Embed Size (px)

Citation preview

The Affordable Care Act and Farm Families

Barbara O’Neill, Ph.D., CFP®

Rutgers Cooperative Extension

Two Affordable Care Act (ACA) impacts on farm families:

As consumers who making health care decisions for their families

As employers of farm workers

• Migrant workers (travel frequently between job sites)

• Seasonal farm workers (local temporary labor force)

• Year-round farm workers

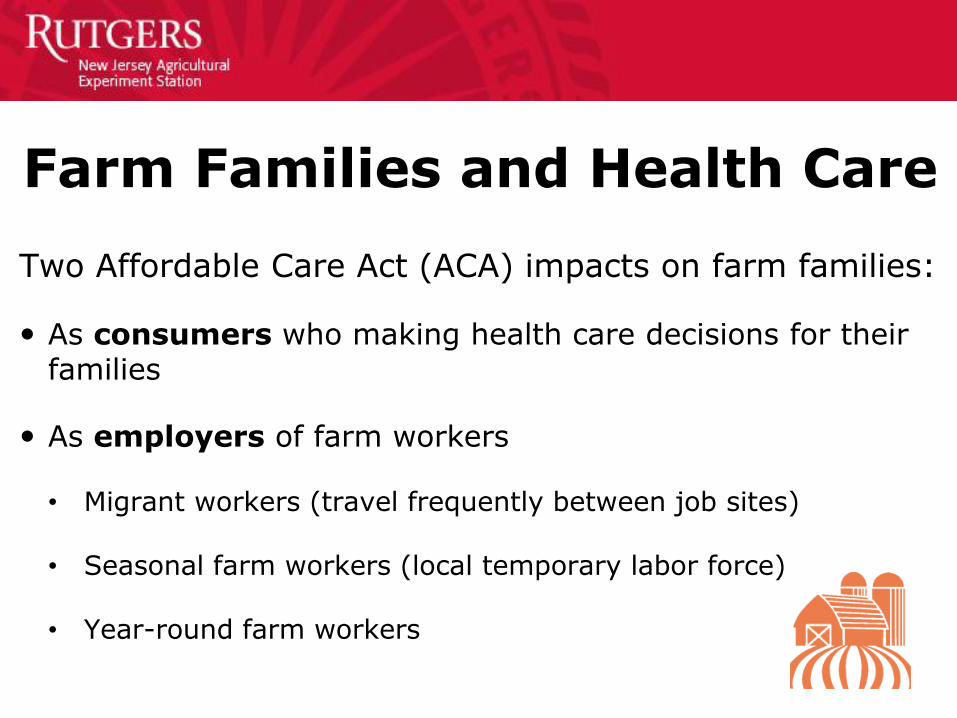

Farm Families and Health Care

• Farmers/ranchers are more likely than the U.S. population as a whole to have health insurance

• Farm work is hazardous; many occupational injuries

• Many relied on individual policies

– Few group options previously

– May have used a high-deductible policy paired with a HSA

• Marketplaces offer new insurance options with lower premiums because it is no longer legal to charge anyone (including farmers) for any pre-existing condition or risks associated with a higher risk occupation (such as farming)

