Embed Size (px)

Citation preview

The Role of Funders in Digital Finance: Peer Experiences

9 March 2016

What we will cover: Peer Experiences

• How do you select and work with partners?

• How to you understand and work with the incentives of market actors/partners?

• What are your key lessons from a funder perspective?

2

CGAP LEARNING EVENT FOR DFS FUNDERS

Bill and Melinda Gates Foundation

Presented by Jason Lamb

© 2014 Bill & Melinda Gates Foundation

March 9, 2016

© Bill & Melinda Gates Foundation | 4

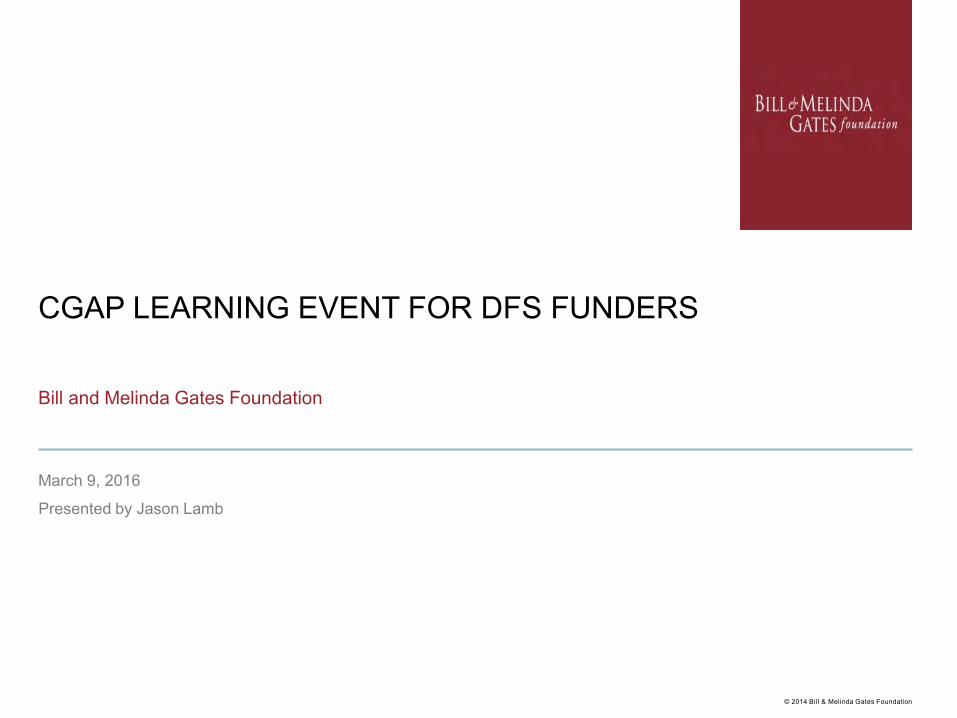

STAGES OF MARKET DEVELOPMENT Regulations and digital payment infrastructures are precursors to a full digital payment ecosystem and high impact services

Enabling Environment

Digital Payment Platform

Digital Payment Ecosystem

High Impact Digital Financial Services

Basic Connectivity Critical mass of mobile coverage and penetration amongst rural poor

1 Enabling regulations that support poor people to open accounts and providers to outsource distribution, and to protect users

2 Poor people adopt and use low-cost digital systems for P2P, basic transfers, and interoperability

3 Poor people get money, spend money, and conduct financial transactions digitally, including bulk, many-to-on, pay-as-you-go, and proximity payments .

4

India

Nigeria

Indonesia

Pakistan

Uganda

Bangladesh

Poor people adopt and use digital to move out of poverty and stay out of poverty

Kenya

Tanzania

Home | Intro | Appendix What If |

What If: We could turn a 30 day sign up process into 30 seconds?

What If: Everyone was an agent?

What If: Anyone with a phone could send or receive money?

What If: Payment processing was digital and close to zero in cost?

What If: You could send money to any person in the world?

What If: Every mobile phone came with a savings account and insurance?

What If: Assessing risk for a billion new customers was cost-effective?

