Embed Size (px)

Citation preview

PSEG PowerStrategic Direction

Frank CassidyPresident & COO

35

Power OverviewPSEG Power’s portfolio optimization strategy provides incremental

profit opportunities while mitigating risks

PSEG EnergyResources & Trade (ER&T)

PSEG Power LLC

PSEGNuclear

PSEGFossil

Energy &

Capacity$

Energy &

Capacity

$

Other Energy Related

Products and

Services

Wholesale Electric Energy

Markets• BGS• Other firm contracts• Spot market Gas

Markets

• Wholesale gas customers• Retail gas customers

Gas Contracts& Storage

$Wholesale

Gas & Storage

36

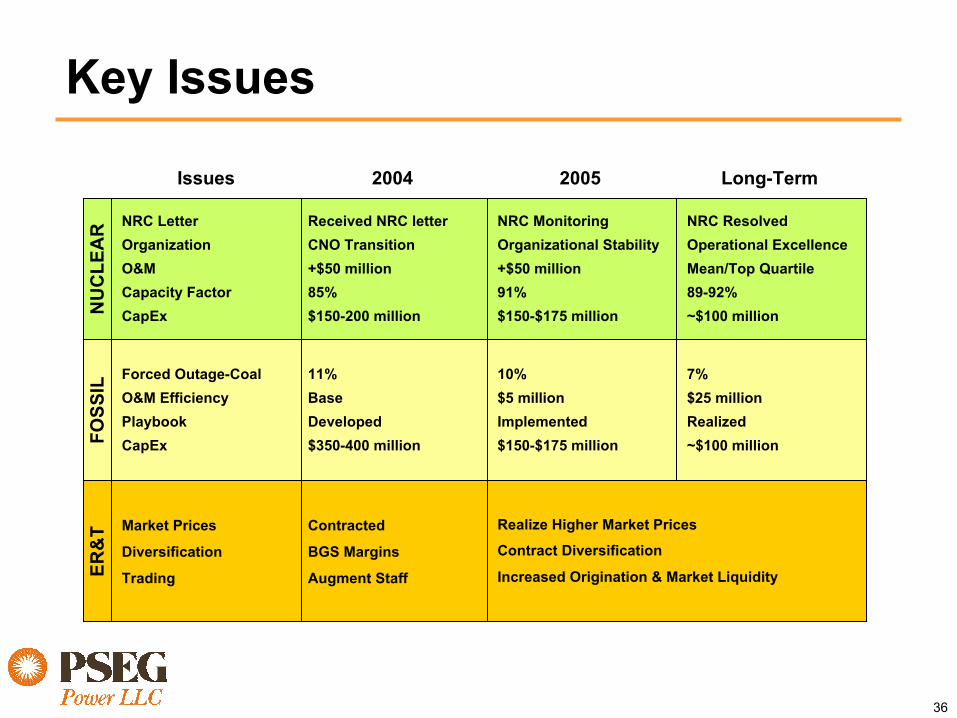

Key Issues

NRC ResolvedOperational ExcellenceMean/Top Quartile89-92%~$100 million

7%$25 millionRealized~$100 million

Received NRC letterCNO Transition+$50 million 85%$150-200 million

11%BaseDeveloped$350-400 million

Contracted

BGS Margins

Augment Staff

NRC LetterOrganizationO&MCapacity FactorCapEx

Forced Outage-CoalO&M EfficiencyPlaybookCapEx

Market Prices

Diversification

Trading

2004 2005 Long-Term

NRC MonitoringOrganizational Stability+$50 million 91%$150-$175 million

10%$5 millionImplemented$150-$175 million

Realize Higher Market Prices

Contract Diversification

Increased Origination & Market Liquidity

Issues

NU

CLE

AR

FOSS

ILER

&T

37

Key Issues

7%$25 millionRealized~$100 million

11%BaseDeveloped$350-400 million

Contracted

BGS Margins

Augment Staff

Forced Outage-CoalO&M EfficiencyPlaybookCapEx

Market Prices

Diversification

Trading

10%$5 millionImplemented$150-$175 million

Realize Higher Market Prices

Contract Diversification

Increased Origination & Market Liquidity

FOSS

ILER

&T

NRC ResolvedOperational ExcellenceMean/Top Quartile89-92%~$100 million

Received NRC letterCNO Transition+$50 million 85%$150-200 million

NRC LetterOrganizationO&MCapacity FactorCapEx

NRC MonitoringOrganizational Stability+$50 million 91%$150-$175 million

NU

CLE

AR

38

NRC ResolvedOperational ExcellenceMean/Top Quartile89-92%~$100 million

Received NRC letterCNO Transition+$50 million 85%$150-200 million

NRC LetterOrganizationO&MCapacity FactorCapEx

NRC MonitoringOrganizational Stability+$50 million 91%$150-$175 millionN

UC

LEA

RKey Issues

7%$15 millionRealized$100 million

11%BaseDeveloped$350-400 million

Contracted

BGS Margins

Augment Staff

Forced Outage-CoalO&M EfficiencyPlaybookCapEx

Market Prices

Diversification

Trading

2004 2005 Long-Term

10%$5 millionImplemented$165 million

Realize Higher Market Prices

Contract Diversification

Increased Origination & Market Liquidity

Issues

FOSS

ILER

&T

Long-Term7%$25 millionRealized~$100 million

200411%BaseDeveloped$350-400 million

IssuesForced Outage-CoalO&M EfficiencyPlaybookCapEx

200510%$5 millionImplemented$150-$175 million

FOSS

IL

39

NRC MonitoringOrganizational Stability+$50 million 91%$150-$175 million

Key Issues

NRC ResolvedOperational ExcellenceMean/Top Quartile89-92%~$100 million

7%$25 millionRealized$100 million

Received NRC letterCNO Transition$50 million 85%$150-200 million

11%BaseDeveloped$350-400 million

Contracted

BGS Margins

Augment Staff

NRC LetterOrganizationO&MCapacity FactorCapEx

Forced Outage-CoalO&M EfficiencyPlaybookCapEx

Market Prices

Diversification

Trading

2004 2005 Long-Term

10%$5 millionImplemented$165 million

Realize Higher Market Prices

Contract Diversification

Increased Origination & Market Liquidity

Issues

NU

CLE

AR

FOSS

ILER

&T

2004

Contracted

BGS Margins

Augment Staff

Issues

Market Prices

Diversification

Trading

2005 & Long-TermRealize Higher Market Prices

Contract Diversification

Increased Origination & Market Liquidity

ER&

T

40

PSEG Power Business Objectives• Nuclear Operations

– Operate safely– Improve capacity factor– Upgrade assets– Operate at industry mean O&M levels