Farm Families and Health Care

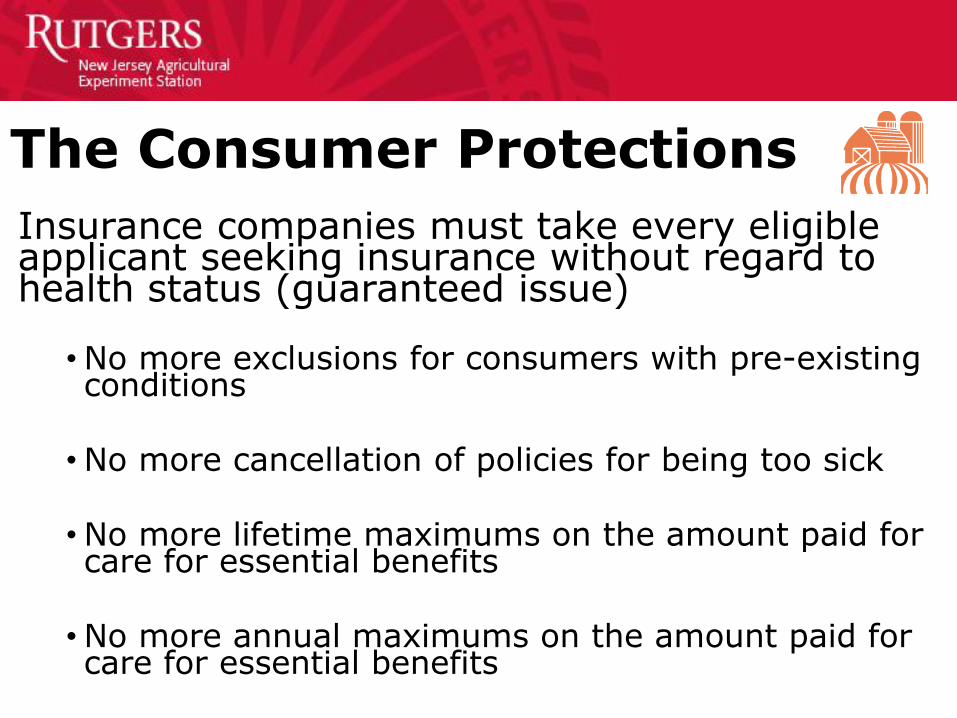

Insurance companies must take every eligible applicant seeking insurance without regard to health status (guaranteed issue)

•No more exclusions for consumers with pre-existing conditions

•No more cancellation of policies for being too sick

•No more lifetime maximums on the amount paid for care for essential benefits

•No more annual maximums on the amount paid for care for essential benefits

The Consumer Protections

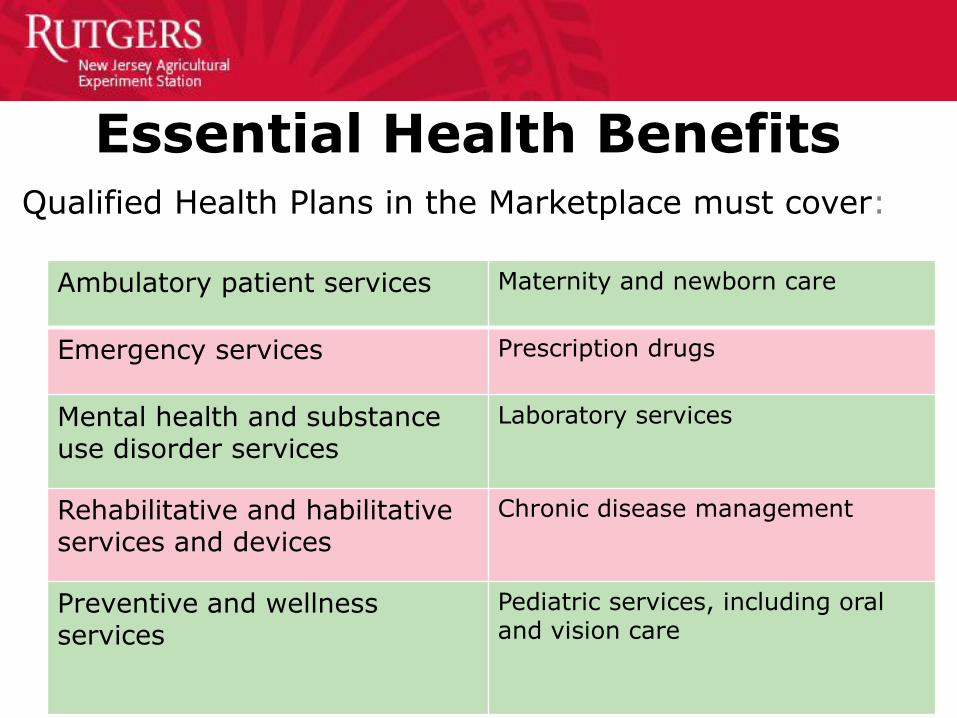

Essential Health Benefits Qualified Health Plans in the Marketplace must cover:

