Embed Size (px)

Citation preview

SNB Abandon

of Euro Cap

Actions for

Finance Directors

Expert Webcast

Friday, 23 January 2015

Welcome

Lukas Marty

Head of Audit

2© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

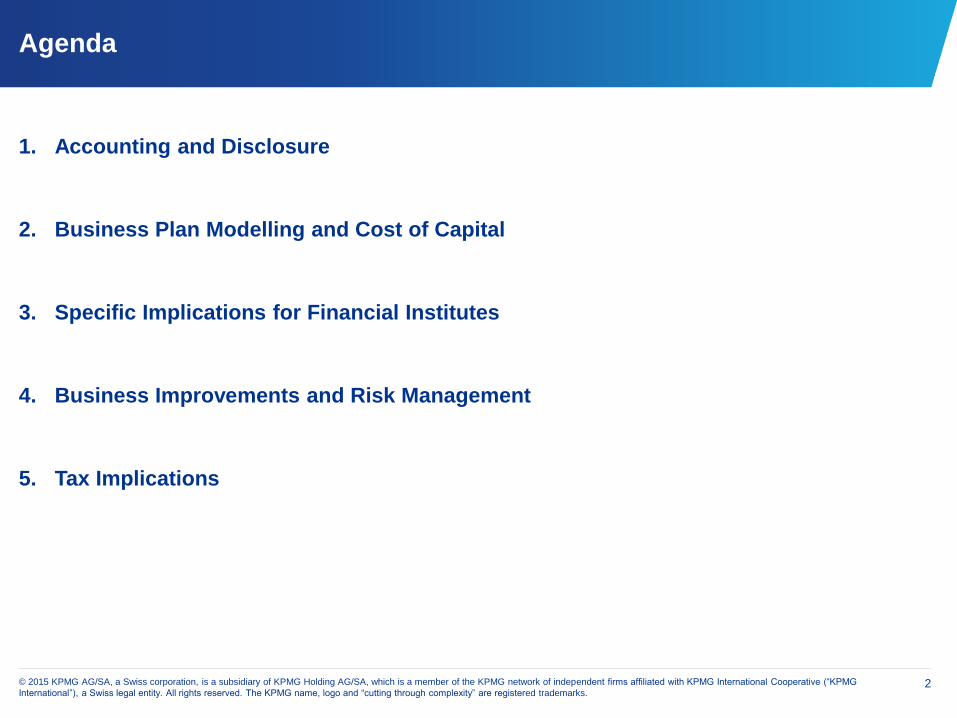

Agenda

1. Accounting and Disclosure

2. Business Plan Modelling and Cost of Capital

3. Specific Implications for Financial Institutes

4. Business Improvements and Risk Management

5. Tax Implications

Accounting and Disclosure

Reto Eberle

Department of Professional Practice

4© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

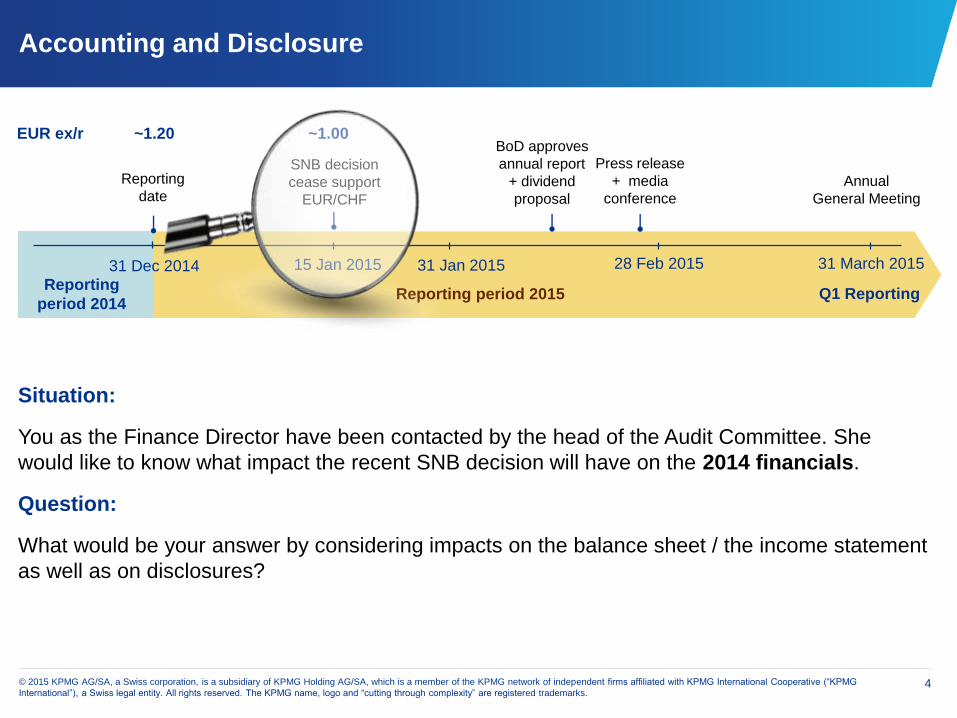

Accounting and Disclosure

Situation:

