Embed Size (px)

Citation preview

AlMoatassem MostafaLecture Eight: Sunday, 27 November 2016

Taxation & Tax Legislation

Essay Two: Tax Policy &

Tax Legislation

Definition of Tax Policy &

Tax Legislation

Principles of Tax Policy

Tax Compliance

•Tax Compliance• Basis for compliance

• The carrot and stick approach• The responsible citizen approach

• Tax evasion, tax avoidance, and tax planning

Lecture Outline

Tax Compliance• Tax compliance is the degree to which taxpayers comply

with tax rules fully, on time, and as required. Tax compliance, therefore, includes full declaration of income, filing tax returns in the required formats, and paying taxes on time.

Tax Compliance• The importance of tax compliance emerges from the fact

that taxation is regarded as a major source of public revenues.

• Noncompliance results in the insufficiency of revenues resulting from taxation as planned by the government.

• It also results in negative impacts on equity since one of the main objectives of taxation is the redistribution of income and wealth.

• Noncompliance to a tax implies a shift of resources from those who comply to those who do not

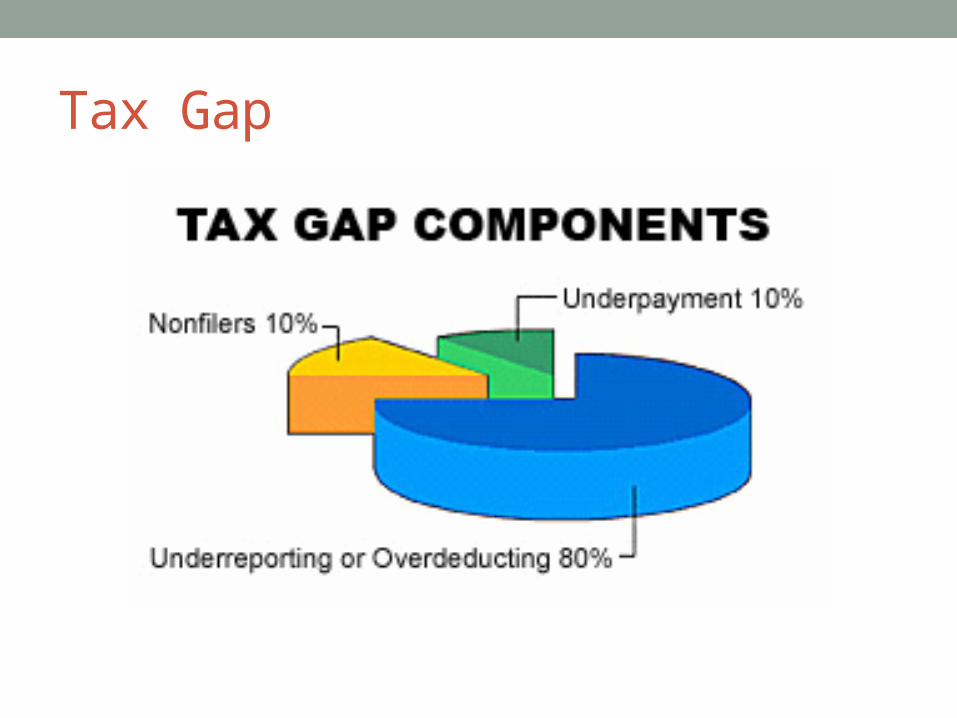

Tax Gap• The degree of noncompliance to a tax could be evaluated

according to what is called tax gap; that is the difference between the achieved revenue and revenue that would be received in case of full compliance with a tax.

• The time of compliance is also essential. Although late payment of tax might address the issue of tax gap, it cannot be regarded as full compliance because one of the major considerations of compliance is the payment of taxes whenever they are due and without any delays.

Tax Gap

Tax Compliance• It must be noted that successful tax legislation involves

voluntary compliance by taxpayers without any notifications, reminders, or threat of legal penalties on the side of tax administration.

• However, this does not contradict with the fact that committed taxpayers might not fully understand their obligations or unable to meet them for some reasons.

• This explains the importance of allocating additional expenditures for activities that contribute to improving voluntary compliance.

