Embed Size (px)

Citation preview

Trading processes and Exchange

platforms

Institutional and organizational designs of the gas hubs in

Europe: An introduction to the Iberian Gas Hub

24th June 2014, Bilbao

2

Exchange trading inside PEGAS

Interactions between gas market participants – role allocation

Preconditions for a positive hub development

Agenda

3

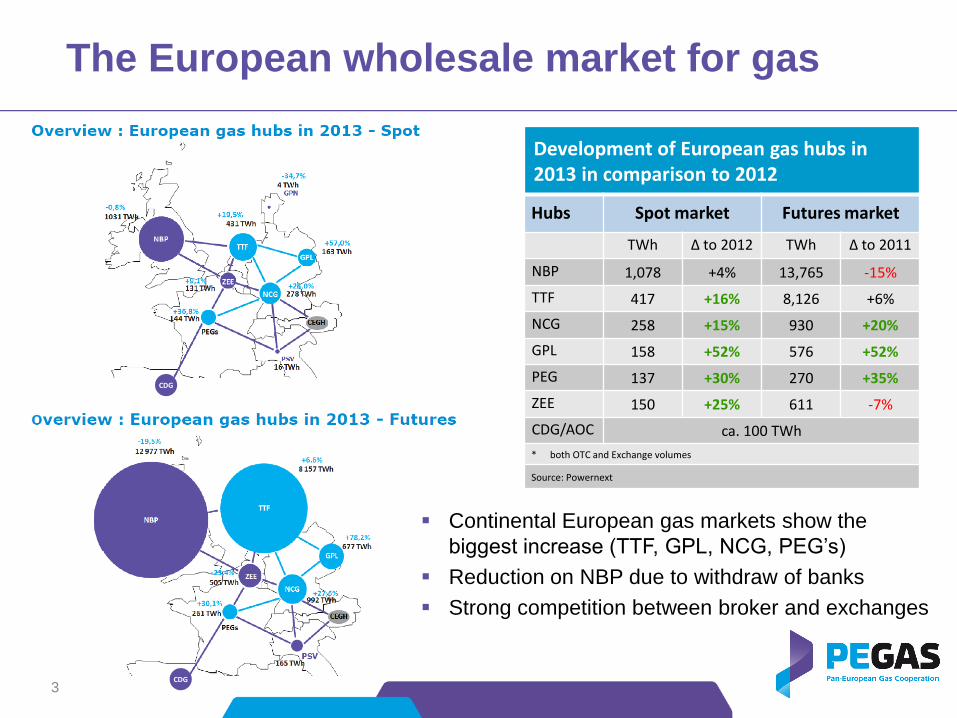

The European wholesale market for gas

Development of European gas hubs in 2013 in comparison to 2012

Hubs Spot market Futures market

TWh Δ to 2012 TWh Δ to 2011

NBP 1,078 +4% 13,765 -15%

TTF 417 +16% 8,126 +6%

NCG 258 +15% 930 +20%

GPL 158 +52% 576 +52%

PEG 137 +30% 270 +35%

ZEE 150 +25% 611 -7%

CDG/AOC ca. 100 TWh

* both OTC and Exchange volumes

Source: Powernext

Continental European gas markets show the

biggest increase (TTF, GPL, NCG, PEG’s)

