Embed Size (px)

Citation preview

#cbizmhmwebinar 1

CBIZ & MHM Executive Education Series™

IAS 38: Accounting for Intangibles Under IFRS Marco Pulido July 16, 2015

#cbizmhmwebinar 2

About Us

• Together, CBIZ & MHM are a Top Ten accounting provider • Offices in most major markets • Tax, audit and attest* and advisory services • Over 2,900 professionals nationwide

A member of Kreston International A global network of independent accounting firms

#cbizmhmwebinar 3

Before We Get Started…

• To view this webinar in full screen mode, click on view options in the upper right hand corner.

• Click the Support tab for technical assistance.

• If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

#cbizmhmwebinar 4

CPE Credit

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar. External participants will receive their CPE certificate via email immediately following the webinar.

#cbizmhmwebinar 5

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

#cbizmhmwebinar 6

Presenter

Marco has over 15 years of experience in public accounting working

with U.S. GAAP, IFRS and other foreign accounting standards in the U.S.,

Europe and in Latin America with Big 4 accounting firms. He has

experience with SEC filers (foreign and domestic) and private companies.

Marco is a CPA certified in California and has IFRS certifications by the

Institute of Chartered Accountants in England and Wales (ICAEW) and

the American Institute of Certified Public Accountants (AICPA). Technical

accounting expertise includes the following industries: Retail,

Distribution & Manufacturing – Professional Services –

Construction/Real Estate – Technology – Energy (Oil & Gas) –

Agriculture.

310.268.2746 • [email protected]

Marco Pulido, CPA MHM Shareholder

#cbizmhmwebinar 7

Agenda

Principles of IAS 38

02

01

03

04

Criteria for Capitalization and Amortization

Requirements for Capitalization of Internally Generated Costs

Subsequent Valuation Models

05 Differences Between U.S. GAAP and IFRS

#cbizmhmwebinar 8

PRINCIPLES OF IAS 38

#cbizmhmwebinar 9

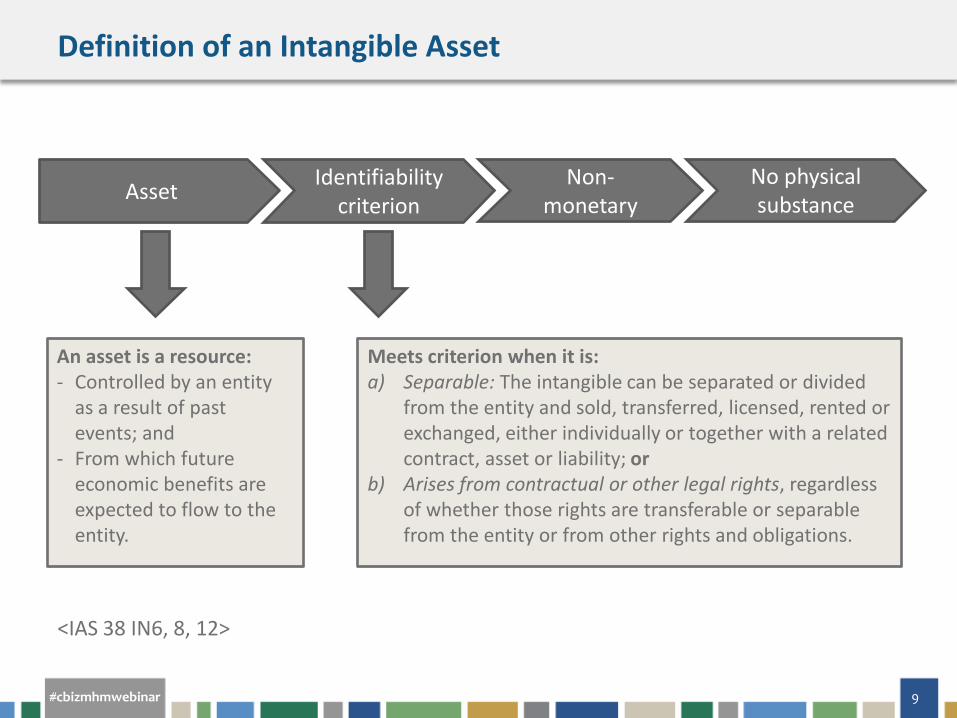

Definition of an Intangible Asset

<IAS 38 IN6, 8, 12>

Asset Identifiability criterion

Non-monetary

No physical substance

An asset is a resource: - Controlled by an entity

as a result of past events; and

- From which future economic benefits are expected to flow to the entity.

Meets criterion when it is: a) Separable: The intangible can be separated or divided

from the entity and sold, transferred, licensed, rented or exchanged, either individually or together with a related contract, asset or liability; or

b) Arises from contractual or other legal rights, regardless of whether those rights are transferable or separable from the entity or from other rights and obligations.

#cbizmhmwebinar 10

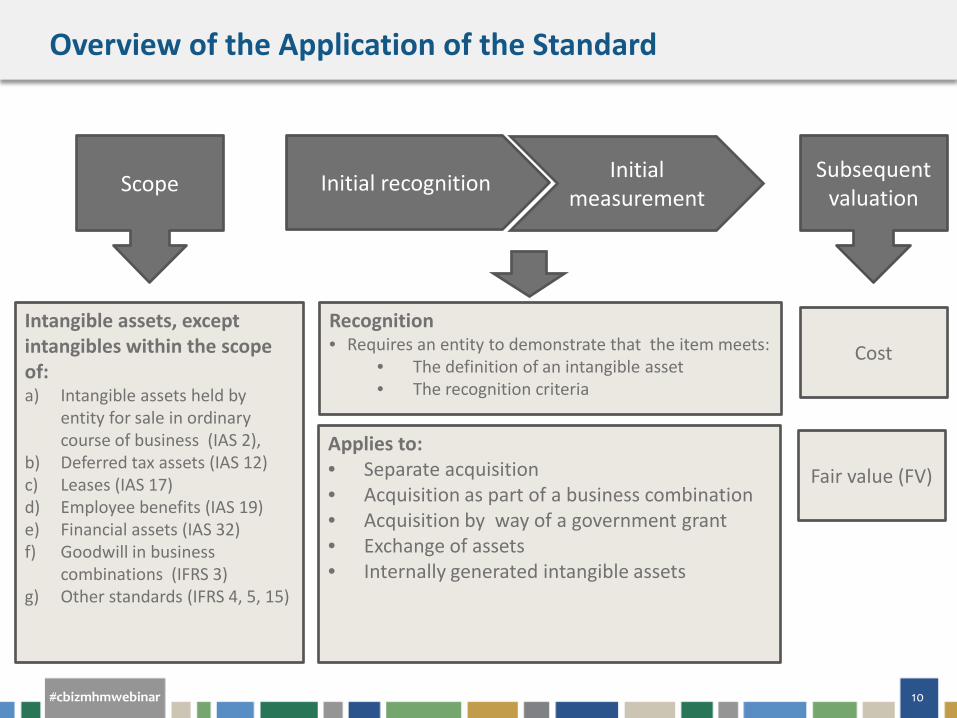

Scope Initial recognition Subsequent valuation

Initial measurement

Intangible assets, except intangibles within the scope of: a) Intangible assets held by

entity for sale in ordinary course of business (IAS 2),

b) Deferred tax assets (IAS 12) c) Leases (IAS 17) d) Employee benefits (IAS 19) e) Financial assets (IAS 32) f) Goodwill in business

combinations (IFRS 3) g) Other standards (IFRS 4, 5, 15)