Ambulatory patient services Maternity and newborn care

Emergency services Prescription drugs

Mental health and substance use disorder services

Laboratory services

Rehabilitative and habilitative services and devices

Chronic disease management

Preventive and wellness services

Pediatric services, including oral and vision care

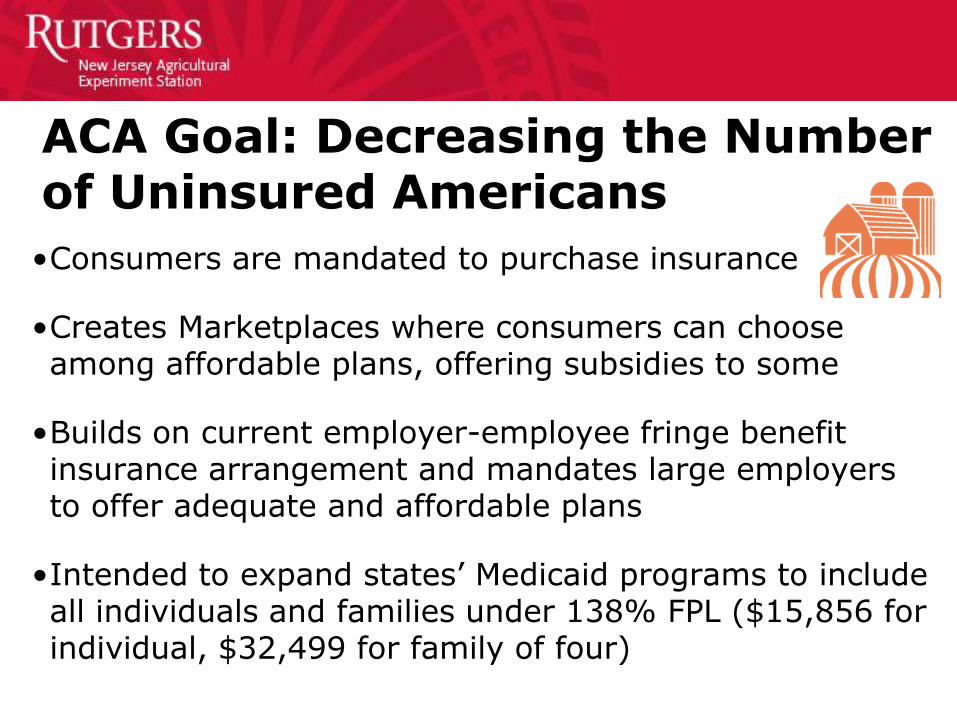

•Consumers are mandated to purchase insurance

•Creates Marketplaces where consumers can choose among affordable plans, offering subsidies to some

•Builds on current employer-employee fringe benefit insurance arrangement and mandates large employers to offer adequate and affordable plans

•Intended to expand states’ Medicaid programs to include all individuals and families under 138% FPL ($15,856 for individual, $32,499 for family of four)