Basis for Compliance• Some economists have searched for a basis for tax

compliance by taxpayers. • In this regard, two main approaches were introduced to

analyse tax compliance. • The first approach attributes compliance or

noncompliance to the probability of detection and penalties in case of noncompliance (the carrot and stick approach).

• The second one links compliance to a tax to activities that improve voluntary compliance (the responsible citizen approach)

The Carrot and Stick Approach • The carrot and stick approach represents a combination

of rewards and punishments in order to influence the behaviour of taxpayers. In this sense, tax authorities develop policies to encourage taxpayers to comply fully with a tax in addition to punishments to discourage them from tax evasion.

The Carrot and Stick Approach • This approach is based mainly on economic rationality.

Rational choice theory is suggests that individuals always make logical decisions that provide them with the greatest benefit or satisfaction based on the available choices.

• Consequently, some taxpayers evade taxes because this results in maximizing their income and wealth. Certain factors affect the noncompliance of taxpayers; these factors include tax rate, the probability of detection, and the penalties enforced in case on noncompliance.

The Carrot and Stick Approach • Although this approach conforms to the principle of

economic rationality, it fails to completely explain the basis for compliance and noncompliance.

• From a practical perspective, this approach does not explain why some taxpayers continue to comply with taxes despite the reduction of enforcement activities, including tax auditing.

• One possible explanation is information reporting required from taxpayers. Information reporting documents have greatly facilitated the task of tax authorities in matching them with tax returns. It, additionally, reduces tax evasion and unintentional reporting errors because it specifies what exactly should be reported to tax authorities.

The Responsible Citizen Approach• This approach suggests that the behaviour of taxpayers in

complying with taxes is influenced by a number of factors.• These factors include social support, social influence,

attitudes, and certain background characteristics, such as age, gender, and culture.

• Based on this approach, taxpayers do not always seek maximizing their income and wealth by evading taxes. Different considerations, including equity, beliefs, and norms influence their behaviour towards tax authorities.

The Responsible Citizen Approach• This behavioural approach suggests that some taxpayers might pay more than

their legal obligation because they consider tax as their contribution towards the society and that their contributions could promote a better health or educational systems. Consequently, not all taxpayers seek tax evasion by every possible way.

• A successful tax policy should, therefore, consider a combination of factors to achieve high rates of compliance rather than merely specifying rewards and punishments. Motivation, encouragement, and support provided for taxpayers should be a priority. The success of a taxation system achieves the interests of different stakeholders in the society, including tax authorities, governments, and the individuals themselves. This success is achieved by compliance that considers the behaviour of taxpayers rather than rewards and punishments.

• The importance of behavioural contribution in promoting compliance to taxation is already evident in a number of taxation systems worldwide. Taxation systems in Australia, Canada, Sweden, the UK, and the USA, have adopted the behavioural approach as a guide to their compliance rules. Tax authorities in these countries are in continuous contact with taxpayers in order to promote awareness and compliance.

Tax Evasion, Tax Avoidance, and Tax Planning

• some taxpayers use various strategies in an attempt to reduce their obligations.

• In this regard, a distinction must be made between three terms that are used interchangeably to describe the reduction of tax liability; these terms include tax evasion, tax avoidance, and tax planning.

• Although the main objective of these strategies is the same, which is the reduction of tax liability, the mechanism and legitimacy of each of them is different.

