Embed Size (px)

Citation preview

Valeant

Pharmaceuticals

International, Inc.

First Quarter 2015

Financial Results Conference Call

April 29, 2015

1

Forward-looking Statements Forward-looking Statements Certain statements made in this presentation may constitute forward-looking statements, including, but not limited to, statements regarding the

expected integration of the Dendreon and Salix businesses, the amount and timing of expected synergies, expected future performance, including

2015 guidance with respect to revenue, Cash EPS, organic growth, our inventory reduction program, and our outlook with respect to performance in

2016, expectations with respect to gross margins, marketing efforts, debt reduction, and restructuring expenses, the timing of and outcome of

regulatory approvals and commercial plans with respect to product candidates. Forward-looking statements may generally be identified by the use

of the words “anticipates,” “expects,” “intends,” “plans,” “should,” “could,” “would,” “may,” “will,” “believes,” “estimates,” “potential,” “target,” or

“continue” and variations or similar expressions. These statements are based upon the current expectations and beliefs of management and are

subject to certain risks and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements.

These risks and uncertainties include, but are not limited to, risks and uncertainties discussed in the Company's most recent annual or quarterly

report and detailed from time to time in Valeant’s other filings with the Securities and Exchange Commission and the Canadian Securities

Administrators, which factors are incorporated herein by reference. Readers are cautioned not to place undue reliance on any of these forward-

looking statements. These forward-looking statements speak only as of the date hereof. Valeant undertakes no obligation to update any of these

forward-looking statements to reflect events or circumstances after the date of this presentation or to reflect actual outcomes. Non-GAAP Information To supplement the financial measures prepared in accordance with generally accepted accounting principles (GAAP), the Company uses non-GAAP financial measures that exclude certain items. Management uses non-GAAP financial measures internally for strategic decision making, forecasting future results and evaluating current performance. By disclosing non-GAAP financial measures, management intends to provide investors with a meaningful, consistent comparison of the Company’s core operating results and trends for the periods presented. Non-GAAP financial measures are not prepared in accordance with GAAP; therefore, the information is not necessarily comparable to other companies and should be considered as a supplement to, not a substitute for, or superior to, the corresponding measures calculated in accordance with GAAP. The Company has provided preliminary results and guidance with respect to cash earnings per share, adjusted cash flows from operations and organic product growth rates, which are non-GAAP financial measures. The Company has not provided a reconciliation of these preliminary and forward-looking non-GAAP financial measures due to the difficulty in forecasting and quantifying the exact amount of the items excluded from the non-GAAP financial measures that will be included in the comparable GAAP financial measures. Reconciliations of historical non-GAAP financials can be found at www.valeant.com.

Note 1: The guidance in this presentation is only effective as of the date given,

April 29, 2015, and will not be updated or affirmed unless and until the Company

publicly announces updated or affirmed guidance.

2

1. First Quarter 2015 Results

2. Business Performance

3. Dendreon and Salix Integration

4. Financial Summary and 2015 Guidance

Agenda

3

Continued outperformance of U.S. businesses, driven by recent

product launches, fueled top line and bottom line results

Exceeded Q1 Guidance despite losing $140 million of revenues and $0.12

Cash EPS due to the rising U.S. dollar

Excluding negative impact from foreign exchange and divestiture of

injectable business, revenue increased 27% and Cash EPS increased

50% Y/Y

Strong performance from most business units around the

world helped to fuel 15% same store organic growth in Q1

Third consecutive quarter of organic growth >15%

Salix and Dendreon integrations largely complete

Salix to deliver more than $530 million in synergies and achieve $500

million run rate synergies by the end of Q2

Dendreon to deliver more than $130 million in synergies and achieve 90%

run rate synergies by year-end

Dendreon profitable in Q1 with revenues as expected

Q1 Highlights (1/2)

4

Increasing 2015 Cash EPS guidance to $10.90 - $11.20

Based on outperformance of Legacy Valeant, coupled with contributions

from Salix and Dendreon

Total company organic growth > 10% (same store) Q2 through Q4;

