Embed Size (px)

Citation preview

Understanding Rules of Originin International Trade Policy

Mr. CHEA Socheat, Director of Europe, Middle East, and Africa Department

Ministry of CommerceEmail: [email protected]

03-04 June 2015Phnom Penh

1

Objectives• Is it an Originating Product? Cambodia?• Terminologies of Origin and Rules of

Origin• The Use of Rules of Origin in Trade• Technical Elements of Rules of Origin:

WO and ST (VA, CTC, SP)• Self Certification • Economic Effects of Rules of Origin

2

Is it an Originating Product? Cambodia?

• Is it originated in this country? It may be wrong if one says country of origin of a product is:– Country where the goods are purchased or purchase is paid– Country where the company’s or factory head office is based – If two countries of origin: the one where we buy most – Where the goods are shipped from – Where the product is made

• Country of origin of a product can only be determined by Rules of Origin.

3

Originating Products?

4

Originating Products?

5

Originating Products?

6

Originating Products

7

CAMBODIAUSA

CHINAKOREA

Terminologies of Origin and ROO• Origin: born from a particular ancestor or, more generally it is

the act or fact of beginning from something, source or cause, starting point.

• It can be your nationality which is determined by your place of birth, by the origin or your parent, by your marriage with someone or by your prolonged residency in a given country. Your origin grants certain benefits like being able to live, work, access social security or run for elected posts.

• The origin of goods determines the nationality of a good or the country where a good was obtained or where it was manufactured. ROO defines the conditions under which a product is deemed as originating and therefore suitable for preferential treatment.

8

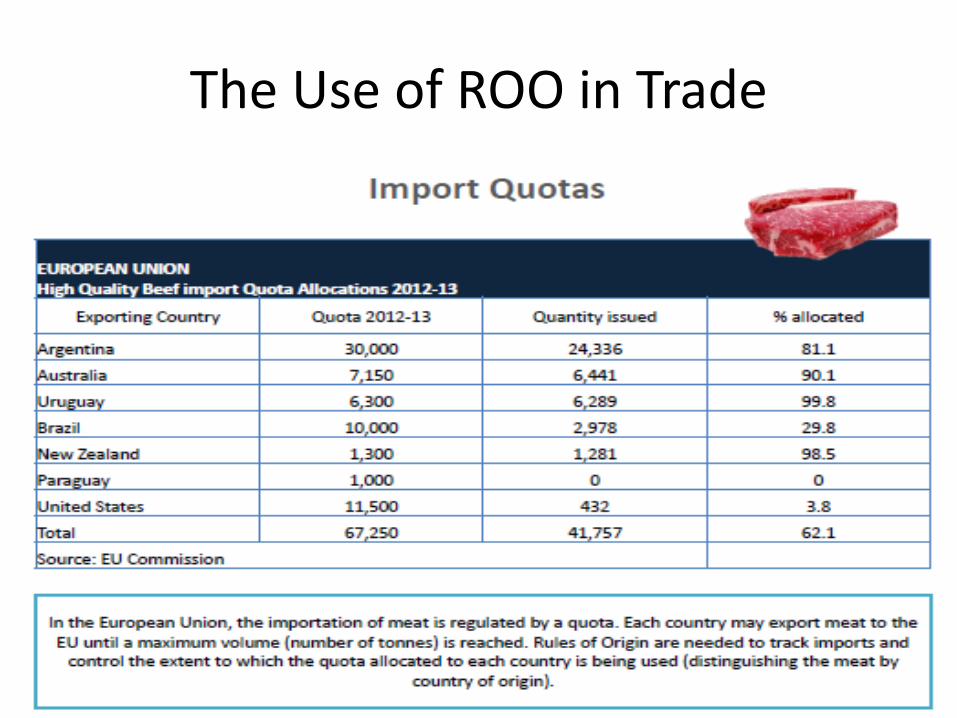

The Use of ROO in Trade

• Rules of Origin are used in international trade every time the treatment of an imported item varies depending on where it was produced; that is every time there needs to be a distinction based on the country of origin.

• Most commonly, this happens at the importation of a good, to determine which tariff rate should apply.

• However, certain countries may also apply other trade policy measures which require the utilization of rules of origin for the implementation.

9

The Use of ROO in Trade

• Customs treatment: import duties or tariffs• Quotas/quantitative restrictions• Anti-dumping or countervailing duties• Sanitary measures (inspection, quarantine)• Trade statistics• Country of origin marks in labels

10

• Two types of RoO: preferential (preferential trade agreement) and non preferential (MFN treatment)

• The justification for preferential RoO is to ensure that non-members do not obtain access to regional preferences (avoid trade deflection or free rider). All preferential trade agreements have rules of origin to ensure that the benefits of an agreement are only given to those products which originate in one of the parties to the agreement.

• The aim of preferential ROO is not so much to determine the real origin of a good, but rather to confirm that a good claiming preferential status actually meets the conditions set in the agreement.

• Non preferential roo involves no tariff concession. The determination of the origin is for trade policy measures (embargo, quota,..)

The Use of ROO in Trade

The Use of ROO in Trade

12

The Use of ROO-Trade Creation and Trade Diversion

• prevent deflection of trade and transhipment in an effort to (falsely) obtain origin and therefore preferential treatment

13

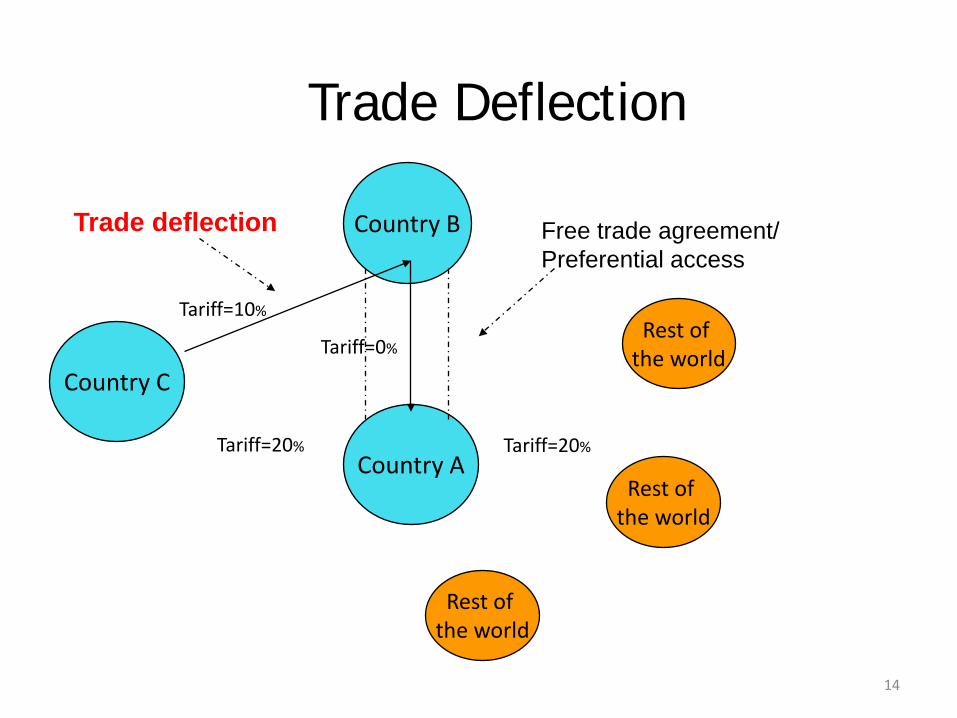

Trade Deflection

Country C

Country B

Country A

Free trade agreement/Preferential access

Rest of the world

Rest of the world

Rest of the world

Trade deflection

Tariff=10%

Tariff=0%

Tariff=20%Tariff=20%

14

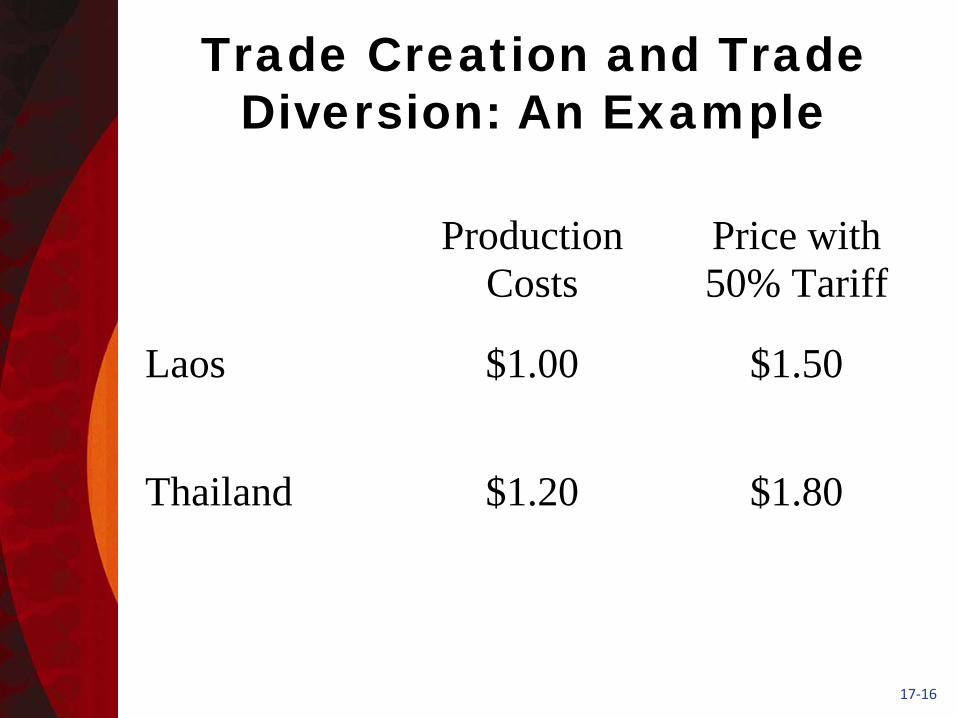

Trade Creation and Trade Diversion: An Example

• Suppose we have three countries: Cambodia, Laos, and Thailand.