ACA Goal: Decreasing the Number of Uninsured Americans

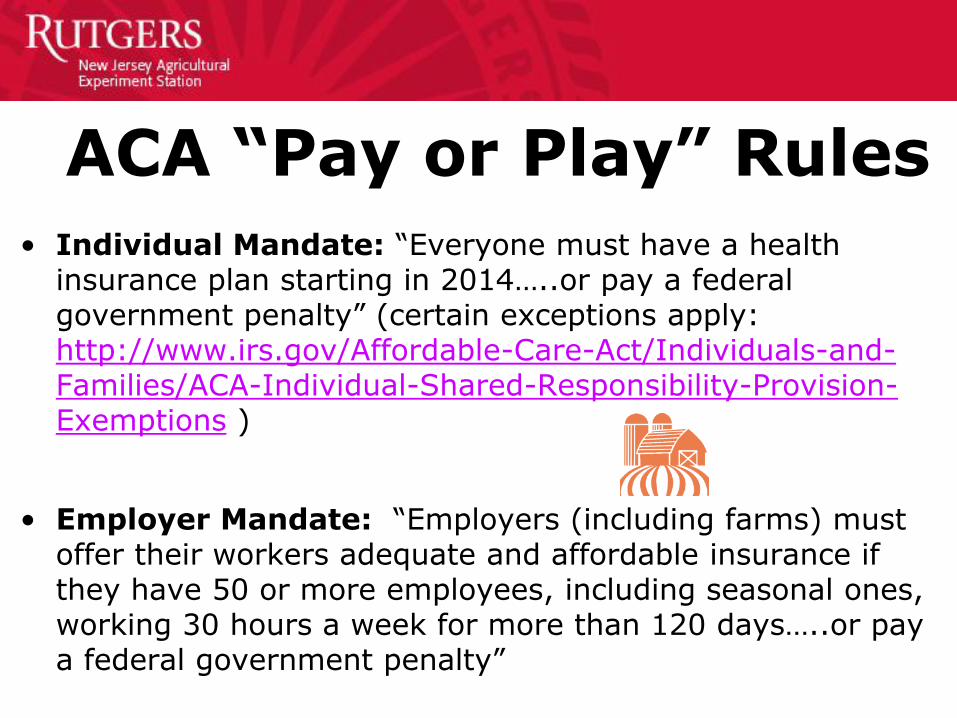

• Individual Mandate: “Everyone must have a health insurance plan starting in 2014…..or pay a federal government penalty” (certain exceptions apply: http://www.irs.gov/Affordable-Care-Act/Individuals-and-Families/ACA-Individual-Shared-Responsibility-Provision-Exemptions )

• Employer Mandate: “Employers (including farms) must offer their workers adequate and affordable insurance if they have 50 or more employees, including seasonal ones, working 30 hours a week for more than 120 days…..or pay a federal government penalty”

ACA “Pay or Play” Rules

Employed based insurance is deemed affordable if

the annual premium for a self-only plan (not a

family plan) costs less than 9.5% of a person’s

annual household gross income (safe-harbor rule:

use an employee’s W-2 Form income)

http://www.shrm.org/hrdisciplines/benefits/articles/pages/what-is-affordable-coverage.aspx

Insurance Affordability

Insurance is deemed adequate if it is a 60/40 plan.

That is, no more than 40% of the total health care

costs in a year would be expected to be paid by the

average person insured in this type of plan. Many

employer-provided plans were 50/50 or even less.

Insurance Adequacy

• Effective March 31, 2014, Americans must be enrolled in a health insurance plan

• With few exceptions, if you are not insured, and your income is over 138% of the FPL, you will be required to pay a penalty (tax) on income tax return

– Penalty for no coverage will rise from $95 for adults or 1% of family income, whichever is greater (2014), to $695 or 2.5% of family income… (2016) http://kff.org/infographic/the-requirement-to-buy-coverage-under-the-affordable-care-act/

ACA for Consumers: The Individual Mandate

• Children are also required to be insured. May be through

– Public insurance (e.g. state’s Children’s Health Insurance Program or CHIP) or

– Parents’ obligations (via employer plan or private purchase); Fines for uninsured children are half that of the adults up to a family maximum ($285 for 2014, $975 for 2015, and $2,085 for 2016)

• ACA tax is assessed on federal income tax return

– May need to adjust estimated payments and/or W-4

ACA for Consumers: Individual Mandate (Continued)

• Lowest income residents (< 138% of FPL) will be enrolled in Medicaid (legal residents only) in expansion states

• Higher income workers can get coverage through

– Medicare (age 65+)

– Large employers (farm or off-farm employer)

– State health insurance marketplaces (see www.healthcare.gov)

– Private market (e.g., insurance brokers, health co-ops)