Recognition • Requires an entity to demonstrate that the item meets:

• The definition of an intangible asset • The recognition criteria

Applies to: • Separate acquisition • Acquisition as part of a business combination • Acquisition by way of a government grant • Exchange of assets • Internally generated intangible assets

Cost

Fair value (FV)

Overview of the Application of the Standard

#cbizmhmwebinar 11

CRITERIA FOR CAPITALIZATION AND AMORTIZATION

#cbizmhmwebinar 12

No

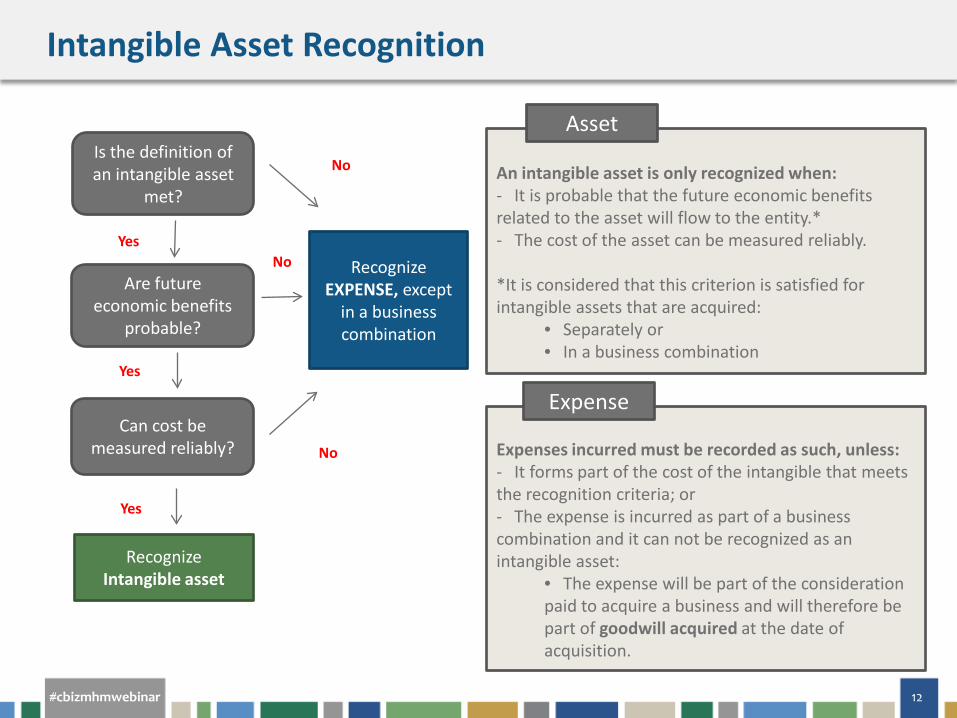

Intangible Asset Recognition

Is the definition of an intangible asset

met?

Are future economic benefits

probable?

Can cost be measured reliably?

Recognize Intangible asset

Recognize EXPENSE, except

in a business combination

An intangible asset is only recognized when: - It is probable that the future economic benefits related to the asset will flow to the entity.* - The cost of the asset can be measured reliably. *It is considered that this criterion is satisfied for intangible assets that are acquired:

• Separately or • In a business combination

Expenses incurred must be recorded as such, unless: - It forms part of the cost of the intangible that meets the recognition criteria; or - The expense is incurred as part of a business combination and it can not be recognized as an intangible asset:

• The expense will be part of the consideration paid to acquire a business and will therefore be part of goodwill acquired at the date of acquisition.

Expense

No

No

Yes

Yes

Yes

Asset

#cbizmhmwebinar 13

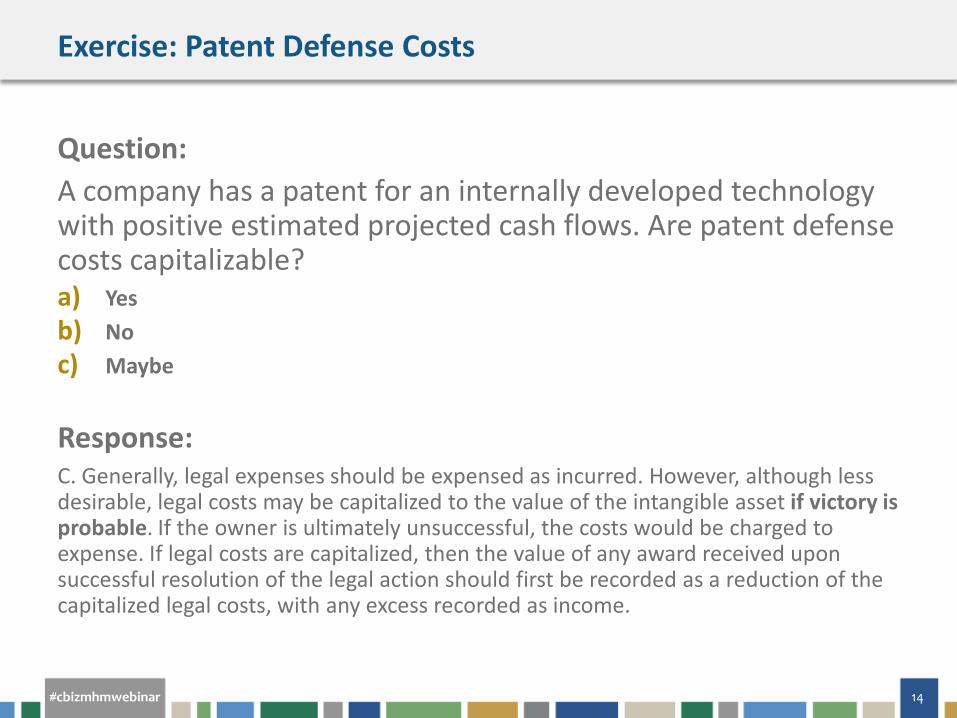

Exercise: Patent Defense Costs

Question: A company has a patent for an internally developed technology with positive estimated projected cash flows. Are patent defense costs capitalizable? a) Yes b) No c) Maybe

#cbizmhmwebinar 14

Exercise: Patent Defense Costs

Question: A company has a patent for an internally developed technology with positive estimated projected cash flows. Are patent defense costs capitalizable? a) Yes b) No c) Maybe

Response: C. Generally, legal expenses should be expensed as incurred. However, although less desirable, legal costs may be capitalized to the value of the intangible asset if victory is probable. If the owner is ultimately unsuccessful, the costs would be charged to expense. If legal costs are capitalized, then the value of any award received upon successful resolution of the legal action should first be recorded as a reduction of the capitalized legal costs, with any excess recorded as income.