• Initially, Cambodia imports textiles and applies a 50% tariff to textiles from both Laos and Thailand.

• Suppose that Laos is able to produce a unit of textiles for $1, whereas it costs Thailand producers $1.20 per unit.

Trade Creation and Trade Diversion: An Example

Production Costs

Price with 50% Tariff

Laos $1.00 $1.50

Thailand $1.20 $1.80

17-16

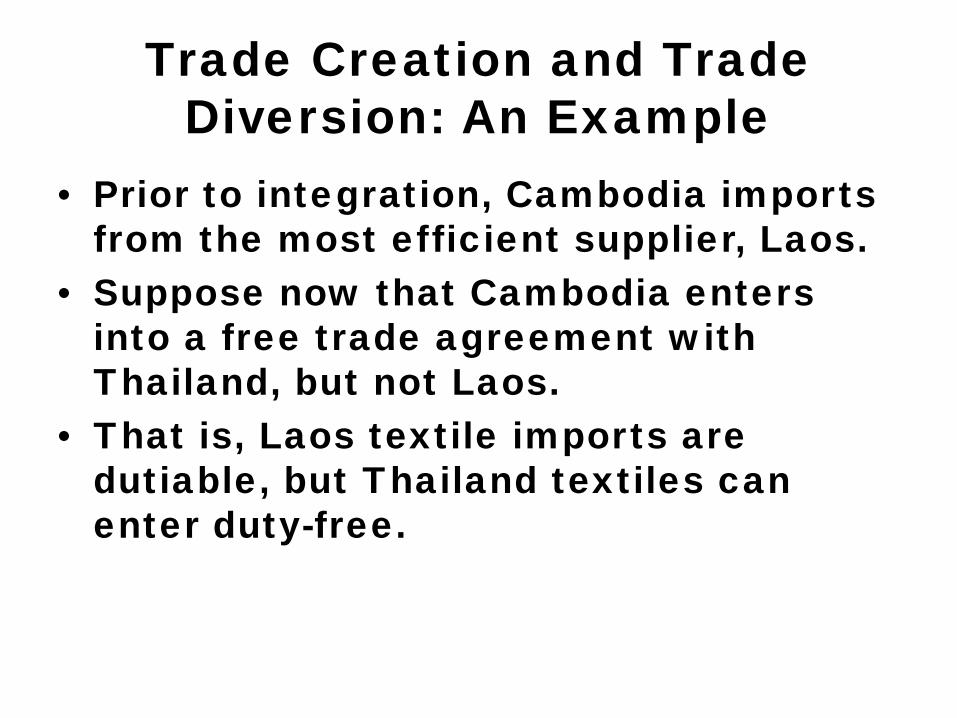

Trade Creation and Trade Diversion: An Example

• Prior to integration, Cambodia imports from the most efficient supplier, Laos.

• Suppose now that Cambodia enters into a free trade agreement with Thailand, but not Laos.

• That is, Laos textile imports are dutiable, but Thailand textiles can enter duty-free.

Trade Creation and Trade Diversion: An Example

Production Costs

Price with 50% Tariff

Price with FTA

Laos $1.00 $1.50 $1.50

Thailand $1.20 $1.80 $1.20

17-18

Trade Creation and Trade Diversion: An Example

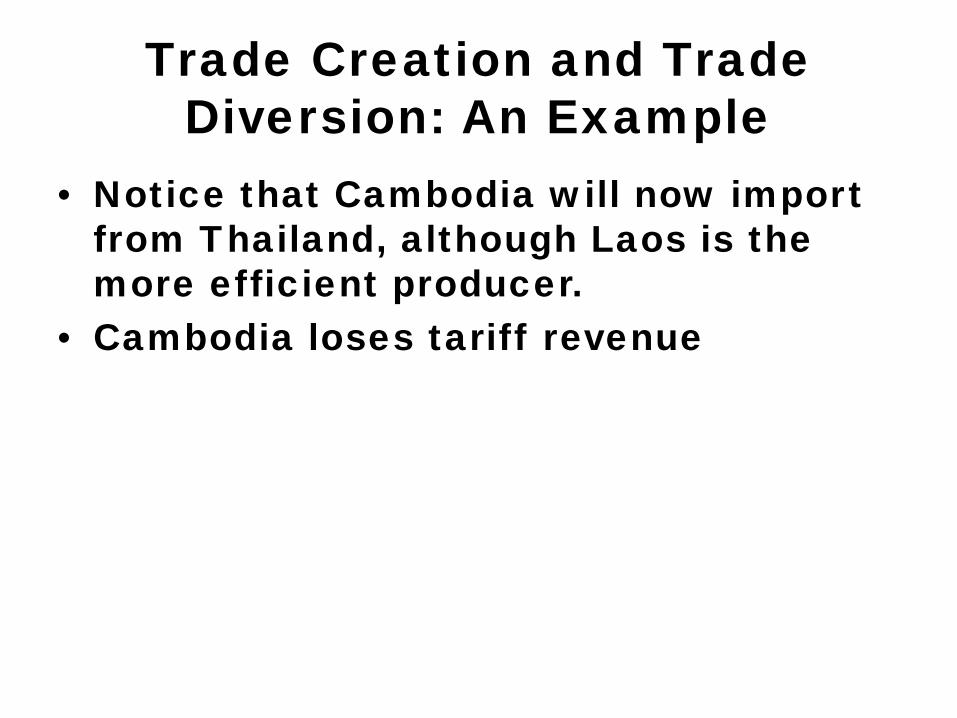

• Notice that Cambodia will now import from Thailand, although Laos is the more efficient producer.

• Cambodia loses tariff revenue

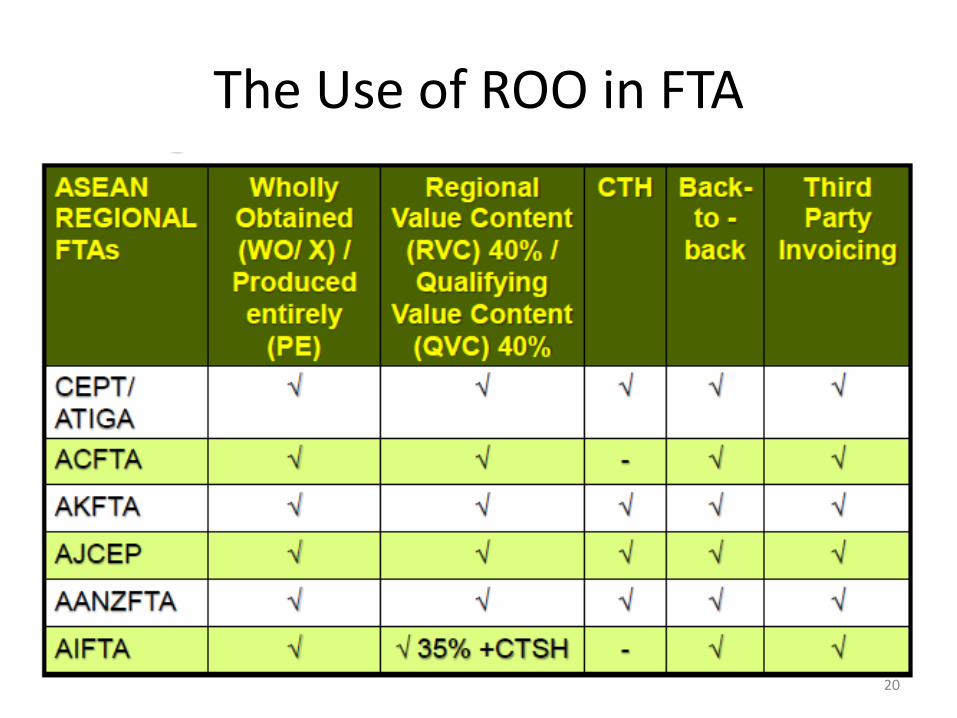

The Use of ROO in FTA

20

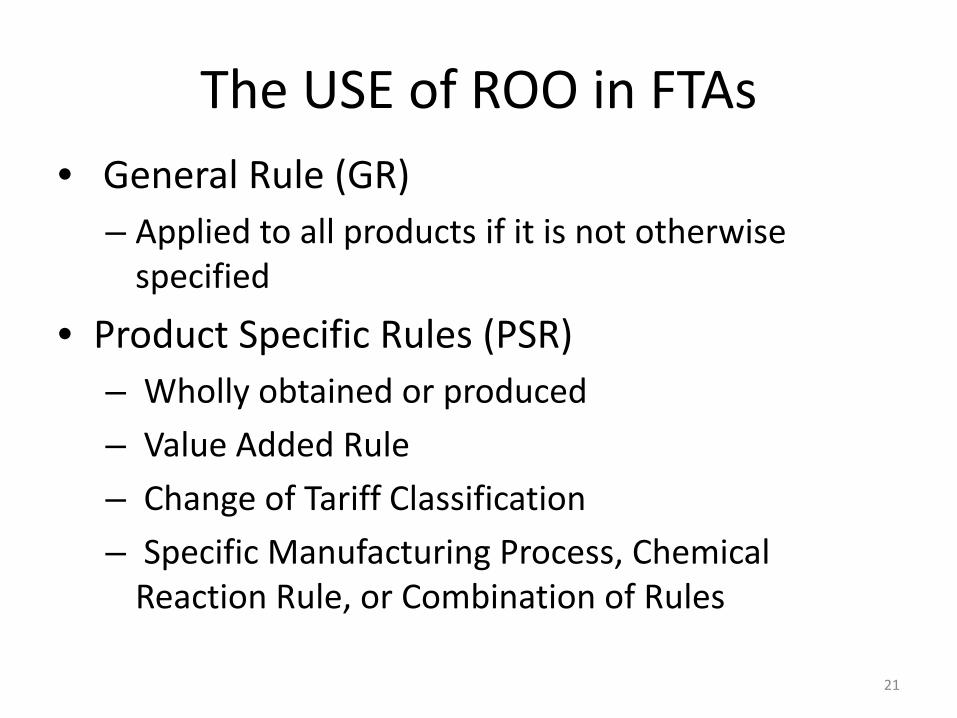

The USE of ROO in FTAs• General Rule (GR)

