Embed Size (px)

Citation preview

Tyre Industry in IndiaCOMPETITION OR COLLUSION

Table of Contents

Industry Overview Government Policy Evolution Present Situation How Does the Industry Work? Customer Segments Factors affecting Tyre Prices Top 10 Players Market Shares and Category wise

Production

Structural Factors of Indian Tyre Industry

Case of Collusion (CCI) Companies under scanner Findings of the DG Result of the Case Competitive Scenario of Indian Tyre

Industry Porter’s 5 Force Model Change in Technology

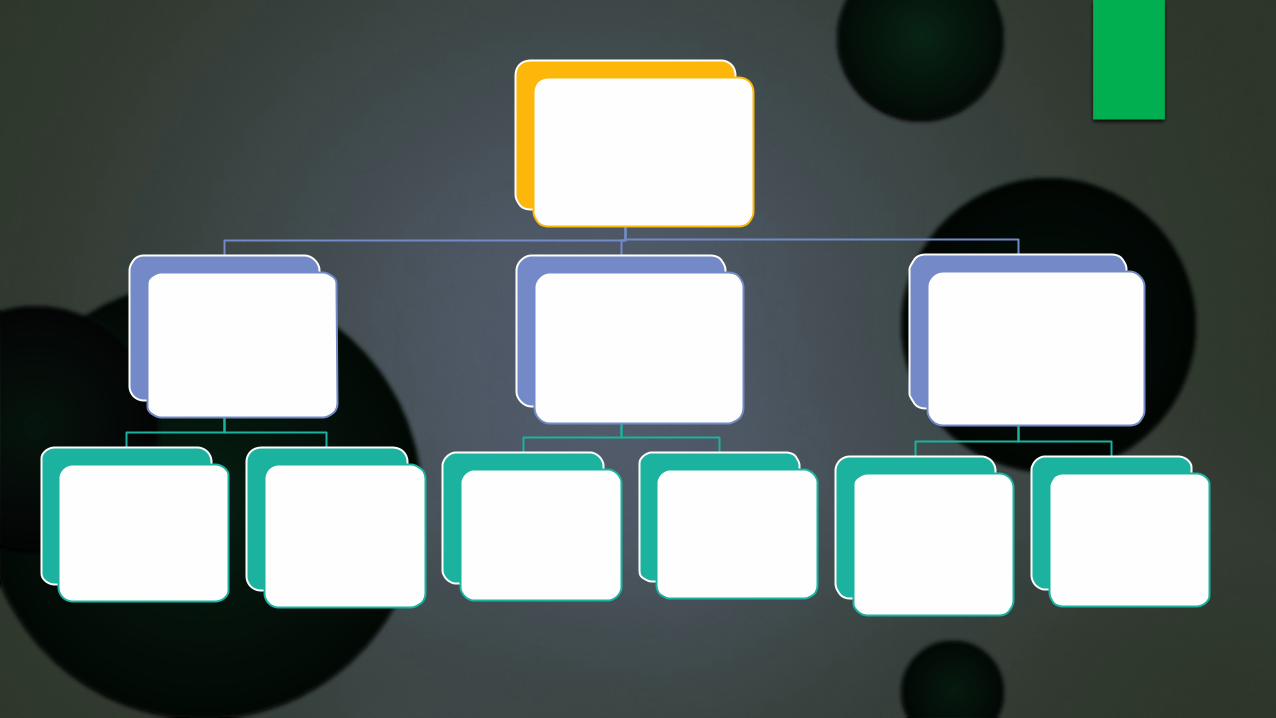

Indian Tyre Industry

Commercial vehicles

Light Commercial vehicle (LCV)

Heavy Commercial

Vehicle (HCV)

Passenger Vehicles

Cars Motor Cycles

Others

Farm VehiclesIndustrial

vehicle

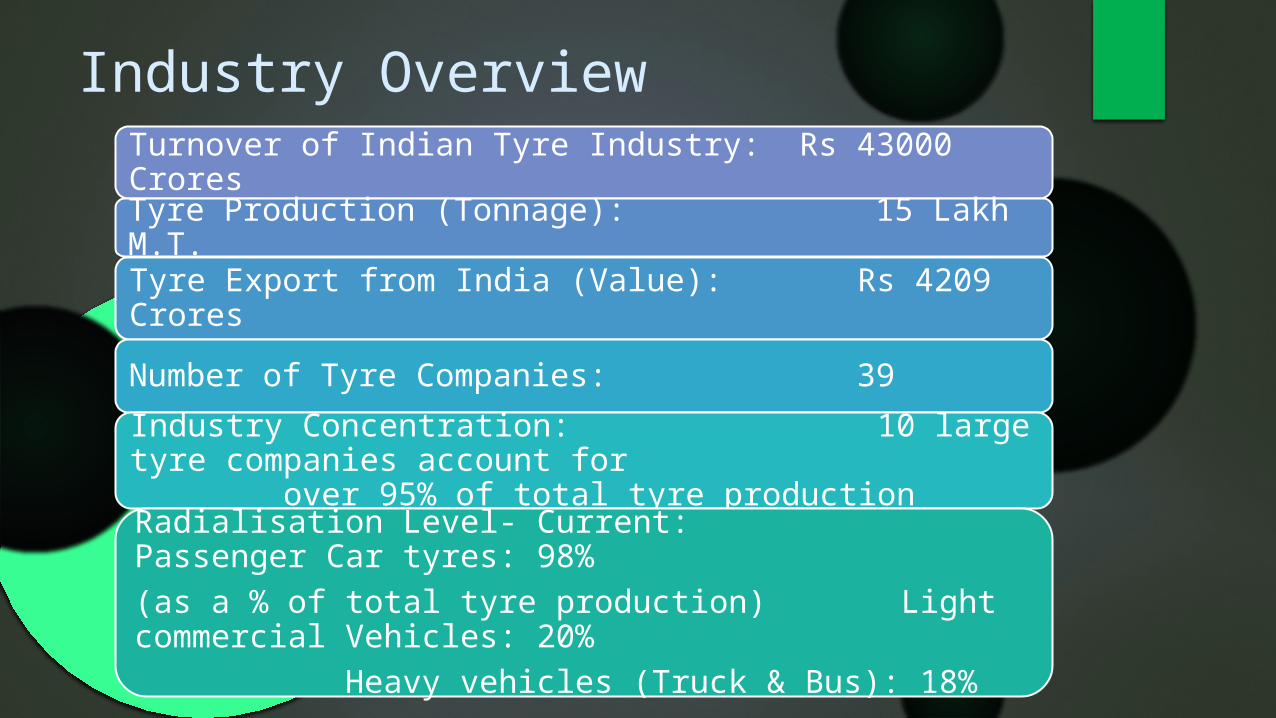

Industry OverviewTurnover of Indian Tyre Industry: Rs 43000 Crores

Tyre Production (Tonnage): 15 Lakh M.T.

Tyre Export from India (Value): Rs 4209 Crores

Number of Tyre Companies: 39

Industry Concentration: 10 large tyre companies account for over 95% of total tyre production

Radialisation Level- Current: Passenger Car tyres: 98%(as a % of total tyre production) Light commercial Vehicles: 20%