More ACA Consumer Provisions

• Marketplaces are managed either by the state or federal

government

• People can get help applying:

o https://localhelp.healthcare.gov/

• 2015 Open enrollment period: 11/15/14- 2/15/15

• Qualifying life events are reasons for enrolling out of usual schedule (special enrollment)

https://www.healthcare.gov/marketplace-deadlines/2015/

Health Insurance Marketplace

Different Levels of Plans • 4 Levels of Coverage – Bronze, Silver, Gold, and

Platinum

• Each has a different value for level of coverage • Bronze: 60%. Silver: 70%. Gold: 80%. Platinum: 90% (adequacy

values, how much plan vs. insured pays) • Any costs not covered by the plan are paid by individuals through

deductibles, co-pays, co-insurance

• Each plan level must cover same minimum essential health benefits

• What differs is amount of cost-sharing required • Example: Bronze plan will have the least generous coverage (60%)

with more out-of-pocket costs

Health Insurance Subsidies

Two provisions to lower health insurance premiums and out-of-pocket costs for LMI households

• Premium Tax Credits- Help people pay monthly cost of having a Marketplace plan; based on family size and household income from 100% (138%) to 400% of FPL

• Cost-Sharing Reductions- Decrease the charges that people having a Marketplace plan must pay OOP for deductibles, copayments, and coinsurance; must have income up to 250% of FPL and be enrolled in a Silver plan

ACA Benefits for Farm Families as Consumers

• Some families with incomes low enough to qualify for Medicaid or tax subsidies have a high net worth (median net worth of farmers is 5x U.S. median net worth)

• The ACA does NOT have an asset test; only income and family size are considered

• Lack of an asset test is a significant advantage for farm families with low cash incomes

• Farmers often have flexibility to manage taxable income (i.e., timing receipt of income and capital expenses)

• Farmers may qualify for benefits that were previously only available to low income/low asset households

What Does the ACA Mean for Farm

Owners as Employers?

• Sole proprietors are considered “individuals” and are subject to ACA individual mandate

• Can shop for coverage for farmer/family in state Marketplace or privately

• Will probably have substantial cost savings in Marketplace vs. policies offered in private health insurance market

– Especially with available government subsidies

Sole Proprietorships

• American Farm Bureau: “The vast majority [of farm owners] likely won’t have to offer insurance”

• Department of Health and Human Services: “96% of all businesses will be exempt from the law”

• Only 0.2% of U.S. businesses with 50+ employees did not already provide health insurance to FT employees

