Embed Size (px)

Citation preview

Social Protest, Housing, Regulation, and more…

Dr. Michael Sarel, Head of Kohelet Economics Forum

December 2014

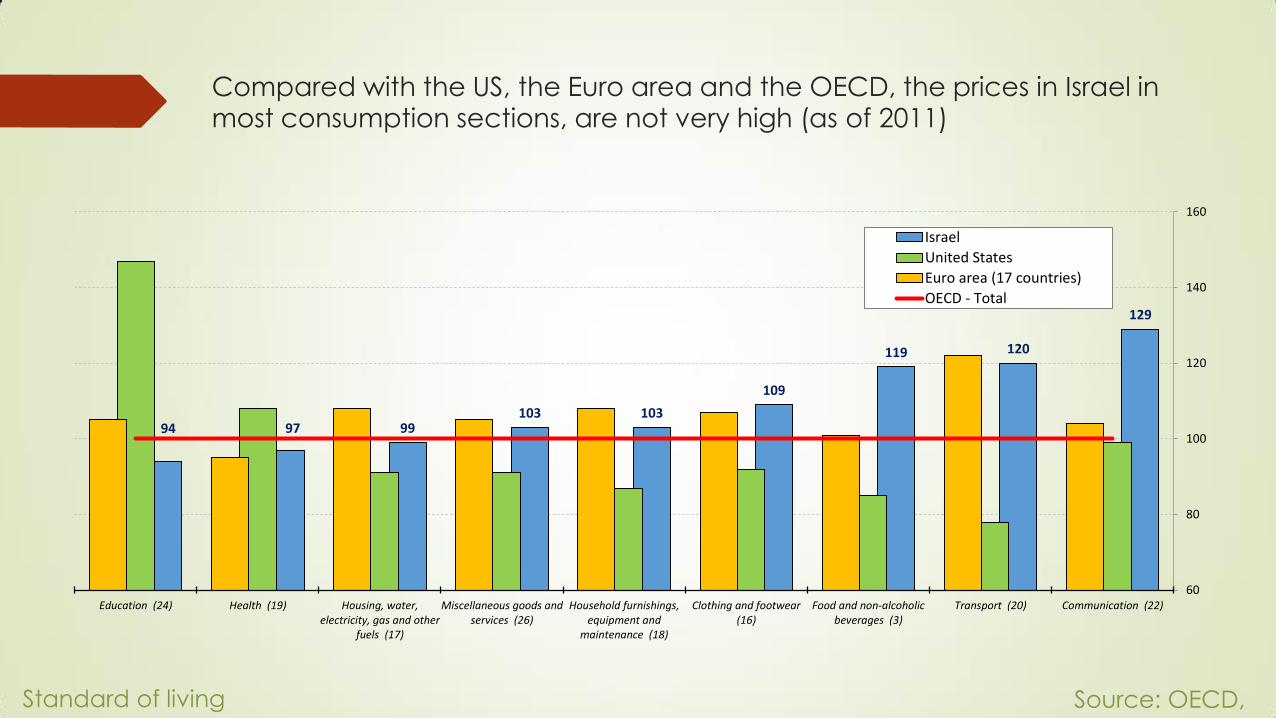

Compared with the US, the Euro area and the OECD, the prices in Israel in most consumption sections, are not very high (as of 2011)

129

120 119

109

103 103 99 97 94

60

80

100

120

140

160

Communication (22)Transport (20)Food and non-alcoholicbeverages (3)

Clothing and footwear(16)

Household furnishings,equipment and

maintenance (18)

Miscellaneous goods andservices (26)

Housing, water,electricity, gas and other

fuels (17)

Health (19)Education (24)

Israel

United States

Euro area (17 countries)

OECD - Total

Source: OECD, 2011

Standard of living

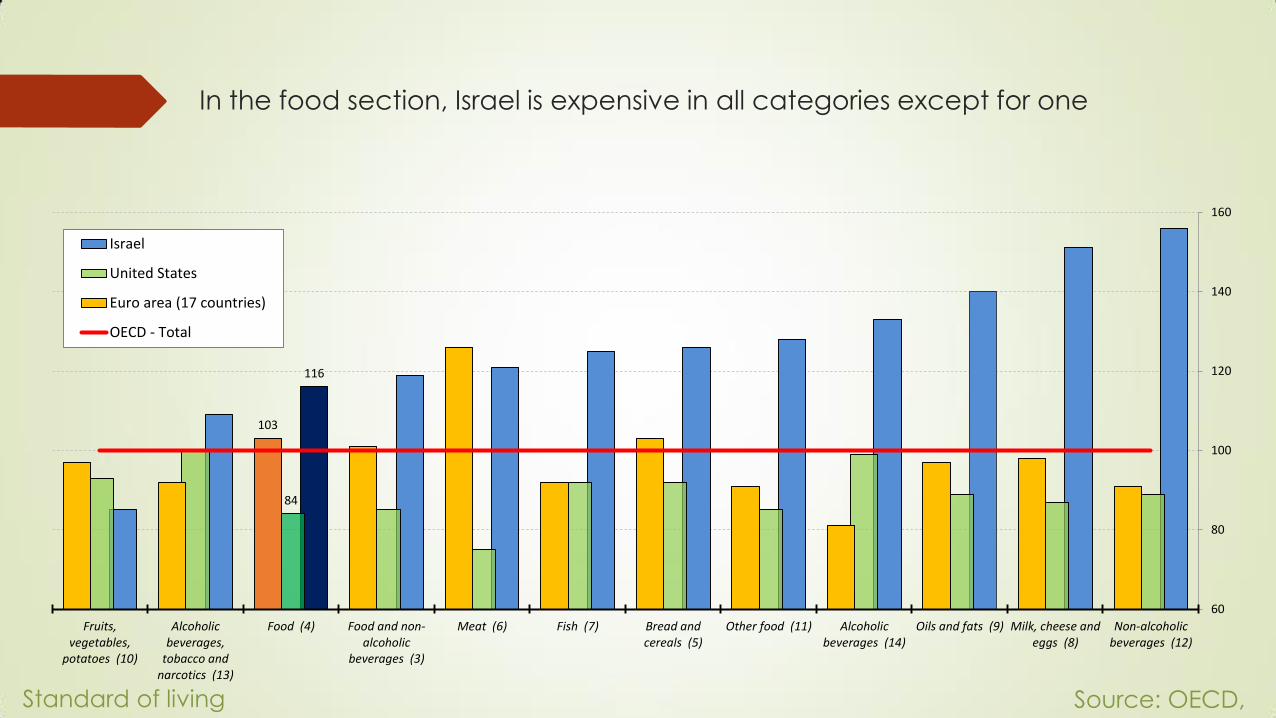

In the food section, Israel is expensive in all categories except for one

116

84

103

60

80

100

120

140

160

Non-alcoholicbeverages (12)

