Embed Size (px)

Citation preview

SPECIAL MONTHLY REPORT ONSPECIAL MONTHLY REPORT ON

BullionsBullions(July 2015)

1

BU

LL

ION

S

July 2015

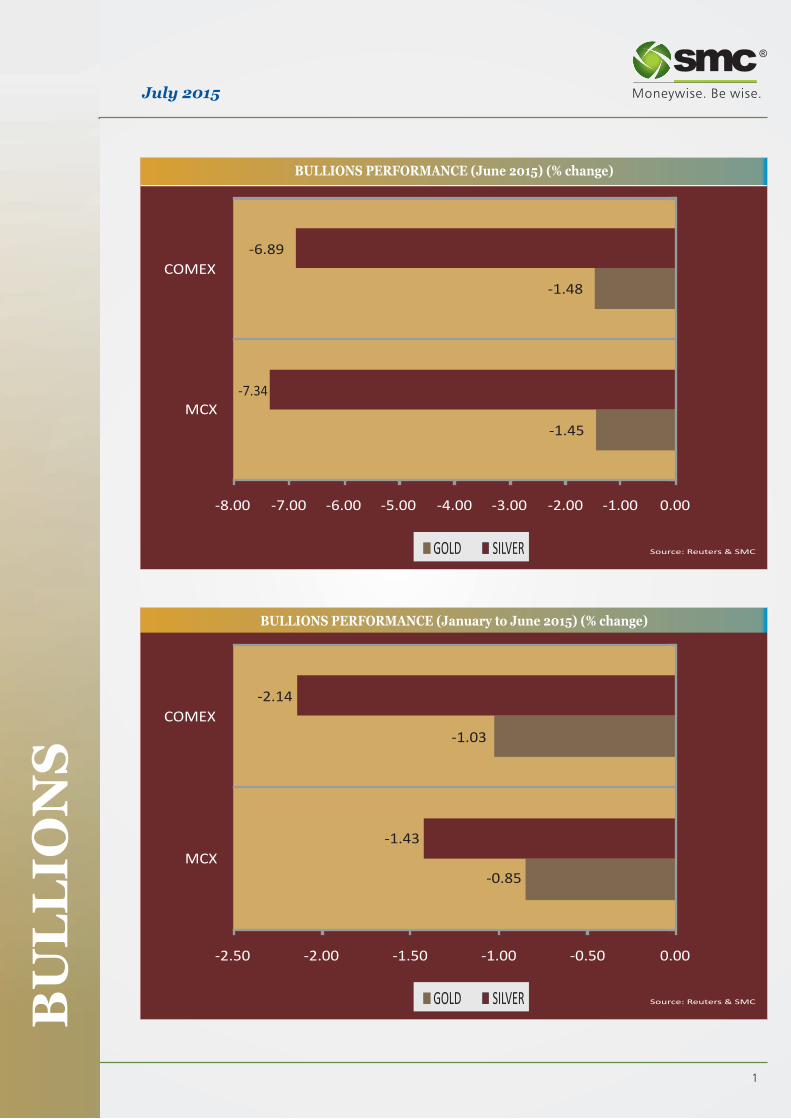

BULLIONS PERFORMANCE (June 2015) (% change)

BULLIONS PERFORMANCE (January to June 2015) (% change)

-1.45

-1.48

-7.34

-6.89

-8.00 -7.00 -6.00 -5.00 -4.00 -3.00 -2.00 -1.00 0.00

MCX

COMEX

GOLD SILVER Source: Reuters & SMC

-0.85

-1.03

-1.43

-2.14

-2.50 -2.00 -1.50 -1.00 -0.50 0.00

MCX

COMEX

GOLD SILVER Source: Reuters & SMC

2

BULLIONS

Overview

In the month of June bullion counter traded with

volatile path as on one side rise in greenback and

fear of interest rate hike in US kept the prices under

pressure while on the other side physical demand at

lower levels capped the downside. Overall gold

traded in range of 26350-27245 in MCX and

$1161.9-1204.7 in COMEX. Silver traded in range of

$15.43-17.18 in COMEX and 35272-39150 in MCX.