– Applied to all products if it is not otherwise specified

• Product Specific Rules (PSR)– Wholly obtained or produced– Value Added Rule– Change of Tariff Classification– Specific Manufacturing Process, Chemical

Reaction Rule, or Combination of Rules

21

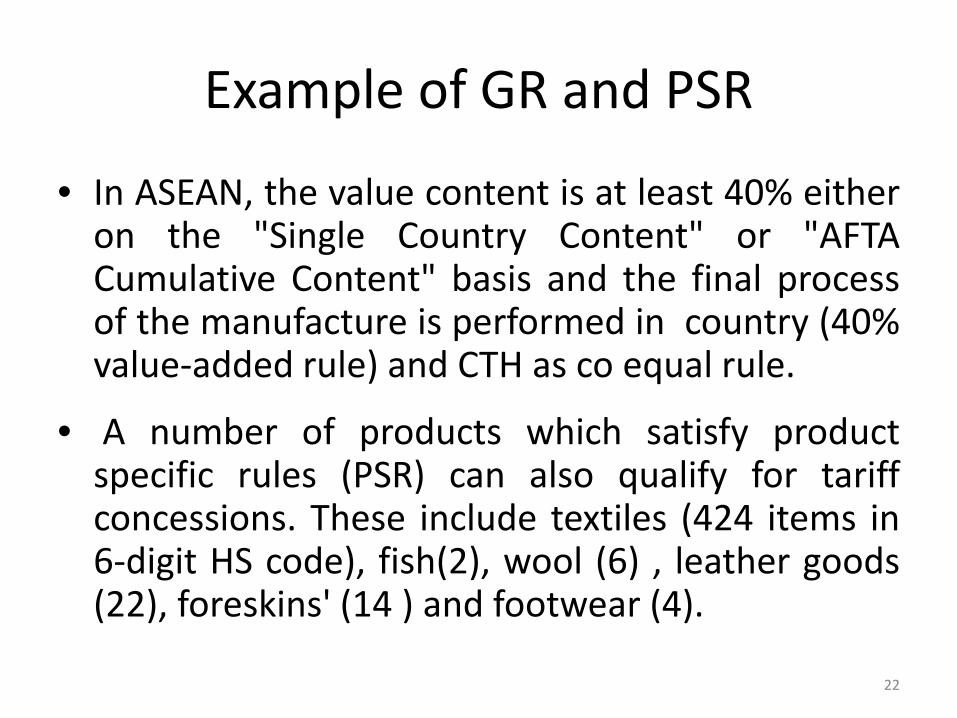

Example of GR and PSR

• In ASEAN, the value content is at least 40% eitheron the "Single Country Content" or "AFTACumulative Content" basis and the final processof the manufacture is performed in country (40%value-added rule) and CTH as co equal rule.

• A number of products which satisfy productspecific rules (PSR) can also qualify for tariffconcessions. These include textiles (424 items in6-digit HS code), fish(2), wool (6) , leather goods(22), foreskins' (14 ) and footwear (4).

22

23

Goods underwent substantial transformation process

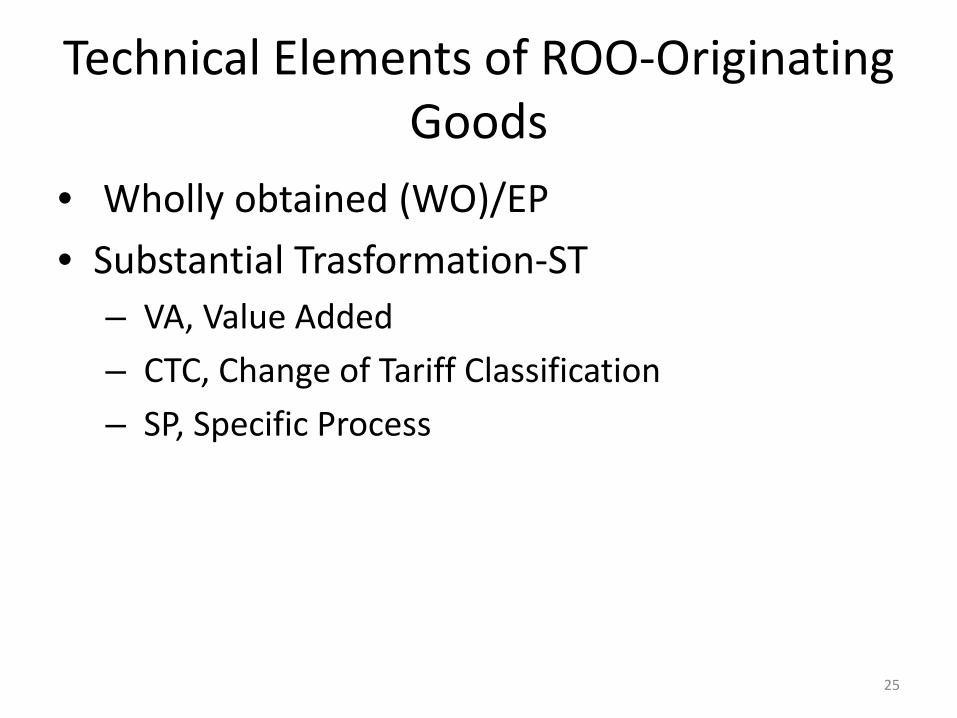

Technical Elements of ROO-Originating Goods

Products manufactured from exporting country wholly or partlyfrom imported materials or components, including materials ofundetermined or of unknown origin, are considered asORIGINATING in that country if its materials, parts orcomponents have undergone SUBSTANTIAL WORKING ORPROCESSING there.

24

Technical Elements of ROO-Originating Goods

• Wholly obtained (WO)/EP• Substantial Trasformation-ST

– VA, Value Added– CTC, Change of Tariff Classification– SP, Specific Process

25

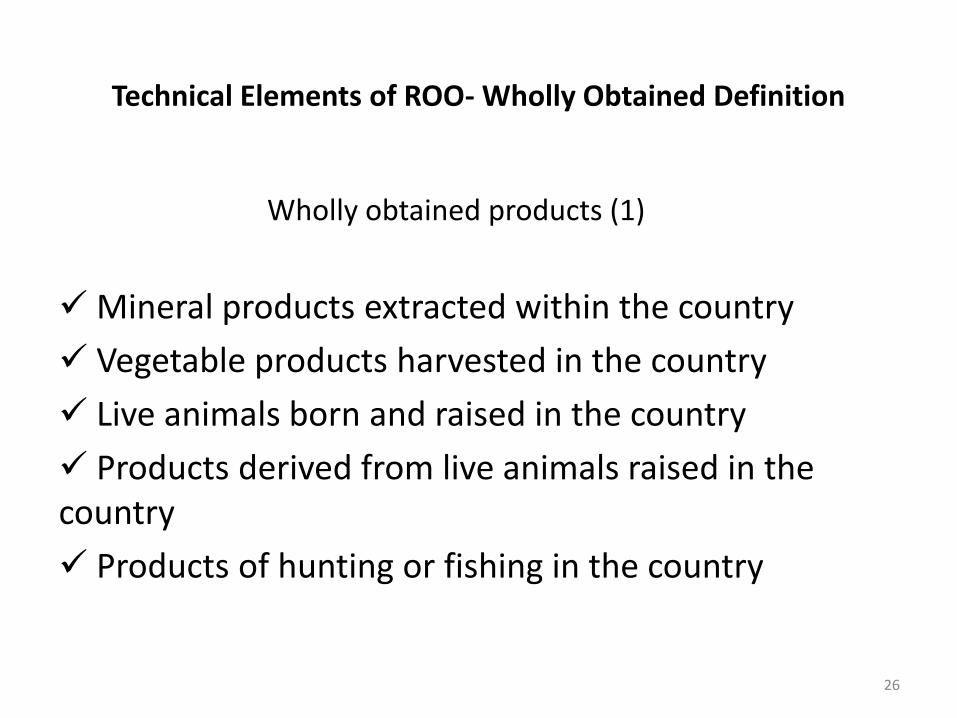

Technical Elements of ROO- Wholly Obtained Definition

Wholly obtained products (1)

Mineral products extracted within the country Vegetable products harvested in the country Live animals born and raised in the country Products derived from live animals raised in the country Products of hunting or fishing in the country

26

Technical Elements of ROO- Wholly Obtained

Wholly obtained products (2)

Products of sea-fishing and other products taken from the sea outside a country’s territorial sea by vessels registered or recorded in the country concerned and flying the flag of that country

Goods obtained or produced on board factory ships from the products above provided that such factory ships are registered or recorded in that country and fly its flag

Products taken from the seabed or subsoil beneath the seabed outside the territorial sea provided that that country has exclusive rights to exploit that seabed or subsoil