Bausch + Lomb organic growth ~ 10% full year 2015

Reconfirming 20%+ Cash EPS accretion and expectation to

exceed $7.5 billion EBITDA in 2016

Q1 Highlights (2/2)

5

Q1 2015 Q1 2014 Y/Y%

Adjusted

Y/Y%(a),(b)

Total Revenue $2.19 B $1.89 B 16% 27%

Cash EPS $2.36 $1.76 34% 50%

Salix Acquisition Related

Includes ($0.01) impact from incremental shares issued

Excludes ($0.02) impact from cash interest expense for debt issued

prior to close

Q1 2015 Financial Results

a) FX Impact: Revenue -$140 million and Cash EPS -$0.12

b) 2014 includes $53 million in revenue and $0.11 Cash EPS from divested injectable business

6

Same Store Sales – Y/Y growth rates for businesses that have

been owned for one year or more

Q1 2015

Total U.S. 26%

Total Developed 18%

Total Emerging Markets 7%

Total Company 15%

Pro Forma – Y/Y growth rates for entire business, including

businesses that have been acquired within the last year

Q1 2015

Total U.S. 36%

Total Developed 25%

Total Emerging Markets 7%

Total Company 21%

Q1 2015 Organic Growth

7

Country/Region Q1 2015 Product Sales Y/Y%

United States $321 14%

Consumer $111 4%

Rx Pharma $116 32%

Surgical $48 0%

Contact Lens $48 17%

Other Developed Markets $240 -4%

Emerging Markets $184 7%

Total (a) $745 6%

Bausch + Lomb Organic Growth

Other Developed Markets impacted by Japan’s -14% Y/Y due to April 1, 2014 sales

tax increase in Japan, which resulted in incremental Q1 2014 demand

Excluding impact from Japan – Bausch + Lomb grew 8% Y/Y

(a) Excludes Bausch + Lomb generics which are managed and reported with Valeant generics and total company organic growth

8

Top 20 products revenue of $857M in Q1 2015, representing

40% of total revenue

Largest product contributed ~3% of Q1 revenue

Top 10 products contributed 27% of Q1 revenue

Top 20 products, excluding newly acquired products

(Provenge, Isuprel, Nitropress), grew 36% Q1 2015 over Q1

2014

Majority of growth from volume

Once Salix wholesaler inventory levels have normalized,

4-5 Salix products will enter the Top 20

Q1 2015 Top 20 Brands

9

Product Q1 14 Q2 Q3 Q4 Q1 15

1) Isuprel® - - - - $72

2) Wellbutrin® $69 $72 $80 $82 $68

3) Jublia® - $3 $12 $54 $62

4) Nitropress® - - - - $62

5) Ocuvite®/PreserVision® $60 $66 $62 $62 $60

6) Xenazine® $50 $54 $56 $52 $57

7) Solodyn® $51 $43 $54 $61 $57

8) Targretin® Capsules $15 $29 $44 $48 $51

9) Lotemax® Franchise $26 $45 $35 $47 $43

10) ReNu Multiplus® $55 $49 $41 $46 $42

Q1 2015 Top 20 Brands (1/2) ($M)

10

Product Q1 Q2 Q3 Q4 Q1

11) Virazole® $13 $7 $3 $17 $33

12) Arestin® $15 $30 $30 $38 $32

13) CeraVe® $22 $26 $21 $27 $30

14) Provenge® - - - - $30

15) Retin-A® Franchise $18 $19 $30 $30 $28

16) BioTrue® Solution $24 $27 $26 $25 $28

17) Elidel® $26 $25 $22 $31 $26

18) Carac® $12 $12 $14 $42 $26

19) Ziana® $14 $13 $17 $23 $26

20) Zovirax® Franchise $40 $19 $23 $35 $25

Q1 2015 Top 20 Brands (2/2) ($M)

11

U.S. Dermatology Highlights All promoted products had positive organic growth

Driven by new product launches, dermatology grew 38% Y/Y

Jublia

Jublia TRxs Up 87% Q/Q resulting from sales force and DTC efforts

New Jublia Tennis Commercial aired April 20th featuring John McEnroe

Jublia 8mL launch planned for early May

#1 among Dermatologists with 50% market share

#1 among Podiatrists with 38% market share

Primary care writers continue to grow

Onexton

January launch; script trends similar to Jublia launch; ~5,000 scripts per week after