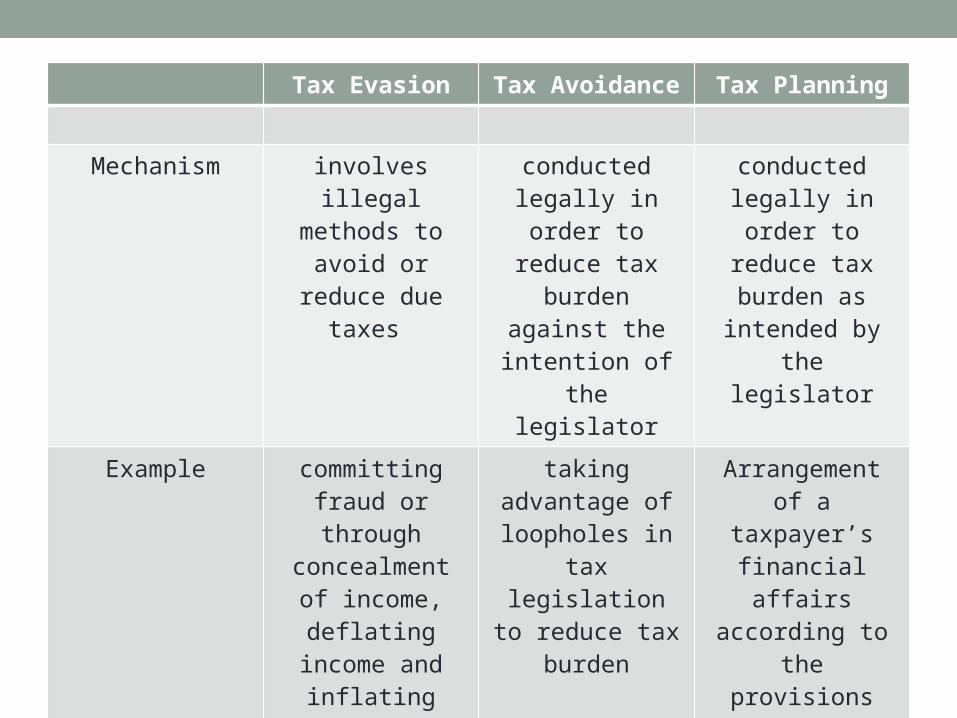

Tax Evasion• Tax evasion is an unlawful practice where a taxpayer

deliberately avoids paying his real tax liability. • Tax evasion applies to both the illegal non-payment of

taxes as well as the illegal reduction of tax burden. • Illegal non-payment of taxes might take place by

committing fraud or through concealment of income, while illegal reduction of tax burden might take place by deflating income and inflating expenses.

• Income deflation and expenses inflation would result in a reduction in the taxable income, and therefore the tax burden. Tax evasion is generally subject to criminal penalties.

Tax Evasion• For a person to be charged of tax evasion, tax authorities

must ensure that such evasion was intentional as a result of fraud and/or concealment of income.

• For instance, taxpayers could attempt to conceal assets by associating them with a person other than themselves. Income concealment might also include failure to report work that did not follow traditional payment recording methods, such as accepting a cash payment for goods or services without reporting them properly in tax returns.

Tax Avoidance• In contrast, tax avoidance is the alteration of a taxpayer’s

financial affairs using legal methods in order to reduce the tax burden.

• The essence of tax avoidance is, therefore, using the loopholes in tax legislation, such as making advantage of deductions, allowances, or exemptions, in order to reduce the due tax.

• Although tax avoidance is a legal practice, it is not always favoured by tax authorities because it involves some kind of manipulation of a taxpayer’s financial affairs, which contradicts with the intentions of the legislator.

Tax Avoidance• In other cases, nevertheless, tax avoidance is intended by

legislators for the benefit of the taxpayers. In the United States, for instance, lawmakers have used the Internal Revenue Code to manipulate the taxpayers’ affairs to make them eligible for tax credit, deductions, and exemptions in various aspects of people’s lives including health care, saving and investing, education, energy use and other activities.

• The tax benefits in qualified pension plans are granted to encourage self-sufficiency in pensions. The death benefits of a life insurance policy are exempted from taxes to achieve family protection. Capital gains are subject to taxes at a low rate to stimulate investment.

Tax Avoidance

Tax Planning• Finally, tax planning refers to the arrangement of a

taxpayer’s financial affairs according to the provisions and rules of tax legislation to reduce tax burden or to increase after-tax returns.

• Here the taxpayer is making advantage of the intended effects of tax rules and within the limits of law to obtain deductions, exemptions, or after-tax returns.

• Tax planning is, consequently, a legal practice; taxpayers are encouraged to conduct tax planning to pay their respective due taxes.