Reduction on NBP due to withdraw of banks

Strong competition between broker and exchanges

CDG

CDG

4

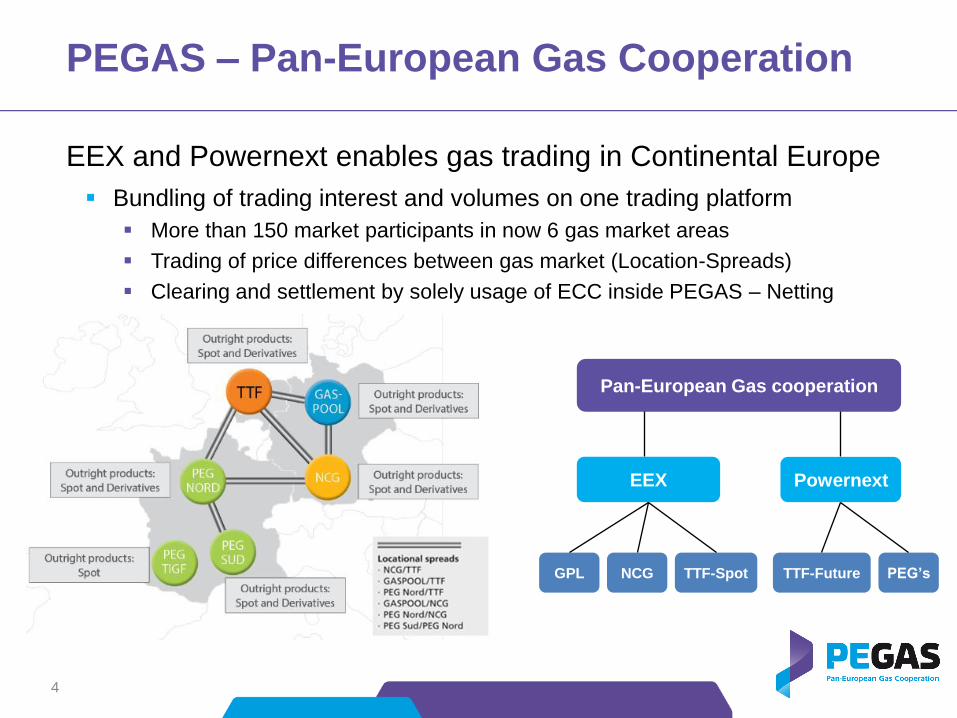

PEGAS – Pan-European Gas Cooperation

Bundling of trading interest and volumes on one trading platform

More than 150 market participants in now 6 gas market areas

Trading of price differences between gas market (Location-Spreads)

Clearing and settlement by solely usage of ECC inside PEGAS – Netting

EEX and Powernext enables gas trading in Continental Europe

Powernext

Pan-European Gas cooperation

EEX

PEG’s TTF-Future TTF-Spot NCG GPL

5

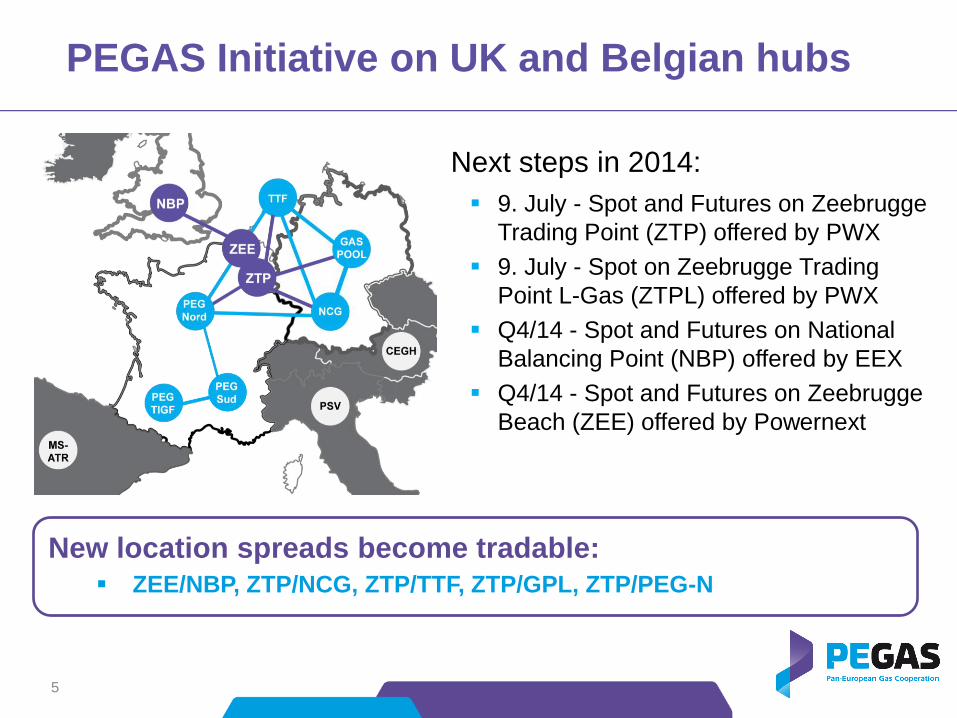

PEGAS Initiative on UK and Belgian hubs

Next steps in 2014:

9. July - Spot and Futures on Zeebrugge

Trading Point (ZTP) offered by PWX

9. July - Spot on Zeebrugge Trading

Point L-Gas (ZTPL) offered by PWX

Q4/14 - Spot and Futures on National

Balancing Point (NBP) offered by EEX

Q4/14 - Spot and Futures on Zeebrugge

Beach (ZEE) offered by Powernext

New location spreads become tradable:

ZEE/NBP, ZTP/NCG, ZTP/TTF, ZTP/GPL, ZTP/PEG-N

6

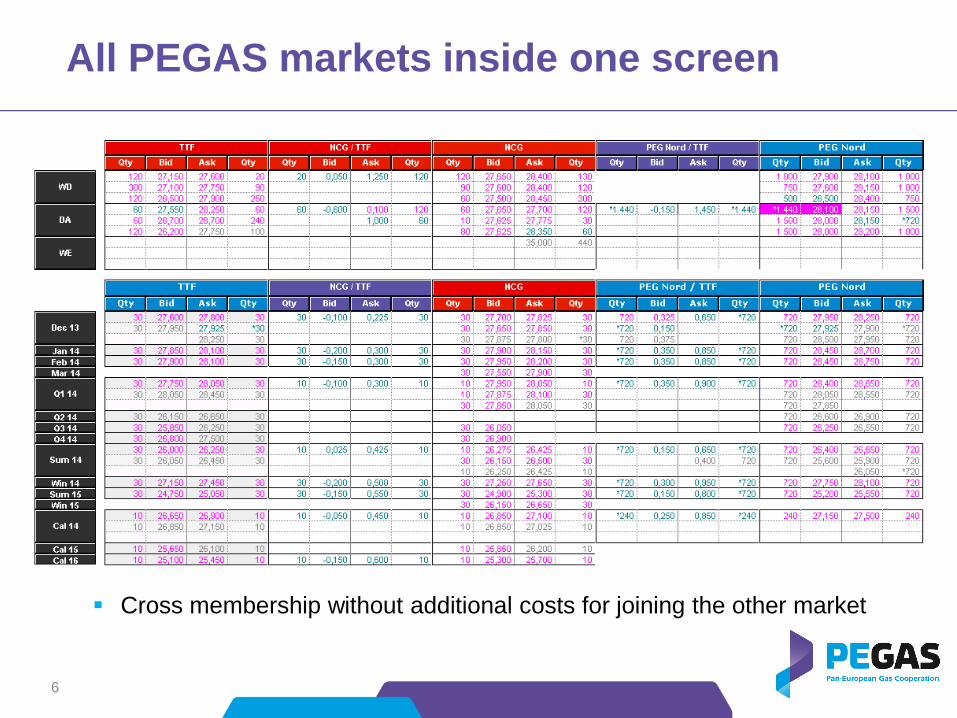

All PEGAS markets inside one screen

Cross membership without additional costs for joining the other market

7

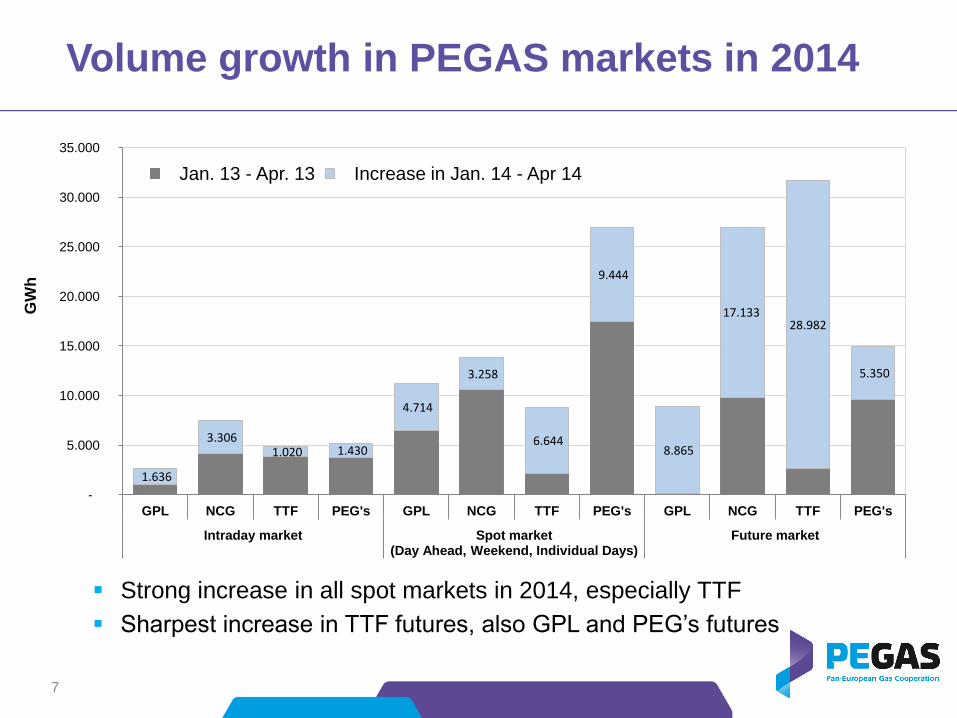

Volume growth in PEGAS markets in 2014

1.636

3.306 1.020 1.430

4.714

3.258

6.644

9.444

8.865

17.133 28.982

5.350

-

5.000

10.000

15.000

20.000

25.000

30.000

35.000

GPL NCG TTF PEG's GPL NCG TTF PEG's GPL NCG TTF PEG's

Intraday market Spot market (Day Ahead, Weekend, Individual Days)