27

Examples of WO

• Rice• Maize

• Born and raised animal• Mining• Fishing with ship flying Cambodia flag and crew

of Khmer national

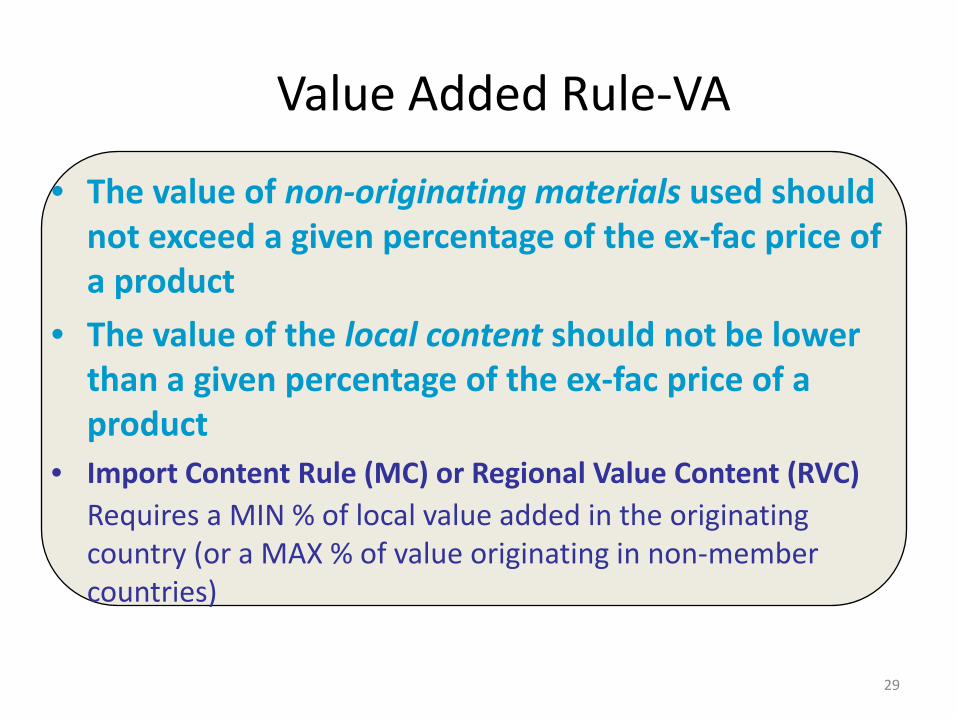

Value Added Rule-VA

• The value of non-originating materials used should not exceed a given percentage of the ex-fac price of a product

• The value of the local content should not be lower than a given percentage of the ex-fac price of a product

• Import Content Rule (MC) or Regional Value Content (RVC)Requires a MIN % of local value added in the originating country (or a MAX % of value originating in non-member countries)

29

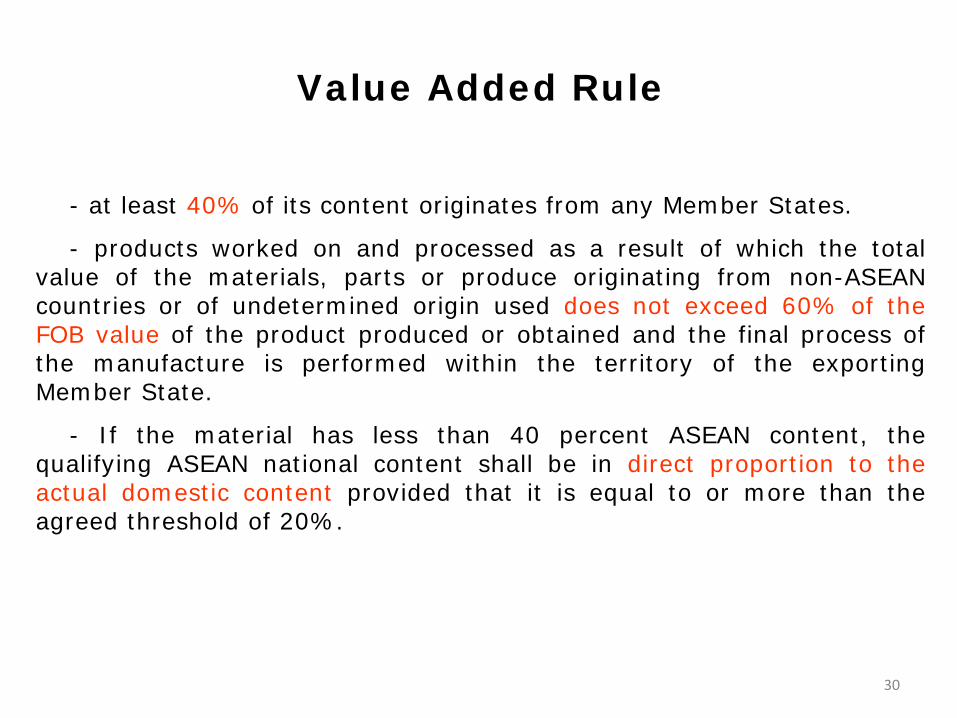

Value Added Rule

- at least 40% of its content originates from any Member States.

- products worked on and processed as a result of which the totalvalue of the materials, parts or produce originating from non-ASEANcountries or of undetermined origin used does not exceed 60% of theFOB value of the product produced or obtained and the final process ofthe manufacture is performed within the territory of the exportingMember State.

- If the material has less than 40 percent ASEAN content, thequalifying ASEAN national content shall be in direct proportion to theactual domestic content provided that it is equal to or more than theagreed threshold of 20%.