Customer Activation Distribution Payments Front-End

Payments Back-End Integration Products Analytics

What If

© Bill & Melinda Gates Foundation | 6

© Bill & Melinda Gates Foundation | 6

GLOBAL PARTNER FOCUS: BETTER THAN CASH ALLIANCE

OBJECTIVES

The Better Than Cash Alliance partners with governments, companies, and international organizations that are the key drivers behind the transition to make digital payments widely available by: Advocating for the transition from cash to digital payments in a way that advances financial inclusion and promotes responsible digital finance. Conducting Research and sharing the experiences of our members to inform strategies for making the transition. Catalyzing the development of inclusive digital payments ecosystems in member countries to reduce costs, increase transparency, advance financial inclusion– particularly for women– and drive inclusive growth.

MEMBERS • 16 governments (including India,

Bangladesh, Pakistan, Mexico) • 18 international organizations • 2 companies • 7 resource partners

GEOGRAPHIC FOCUS

• GLOBAL

2016 FUNDING COMMITMENT

$1.2M

RESOURCE PARTNERS

• Bill & Melinda Gates Foundation • Citi Foundation • MasterCard • Omidyar Network • USAID • VISA • UNCDF

© Bill & Melinda Gates Foundation | 7

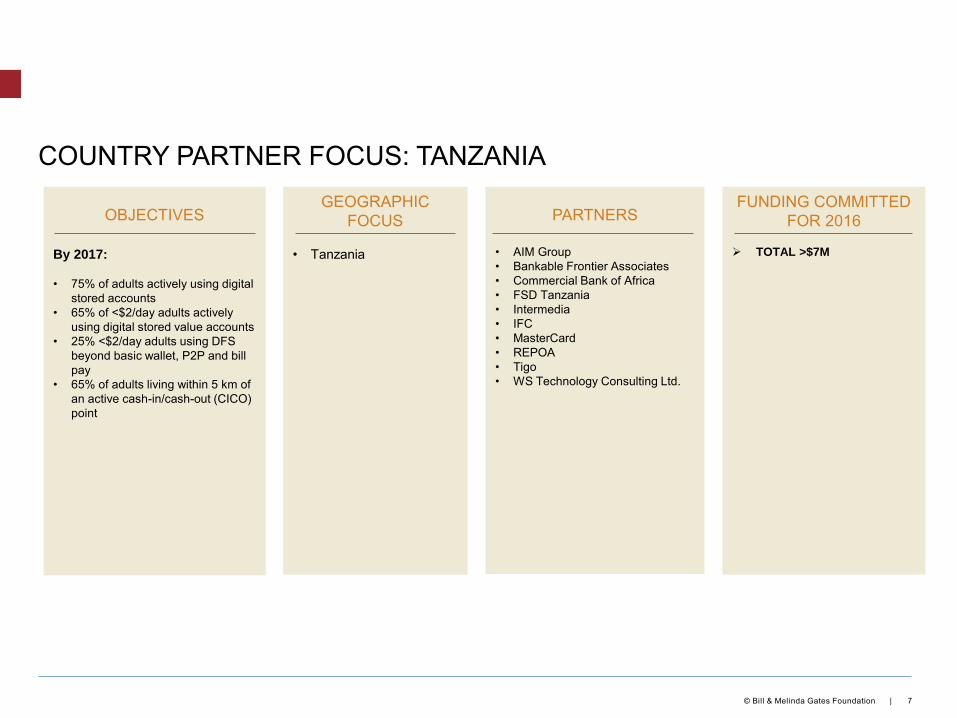

COUNTRY PARTNER FOCUS: TANZANIA

OBJECTIVES

By 2017:

• 75% of adults actively using digital stored accounts

• 65% of <$2/day adults actively using digital stored value accounts

• 25% <$2/day adults using DFS beyond basic wallet, P2P and bill pay

• 65% of adults living within 5 km of an active cash-in/cash-out (CICO) point

PARTNERS • AIM Group • Bankable Frontier Associates • Commercial Bank of Africa • FSD Tanzania • Intermedia • IFC • MasterCard • REPOA • Tigo • WS Technology Consulting Ltd.

