Embed Size (px)

Citation preview

Recent Developments in China’s Stock Markets

August 2015

Published by:

Ali Dagli (Partner), Okan Inaltay (Analyst), Zepeng “Frank” Wu (Intern)

2

Table of Contents

1 Recent Developments in China’s Stock Markets

2 GP Bullhound Update

3

Executive Summary on China’s Stock Market Developments

After the Global Financial Crisis of 2007-2008, China’s stock market remained stable

China’s markets are too big to ignore: as of May 2015, 3 of the world’s 6 largest stock

exchanges are Chinese (including Hong Kong as the 6th largest)

China’s markets started their dramatic rise in November 2014 and after just 7 months in June

2015, reached their highest levels since 2008

This was a $8 trillion (125%+) increase in less than 1 year and half the companies listed on

the Shanghai and Shenzhen exchanges were priced above 85x earnings

With the one month plunge in June 2015, China’s stock markets in total lost $4 trillion;

>2x the size of India’s entire stock market and >15x of total GDP in Greece

The major cause for the massive decline was the deleveraging process of the colossal

amount of margin trading

― When stock prices fell, investors who bought stocks with borrowed money had to either

increase their margin or liquidate their positions

― As investors liquidated their positions, the stock prices fell further, which prompted more

investors to liquidate their positions, resulting in an ever-accelerating downward spiral

― The deleveraging process slowed down due to a large number of company trading

suspensions and Chinese government’s actions

After unprecedented levels of Chinese government actions, China’s markets rebounded

and stabilized a bit, before crashing again on August 24 dubbed “Black Monday” – Over

80% of the stocks listed in Shanghai were down by more than 10%

China’s stock market developments should draw Western investors’ attention, as declines

on China’s exchanges negatively affected US-listed Chinese companies during the last 3

months, especially Sohu (-35%), Youku (-48%), and Sina (-23%)

The increased market volatility also poses question on whether the wave of US-listed Chinese

companies delisting in the US and relisting in China will continue

With the recent market volatility and significant decline in valuations, publicly-listed Chinese

companies that are aggressive with overseas acquisition plans will likely shift to more cash-

based acquisition strategies

Although the GDP in China continues to grow at a healthy rate (7.7% vs 5.0% in India and

2.2% in US) and the amount available for trading is still a relatively small portion of GDP

(1/3rd compared with 100%+ in western markets)…

…questions still remain on whether or not state intervention failed, how far this could go,

and how badly these recent developments damaged confidence of Chinese (85% is retail)

and foreign investors (only 2% of total) in Chinese equity markets – and more importantly

confidence in the Chinese government

Sources: Bloomberg.com, CapitalIQ, Economist.com, FactSet.com, Eastday.com, Forbes.com, FT.com, Money.cnn.com, SSE.com.cn, SZSE.cn, and WSJ.com

Notes: $ represents USD

8/24/2014 11/24/2014 2/24/2015 5/24/2015 8/24/2015

1 year period

Shanghai Composite

Margin Balance

Shenzhen Composite

Hang Seng Index

4

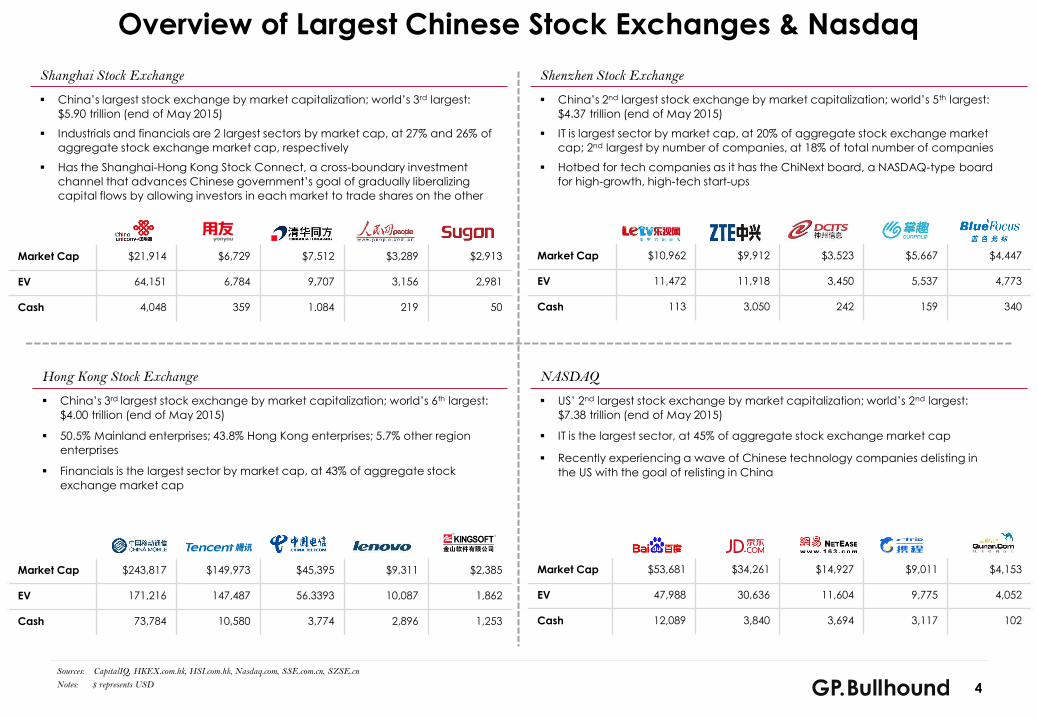

Overview of Largest Chinese Stock Exchanges & Nasdaq

Shanghai Stock Exchange

China’s largest stock exchange by market capitalization; world’s 3rd largest:

$5.90 trillion (end of May 2015)

Industrials and financials are 2 largest sectors by market cap, at 27% and 26% of

aggregate stock exchange market cap, respectively

Has the Shanghai-Hong Kong Stock Connect, a cross-boundary investment

channel that advances Chinese government’s goal of gradually liberalizing

capital flows by allowing investors in each market to trade shares on the other

Hong Kong Stock Exchange

China’s 3rd largest stock exchange by market capitalization; world’s 6th largest:

$4.00 trillion (end of May 2015)

50.5% Mainland enterprises; 43.8% Hong Kong enterprises; 5.7% other region

enterprises

Financials is the largest sector by market cap, at 43% of aggregate stock

exchange market cap

Shenzhen Stock Exchange

China’s 2nd largest stock exchange by market capitalization; world’s 5th largest:

$4.37 trillion (end of May 2015)

IT is largest sector by market cap, at 20% of aggregate stock exchange market

cap; 2nd largest by number of companies, at 18% of total number of companies

Hotbed for tech companies as it has the ChiNext board, a NASDAQ-type board

for high-growth, high-tech start-ups

NASDAQ

US’ 2nd largest stock exchange by market capitalization; world’s 2nd largest:

$7.38 trillion (end of May 2015)

