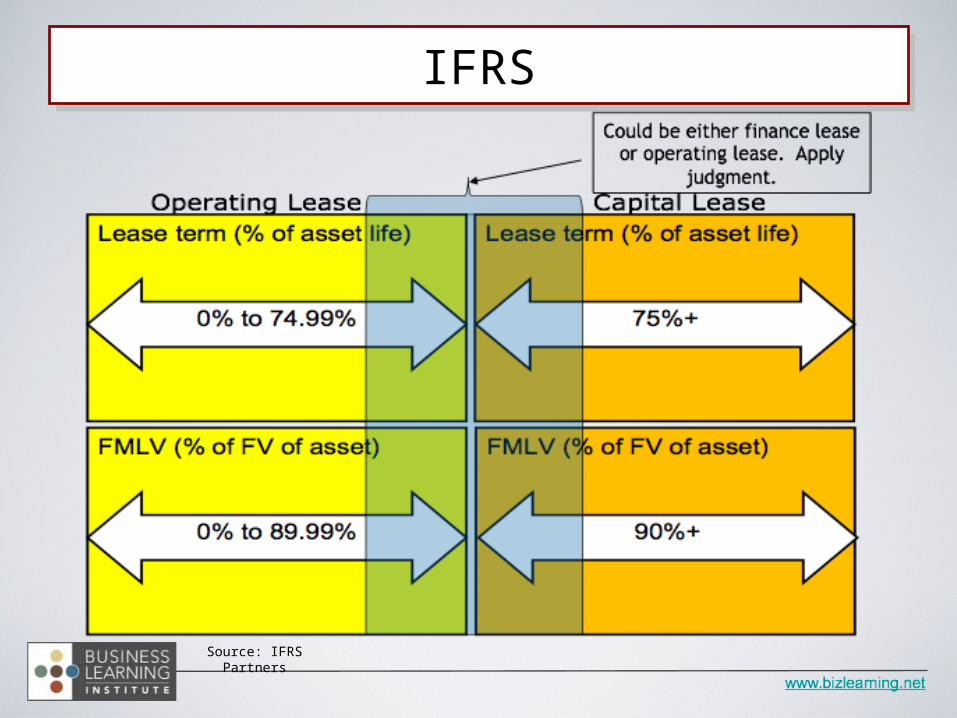

US GAAP IFRS

Requires a capital lease treatment if the lease term is equal to or greater than 75% of the assets economic life

Requires a finance lease treatment if the lease term is for the major part of the economic life of the asset even of the title is not transferred.

Requires a capital lease treatment if the PV of the minimum lease payments exceeds 90% of the assets fair value.

Requires a finance lease treatment if at the inception of the lease the present value of the minimum lease payments amounts to at least substantially all of the fair value of the leased asset

Current DifferencesCurrent Differences

Source: IFRS Partners

Lease term (% of asset life)Operating Lease

0% to 74.99%

FMLV (% of FV of asset)

0% to 89.99%

Capital LeaseLease term (% of asset life)

75%+

FMLV (% of FV of asset)

90%+

Bright Line

U.S. GAAPU.S. GAAP

Source: IFRS Partners

IFRSIFRS

Intangible AssetsIntangible AssetsIAS 38IAS 38

US GAAP IFRS

Development costs are expensed as incurred unless addressed by a separate standard. Development costs related to computer software developed for external use are capitalized once technological feasibility is established. Internal use software development, only those costs incurred during the application development stage may be capitalized.

Development costs are capitalized when technical and economic feasibility of a project can be demonstrated in accordance with specific criteria: demonstrating technical feasibility, intent to complete the asset, and ability to sell the asset in the future. There is no separate guidance addressing computer software development costs.

Differences

Goodwill Impairment- IFRS

The Standard permits: The annual impairment test for a cash-generating unit

(group of units) to which goodwill has been allocated to be performed at any time during an annual reporting period, provided the test is performed at the same time every year.

Different cash-generating units (groups of units) to be tested for impairment at different times.