Meanwhile movement of local currency rupee

affected the prices on domestic bourses. In early

June yellow metal got some support from bullish

remarks from the Federal Reserve and on safe-

haven demand due to Greece debt worries. While the

Fed did not raise U.S. interest rates in its meeting

and stated that U.S. economy continues to improve,

Yellen did signal in her press briefing that the Fed

will remain “highly accommodative” even when it

does raise interest rates likely later this year.

Increasing worries about Greece defaulting on its

debt obligations to the European Union and

International Monetary Fund have supported the

prices. Precious metals have benefited strongly in

recent years from record low U.S. rates, which have

cut the opportunity cost of holding non-yielding

assets while keeping the dollar in check. Fear of hike

in interest rate by fed offset the safe haven demand

amid Greece concerns and pressurized gold lower in

second half of the month.

Outlook

In the month of July bullion counter can trade on

volatile path as US interest rates hike and Greece

debt concerns can give direction to the prices.

Meanwhile global geopolitical tensions in Middle

East and increase in physical demand may cap the

downside. On domestic bourses the movements of

local currency rupee will be the key factor to watch

out which can move in range of 62.70-64.30 in the

month of July. Gold can trade in range of Rs

25700-27500 in MCX and $1130-1230 in

COMEX. Silver can trade in range of 34000-

39500 in MCX and $15-17 in COMEX. The

gold/silver ratio can move in range of 68-76 in near

term. Bailout talks between the Greek leftwing

government and foreign lenders broke down over BU

LL

ION

S

the weekend and the European Central Bank froze vital

funding support to Greece's banks, leaving Athens with

little choice but to shut down the system to keep the

banks from collapsing. The failure to reach a deal with

creditors resulted in default of 1.6 billion euros of loans

from the International Monetary Fund The impending

default on the IMF loans leaves Greece sliding towards a

euro exit and also carries broad implications for the

global financial system. The World Gold Council (WGC)

announced that the demand for gold in India continues

to be stable with a 15 per cent increase in Q1 Calendar

Year 2015 at 191.7 tonnes, as compared with 167.1

tonnes in Q1 CY2014. Partial removal of the import

curbs in India (with the exception of a duty reduction)

and the Budget announcements introducing new gold

products, the environment for gold has been

encouraging in the past few months, resulting in buying

behavior slowly returning to normalcy.

Uncertainty in Greece over debt crises

Greek voters have decisively rejected the terms

of an international bailout.

The final result in the referendum, published by the

interior ministry, was 61.3% "No", against 38.7% who

voted "Yes". Greece's governing Syriza party had

campaigned for a "No", saying the bailout terms were

humiliating.

Greek Prime Minister Alexis Tsipras said that Greeks

had voted for a "Europe of solidarity and democracy".

“Greece will go back to the negotiating table and our

primary priority is to reinstate the financial stability of

the country," he said in a televised address.

