Embed Size (px)

Citation preview

The Data RevolutionCreating customer value in the digital

age

Karin Kruger, KPMG Data & Analytics

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

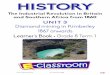

BIG DATA DATA & ANALYTICS

MOBILIZATIONSOCIAL CONNECTEDNESS

CLOUDCOMPUTING

CYBER SECURITY

URBANIZATION

REGULATORY CHANGE

CONSUMER EMPOWERMENT

SHIFTING DEMOGRAPHICS

INFRASTRUCTURE RE-INVESTMENT

GLOBALIZATION

LOW COST / HIGH FUNCTIONING DEVICES

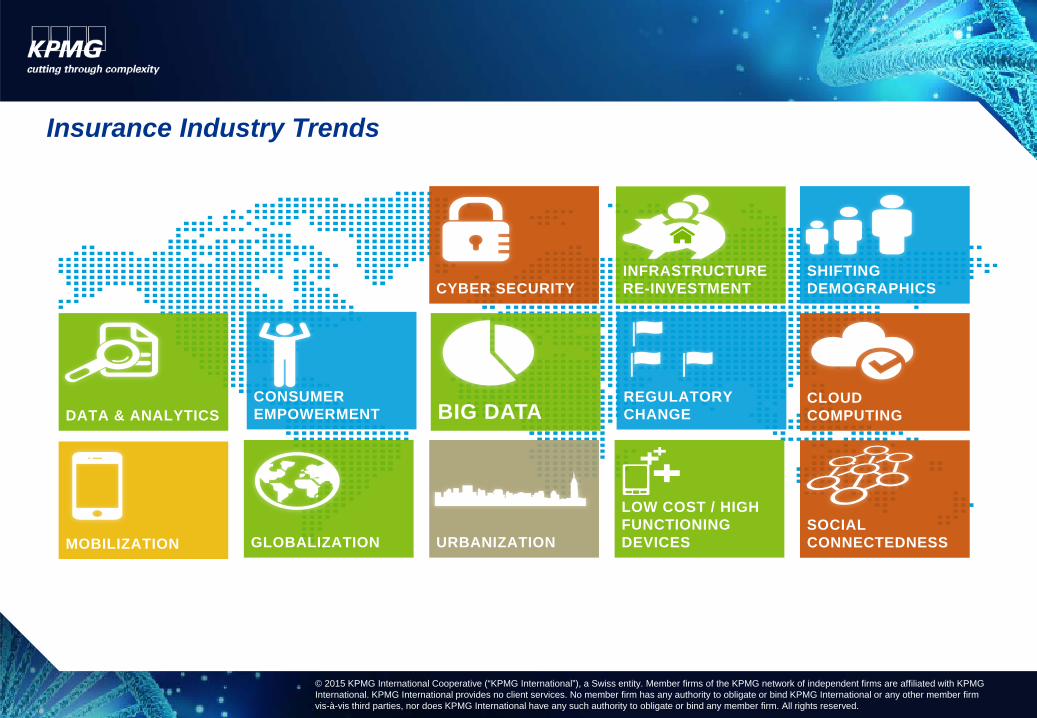

Insurance Industry Trends

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

15y e a r s

DATA & ANALYTICS

MOBILIZATIONSOCIAL CONNECTEDNESS

69% of CxOs surveyed consider D&A important to Revenue Growth

100M users on Facebook – 80% via mobile phone

59%of world population l iving in cit ies, 2030 up 8.5%

1.8 billionglobal middle class

3.2 billionby 2020

Mobile penetrationin Africa

20002%

201478%

Android’s market share in Africais 59% 59%

Mars asked 2.5m Facebook fans to pick M&M colours

Air passenger traff ic could doublein 15 years

15y e a r s

of IT budgets were spent on cloud computing in 2013

33%

73% of world exports wi l l come from emerging markets by 2030

Estimated cost of compliance globally is set to pass $1 trillion mark this year

90% of the world’s data was created in the last 2 years

Insurance Industry Trends

Spend due to breaches reached $500b in 2014

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

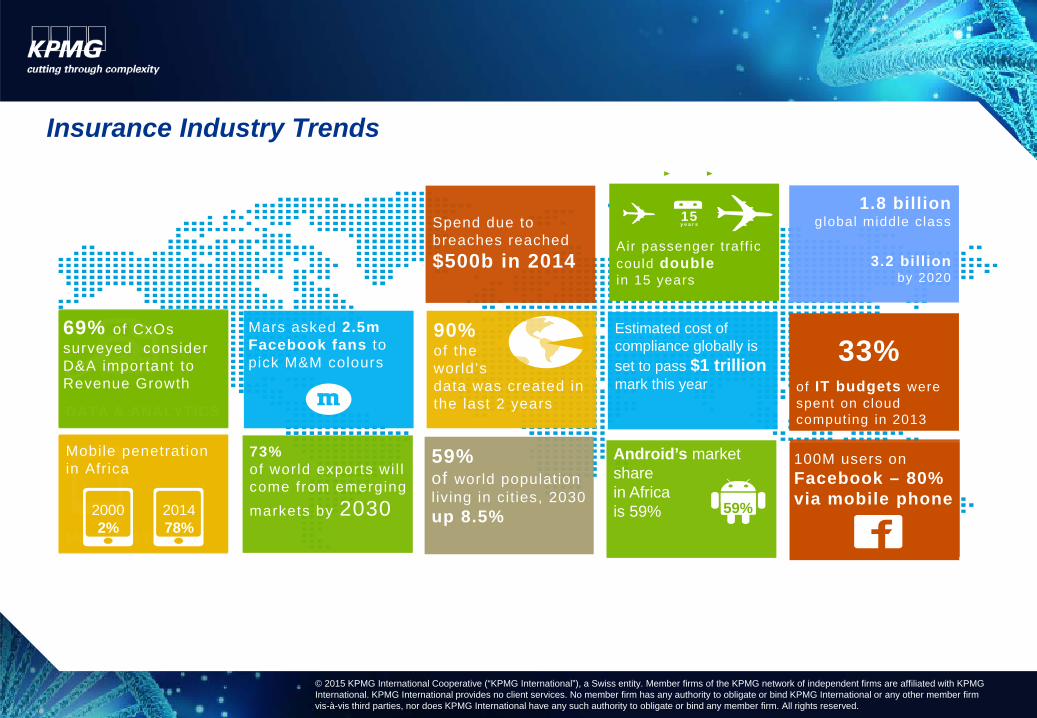

What does it mean to be digital and technology led?