A cash-generating unit is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or groups of assets

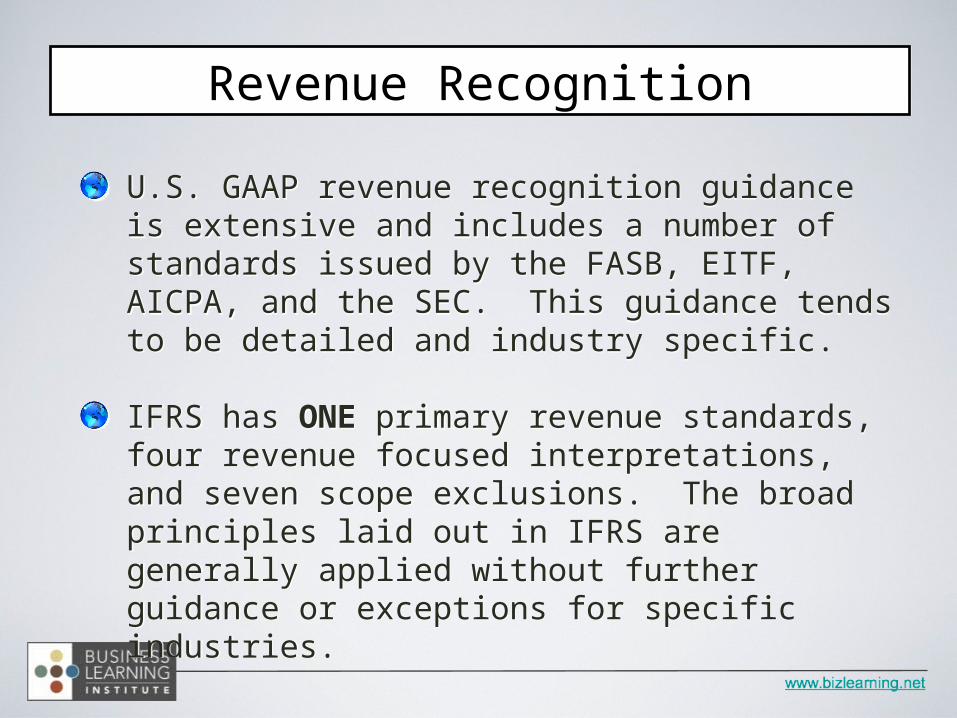

Revenue RecognitionRevenue RecognitionIAS 18IAS 18

Revenue Recognition

U.S. GAAP revenue recognition guidance is extensive and includes a number of standards issued by the FASB, EITF, AICPA, and the SEC. This guidance tends to be detailed and industry specific.

IFRS has ONE primary revenue standards, four revenue focused interpretations, and seven scope exclusions. The broad principles laid out in IFRS are generally applied without further guidance or exceptions for specific industries.

U.S. GAAP revenue recognition guidance is extensive and includes a number of standards issued by the FASB, EITF, AICPA, and the SEC. This guidance tends to be detailed and industry specific.

IFRS has ONE primary revenue standards, four revenue focused interpretations, and seven scope exclusions. The broad principles laid out in IFRS are generally applied without further guidance or exceptions for specific industries.

First-time Adoption of International First-time Adoption of International Financial Reporting StandardsFinancial Reporting Standards

IFRS 1IFRS 1

Is transparent for users and comparable over all periods presented;

Provides a suitable starting point for accounting IFRSs and;

Can be generated at a cost that does not exceed the benefits to users

ObjectiveObjectiveObjectiveObjective

An entity shall apply this IFRS in:

•Its first IFRS financial statements; and

•Each interim financial, if any, that presents under IAS 34 Interim Financial Reporting for part of the period covered by its first IFRS financial statements.

•There must be an explicit and unreserved statement of compliance with IFRSs in the first set of IFRS prepared financial statements.

ScopeScopeScopeScope

There is full retrospective application of all IFRS standards in effect as of the closing of the balance sheet date (reporting date) to a company’s first IFRS statements.

Key PrincipleKey PrincipleKey PrincipleKey Principle

IFRS 1 requires companies to:1.Identify the first IFRS financial statements2.Prepare an opening statement of financial position at the date of transition to IFRS3.Select accounting policies that comply with IFRS, and those policies retrospectively to all periods presented4.Consider whether to apply any of the 20 optional exemptions and four short-term exemptions from retrospective application. 5.Apply the seven mandatory exemptions from retrospective application.6.Make extensive disclosures to explain the transition.

First Set of IFRS Financial StatementsFirst Set of IFRS Financial StatementsFirst Set of IFRS Financial StatementsFirst Set of IFRS Financial Statements