14 weeks

First commercial aired April 6

Fully integrated DTC campaign accelerating growth

Retin-A Micro Franchise

Sales up >50% Y/Y

Luzu

New Luzu DTC campaign accelerated weekly TRx to new high

Obagi and Solta

Combined growth of 24% Y/Y

12

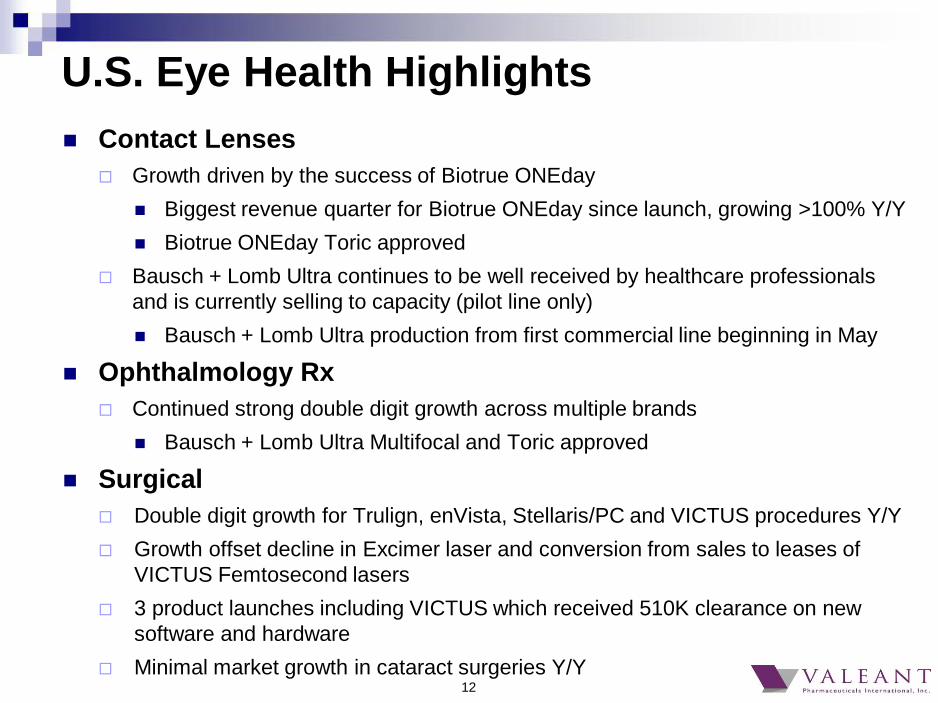

Contact Lenses

Growth driven by the success of Biotrue ONEday

Biggest revenue quarter for Biotrue ONEday since launch, growing >100% Y/Y

Biotrue ONEday Toric approved

Bausch + Lomb Ultra continues to be well received by healthcare professionals

and is currently selling to capacity (pilot line only)

Bausch + Lomb Ultra production from first commercial line beginning in May

Ophthalmology Rx

Continued strong double digit growth across multiple brands

Bausch + Lomb Ultra Multifocal and Toric approved

Surgical

Double digit growth for Trulign, enVista, Stellaris/PC and VICTUS procedures Y/Y

Growth offset decline in Excimer laser and conversion from sales to leases of

VICTUS Femtosecond lasers

3 product launches including VICTUS which received 510K clearance on new

software and hardware

Minimal market growth in cataract surgeries Y/Y

U.S. Eye Health Highlights

13

Neuro & Other/Generics

Organic growth driven by Xenazine, Ammonul and Virazole

Consumer

Strong organic revenue growth from CeraVe (40%), Preservision (20%), Occuvite

(15%) and Soothe XP (19%)

Lens care grew 17% Y/Y driven by 24% growth in BioTrue Multipurpose Solutions

Oral Health

High double digit growth driven by strong volume growth for Arestin

Continued additions to the dental product portfolio

Other U.S. Business Highlights

14

Emerging Markets - Europe/Middle East, $212M Revenues, 6%

Y/Y Organic Growth

Strong organic growth in Poland (29%) and the Middle East (26%)