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

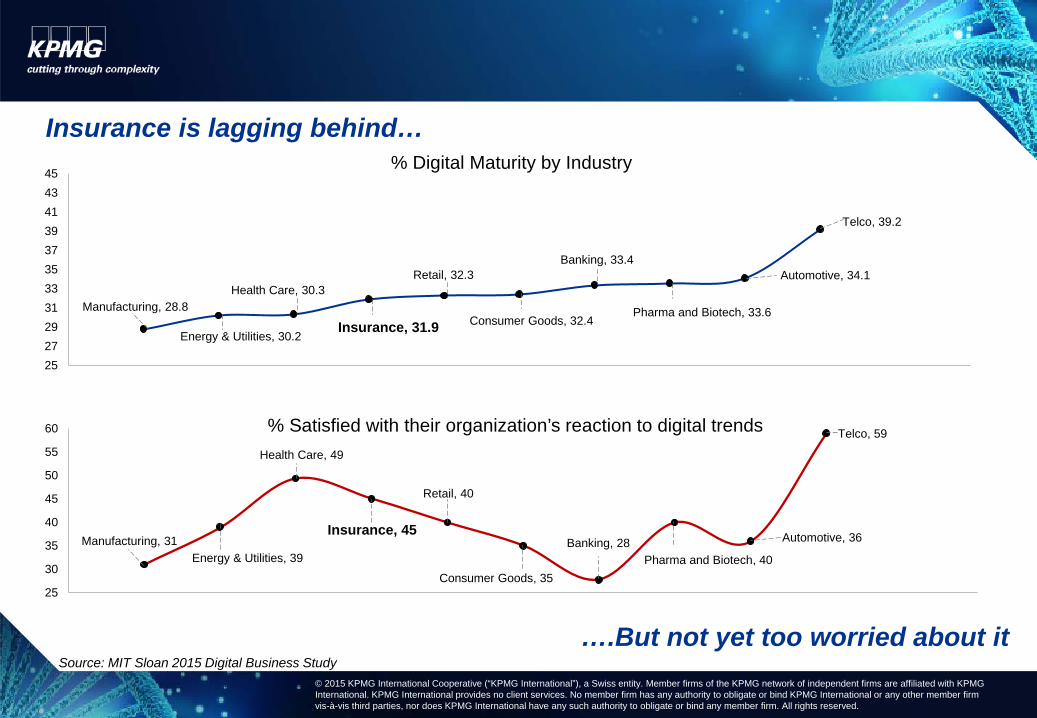

Manufacturing, 28.8

Energy & Utilities, 30.2

Health Care, 30.3

Insurance, 31.9

Retail, 32.3

Consumer Goods, 32.4

Banking, 33.4

Pharma and Biotech, 33.6

Automotive, 34.1

Telco, 39.2

2527293133353739414345

% Digital Maturity by Industry

….But not yet too worried about it

Manufacturing, 31Energy & Utilities, 39

Health Care, 49

Insurance, 45

Retail, 40

Consumer Goods, 35

Banking, 28Pharma and Biotech, 40

Automotive, 36

Telco, 59

25

30

35

40

45

50

55

60 % Satisfied with their organization’s reaction to digital trends

Source: MIT Sloan 2015 Digital Business Study

Insurance is lagging behind…

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

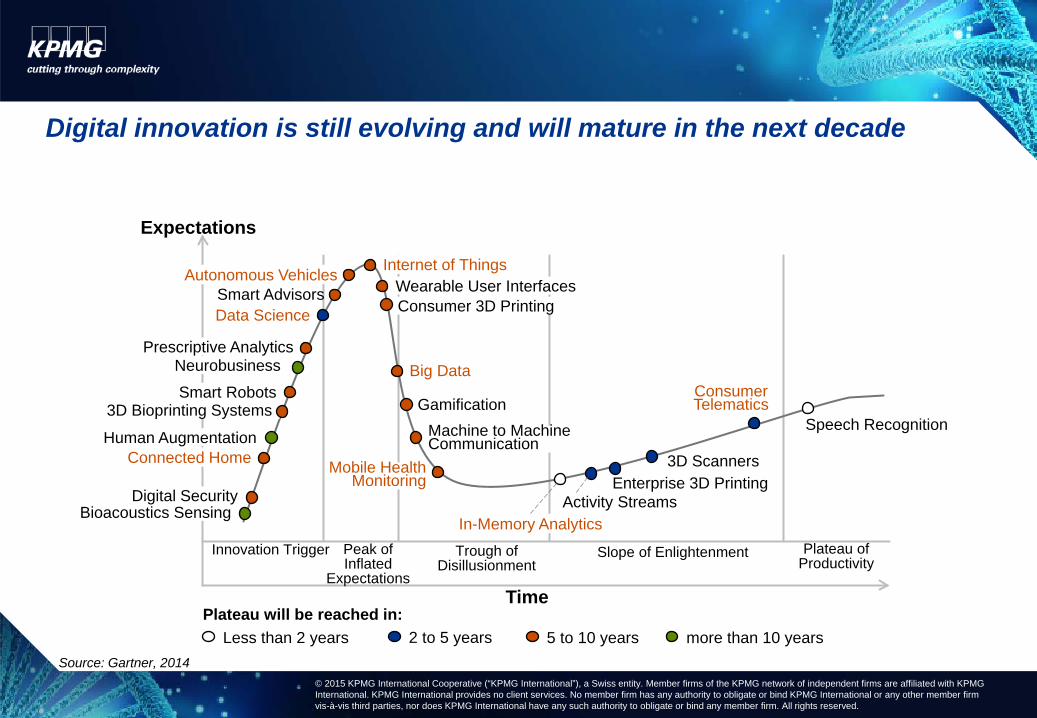

Plateau will be reached in:Less than 2 years 2 to 5 years 5 to 10 years more than 10 years

Innovation Trigger

Time

Peak of Inflated

Expectations

Trough of Disillusionment

Slope of Enlightenment Plateau of Productivity

Expectations

Enterprise 3D Printing3D Scanners

Consumer Telematics

Speech Recognition

Bioacoustics SensingDigital Security

Connected HomeHuman Augmentation

3D Bioprinting SystemsSmart Robots

NeurobusinessPrescriptive Analytics

Data ScienceSmart Advisors

Autonomous Vehicles Internet of ThingsWearable User InterfacesConsumer 3D Printing

Big Data

GamificationMachine to Machine Communication

Mobile Health Monitoring

In-Memory AnalyticsActivity Streams

Source: Gartner, 2014

Digital innovation is still evolving and will mature in the next decade

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Source: Marketer, 2014; Customer Experience Barometer, KPMG International, 2014;