30

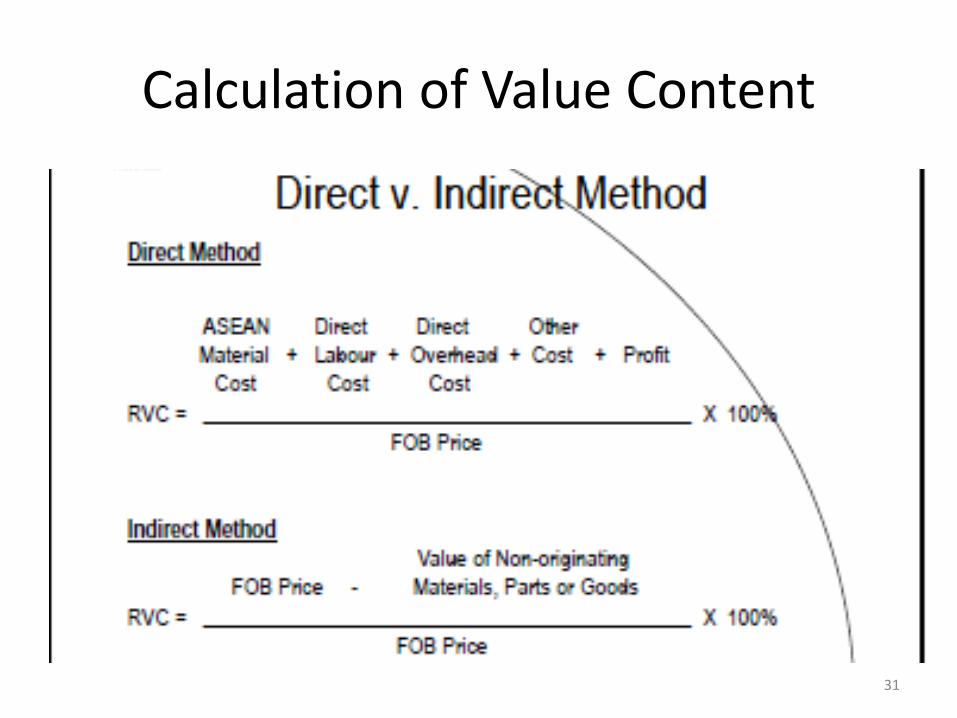

Calculation of Value Content

31

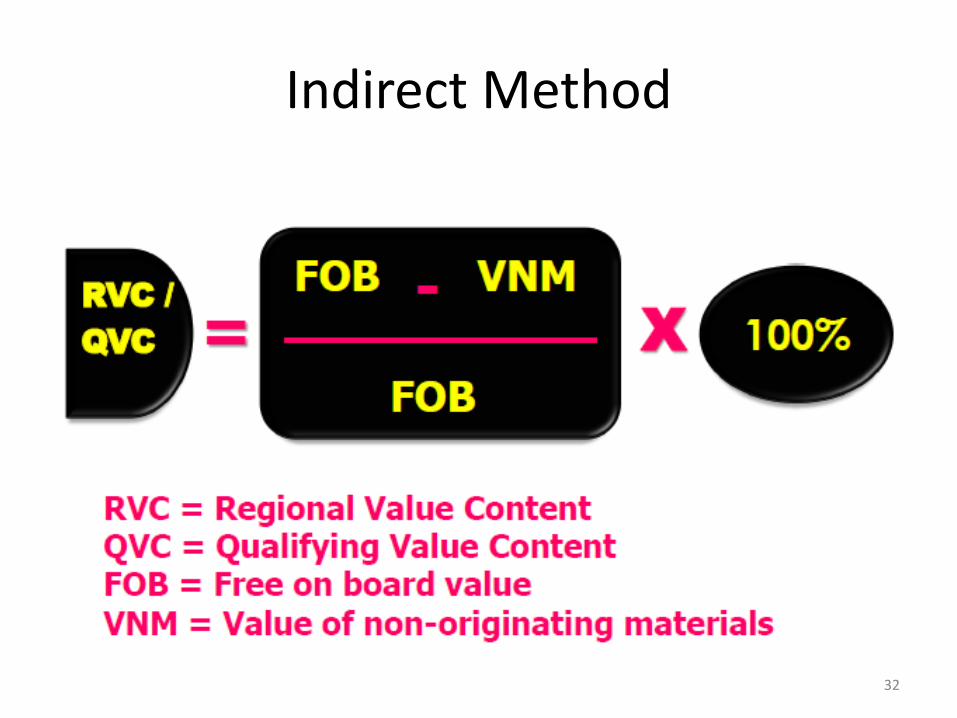

Indirect Method

32

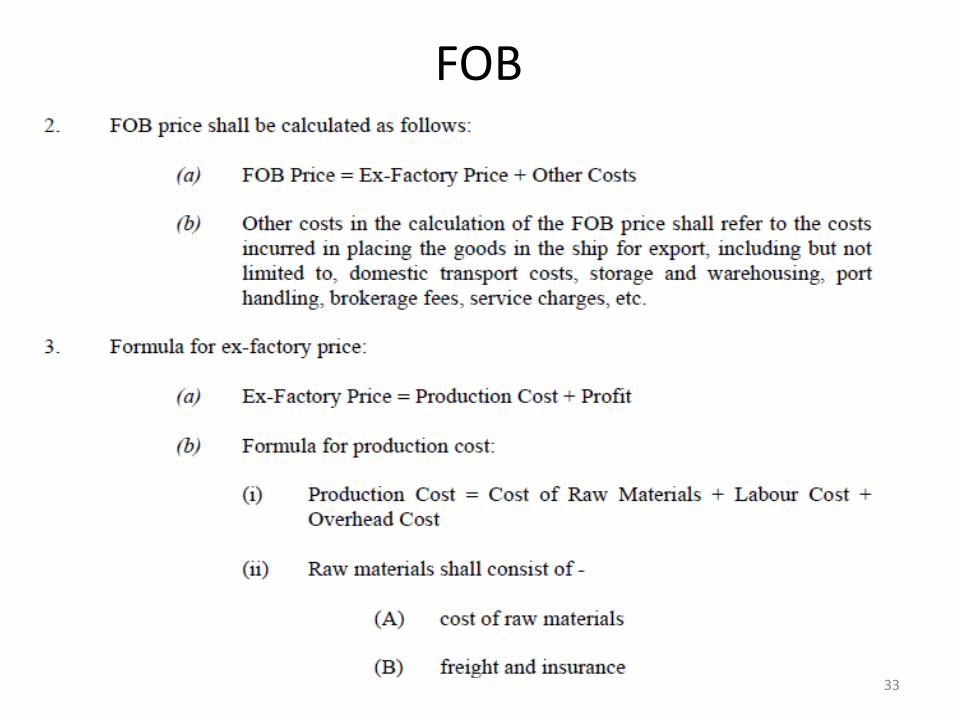

FOB

33

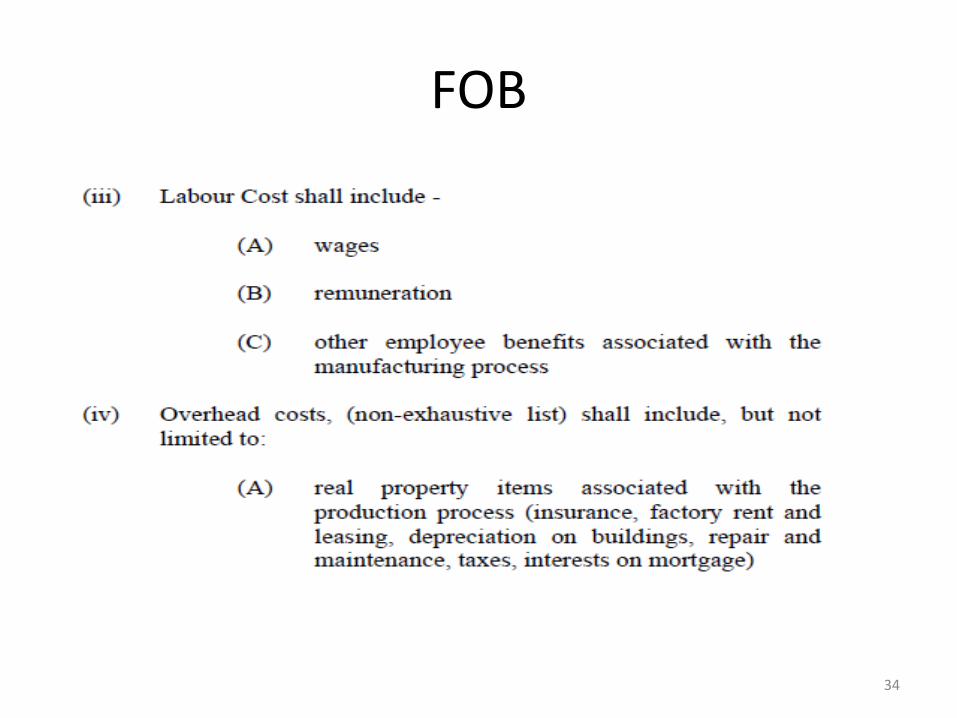

FOB

34

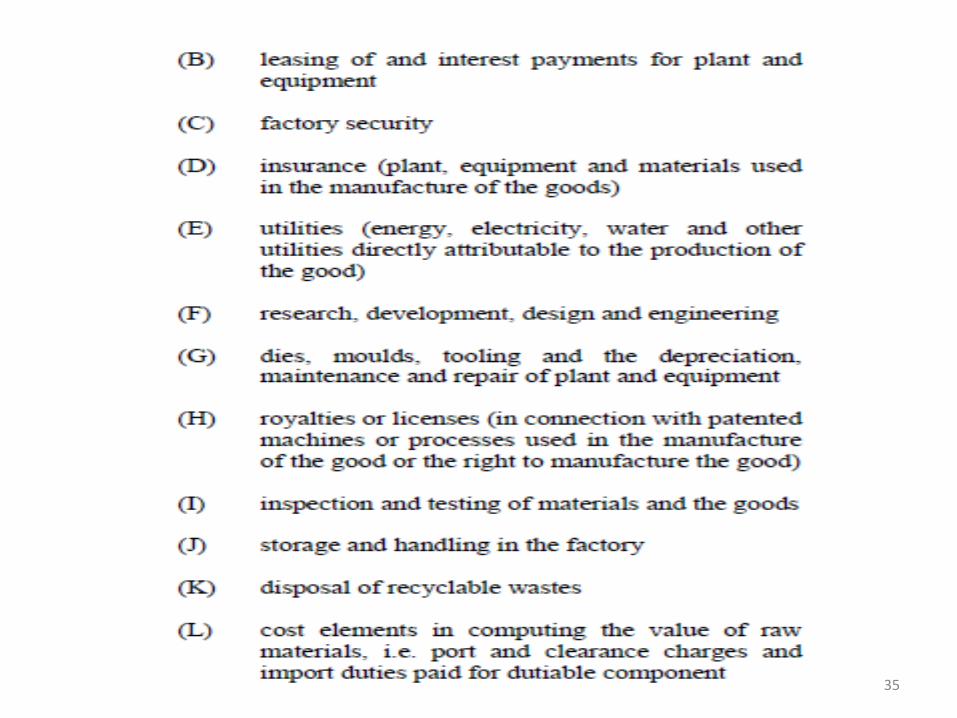

35

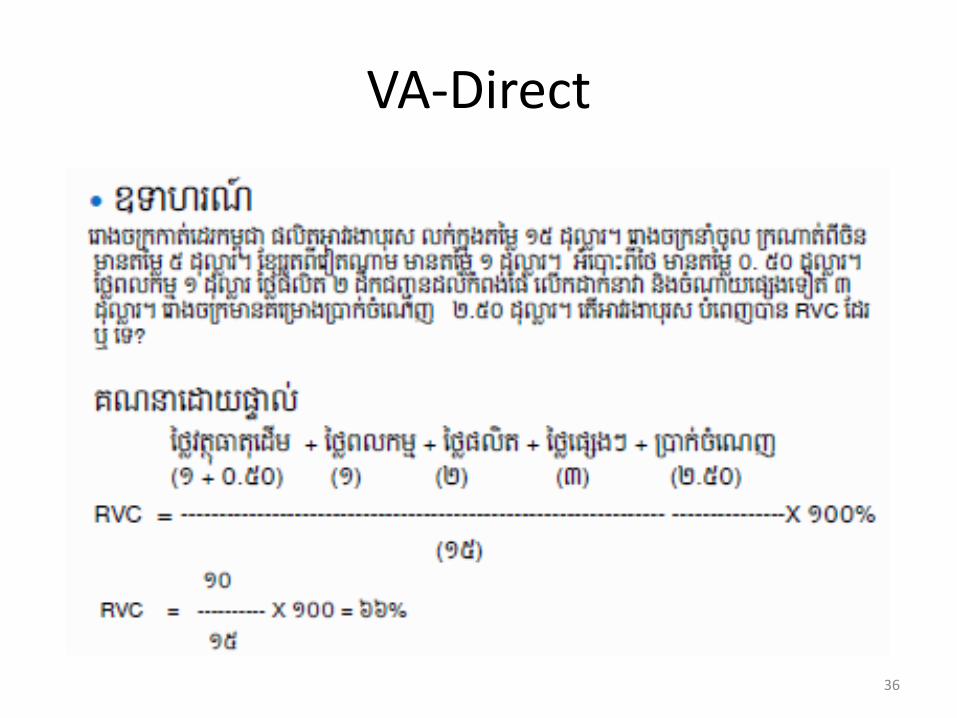

VA-Direct

36

VA-Indirect

37

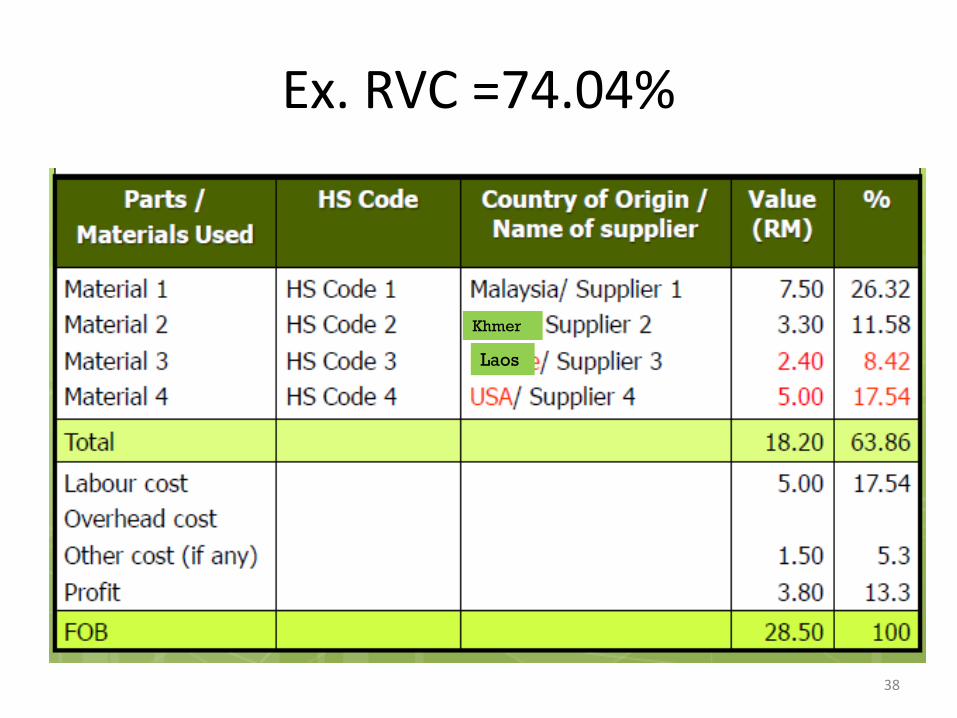

Ex. RVC =74.04%

Khmer

Laos

38

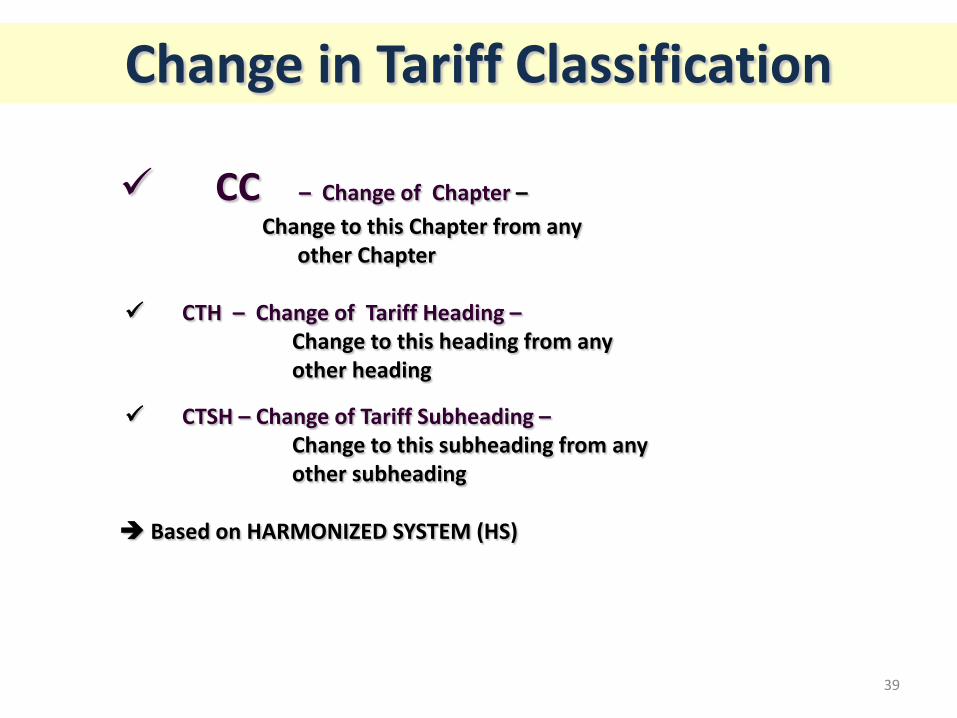

CC – Change of Chapter –Change to this Chapter from any

other Chapter

CTH – Change of Tariff Heading –Change to this heading from any other heading

CTSH – Change of Tariff Subheading –Change to this subheading from any other subheading