Milk, cheese andeggs (8)

Oils and fats (9)Alcoholicbeverages (14)

Other food (11)Bread andcereals (5)

Fish (7)Meat (6)Food and non-alcoholic

beverages (3)

Food (4)Alcoholicbeverages,

tobacco andnarcotics (13)

Fruits,vegetables,

potatoes (10)

Israel

United States

Euro area (17 countries)

OECD - Total

Source: OECD, 2011

Standard of living

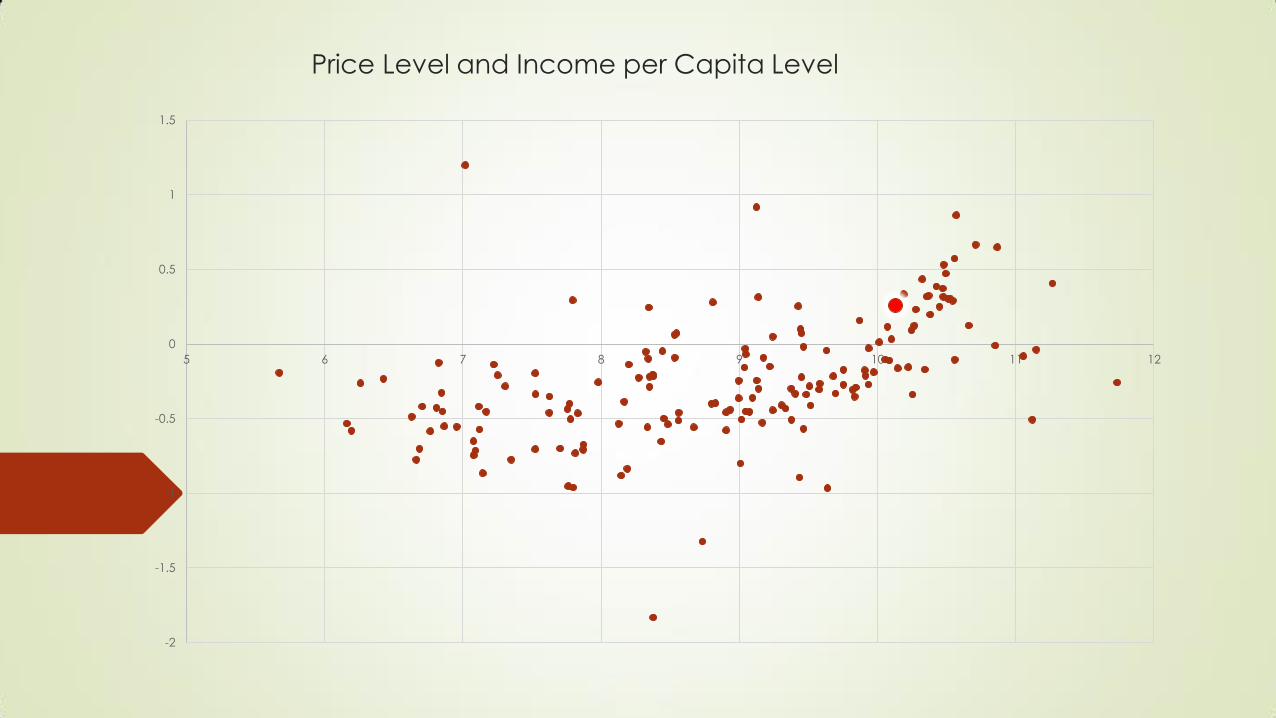

Price Level and Income per Capita Level

-2

-1.5

-1

-0.5

0

0.5

1

1.5

5 6 7 8 9 10 11 12

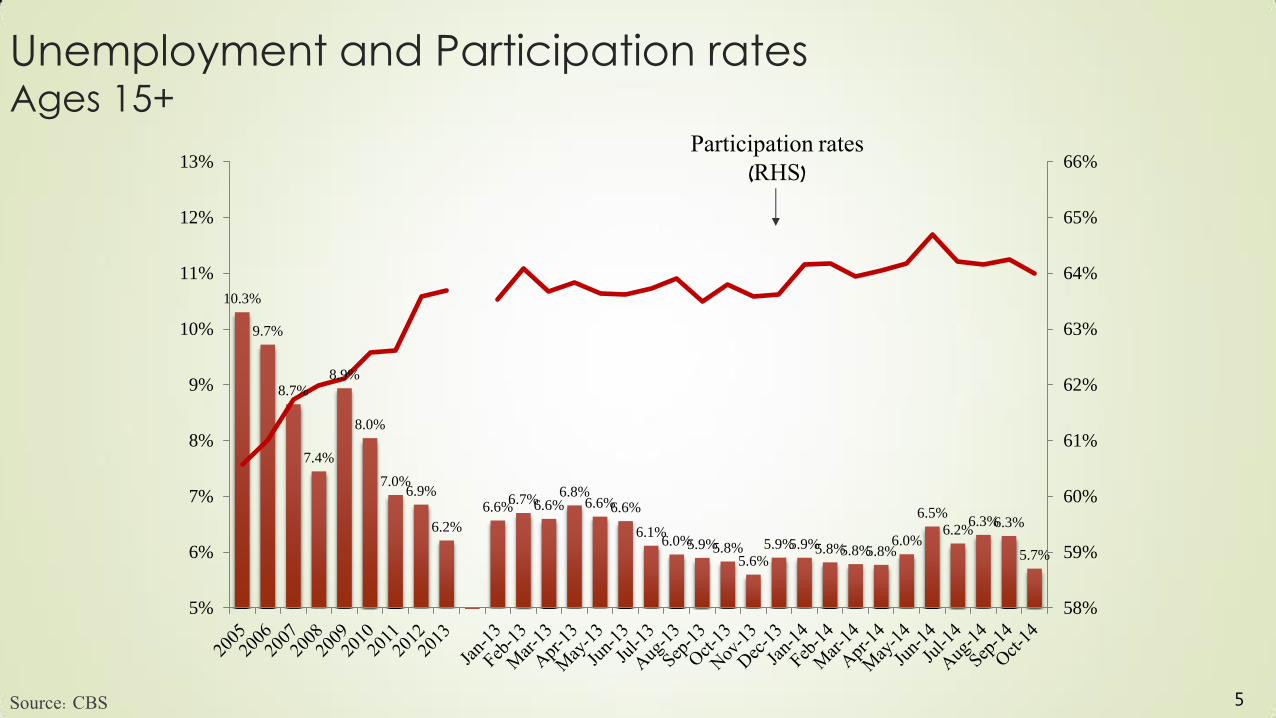

10.3%

9.7%

8.7%

7.4%

8.9%

8.0%

7.0% 6.9%

6.2%

6.6% 6.7% 6.6%

6.8% 6.6% 6.6%

6.1% 6.0% 5.9% 5.8%

5.6%

5.9% 5.9% 5.8% 5.8% 5.8% 6.0%

6.5%

6.2% 6.3% 6.3%

5.7%

58%

59%

60%

61%

62%

63%

64%

65%

66%

5%

6%

7%

8%

9%

10%

11%

12%

13%

5

Unemployment and Participation rates Ages 15+

Source: CBS

Participation rates (RHS)