Future market

GW

h

Jan. 13 - Apr. 13 Increase in Jan. 14 - Apr 14

Strong increase in all spot markets in 2014, especially TTF

Sharpest increase in TTF futures, also GPL and PEG’s futures

8

0

20

40

60

80

100

120

140

160

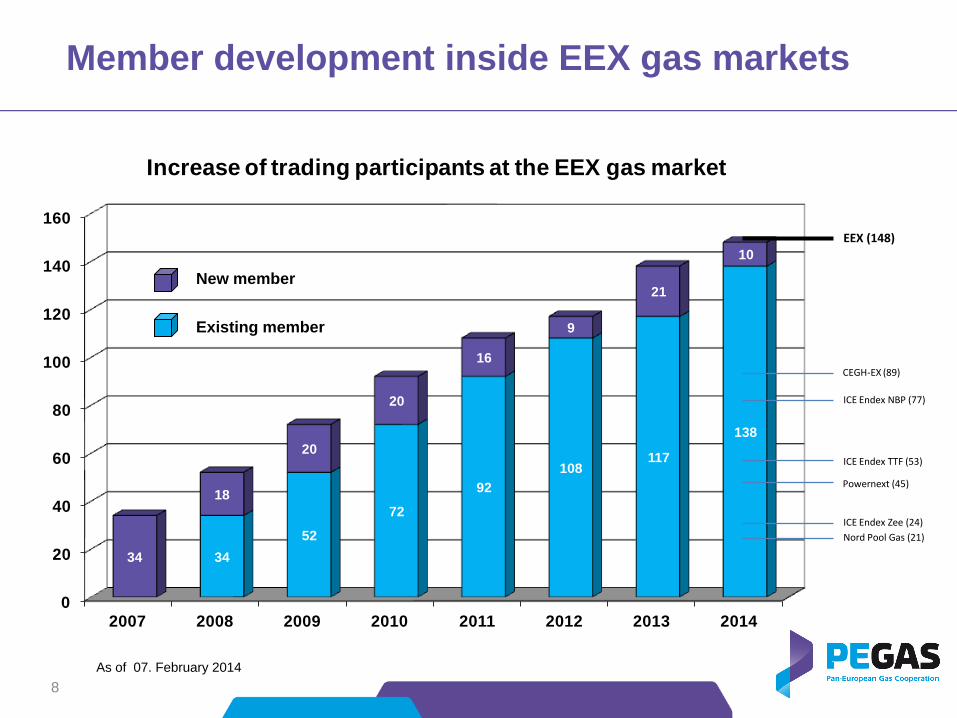

2007 2008 2009 2010 2011 2012 2013 2014

34

52

72

92

108117

138

34

18

20

20

16

9

21

10

Increase of trading participants at the EEX gas market

Member development inside EEX gas markets

New member

Existing member

CEGH-EX (89)

ICE Endex Zee (24)

ICE Endex TTF (53)

ICE Endex NBP (77)

Powernext (45)

Nord Pool Gas (21)

EEX (148)