You as the Finance Director have been contacted by the head of the Audit Committee. She

would like to know what impact the recent SNB decision will have on the 2014 financials.

Question:

What would be your answer by considering impacts on the balance sheet / the income statement

as well as on disclosures?

SNB decision

cease support

EUR/CHF

15 Jan 2015 28 Feb 2015 31 March 2015

EUR ex/r ~1.20 ~1.00

Press release

+ media

conference

BoD approves

annual report

+ dividend

proposal

Annual

General Meeting

Reporting

date

Reporting period 2015 Q1 Reporting

31 Jan 201531 Dec 2014

Reporting

period 2014

5© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

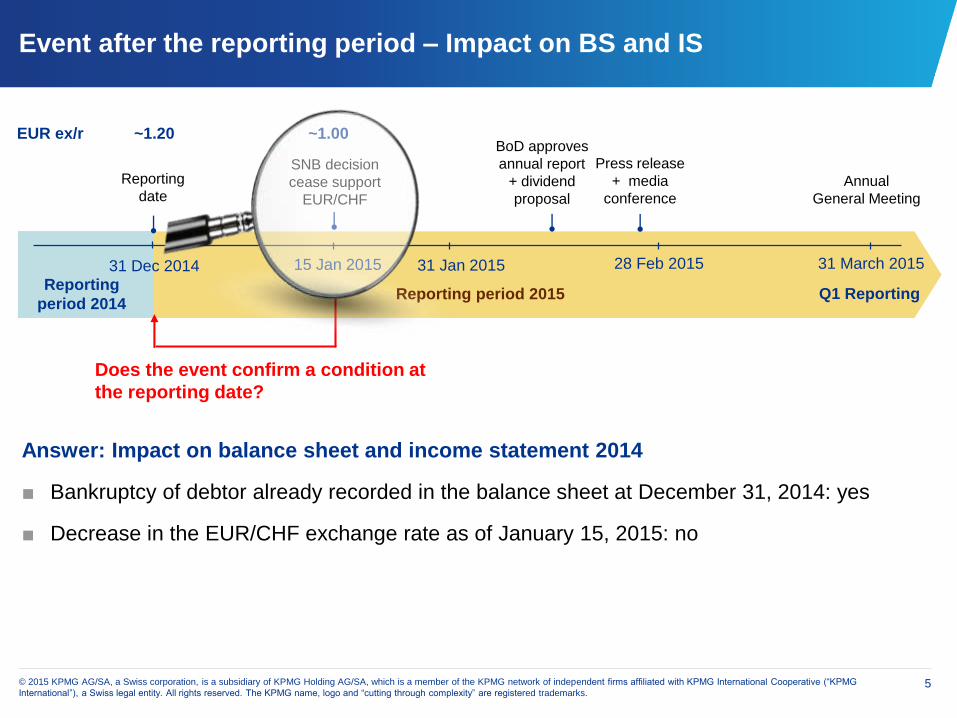

Answer: Impact on balance sheet and income statement 2014

■ Bankruptcy of debtor already recorded in the balance sheet at December 31, 2014: yes

■ Decrease in the EUR/CHF exchange rate as of January 15, 2015: no

SNB decision

cease support

EUR/CHF

15 Jan 2015 28 Feb 2015 31 March 2015

EUR ex/r ~1.20 ~1.00

Press release

+ media

conference

BoD approves

annual report

+ dividend

proposal

Annual

General Meeting

Reporting

date

Reporting period 2015 Q1 Reporting

31 Jan 201531 Dec 2014

Reporting

period 2014

Does the event confirm a condition at

the reporting date?