Heavy vehicles (Truck & Bus): 18%

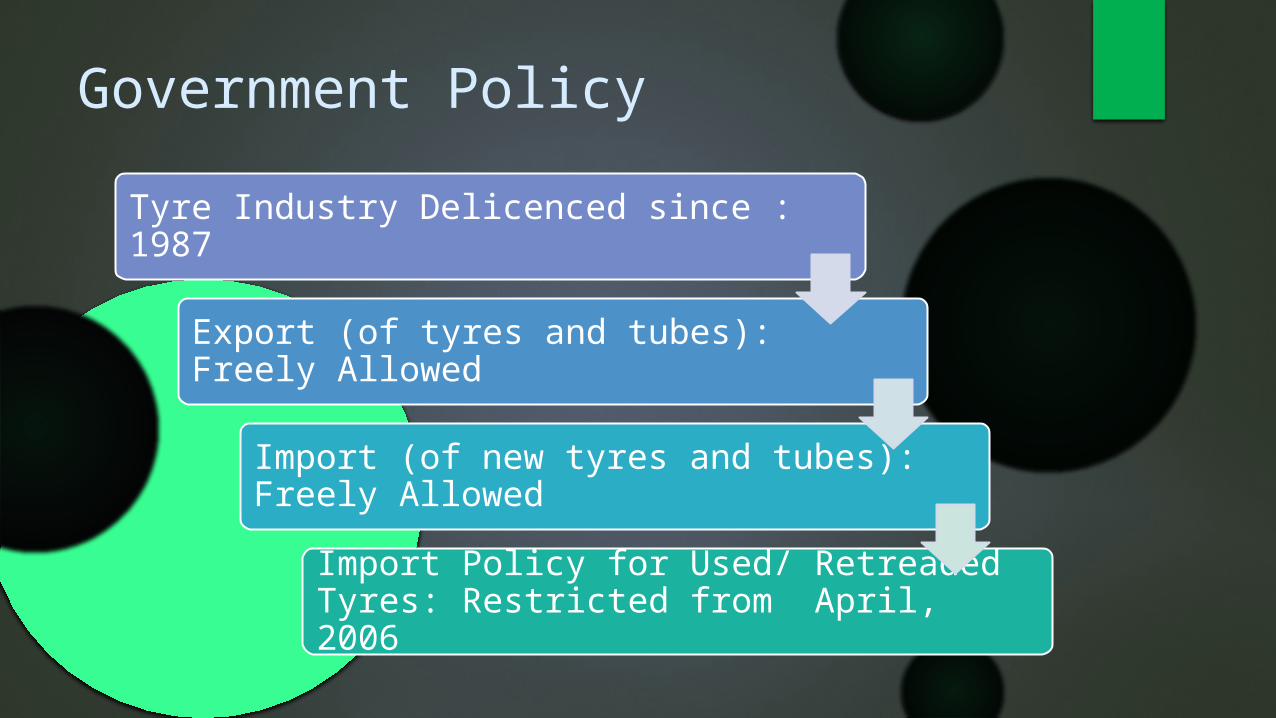

Government Policy

Tyre Industry Delicenced since : 1987

Export (of tyres and tubes): Freely Allowed

Import (of new tyres and tubes): Freely Allowed

Import Policy for Used/ Retreaded Tyres: Restricted from April, 2006

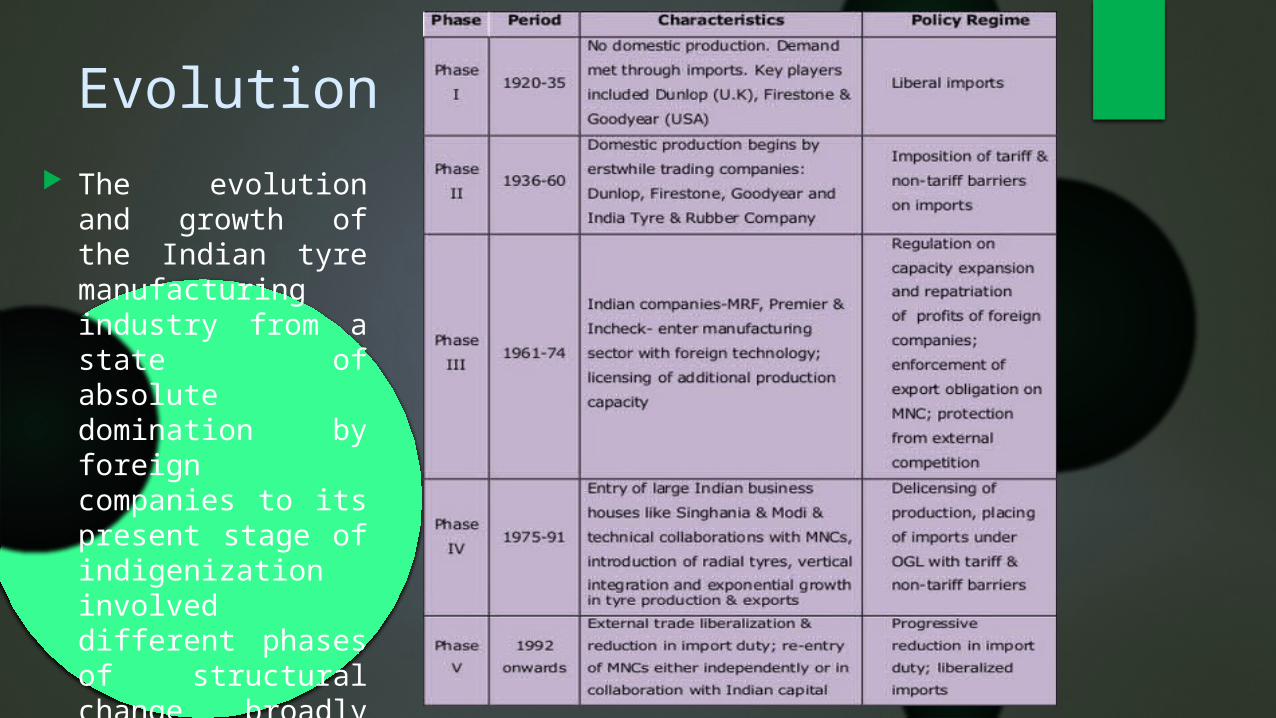

Evolution The evolution and

growth of the Indian tyre manufacturing industry from a state of absolute domination by foreign companies to its present stage of indigenization involved different phases of structural change broadly reflecting various policy regimes in the economy.

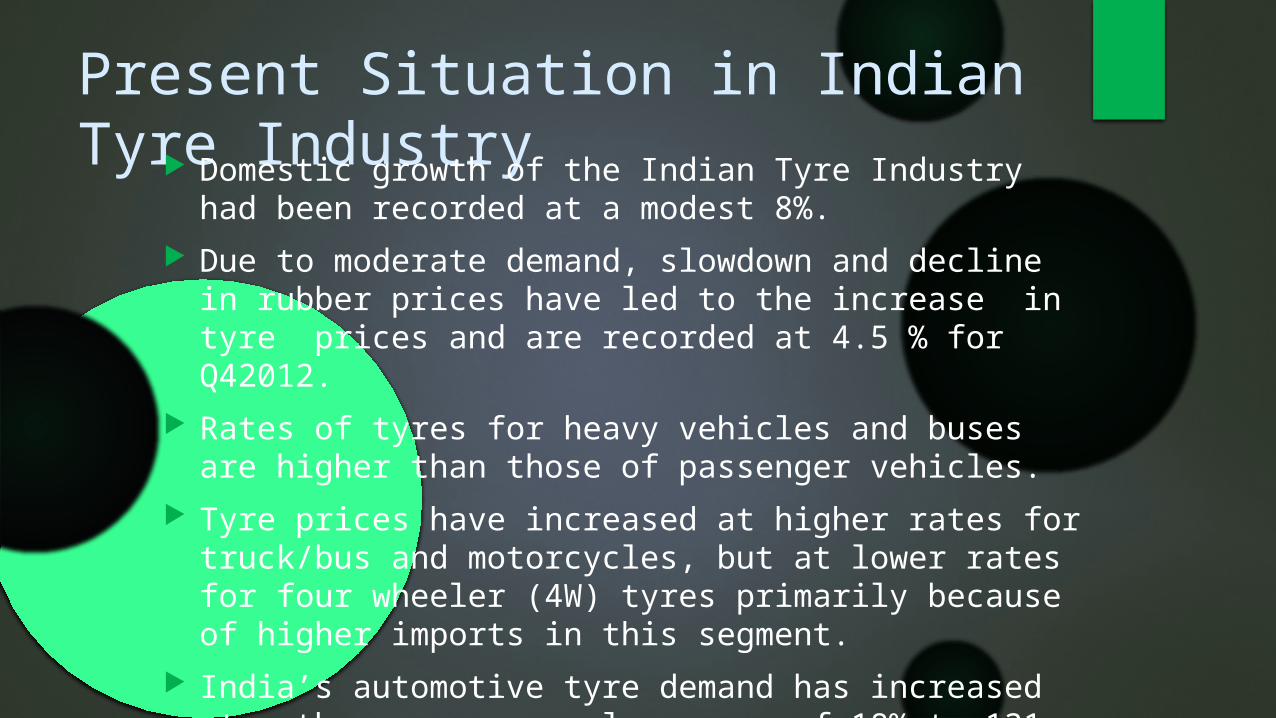

Present Situation in Indian Tyre Industry Domestic growth of the Indian Tyre Industry had been recorded at a

modest 8%. Due to moderate demand, slowdown and decline in rubber prices

have led to the increase in tyre prices and are recorded at 4.5 % for Q42012.

Rates of tyres for heavy vehicles and buses are higher than those of passenger vehicles.

Tyre prices have increased at higher rates for truck/bus and motorcycles, but at lower rates for four wheeler (4W) tyres primarily because of higher imports in this segment.

India’s automotive tyre demand has increased at a three year annual average of 18% to 131 million in FY2012.

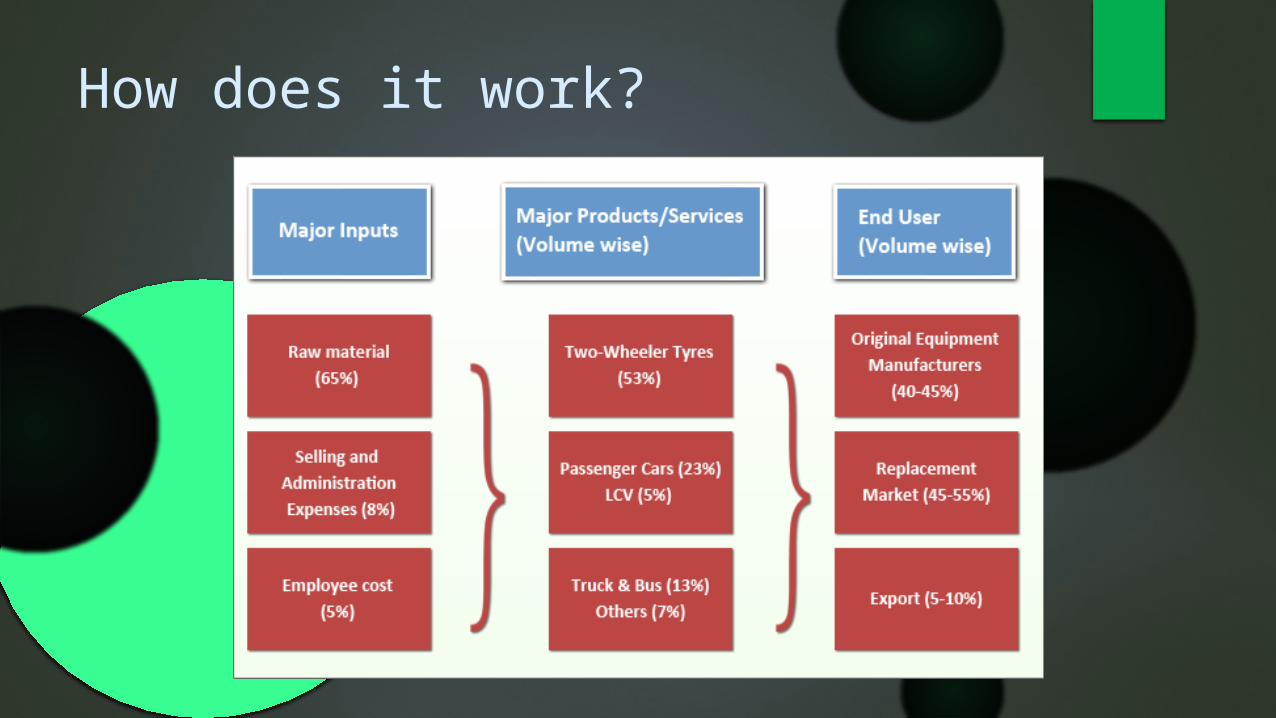

How does it work?