• Fossil Operations– Operate safely and predictably– Implement industry best practices– Reduce O&M

• ER&T Operations– Realize value of diverse electric and gas asset portfolio

PSEG Nuclear Strategic Direction

Chris Bakken President & Chief Nuclear Officer

42

PSEG Nuclear: Asset Profile

• Operated by PSEG Nuclear

• PSEG Ownership: 100%

• Technology:Boiling Water Reactor

• Total Capacity: 1,049 MW

• Owned Capacity: 1,049 MW

• License Expiration: 2026

• Operated by PSEG Nuclear

• PSEG Ownership: 57% Exelon other Co-Owner

• Technology: Pressurized Water Reactor

• Total Capacity: 2,275 MW

• Owned Capacity: 1,306 MW

• License Expiration: 2016 and 2020

• Operated by Exelon

• PSEG Ownership: 50%

• Technology:Boiling Water Reactor

• Total Capacity: 2,224 MW

• Owned Capacity: 1,112 MW

• License Expiration: 2033 and 2034

Hope Creek

Salem Units 1 and 2

Peach Bottom Units 2 and 3

43

• Operate safely

• Improve capacity factor

• Upgrade assets

• Operate at industry mean O&M levels

Key Objectives

44

Discussion Points

• Work Environment Progress

• Plant Operations

• O&M

45

Work Environment - Current Status

• NRC closed investigation

• Two cross-cutting issues– Problem Identification and Resolution– Safety Conscious Work Environment

• Issues being addressed

• NRC concurrence with approach

• Monitor progress going forward

46

MAY 05MAR 05FEB 05 APR 05JAN 05DEC 04NOV 04OCT 04SEP 04

HOPE CREEK OUTAGEHOPE CREEK OUTAGE

Work Environment - Next Steps

Public Meeting

with NRC

Public Meeting

with NRC

Post SCWE Metrics

SALEM OUTAGESALEM OUTAGE

Post SCWE Metrics

Post SCWE Metrics

SYNERGY SURVEYSYNERGY SURVEY

47

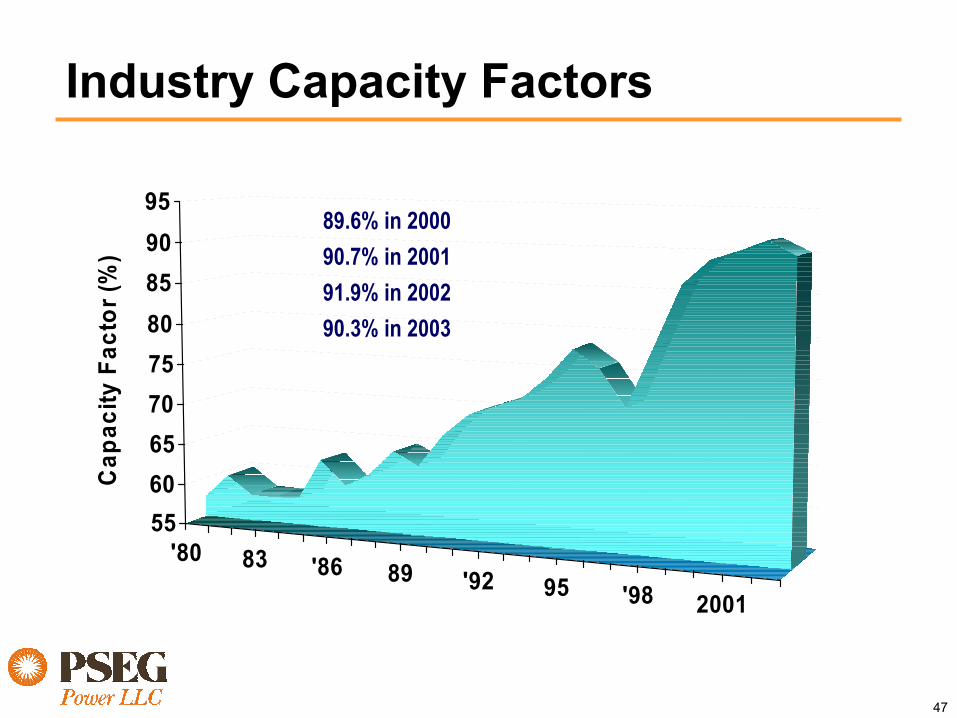

Industry Capacity Factors

'80 83 '86 89 '92 95 '98 2001

556065707580859095

Cap

acity

Fac

tor (

%)