Tax Evasion Tax Avoidance Tax Planning

Mechanism involves illegal methods to avoid

or reduce due taxes

conducted legally in order to reduce

tax burden against the

intention of the legislator

conducted legally in order to reduce

tax burden as intended by the

legislator

Example committing fraud or through

concealment of income, deflating

income and inflating expenses

taking advantage of loopholes in tax

legislation to reduce tax burden

Arrangement of a taxpayer’s

financial affairs according to the provisions and

rules of tax legislation to

reduce tax burden or to increase

after-tax returns.Legitimacy Illegal and subject

to criminal penalties

legal legal

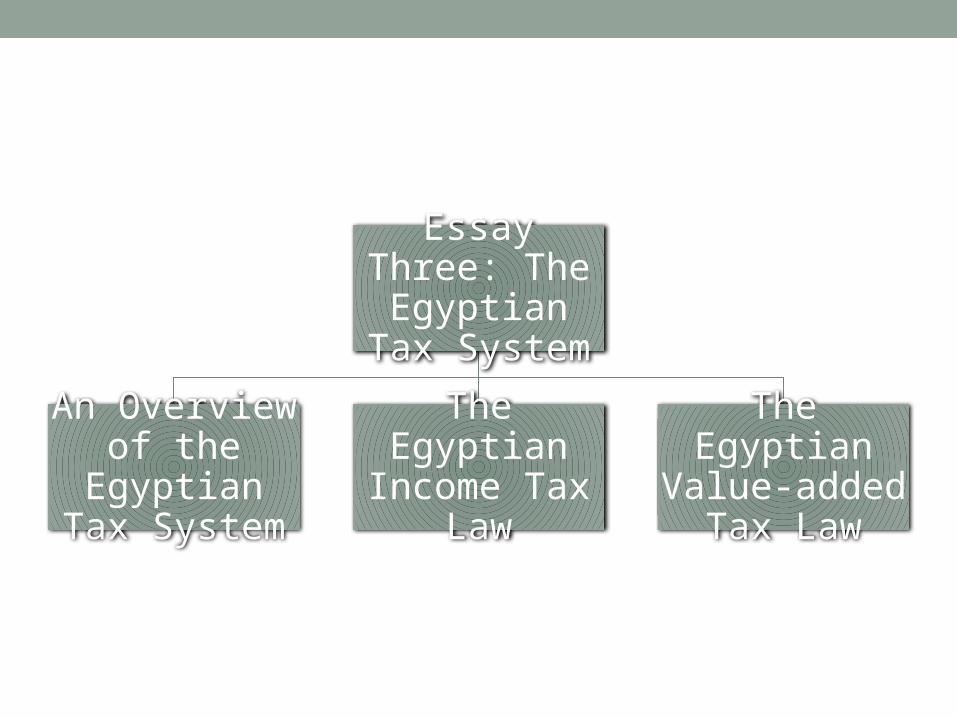

Essay Three: The Egyptian Tax System

An Overview of the

Egyptian Tax System

The Egyptian Income Tax

Law

The Egyptian Value-added

Tax Law

An Overview of the Egyptian Tax System

• The Egyptian tax system encompasses different types of direct and indirect taxes, including income tax and value-added tax.

• The Egyptian tax system has been subject to an ongoing reform process in order to reduce the negative impacts of increased tax rates and inefficient tax administration.

• These tax reforms have aimed to boost public revenues, promote investment, especially FDI, and address tax compliance issues, including tax evasion.

An Overview of the Egyptian Tax System

• The Evolution of the Egyptian Tax System• Structure of the Egyptian Tax System• Tax Reforms, Incentives, and Complaince

