Embed Size (px)

Citation preview

How new VAT regulations will affects SMEs- and how to prepare

The Webinar

Me: Neil O’Brien

Owner of Accentis

Numbers geek

Data nerd

Fellow of The Institute of Chartered Accountants

Former CFO in two MBOs with successful exits

Advisor to SME Entrepreneurs

Virgin Start Up Mentor

The Why?

The EU want to crack down on tech companieswho use foreign based businesses to funnelsales and reduce their VAT liabilities.

The When

On 1 January 2015 the VAT rules for cross-border B2C supplies of ‘digital services’ (ie,Telecoms, broadcasting and electronic serviceswill change

From then, VAT must be accounted for (whenapplicable) in the member state where thecustomer normally lives, rather than where thesupplier of the service is established.

The What Not

Using the internet just to communicate or facilitate trading does not necessarily mean that you are supplying electronic services.

The following DO NOT fall under the new rules:– Supplying goods where ordering is processed

online

– Supplying physical books, newsletters or journals

– Education or professional courses where the content is delivered by a teacher over the internet

The What Is

From 1 January 2015, VAT only applies to services that are electronically supplied to EU consumers, such as:

• Images, ebooks or other digitised files (pdfetc)

• Music, films and games

• Online magazines

What does ‘electronically supplied’ mean

E-services which are automatically delivered over the internet where there is little or no human interaction.

E.g. when a sales is made online and the content downloads to a device or they receive an automated email containing the content OR a prepopulated email where the seller attaches the digital content and clicks ‘send

Examples of ‘digital services’

• Pfd’s automatically sent by the sellers system.

• Pdf’s automatically downloaded by the sellers system.

• Stock photographs available for automatic download.

• Pre recorded videos for online course (but not if the online course includes live support from a tutor)

• Link to online content sent by manual email

Current rules

If you buy a download ‘widget’ from the UK

You pay £10.

The UK Government collects £1.67 in VAT

The seller collects £8.33 in income

Current rules

If you buy a download ‘widget’ from Luxemburg

You pay £10.

The Luxemburg Government collects £1.30 in VAT

The seller collects £8.70 in income

The Consumer wins

UK (and other higher VAT countries) lose

Lower VAT rate countries win

The EU doesn’t like this because it creates unfair competition in a market that is based upon free

market economics

So

They changed the VAT laws…….

Welcome to the mess that is

VAT MOSS

The change?

In simplistic terms ‘digitally delivered’ goods and services are now deemed to ‘consumed’ based upon where the consumer is established rather than where the seller is established.

The supplier will now be selling in up to 28 different EU countries.

And have to register and account for VAT in each country that they sell to should they breach any countries VAT Registration Limits.

Why a headache

Because with 28 Countries you need to understand the VAT registration thresholds for each.

And also apply one of the 75 different VAT rates applicable.

And keep detailed records of each transaction for 10 years.

Frankly, it would be an admin overload and I’d even close my business!

I’m below the VAT registration threshold

You may well be below the UK registration threshold (£81k). But in the EU registration

thresholds are as low as

Who does it affect

Anyone who sells products or services that are

telecommunications, broadcasting and electronic services outside of

the UK.

How does it affect me?

You have a choice (Hurrah)

Come 1 Jan 2015, if YOU* sell ‘electronic services’ to consumers in the EU, you can either:

– Register and account for VAT in each member state that you sell to, or

– Register for VAT Mini One Stop Shop (MOSS)

* Some 3rd party platforms will handle the sale and be accountable for VAT themselves

Register in each state I sell to?

To keep it short, don’t bother going down this route unless you have a lot of sales to a particular territory.

It is simply too much of a logistical admin headache.

Register for MOSS

This is by far the simplest and easiest way to get around the headache.

But is causes a migraine…….

What is MOSS

MOSS is a UK system to make the accounting for an payment of EU VAT ‘simpler’.

Once you are registered, you ‘simply’ submit an MOSS VAT return every calendar quarter.

Easy, isn’t it…..

The downside

• To join MOSS you need to be VAT registered.

• You need a mechanism of validating where the customer ‘is established’.