89.6% in 200090.7% in 200191.9% in 200290.3% in 2003

48

75

80

85

90

95

100

Cap

acity

Fac

tor %

2000 2001 2002 2003 2004 2005 2006 2007

Industry PSEG Nuclear

PSEG Capacity Factor

49

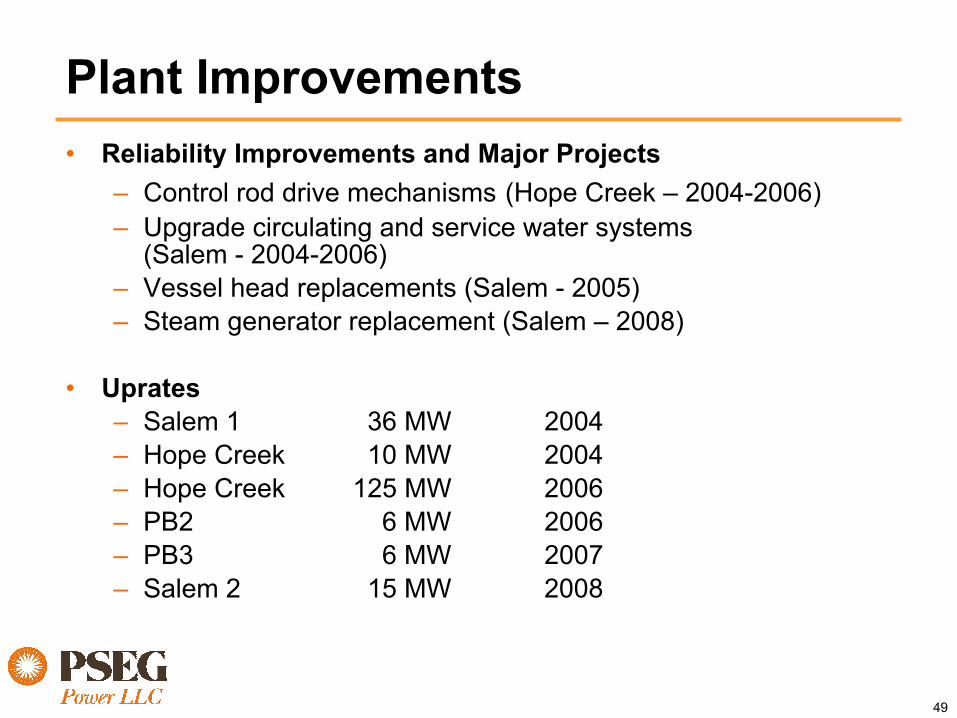

Plant Improvements• Reliability Improvements and Major Projects

– Control rod drive mechanisms (Hope Creek – 2004-2006)– Upgrade circulating and service water systems

(Salem - 2004-2006)– Vessel head replacements (Salem - 2005)– Steam generator replacement (Salem – 2008)

• Uprates– Salem 1 36 MW 2004– Hope Creek 10 MW 2004– Hope Creek 125 MW 2006– PB2 6 MW 2006– PB3 6 MW 2007– Salem 2 15 MW 2008

50

Capital Program

Expected 5-yr capital investment to be approximately $640 million

Capital Expenditures - PSEG Share

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

2005 2006 2007 2008 2009

Mill

ions

51

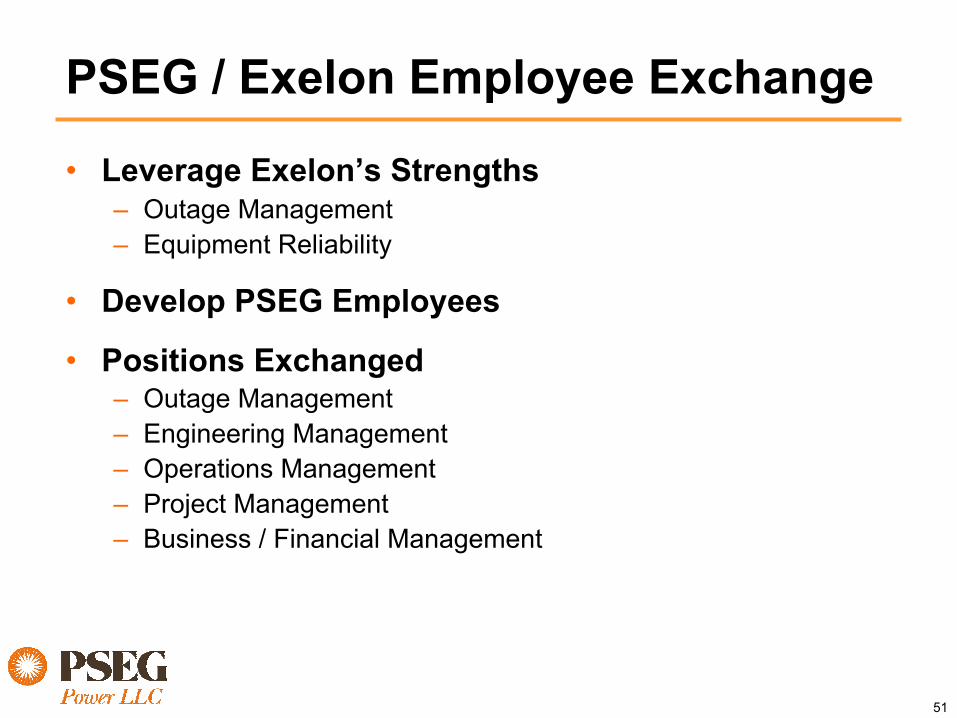

PSEG / Exelon Employee Exchange

• Leverage Exelon’s Strengths– Outage Management– Equipment Reliability

• Develop PSEG Employees

• Positions Exchanged– Outage Management– Engineering Management– Operations Management– Project Management– Business / Financial Management

52

Value of Increased Nuclear Output

• PSEG share of NJ output increases by nearly 3,000 GWhrs/yr by 2007 – an improvement of more than 10% over 2004

• At a $35 - $40 gross margin, the opportunity to Power is $100 - $120 million– $65 – $80 million from performance improvement– $35 – $40 million from uprates

53

Near-Term O&M Cost Drivers• Increased Outage Scope

– Control rod drive mechanism– Reliability improvements

• Upgrade of Facilities

• Supplemental Labor to Address Issues

• Security

54

Key TakeawaysNuclear has a strong plan for performance improvement, resulting

in considerable financial upside to Power

$45 M - $55 MO&M

Uprates

Unit Performance

$35 M - $40 M

$65 M - $80 M

Pretax margin opportunity $ 145 M - $175 M

PSEG Fossil Strategic Direction

Mike Thomson President

56

PSEG Fossil: Asset Profile

Variable Cost

Low

High

Coal

CCGT

Peaking (simple cycle & steam)

Demand On SystemLow High

2396 MW 5121 MW 4774 MW

46 Units in NJ/CT/PA Bergen (NJ) 1221 MWWaterford (OH) 821 MWLawrenceburg (IN) 1096 MWBEC (NY 2005) 763 MWLinden (NJ 2006) 1220 MWKeystone (PA) 388 MW