Customer Segments

The tyre manufactures cater to the following major customer segments either directly or indirectly through dealers/ marketing agents: Original Equipment Manufacturers (OEMs) Replacement Market (aftermarket) Export Segment State Transport Undertakings (STUs)

Factors Influencing Tyre Prices

The industry is highly raw material (RM) intensive. Raw material costs accounts for 80-85% of the total

production cost of tyres. Natural rubber constitutes is the major raw material used by

the industry and accounts for around 43% of the total cost. The other raw materials consumed by the tyre industry are

crude derivatives such as synthetic rubber (SBR – styrene butadiene rubber, PBR – polybutadiene rubber), nylon tyre cord fabric, carbon black and rubber chemicals.

Therefore, rising crude oil prices increase raw material costs and affect the profitability of the company.

“Major components which affect the prices of tyres are the

cost of natural rubber and the excise

duty.”

Top 10 Tyre Companies in India

1. MRF 2. Apollo Tyres 3. JK Tyres 4. CEAT Tyres 5. Balakrishna Tyres 6. Goodyear Tyres 7. TVS Srichakra 8. Falcon Tyres 9. Govind Rubber 10. Krypton Tyres

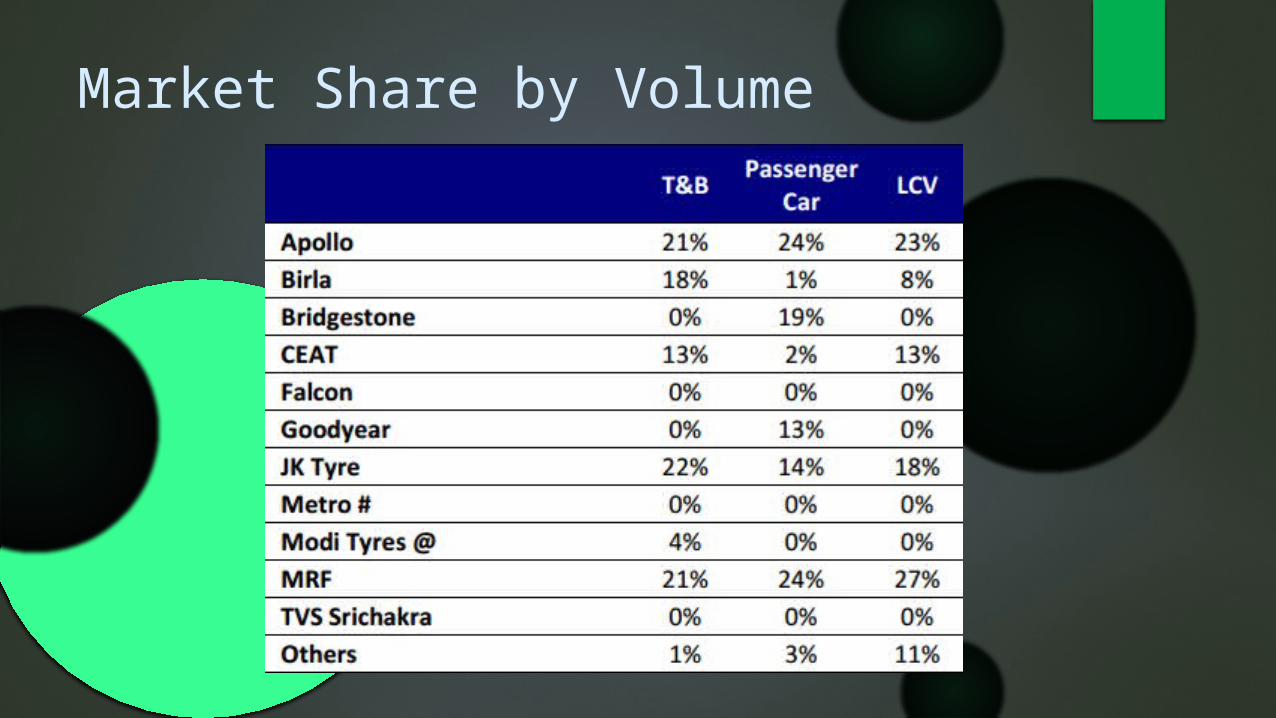

Market Share by Volume

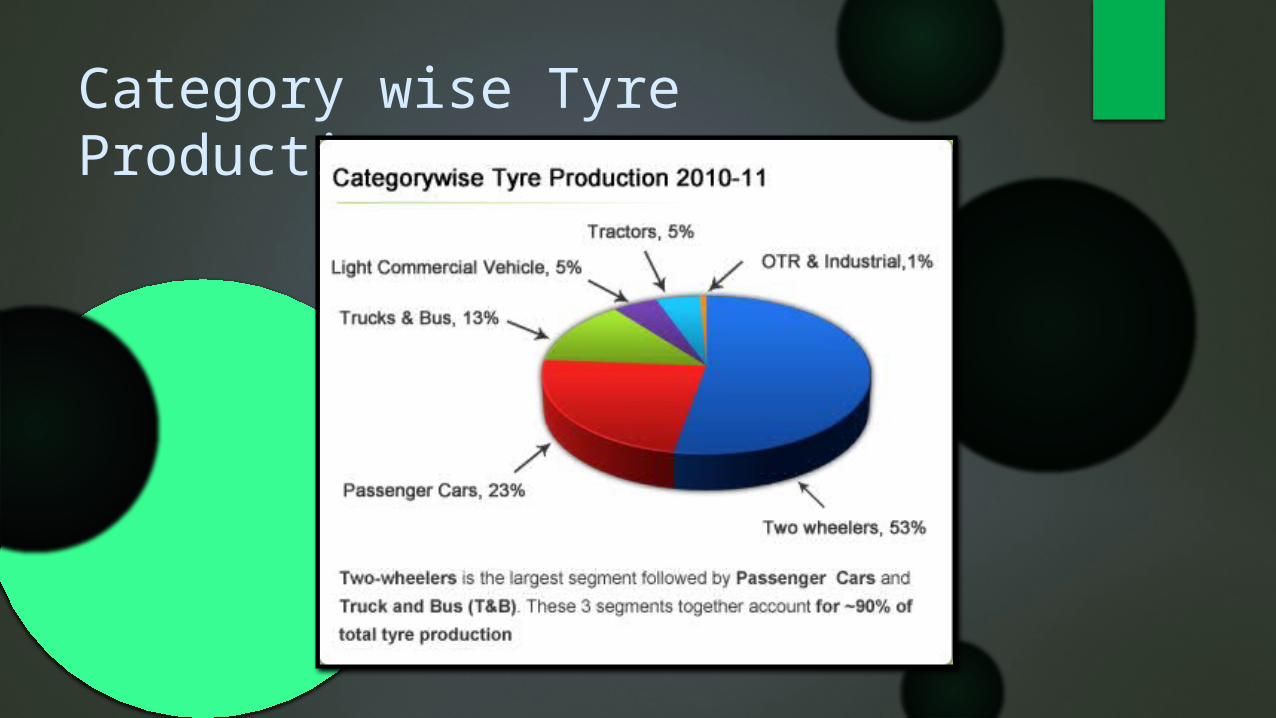

Category wise Tyre Production

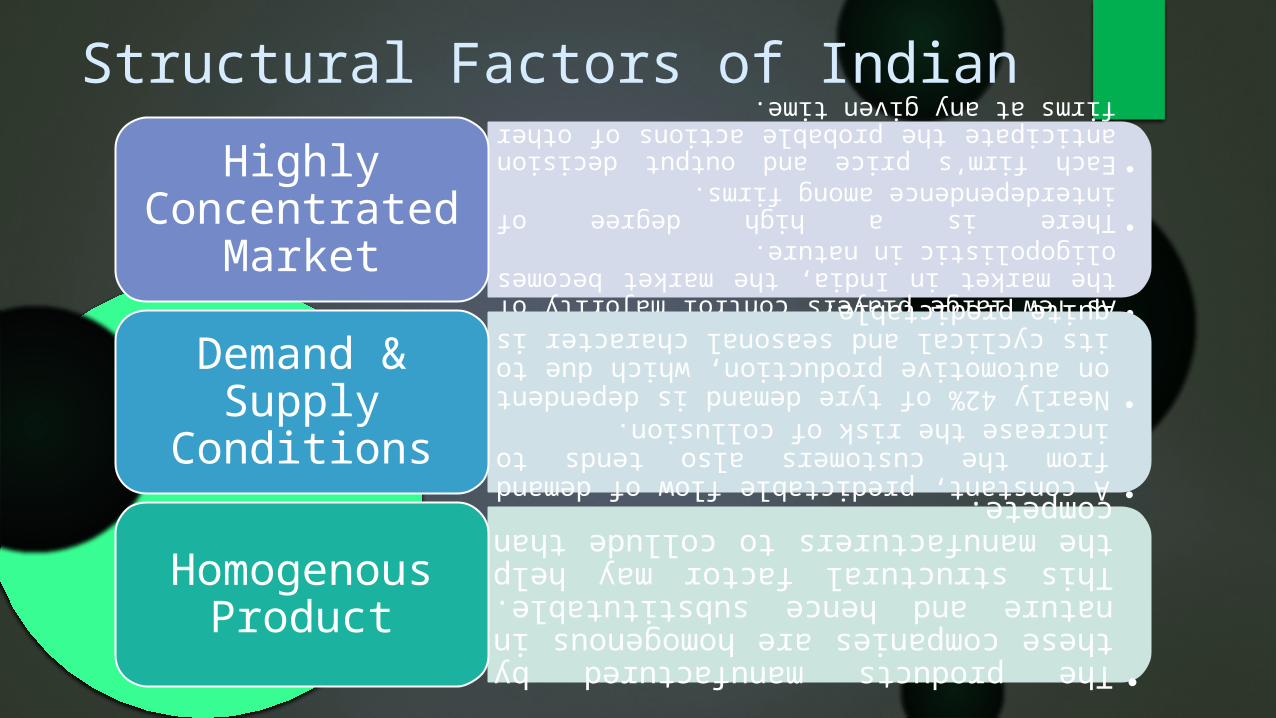

Structural Factors of Indian •As few

large players control majority of the market in India, the market becomes oligopolistic in nature.

•There is a high degree of interdependence among firms.

•Each firm’s price and output decision anticipate the probable actions of other firms at any given time.

Highly Concentrated

Market