Event after the reporting period – Impact on BS and IS

6© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

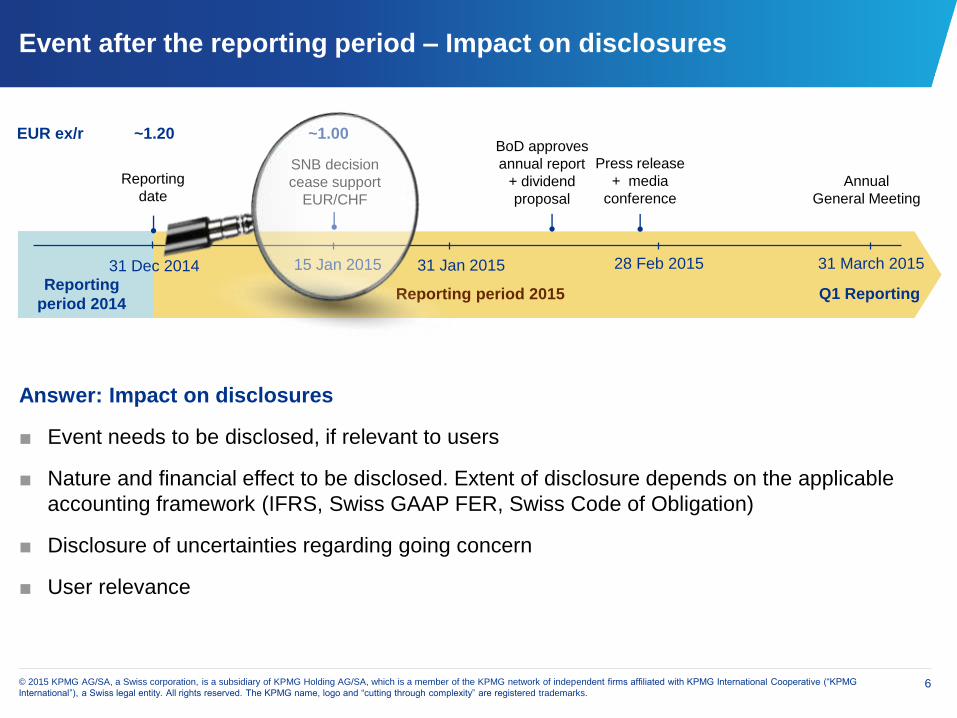

Answer: Impact on disclosures

■ Event needs to be disclosed, if relevant to users

■ Nature and financial effect to be disclosed. Extent of disclosure depends on the applicable

accounting framework (IFRS, Swiss GAAP FER, Swiss Code of Obligation)

■ Disclosure of uncertainties regarding going concern

■ User relevance

SNB decision

cease support

EUR/CHF

15 Jan 2015 28 Feb 2015 31 March 2015

EUR ex/r ~1.20 ~1.00

Press release

+ media

conference

BoD approves

annual report

+ dividend

proposal

Annual

General Meeting

Reporting

date

Reporting period 2015 Q1 Reporting

31 Jan 201531 Dec 2014

Reporting

period 2014

Event after the reporting period – Impact on disclosures

7© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

Dividend

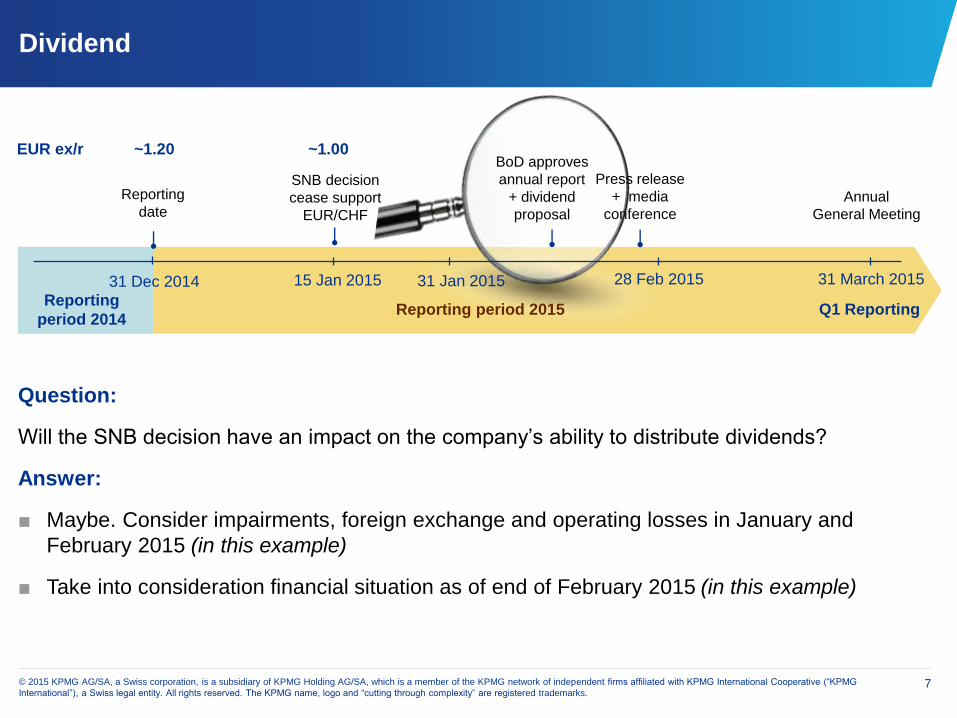

Question:

Will the SNB decision have an impact on the company’s ability to distribute dividends?