Conemaugh (PA) 382 MWHudson (NJ) 608 MWMercer (NJ) 648 MWBridgeport (CT) 370 MW

$25 - $45/mwh $40 - $60/mwh $60 + /mwh

57

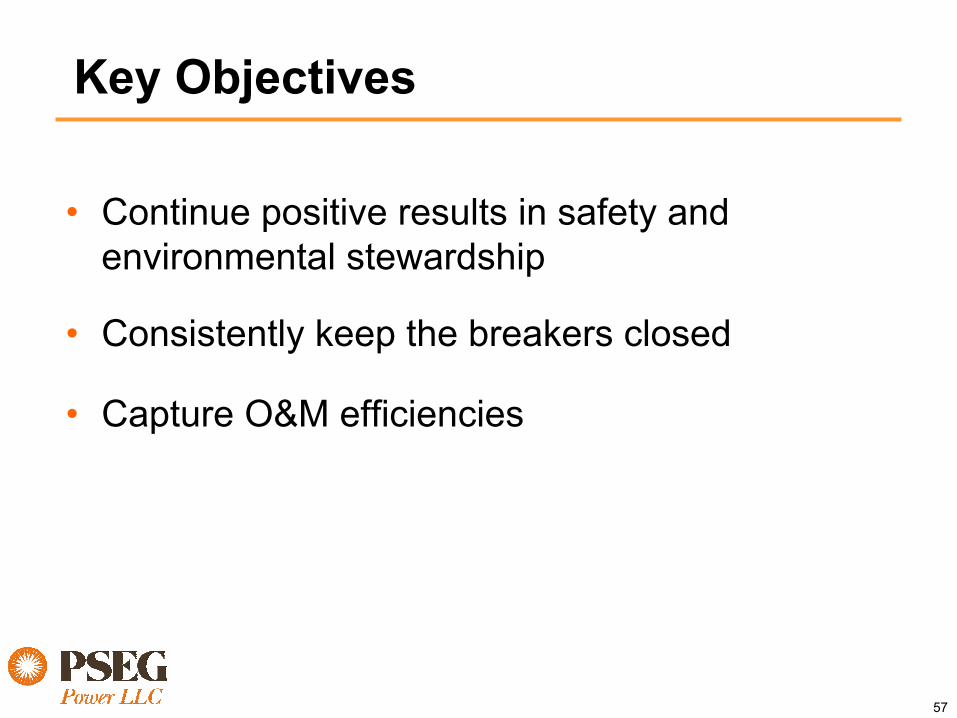

Key Objectives

• Continue positive results in safety and environmental stewardship

• Consistently keep the breakers closed

• Capture O&M efficiencies

58

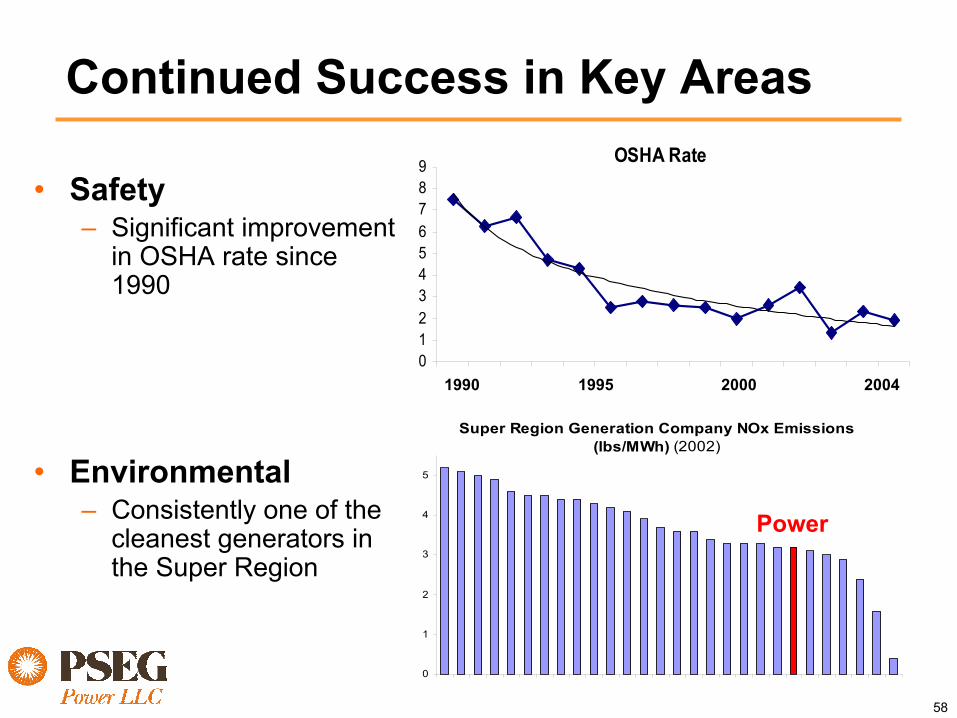

Continued Success in Key Areas

• Safety– Significant improvement

in OSHA rate since 1990

• Environmental– Consistently one of the

cleanest generators in the Super Region

Super Region Generation Company NOx Emissions (lbs/MWh) (2002)

0

1

2

3

4

5

Power

OSHA Rate

0123456789

1990 1995 20001990 1995 2000 2004

59

Revenue Enhancement Opportunity

Fossil Generation at Market Prices($ million)

