Embed Size (px)

Citation preview

SUBMITTED TO:- SUBMITTED BY:-RASHMI VISHKARMA ADITI TRIPATHI(1150810003)

ARCHANA DIXIT(1150810016)

MUDIT MISHRA(1150810030)

SAUMYA GUPTA(1150810045)

Price. Determination Of Price. Factors Effecting Price. Factors Kept In Mind Before Determining The Price.

Perfect Competition Definition. Meaning. Features. Perfect Competition Vs Pure Competition. Condition For Firms Equilibrium Under Perfect

Competition. Price Under Perfect Competition In Short Period. Price Under Perfect Competition In Long Period.

Monopoly. Features. Demand & Revenue Under Monopoly. Determination Of Price & Equilibrium Under

Monopoly. Price Determination Under Short & Long Period. Price Discriminating Monopoly. Price & output determination under discriminating

monopoly.

Oligopoly. Types Of Oligopoly. Features Of Oligopoly. Sources Of Oligopoly Market.

Duopoly Definition.

Duopoly exists when.

Best Response function.

Types of duopoly. Cournot Model.

Stackelberg Model.

Advantages.

Disadvantages.

Assumption.

Definition of price.

Definition of price determination.

Objectives of price determination.

Need of price determination.

Factors effecting of price determination.

Determination Of Price.

Factors Effecting Price.

Factors Kept In Mind Before Determining The Price.

The value that one will purchase a finite quantity, weight, or other measure of a good or service.

OR

Price is the sacrifice that one party pays another to receive something in exchange.

Pricing is the process of determining what a company will receive in exchange for its product.

Maximize long-run & short-run profit.

Increase sales.

Increase market share.

TO OBTAIN THE TARGET OF RETURN OF INVESTMENT.

Company growth.

To obtain or maintain the loyalty and enthusiasm of distribution and other sales personnel.

Market price serves as the adjustment mechanism to move markets to equilibrium.

Factors

Your Cost

Market Demand

Your Profit

Industry Standards

Who is Your Client

Skill Level

Experience

Excess demand exists when, at the current price, the quantity demanded is greater than quantity supplied.

Excess supply exists when, at the current price, the quantity supplied is greater than the quantity demanded.

supply

demand

price

quantity

p = $3

QD QS

EXCESS SUPPLY

supply

demand

price

quantity

QDQS

EXCESS DEMAND

When there is EXCESS DEMAND for a good, price will tend to rise.

When there is EXCESS SUPPLY of a good, price will tend to fall.