IT is the largest sector, at 45% of aggregate stock exchange market cap

Recently experiencing a wave of Chinese technology companies delisting in

the US with the goal of relisting in China

Market Cap $21,914 $6,729 $7,512 $3,289 $2,913

EV 64,151 6,784 9,707 3,156 2,981

Cash 4,048 359 1.084 219 50

Market Cap $10,962 $9,912 $3,523 $5,667 $4,447

EV 11,472 11,918 3,450 5,537 4,773

Cash 113 3,050 242 159 340

Market Cap $243,817 $149,973 $45,395 $9,311 $2,385

EV 171,216 147,487 56.3393 10,087 1,862

Cash 73,784 10,580 3,774 2,896 1,253

Market Cap $53,681 $34,261 $14,927 $9,011 $4,153

EV 47,988 30,636 11,604 9,775 4,052

Cash 12,089 3,840 3,694 3,117 102

Sources: CapitalIQ, HKEX.com.hk, HSI.com.hk, Nasdaq.com, SSE.com.cn, SZSE.cn

Notes: $ represents USD

5

¥1,500

¥2,000

¥2,500

¥3,000

¥3,500

¥4,000

¥4,500

¥5,000

¥5,500

Overview of the Recent Developments in China’s Stock Market Frequent rates cuts: since November 2014, People's Bank of China has been cutting

interest rate and reserve requirement ratios and at shorter intervals

Huge increase in retail/small-time day traders: reaches 90m retail accounts; 2/3 of

new Chinese investors in 2014 did not complete high school

Leverage has soared: outstanding loans to stock investors reached a record 1.67

trillion yuan ($269Bn) as of April 13, 2015, up 300% from a year earlier

Stock transaction volume in China surged: turnover on China’s stock exchanges

surged past the US in May 2015 to a record $380Bn

Trading at increasingly higher multiples: ChiNext, China’s small-cap board, had a PE

ratio of 90, 2x that of internet stocks at peak of America’s dotcom bubble in 2000

Government-induced optimism: financial reforms supported share prices and

government strategy of “Entrepreneurship Across Country” backed high

expectations of high-growth tech companies

Huge surge in buying on margin: due to doubling in price; Loans to investors rose

300% in a year

Many stocks bought on debt: the unwinding of these massive loans helps explain

why the government has been unable to stop the rout

Retail investors’ panic was also a major factor to market plunge: China’s markets

are dominated by retail investors as 85% of all trades are retail

Foreign speculation was likely not the cause of this plunge as less than 2% of

Chinese shares are owned by foreigners

Over 50% of all Chinese stocks have suspended from trading

Chinese stocks tumbled even as actual GDP growth (7% YoY in Q2 2015) surpassed

Beijing’s expectation; possibility that China’s stock prices are in part disconnected

from economic fundamentals

Unprecedented government actions—trading and IPO suspensions, loose credit

policies, and stimulus packages—boosted the market

More weak economic data on China’s economy triggered shares in mainland

China to record increasing losses across its four major stock exchanges

The lack of confidence in government measures and the worry of government

withdrawal of these support began causing more volatility

Government support begins to show signs of working: stock markets show signs of

stabilization

Securities Regulatory Commission begins investigating “malicious” short sellers – it

began demanding trading records from brokerage houses

Chinese government plans to pump new liquidity into market: cash infusion is to

offset its initial move in devaluing tightly controlled Yuan currency

Chinese stock market continues to severely decline, recording largest 1-day loss

since February 2007 (8.7%); Global markets across Asia, Europe, and US are sent into

a tailspin amidst uncertainty

1

2

3

4

5

Sources: Bloomberg.com, CapitalIQ, Economist.com, Forbes.com, FT.com, Money.cnn.com, SSE.com.cn, SZSE.cn, and WSJ.com

Notes: Blue line represents Shanghai Stock Exchange Composite Index; rise and fall figures represents the total market valuation of the Shanghai, Shenzhen, and Hong Kong Stock exchanges

$ represents USD

6

Fall of $4 trillion

in less than a month;

global markets are not

negatively affected

Largest 1-day

rise since March

2009

3

Market selloff

continues

4

5Market

seems

to have

stabilized

6

Largest 1-day fall

since Feb 2007;

Global markets

negatively

affected

6

$20,000

$21,000

$22,000

$23,000

$24,000

$25,000

$26,000

$27,000

$28,000

$29,000

$30,000

10

¥500

¥1,000

¥1,500

¥2,000

¥2,500

¥3,000

¥3,500

¥1,500

¥2,000

¥2,500

¥3,000

¥3,500

¥4,000

¥4,500

¥5,000

¥5,500

$4,000

$4,200

$4,400

$4,600

$4,800

$5,000

$5,200

$5,400

Nasdaq Composite Index

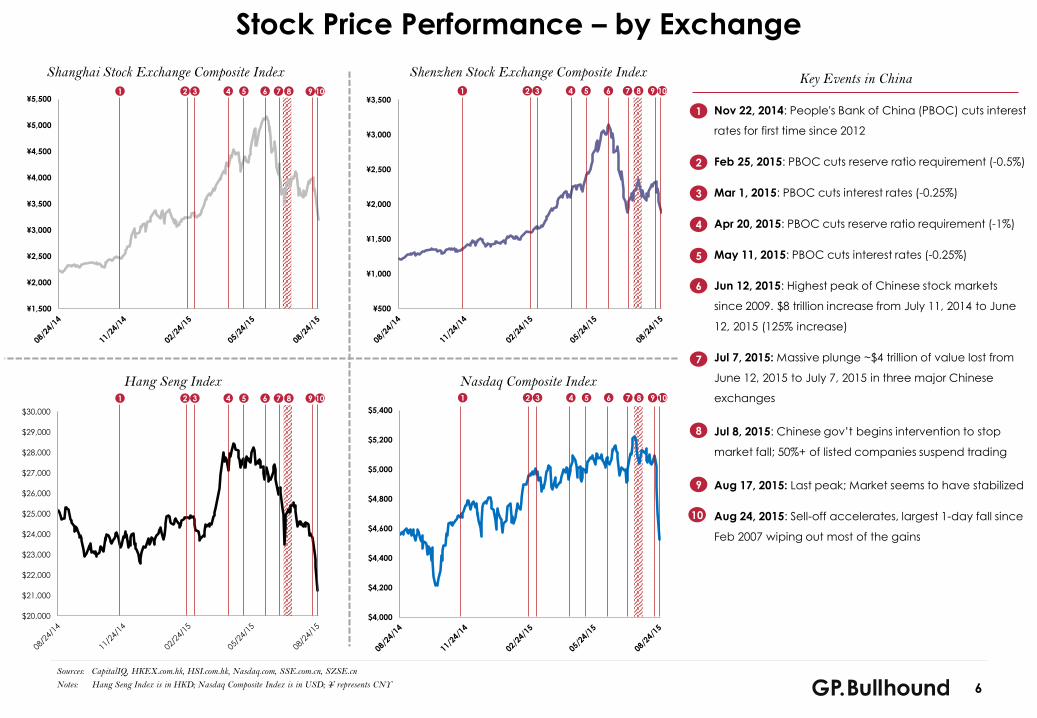

Stock Price Performance – by Exchange

Shenzhen Stock Exchange Composite Index Key Events in ChinaShanghai Stock Exchange Composite Index