• Fossil plays an integral part in Power’s profitability

• Opportunity exists to further enhance margin contribution to Power

• Points of attack:– Address existing issues– Rigorous preventative

maintenance program 050

100150200250300350400450500

2003A 2004F

MaintenancePlanning &ExecutionOperatingPerformance

Market BasedRevenues

60

• Improved unit performance- $60-$70 million

• Capture O&M efficiencies inexecution of planned maintenance

- $15-$25 million

Fossil Value Enhancement Plan C

urre

nt P

erfo

rman

ce

$95 m

$75 m

2004

Existing Fleet

61

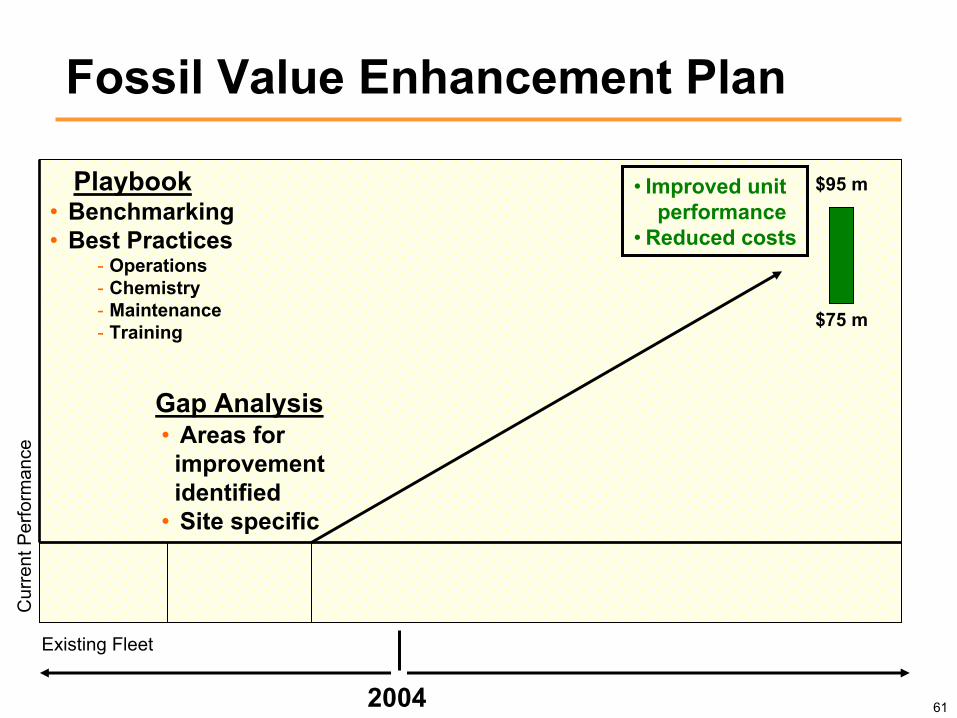

Playbook • Improved unitperformance

• Reduced costs• Benchmarking• Best Practices

- Operations- Chemistry- Maintenance- Training

Cur

rent

Per

form

ance

Gap Analysis• Areas forimprovement identified

• Site specific

$95 m

$75 m

Fossil Value Enhancement Plan

Existing Fleet

2004

62

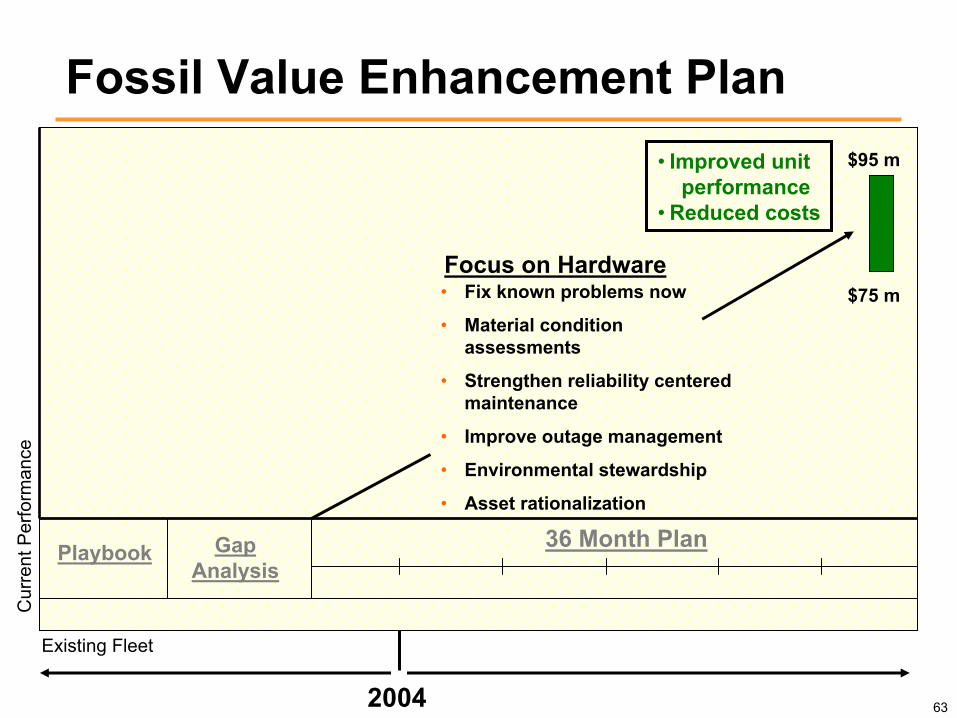

Playbook Gap Analysis

• Establish the actionable priorities and responsibilities for Playbook implementation