6

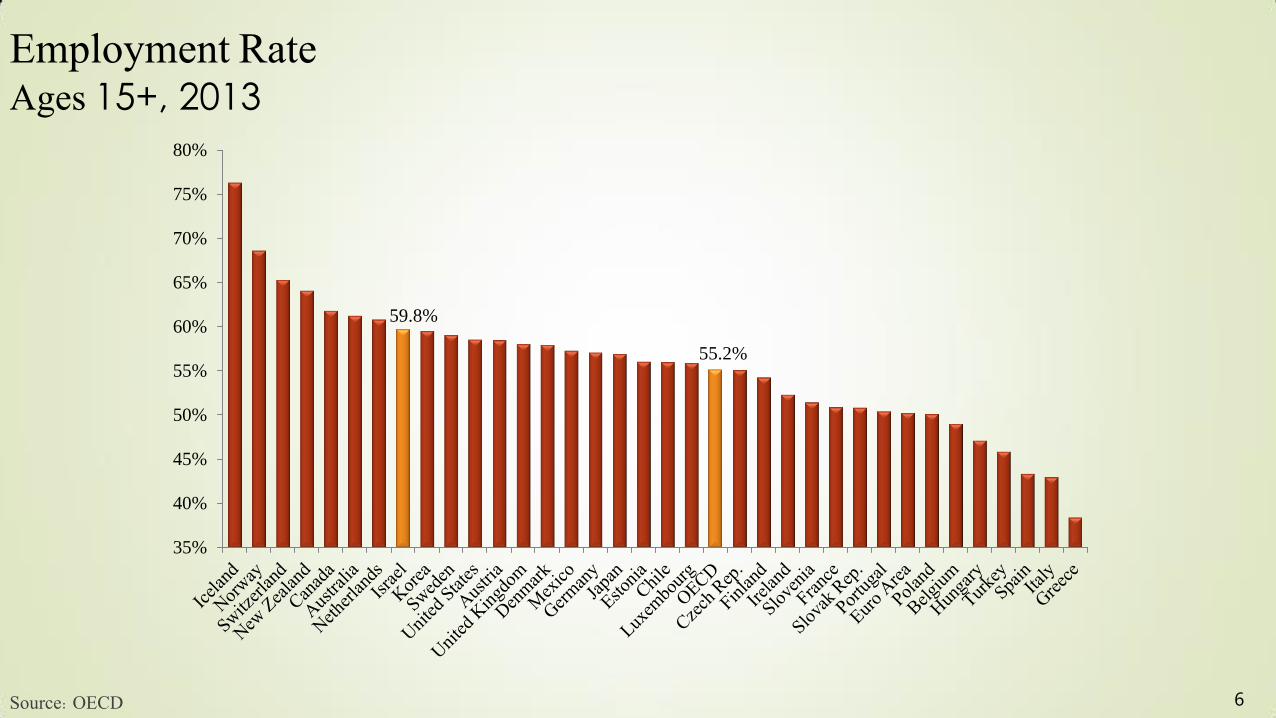

Employment Rate Ages 15+, 2013

Source: OECD

59.8%

55.2%

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

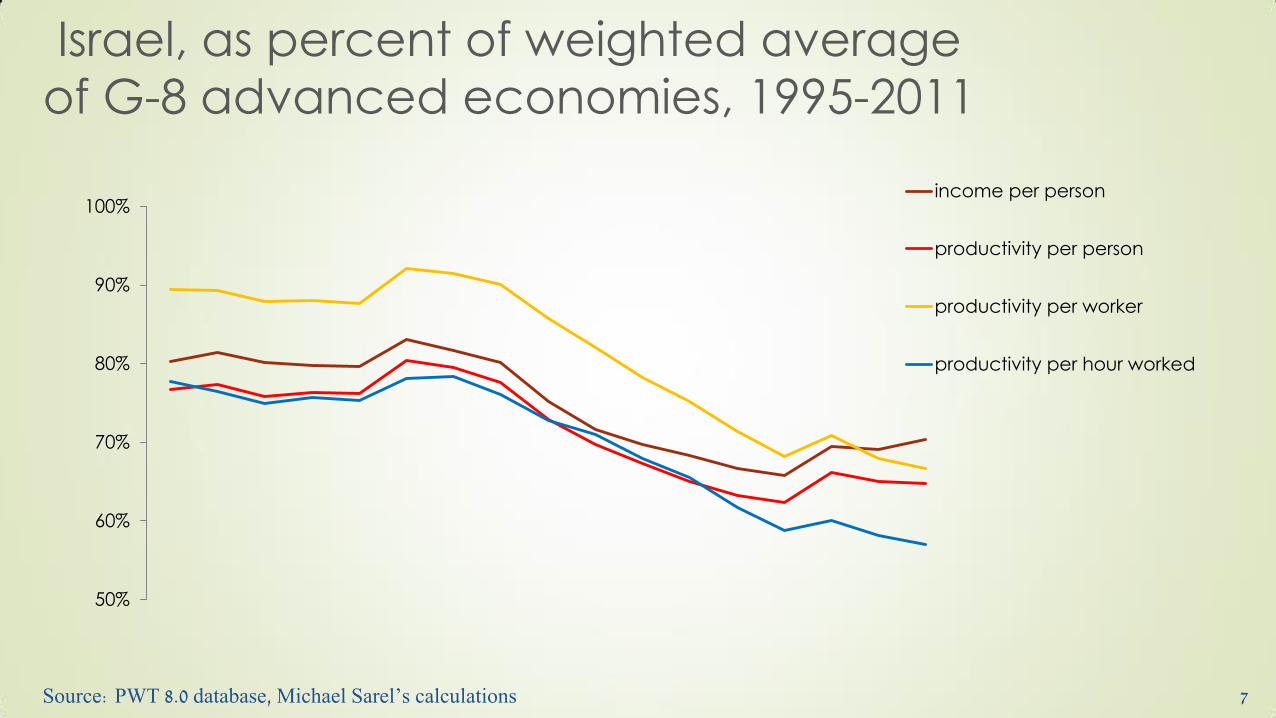

Israel, as percent of weighted average

of G-8 advanced economies, 1995-2011

50%

60%

70%

80%

90%

100%income per person

productivity per person

productivity per worker

productivity per hour worked