GEOGRAPHIC FOCUS

• Tanzania

FUNDING COMMITTED FOR 2016

TOTAL >$7M

© Bill & Melinda Gates Foundation | 8

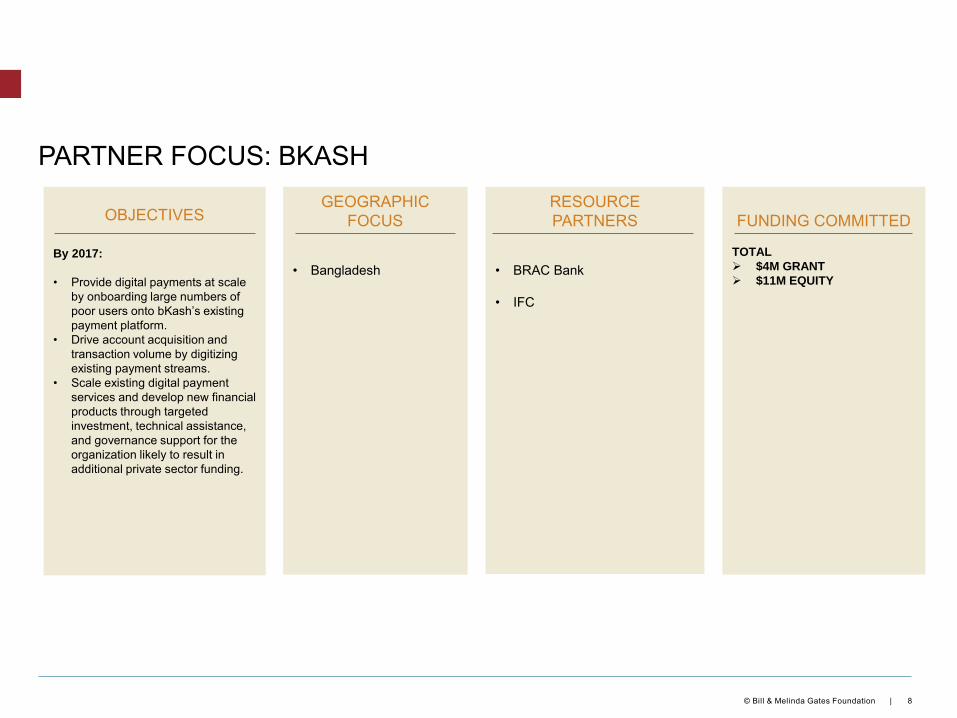

PARTNER FOCUS: BKASH

OBJECTIVES By 2017:

• Provide digital payments at scale

by onboarding large numbers of poor users onto bKash’s existing payment platform.

• Drive account acquisition and transaction volume by digitizing existing payment streams.

• Scale existing digital payment services and develop new financial products through targeted investment, technical assistance, and governance support for the organization likely to result in additional private sector funding.

RESOURCE PARTNERS

• BRAC Bank

• IFC

GEOGRAPHIC FOCUS

• Bangladesh

FUNDING COMMITTED

TOTAL

$4M GRANT

$11M EQUITY

THANK YOU

IFC Partnership for Financial Inclusion

10

Funders Roundtable Paris – CGAP

Wednesday 9 March 2016

David Crush, Program Manager IFC

The Why

Could Mobile Financial Services

transform your business?