• Actions target specific operating & productivity metrics

• Plant investment and operations tied to asset mission

• Integrated into performance management and compensation plans

36 Month Plan

Cur

rent

Per

form

ance

$95 m

$75 m

• Improved unitperformance

• Reduced costs

Fossil Value Enhancement Plan

Existing Fleet

2004

63

Playbook Gap Analysis

36 Month Plan

Cur

rent

Per

form

ance

Focus on Hardware• Fix known problems now

• Material condition assessments

• Strengthen reliability centered maintenance

• Improve outage management

• Environmental stewardship

• Asset rationalization

$95 m

$75 m

• Improved unitperformance

• Reduced costs

Fossil Value Enhancement Plan

Existing Fleet

2004

64

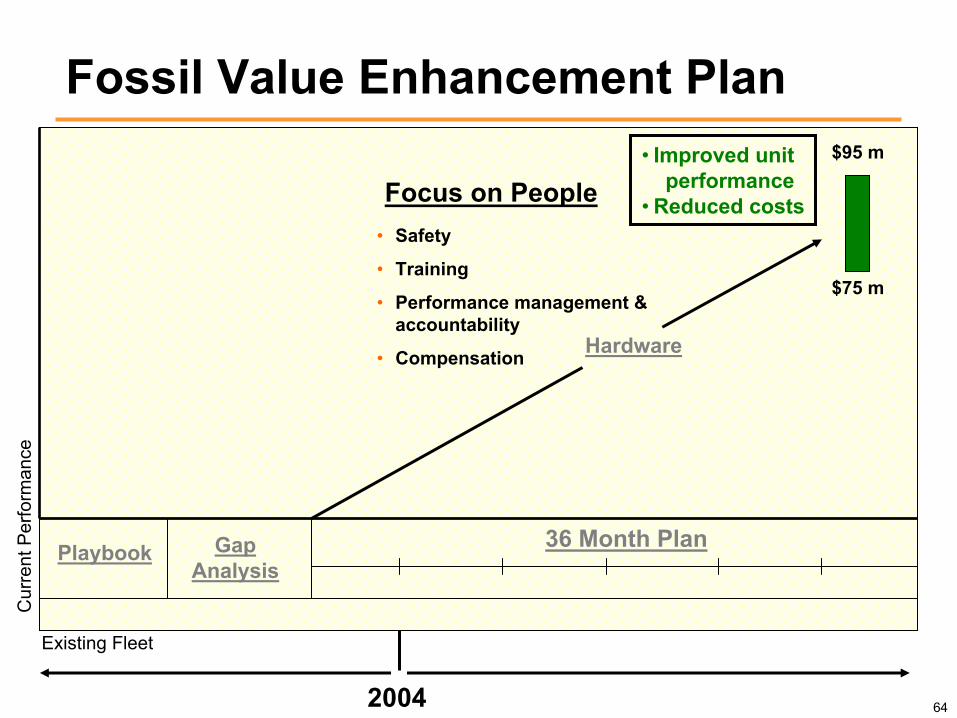

• Safety

• Training

• Performance management & accountability

• Compensation

Playbook Gap Analysis

36 Month Plan

Cur

rent

Per

form

ance

Hardware

$95 m

$75 m

Focus on People• Improved unit

performance• Reduced costs

Fossil Value Enhancement Plan

Existing Fleet

2004

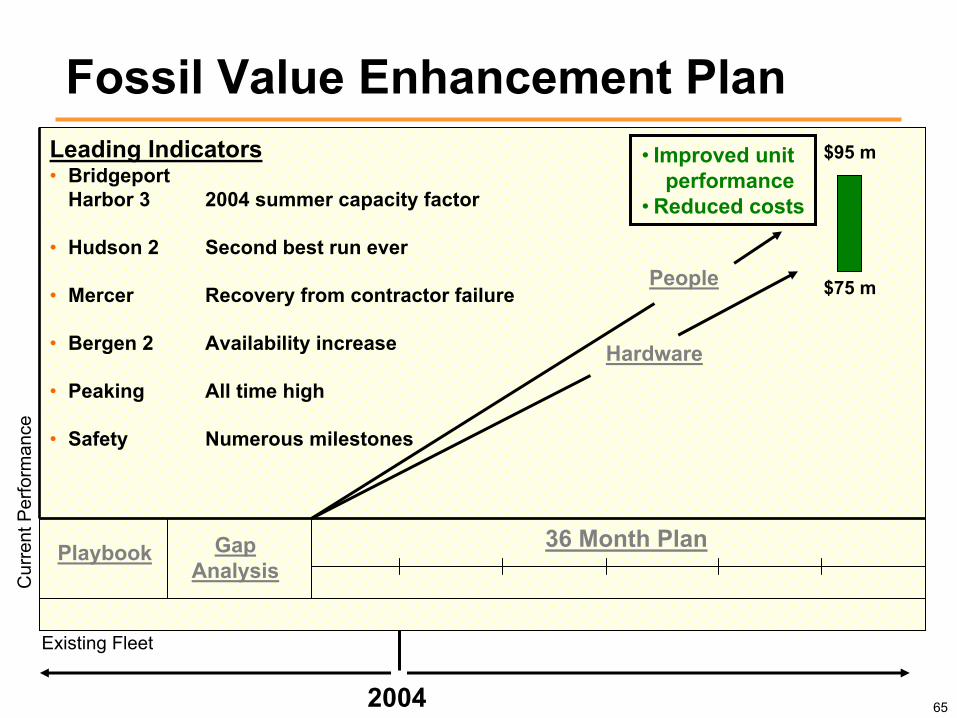

65

Playbook Gap Analysis

36 Month Plan

Cur

rent

Per

form

ance

Hardware

$95 m

$75 mPeople

Leading Indicators• Bridgeport

Harbor 3 2004 summer capacity factor

• Hudson 2 Second best run ever

• Mercer Recovery from contractor failure

• Bergen 2 Availability increase

• Peaking All time high

• Safety Numerous milestones

• Improved unitperformance

• Reduced costs

Fossil Value Enhancement Plan

Existing Fleet

2004

66

Playbook Gap Analysis

36 Month Plan

Cur

rent

Per

form

ance

Hardware

$95 m

$75 mPeople

Fossil Value Enhancement Plan

Existing Fleet

2004

• Improved unit performance- $60-$70 million

• Capture O&M efficiencies inexecution of planned maintenance

- $15-$25 million

PSEG ER&T Strategic Direction

Steve Teitelman President

68

Energy Resources & Trade (ER&T) Business Profile

ER&T

PortfolioManagement

FuelSupply

AssetBacked

WholesaleCommodity

Trading

RiskManagement

Market/BusinessDevelopment

Single point accountability for gross margin optimization

69

Portfolio Management – Operational Strategy

• Maximize cash in the short term relative to unit cost, availability, spot price, fuel price and import capability

• Portfolio provides opportunities to seek structured transactions that provide higher margins

• Understand and influence the development of fair market rules

• Same proven business model for 5 years

70

Portfolio Management - Net PositionPower’s objective is to contract over 75% of its planned

generation for the next 18-24 months

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

GW

h

Nuclear Baseload Coal Intermediate Coal CC

Steam / CT Contracted Load & Sales Contracted Load

2004 2005 2006 2007

Total Fleet Monthly RTC GWh Position

71

Portfolio Management – Fuel Strategy

• Maximize value relative to the spark spread

• Fuel switch to extract value

• Hedge coal, oil and gas relative to contracts and hedges

• Utilize wholesale gas system for balancing fuel consumption and option value

• Trade fuels (gas, coal and oil) in conjunction with the portfolio position

• Modify fuel inventory to maximize value

• Gas throughput

• Gas storage capacity

• Coal contracts

• Oil storage capacity

• Emissions credits

• Generation assets/contracts

• Gas contracts

• Transmission rights

Assets Strategy

72

Fuel Strategy - Coal

Domestic

South America

Indonesia

24% 6%

70%

Source of Supply

-

1

2

3

4

5

6

7

2005 2006 2007 2008Year

Milli

on T

ons

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Keystone Conemaugh Bridgeport HarborMercer Hudson Contracted