Hang Seng Index

Nov 22, 2014: People's Bank of China (PBOC) cuts interest

rates for first time since 2012

Feb 25, 2015: PBOC cuts reserve ratio requirement (-0.5%)

Mar 1, 2015: PBOC cuts interest rates (-0.25%)

Apr 20, 2015: PBOC cuts reserve ratio requirement (-1%)

May 11, 2015: PBOC cuts interest rates (-0.25%)

Jun 12, 2015: Highest peak of Chinese stock markets

since 2009. $8 trillion increase from July 11, 2014 to June

12, 2015 (125% increase)

Jul 7, 2015: Massive plunge ~$4 trillion of value lost from

June 12, 2015 to July 7, 2015 in three major Chinese

exchanges

Jul 8, 2015: Chinese gov’t begins intervention to stop

market fall; 50%+ of listed companies suspend trading

Aug 17, 2015: Last peak; Market seems to have stabilized

Aug 24, 2015: Sell-off accelerates, largest 1-day fall since

Feb 2007 wiping out most of the gains

Sources: CapitalIQ, HKEX.com.hk, HSI.com.hk, Nasdaq.com, SSE.com.cn, SZSE.cn

Notes: Hang Seng Index is in HKD; Nasdaq Composite Index is in USD; ¥ represents CNY

1

2

3

4

5

6

7

8

2 3 4 5 6 7 81

9

10

9 10 2 3 4 5 6 7 81 9

2 3 4 5 6 7 81 9 10 2 3 4 5 6 7 81 109

7

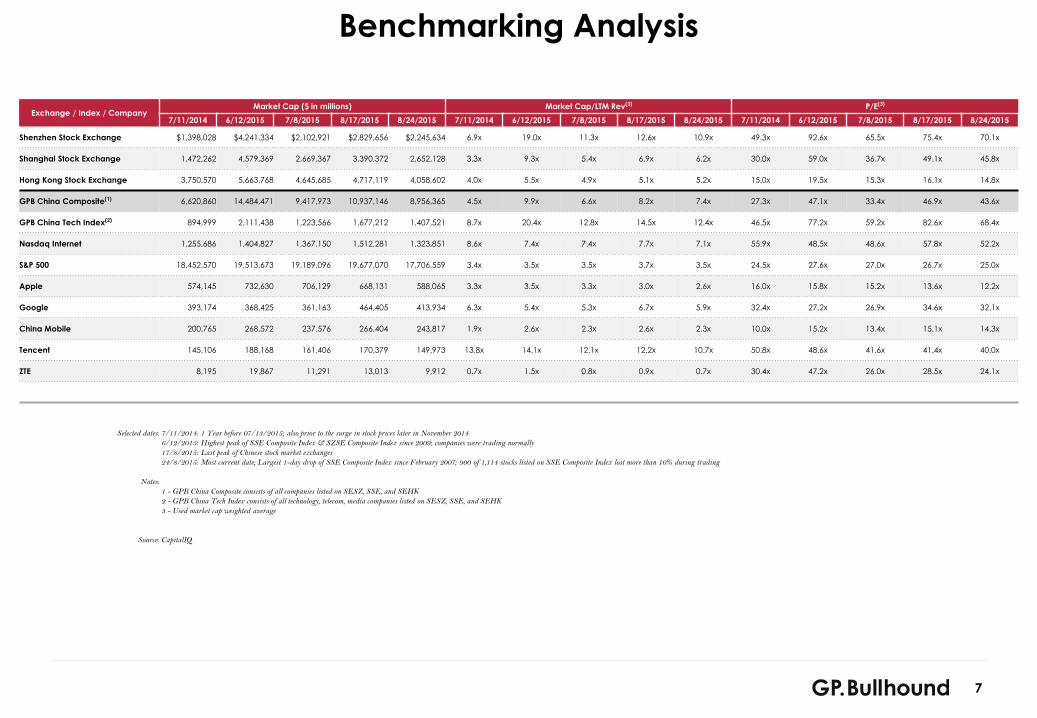

Benchmarking Analysis

Exchange / Index / CompanyMarket Cap ($ in millions) Market Cap/LTM Rev(3) P/E(3)

7/11/2014 6/12/2015 7/8/2015 8/17/2015 8/24/2015 7/11/2014 6/12/2015 7/8/2015 8/17/2015 8/24/2015 7/11/2014 6/12/2015 7/8/2015 8/17/2015 8/24/2015

Shenzhen Stock Exchange $1,398,028 $4,241,334 $2,102,921 $2,829,656 $2,245,634 6.9x 19.0x 11.3x 12.6x 10.9x 49.3x 92.6x 65.5x 75.4x 70.1x

Shanghai Stock Exchange 1,472,262 4,579,369 2,669,367 3,390,372 2,652,128 3.3x 9.3x 5.4x 6.9x 6.2x 30.0x 59.0x 36.7x 49.1x 45.8x

Hong Kong Stock Exchange 3,750,570 5,663,768 4,645,685 4,717,119 4,058,602 4.0x 5.5x 4.9x 5.1x 5.2x 15.0x 19.5x 15.3x 16.1x 14.8x

GPB China Composite(1) 6,620,860 14,484,471 9,417,973 10,937,146 8,956,365 4.5x 9.9x 6.6x 8.2x 7.4x 27.3x 47.1x 33.4x 46.9x 43.6x

GPB China Tech Index(2) 894,999 2,111,438 1,223,566 1,677,212 1,407,521 8.7x 20.4x 12.8x 14.5x 12.4x 46.5x 77.2x 59.2x 82.6x 68.4x

Nasdaq Internet 1,255,686 1,404,827 1,367,150 1,512,281 1,323,851 8.6x 7.4x 7.4x 7.7x 7.1x 55.9x 48.5x 48.6x 57.8x 52.2x

S&P 500 18,452,570 19,513,673 19,189,096 19,677,070 17,706,559 3.4x 3.5x 3.5x 3.7x 3.5x 24.5x 27.6x 27.0x 26.7x 25.0x

Apple 574,145 732,630 706,129 668,131 588,065 3.3x 3.5x 3.3x 3.0x 2.6x 16.0x 15.8x 15.2x 13.6x 12.2x

Google 393,174 368,425 361,163 464,405 413,934 6.3x 5.4x 5.3x 6.7x 5.9x 32.4x 27.2x 26.9x 34.6x 32.1x

China Mobile 200,765 268,572 237,576 266,404 243,817 1.9x 2.6x 2.3x 2.6x 2.3x 10.0x 15.2x 13.4x 15.1x 14.3x

Tencent 145,106 188,168 161,406 170,379 149,973 13.8x 14.1x 12.1x 12.2x 10.7x 50.8x 48.6x 41.6x 41.4x 40.0x

ZTE 8,195 19,867 11,291 13,013 9,912 0.7x 1.5x 0.8x 0.9x 0.7x 30.4x 47.2x 26.0x 28.5x 24.1x

Selected dates: 7/11/2014: 1 Year before 07/13/2015; also prior to the surge in stock prices later in November 2014

6/12/2015: Highest peak of SSE Composite Index & SZSE Composite Index since 2009; companies were trading normally