Russia organic growth negative given strong consumer buying in Q4 14 ahead of

retail price increases

Emerging Markets - Asia, $125M Revenues, 10% Y/Y Organic

Growth

Strong organic growth across most markets including Thailand (30%+), China

(17%), S. Korea (15%), and Malaysia (13%)

Emerging Markets - Latin America, $89M Revenues, 7% Y/Y

Organic Growth

Mexico delivered 11% organic growth

ROW Developed, $361M Revenues, -1% Y/Y Organic Growth

Strong performance in Canada and Australia, with 9% and 3% organic growth,

respectively

Japan declined by (10%) Y/Y due to April 1, 2014 sales tax increase which resulted

in incremental Q1 2014 demand

Rest of World Business Highlights

15

Dendreon off to a strong start

Revenue on plan

Profitable in Q1 as a result of restructuring of the business

All synergies identified with total plan of ~ $130 million+ (including

manufacturing)

90% of synergies on a run rate basis to be achieved by year-end

Gross margins in mid-60% by year-end

Focus on new accounts while maintaining support with existing users

Renewed emphasis on urology in addition to oncology

Dendreon Integration

16

Salix Integration (1/3)

Completed acquisition on April 1, 2015

New Leadership team appointed

Bill Bertrand: General Manager, former COO Salix

John Temperato: Head of Sales, previously held senior sales positions at

Salix

Tom Hadley: Head of Marketing, former marketing lead for Jublia and

Luzu

Synergies

All synergies identified, plan to exceed original synergy guidance of $500M

with $530 million in synergies now expected

$500 million run rate synergies to be captured by end of Q2 – remainder by

year-end

All office based employees notified Day 1

Order to cash processes integrated Day 1

17

Recent Salix TRx Trends (2/3)

+19% y/y

Sources: SHS PHAST and Company Data

18

Salix Integration (3/3)

Expanded and refocused sales forces

Maintaining three specialty GI sales forces with some realignment

Expanding Hospital and Federal teams which will also promote select

Valeant products

Creating new sales force to provide greater focus on pain covering Relistor

and Valeant brands

Plan to cover primary care through specialty sales force coupled with

extensive DTC advertising once IBS-D indication is approved

Refocused marketing

Greater focus on DTC and patient engagement across brands

Xifaxan - IBS-D Update

PDUFA date of May 28

In discussion with the FDA on labeling

19

Key R&D Milestones for 2015

Product Category Action Status

EnVista Toric Eye Health File PMA 1H 2015 Additional studies requested

To Be Filed mid- 2016

Luminesse™ (Brimonidine) Eye Health File NDA 1H 2015 Filed NDA in March

Vesneo (glaucoma) Eye Health File NDA 1H 2015 On Track

Lotemax Gel Next Gen Eye Health File NDA 2H 2015 Filing delayed until mid-2016

Ultra Multi Focal Eye Health File PMA 1H 2015 Approved

Ultra Toric Eye Health File PMA 2H 2015 Approved

BioTrue Toric Eye Health File PMA 2H 2015 Approved

IDP-118 (moderate to

severe plaque psoriasis) Derm Initiate Phase III 1H 2015 Phase III Initiated

IDP – 120 (novel acne

combination ) Derm Initiate Phase II 2H 2015 On Track

Arestin LCM Oral Health File NDA 2H 2015 On Track

Xifaxan (IBS-D Indication) Gastrointestinal PDUFA Date May 28 On Track

Financial Outlook

Howard Schiller

21

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

Total Revenue $1,886M $2,041M $2,056M $2,280M $2,191M

Cost of Goods Sold% (% of product sales) 26% 28% 26% 24% 25%

SG&A% (% of total revenue) 26% 25% 24% 23% 26%

R&D Expense $61M $66M $59M $59M $56M

Operating Margin (% of total revenue) (excluding amortization) 45% 44% 47% 50% 47%

Cash EPS (Reported) $1.76 $1.91 $2.11 $2.58 $2.36

GAAP Cash Flow from Operations $484M $376M $619M $816M $491M

Adjusted Cash Flow from Operations* $636M $500M $771M $624M $708M

Fully Diluted Share Count 342M 341M 341M 342M 343M

Financial Summary

Geographic breakdown

64%

8%

10%

6% 4%

8%

United States

Emerging Europe, Africa, & Middle East

Asia

Western Europe

Canada / Australia

Latin America

Based on actuals & projected 2016 revenue

Q1 15

64%

20%

8% 4%

6%

10%

19% 49%

12%

9%

22

12%

9%

5% 7%

13%

53%

Q1 14 2016 Est.