As of 07. February 2014

9

Exchange trading inside PEGAS

Interactions between gas market participants – role allocation

Preconditions for a positive hub development

Agenda

10

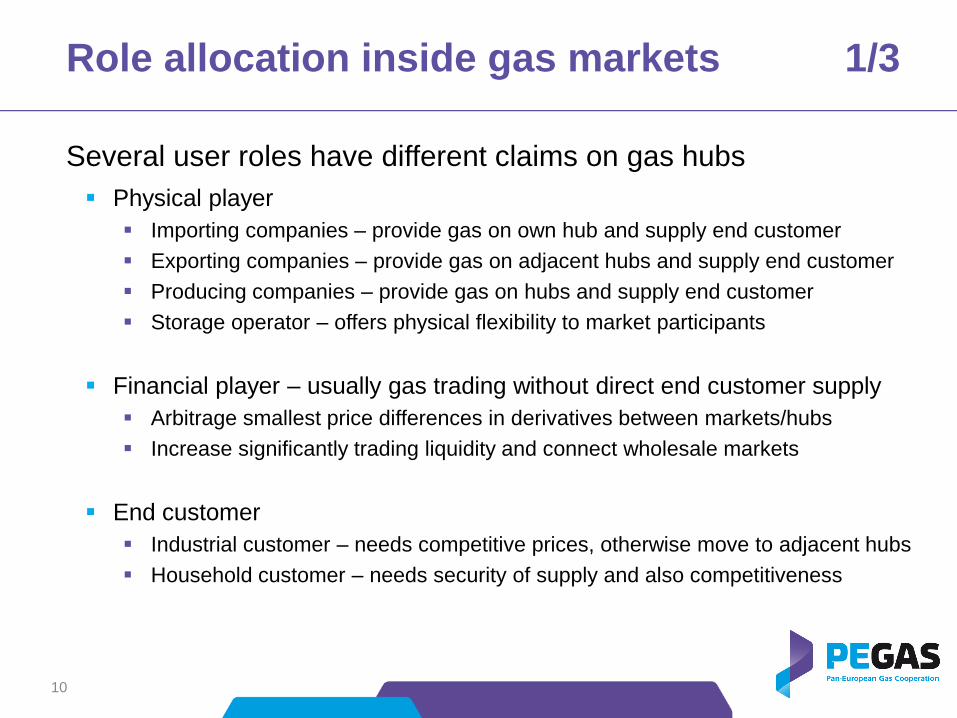

Role allocation inside gas markets 1/3

Physical player

Importing companies – provide gas on own hub and supply end customer

Exporting companies – provide gas on adjacent hubs and supply end customer

Producing companies – provide gas on hubs and supply end customer

Storage operator – offers physical flexibility to market participants

Financial player – usually gas trading without direct end customer supply

Arbitrage smallest price differences in derivatives between markets/hubs

Increase significantly trading liquidity and connect wholesale markets

End customer

Industrial customer – needs competitive prices, otherwise move to adjacent hubs

Household customer – needs security of supply and also competitiveness

Several user roles have different claims on gas hubs

11

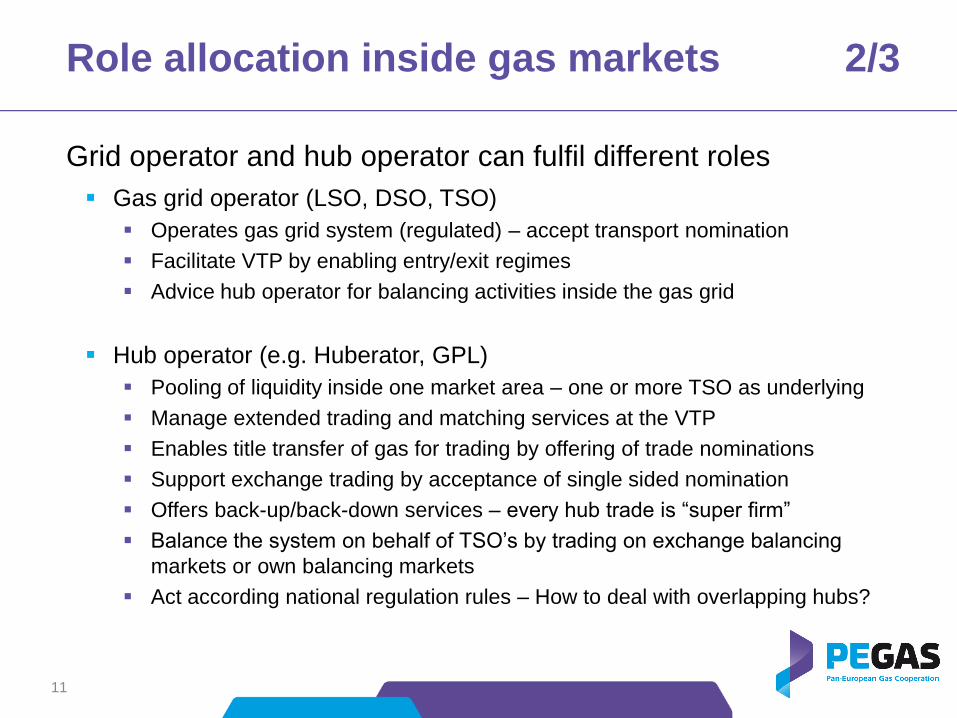

Role allocation inside gas markets 2/3

Gas grid operator (LSO, DSO, TSO)

Operates gas grid system (regulated) – accept transport nomination

Facilitate VTP by enabling entry/exit regimes

Advice hub operator for balancing activities inside the gas grid

Hub operator (e.g. Huberator, GPL)

Pooling of liquidity inside one market area – one or more TSO as underlying

Manage extended trading and matching services at the VTP

Enables title transfer of gas for trading by offering of trade nominations

Support exchange trading by acceptance of single sided nomination

Offers back-up/back-down services – every hub trade is “super firm”

Balance the system on behalf of TSO’s by trading on exchange balancing

markets or own balancing markets

Act according national regulation rules – How to deal with overlapping hubs?