Source: PWT 8.0 database, Michael Sarel’s calculations 7

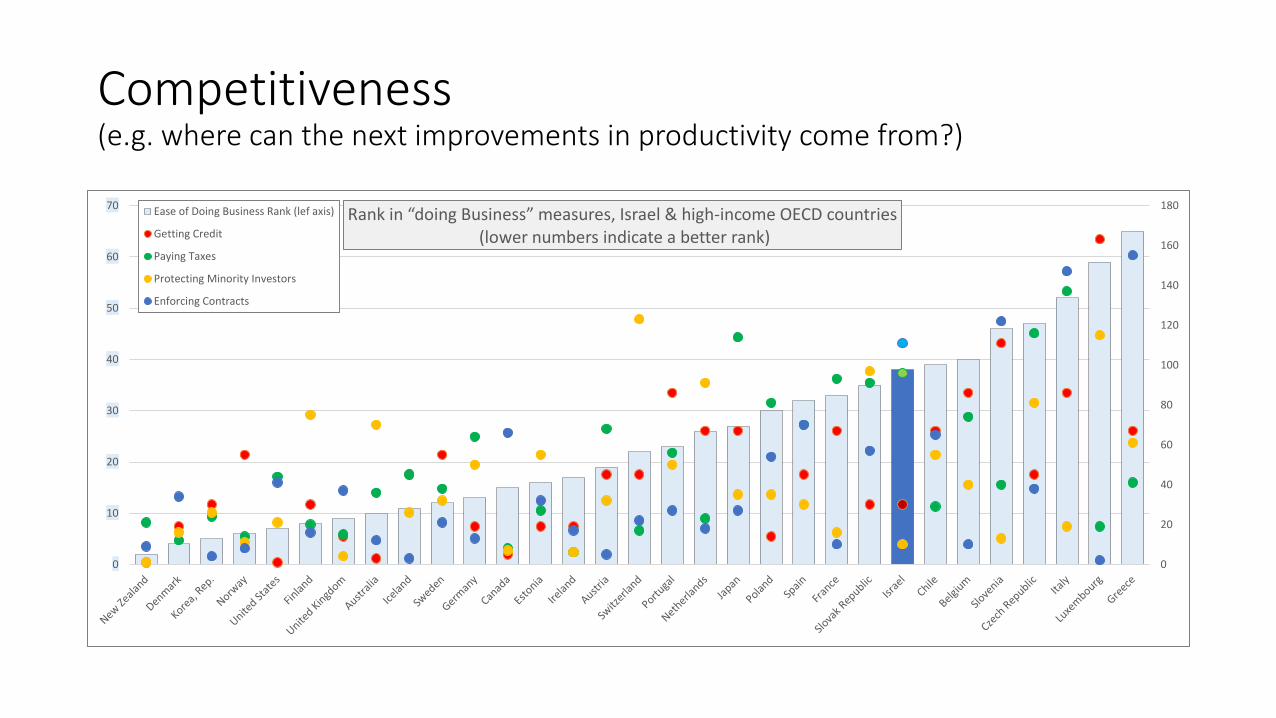

Competitiveness (e.g. where can the next improvements in productivity come from?)

0

20

40

60

80

100

120

140

160

180

0

10

20

30

40

50

60

70Rank in “doing Business” measures, Israel & high-income OECD countries

(lower numbers indicate a better rank)

Ease of Doing Business Rank (lef axis)