July 2015

3

BU

LL

ION

SJuly 2015

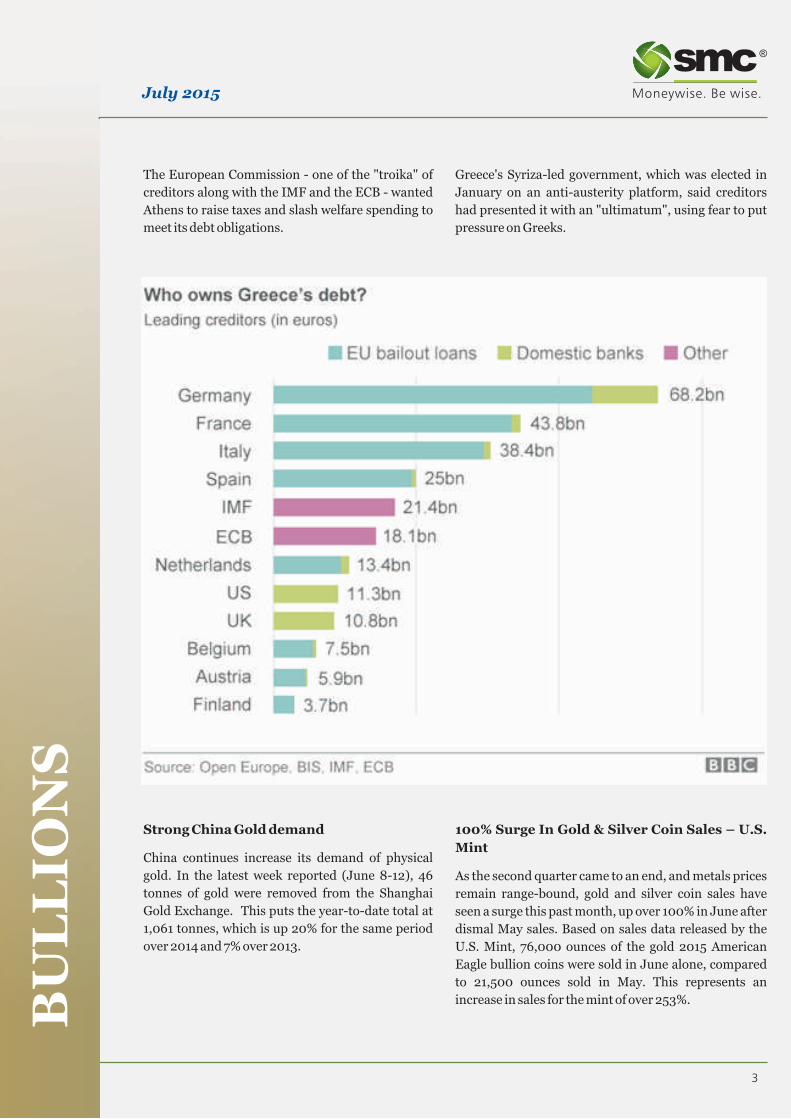

Greece's Syriza-led government, which was elected in

January on an anti-austerity platform, said creditors

had presented it with an "ultimatum", using fear to put

pressure on Greeks.

The European Commission - one of the "troika" of

creditors along with the IMF and the ECB - wanted

Athens to raise taxes and slash welfare spending to

meet its debt obligations.

100% Surge In Gold & Silver Coin Sales – U.S.

Mint

As the second quarter came to an end, and metals prices

remain range-bound, gold and silver coin sales have

seen a surge this past month, up over 100% in June after

dismal May sales. Based on sales data released by the

U.S. Mint, 76,000 ounces of the gold 2015 American

Eagle bullion coins were sold in June alone, compared

to 21,500 ounces sold in May. This represents an

increase in sales for the mint of over 253%.

Strong China Gold demand

China continues increase its demand of physical

gold. In the latest week reported (June 8-12), 46

tonnes of gold were removed from the Shanghai

Gold Exchange. This puts the year-to-date total at

1,061 tonnes, which is up 20% for the same period

over 2014 and 7% over 2013.