17/8/2015: Last peak of Chinese stock market exchanges

24/8/2015: Most current date; Largest 1-day drop of SSE Composite Index since February 2007; 900 of 1,114 stocks listed on SSE Composite Index lost more than 10% during trading

Notes:

1 - GPB China Composite consists of all companies listed on SESZ, SSE, and SEHK

2 - GPB China Tech Index consists of all technology, telecom, media companies listed on SESZ, SSE, and SEHK

3 - Used market cap weighted average

Source: CapitalIQ

8

¥3,000

¥3,500

¥4,000

¥4,500

¥5,000

¥5,500

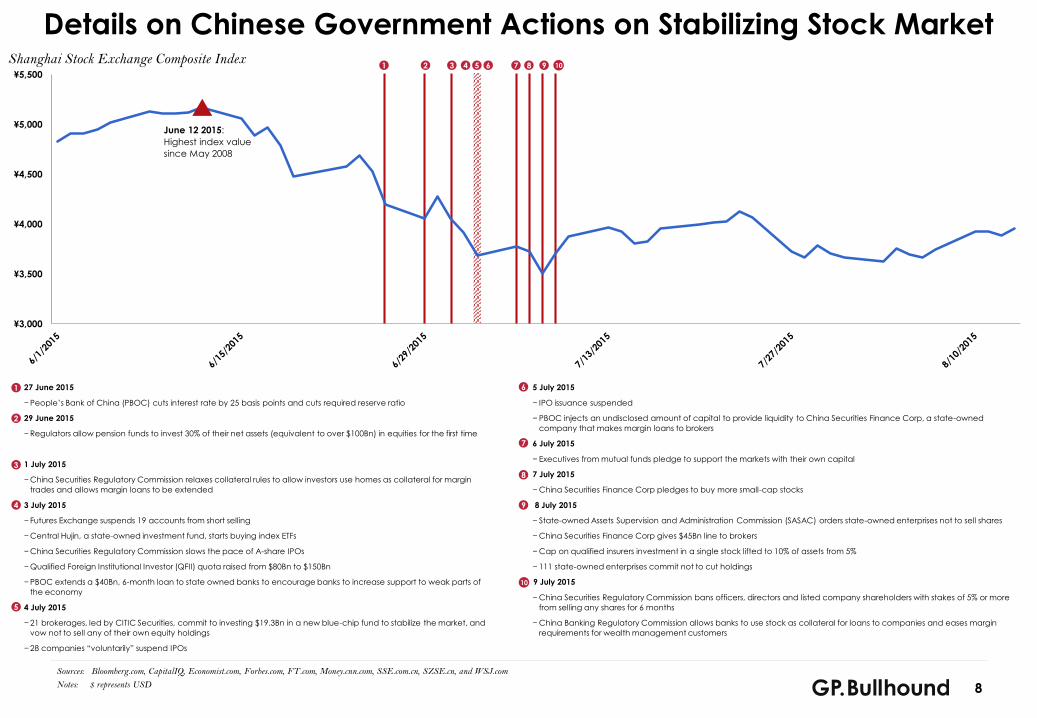

27 June 2015

− People’s Bank of China (PBOC) cuts interest rate by 25 basis points and cuts required reserve ratio

29 June 2015

− Regulators allow pension funds to invest 30% of their net assets (equivalent to over $100Bn) in equities for the first time

1 July 2015

− China Securities Regulatory Commission relaxes collateral rules to allow investors use homes as collateral for margin

trades and allows margin loans to be extended

3 July 2015

− Futures Exchange suspends 19 accounts from short selling

− Central Hujin, a state-owned investment fund, starts buying index ETFs

− China Securities Regulatory Commission slows the pace of A-share IPOs

− Qualified Foreign Institutional Investor (QFII) quota raised from $80Bn to $150Bn

− PBOC extends a $40Bn, 6-month loan to state owned banks to encourage banks to increase support to weak parts of

the economy

4 July 2015

− 21 brokerages, led by CITIC Securities, commit to investing $19.3Bn in a new blue-chip fund to stabilize the market, and

vow not to sell any of their own equity holdings

− 28 companies “voluntarily” suspend IPOs

5 July 2015

− IPO issuance suspended

− PBOC injects an undisclosed amount of capital to provide liquidity to China Securities Finance Corp, a state-owned

company that makes margin loans to brokers

6 July 2015

− Executives from mutual funds pledge to support the markets with their own capital

7 July 2015

− China Securities Finance Corp pledges to buy more small-cap stocks

8 July 2015

− State-owned Assets Supervision and Administration Commission (SASAC) orders state-owned enterprises not to sell shares

− China Securities Finance Corp gives $45Bn line to brokers

− Cap on qualified insurers investment in a single stock lifted to 10% of assets from 5%

− 111 state-owned enterprises commit not to cut holdings

9 July 2015

− China Securities Regulatory Commission bans officers, directors and listed company shareholders with stakes of 5% or more

from selling any shares for 6 months

− China Banking Regulatory Commission allows banks to use stock as collateral for loans to companies and eases margin

requirements for wealth management customers

Details on Chinese Government Actions on Stabilizing Stock Market9876521 43 10

Shanghai Stock Exchange Composite Index

1

2

3

4

5

6

7

8

9

10

Sources: Bloomberg.com, CapitalIQ, Economist.com, Forbes.com, FT.com, Money.cnn.com, SSE.com.cn, SZSE.cn, and WSJ.com

Notes: $ represents USD

June 12 2015:

Highest index value

since May 2008

9

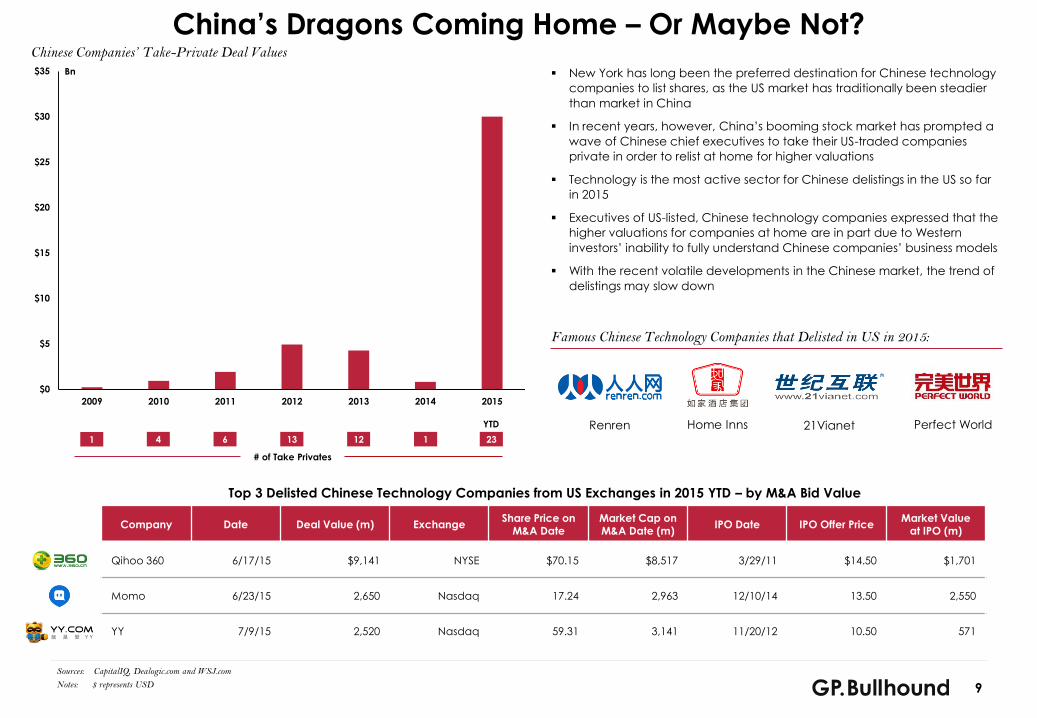

China’s Dragons Coming Home – Or Maybe Not?