Source: GSMA, State of the Industry 2014

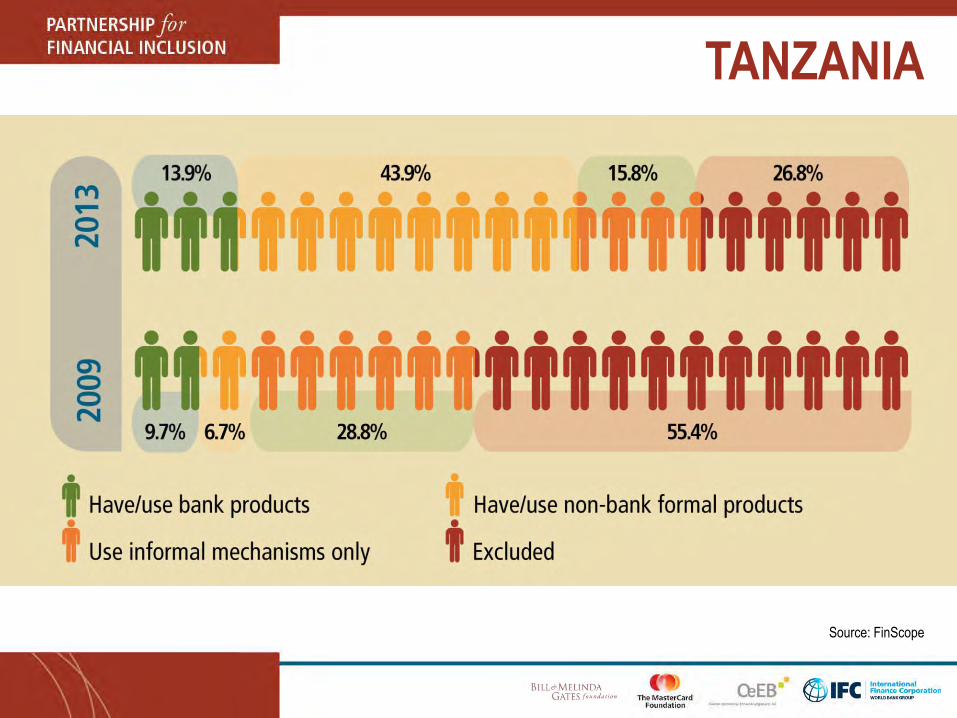

Source: FinScope

TANZANIA

The What

Digital Financial Services?

supply

chain payments

government

disbursements credit

insurance bill

payments

payroll

services

local

remittances

savings

products

supply

chain

payments

social

payments

airtime

top up pension

contributions

retail

purchases

PAYMENTS

SAVINGS

LOANS INSURANCE

TV ON DEMAND

PAYG SOLAR POWER

PAYG WATER

AGRICULTURAL

MICRO-INSURANCE

HEALTH SERVICES PAYG TEXTBOOKS

The How

FORMAT: A joint initiative by IFC and The MasterCard Foundation. TIMELINE: Started in 2011, ends in December 2018. OBJECTIVE: Expand microfinance and advance digital financial services in Sub-Saharan Africa. FUNDING: $37.4 million from MCF CLIENTS: Microfinance institutions, banks, MNOs DELIVERABLES:

• Bank 5.3 million previously unbanked people in Sub-Saharan Africa • Develop and test innovative business models to advance financial

inclusion • Research and Knowledge sharing program for the industry and the

public good

OTHER PARTNERS: Development Bank of Austria, Bill & Melinda Gates Foundation, CGAP, SECO and World Bank.

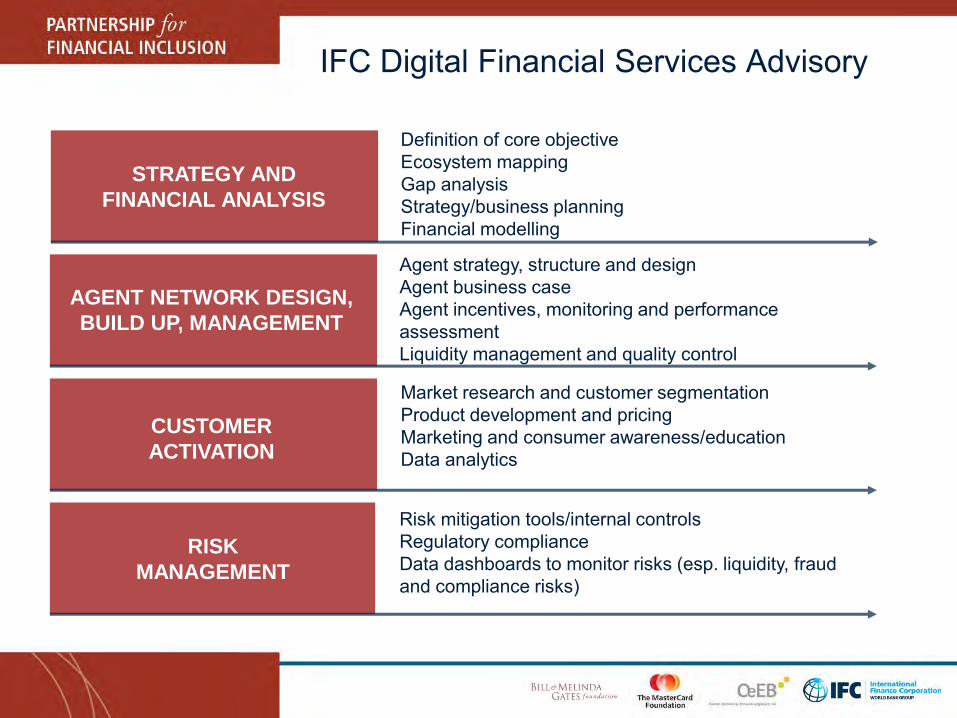

STRATEGY AND

FINANCIAL ANALYSIS

CUSTOMER

ACTIVATION

AGENT NETWORK DESIGN,

BUILD UP, MANAGEMENT

RISK

MANAGEMENT

Definition of core objective Ecosystem mapping Gap analysis Strategy/business planning Financial modelling