•A constant, predictable flow of demand from the customers also tends to increase the risk of collusion.

•Nearly 42% of tyre demand is dependent on automotive production, which due to its cyclical and seasonal character is quite predictable.

Demand & Supply

Conditions

•The products manufactured by these companies are homogenous in nature and hence substitutable. This structural factor may help the manufacturers to collude than compete.

Homogenous Product

Structural Factors contd..

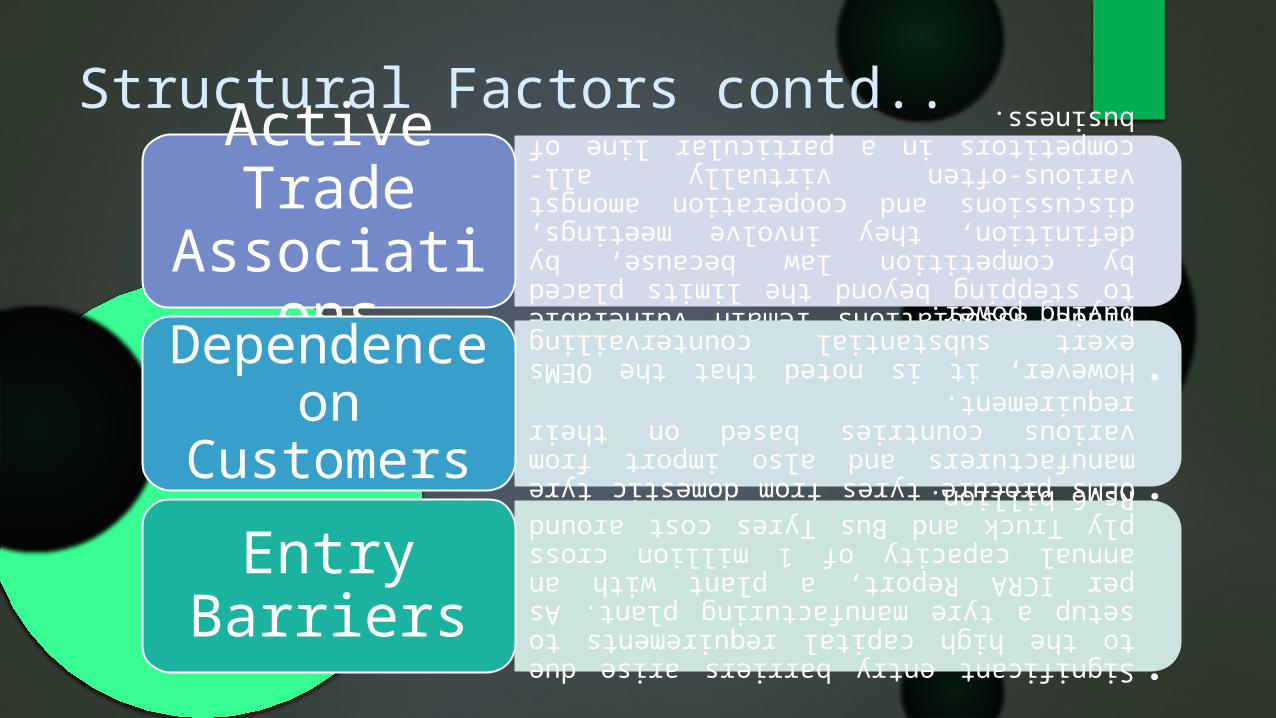

•Trade associations remain vulnerable to stepping beyond the limits placed by competition law because, by definition, they involve meetings, discussions and cooperation amongst various-often virtually all-competitors in a particular line of business.

Active Trade Associations

•OEMs procure tyres from domestic tyre manufacturers and also import from various countries based on their requirement.

•However, it is noted that the OEMs exert substantial countervailing buying power.

Dependence on Customers

•Significant entry barriers arise due to the high capital requirements to setup a tyre manufacturing plant. As per ICRA Report, a plant with an annual capacity of 1 million cross ply Truck and Bus Tyres cost around Rs.6 billion.

Entry Barriers

The Inception Of the Case Of Collusion Against Major Tyre Players in Indian Market

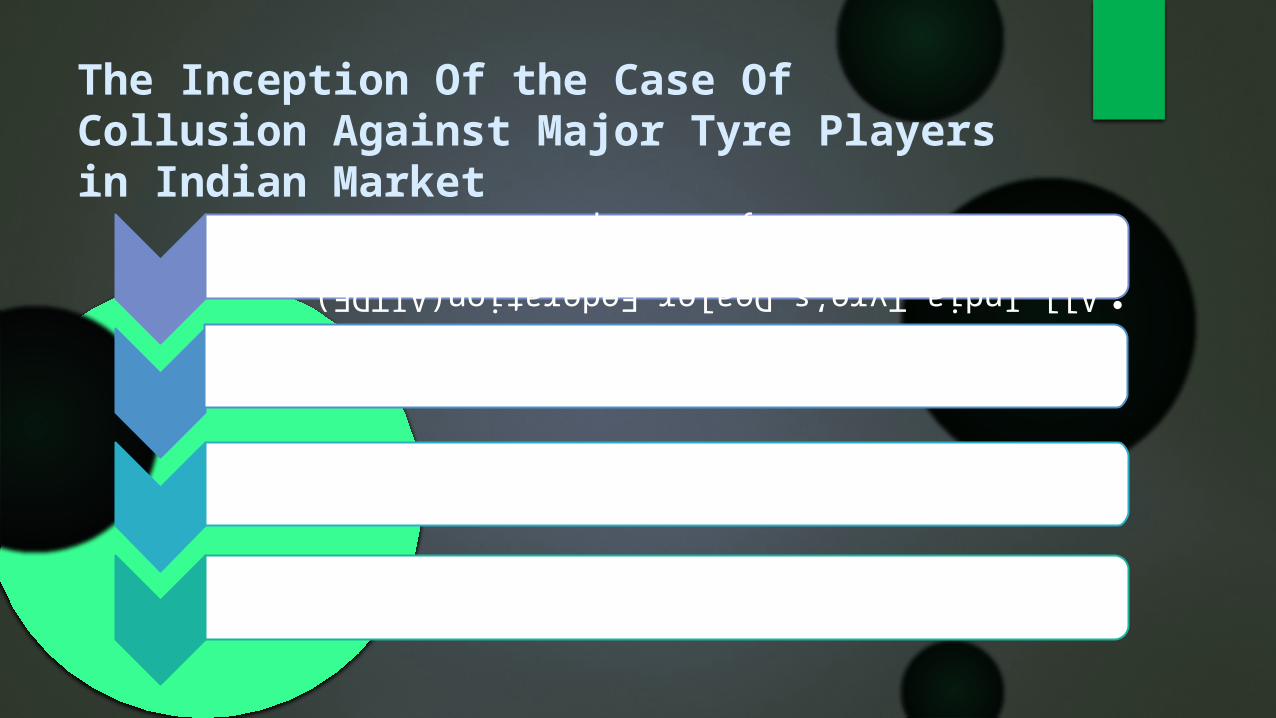

•All India Tyre’s Dealer Federation(AITDF) filed a complaint against tyre manufacturers before the ministry of corporate affairs.

•The Ministry forwarded the case to the MRTP commission.

•Finally the case was transferred to the Competition Commission Of India (CCI).

•The CCI directed the DG (I&R) to conduct an investigation into this matter.