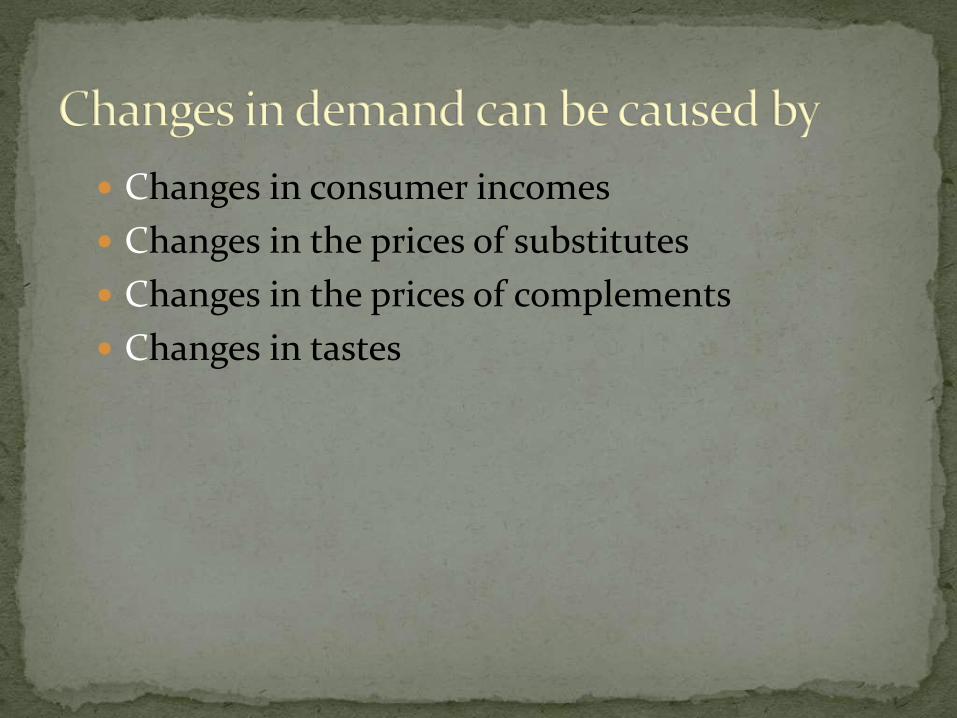

Changes in consumer incomes

Changes in the prices of substitutes

Changes in the prices of complements

Changes in tastes

Changes in prices of inputs.

Changes in technology.

Changes in taxes.

P

Q

supply

p0

q0

demand @ old beer price

demand @ higher beer pricep1

q1

Definition.

Meaning.

Features.

Perfect Competition Vs Pure Competition.

Condition For Firms Equilibrium Under Perfect Competition.

Price Under Perfect Competition In Short Period.

Price Under Perfect Competition In Long Period.

Perfect competition is the theoretical case illustrating the most competitive market possible.

• “Perfect Competition Exists In Markets Where There Are So Many Sellers That No One Is Big Enough To Have Any Appreciable Influence Over Market

Price.”-Prof. Bach

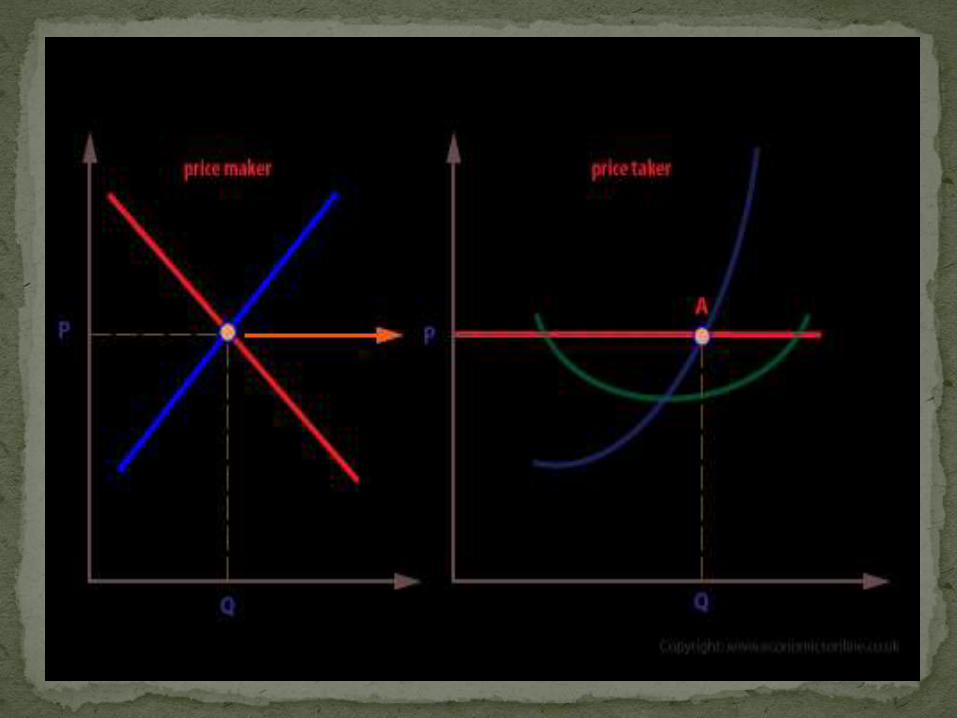

Both buyers and sellers are price takers.