#cbizmhmwebinar 15

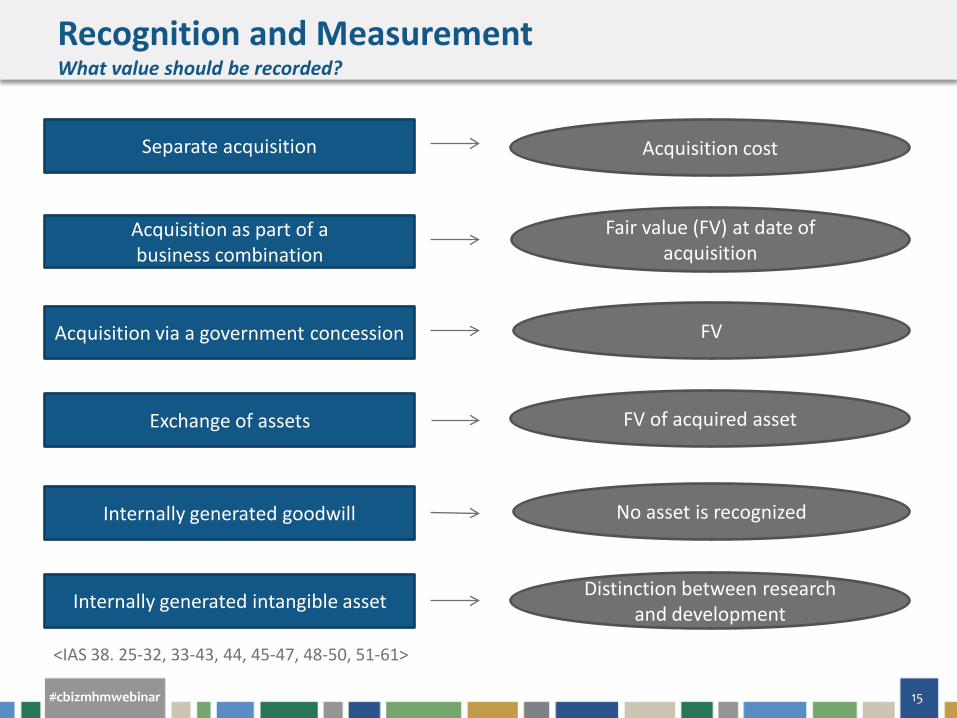

Recognition and Measurement What value should be recorded?

Separate acquisition

Acquisition as part of a business combination

Acquisition via a government concession

Exchange of assets

Internally generated goodwill

Internally generated intangible asset

Acquisition cost

Fair value (FV) at date of acquisition

FV

FV of acquired asset

No asset is recognized

Distinction between research and development

<IAS 38. 25-32, 33-43, 44, 45-47, 48-50, 51-61>

#cbizmhmwebinar 16

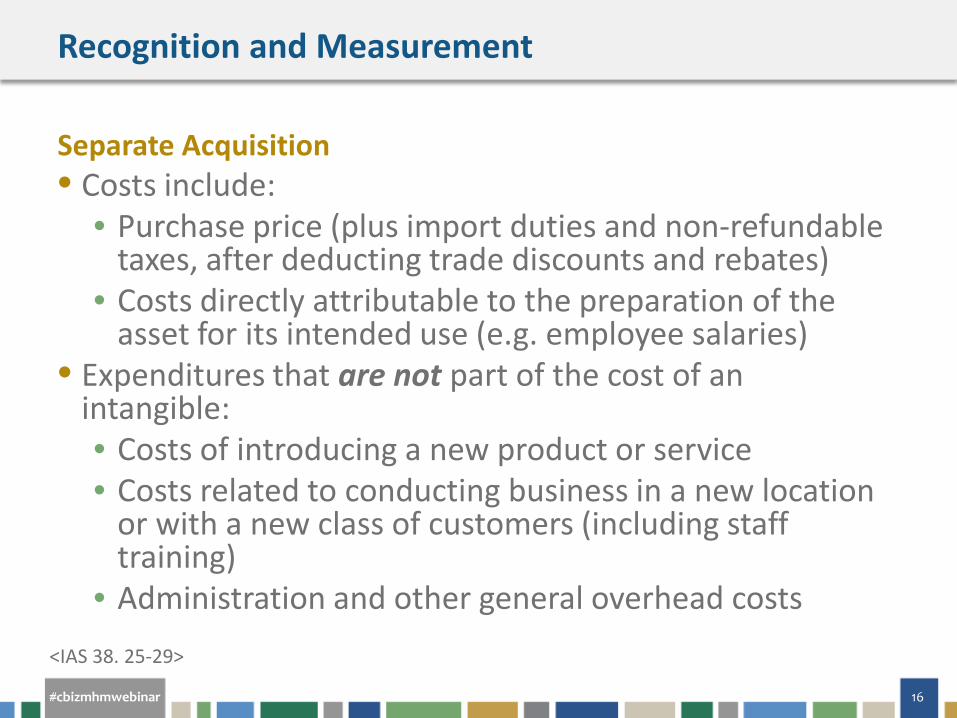

Recognition and Measurement

Separate Acquisition • Costs include:

• Purchase price (plus import duties and non-refundable taxes, after deducting trade discounts and rebates)

• Costs directly attributable to the preparation of the asset for its intended use (e.g. employee salaries)

• Expenditures that are not part of the cost of an intangible: • Costs of introducing a new product or service • Costs related to conducting business in a new location

or with a new class of customers (including staff training)

• Administration and other general overhead costs <IAS 38. 25-29>

#cbizmhmwebinar 17

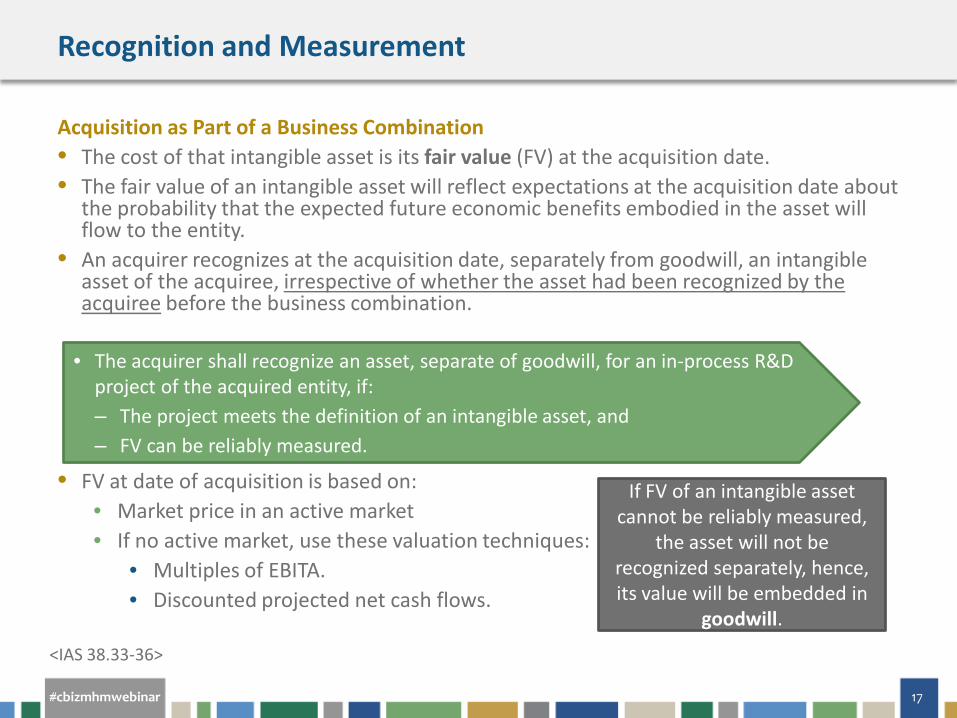

Recognition and Measurement

Acquisition as Part of a Business Combination • The cost of that intangible asset is its fair value (FV) at the acquisition date. • The fair value of an intangible asset will reflect expectations at the acquisition date about

the probability that the expected future economic benefits embodied in the asset will flow to the entity.