Answer:

■ Maybe. Consider impairments, foreign exchange and operating losses in January and

February 2015 (in this example)

■ Take into consideration financial situation as of end of February 2015 (in this example)

SNB decision

cease support

EUR/CHF

15 Jan 2015 28 Feb 2015 31 March 2015

EUR ex/r ~1.20 ~1.00

Press release

+ media

conference

BoD approves

annual report

+ dividend

proposal

Annual

General Meeting

Reporting

date

Reporting period 2015 Q1 Reporting

31 Jan 201531 Dec 2014

Reporting

period 2014

8© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

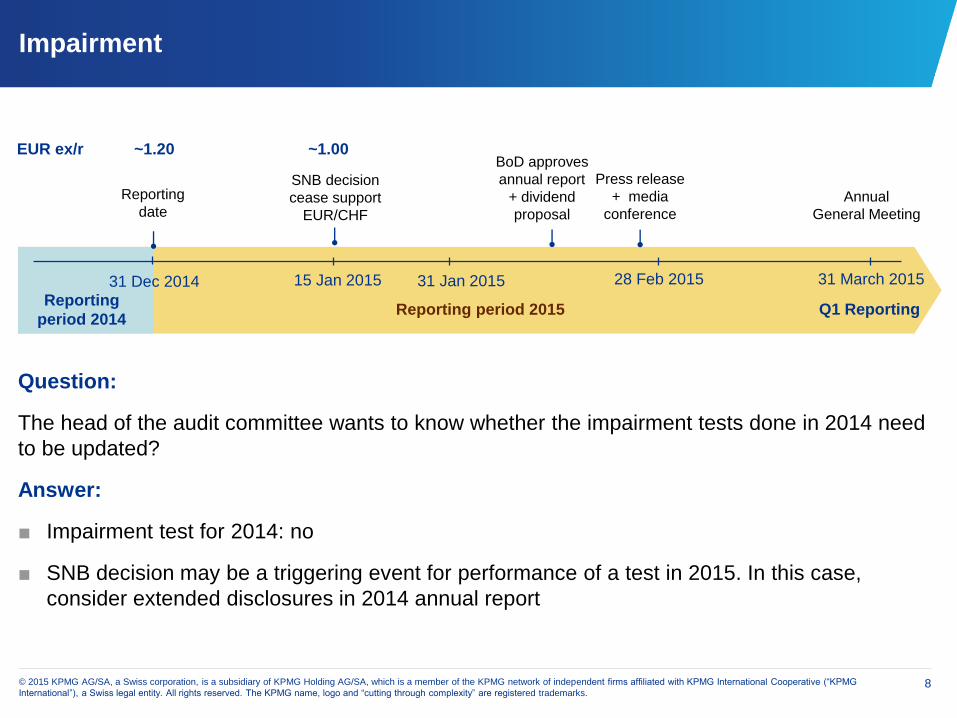

Impairment

Question:

The head of the audit committee wants to know whether the impairment tests done in 2014 need

to be updated?

Answer:

■ Impairment test for 2014: no

■ SNB decision may be a triggering event for performance of a test in 2015. In this case,