http://www.forbes.com/sites/theyec/2013/04/22/is-the-affordable-care-act-really-

bad-for-business/

http://farmdocdaily.illinois.edu/2014/09/small-farms-and-the-aca.html

http://www.rwjf.org/content/dam/farm/reports/issue_briefs/2014/rwjf413248

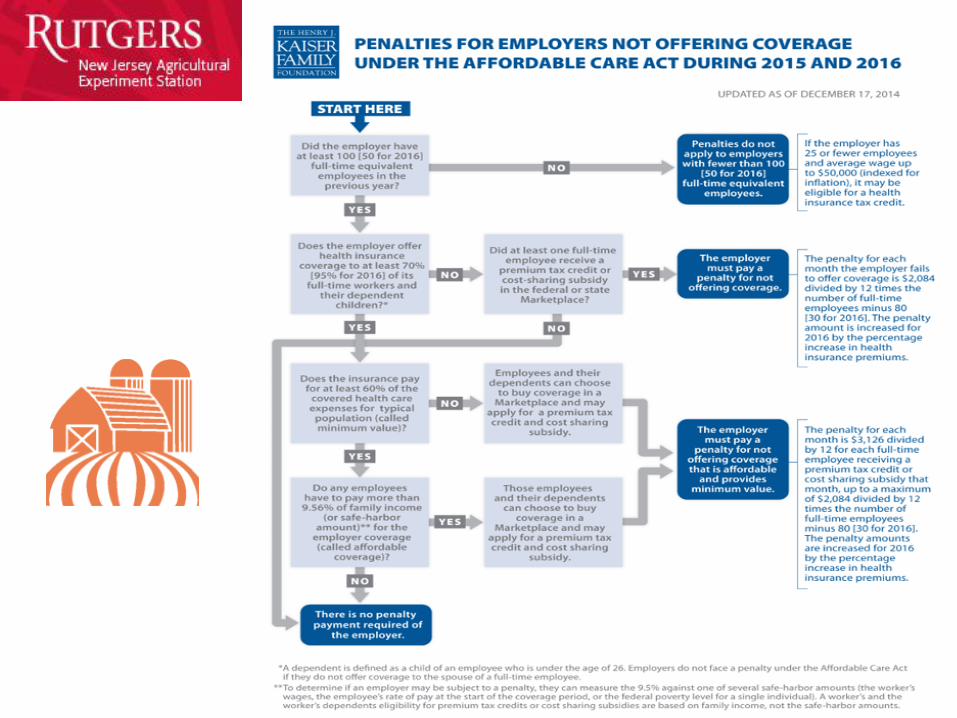

ACA Employer Mandate

Small employers (< 50 FTE) are not mandated to offer health insurance to full-time employees

But their workers may be mandated to purchase coverage and may likely do so with subsidies in the Marketplace

If employers offer insurance, must be offered equally to everyone

SHOP (Small Business Health Option Program) Exchange available for small employers

For 2015, SHOP Marketplace is open to employers with 50 or fewer full-time equivalent employees (FTEs). By 2016, those with 100 or fewer FTEs can use the SHOP

90 day waiting periods are allowable for new employees

ACA Employer Provisions

Small Business Health Care Tax Credits

All of the following must apply:

• Fewer than 25 full-time equivalent (FTE) employees

• Average employee salary is 50,000 per year or less (inflation indexed)

• Employer pays at least 50% of full-time employees' premium costs

• Employer offers coverage to full-time employees through SHOP

Marketplace: https://www.healthcare.gov/small-businesses/provide-shop-coverage/small-business-tax-credits/

Tax credit is worth up to 50% of contribution toward employees'

premium costs (up to 35% for tax-exempt employers).

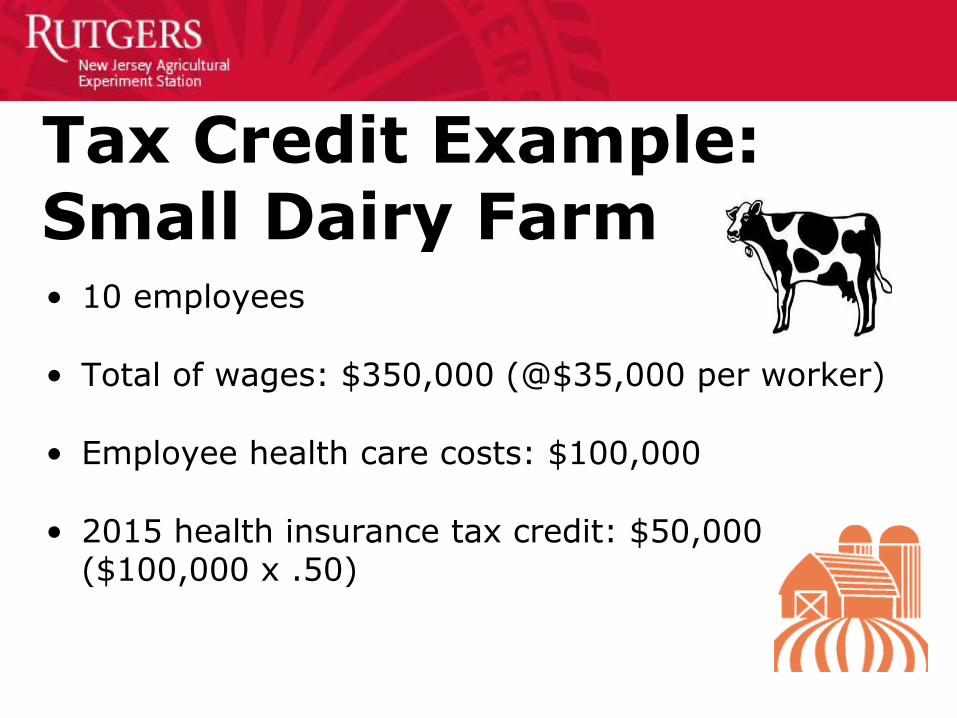

• 10 employees

• Total of wages: $350,000 (@$35,000 per worker)