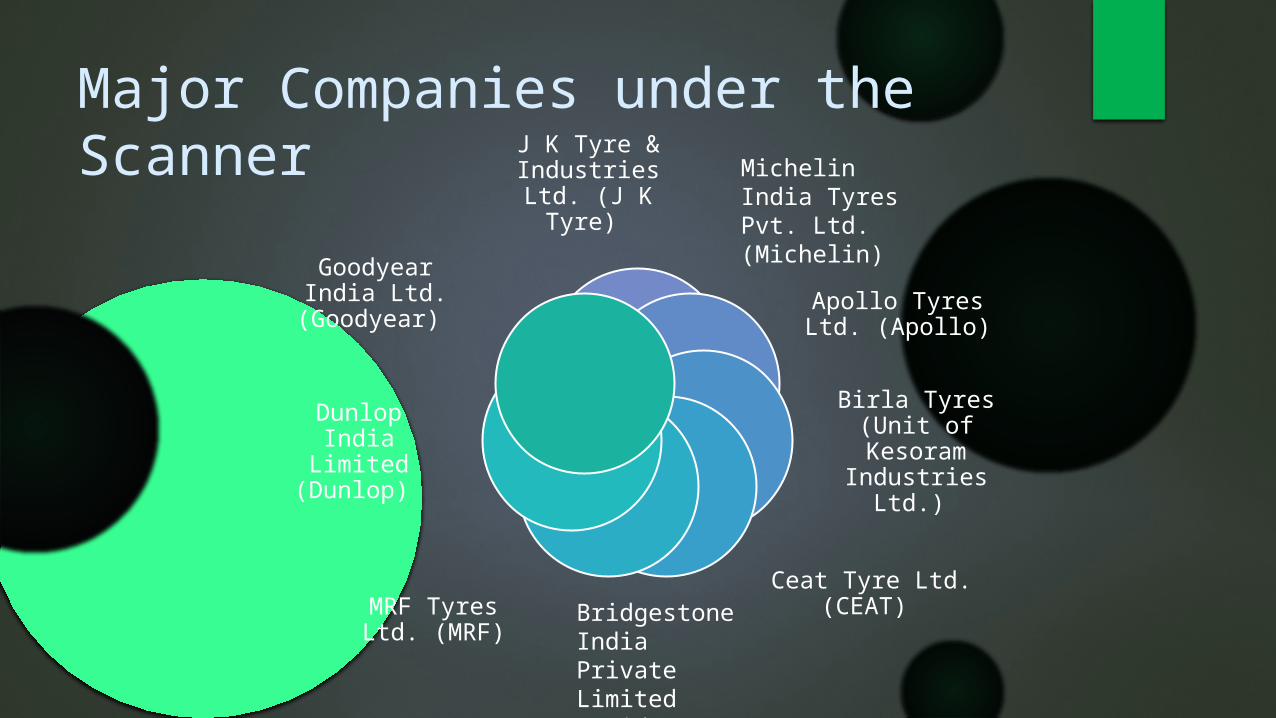

Major Companies under the ScannerJ K Tyre &

Industries Ltd. (J K Tyre)

Apollo Tyres Ltd. (Apollo)

Birla Tyres (Unit of Kesoram

Industries Ltd.)

Ceat Tyre Ltd. (CEAT) MRF Tyres Ltd. (MRF)

Dunlop India Limited (Dunlop)

Goodyear India Ltd. (Goodyear)

Bridgestone India Private Limited (Bridgestone)

Michelin India Tyres Pvt. Ltd. (Michelin)

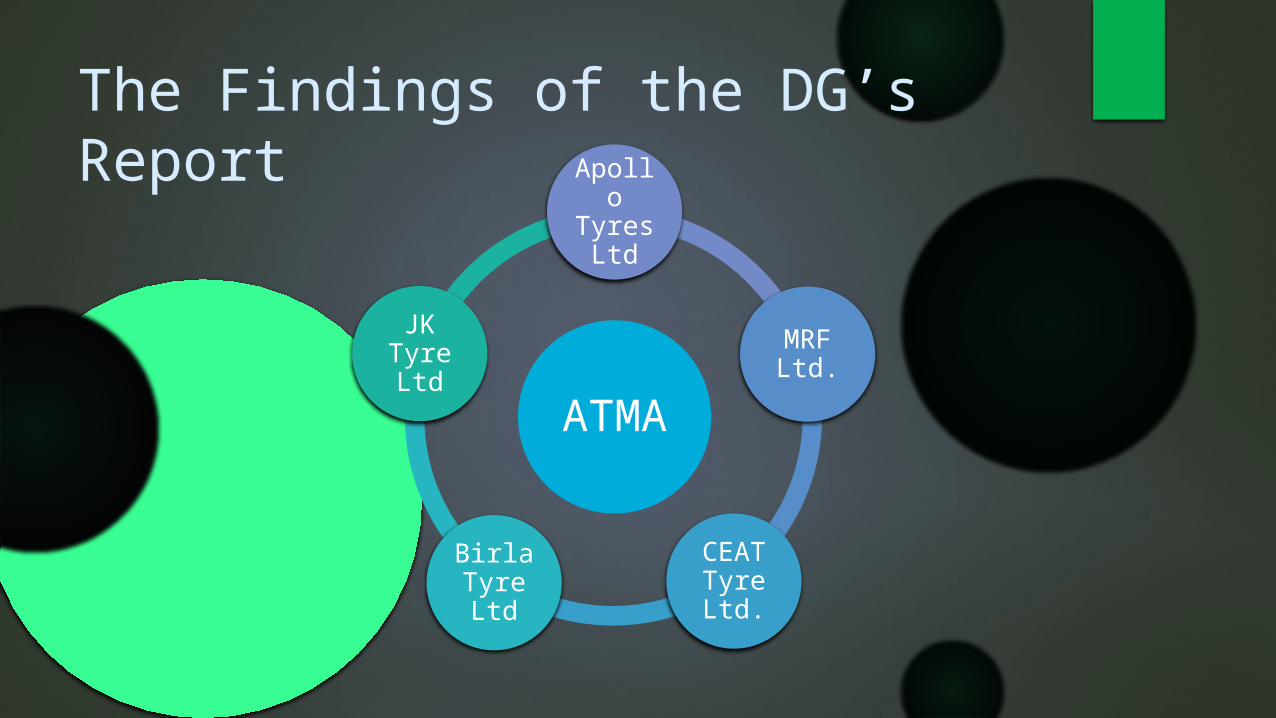

The Findings of the DG’s Report

ATMA

Apollo Tyres Ltd

MRF Ltd.

CEAT Tyre Ltd.

Birla Tyre Ltd

JK Tyre Ltd

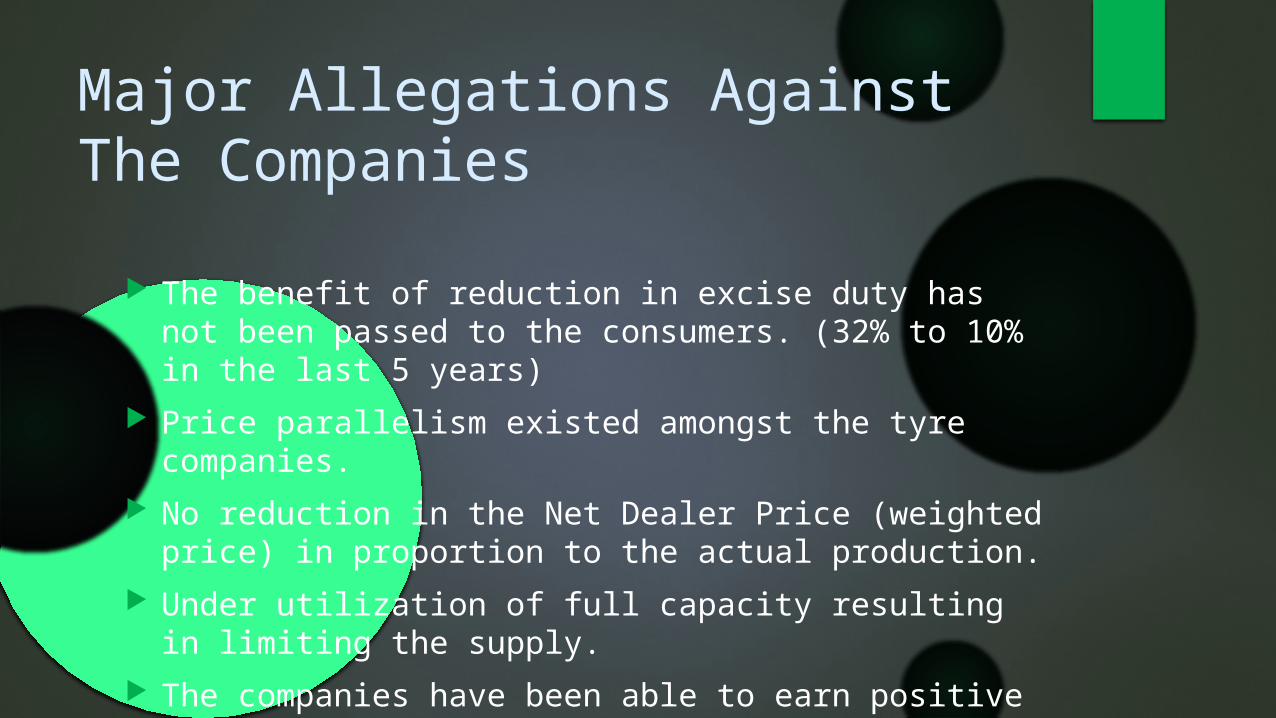

Major Allegations Against The Companies

The benefit of reduction in excise duty has not been passed to the consumers. (32% to 10% in the last 5 years)

Price parallelism existed amongst the tyre companies. No reduction in the Net Dealer Price (weighted price) in proportion

to the actual production. Under utilization of full capacity resulting in limiting the supply. The companies have been able to earn positive margins in most of

the period under investigation.