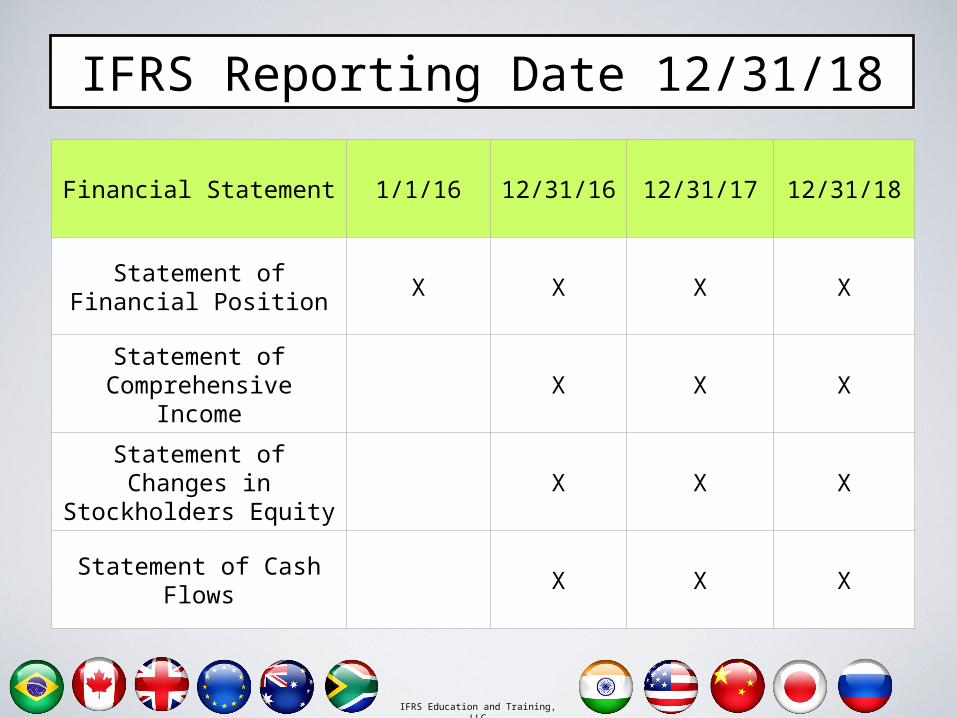

Transition date is identified as the beginning of the earliest period for which full comparative information is presented in accordance with IFRS.

Reporting date is defined as the closing balance sheet for the first IFRS statements.

Important DatesImportant DatesImportant DatesImportant Dates

IFRS Education and Training, LLCIFRS Education and Training, LLC

Financial Statement 1/1/16 12/31/16 12/31/17 12/31/18

Statement of Financial Position

X X X X

Statement of Comprehensive Income

X X X

Statement of Changes in Stockholders Equity

X X X

Statement of Cash Flows X X X

IFRS Reporting Date 12/31/18

An entity shall, in its opening IFRS statement of financial position: Recognise all assets and liabilities whose recognition is required by IFRSs; Not recognise items as assets or liabilities if IFRSs do not permit such recognition; Reclassify items that it recognised in accordance with previous GAAP as one type of asset, liability or component of equity, but are a different type of asset, liability or component of equity in accordance with IFRSs; and Apply IFRSs in measuring all recognised assets and liabilities.

Opening IFRS Statement of Financial Opening IFRS Statement of Financial PositionPosition

Opening IFRS Statement of Financial Opening IFRS Statement of Financial PositionPosition

The Board has identified 20 optional exemptions, 4 short-term exemptions,

and 7 mandatory exemptions in order to provide companies some relief from the

cost of full retrospective application.

Cost Benefit ReliefCost Benefit ReliefCost Benefit ReliefCost Benefit Relief

1. Business Combinations2. Share-based payment transactions3. Insurance contracts4. Fair Value Deemed as cost5. Leases6. Cumulative translation differences7. Investments in subsidiaries, jointly controlled

entities, and associates8. Assets and liabilities of subsidiaries, associates,

and joint ventures9. Compound financial instruments

20 Optional Exemptions20 Optional Exemptions20 Optional Exemptions20 Optional Exemptions

10.Designation of previously recognized financial instruments

11.Assets and liabilities measured at fair value12.Fair value measurement of financial assets or financial

liabilities at initial recognition13.Decommissioning liabilities included in the cost of

property, plant, and equipment14.Financial assets or intangible assets accounted for in

accordance with IFRIC 12, Service Concession Arrangements

15.Borrowing costs16.Transfer of assets from customers17.Extinguishing financial liabilities with equity instruments18.Hyperinflation19.Joint arrangements and impairment test20.Stripping costs in the production phase of a surface mine

20 Optional Exemptions20 Optional Exemptions20 Optional Exemptions20 Optional Exemptions

1. Certain first-time adopters can avail themselves from the requirement to restate comparative information for IFRS 9

2. Entities that choose not to comply with IFRS 7 and IFRS 9 in their first year of transition

3. Use of the IFRS 7 transition provisions for financial instrument disclosures

4. Use of the IAS 19 transition provisions for financial instrument disclosures

Short-term Exemptions from IFRSsShort-term Exemptions from IFRSsShort-term Exemptions from IFRSsShort-term Exemptions from IFRSs

1. Estimates 2. Financial assets and financial

liabilities derecognition;3. Hedge accounting;4. Non-controlling interests;5. Classification and measurement of

financial assets;6. Embedded derivatives; and7. Government loans.