consider extended disclosures in 2014 annual report

SNB decision

cease support

EUR/CHF

15 Jan 2015 28 Feb 2015 31 March 2015

EUR ex/r ~1.20 ~1.00

Press release

+ media

conference

BoD approves

annual report

+ dividend

proposal

Annual

General Meeting

Reporting

date

Reporting period 2015 Q1 Reporting

31 Jan 201531 Dec 2014

Reporting

period 2014

Business Plan Modelling

and Cost of Capital

Johannes Post

Head of Valuation and Financial Modeling

10© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

Business plan modelling and cost of capital

Purposes of financial planning

■ Impairment testing

■ Annual budgets

■ Mid-term planning

■ Short-term liquidity planning

Use of forward looking financials

■ Disclosures to financial reporting 2014

■ Ad-hoc media questions

■ Guidance for the IR department

■ Next earnings call

■ Tax planning and transfer pricing

■ Debt financing and related coverage ratios

11© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

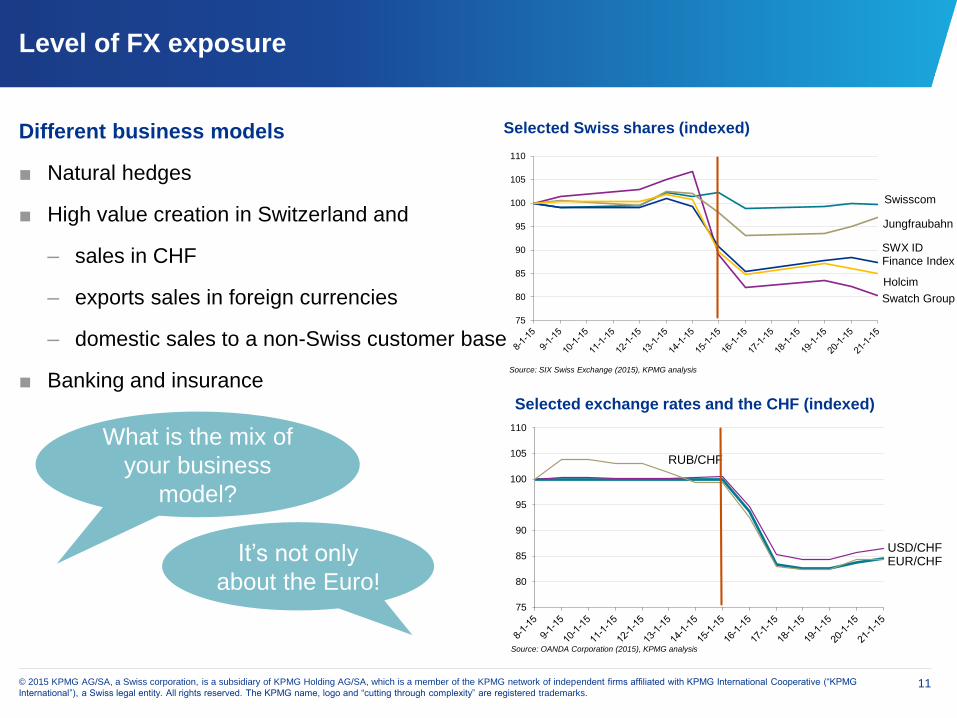

Level of FX exposure

Different business models

■ Natural hedges

■ High value creation in Switzerland and

– sales in CHF

– exports sales in foreign currencies

– domestic sales to a non-Swiss customer base

■ Banking and insurance

What is the mix of

your business

model?

It’s not only

about the Euro!

Swisscom

Swatch Group

Jungfraubahn

SWX ID Finance Index

Holcim

75

80

85

90

95

100

105

110

Selected Swiss shares (indexed)

Source: SIX Swiss Exchange (2015), KPMG analysis

EUR/CHFUSD/CHF

RUB/CHF

75

80

85

90

95

100

105

110

Selected exchange rates and the CHF (indexed)

Source: OANDA Corporation (2015), KPMG analysis

12© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

Application of FX rates in the business plan

Technical adjustments of the FX rates in the business model

■ Uncertainty about the FX rates in terms of magnitude and timing

■ Spot rates or forward looking rates

■ Simulations, scenarios and sensitivities help to cope with this uncertainty

What is the

appropriate

granularity of my

model?

Is my model integrated and

flexible to assess scenarios

and sensitivities?

What is the right

balance of accuracy

and practicality?

13© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

Assessment of the business impact

Economic impact of the unexpected appreciation of the FX

■ Reduction of sales volume

■ Adjustments of cost basis

– Positive if importing goods and services

– Personnel costs – timing and magnitude?

– Suppliers pass on their price and margin effects?

– Related costs with new hedging strategies

■ Revaluation of financial investments

■ Investments in CAPEX, Working Capital or M&A

■ Interest expenses

14© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

Verification of assumptions

Sound verification of assumptions may include:

■ Historical trends of the own business

■ Sector expectations regarding growth and profitability

■ Benchmark data of peer companies

■ Macroeconomic trends

■ Analyst reports and capital market consensus

How reliable are

those data in the

current

environment?