Getting Credit

Paying Taxes

Protecting Minority Investors

Enforcing Contracts

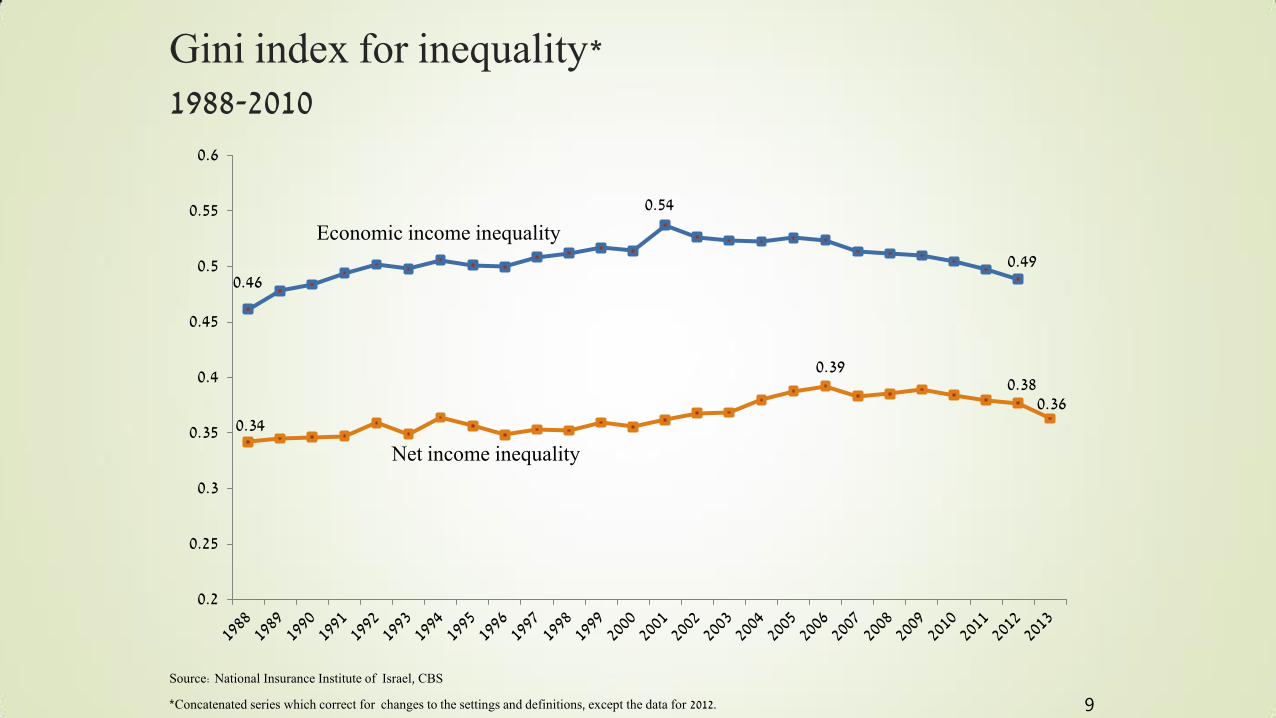

0.46

0.54

0.49

0.34

0.39 0.38

0.36

0.2

0.25

0.3

0.35

0.4

0.45

0.5

0.55

0.6

9

Gini index for inequality* 1988-2010

Source: National Insurance Institute of Israel, CBS

*Concatenated series which correct for changes to the settings and definitions, except the data for 2012.

Economic income inequality

Net income inequality

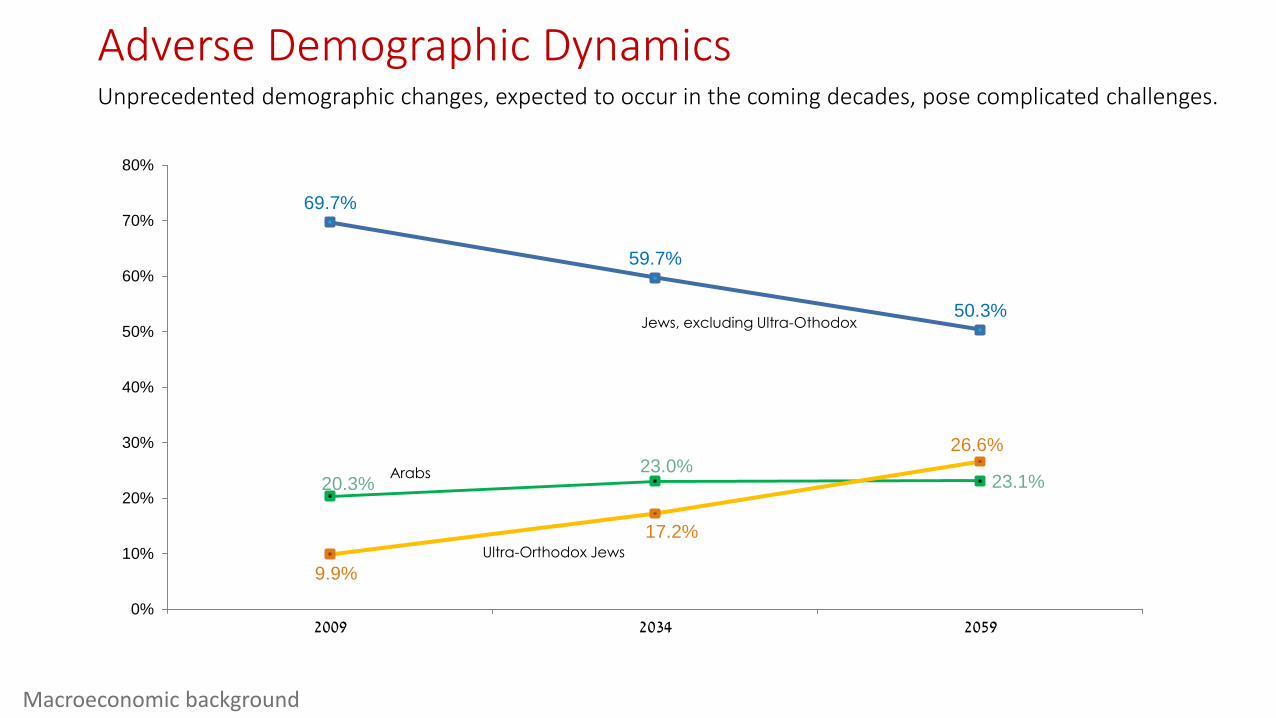

69.7%

59.7%

50.3%

20.3% 23.0%

23.1%

9.9%

17.2%

26.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2009 2034 2059

Ultra-Orthodox Jews

Arabs

Jews, excluding Ultra-Othodox

Macroeconomic background

Adverse Demographic Dynamics Unprecedented demographic changes, expected to occur in the coming decades, pose complicated challenges.