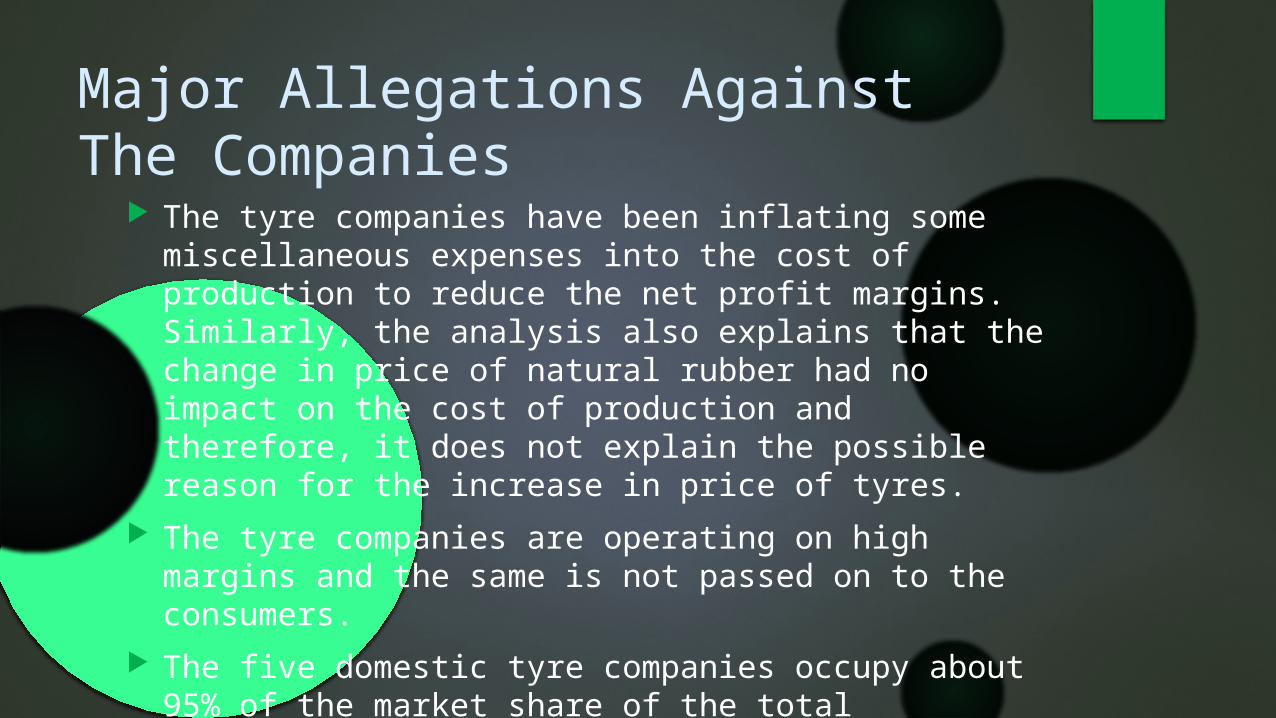

Major Allegations Against The Companies

The tyre companies have been inflating some miscellaneous expenses into the cost of production to reduce the net profit margins. Similarly, the analysis also explains that the change in price of natural rubber had no impact on the cost of production and therefore, it does not explain the possible reason for the increase in price of tyres.

The tyre companies are operating on high margins and the same is not passed on to the consumers.

The five domestic tyre companies occupy about 95% of the market share of the total production. This high concentration made OEMs and the replacement market highly dependent on these companies.

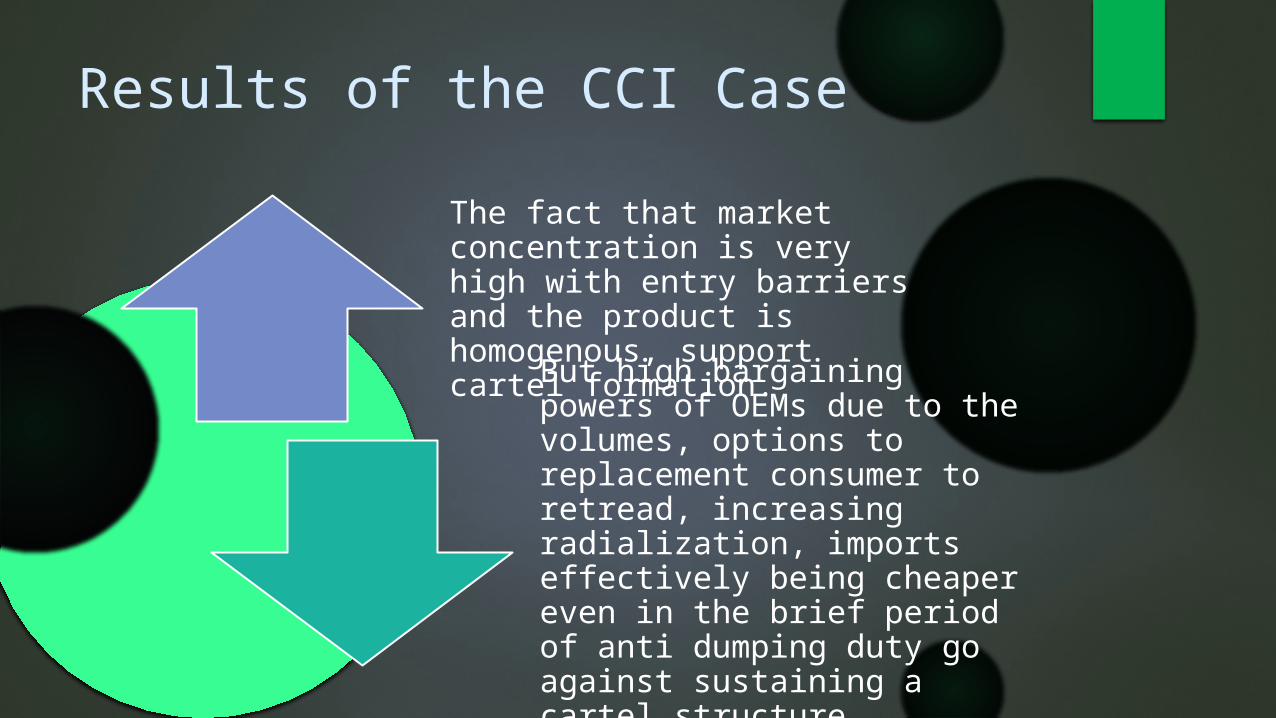

Results of the CCI Case

The fact that market concentration is very high with entry barriers and the product is homogenous, support cartel formation.

But high bargaining powers of OEMs due to the volumes, options to replacement consumer to retread, increasing radialization, imports effectively being cheaper even in the brief period of anti dumping duty go against sustaining a cartel structure.

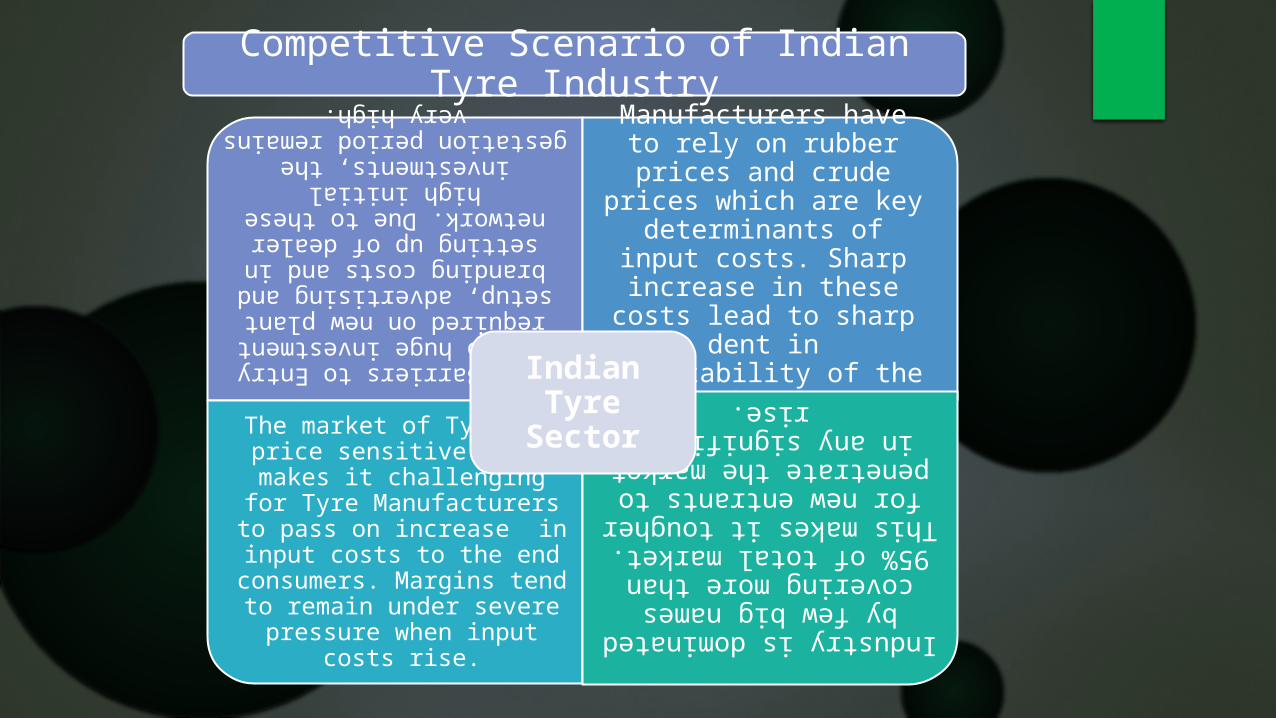

Competitive Scenario of Indian Tyre Industry

High Barriers to Entry due to huge

investment required on new

plant setup, advertising and

branding costs and in setting up of dealer network.