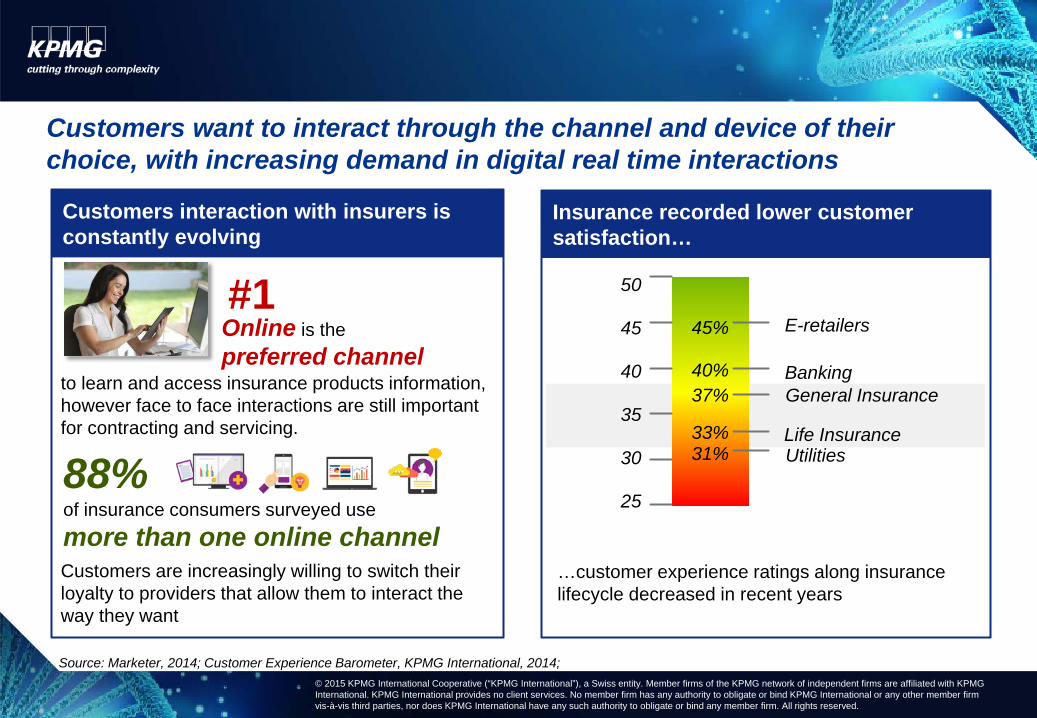

Insurance recorded lower customer satisfaction…

50

45

40

35

30

25

45%

40%37%

33%31%

E-retailers

Banking

Life InsuranceUtilities

General Insurance

…customer experience ratings along insurance lifecycle decreased in recent years

Customers interaction with insurers is constantly evolving

Online is the preferred channel

#1

Customers are increasingly willing to switch their loyalty to providers that allow them to interact the way they want

to learn and access insurance products information, however face to face interactions are still important for contracting and servicing.

88% of insurance consumers surveyed use more than one online channel

Customers want to interact through the channel and device of their choice, with increasing demand in digital real time interactions

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Digital Innovation Trends

Rich personalizationCustomers want experiences tailored to their unique needs and wants, with content that

delivers value

Behavioural securityIdentify distinguishing

behaviour to provide effortless security i.e. how hard or fast we type in order to spot and

prevent identity fraud

Minimum Viable OfferTaking a small, very simple

feature set, as an experiment that captures your customer’s value. Think Big, Start Small

– test, learn, refine.

Advisor/Agent mobilityCustomers seek increased

interactions with their advisors and want more value from

these interactions

Mobile first designMobile centric design leveraging the unique

capabilities of mobile devices location aware , cameras and

other sensors.