Bn New York has long been the preferred destination for Chinese technology

companies to list shares, as the US market has traditionally been steadier

than market in China

In recent years, however, China’s booming stock market has prompted a

wave of Chinese chief executives to take their US-traded companies

private in order to relist at home for higher valuations

Technology is the most active sector for Chinese delistings in the US so far

in 2015

Executives of US-listed, Chinese technology companies expressed that the

higher valuations for companies at home are in part due to Western

investors’ inability to fully understand Chinese companies’ business models

With the recent volatile developments in the Chinese market, the trend of

delistings may slow down

Famous Chinese Technology Companies that Delisted in US in 2015:

Chinese Companies’ Take-Private Deal Values

Company Date Deal Value (m) ExchangeShare Price on

M&A DateMarket Cap on M&A Date (m)

IPO Date IPO Offer Price Market Value

at IPO (m)

Qihoo 360 6/17/15 $9,141 NYSE $70.15 $8,517 3/29/11 $14.50 $1,701

Momo 6/23/15 2,650 Nasdaq 17.24 2,963 12/10/14 13.50 2,550

YY 7/9/15 2,520 Nasdaq 59.31 3,141 11/20/12 10.50 571

$0

$5

$10

$15

$20

$25

$30

$35

2009 2010 2011 2012 2013 2014 2015

1 4 6 23113 12

YTD

# of Take Privates

Top 3 Delisted Chinese Technology Companies from US Exchanges in 2015 YTD – by M&A Bid Value

Renren Home Inns 21Vianet Perfect World

Sources: CapitalIQ, Dealogic.com and WSJ.com

Notes: $ represents USD

10

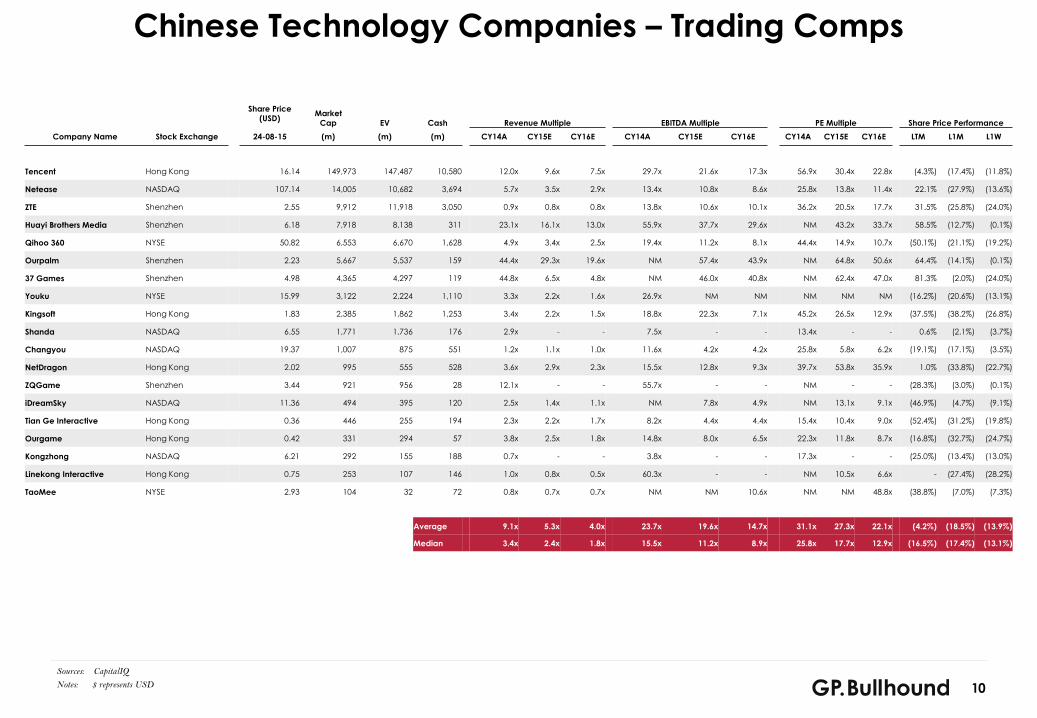

Chinese Technology Companies – Trading Comps

Sources: CapitalIQ

Notes: $ represents USD

Share Price

(USD)Market

Cap EV Cash Revenue Multiple EBITDA Multiple PE Multiple Share Price Performance

Company Name Stock Exchange 24-08-15 (m) (m) (m) CY14A CY15E CY16E CY14A CY15E CY16E CY14A CY15E CY16E LTM L1M L1W

Tencent Hong Kong 16.14 149,973 147,487 10,580 12.0x 9.6x 7.5x 29.7x 21.6x 17.3x 56.9x 30.4x 22.8x (4.3%) (17.4%) (11.8%)

Netease NASDAQ 107.14 14,005 10,682 3,694 5.7x 3.5x 2.9x 13.4x 10.8x 8.6x 25.8x 13.8x 11.4x 22.1% (27.9%) (13.6%)

ZTE Shenzhen 2.55 9,912 11,918 3,050 0.9x 0.8x 0.8x 13.8x 10.6x 10.1x 36.2x 20.5x 17.7x 31.5% (25.8%) (24.0%)

Huayi Brothers Media Shenzhen 6.18 7,918 8,138 311 23.1x 16.1x 13.0x 55.9x 37.7x 29.6x NM 43.2x 33.7x 58.5% (12.7%) (0.1%)

Qihoo 360 NYSE 50.82 6,553 6,670 1,628 4.9x 3.4x 2.5x 19.4x 11.2x 8.1x 44.4x 14.9x 10.7x (50.1%) (21.1%) (19.2%)

Ourpalm Shenzhen 2.23 5,667 5,537 159 44.4x 29.3x 19.6x NM 57.4x 43.9x NM 64.8x 50.6x 64.4% (14.1%) (0.1%)

37 Games Shenzhen 4.98 4,365 4,297 119 44.8x 6.5x 4.8x NM 46.0x 40.8x NM 62.4x 47.0x 81.3% (2.0%) (24.0%)

Youku NYSE 15.99 3,122 2,224 1,110 3.3x 2.2x 1.6x 26.9x NM NM NM NM NM (16.2%) (20.6%) (13.1%)