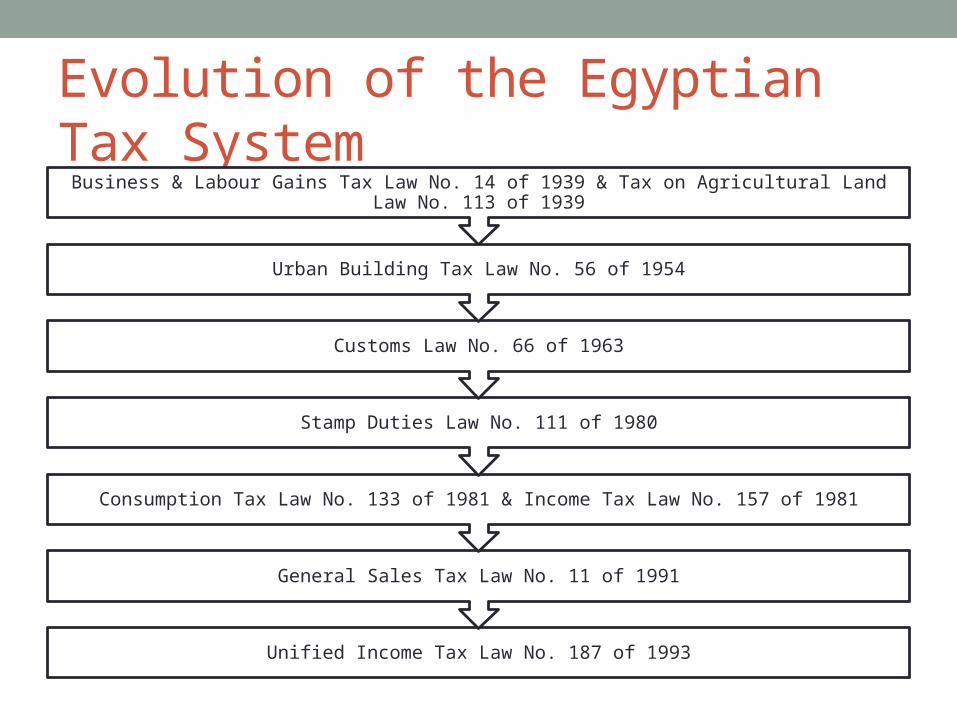

Evolution of the Egyptian Tax System

Unified Income Tax Law No. 187 of 1993

General Sales Tax Law No. 11 of 1991

Consumption Tax Law No. 133 of 1981 & Income Tax Law No. 157 of 1981

Stamp Duties Law No. 111 of 1980

Customs Law No. 66 of 1963

Urban Building Tax Law No. 56 of 1954

Business & Labour Gains Tax Law No. 14 of 1939 & Tax on Agricultural Land Law No. 113 of 1939

Evolution of the Egyptian Tax System• The current income tax law is Law No. 91 of 2005, which

was later amended by Law No. 96 of 2015.• Regarding indirect taxes, the Value-added tax Law No. 67

of 2016 abolished the General Sales Tax Law No. 11 of 1991. Consequently, starting from 2016, Egypt has replaced sales tax with a VAT tax.

• The current customs law is Law No. 95 of 2005 that amended the previous customs law (Law No 66 of 1963).