• Employee health care costs: $100,000

• 2015 health insurance tax credit: $50,000 ($100,000 x .50)

Tax Credit Example: Small Dairy Farm

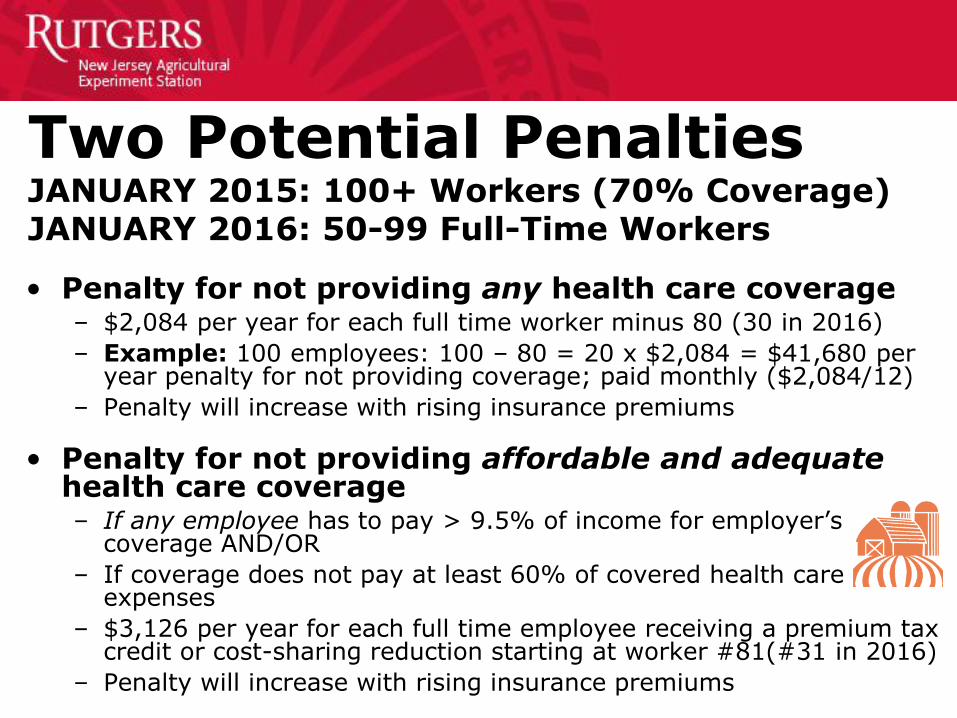

• Penalty for not providing any health care coverage – $2,084 per year for each full time worker minus 80 (30 in 2016)

– Example: 100 employees: 100 – 80 = 20 x $2,084 = $41,680 per year penalty for not providing coverage; paid monthly ($2,084/12)

– Penalty will increase with rising insurance premiums

• Penalty for not providing affordable and adequate health care coverage – If any employee has to pay > 9.5% of income for employer’s

coverage AND/OR

– If coverage does not pay at least 60% of covered health care expenses

– $3,126 per year for each full time employee receiving a premium tax credit or cost-sharing reduction starting at worker #81(#31 in 2016)