Based on HARMONIZED SYSTEM (HS)

Change in Tariff Classification

39

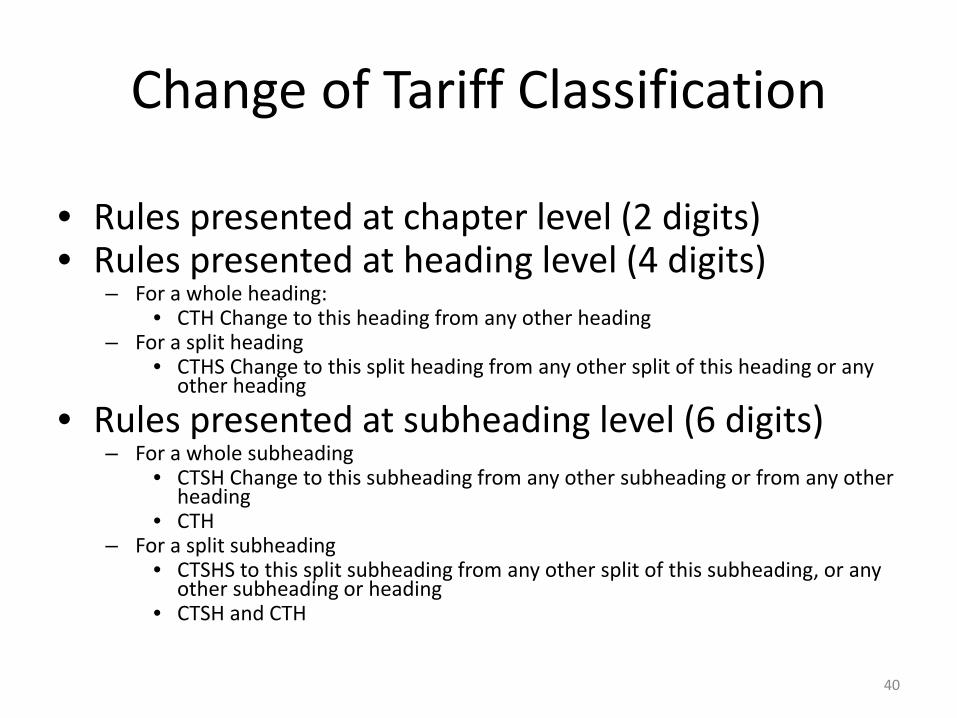

Change of Tariff Classification

• Rules presented at chapter level (2 digits)• Rules presented at heading level (4 digits)

– For a whole heading:• CTH Change to this heading from any other heading

– For a split heading • CTHS Change to this split heading from any other split of this heading or any

other heading

• Rules presented at subheading level (6 digits)– For a whole subheading

• CTSH Change to this subheading from any other subheading or from any other heading

• CTH – For a split subheading

• CTSHS to this split subheading from any other split of this subheading, or any other subheading or heading