9%

7%

3% 4% 6%

71%

23

Restructuring and Integration Expenses

Q1 restructuring and integration expenses of $65M

As projected, pre-2015 transactions represented < $25M; Majority related

to Bausch + Lomb Waterford plant

2015 transactions represented $41M in the quarter of which Dendreon was

$35M

Q2 restructuring and integration expenses for pre-2015

transactions expected to be < $10M

Salix and Dendreon

Salix: Restructuring and integration expenses expected to be ~$300M

Significant restructuring accounting charge to occur in Q2 2015, while cash

severance will be paid out over 1-3 years, depending upon employee position

Dendreon: Additional $20M restructuring charge in 2015 (for a total of $55M

or ~40% of synergies)

24

Adjusted cash flow from operations excludes build up of A/R related to

Marathon where we did not purchase A/R

Under the terms of a renegotiated managed care contract, two quarterly

rebate payments made in Q1 2015

Excluding second payment, adjusted cash flow would be $757 million,

or 94% cash conversion

Investment in working capital was $78 million driven largely by an increase

in inventory

Cash Flow from Operations

Q1 2015

Adjusted Net Income

$809 million

GAAP Cash Flow from

Operations

$491 million

Adjusted Cash Flow from

Operations

$708 million

Cash Conversion 88%

25

Post- Salix: $31.2B total debt

Weighted average cost of debt: 5.1%

~ 40% bank / 60% bonds

Revolver currently undrawn

Bonds for Salix acquisition consolidated on Balance Sheet in Q1

even though transaction had not yet closed

~ $10.1 B bonds closed into escrow on March 27th

Proceeds from bonds included in restricted cash

Proceeds from equity included in cash and cash equivalents

Fees and expenses related to Salix debt financing in accrued liabilities

Accounts Receivable DSO* in line with previous years (calculated

using gross sales):

Q1 2014: 72 Days

Q1 2015: 71 Days

* Gross revenue is disclosed in 10K for calculation purposes

Balance Sheet

26

Updated 2015 Guidance (1/2)

Organic growth > 10% (same store) expected Q2 through Q4

Bausch + Lomb organic growth ~10% for full year 2015

Timing of synergy capture Salix to deliver more than $530 million in synergies and achieve $500

million run rate synergies by the end of Q2

Dendreon to deliver more than $130 million in synergies and achieve

90% of run rate synergies by year-end

Debt and Shares Outstanding

Weighted average cost of debt: ~5.1%

350 million fully diluted shares outstanding Q2 through Q4

New 2015 Previous 2015

Revenues $10.4 - $10.6 billion $9.2 - $9.3 billion

Cash EPS $10.90 - $11.20 per share $10.10 - $10.40 per share

27

Updated 2015 Guidance (2/2) Salix revenue of ~$1.0 billion

Does not assume IBS-D approval; we will update guidance post approval

Assumes inventory levels reduced to 1.5 months or less by year end

Operating cash flow

Legacy Valeant will continue to target greater than 90% cash conversion

Salix operating cash flow impacted by wholesaler inventory work down program

Will update guidance for operating cash flow when work down program is well under

way

Guidance does not include use of balance sheet

Expect debt paydown and small acquisitions

Q2 Guidance

Revenues: $2.45 - $2.55 billion

Cash EPS: $2.40 - $2.50

Reflects significant inventory work down of Salix products

2016 Outlook

Reconfirm 20%+ Cash EPS accretion assuming IBS-D approval by end of 2015

Expect to exceed $7.5B EBITDA in 2016

Valeant

Pharmaceuticals

International, Inc.

First Quarter 2015

Financial Results Conference Call

April 29, 2015