Voice of the CustomerConsumers are engaging with brands on their terms - taking a VOC approach gives rise to insurance innovations such as

Quick quote design etc

Source: KPMG International, 2015

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

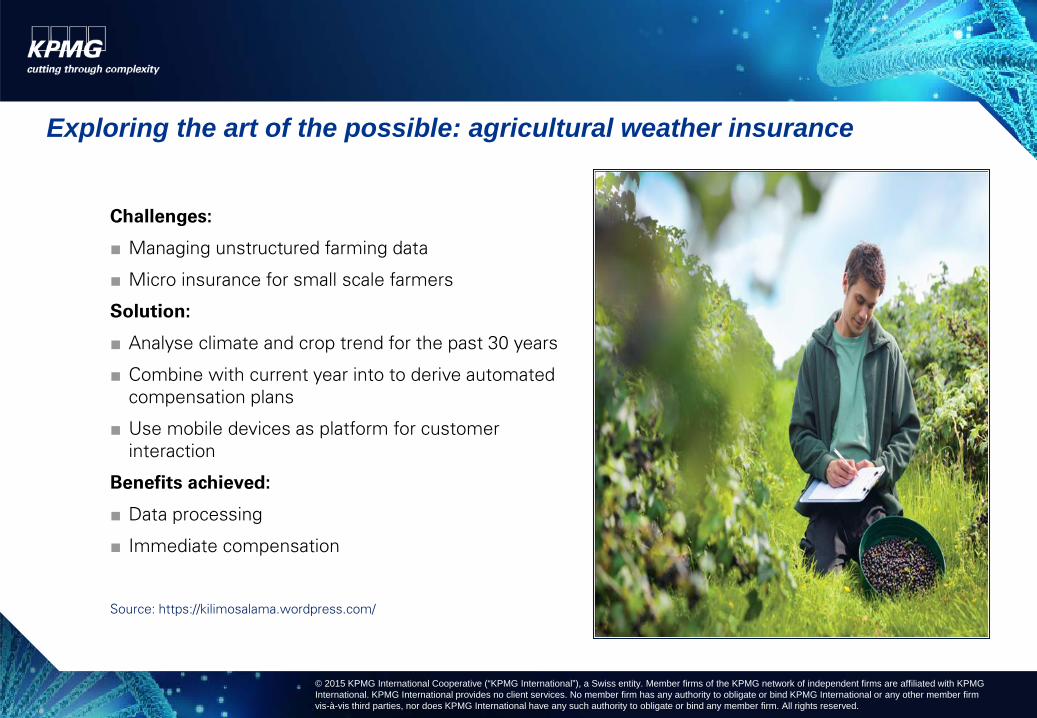

Challenges:

■ Managing unstructured farming data

■ Micro insurance for small scale farmers

Solution:

■ Analyse climate and crop trend for the past 30 years

■ Combine with current year into to derive automated compensation plans

■ Use mobile devices as platform for customer interaction

Benefits achieved:

■ Data processing

■ Immediate compensation

Source: https://kilimosalama.wordpress.com/

Exploring the art of the possible: agricultural weather insurance

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Challenges:

■ Very poor population in informal sector

Solution:

■ Health insurance on mobile platform, pay premiums via mobile payment options, access medical services using mobile device

Benefits achieved:

■ Reduced healthcare costs

■ Paperless, mobile platform ease access to medical services

Source: http://www.edgepointtz.com/bima.php

Exploring the art of the possible: micro health insurance

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Challenges:

■ Improve underwriting at lower risk

■ Develop client centric products

Solution:

■ Combine internal and external data assets

■ Create technical platform for real time underwriting

■ Predictive analytics, biometrics and client experience analytics

Benefits achieved:

■ Real time e-solution to clients, across all electronic platforms

Exploring the art of the possible: electronic underwriting

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Challenges:

■ Need for digital innovation

■ Improvement needed in customer experience

■ Develop client centric products

Solution:

■ Combine modular product technology and a digital customer experience

Benefits achieved:

■ Single lifetime policy that can be customized to offer relevant cover without the hassle of separate contracts

■ End to end customer journey on digital platform that enables customer centricity

Exploring the art of the possible: single lifetime policy

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Challenges:

■ Costly pathological tests

■ Less efficient existing processes

Solution:

■ Analysis of customers’ online activities and social media profiles to determine coverage

■ Predictive Modelling

Benefits achieved:

■ Social media analytics considered more efficient and customer-friendly

■ Cost savings

Exploring the art of the possible: social media risk assessment

© 2015 KPMG International. KPMG International is a Swiss cooperative of which all KPMG firms are members. KPMG International provides no services to clients. Each member firm is a separate and independent legal entity and each describes itself as such. All rights reserved.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

Continue the discussion:

Karin Kruger

KPMG Data & Analytics

KPMG Wanooka Place

1 Albany Road, Parktown, South Africa

Tel: +27 79 512 [email protected]