Due to these high initial investments,

the gestation period remains

very high.

Manufacturers have to rely on rubber prices and crude prices which are key determinants of input costs. Sharp increase in these costs lead to sharp dent in profitability of the industry.

The market of Tyres is price sensitive which makes it

challenging for Tyre Manufacturers to pass on increase in input costs

to the end consumers. Margins tend to remain under severe

pressure when input costs rise.

Industry is dominated by few big names covering more

than 95% of total market. This

makes it tougher for new entrants to penetrate the

market in any significant rise.

Indian Tyre Sector

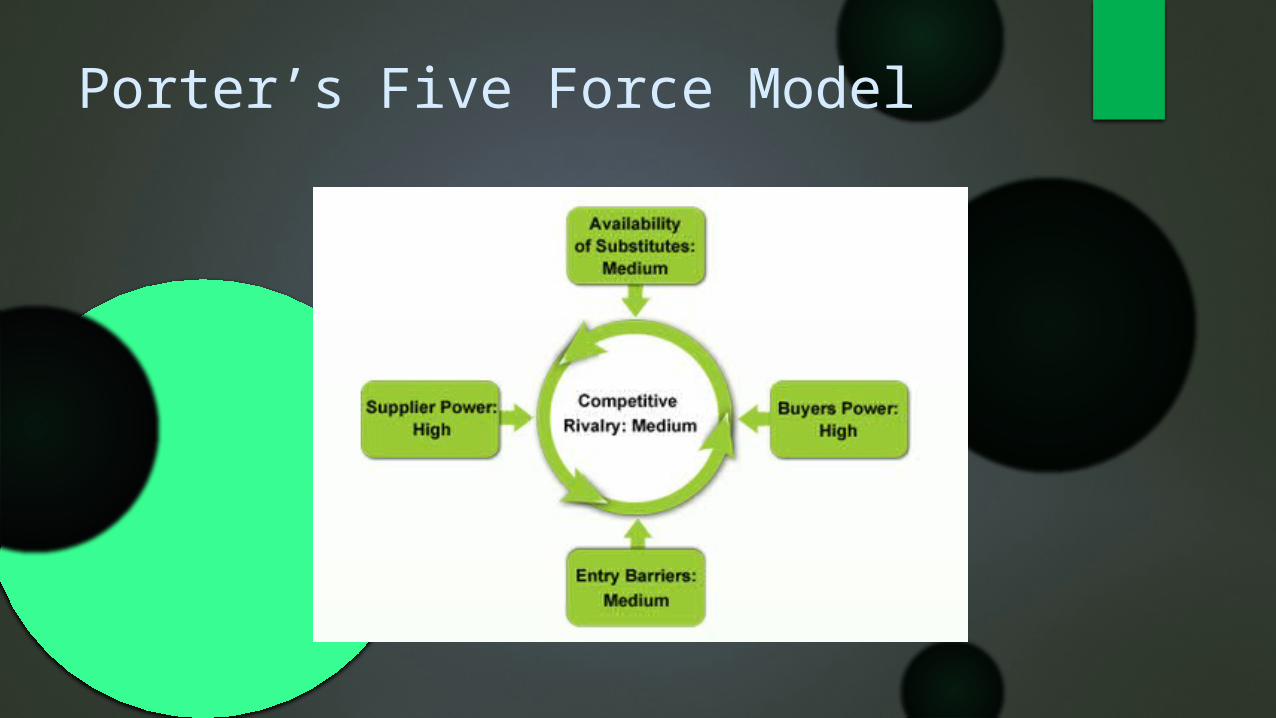

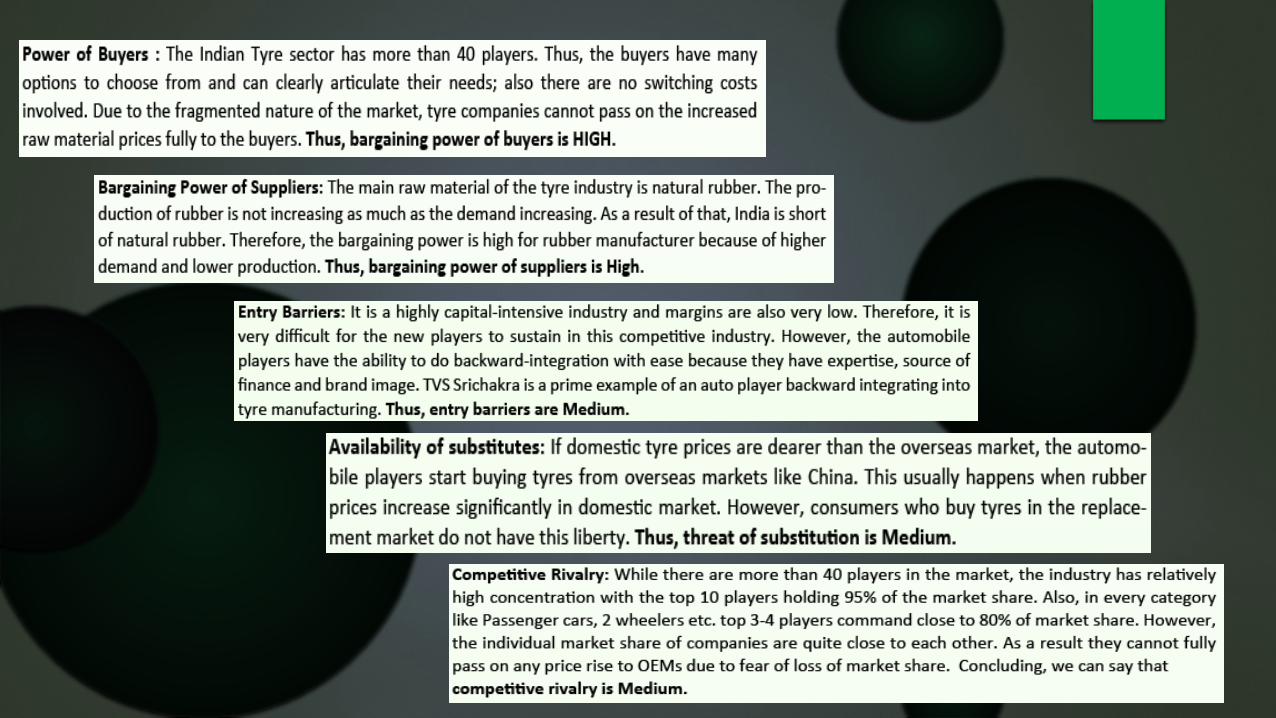

Porter’s Five Force Model

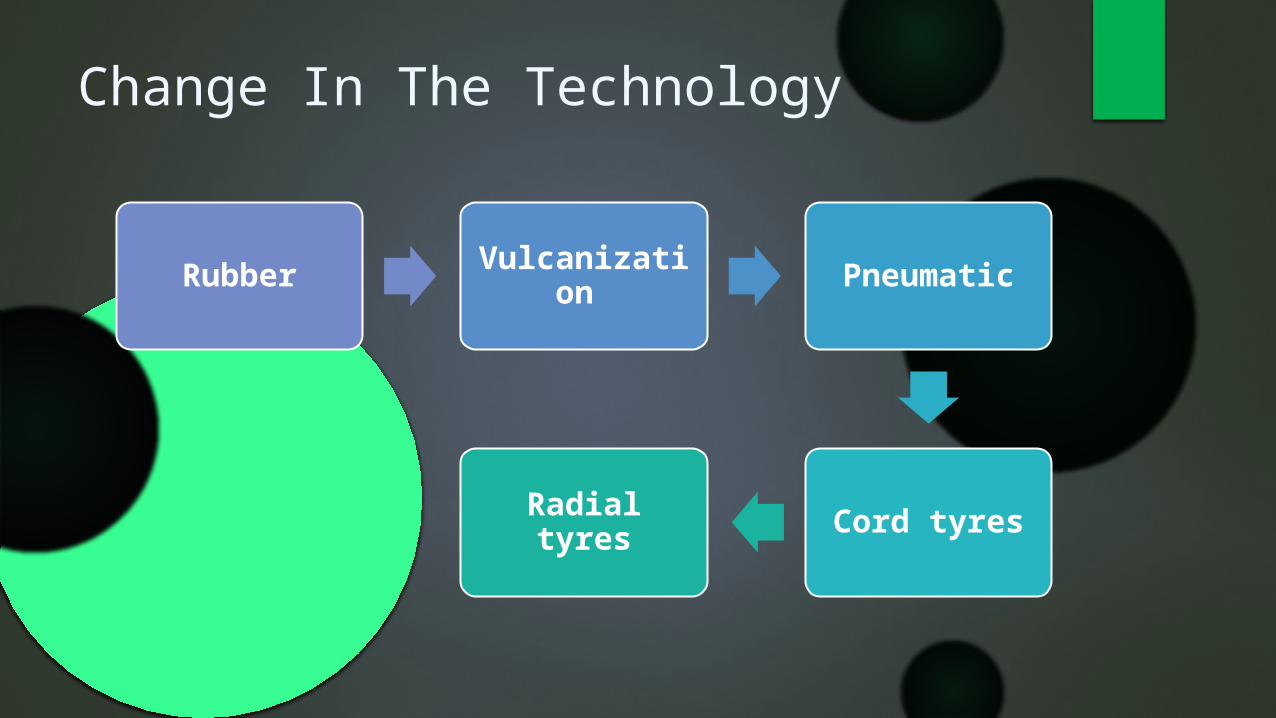

Change In The Technology

Rubber Vulcanization Pneumatic

Cord tyresRadial tyres

Before The Advent Of Vulcanized Rubber

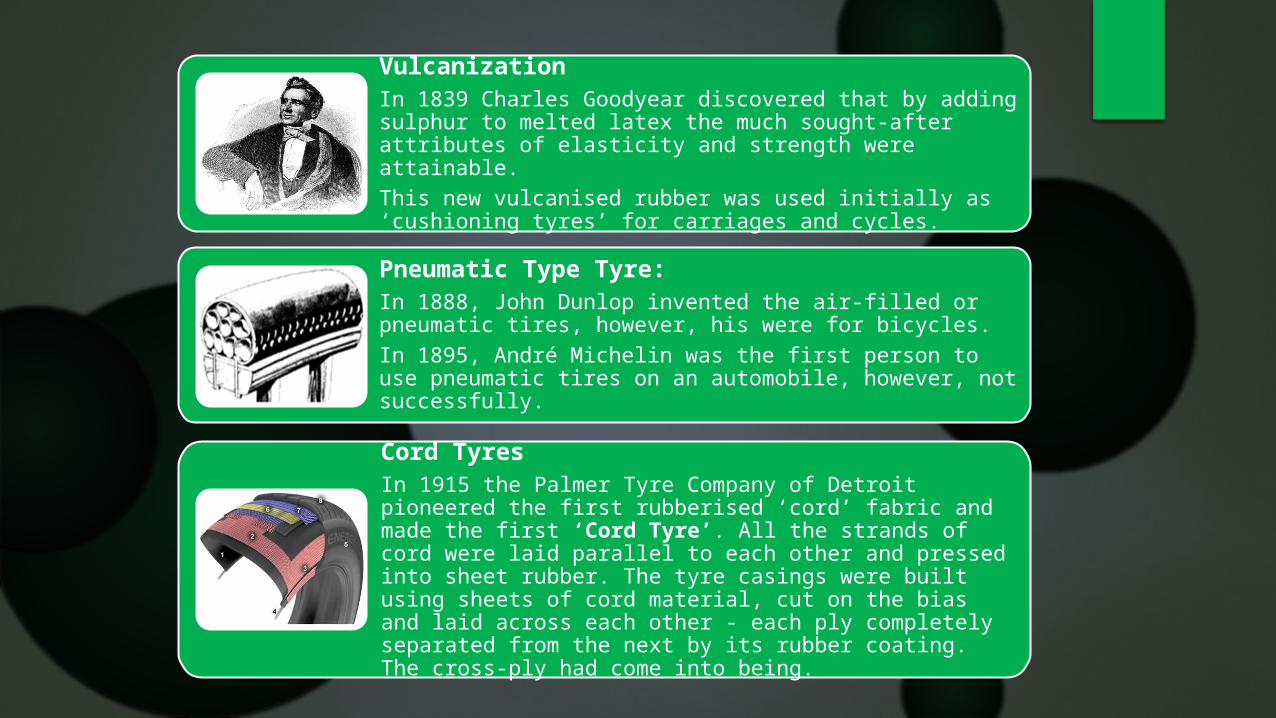

VulcanizationIn 1839 Charles Goodyear discovered that by adding sulphur to melted latex the much sought-after attributes of elasticity and strength were attainable. This new vulcanised rubber was used initially as ‘cushioning tyres’ for carriages and cycles.

Pneumatic Type Tyre:In 1888, John Dunlop invented the air-filled or pneumatic tires, however, his were for bicycles. In 1895, André Michelin was the first person to use pneumatic tires on an automobile, however, not successfully.

Cord TyresIn 1915 the Palmer Tyre Company of Detroit pioneered the first rubberised ‘cord’ fabric and made the first ‘Cord Tyre’. All the strands of cord were laid parallel to each other and pressed into sheet rubber. The tyre casings were built using sheets of cord material, cut on the bias and laid across each other - each ply completely separated from the next by its rubber coating. The cross-ply had come into being.

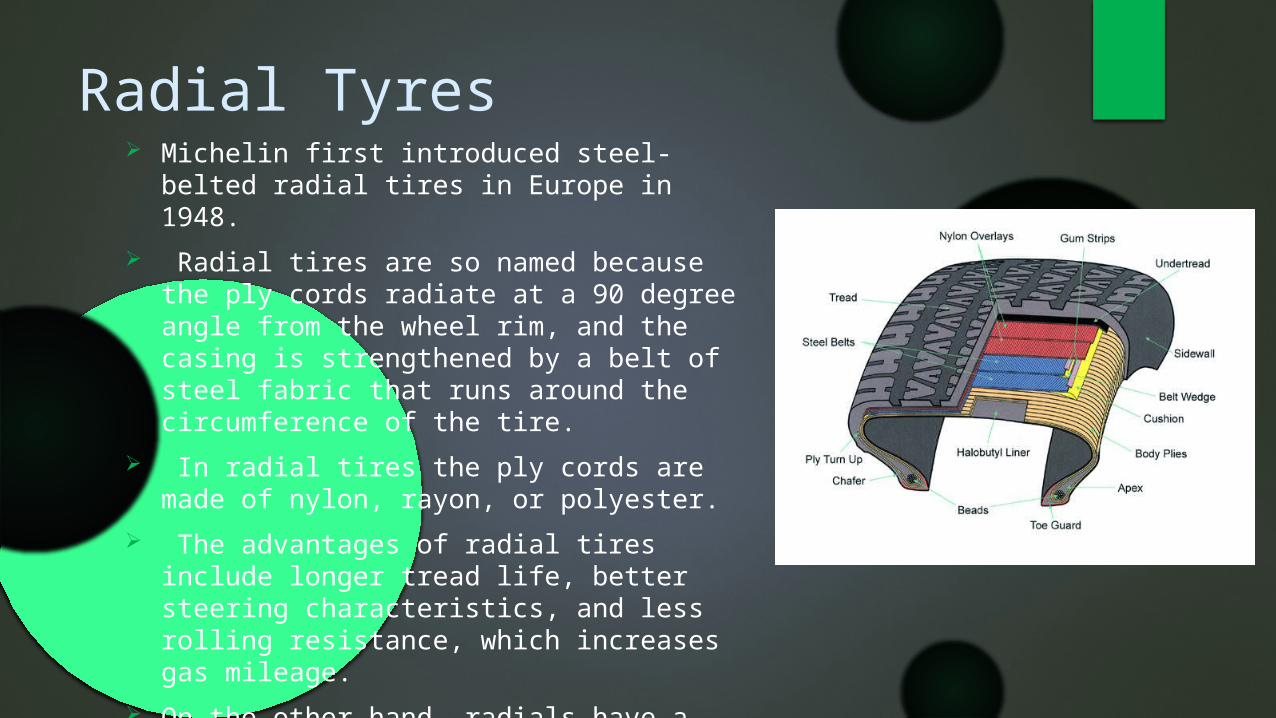

Radial Tyres Michelin first introduced steel-belted radial tires in