A price taker is a firm or individual who takes the market price as given.

In most markets, households are price takers – they accept the price offered in stores.

The retailer is not perfectly competitive.

A store is not a price taker but a price maker.

The number of firms is large. Any one firm's output is minuscule when compared

with the total market.

Large means that what one firm does has no bearing on what other firms do.

The firms' products are identical. This requirement means that each firm's output is

indistinguishable from any competitor's product.

There are no barriers to entry. Barriers to entry are social, political, or economic

impediments that prevent other firms from entering the market.

Barriers sometimes take the form of patents granted to produce a certain good.

Technology may prevent some firms from entering the market.

Social forces such as bankers only lending to certain people may create barriers.

There is complete information. Firms and consumers know all there is to know about

the market – prices, products, and available technology.

Any technological advancement would be instantly known to all in the market.

Firms are profit maximizers. The goal of all firms in a perfectly competitive market is

profit and only profit.

Firm owners receive only profit as compensation, not salaries.

Pure Competition IS ABSENCE OF MONOPOLY…

CHARACTERISTICS OF PURE COMPETITION

Large no. of buyers & sellers, Homogeneous Products, Free entry & exit of firms.

It means the level of output where firm is maximizing it’s profits & therefore , has no tendency to change its output…

Marginal Cost Curve should cut the Marginal Revenue curve from below.

Marginal Cost= Marginal Revenue= Average Revenue

AR : Average Revenue curve MR : Marginal Revenue curve D : Demand)curve

AR=MR=D

It would be a horizontal line or parallel to the X-axis

Condition : 1

Marginal Cost= Marginal Revenue=Average Revenue

MC=MR=AR

Condition : 2

Marginal Cost Curve should cut

the Marginal Revenue curve

from below.

Short Period is defined as the time period in which the firm can change its output without changing the existing plant & machinery.

Price will be affected because we cannot increase our supply acc. to demand..

Only variable factors can be altered..

Price set so in the short run is EQUILIBRIUM PRICE..

Price at which there is no tendency to change in the current situation..

Demand & Supply are equal…

Pricing Decision is influenced by these two forces of DEMAND & SUPPLY…

LAW OF DEMAND

Applicable for buyers…

Price is inversely proportional to the demand…

Applicable for suppliers…

Price is directly proportional to the supply…

LAW OF SUPPLY

CASES OF FIRM’S EQUILIBRIUM IN SHORT PERIOD

SUPER-NORMALPROFITS

SHUTDOWN POINT

LOSS

NORMALPROFITS

SUPER-NORMALPROFITS

In situation of

firm’s

equilibrium

(i) MC=MR=AR

(ii) AR>SAC

AR>SAC

NORMALPROFITS

In situation of

firm’s

equilibrium

(i) MC=MR=AR

(ii) AR=min(SAC)

AR=SAC

Firms can also earn zero profit or even a loss where MC = MR.

Even though economic profit is zero, all resources, including entrepreneurs, are being paid their opportunity costs.

In all three cases (profit, loss, zero profit), determining the profit-maximizing output level does not depend on fixed cost or average total cost, by only where marginal cost equals price.

LOSS

In situation of

firm’s

equilibrium

(i) MC=MR=AR

(ii) AR<(SAC)

AR<SAC

The shutdown point is the point at which the firm will gain more by shutting down than it will by staying in business.

As long as total revenue is more than total variable cost, temporarily producing at a loss is the firm’s best strategy since it is taking less of a loss than it would by shutting down.