Grid operator and hub operator can fulfil different roles

12

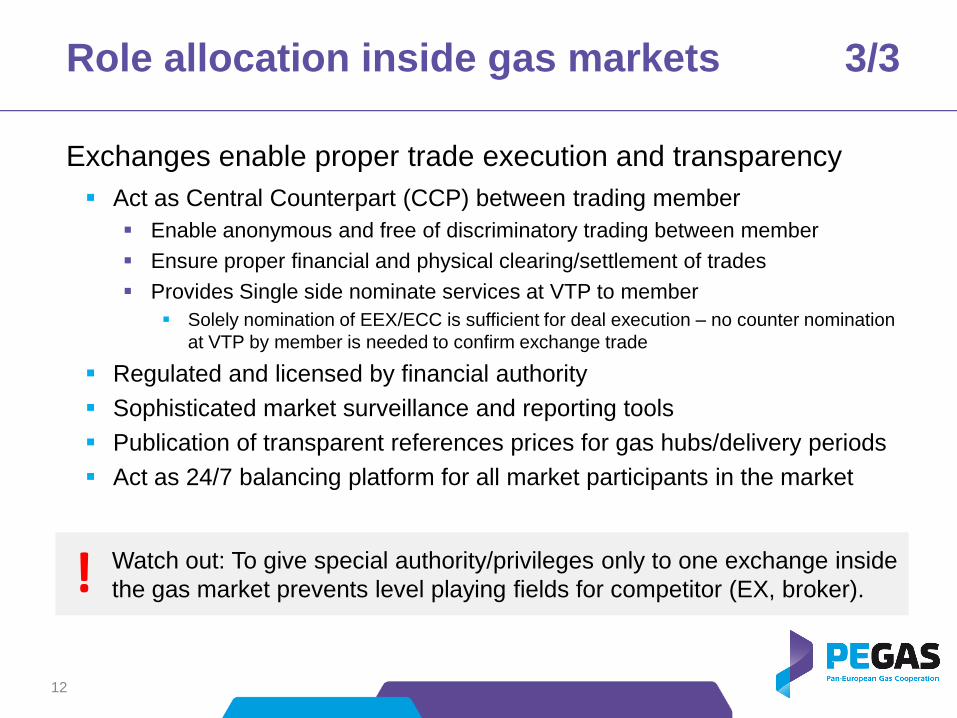

Role allocation inside gas markets 3/3

Act as Central Counterpart (CCP) between trading member

Enable anonymous and free of discriminatory trading between member

Ensure proper financial and physical clearing/settlement of trades

Provides Single side nominate services at VTP to member

Solely nomination of EEX/ECC is sufficient for deal execution – no counter nomination

at VTP by member is needed to confirm exchange trade

Regulated and licensed by financial authority

Sophisticated market surveillance and reporting tools

Publication of transparent references prices for gas hubs/delivery periods

Act as 24/7 balancing platform for all market participants in the market

Exchanges enable proper trade execution and transparency

Watch out: To give special authority/privileges only to one exchange inside

the gas market prevents level playing fields for competitor (EX, broker). !