Under IFRS the application of the concepts Value in Use or

Fair Value less Cost of Disposal should be reconsidered

Market capitalization of publicly listed companies might currently deviate substantially

from a fundamental value

15© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

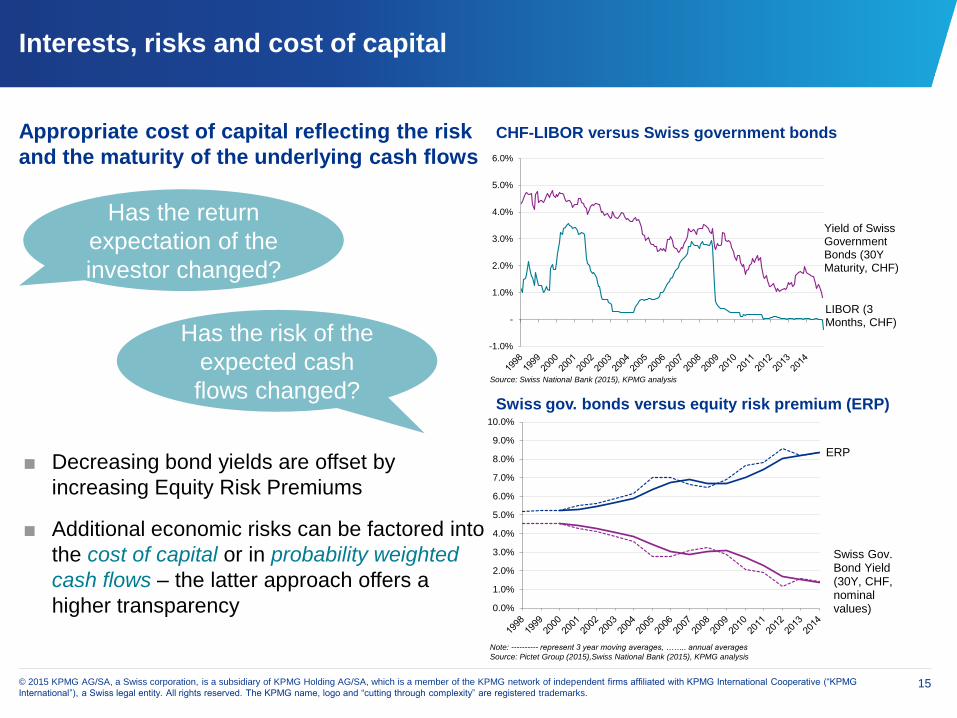

Interests, risks and cost of capital

Appropriate cost of capital reflecting the risk

and the maturity of the underlying cash flows

Swiss gov. bonds versus equity risk premium (ERP)

Note: ---------- represent 3 year moving averages, …….. annual averages

Source: Pictet Group (2015),Swiss National Bank (2015), KPMG analysis

■ Decreasing bond yields are offset by

increasing Equity Risk Premiums

■ Additional economic risks can be factored into

the cost of capital or in probability weighted

cash flows – the latter approach offers a

higher transparency

Has the return

expectation of the

investor changed?

Has the risk of the

expected cash

flows changed?

LIBOR (3 Months, CHF)

Yield of Swiss Government Bonds (30Y Maturity, CHF)

-1.0%

-

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

CHF-LIBOR versus Swiss government bonds

Source: Swiss National Bank (2015), KPMG analysis

Swiss Gov. Bond Yield (30Y, CHF, nominal values)