• You need to keep this data for 10 years

HMRC have listened and made it ‘easier’

To join MOSS you need a VAT number but

YOU WILL NOT LOSE YOUR UK VAT REGISTRATION THRESHOLD

Proposed Guidance

HMRC will allow ‘business splitting’

What does this mean?

You will ‘only’ have to account for VAT on EU sales until you reach the UK VAT registration

limit.

You still need to validate where your customer is ‘established’

How?

Your ‘systems’ need to collate ‘two pieces of non-contradictory evidence’ to prove the location of the customer.

Here’s the “fun” part….

Presumptions for the location of the customer

Article 13a: ‘The place where a non taxable [not registered for VAT] legal person is established….shall be:

a. the place where the functions of its central administration are carried out, or

b. the place of any other establishment characterised by a sufficient degree of permanence and a suitable structure in terms of human and technical resources to enable it to receive and use the services supplied to it for its own needs’.

Means their home address

Presumptions for the location of the customer

Article 18:

‘Unless he has information to the contrary, the supplier may regard a customer established within the Community as a nontaxable person [not VAT registered] when he can demonstrate that the customer has not communicated his individual VAT identification number to him.

Means you charge them VAT unless they give you a VAT number

Presumptions for the location of the customer

Article 24a:

‘if the recipient of the service is needed for the service to be provided to him by that supplier, it shall be presumed that the customer is established, has his permanent address or usually resides at the place of that location and that the service is effectively used and enjoyed there.’

Meaning that for physical use of electronic services the place of supply is where the

customer uses that service

Presumptions for the location of the customer

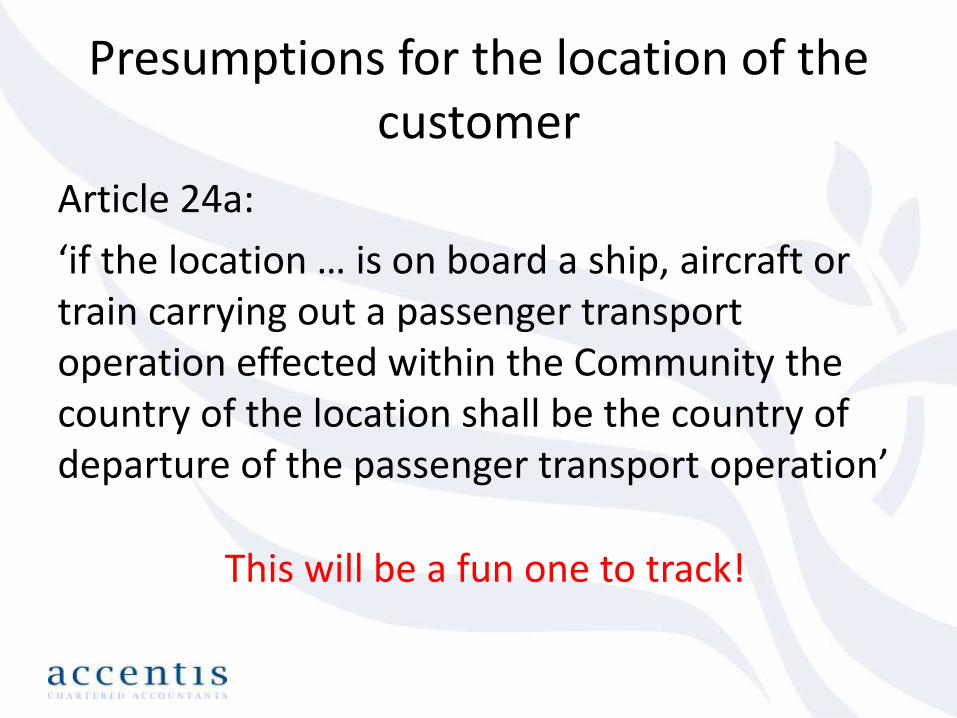

Article 24a:

‘if the location … is on board a ship, aircraft or train carrying out a passenger transport operation effected within the Community the country of the location shall be the country of departure of the passenger transport operation’

This will be a fun one to track!