• An acquirer recognizes at the acquisition date, separately from goodwill, an intangible asset of the acquiree, irrespective of whether the asset had been recognized by the acquiree before the business combination.

• FV at date of acquisition is based on:

• Market price in an active market • If no active market, use these valuation techniques:

• Multiples of EBITA. • Discounted projected net cash flows.

• The acquirer shall recognize an asset, separate of goodwill, for an in-process R&D project of the acquired entity, if: ‒ The project meets the definition of an intangible asset, and ‒ FV can be reliably measured.

If FV of an intangible asset cannot be reliably measured,

the asset will not be recognized separately, hence, its value will be embedded in

goodwill.

<IAS 38.33-36>

#cbizmhmwebinar 18

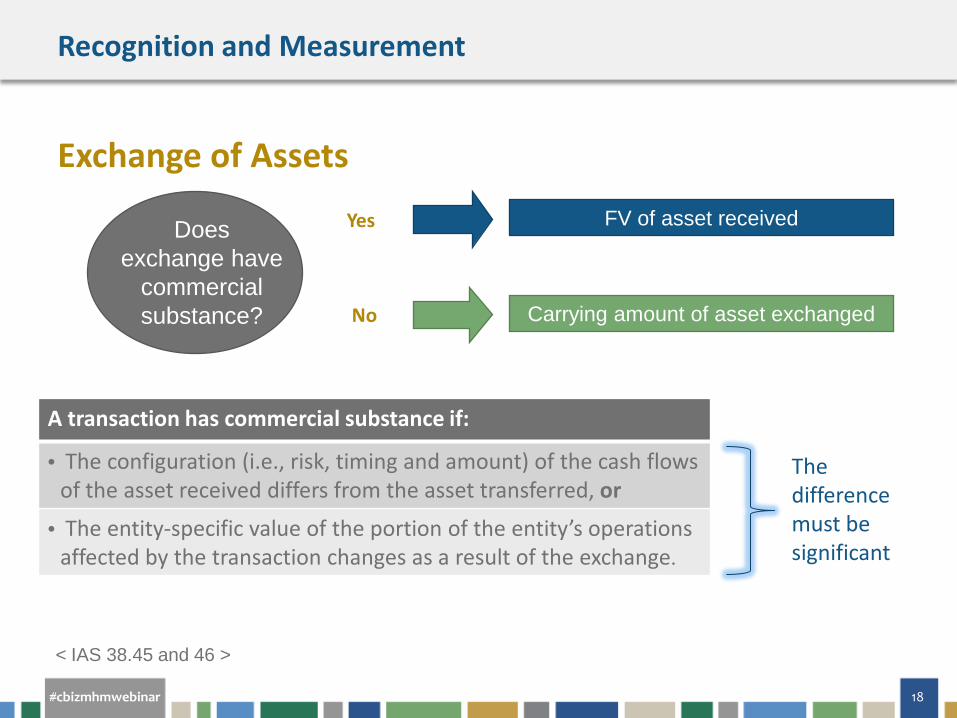

Recognition and Measurement

Exchange of Assets

Does exchange have

commercial substance?

Yes

No

FV of asset received

Carrying amount of asset exchanged

A transaction has commercial substance if:

• The configuration (i.e., risk, timing and amount) of the cash flows of the asset received differs from the asset transferred, or

• The entity-specific value of the portion of the entity’s operations affected by the transaction changes as a result of the exchange.

< IAS 38.45 and 46 >

The difference must be significant

#cbizmhmwebinar 19

REQUIREMENTS FOR CAPITALIZATION OF INTERNALLY GENERATED COSTS

#cbizmhmwebinar 20

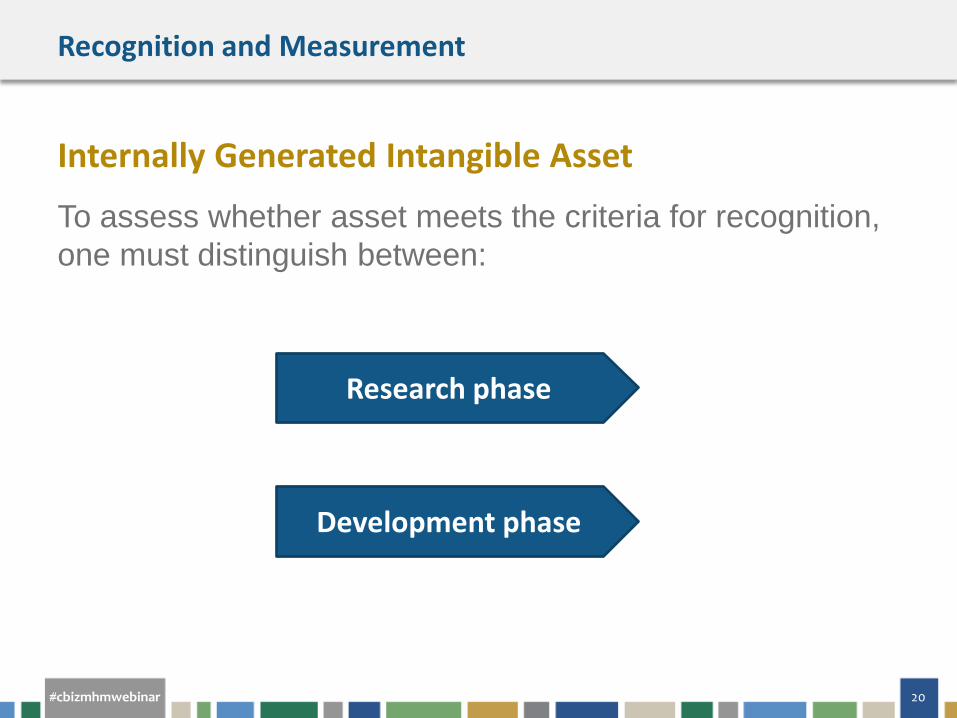

Recognition and Measurement

Internally Generated Intangible Asset

To assess whether asset meets the criteria for recognition, one must distinguish between:

Research phase

Development phase

#cbizmhmwebinar 21

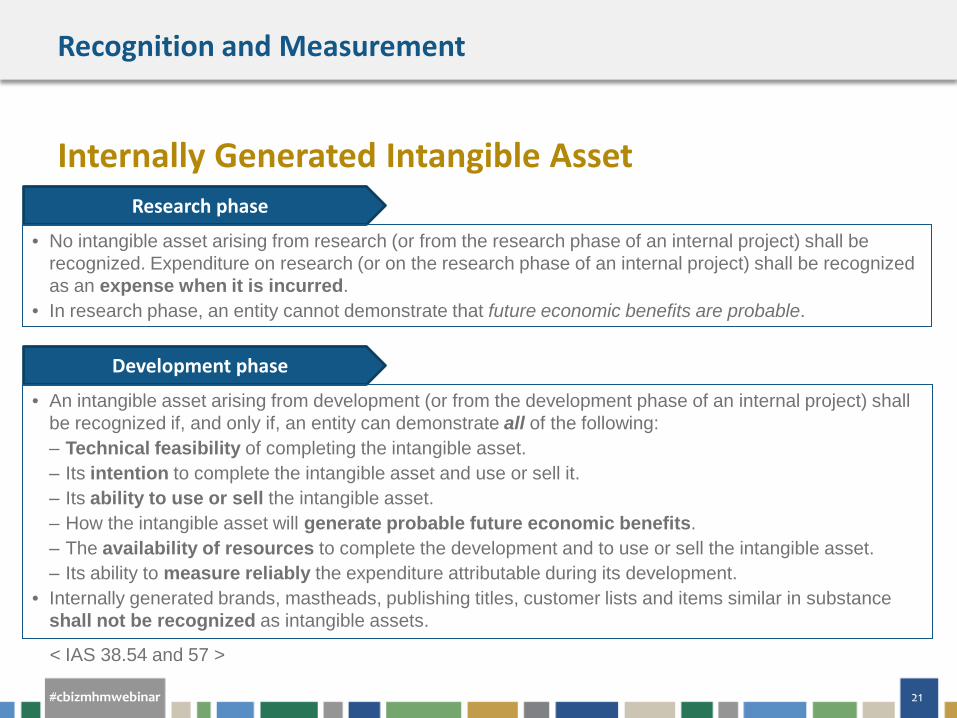

Recognition and Measurement

Internally Generated Intangible Asset Research phase

• No intangible asset arising from research (or from the research phase of an internal project) shall be recognized. Expenditure on research (or on the research phase of an internal project) shall be recognized as an expense when it is incurred.

• In research phase, an entity cannot demonstrate that future economic benefits are probable.

Development phase

• An intangible asset arising from development (or from the development phase of an internal project) shall be recognized if, and only if, an entity can demonstrate all of the following: ‒ Technical feasibility of completing the intangible asset. ‒ Its intention to complete the intangible asset and use or sell it. ‒ Its ability to use or sell the intangible asset. ‒ How the intangible asset will generate probable future economic benefits. ‒ The availability of resources to complete the development and to use or sell the intangible asset. ‒ Its ability to measure reliably the expenditure attributable during its development.

• Internally generated brands, mastheads, publishing titles, customer lists and items similar in substance shall not be recognized as intangible assets.

< IAS 38.54 and 57 >

#cbizmhmwebinar 22

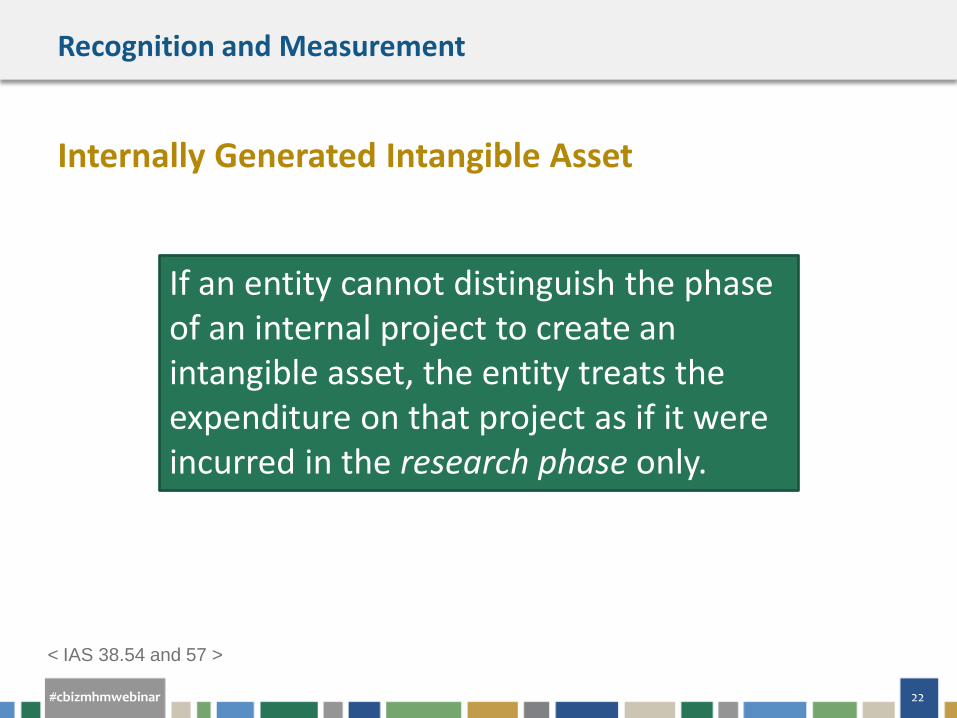

Recognition and Measurement

Internally Generated Intangible Asset

< IAS 38.54 and 57 >

If an entity cannot distinguish the phase of an internal project to create an intangible asset, the entity treats the expenditure on that project as if it were incurred in the research phase only.

#cbizmhmwebinar 23

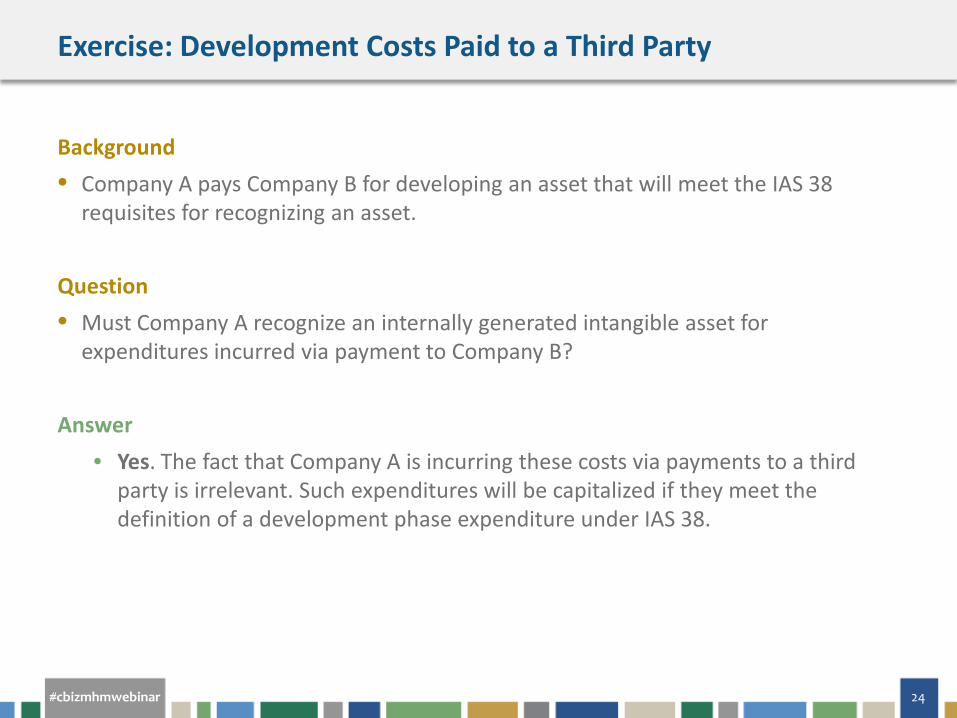

Exercise: Development Costs Paid to a Third Party

Background • Company A pays Company B for developing an asset that will meet the IAS 38

requisites for recognizing an asset. Question • Must Company A recognize an internally generated intangible asset for

expenditures incurred via payment to Company B?

#cbizmhmwebinar 24

Exercise: Development Costs Paid to a Third Party

Background • Company A pays Company B for developing an asset that will meet the IAS 38

requisites for recognizing an asset. Question • Must Company A recognize an internally generated intangible asset for

expenditures incurred via payment to Company B? Answer

• Yes. The fact that Company A is incurring these costs via payments to a third party is irrelevant. Such expenditures will be capitalized if they meet the definition of a development phase expenditure under IAS 38.