4

BU

LL

ION

SJuly 2015

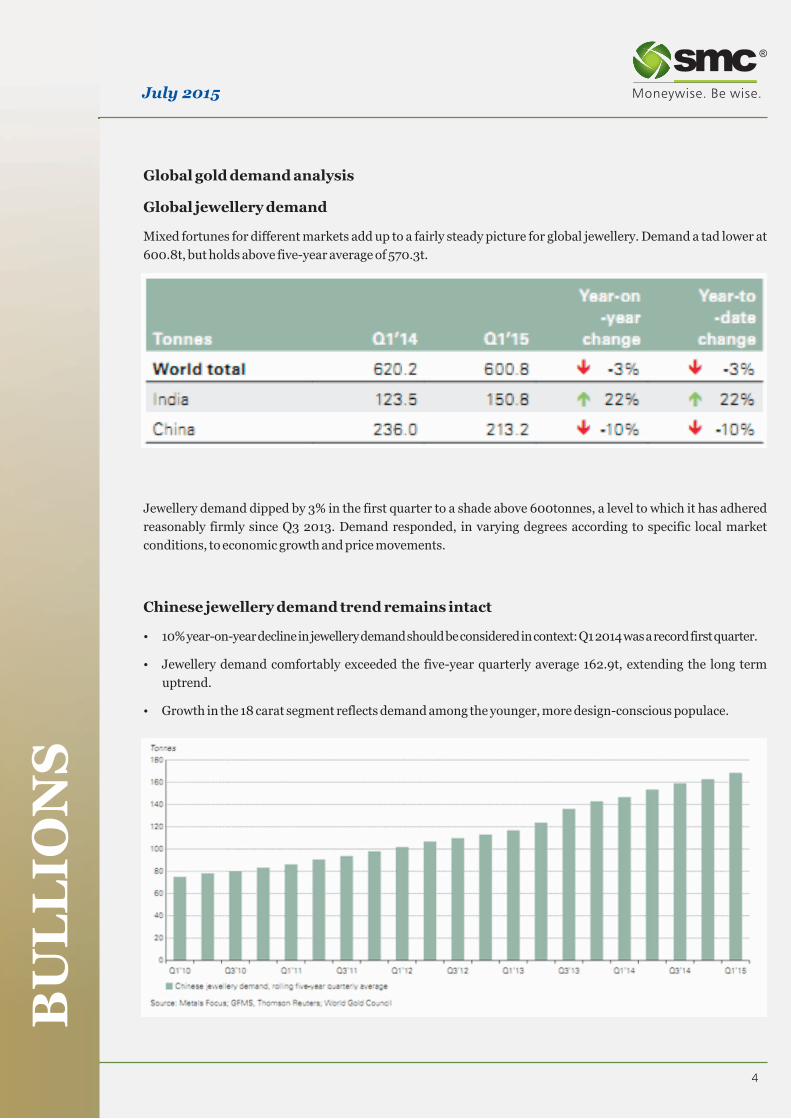

Global gold demand analysis

Global jewellery demand

Mixed fortunes for different markets add up to a fairly steady picture for global jewellery. Demand a tad lower at

600.8t, but holds above five-year average of 570.3t.

Jewellery demand dipped by 3% in the first quarter to a shade above 600tonnes, a level to which it has adhered

reasonably firmly since Q3 2013. Demand responded, in varying degrees according to specific local market

conditions, to economic growth and price movements.

Chinese jewellery demand trend remains intact

�10% year-on-year decline in jewellery demand should be considered in context: Q1 2014 was a record first quarter.

�Jewellery demand comfortably exceeded the five-year quarterly average 162.9t, extending the long term

uptrend.

�Growth in the 18 carat segment reflects demand among the younger, more design-conscious populace.