• CTSH and CTH

40

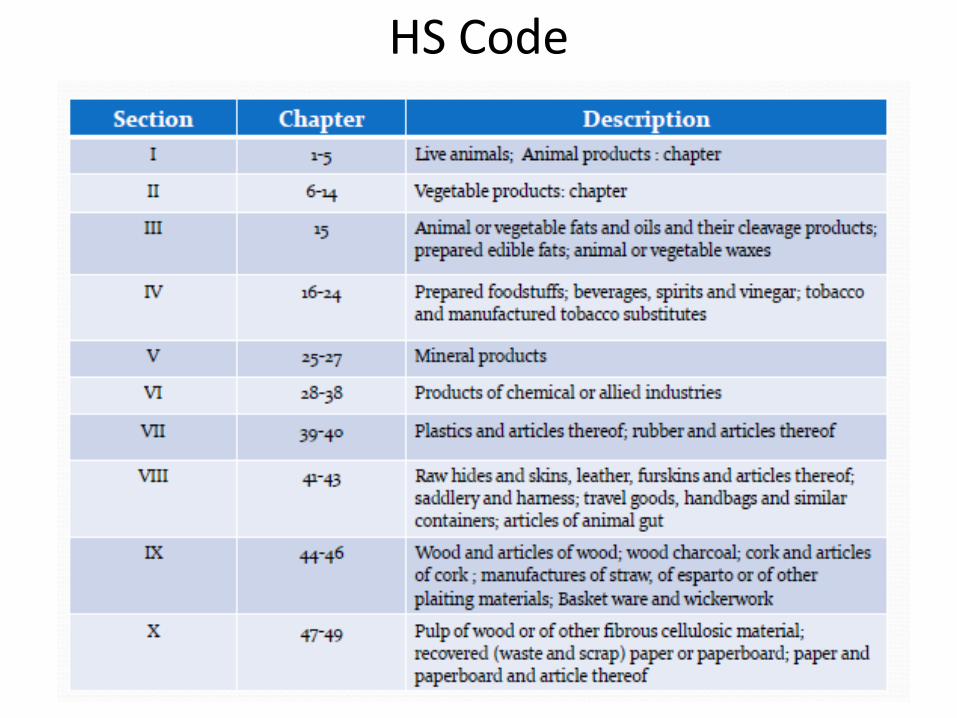

HS Code

41

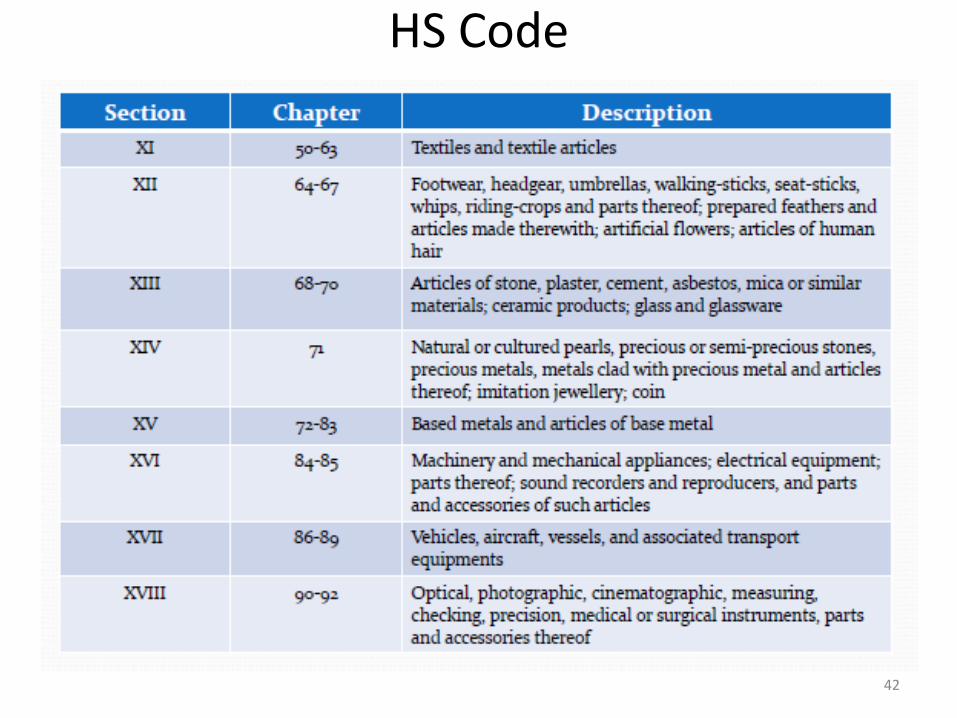

HS Code

42

HS Code

43

Change of Tariff Classification

44

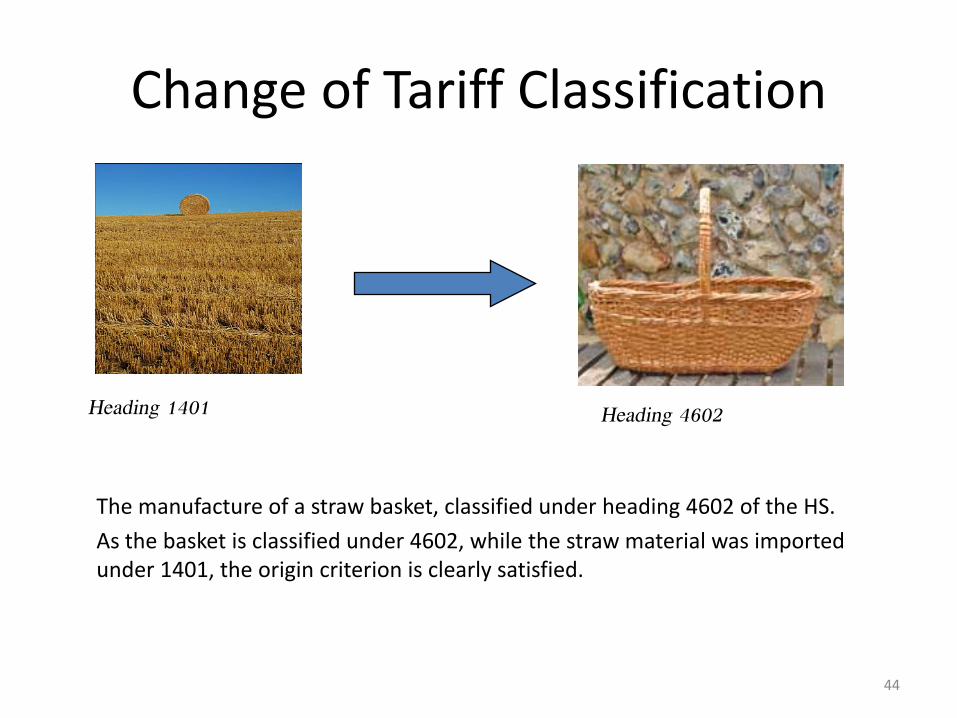

The manufacture of a straw basket, classified under heading 4602 of the HS. As the basket is classified under 4602, while the straw material was imported under 1401, the origin criterion is clearly satisfied.

Heading 4602Heading 1401

Change of Tariff Classification

A Cambodia oil factory buys copra from various farmers as a raw material for the production of a refined oil to be exported to Australia.

CambodiaCoconut / CopraH.S. 801.19

Refined Oil H.S. 1513.19

Exported

Australia

45

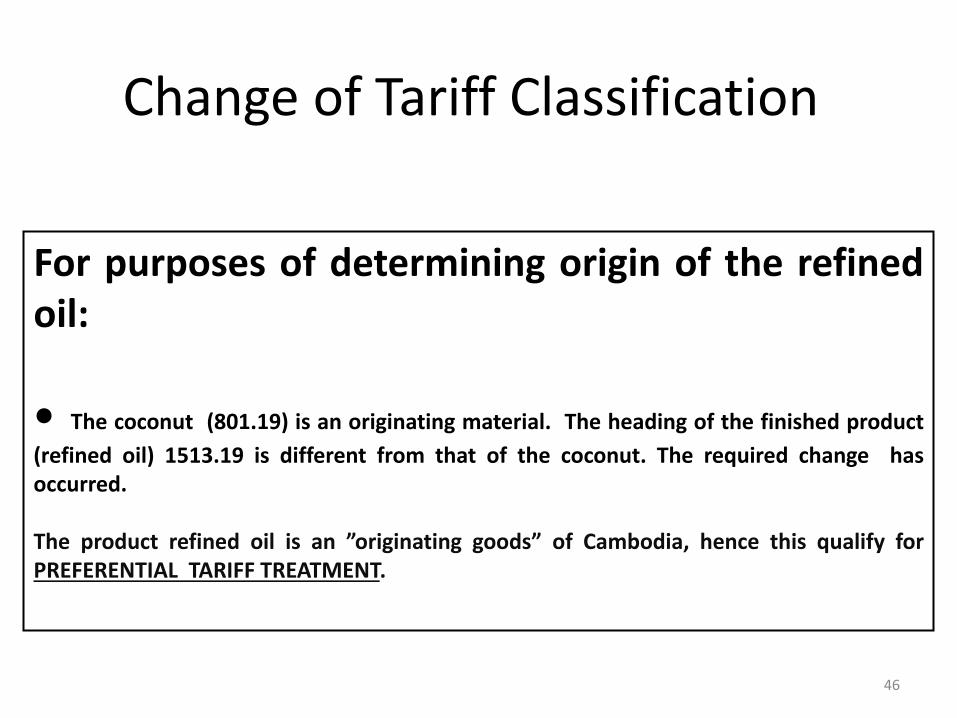

For purposes of determining origin of the refinedoil:

• The coconut (801.19) is an originating material. The heading of the finished product(refined oil) 1513.19 is different from that of the coconut. The required change hasoccurred.

The product refined oil is an ”originating goods” of Cambodia, hence this qualify forPREFERENTIAL TARIFF TREATMENT.

Change of Tariff Classification

46

The HS code of refined oil is 1513.19 and its origin rule underATIGA is “A regional value content of not less than 40 percent;or

A change to subheading 1513.19 from any other. The rulerequires that the 6-digit (i.e. subheading) code of the refinedoil be different from those of the materials used in itsproduction in Cambodia.

Change of Tariff Classification

47

Specific Process

Articles of ApparelChapter 62 of the HS, for which (mostheadings) the rule is "manufacture fromfabric".

This means that you can import fabric. Sewingand possible other subsequent manufacturingstages must be carried out in the beneficiarycountry in order to obtain origin.

The so called ”single transformation rule”

48

Specific Process

rule for the same chapter (62) was "manufacture from yarn"

Weaving and sewing, plus allsubsequent manufacturing stagesmust be carried out in thebeneficiary country in order toobtain origin.

The so called ”double transformation rule”

49

Some Other Important Features

• Cumulation• Tolerance or de minimis

50

De minimis Rule

• The Tolerance rule:– Non-originating materials may be used in the

manufacture of a product, even if the rule of sufficient working is not fulfilled, provided that their total value does not exceed 10% of the ex-works price of the product. (specific product rules for textiles)

• Examples:– Parts of same heading as end product, so no CTH.