ERP

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Specific Implications for

Financial Institutes

Philipp Rickert

Head of Financial Services

17© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

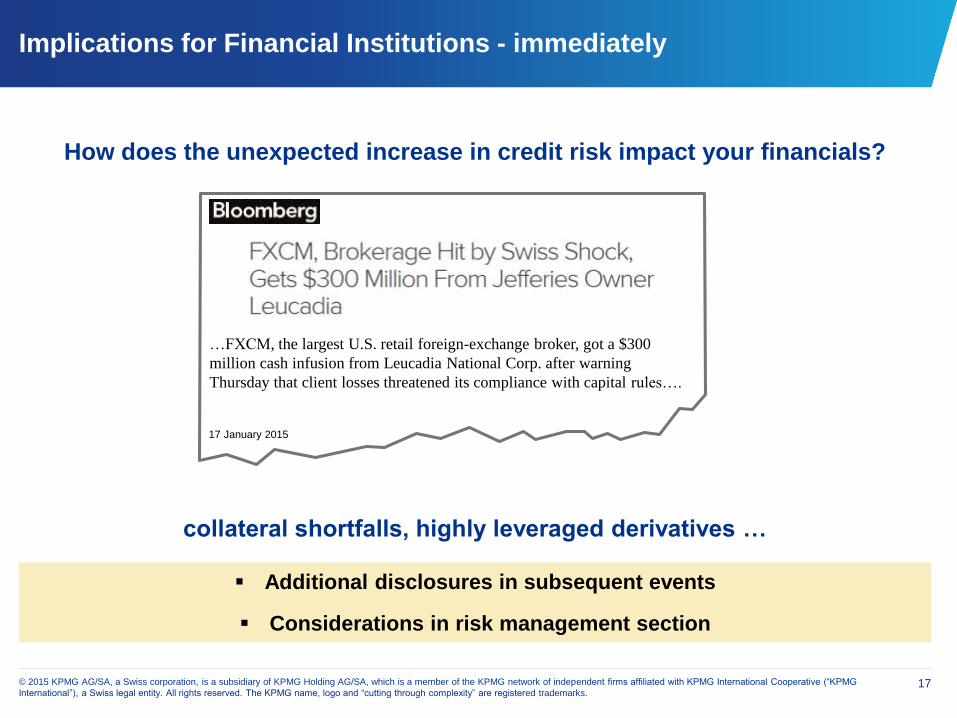

Implications for Financial Institutions - immediately

How does the unexpected increase in credit risk impact your financials?

collateral shortfalls, highly leveraged derivatives …

Additional disclosures in subsequent events

Considerations in risk management section

…FXCM, the largest U.S. retail foreign-exchange broker, got a $300

million cash infusion from Leucadia National Corp. after warning

Thursday that client losses threatened its compliance with capital rules….

17 January 2015

18© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

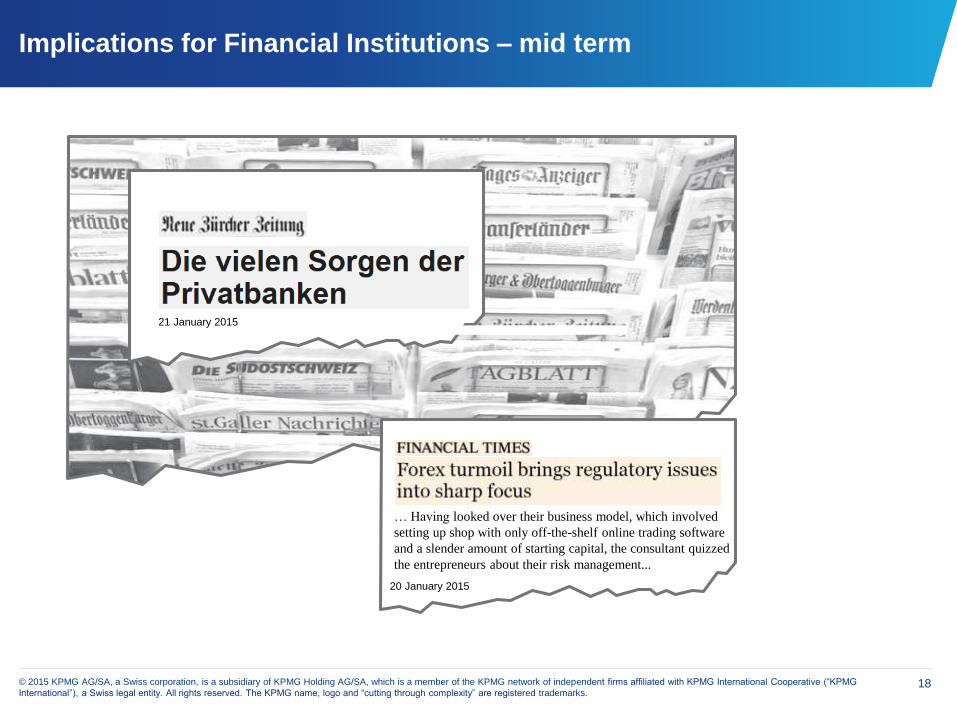

… Having looked over their business model, which involved

setting up shop with only off-the-shelf online trading software

and a slender amount of starting capital, the consultant quizzed

the entrepreneurs about their risk management...