5

BU

LL

ION

SJuly 2015

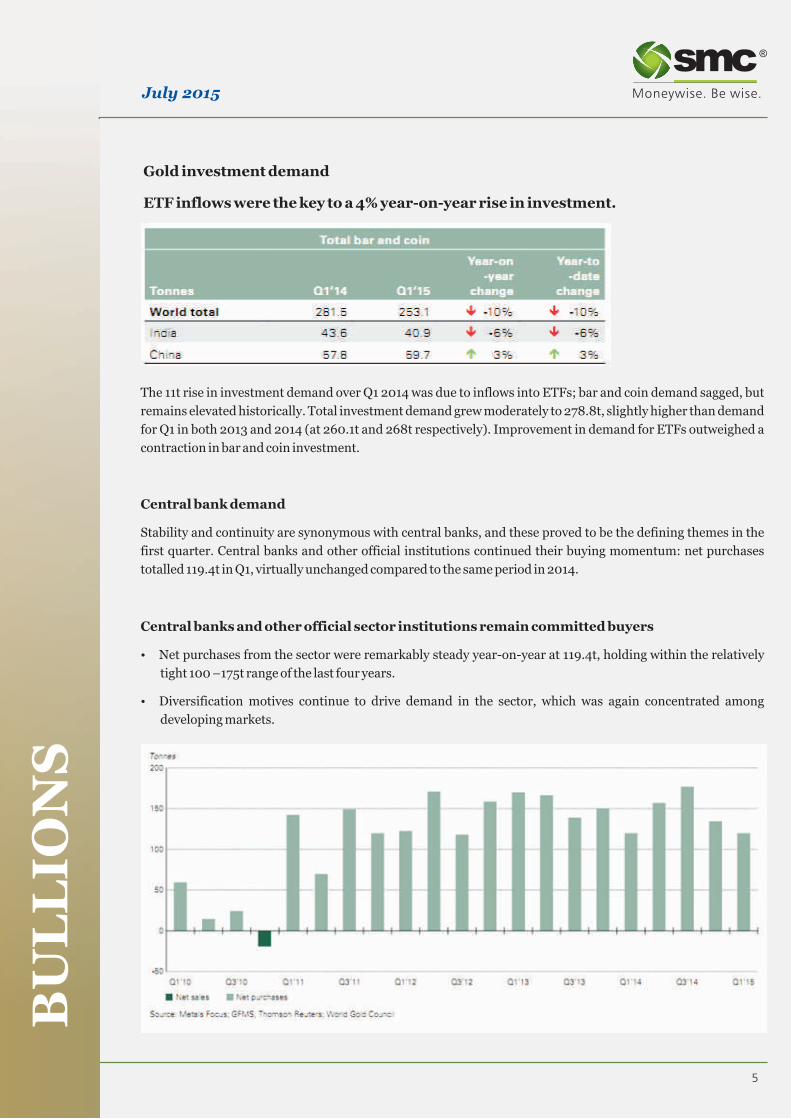

Gold investment demand

ETF inflows were the key to a 4% year-on-year rise in investment.

The 11t rise in investment demand over Q1 2014 was due to inflows into ETFs; bar and coin demand sagged, but

remains elevated historically. Total investment demand grew moderately to 278.8t, slightly higher than demand

for Q1 in both 2013 and 2014 (at 260.1t and 268t respectively). Improvement in demand for ETFs outweighed a

contraction in bar and coin investment.

Central bank demand

Stability and continuity are synonymous with central banks, and these proved to be the defining themes in the

first quarter. Central banks and other official institutions continued their buying momentum: net purchases

totalled 119.4t in Q1, virtually unchanged compared to the same period in 2014.

Central banks and other official sector institutions remain committed buyers

�Net purchases from the sector were remarkably steady year-on-year at 119.4t, holding within the relatively

tight 100 –175t range of the last four years.

�Diversification motives continue to drive demand in the sector, which was again concentrated among

developing markets.