However, permitted under tolerance rule if not more than 10% of total value

51

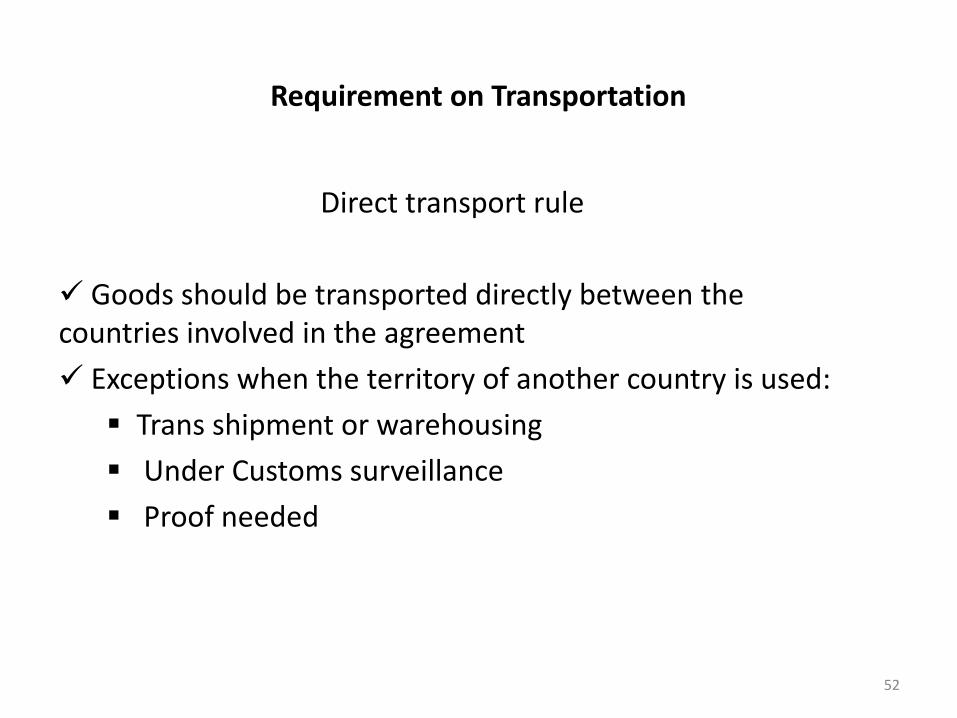

Requirement on Transportation

Direct transport rule

Goods should be transported directly between the countries involved in the agreement Exceptions when the territory of another country is used: Trans shipment or warehousing Under Customs surveillance Proof needed

52

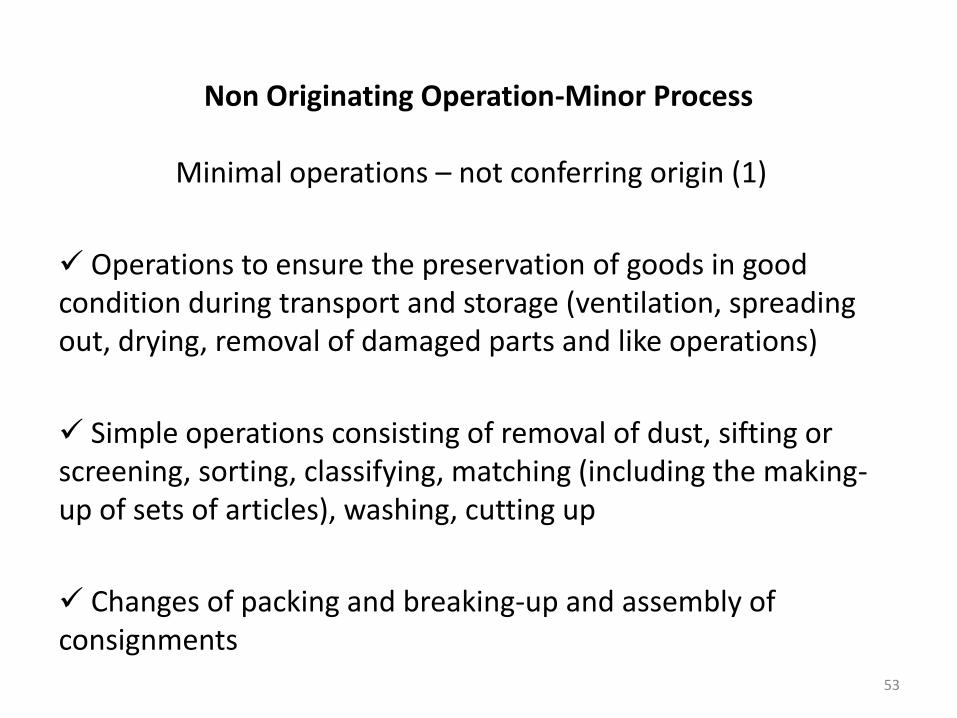

Non Originating Operation-Minor Process

Minimal operations – not conferring origin (1)

Operations to ensure the preservation of goods in good condition during transport and storage (ventilation, spreading out, drying, removal of damaged parts and like operations)

Simple operations consisting of removal of dust, sifting or screening, sorting, classifying, matching (including the making-up of sets of articles), washing, cutting up

Changes of packing and breaking-up and assembly of consignments

53

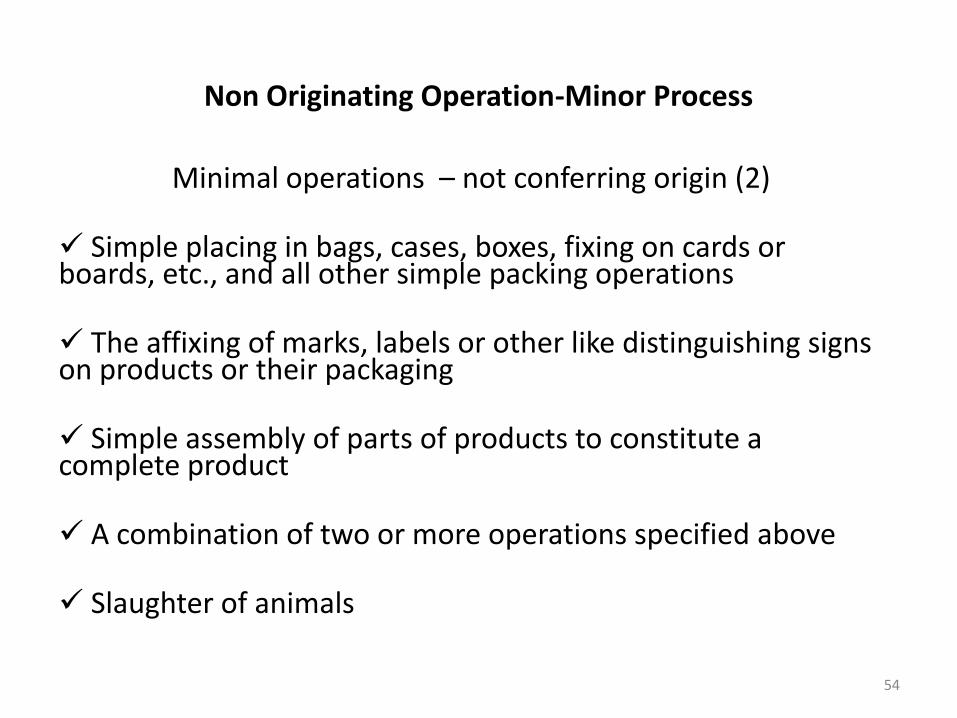

Non Originating Operation-Minor Process

Minimal operations – not conferring origin (2)

Simple placing in bags, cases, boxes, fixing on cards or boards, etc., and all other simple packing operations

The affixing of marks, labels or other like distinguishing signs on products or their packaging

Simple assembly of parts of products to constitute a complete product

A combination of two or more operations specified above

Slaughter of animals

54

Self Certification-SC

55

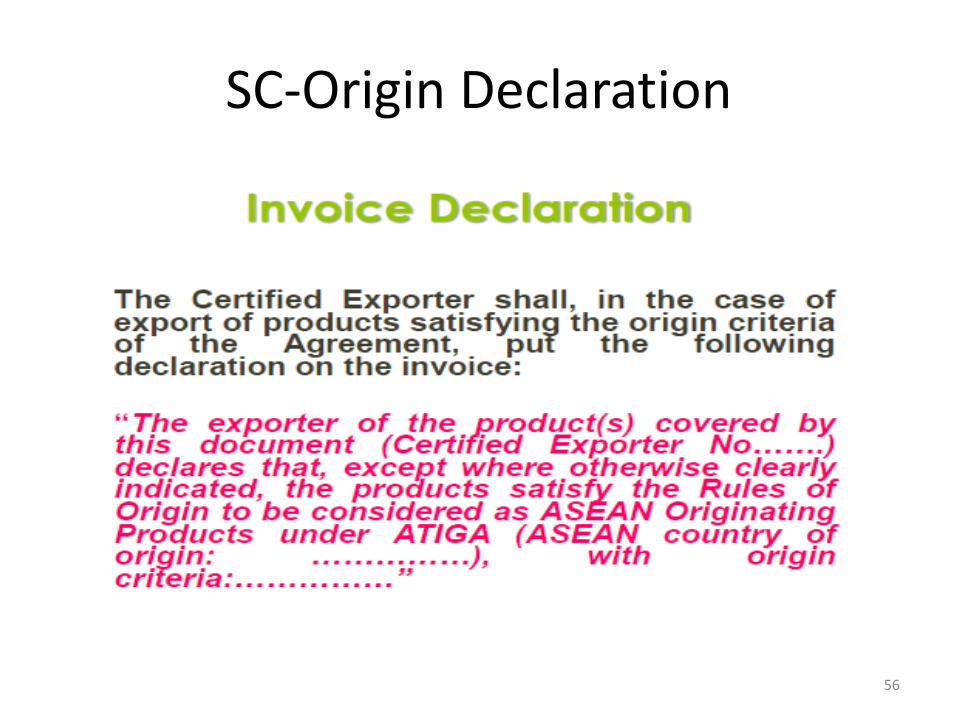

SC-Origin Declaration

56

The Effects of Rules of Origin

• ROO have a direct impact on market access conditions because importing country sets the conditions for the entry of goods in its territory.

• Encourage foreign and domestic investment where the rules facilitate international trade.

• Influence the capacity for firms to integrate international value chains.

• Influence the ability of firms to benefit from regional or preferential trade agreements

• Encourage or discourage linkages between export sectors and national industries.

57

Effects of Rules of Origin

• ROO may require producers to change their suppliers to qualify for regional or preferential trade agreements.

• ROO could have a significant impact on the cost of producing a good and might therefore affect its competitiveness and trade opportunities.

• If the rules is not clear, exporters and importers may have great difficulty predicting which treatment their goods will receive, making it more difficult to make business plans and decisions. If the rules are complex, companies may need to hire and dedicate staff specifically to understand them and reduce the risks associated with regulatory uncertainty which increase their costs.

58

Thank You

Questions??59