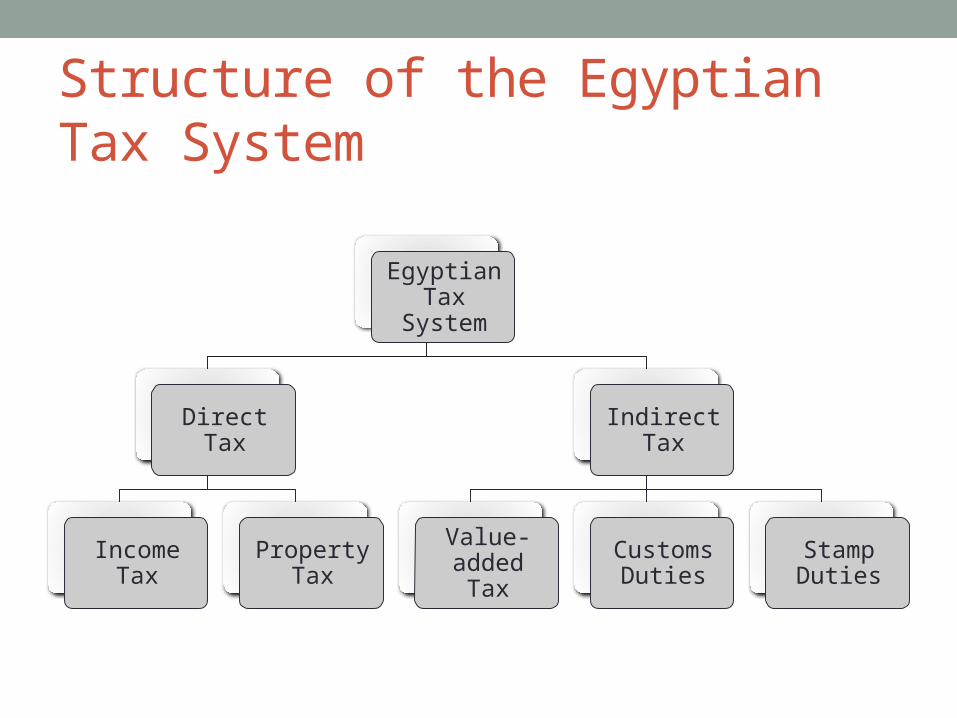

Structure of the Egyptian Tax System

Egyptian Tax

System

Direct Tax

Income Tax

Property Tax

Indirect Tax

Value-added Tax

Customs Duties

Stamp Duties

Structure of the Egyptian Tax System• The Egyptian Ministry of Finance plans, prepares and

manages public budget and public debt. • This is carried out by preparing legislations, planning

revenues and expenditures, managing and supervising the government spending, and preparing a framework for economic policy and development.

• The ministry analyses and design tax policies, customs duties and tariff policies, and other types of public income. It additionally analyses and manages public expenditures. Finally, it develops policies on domestic and international finance

Structure of the Egyptian Tax System• The main objectives of the ministry include:

• Promoting a fair and efficient tax and benefit system with incentives to work, save and invest.

• The Ministry of Finance is, therefore, responsible for the regulation and enforcement of the various tax legislations via its tax departments.

• In addition, these tax departments take part in the amendment, designation, and drafting of tax legislations. These departments are as follows: • General Tax Authority which is in charge of the income tax law, stamp duties

law;• Customs Authority which is responsible for customs duties;• General Sales Tax Authority which is in charge of the general sales tax law; and• Real Estate Tax Authority, which is in charge of the agricultural land tax law and

building tax law.

Structure of the Egyptian Tax System• In 2006, the Presidential Decree No. 154 of 2006 resulted

in merging of the General Tax Authority and the General Sales Tax Authority into one department, which is the Egyptian Tax Authority (ETA).

• ETA is currently responsible for the collection of income tax, VAT tax, and stamps duties.

• Customs Authority is responsible for the collection of customs.

• Finally, the Real Estate Tax Authority is in charge of the collection of real estate tax.

Tax Reforms, Incentives, and Compliance• Several tax reforms took place in Egypt in order to, boost

revenues, enhance investment, and reduce tax evasion. • The reforms have taken the form of continuous amendments of

existing tax legislations and enacting new ones. • Income Tax Law has been subject to continuous amendments

since its introduction in 1939. • For instance, the government adopted major tax reforms by

introducing a new income tax law (Law No. 91 of 2005). The main aim of the new law was to address inefficiencies related to tax rates and tax administration. The new law resulted in reductions in tax rates by 50% and switched to a self-assessment tax regime.

• In 2015, the Income Tax Law No. 91 of 2005 was partially amended by a Presidential Decree that promulgated Law No. 96 of 2015

Tax Reforms, Incentives, and Compliance• The same applies for the General Sales Tax Law that was subject to

successive amendments until it was eventually abolished by enactment of the new Egyptian Value-added Tax Law No. 67 of 2016.

• The Egyptian tax system offers two categories of tax incentives for investment.

• The first category is offered according to Income Tax Law and could be benefited by all businesses in Egypt.

• The second one is offered only to businesses operating under Investment Law. Under Income Tax Law, businesses could benefit from tax holidays and tax incentives in order to reduce their tax burden.

• In addition, Investment Law No. 8 of 1997 included various tax incentives, customs exemptions, and many investor guarantees. Such incentives might also take the form of free economic zones where businesses operating in these zones are exempted from corporate tax.

Tax Reforms, Incentives, and Compliance

• In 2014, The General Anti-Avoidance Rules (GAAR) were introduced in the Egyptian tax system.

• The primary objective of the GAAR is to deter taxpayers from entering into arrangements for the purpose of obtaining an “abusive” tax advantage.

• The GAAR gives the tax authority the right to challenge any cases where it suspects that the main objective of the transaction is to defer, reduce or avoid paying tax and would accordingly have the right to reassess the due taxes that were relevant to the transaction.