SHUT-DOWN POINT

In situation of firm’s

equilibrium

(i) MC=MR=AR=

min SAVC

(ii) AR=SAVC<SAC

AR<SAC : AR=SAVC

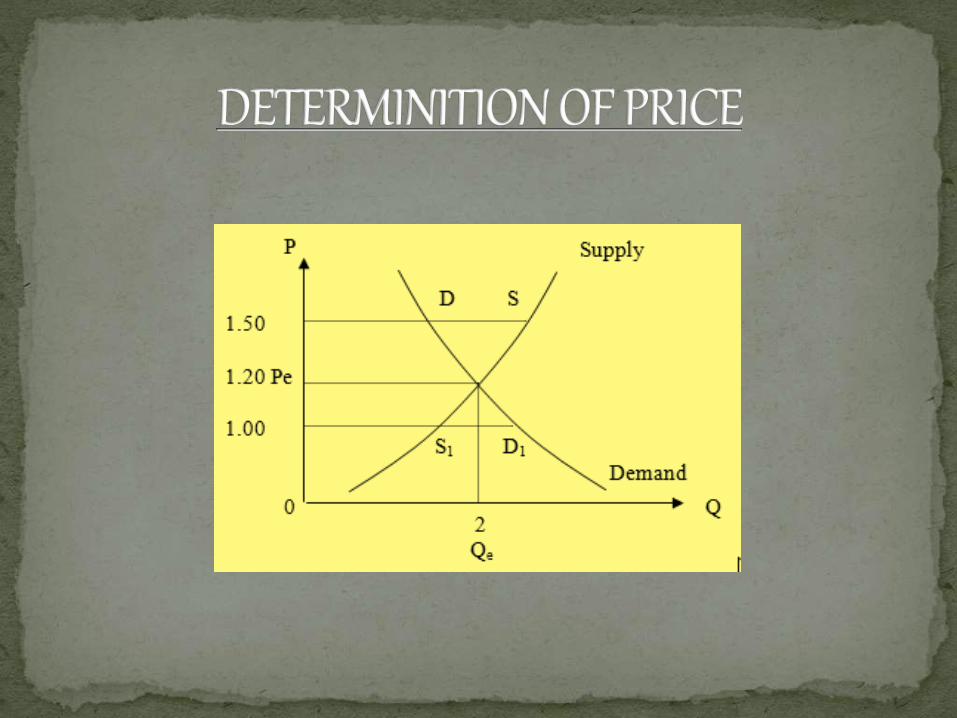

Equilibrium Price is determined at the point where the se forces are EQUAL…

Quantity demanded & supplied at this point is EQULIBRIUM QUANTITY…

When the price is less /more than equilibrium price , then there will be tendency of movement of this equilibrium output & ultimately equilibrium price will prevail…

Demand & Supply forces counteract each other…

Industry :as price maker

Firm :as price taker.

Long Period is defined as that period during which , all factors become variable factors & firms can change their scale of production…

Price that prevails in long-run is NORMAL PRICE..

Supply plays a dominant role in determination of long-run normal price..

Demand & Supply can be adjusted to every possible way as per requirement in long run..

Change all types of fixed factors..

Normal Price is always equal to minimum long run average cost..

Supply gets sufficient time to adjust itself according to changed conditions & demand..

In situation of

firm’s

equilibrium

(i) MC=MR=AR=

min LAC

(ii) AR(P)=LAC

AR=LAC

Definition.

Features.

Type.

Demand & Revenue Under Monopoly.

Price Discriminating Monopoly.

Monopolistic competition.

Advantages And Disadvantages.

“A pure monopoly exists when there is only one producer in a market. There are no direct competitors.”

-According to Prof. Ferguson

“Pure or absolute monopoly exists when a single firm is the sole producer for a product for which there are no close substitutes.”

-Mc Connel

One seller & large number of buyers:Under monopoly there should be single

producer of the commodity.

The buyers of the product are in large number.

Only Seller can influence the price.

Monopoly is also an industry:• There is only one firm & the difference

between firm & industry disappears.

Restrictions on the entry of new firms:There are some restrictions on the entry of new

firms into monopoly industry

There is no competitor o a monopoly firm.