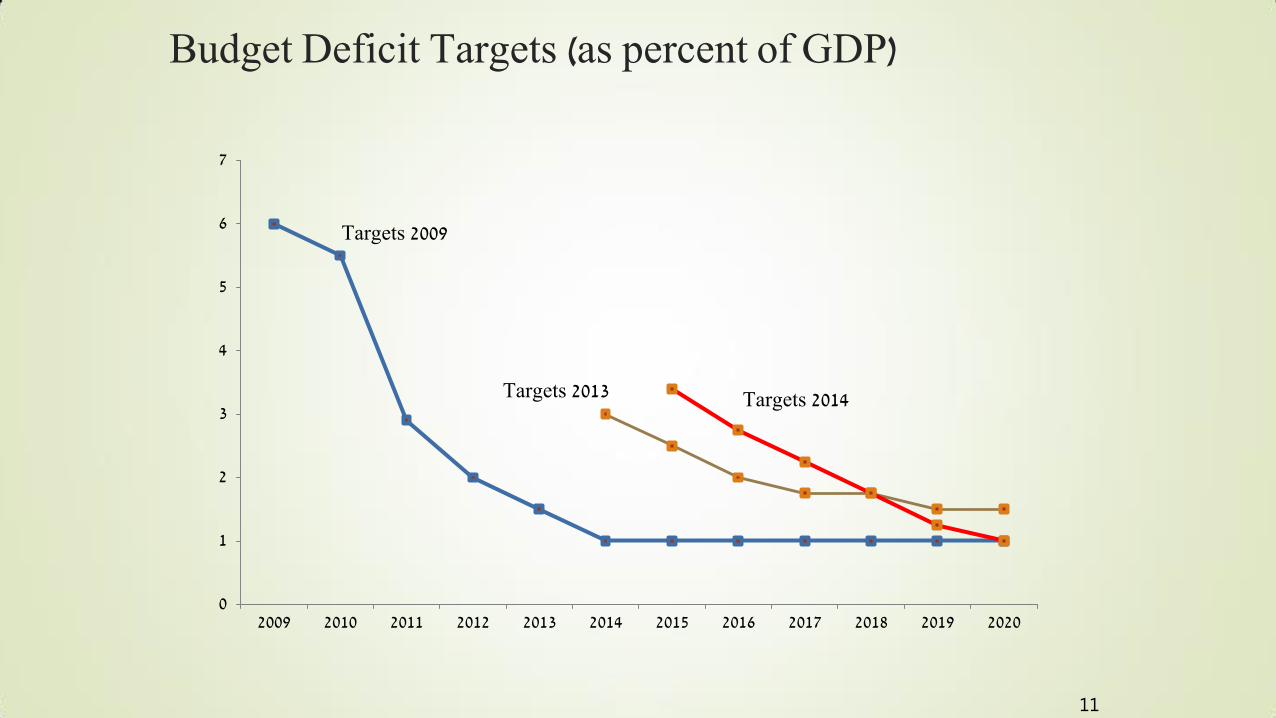

0

1

2

3

4

5

6

7

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

11

Budget Deficit Targets (as percent of GDP)

Targets 2009

Targets 2013 Targets 2014

12

Prosperity-Promoting Policies

Market-friendly vs. government-controlled economy

Flexible labor markets vs. excessive regulation and “workers’ rights”

Professional, long-term considerations vs. political, populist, short-term approach

The role of public education

80

90

100

110

120

130

140

150

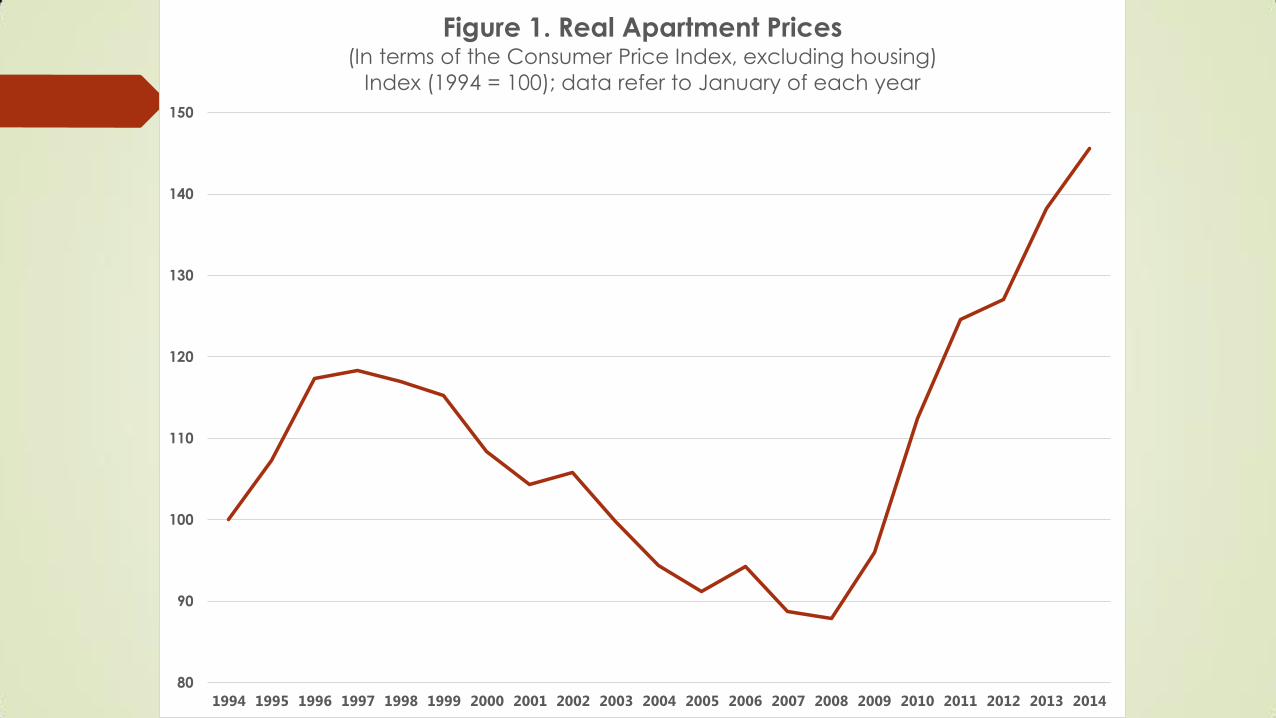

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Figure 1. Real Apartment Prices (In terms of the Consumer Price Index, excluding housing)