6

BU

LL

ION

SJuly 2015

Gold supply

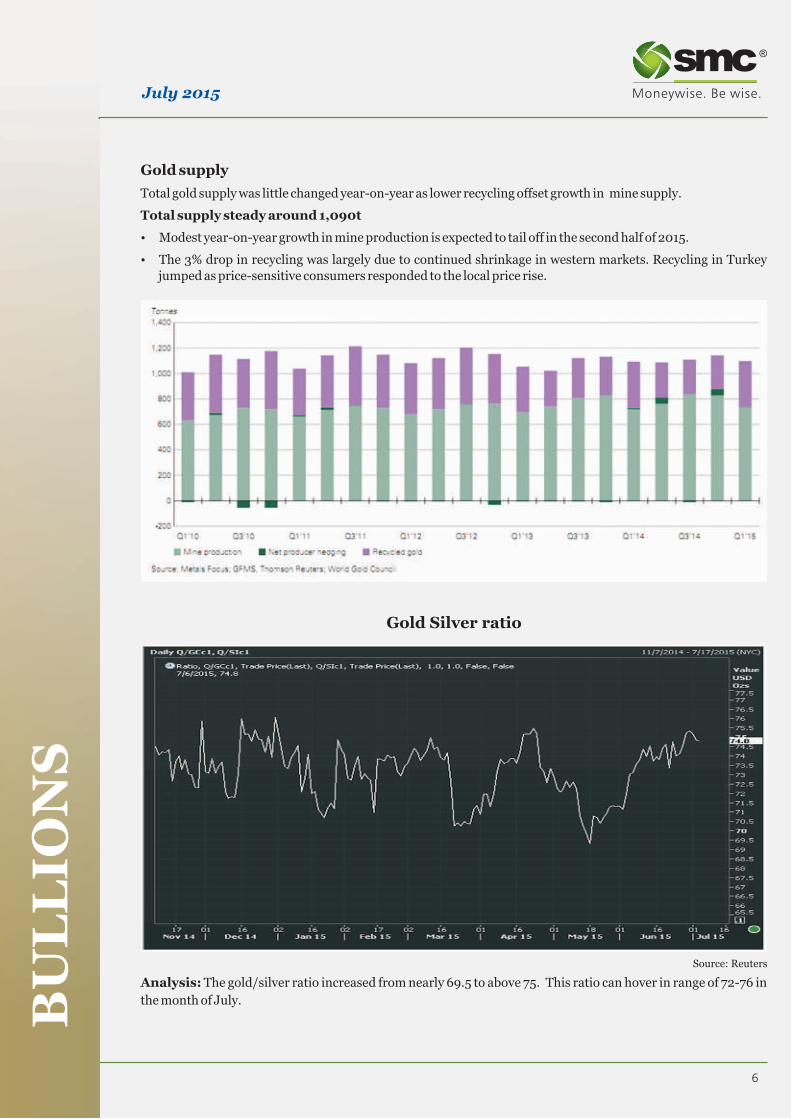

Total gold supply was little changed year-on-year as lower recycling offset growth in mine supply.

Total supply steady around 1,090t

�Modest year-on-year growth in mine production is expected to tail off in the second half of 2015.

�The 3% drop in recycling was largely due to continued shrinkage in western markets. Recycling in Turkey jumped as price-sensitive consumers responded to the local price rise.

Gold Silver ratio

Source: Reuters

Analysis: The gold/silver ratio increased from nearly 69.5 to above 75. This ratio can hover in range of 72-76 in

the month of July.

7

BU

LL

ION

SJuly 2015

Range

Gold MCX 25700-27500 Rs per 10 gms

COMEX $1130-1230 per troy ounce

Gold Hedge NCDEX Rs 23200-25000 per 10 gms

Silver MCX Rs 34000-39500 per kg

COMEX $15 -17 per ounce

Silver Hedge NCDEX Rs 31000-36000 per kg

In the month of July 2015 bullion counter

will remain on volatile path. Movement of

greenback and Greece concerns will give

further direction to the prices. Moreover

condition of global economy and movement

of local currency rupee coupled with

Physical, ETF demand will also influence its

prices.

8

BU

LL

ION

SJuly 2015

SMC Global Securities Limited is proposing, subject to receipt of requisite approvals, market conditions and other considerations, a further public offering of its equity shares and has filed the Draft Red Herring Prospectus with the Securities and Exchange Board of India (“SEBI”) and the Stock Exchanges. The Draft Red Herring Prospectus is available on the website of SEBI at www.sebi.gov.in and on the websites of the Book Running Lead Manager i.e., ICICI Securities Limited at www.icicisecurities.com and the Co- Book Running Lead Manager i.e., Elara Capital (India) Private Limited at www.elaracapital.com . Investors should note that investment in equity shares involves a high degree of risk and for details relating to the same, please see the section titled “Risk Factors” of the aforementioned offer document.

Disclaimer:

This report is for the personal information of the authorized recipient and doesn't construe to be any investment, legal or taxation advice to you. It is only for private circulation and use .The report is based upon information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied upon as such. No action is solicited on the basis of the contents of the report. The report should not be reproduced or redistributed to any other person(s)in any form without prior written permission of the SMC.

The contents of this material are general and are neither comprehensive nor inclusive. Neither SMC nor any of its affiliates, associates, representatives, directors or employees shall be responsible for any loss or damage that may arise to any person due to any action taken on the basis of this report. It does not constitute personal recommendations or take into account the particular investment objectives, financial situations or needs of an individual client or a corporate/s or any entity/s. All investments involve risk and past performance doesn't guarantee future results. The value of, and income from investments may vary because of the changes in the macro and micro factors given at a certain period of time. The person should use his/her own judgment while taking investment decisions.

Please note that we and our affiliates, officers, directors, and employees, including persons involved in the preparation or issuance if this material;(a) from time to time, may have long or short positions in, and buy or sell the commodities thereof, mentioned here in or (b) be engaged in any other transaction involving such commodities and earn brokerage or other compensation or act as a market maker in the commodities discussed herein (c) may have any other potential conflict of interest with respect to any recommendation and related information and opinions. All disputes shall be subject to the exclusive jurisdiction of Delhi High court.

Sandeep Joon Sr. Research Analyst (Metals & Energy)

Boardline : 011-30111000 Extn: 683 [email protected]