13

Exchange trading inside PEGAS

Interactions between gas market participants – role allocation

Preconditions for a positive hub development

Agenda

14

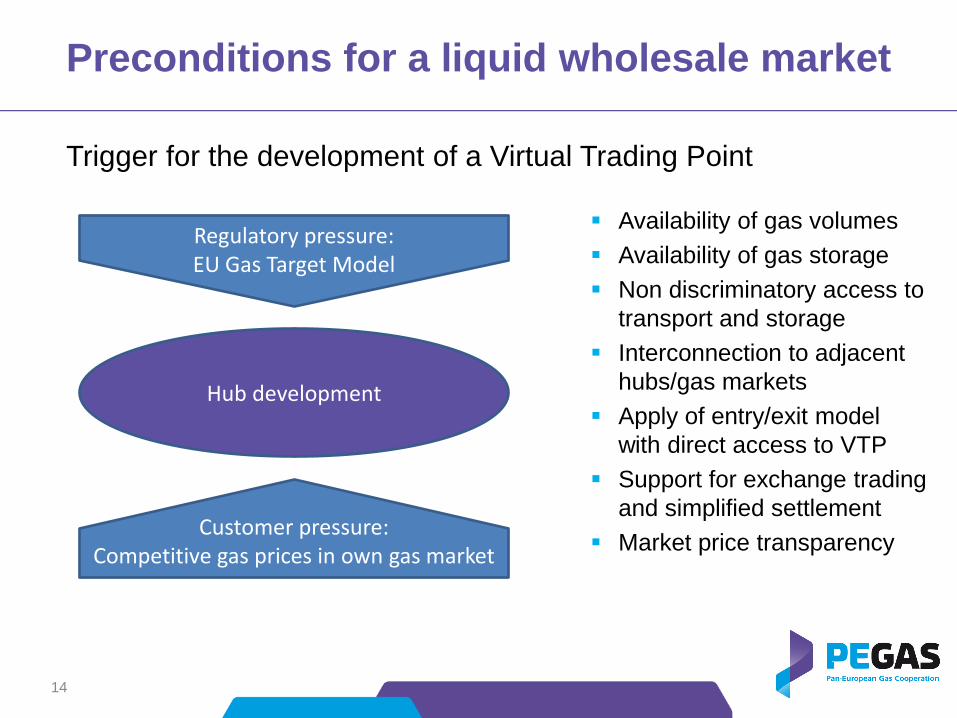

Preconditions for a liquid wholesale market

Availability of gas volumes

Availability of gas storage

Non discriminatory access to

transport and storage

Interconnection to adjacent

hubs/gas markets

Apply of entry/exit model

with direct access to VTP

Support for exchange trading

and simplified settlement

Market price transparency

Trigger for the development of a Virtual Trading Point

Regulatory pressure: EU Gas Target Model

Customer pressure: Competitive gas prices in own gas market

Hub development

15

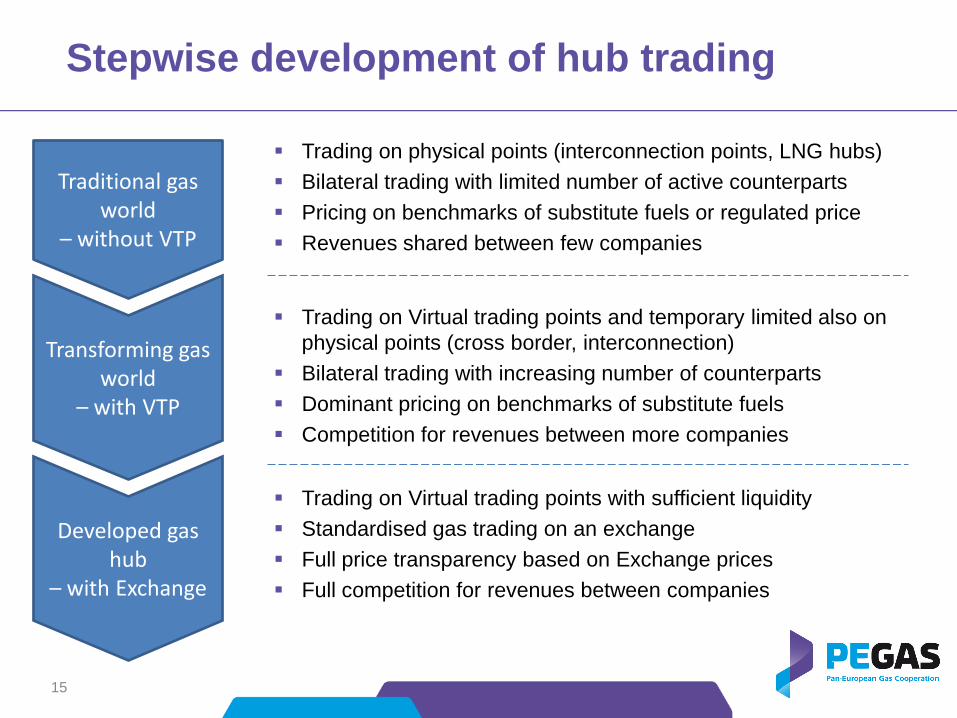

Stepwise development of hub trading

Trading on physical points (interconnection points, LNG hubs)

Bilateral trading with limited number of active counterparts

Pricing on benchmarks of substitute fuels or regulated price

Revenues shared between few companies

Traditional gas world

– without VTP

Transforming gas world

– with VTP

Trading on Virtual trading points and temporary limited also on

physical points (cross border, interconnection)