Presumptions for the location of the customer

Article 24b: If the services are supplied:

– via a fixed land line, the place of supply is where that fixed land line is location.

– via a mobile network is the country identifier of the SIM code used to receive the services.

– Under circumstances other than the above the supply is based on two items of non-contradictory evidence.

The easiest non-contradictory location evidence to collect

• The billing address of the customer

• The IP address of the device used by the customer or any other method of geolocation.

• Bank location used to make the payment or billing address held by that bank

• Any other commercially relevant information

Registration for MOSS

1. You need a Government Gateway Account (register athttps://online.hmrc.gov.uk/registration)

2. You need to have a UK VAT number (register at https://online.hmrc.gov.uk/registration/newbusiness/business-allowed)

3. Once you have both of these, you can apply for MOSS via https://online.hmrc.gov.uk/registration/organisation/moss/introduction

VAT Return

You will need to complete a UK VAT return each quarter (even though it is a ‘nil’ return).

You will need to complete a MOSS VAT return each calendar quarter.

Tip: Ensure that you select the business activity entitled ‘Supplies of Digital Services (below UK VAT Threshold) under MOSS arrangements when you register for UK VAT. HMRC will then align your VAT periods so you can complete the UK and MOSS return at the same time.

MOSS Registration

• It is ‘open for business’, but clunky!

• You don’t have to register by 31 December 2014. You can wait until you sell your first digital cross border service and then register.

• You need to register by the 10th Day of the month following your first digital sale. – E.g. if you sell a product on 15 February 2015, you

have until 10 March 2015 to register your application.

Record Keeping

You need at least two corresponding pieces of information to evidence where each supply is made.

How?HMRC suggest asking customers to confirm either:

– Country– Billing address

Then validate this using your payment gateway Address Verification Service (AVS)

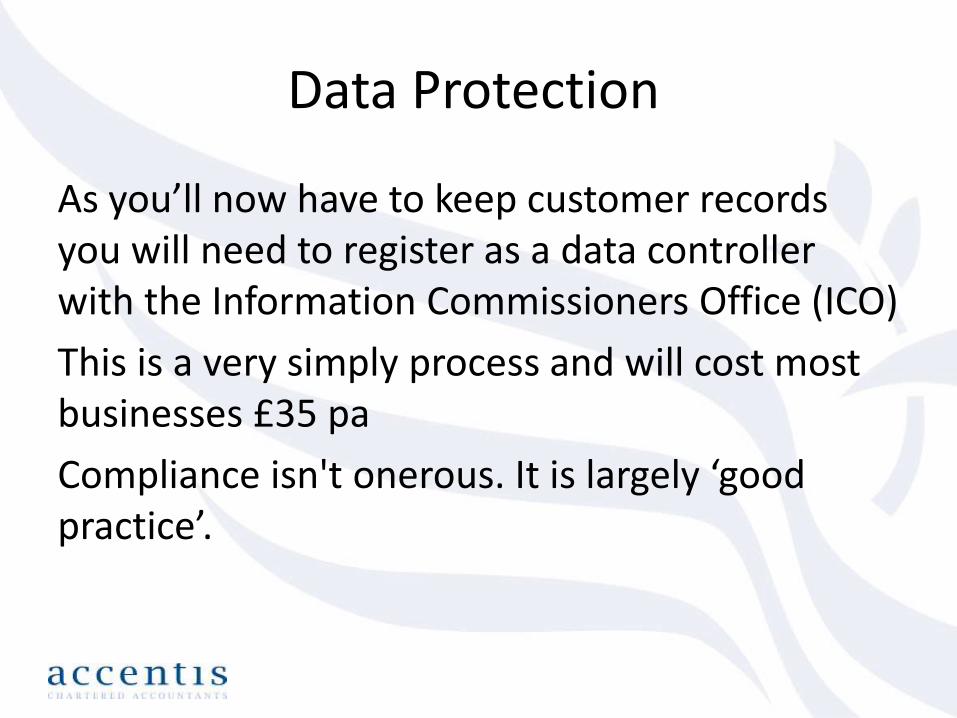

Data Protection

As you’ll now have to keep customer records you will need to register as a data controller with the Information Commissioners Office (ICO)

This is a very simply process and will cost most businesses £35 pa

Compliance isn't onerous. It is largely ‘good practice’.