Kingsoft Hong Kong 1.83 2,385 1,862 1,253 3.4x 2.2x 1.5x 18.8x 22.3x 7.1x 45.2x 26.5x 12.9x (37.5%) (38.2%) (26.8%)

Shanda NASDAQ 6.55 1,771 1,736 176 2.9x - - 7.5x - - 13.4x - - 0.6% (2.1%) (3.7%)

Changyou NASDAQ 19.37 1,007 875 551 1.2x 1.1x 1.0x 11.6x 4.2x 4.2x 25.8x 5.8x 6.2x (19.1%) (17.1%) (3.5%)

NetDragon Hong Kong 2.02 995 555 528 3.6x 2.9x 2.3x 15.5x 12.8x 9.3x 39.7x 53.8x 35.9x 1.0% (33.8%) (22.7%)

ZQGame Shenzhen 3.44 921 956 28 12.1x - - 55.7x - - NM - - (28.3%) (3.0%) (0.1%)

iDreamSky NASDAQ 11.36 494 395 120 2.5x 1.4x 1.1x NM 7.8x 4.9x NM 13.1x 9.1x (46.9%) (4.7%) (9.1%)

Tian Ge Interactive Hong Kong 0.36 446 255 194 2.3x 2.2x 1.7x 8.2x 4.4x 4.4x 15.4x 10.4x 9.0x (52.4%) (31.2%) (19.8%)

Ourgame Hong Kong 0.42 331 294 57 3.8x 2.5x 1.8x 14.8x 8.0x 6.5x 22.3x 11.8x 8.7x (16.8%) (32.7%) (24.7%)

Kongzhong NASDAQ 6.21 292 155 188 0.7x - - 3.8x - - 17.3x - - (25.0%) (13.4%) (13.0%)

Linekong Interactive Hong Kong 0.75 253 107 146 1.0x 0.8x 0.5x 60.3x - - NM 10.5x 6.6x - (27.4%) (28.2%)

TaoMee NYSE 2.93 104 32 72 0.8x 0.7x 0.7x NM NM 10.6x NM NM 48.8x (38.8%) (7.0%) (7.3%)

Average 9.1x 5.3x 4.0x 23.7x 19.6x 14.7x 31.1x 27.3x 22.1x (4.2%) (18.5%) (13.9%)

Median 3.4x 2.4x 1.8x 15.5x 11.2x 8.9x 25.8x 17.7x 12.9x (16.5%) (17.4%) (13.1%)

11

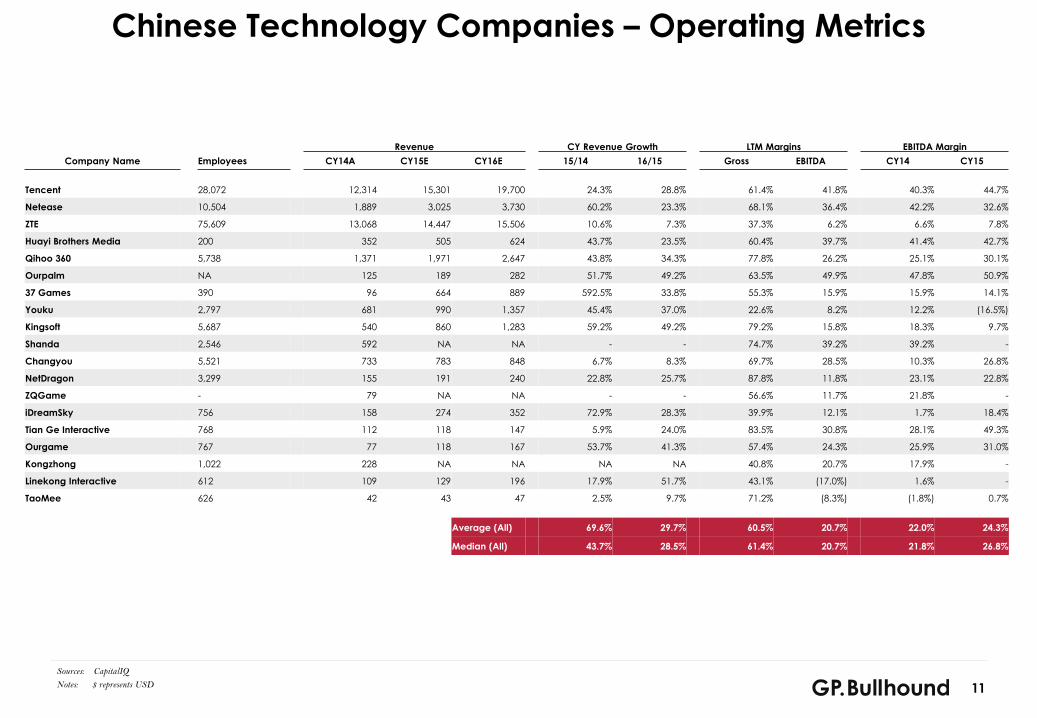

Chinese Technology Companies – Operating Metrics

Sources: CapitalIQ

Notes: $ represents USD

Revenue CY Revenue Growth LTM Margins EBITDA Margin

Company Name Employees CY14A CY15E CY16E 15/14 16/15 Gross EBITDA CY14 CY15

Tencent 28,072 12,314 15,301 19,700 24.3% 28.8% 61.4% 41.8% 40.3% 44.7%

Netease 10,504 1,889 3,025 3,730 60.2% 23.3% 68.1% 36.4% 42.2% 32.6%

ZTE 75,609 13,068 14,447 15,506 10.6% 7.3% 37.3% 6.2% 6.6% 7.8%

Huayi Brothers Media 200 352 505 624 43.7% 23.5% 60.4% 39.7% 41.4% 42.7%

Qihoo 360 5,738 1,371 1,971 2,647 43.8% 34.3% 77.8% 26.2% 25.1% 30.1%

Ourpalm NA 125 189 282 51.7% 49.2% 63.5% 49.9% 47.8% 50.9%

37 Games 390 96 664 889 592.5% 33.8% 55.3% 15.9% 15.9% 14.1%

Youku 2,797 681 990 1,357 45.4% 37.0% 22.6% 8.2% 12.2% (16.5%)