Europe in 1948. Radial tires are so named because the ply cords radiate

at a 90 degree angle from the wheel rim, and the casing is strengthened by a belt of steel fabric that runs around the circumference of the tire.

In radial tires the ply cords are made of nylon, rayon, or polyester.

The advantages of radial tires include longer tread life, better steering characteristics, and less rolling resistance, which increases gas mileage.

On the other hand, radials have a harder riding quality, and since they are technologically more complex than bias-ply tires, they are about 45 percent more expensive to make.

Technological Advancement In the Recent Years

Run Flat Tyres• One of the major recent

developments in the tyre world has been the continuing popularity of run flat tyres.

• These allow a car to continue to move safely despite its tyres losing pressure - i.e. because they have run flat.

• Latest available technology is a gel tyre “bonded” to the tyre that means the tyres become similar to a run flat.

Eco Tyres• So-called Low Rolling Resistance tyres are made by adding silica to the tread compound of a tyre. This affects the amount of energy a tyre can absorb while it is turning or ‘rolling’. The less resistance caused during rolling, the less fuel your car requires to move.

• What’s the end result for the motorist? Well according to Michelin, eco tyres can save the average motorist £65.00 a year.

Nitrogen• Filling your tyres with nitrogen

may seem odd but that’s exactly what motor sport and aviation professionals have been doing for years. Nitrogen is completely safe.

• And by using it in a mixture with oxygen to inflate your tyres the theory is that it’s possible to negate the issue of slow deflation, which is caused by oxygen slowly infusing through the tyre wall from the atmosphere.

• Having a tyre that does not deflate means you will improve fuel consumption and will probably improve safety standards too.

Thank You

Group Members:

Pallav Prasad

Pooja Kanjani

Raghvi Maheshwari

Ravi Kumar Singh

Rincy Sarah John

Rahul Arora