Index (1994 = 100); data refer to January of each year

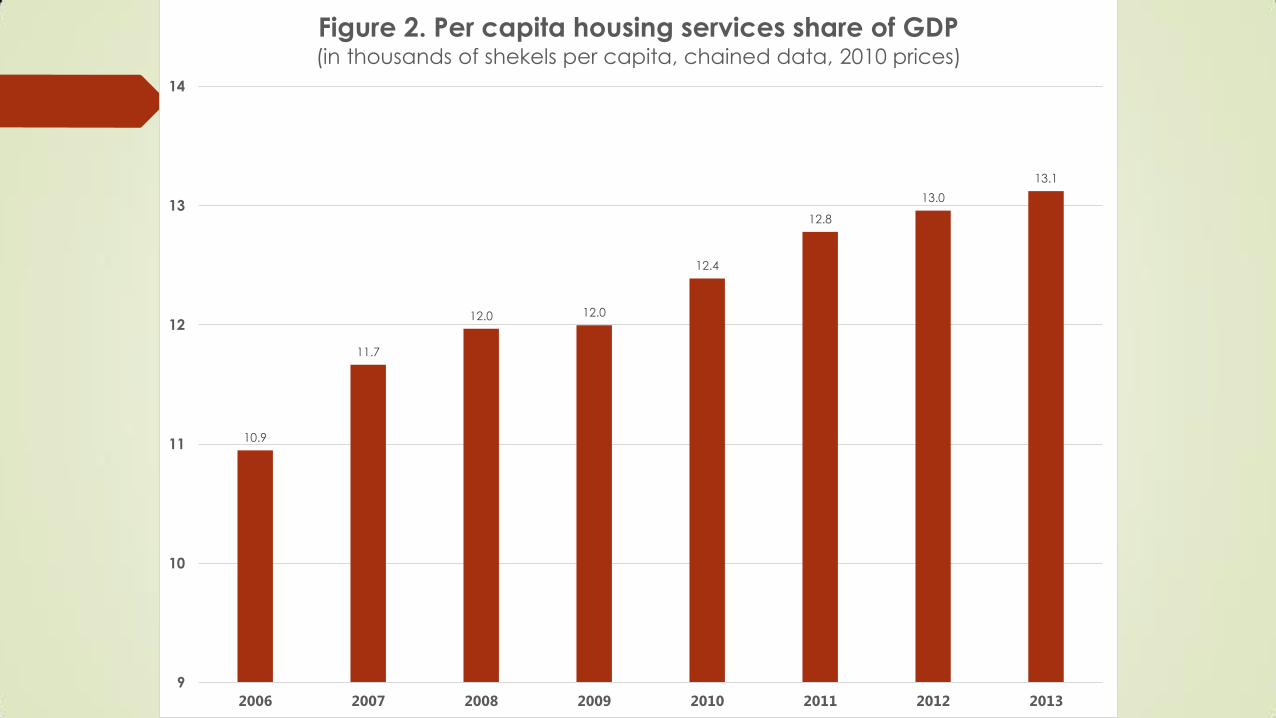

10.9

11.7

12.0 12.0

12.4

12.8

13.0

13.1

9

10

11

12

13

14

2006 2007 2008 2009 2010 2011 2012 2013

Figure 2. Per capita housing services share of GDP (in thousands of shekels per capita, chained data, 2010 prices)

80

85

90

95

100

105

110

115

120

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Figure 4. The ratio between apartment prices (the value of

the property) and rental prices (the value of housing

services) Index (1999 = 100); data refer to January of each year

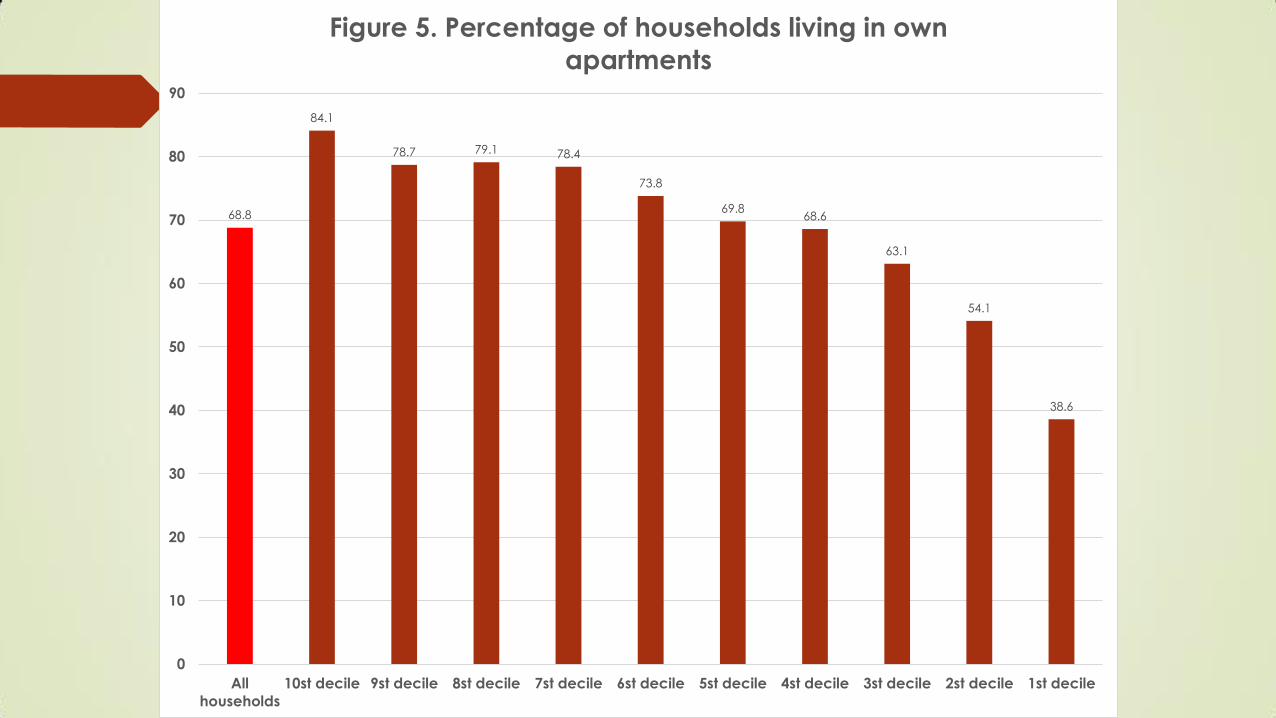

68.8

84.1

78.7 79.1 78.4

73.8

69.8 68.6

63.1

54.1

38.6

0

10

20

30

40

50

60

70

80

90

All

households

10st decile 9st decile 8st decile 7st decile 6st decile 5st decile 4st decile 3st decile 2st decile 1st decile