Kingsoft 5,687 540 860 1,283 59.2% 49.2% 79.2% 15.8% 18.3% 9.7%

Shanda 2,546 592 NA NA - - 74.7% 39.2% 39.2% -

Changyou 5,521 733 783 848 6.7% 8.3% 69.7% 28.5% 10.3% 26.8%

NetDragon 3,299 155 191 240 22.8% 25.7% 87.8% 11.8% 23.1% 22.8%

ZQGame - 79 NA NA - - 56.6% 11.7% 21.8% -

iDreamSky 756 158 274 352 72.9% 28.3% 39.9% 12.1% 1.7% 18.4%

Tian Ge Interactive 768 112 118 147 5.9% 24.0% 83.5% 30.8% 28.1% 49.3%

Ourgame 767 77 118 167 53.7% 41.3% 57.4% 24.3% 25.9% 31.0%

Kongzhong 1,022 228 NA NA NA NA 40.8% 20.7% 17.9% -

Linekong Interactive 612 109 129 196 17.9% 51.7% 43.1% (17.0%) 1.6% -

TaoMee 626 42 43 47 2.5% 9.7% 71.2% (8.3%) (1.8%) 0.7%

Average (All) 69.6% 29.7% 60.5% 20.7% 22.0% 24.3%

Median (All) 43.7% 28.5% 61.4% 20.7% 21.8% 26.8%

12

Table of Contents

1 Recent Developments in China’s Stock Markets

2 GP Bullhound Update

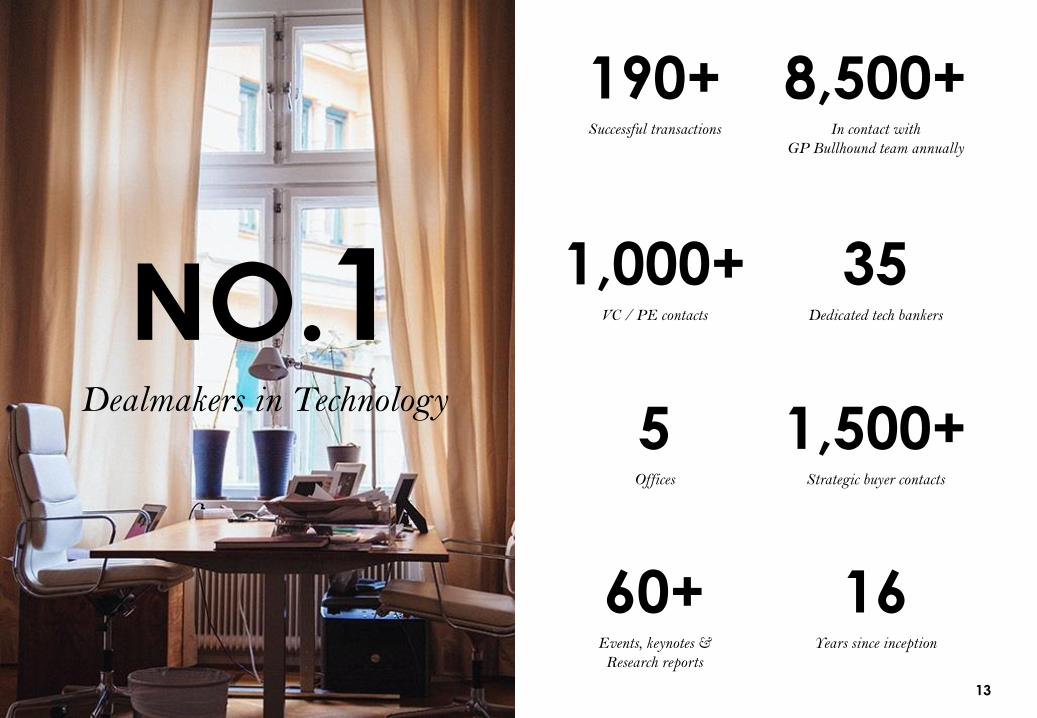

NO.1

190+Successful transactions

8,500+In contact with

GP Bullhound team annually

1,000+VC / PE contacts

35Dedicated tech bankers

5Offices

1,500+Strategic buyer contacts

60+Events, keynotes &

Research reports

16Years since inception

Dealmakers in Technology

13

Our team

HUGH CAMPBELLManaging Partner

MANISH MADHVANIManaging Partner

PER ROMANManaging Partner

SIR MARTIN SMITHChairman

GRAEME BAYLEYPartner & Group CFO

GUILLAUME BONNETONPartner

ALEC DAFFERNERPartner

SIMON NICHOLLSPartner

JULIAN RIEDLBAUERPartner

CLAUDIO ALVAREZDirector

ALI DAGLIPartner

ALEXIS SCORER

Director

ALESSANDRO CASARTELLI

Vice President

PER LINDTORPDirector

ADAM RUDD

Vice President

CARL WESSBERG

Director

RAVI GHEDIAMALCOM HORNER

Vice President

CHRIS PARK

Associate

OLOF RUSTNER

Associate

LORD CLIVE HOLLICK

Senior Advisor

CHRISTIAN LAGERLING

Co-founder &

Senior Advisor

MATT ROGERS

Senior Advisor

CECILIA ROMAN

Senior Advisor

ANDRE SHORTELLPartner

IMAN CRISBY

Business Development Manager

HARRI NEEDHAM

Finance Manager

DAVE NISH

Technology Manager

MATTHEW FINEGOLD

Analyst

OKAN INALTAY

Analyst

MARVIN MAERZ

Analyst Analyst

HARRIET ROSETHORN

CHRIS GRAVESDirector

Vice President

SEBASTIAN MARKOWSKY

ROBERT AHLDINPartner

JOAKIM DAL

Vice President

JOSHUA BURGE

Analyst

MARK SEBBANon-Executive Director

MATHIAS ACKERMANDNon-Executive Director

Associate

ANN GREVELIUSPartner

JOHANNES ÅKERMARK

Associate

ORIANE MILLET

Analyst

Associate

LENKA KOLAROVA

KARL BLOMSTERWALL

Analyst

LUKE BURNS

Analyst

14

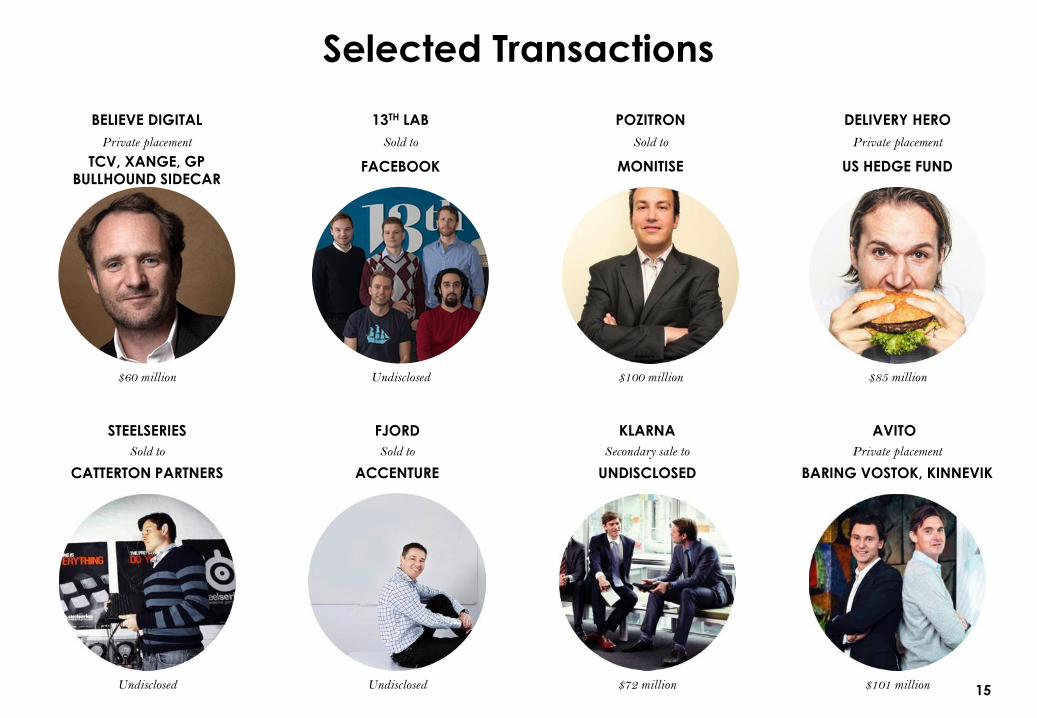

Selected Transactions

STEELSERIES

CATTERTON PARTNERS

Sold to

DELIVERY HERO

US HEDGE FUND

Private placement

BELIEVE DIGITAL

TCV, XANGE, GP BULLHOUND SIDECAR

Private placement

POZITRON

MONITISE

Sold to

Undisclosed

$85 million$60 million $100 million

FJORD

ACCENTURE

Sold to

KLARNA

UNDISCLOSED

Secondary sale to

AVITO

Private placement

Undisclosed $72 million

BARING VOSTOK, KINNEVIK

$101 million

13TH LAB

Sold to

Undisclosed

15

BERLINLONDON MANCHESTERSAN

FRANCISCOSTOCKHOLM

Events &Speaking

Offices

Awards

Latestreports

• GP Bullhound Summit

• Investor Allstars

• Northern Tech Awards

• Extreme Tech Challenge

• Red Herring

• White Bull

• World Internet Conference

• Cebit

• CNN

• CNBC

• BBC

• SIME

THE FUTURE OF ONLINE AND

MOBILE PAYMENTS

THE NEW MOBILE APP

REALITY

CAN EUROPE CREATE BILLION DOLLAR

TECH COMPANIES?

REAL TIME BIDDING IN ONLINE

ADVERTISING

• THE BULLY AWARDS2014 M&A Firm of the year

• THE M&A ADVISOR2013 Dealmaker of the year 40 under 40 award

• A.I. M&A AWARDS2013 Boutique investment bank of the year, UK & Leading adviser of the year

• THE M&A ATLAS AWARDS2010 M&A Boutique Investment Bank of the Year & Green Energy Deal of the Year

2010 Deal of the year & runner-up deal of the year

2010 Corporate finance boutique of the year

• ROSENBLATT SOLICITORS • THE M&A AWARDS

• THE M&A ADVISOR2014 Financial Services Deal of the Year

• INSIDER MEDIA2014 North West 42 under 42

16

TOP TECHNOLOGY PREDICTIONS

2015

• THE M&A ATLAS AWARDS2015 M&A Boutique Investment Bank of the Year & Deal of the Year Small Markets

• ALTERNATIVE INVESTMENT AWARDSBest Technology Focused Investment Banking Firm 2015

EUROPEAN UNICORNS – DO

THEY HAVE LEGS?

LONDON SAN FRANCISCO STOCKHOLM BERLIN MANCHESTERtel. +44 207 101 7560

52 Jermyn Street

London, SW1Y 6LX

United Kingdom

tel. +1 415 986 0191

One Maritime Plaza Suite 1620

San Francisco, CA 94111

USA

tel. +46 8 545 074 14

Birger Jarlsgatan 5

Stockholm, 111 45

Sweden

tel. +49 30 610 80 600

Oberwallstrasse 20

Berlin, 101 17

Germany

tel. +44 161 413 5030

1 New York Street

Manchester, M1 4HD

United Kingdom