Seven Mandatory ExemptionsSeven Mandatory ExemptionsSeven Mandatory ExemptionsSeven Mandatory Exemptions

2009

IFRS for SME’s

6

IFRS for SMEIFRS for SME’’ssIFRS for SMEIFRS for SME’’ss

The AICPA's governing Council on May 18, 2008

Amended Rules 202 & 203 of the Code of Professional Conduct to recognize the IASB as an accounting standard setter and allow a member to express an opinion on financial statements that are prepared using IFRS or IFRS for SME’s as promulgated by the IASB

This gives U.S. private companies the choice whether to adopt IFRS for SME’s.

AICPAAICPAAICPAAICPA

IFRS for SMEs is a self-contained standard of about 230 pages tailored for the needs and capabilities of smaller businesses.2nd Half of 2012 begin reviewing IFRS for SME’s (update)ED mid 2013Final amendments by 1st half 2014Effective date by 20154 - 5 year stable platform

Issued July 2009Issued July 2009Issued July 2009Issued July 2009

An SMEs is defined by the IASB as entities that:•Do not have public accountability, but•Do publish general purpose financial statements for external users.

The breadth of the definition depends on the words “public accountability”

Definition of SMEDefinition of SMEDefinition of SMEDefinition of SME

For purposes of the SME standard, an entity has public accountability if it meets either of the following two criteria:

•Debt or equity instruments are traded or going to be traded in a public market,.

•Entity holds assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses

Public AccountabilityPublic AccountabilityPublic AccountabilityPublic Accountability

Section 1: Small and Medium-Sized Entities Section 2: Concepts and Pervasive Principles Section 3: Financial Statement Presentation Section 4: Statement of Financial Position Section 5: Statement of C-Income and Income Statement Section 6: Statement of Changes in Equity and Statement of Income and Retained Earnings Section 7: Statement of Cash Flows Section 8: Notes to the Financial Statements Section 9: Consolidated and Separate Financial StatementsSection 10: Accounting Policies, Estimates and Errors Section 11: Basic Financial Instruments

35 Sections35 Sections35 Sections35 Sections

Section 12: Other Financial Instruments Issues Section 13: Inventories Section 14: Investments in Associates Section 15: Investments in Joint Ventures Section 16: Investment Property Section 17: Property, Plant and Equipment Section 18: Intangible Assets Other Than Goodwill Section 19: Business Combinations and Goodwill Section 20: Leases Section 21: Provisions and Contingencies Section 22: Liabilities and Equity Section 23: Revenue

35 Sections35 Sections35 Sections35 Sections

Section 24: Government Grants Section 25: Borrowing Costs Section 26: Share-Based Payment Section 27: Impairment of Assets Section 28: Employee Benefits Section 29: Income Tax Section 30: Foreign Currency Translation Section 31: Hyperinflation Section 32: Events after the End of the Reporting Period Section 33: Related Party Disclosures Section 34: Specialized Activities Section 35: Transition to the IFRS for SMEs

35 Sections35 Sections35 Sections35 Sections

Biggest challenges may be a cultural one

Requires more judgment and less reliance on detailed rules and “bright lines”

Companies will be required to understand base principles and objectives, how judgments are made, and how they are applied

IFRS for SMEIFRS for SME’’ssIFRS for SMEIFRS for SME’’ss

The biggest impacts of the transition to IFRS may be in areas other than accounting, such as:•systems requirements,•controls,•training,•resources,•banking covenants,•legal agreements,•compensation arrangements, etc.

Impact of IFRS for SMEImpact of IFRS for SME’’ssImpact of IFRS for SMEImpact of IFRS for SME’’ss

AICPA-IFRS for SME – US GAAP comparison tool: Http://wiki.ifrs.com

Free download of SME standards:http://go.iasb.org/IFRSforSMEsDownload (3 PDFs) includes:•Standard•Illustrative financial statements and disclosure checklist•Basis for conclusions

ResourcesResourcesResourcesResources

Big Bang Theory Video

Peter A. Margaritis, CPA, CGMA [email protected]

614.668.2936

Twitter: @pmargaritisLinkedIn: http://www.linkedin.com/pub/peter-

margaritis-cpa-cgma-macc/2/273/13www.petermargaritis.com