#cbizmhmwebinar 25

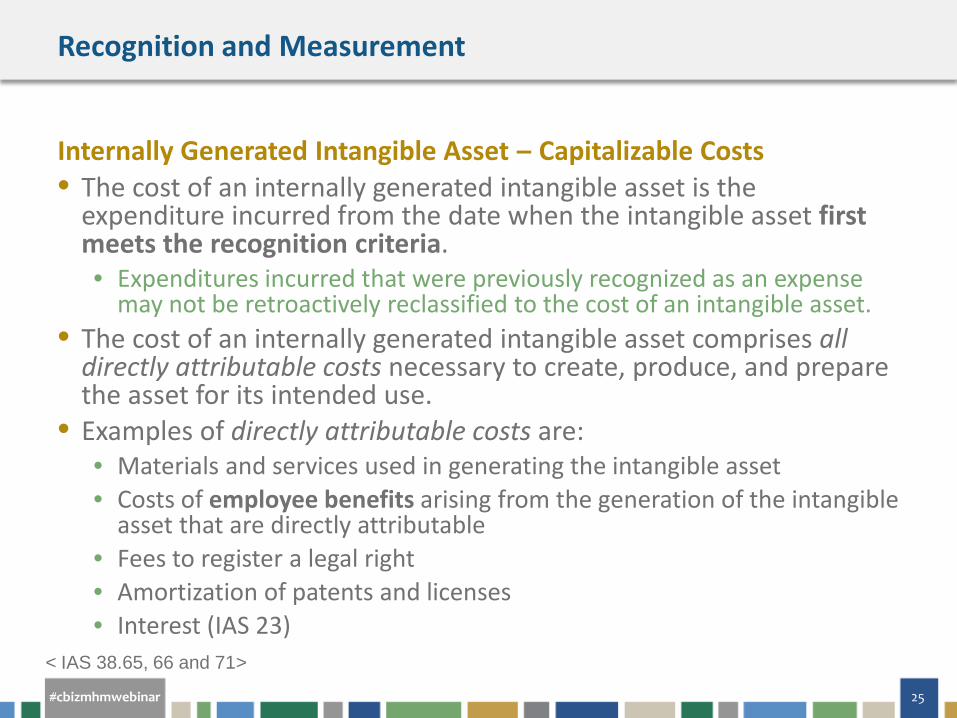

Recognition and Measurement

Internally Generated Intangible Asset – Capitalizable Costs • The cost of an internally generated intangible asset is the

expenditure incurred from the date when the intangible asset first meets the recognition criteria. • Expenditures incurred that were previously recognized as an expense

may not be retroactively reclassified to the cost of an intangible asset. • The cost of an internally generated intangible asset comprises all

directly attributable costs necessary to create, produce, and prepare the asset for its intended use.

• Examples of directly attributable costs are: • Materials and services used in generating the intangible asset • Costs of employee benefits arising from the generation of the intangible

asset that are directly attributable • Fees to register a legal right • Amortization of patents and licenses • Interest (IAS 23)

< IAS 38.65, 66 and 71>

#cbizmhmwebinar 26

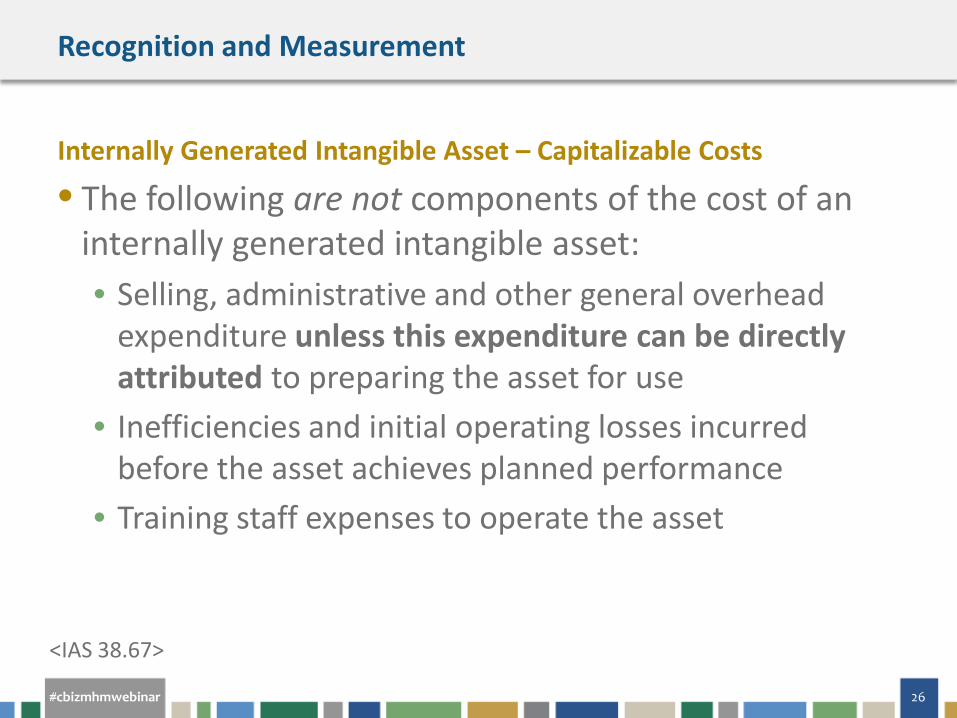

Recognition and Measurement

Internally Generated Intangible Asset – Capitalizable Costs

• The following are not components of the cost of an internally generated intangible asset: • Selling, administrative and other general overhead

expenditure unless this expenditure can be directly attributed to preparing the asset for use

• Inefficiencies and initial operating losses incurred before the asset achieves planned performance

• Training staff expenses to operate the asset

<IAS 38.67>

#cbizmhmwebinar 27

SUBSEQUENT VALUATION MODELS

#cbizmhmwebinar 28

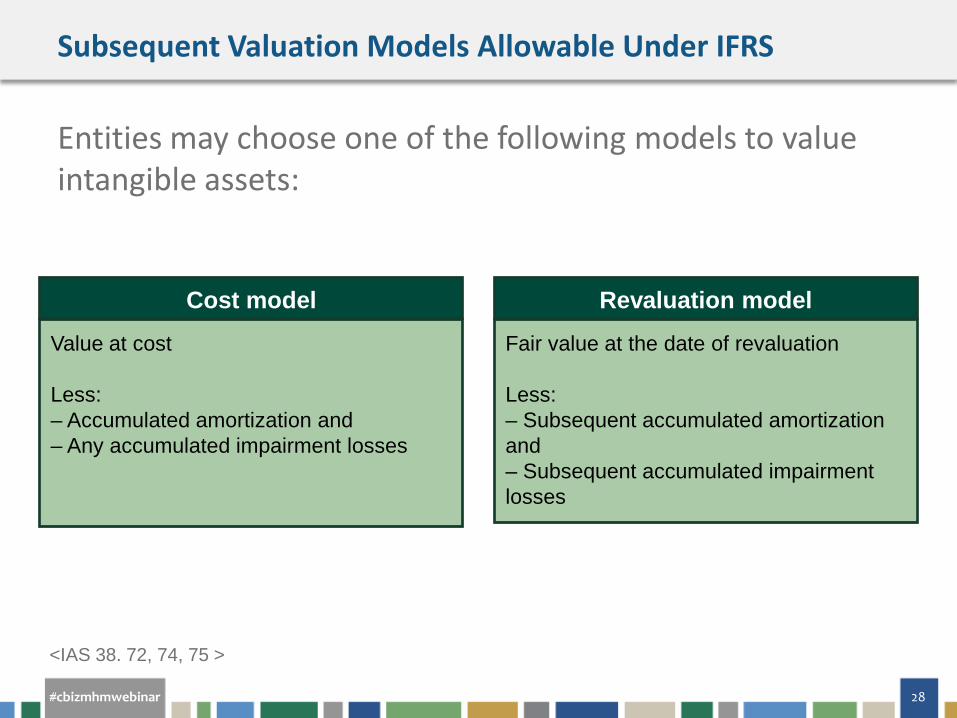

Subsequent Valuation Models Allowable Under IFRS

Entities may choose one of the following models to value intangible assets:

Cost model

Value at cost Less: – Accumulated amortization and – Any accumulated impairment losses

Revaluation model

Fair value at the date of revaluation Less: – Subsequent accumulated amortization and – Subsequent accumulated impairment losses

<IAS 38. 72, 74, 75 >

#cbizmhmwebinar 29

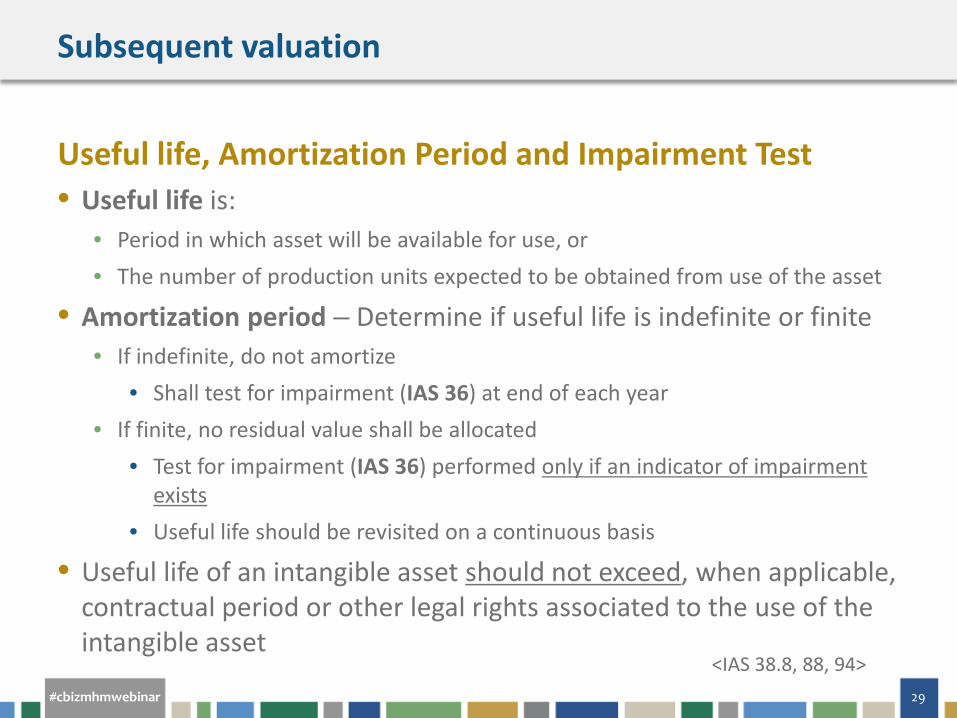

Subsequent valuation

Useful life, Amortization Period and Impairment Test • Useful life is:

• Period in which asset will be available for use, or • The number of production units expected to be obtained from use of the asset

• Amortization period – Determine if useful life is indefinite or finite • If indefinite, do not amortize

• Shall test for impairment (IAS 36) at end of each year • If finite, no residual value shall be allocated

• Test for impairment (IAS 36) performed only if an indicator of impairment exists

• Useful life should be revisited on a continuous basis

• Useful life of an intangible asset should not exceed, when applicable, contractual period or other legal rights associated to the use of the intangible asset