Figure 5. Percentage of households living in own

apartments

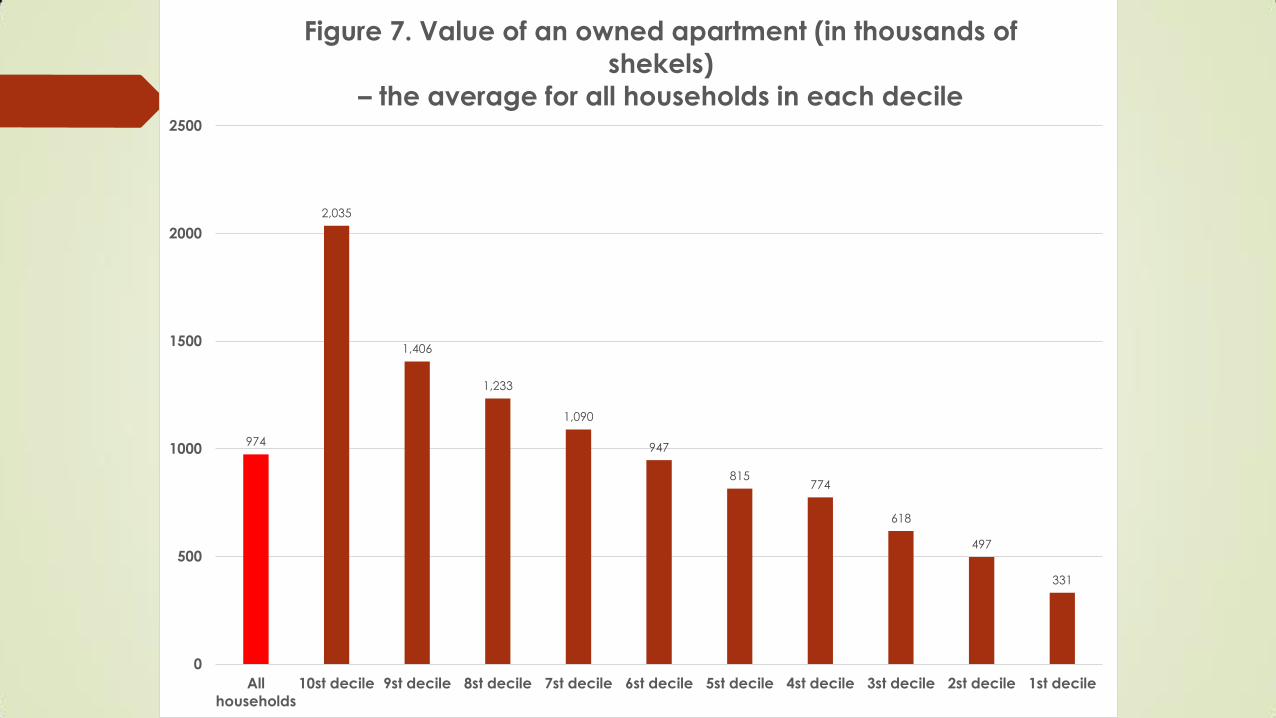

974

2,035

1,406

1,233

1,090

947

815 774

618

497

331

0

500

1000

1500

2000

2500

All

households

10st decile 9st decile 8st decile 7st decile 6st decile 5st decile 4st decile 3st decile 2st decile 1st decile

Figure 7. Value of an owned apartment (in thousands of

shekels)

– the average for all households in each decile

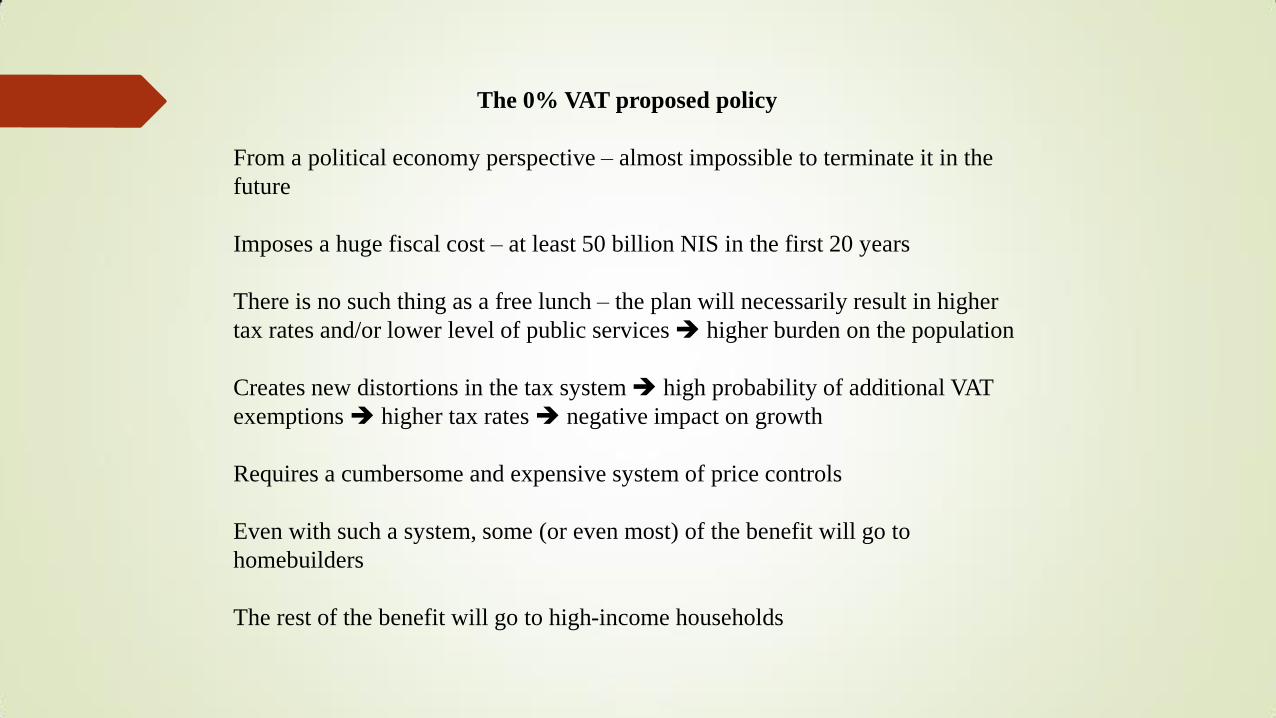

The 0% VAT proposed policy

From a political economy perspective – almost impossible to terminate it in the

future

Imposes a huge fiscal cost – at least 50 billion NIS in the first 20 years

There is no such thing as a free lunch – the plan will necessarily result in higher

tax rates and/or lower level of public services higher burden on the population

Creates new distortions in the tax system high probability of additional VAT

exemptions higher tax rates negative impact on growth

Requires a cumbersome and expensive system of price controls

Even with such a system, some (or even most) of the benefit will go to

homebuilders

The rest of the benefit will go to high-income households

In the department of economy, an act, a habit, an institution, a law, gives birth

not only to an effect, but to a series of effects. Of these effects, the first only is immediate; it manifests itself simultaneously with its cause - it is seen. The others

unfold in succession - they are not seen: it is well for us, if they are foreseen.

Between a good and a bad economist this constitutes the whole difference - the

one takes account of the visible effect; the other takes account both of the effects which are seen, and also of those which it is necessary to foresee. Now

this difference is enormous, for it almost always happens that when the

immediate consequence is favourable, the ultimate consequences are fatal,

and the converse. Hence it follows that the bad economist pursues a small present good, which will be followed by a great evil to come, while the true

economist pursues a great good to come, - at the risk of a small present evil.

That Which is Seen, and That Which is Not Seen Frederic Bastiat, 1850

The zero-VAT plan is not intended for economists

Yair Lapid, 2014