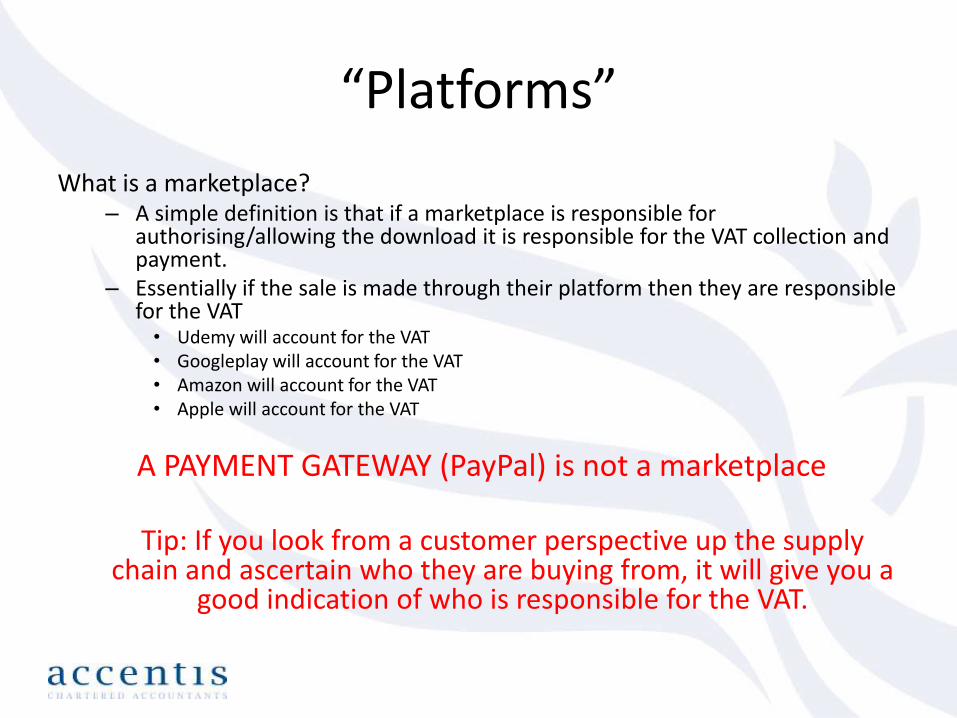

“Platforms”

What is a marketplace?– A simple definition is that if a marketplace is responsible for

authorising/allowing the download it is responsible for the VAT collection and payment.

– Essentially if the sale is made through their platform then they are responsible for the VAT• Udemy will account for the VAT• Googleplay will account for the VAT• Amazon will account for the VAT• Apple will account for the VAT

A PAYMENT GATEWAY (PayPal) is not a marketplace

Tip: If you look from a customer perspective up the supply chain and ascertain who they are buying from, it will give you a

good indication of who is responsible for the VAT.

I wont sell to the EU

Not so simple

There is a piece of EU legislation (the Services Directive) that says that we must not discriminate against EU consumers of services with regard to their nationality or country of residence.

BUT

we are permitted to treat consumers differently when we have an ‘objective reason’ to do so.

Objective reasons

Objective reasons could include:• additional costs incurred because of the distance involved

in delivery, • the technical characteristics of the services, • specific risks linked to rules and regulations in force in other

Member States, • different market conditions, such as pricing by different

competitors or lack of intellectual property rights.

The guidance states “Unfortunately, it is not possible to say in general terms which reasons really are objective. It requires a case-by-case analysis.” Not very helpful…

Next?

If you’re still confused as to what to do, I havean email guide that you can obtain for free from

http://bit.ly/MOSSVAT

Or if you’d like to talk to me 1-2-1, I have setaside five 30 minute slots that you can get for aMASSIVELY discounted £27 (plus VAT of course)from

bit.ly/HELPMEMOSSVAT

Questions

@accentis