– Penalty will increase with rising insurance premiums

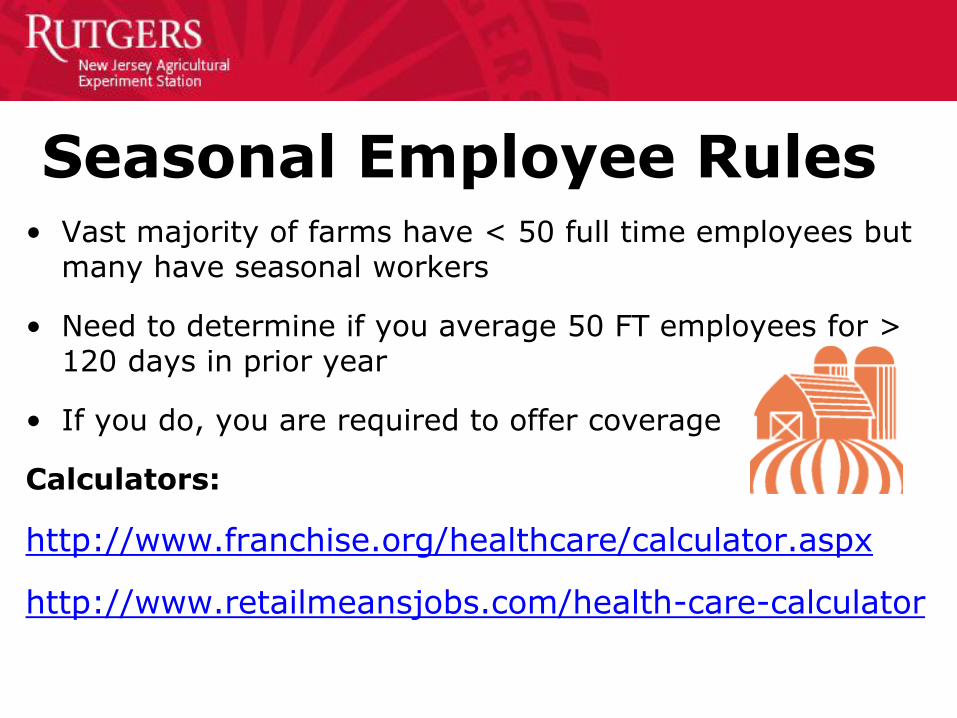

Two Potential Penalties JANUARY 2015: 100+ Workers (70% Coverage) JANUARY 2016: 50-99 Full-Time Workers

• Vast majority of farms have < 50 full time employees but many have seasonal workers

• Need to determine if you average 50 FT employees for > 120 days in prior year

• If you do, you are required to offer coverage

Calculators:

http://www.franchise.org/healthcare/calculator.aspx

http://www.retailmeansjobs.com/health-care-calculator

Seasonal Employee Rules

• Not offer insurance at all and pay a smaller fine

• Make sure insurance that is offered is both adequate and affordable to comply with ACA

Large Employer Options That Make “Business Sense”

But, Keep in Mind…

• More than three-quarters (78%) of 2.1 million U.S. farms do NOT hire labor (Ahearn et al., 2014)

• Rather, labor is provided solely by family members

• For these farmers, obviously, the ACA employer mandate does not apply

• The only way family farms are affected by the ACA is by the individual mandate to have health insurance

http://www.ers.usda.gov/amber-waves/2014-march/family-farming-in-the-united-states.aspx#.VM_qs02_yM8

• Undocumented immigrants aren’t eligible for ACA coverage through marketplaces

• Most seasonal farm workers and their families are uninsured

• Barriers: cost, language, transportation, no sick leave

• Farmworkers may have better access at least to safety net providers (e.g., community health centers that are being better funded through ACA)

Resource: National Center for Farmworker Health: http://www.ncfh.org/

Farm Workers and Health Care

• Compare health insurance options including ACA

• Monitor income/expenses to qualify for subsidies

• Consult a professional advisor if business is close to or above 50 FTE employees

– Do the math: pay or play?

– Develop a plan to optimize mandate requirements within your business model (e.g., more part-time, less full-time, limiting surges of workers to < 120 days)

• Obtain adequate and affordable health insurance if you decide to cover employees. Make sure it both:

– Meets the 60/40 rule

– Costs less than 9.5% of your least (lowest) paid employee’s annual (household) income.

Action Steps for Farm Families

Research-Based Journal Article

http://aepp.oxfordjournals.org/content/early/2014/09/30/aepp.ppu030.short

Ahearn, et al. (September 2014). Implications of Health Care Reform for Farm Businesses and Families. Applied Economic Perspectives and Policy, 1-27.

Abstract: The Affordable Care Act has implications for the source of health insurance for farm households and potentially how much of their time they allocate to off-farm jobs and even the rate at which new operators enter farming. The Act will likely have impacts for the 1% of farms defined to be large employers, which are required to provide coverage for their workers or pay a penalty. While a very small share of all farms, they account for upward of 40% of the production for some commodities. How they adjust their use of farm labor in response to the Affordable Care Act has implications for farm structure.