Continuity of Supply

73

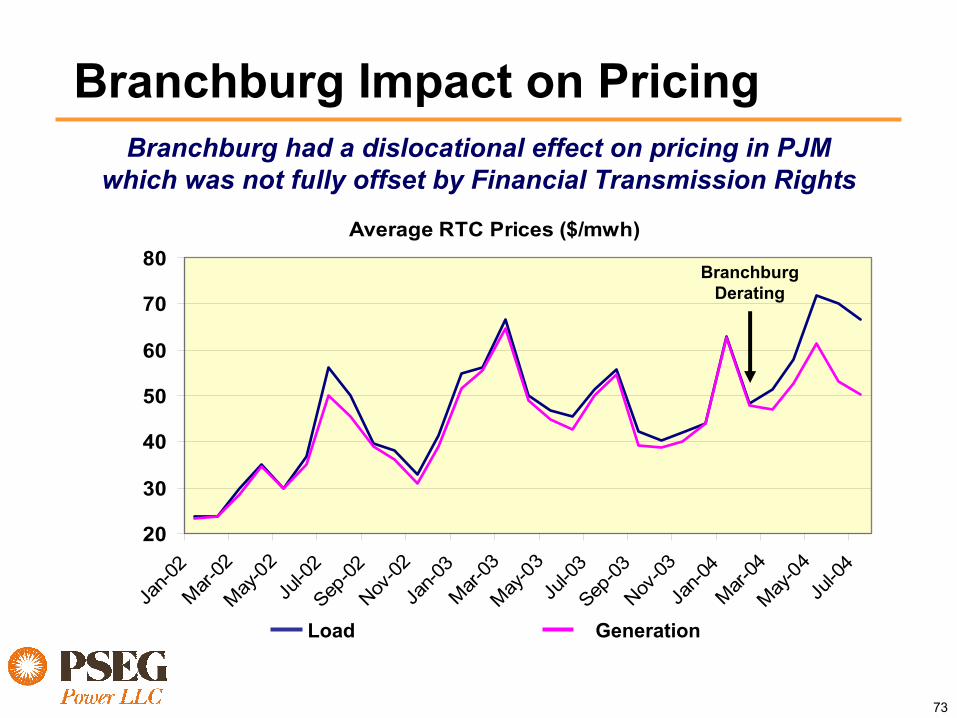

Branchburg Impact on Pricing

Average RTC Prices ($/mwh)

20

30

40

50

60

70

80

Jan-0

2Mar-

02May

-02

Jul-0

2Sep

-02Nov

-02Ja

n-03

Mar-03

May-0

3Ju

l-03

Sep-03

Nov-03

Jan-0

4Mar-

04May

-04

Jul-0

4

Branchburg had a dislocational effect on pricing in PJMwhich was not fully offset by Financial Transmission Rights

BranchburgDerating

Load Generation

74

ER&T Historical PerformanceER&T’s diverse portfolio has provided growth through varying market conditions,

with an increasing reliance on lower risk products

020406080

100120140160180200

1997 1998 1999 2000 2001 2002 2003 2004Est.

ER&T Margins ($ millions)

Asset Based Margins- Greater predictability

Trading -Reduced market making opportunities-Shift from fundamentalto financial players

Reduced market exposure at ER&T is aligned with shifting market conditions

75

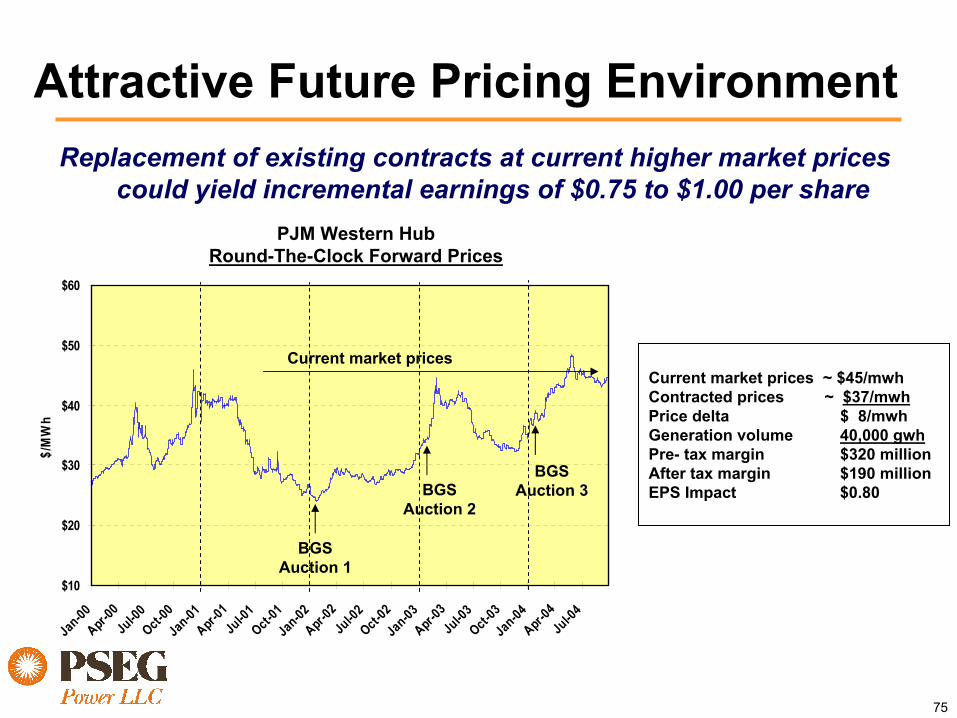

Attractive Future Pricing EnvironmentReplacement of existing contracts at current higher market prices

could yield incremental earnings of $0.75 to $1.00 per share

Current market prices ~ $45/mwhContracted prices ~ $37/mwhPrice delta $ 8/mwhGeneration volume 40,000 gwhPre- tax margin $320 millionAfter tax margin $190 millionEPS Impact $0.80