The contents of this presentation document ("Presentation") shall not be deemed to be any form of offer or binding commitment on the part of GP

Bullhound LLP. This Presentation is provided for use by the intended recipient for information purposes only. It is prepared on the basis that the

recipients are sophisticated investors with a high degree of financial sophistication and knowledge. No representation or warranty, express or implied, is

or will be made in respect of the information contained in this Presentation and no responsibility or liability is or will be accepted by GP Bullhound LLP

in this regard. In particular, but without prejudice to the generality of the foregoing, no representation or warranty is given as to the accuracy,

completeness or reasonableness of any projections, targets, estimates or forecasts contained in this Presentation or in such other written or oral

information that may be provided by GP Bullhound LLP. All liability is expressly excluded to the fullest extent permitted by law. This Presentation may

contain forward-looking statements, which involve risks and uncertainties. Actual results may differ significantly from the results described in such

forward-looking statements. Any past performance information contained in this Presentation is provided for illustrative purposes only and is not

necessarily a guide to future performance and the value of securities may fall as well as rise. In particular, investments in the technology sector can

involve a high degree of risk and investors may not get back the full amount invested. This Presentation should not be construed in any circumstances as

a solicitation or offer, or recommendation, to acquire or dispose of any investment or to engage in any other transaction, or to provide any investment

advice or service and you should not act or refrain from acting upon any information contained on it without seeking appropriate professional advice. In

the event that you should wish to engage GP Bullhound LLP, separate documentation, including an engagement letter, will be provided to you. For the

purposes of the rules and guidance issued by the Financial Conduct Authority ("the FCA"), this Presentation has been communicated by GP Bullhound

LLP, which is authorised and regulated by the FCA in the United Kingdom under number 527314.

This Presentation is only directed at persons who fall within the category of “Professional Clients” as defined in the rules and guidance issued by the FCA

from time to time and any investment or investment activity to which this Presentation relates is available only to such persons and will be engaged in

only with such persons. The information contained in this Presentation must not be relied upon by persons who are not Professional Clients and any

person who is not a Professional Client should return it immediately to GP Bullhound LLP at the address below. This Presentation and any other

information or opinions supplied or given to you by GP Bullhound LLP constitute confidential information. Neither the whole nor any part of the

information contained in this Presentation may be duplicated in any form or by any means. Neither should the information contained in this Presentation,

or any part thereof, be redistributed or disclosed to anyone without the prior written consent of GP Bullhound LLP. GP Bullhound LLP is a limited

liability partnership registered in England and Wales, registered number OC352636, and is authorised and regulated by the FCA. Any reference to a

partner in relation to GP Bullhound LLP is to a member of GP Bullhound LLP or an employee with equivalent standing and qualifications. A list of the

members of GP Bullhound LLP is available for inspection at its registered office: 52 Jermyn Street, London SW1Y 6LX.

For US Persons: This presentation report is distributed to U.S. persons by GP Bullhound Inc. a broker-dealer registered with the SEC and a member of

the FINRA. GP Bullhound Inc. is an affiliate of GP Bullhound LLP. This presentation does not provide personalized advice or recommendations of any

kind. All investments bear certain material risks that should be considered in consultation with an investors financial, legal and tax advisors. Ali Dagli

and Okan Inaltay are employees and Frank Wu is a summer intern of GP Bullhound Inc. that engages in private placement and mergers and acquisitions

advisory activities with clients and counterparties in the Technology sectors.

![[Master Class Programmatic Trading May 2014] Keynote by Simon Nicholls Partner at GP Bullhound](https://img.pdfslide.us/doc/110x75/558e21031a28ab93398b4673/master-class-programmatic-trading-may-2014-keynote-by-simon-nicholls-partner-at-gp-bullhound.jpg)