Agent strategy, structure and design Agent business case Agent incentives, monitoring and performance assessment Liquidity management and quality control

Market research and customer segmentation Product development and pricing Marketing and consumer awareness/education Data analytics

Risk mitigation tools/internal controls Regulatory compliance Data dashboards to monitor risks (esp. liquidity, fraud and compliance risks)

IFC Digital Financial Services Advisory

The Who

BENEFITS FOR OUR CLIENTS

Increased geographical reach Reaching new market segments Lower operational cost Increased efficiency Lower cost of funds (deposit mobilization) Reduced churn (MNOs) Competitive edge

BENEFITS FOR IFC

Increased portfolio value (existing clients) Impact/bank accounts towards 2020 goal of

universal financial access Center of excellence/expertise on DFS Leads on IS Fintech pipeline Competitive edge in AS market

BENEFITS FOR OUR PARTNERS

Advancing donor objectives Market based rigour Leveraging DFI client relationships Leveraging DFI partner relationships Channel for funding Well tested theories of change

BENEFITS FOR END USERS

Improved service levels Greater competition and choice Increased accessibility Improved efficiency Lower costs Greater protection and security

Annex

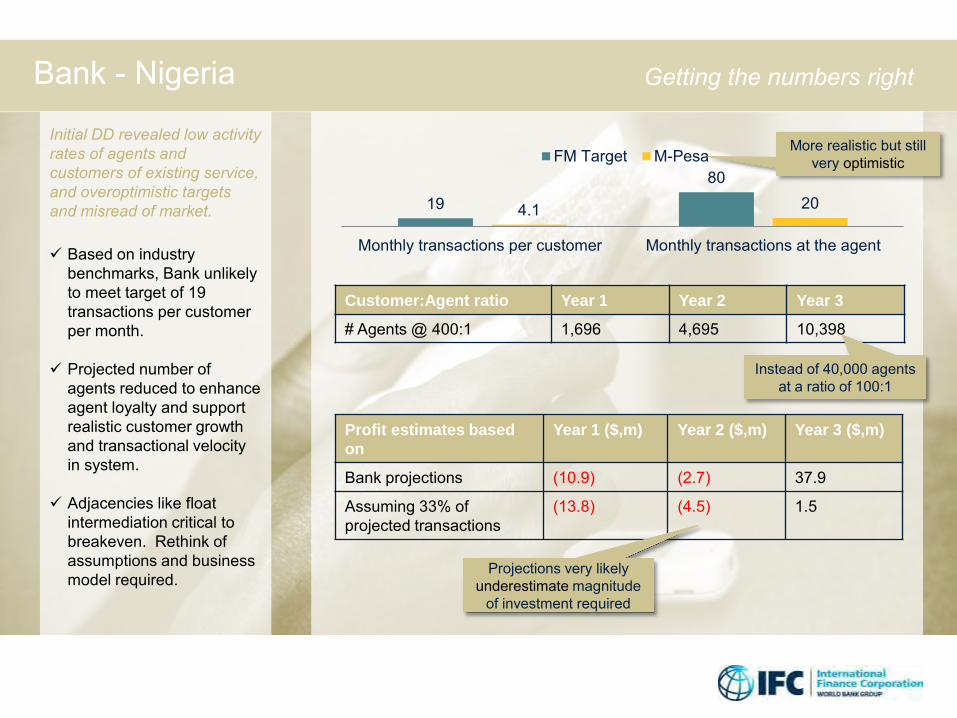

Bank - Nigeria

Customer:Agent ratio Year 1 Year 2 Year 3

# Agents @ 400:1 1,696 4,695 10,398

Instead of 40,000 agents at a ratio of 100:1

19 80

4.1 20

Monthly transactions per customer Monthly transactions at the agent

FM Target M-Pesa

Profit estimates based

on

Year 1 ($,m) Year 2 ($,m)

Year 3 ($,m)

Bank projections (10.9) (2.7) 37.9

Assuming 33% of projected transactions

(13.8) (4.5) 1.5

Projections very likely underestimate magnitude

of investment required

More realistic but still very optimistic

Initial DD revealed low activity rates of agents and customers of existing service, and overoptimistic targets and misread of market.