PJM Western HubRound-The-Clock Forward Prices

$10

$20

$30

$40

$50

$60

Jan-00

Apr-00

Jul-00

Oct-00

Jan-01

Apr-01

Jul-0

1Oct-

01Ja

n-02Apr-

02Ju

l-02

Oct-02

Jan-03

Apr-03

Jul-03

Oct-03

Jan-04

Apr-04

Jul-0

4

$/M

Wh

BGS Auction 1

BGS Auction 2

BGS Auction 3

Current market prices

Summary and 2005 Outlook

Frank Cassidy

77

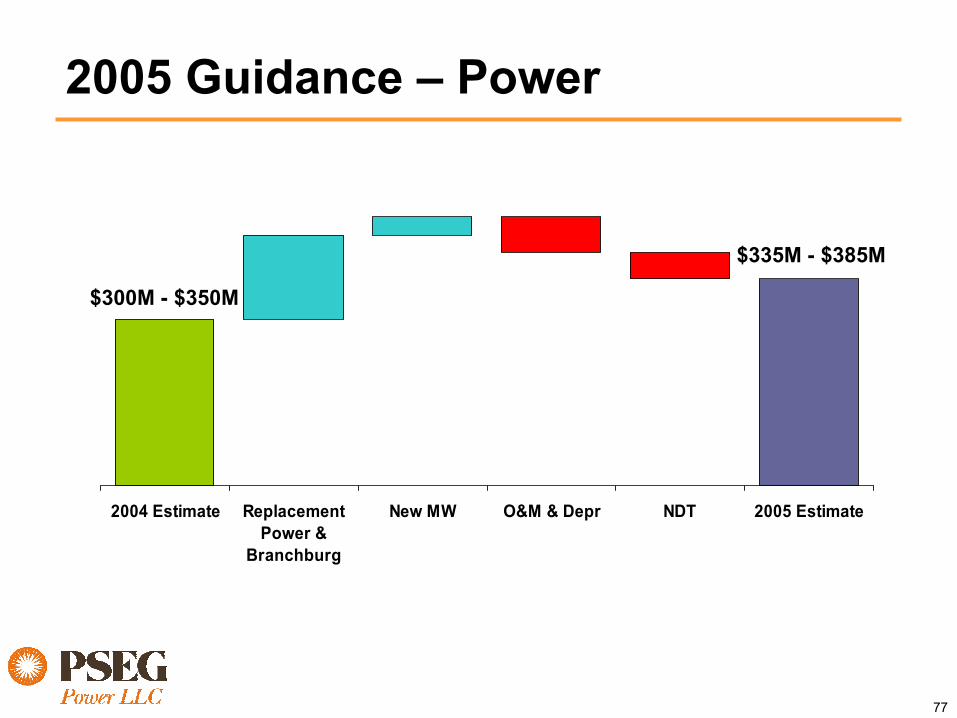

2005 Guidance – Power

2004 Estimate ReplacementPower &

Branchburg

New MW O&M & Depr NDT 2005 Estimate

$300M - $350M

$335M - $385M

78

2005 Assumptions

• Natural gas prices $6.30/mmbtu

• RTC Energy (PJM West) $45/mwh

• East/West differential $2.30/mwh

• Capacity Prices $10/kw-yr

• Nuclear Capacity Factors 91%

79

Sensitivity of 2005 Assumptions

• Natural gas prices +/- $1/mmbtu $.01• RTC energy (PJM West) +/- $5/mwh $.08• Capacity prices +/- $5/kw-yr $.04• East/West differential +/- $2/mwh $.03• Nuclear capacity factors +/- 1% fleet $.03• 2005 BGS auction prices +/- $1/mwh $.01• Coal prices +/- $10/ton $.02

80

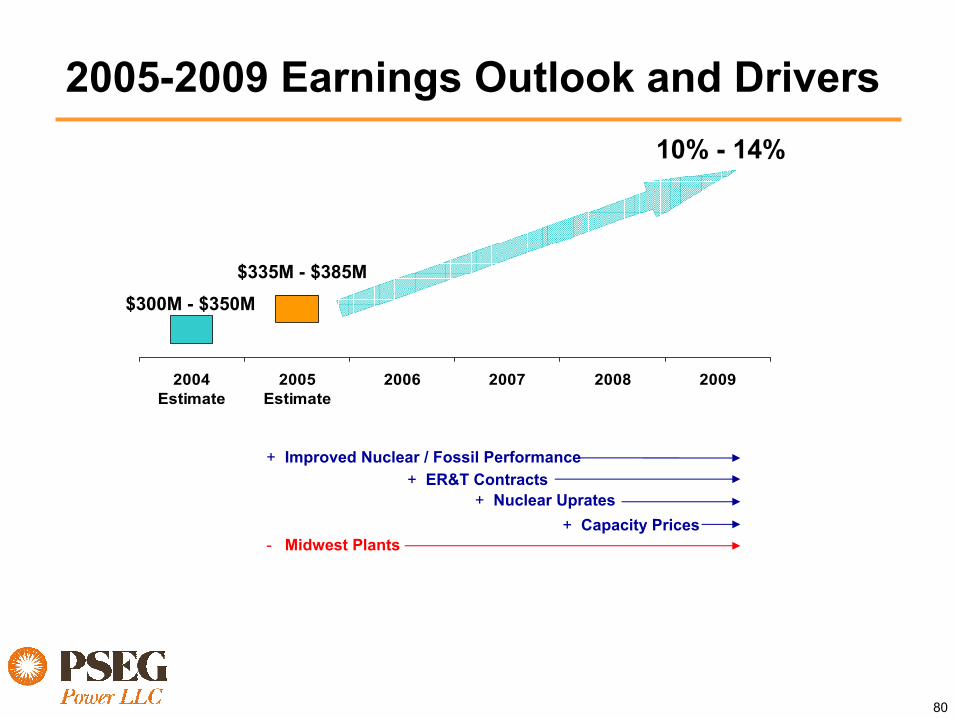

2004Estimate

2005Estimate

2006 2007 2008 2009

10% - 14%

$300M - $350M

+ Capacity Prices

+ Improved Nuclear / Fossil Performance

+ Nuclear Uprates+ ER&T Contracts

- Midwest Plants

$335M - $385M

2005-2009 Earnings Outlook and Drivers

81

Key Takeaways• Power’s forecast has considerable upside• Nuclear

– Enhanced capacity factor $65 - $80M– O&M $50M– Uprates $35 - $40M

• Fossil– Unit performance $60 - $70M– O&M $15 - $25M

• ER&T– Contract repricing at current prices $320M