21 January 2015

20 January 2015

Implications for Financial Institutions – mid term

Business Improvements

and Risk Management

Anne van Heerden

Head of Advisory

20© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

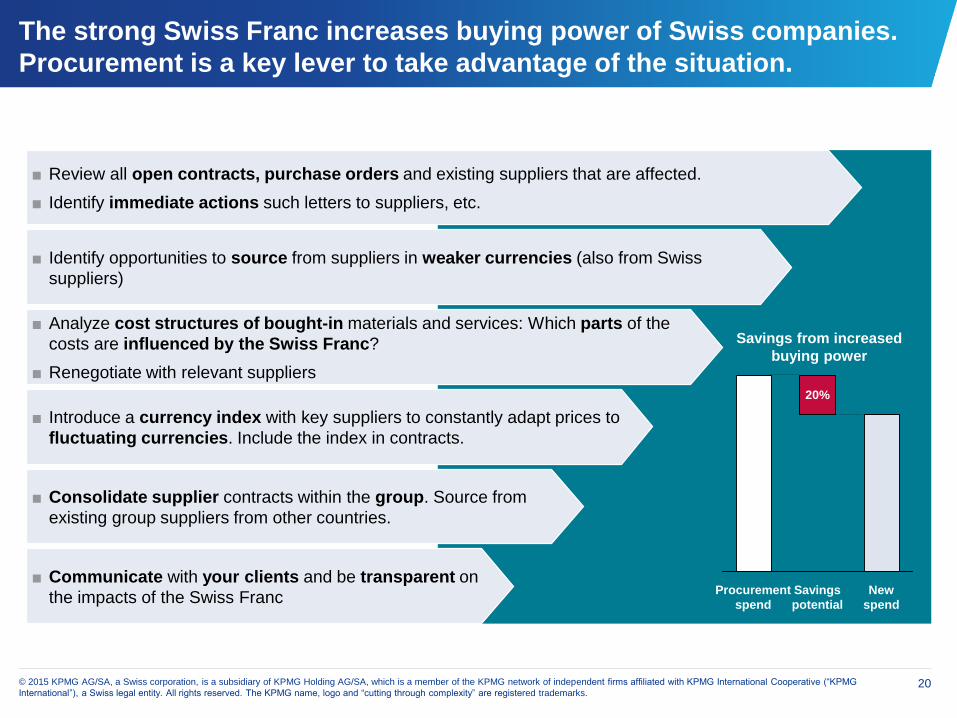

The strong Swiss Franc increases buying power of Swiss companies.

Procurement is a key lever to take advantage of the situation.

■ Review all open contracts, purchase orders and existing suppliers that are affected.

■ Identify immediate actions such letters to suppliers, etc.

■ Identify opportunities to source from suppliers in weaker currencies (also from Swiss

suppliers)

■ Analyze cost structures of bought-in materials and services: Which parts of the

costs are influenced by the Swiss Franc?

■ Renegotiate with relevant suppliers

■ Introduce a currency index with key suppliers to constantly adapt prices to

fluctuating currencies. Include the index in contracts.

■ Consolidate supplier contracts within the group. Source from

existing group suppliers from other countries.

■ Communicate with your clients and be transparent on

the impacts of the Swiss Franc

20%

Procurement

spend

New

spend

Savings

potential

Savings from increased

buying power

21© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

Immediate FX Risk Management Measures

2. Gain Transparency

4. Develop new Hedging Strategy

5. Monitor Risk

3. Review existing Hedging Strategy

Please insert your text

6. Set up Risk Reporting Cockpit

Are you prepared for the new CHF volatility and next FX meltdown?

1. Identify Risk

Tax Implications

Peter Uebelhart

Head of Tax

23© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

Tax implications

Year-end considerations

■ Depreciation / Value adjustment: Relevant period

■ Implications of losses

– Revaluation of Investments: Claw-back / Set-off against profits

– Reduction of distributable reserves / Upstream loans

Considerations for the current year

■ Internal loans, services, supplies

■ P/L implications of FX movement in the current year

■ Allocation of currency risk, interest rates

■ Relocation of business activities

24© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

Q&A

25© 2015 KPMG AG/SA, a Swiss corporation, is a subsidiary of KPMG Holding AG/SA, which is a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG

International”), a Swiss legal entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks.

Contacts

Lukas Marty

Partner

Head of Audit

+41 58 249 36 49

Philipp Rickert

Partner

Head of Financial

Services

+41 58 249 42 13

Anne van Heerden

Partner

Head of Advisory

+41 58 249 28 61

annevanheerden

@kpmg.com

Peter Uebelhart

Partner

Head of Tax

+41 58 249 42 24

KPMG AG

Badenerstrasse 172

P.O. Box 1872

CH-8026 Zurich

www.kpmg.ch

Reto Eberle

Partner

Department of

Professional Practice

+41 58 249 42 43

Johannes Post

Partner

Head of Valuation

& Financial Modelling

+41 58 249 35 92

© 2015 KPMG AG/SA, a Swiss corporation, is a

subsidiary of KPMG Holding AG/SA, which is a

member of the KPMG network of independent firms

affiliated with KPMG International Cooperative

(“KPMG International”), a Swiss legal entity. All rights

reserved. The KPMG name, logo and “cutting through

complexity” are registered trademarks.