Based on industry benchmarks, Bank unlikely to meet target of 19 transactions per customer per month.

Projected number of agents reduced to enhance agent loyalty and support realistic customer growth and transactional velocity in system.

Adjacencies like float intermediation critical to breakeven. Rethink of assumptions and business model required.

Getting the numbers right

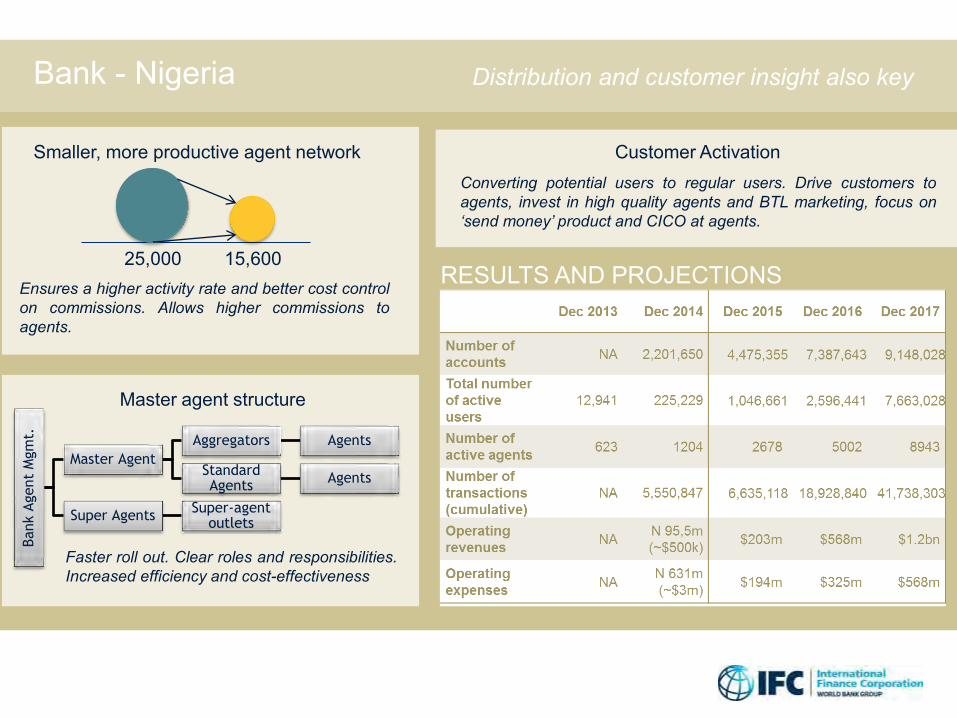

Bank - Nigeria Distribution and customer insight also key

25,000 15,600 Ensures a higher activity rate and better cost control on commissions. Allows higher commissions to agents.

Smaller, more productive agent network

Bank A

gent

Mgm

t.

Master Agent

Aggregators Agents

Standard Agents

Agents

Super Agents Super-agent

outlets

Master agent structure

Faster roll out. Clear roles and responsibilities. Increased efficiency and cost-effectiveness

Customer Activation Converting potential users to regular users. Drive customers to agents, invest in high quality agents and BTL marketing, focus on ‘send money’ product and CICO at agents.

RESULTS AND PROJECTIONS

MFI – Democratic Republic of Congo Transforming the client

1. CONCEPT

REVIEW

2. FINANCIAL

MODELING

3. BUSINESS

CASE

DEVELOPMENT

4. PILOT 5. IMPLEMENT 6. REVIEW AND

ADJUST

Initial plan developed by MFI was overly ambitious, unrealistically based on direct revenue from agent/mobile channels. Little prioritization or

strategic focus.

IFC specialists work onsite with MFI to develop a narrower plan reflecting MFI’s real priorities: an agent network for deposit mobilization

IFC experts model the business case to test initial assumptions with MFI team, and make adjustments.

IFC MFS specialists support MFI throughout the implementation phase, with regular onsite reviews of agent performance and concrete recommendations to optimize the agent network. Additional support on

data analytics, branding, and market segmentation by IFC experts.

IFC microfinance specialists called upon by MFI to support new scaling-up initiative based on value

delivered by IFC during ADC engagement. Phase II project (including IS) now under discussion.

Advancing financial inclusion to improve the lives of the poor

www.cgap.org