Bilateral trading with increasing number of counterparts

Dominant pricing on benchmarks of substitute fuels

Competition for revenues between more companies

Trading on Virtual trading points with sufficient liquidity

Standardised gas trading on an exchange

Full price transparency based on Exchange prices

Full competition for revenues between companies

Developed gas hub

– with Exchange

16

5

10

15

20

25

30

35

Ga

s p

ric

es

in €

pe

r M

Wh

Delivery month

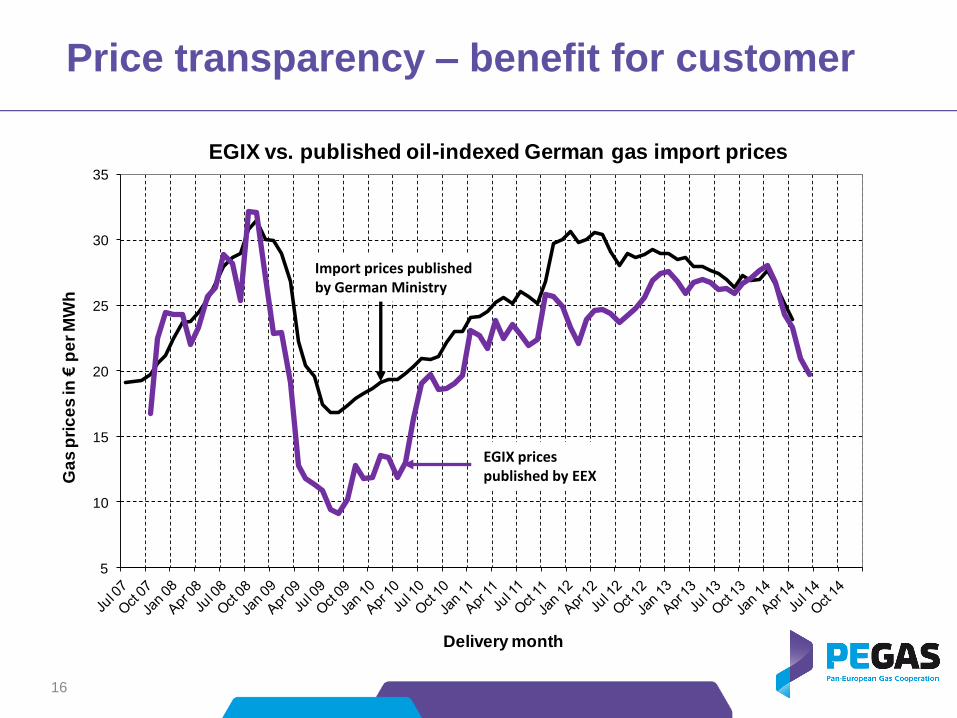

EGIX vs. published oil-indexed German gas import prices

Price transparency – benefit for customer

Import prices published by German Ministry

EGIX prices published by EEX

17

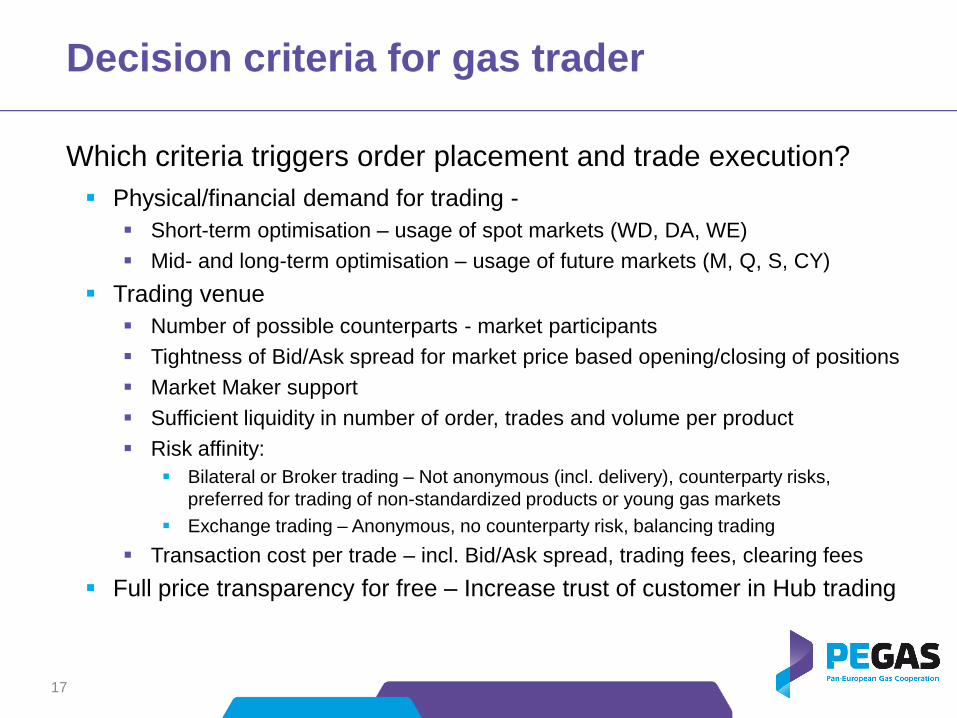

Decision criteria for gas trader

Physical/financial demand for trading -

Short-term optimisation – usage of spot markets (WD, DA, WE)

Mid- and long-term optimisation – usage of future markets (M, Q, S, CY)

Trading venue

Number of possible counterparts - market participants

Tightness of Bid/Ask spread for market price based opening/closing of positions

Market Maker support

Sufficient liquidity in number of order, trades and volume per product

Risk affinity:

Bilateral or Broker trading – Not anonymous (incl. delivery), counterparty risks,

preferred for trading of non-standardized products or young gas markets

Exchange trading – Anonymous, no counterparty risk, balancing trading

Transaction cost per trade – incl. Bid/Ask spread, trading fees, clearing fees

Full price transparency for free – Increase trust of customer in Hub trading

Which criteria triggers order placement and trade execution?

18

Conclusion

Market size – big enough?

Member support – strong enough?

Level playing field for all market player – fair enough?

Balancing trading at the exchange – transparent enough?

Price transparency by usage of hub pricing – Relying enough?

Hubs/VTP could be developed under consideration of

Any more questions?

More information available under www.pegas-trading.com