<IAS 38.8, 88, 94>

#cbizmhmwebinar 30

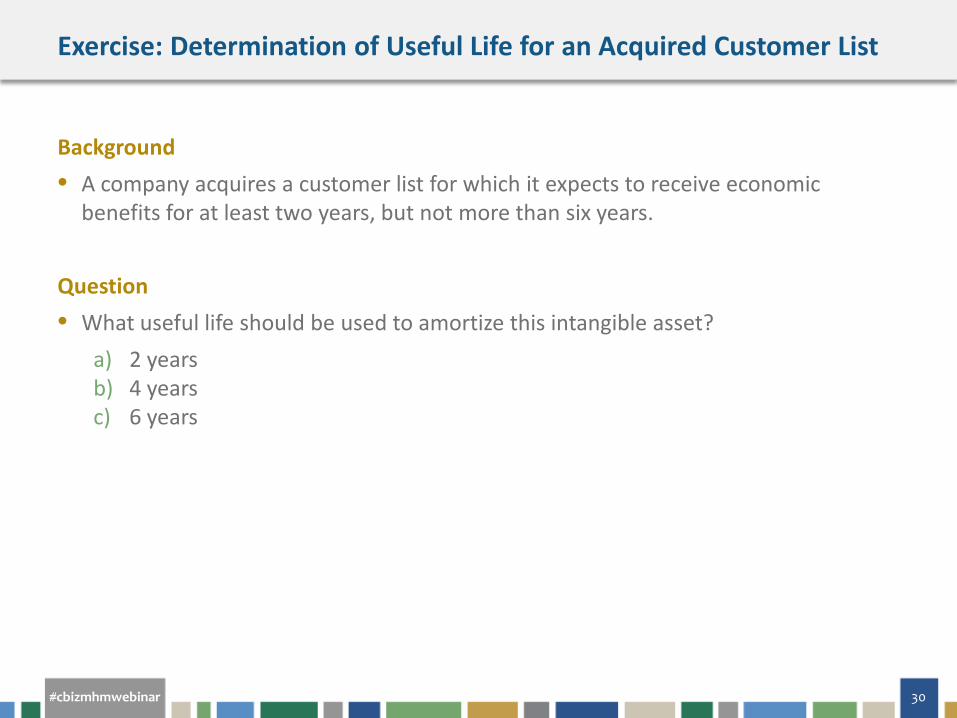

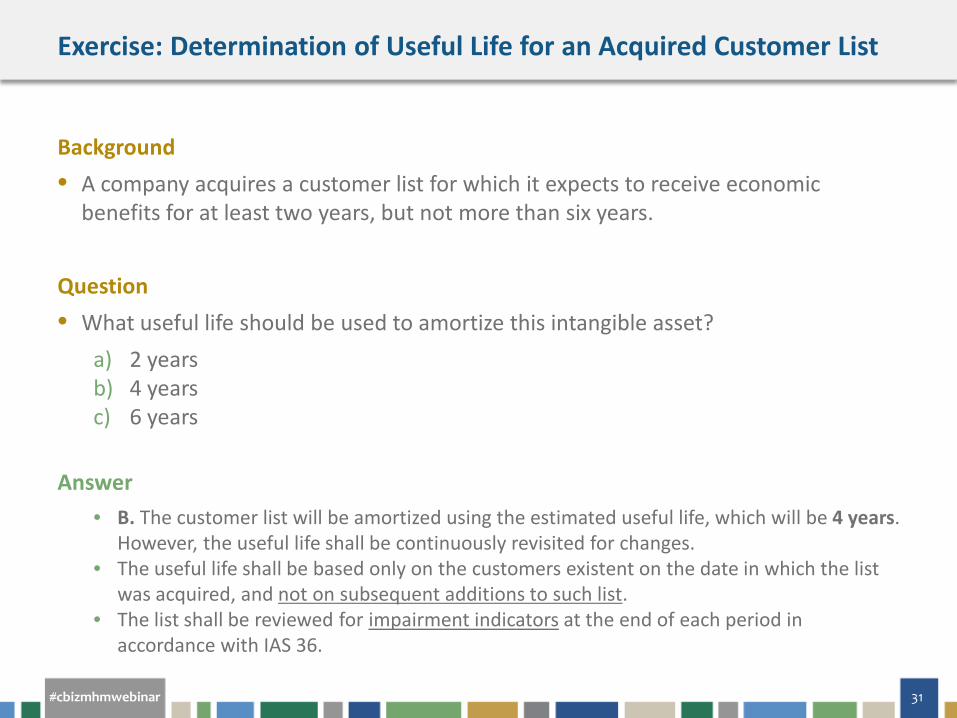

Exercise: Determination of Useful Life for an Acquired Customer List

Background • A company acquires a customer list for which it expects to receive economic

benefits for at least two years, but not more than six years.

Question • What useful life should be used to amortize this intangible asset?

a) 2 years b) 4 years c) 6 years

#cbizmhmwebinar 31

Exercise: Determination of Useful Life for an Acquired Customer List

Background • A company acquires a customer list for which it expects to receive economic

benefits for at least two years, but not more than six years.

Question • What useful life should be used to amortize this intangible asset?

a) 2 years b) 4 years c) 6 years

Answer

• B. The customer list will be amortized using the estimated useful life, which will be 4 years. However, the useful life shall be continuously revisited for changes.

• The useful life shall be based only on the customers existent on the date in which the list was acquired, and not on subsequent additions to such list.

• The list shall be reviewed for impairment indicators at the end of each period in accordance with IAS 36.

#cbizmhmwebinar 32

DIFFERENCES BETWEEN US GAAP AND IFRS

#cbizmhmwebinar 33

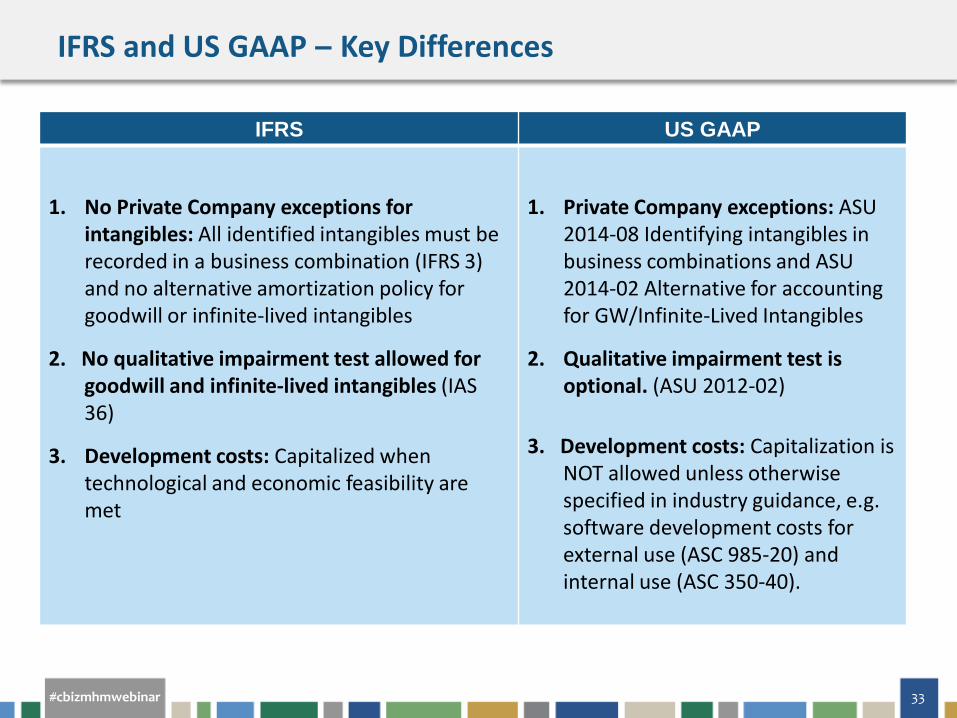

IFRS and US GAAP – Key Differences

IFRS US GAAP

1. No Private Company exceptions for intangibles: All identified intangibles must be recorded in a business combination (IFRS 3) and no alternative amortization policy for goodwill or infinite-lived intangibles

2. No qualitative impairment test allowed for goodwill and infinite-lived intangibles (IAS 36)

3. Development costs: Capitalized when technological and economic feasibility are met

1. Private Company exceptions: ASU 2014-08 Identifying intangibles in business combinations and ASU 2014-02 Alternative for accounting for GW/Infinite-Lived Intangibles

2. Qualitative impairment test is optional. (ASU 2012-02)

3. Development costs: Capitalization is NOT allowed unless otherwise specified in industry guidance, e.g. software development costs for external use (ASC 985-20) and internal use (ASC 350-40).

#cbizmhmwebinar 34

IFRS and US GAAP- Key Differences

IFRS U.S. GAAP

4. Advertising costs: Advertising and promotional

costs are expensed as incurred. A prepayment may be recognized as an asset only when payment for the goods or services is made in advance of receiving the services.

5. Revaluation: Revaluation to fair value of

intangible assets other than goodwill is permitted for a class of intangible assets.

4. Advertising costs: Advertising and

promotional costs are either expensed as incurred or expensed when the advertising takes place for the first time (policy choice).

5. Revaluation: Revaluation is not

permitted.

#cbizmhmwebinar 35

? QUESTIONS

#cbizmhmwebinar 36

If You Enjoyed This Webinar…

Upcoming courses: • 7/23 & 7/29: Revenue Recognition Updates for the Architecture, Engineering and

Construction Industry • 7/23: Unclaimed Property: What You Don’t Know Can Hurt You • 7/30, 8/4 & 8/5: Eye on Washington: Quarterly Business Tax Update, Q2 2015 • 8/19 & 9/17: Creative Ways to Structure Bonus Plans and Ensure Current Tax Deduction • 8/20 & 9/1: How to Make the Most Out of Derivatives and Hedging • 8/27 & 9/11: PPA Plan Restatement: Emerging Opportunities for Pre-Approved Plans • 9/24: The International Guide for Inventory Accounting – IAS 2 Inventories

Recent publications: • Are You Prepared for the ACA Reporting Requirements? • Technology & Life Sciences Report Now Available • Second Quarter Accounting and Financial Reporting Issues Update

#cbizmhmwebinar 37

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/ BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ

![IAS 38: Intangible Assets - riseschool.edu.pk · INTERNATIONAL ACCOUNTING STANDARD 38 INTANGIBLE ASSETS LO1: SCOPE AND DEFINITIONS Scope [Para 2,3] IAS 38 applies to all intangible](https://img.pdfslide.us/doc/110x75/60d26f77f152d20f46438525/ias-38-intangible-assets-international-accounting-standard-38-intangible-assets.jpg)