No close substitutes: If close substitute are available then the

monopolist will not be able to determine the price of his commodity as per his discretion.

Natural monopoly.

Public monopoly.

Legal monopoly.

Simple and discriminating.

Absolute monopoly and limited monopoly.

State monopoly and private monopoly.

In a monopoly situation there is no differencebetween firm & industry. Accordingly, undermonopoly situation, firm’s demand curve alsoconstitutes industry’s demand curve. Demandcurve of the monopolist is also average revenue(AR) curve. It slopes downward. It means if themonopolist fixes high price, the demand willshrink. On the contrary, if he fixes low price, thedemand will expand. Under monopoly, averagerevenue & marginal revenue curves are separatefrom one another. Both slope downwards.

Following facts come to light as a result ofnegative AR & MR:

Demand rises with fall in price (AR). Hence, bylowering the price, a monopolist can sell more unitsof the commodity.

AR is another name of price per unit, i.e., P=AR.

With fall in price, both AR & MR fall, but falling MRis more. Rate of fall in MR is usually more than rate offall in AR.

AR is never 0, but MR may be 0 or even -ve.

Main objective of monopoly is: maximum profit from sale:

It can achieve in 2 ways: firm can either fix price

it can fix the quantity to be sold the customers.

A monopoly firm fixes the price and leave the quantity to be determined by demand of customer in market During fixing the price ,monopoly firm has 2 imp conderation : nature of demand

nature of supply of commodity.

Definition:

It is a market situation in which there are many seller of a particular product but the product of each seller is in some way differentiated in the mind of consumer s from the product of every other seller .

- Leftwitch

A: large number of sellers:

B:freedom of entry or exit:

C:non-price competition:

D:product differentiation:

A Monopolist avoid duplication of staff, equipments, expenses are reduced. this means lower price and consumers benefit .

When there is single producer ,scale of production become large. large output reduced cost…

A monopolist needs not spend huge sum of money on wasteful and competitive advertisement .this reduce selling cost.

Monopoly leads to unequal distribution of income.

It leads restriction in output. By limitation output, one can charge a high price and make more profits.

He limits output: By preventing new firm from entering into industry and this

limitation results in high price

By destroying a portion of article already produced.

By keeping productive resources partly idle.

Definition.

Features of oligopoly.

Types Of Oligopoly.

Classification of Oligopoly Market.

Price and Output Determination in Oligopolistic Market.

The Kinked Demand Curve.

Oligopoly and its Efficiency.

Advantages and Disadvantages.

Comparison b/w Monopoly and Oligopoly.

Oligopoly is a market structure featuring a small number of sellers that together account for a large fraction of market sales.

Oligopoly is derived from the Greek work

“olig” meaning “few” or “a small number.”

An oligopoly is a market structure characterized by:

Few firms

Either standardized or differentiated products

Difficult entry

Oligopoly is :

‘Competition among the few.’OR

‘Few sellers DOMINATE the market.’

•Fewness of sellers

•Seller interdependence

•Feasibility of coordinated action among ostensibly independent firms

•Price rigidity

Types of Oligopoly

On nature of product sold, oligopoly is of two types:

Homogeneous Oligopoly such as industries producing steel, aluminium,etc.

Heterogeneous Oligopoly or Differentiated Oligopolysuch as industries manufacturing automobiles,tvsets,computers,etc.

Classifications Of Oligopoly

Open and Closed Oligopoly Partial and Full Oligopoly

Perfect and imperfect Oligopoly

Syndicated and OrganisedOligopoly

Collusive and Non-Collusive Oligopoly

We have good models of price-output determination for the

structural cases of pure competition and pure monopoly. Oligopoly is

more problematic, and a wide range of outcomes is possible.

Some economists have assumed that oligopolists firms ignore interdependence which however helps in finding the equilibrium price and output of a particular oligopolist firm.

Second assumption is that oligopolist is able to predict the reaction pattern of the rivals.

Third assumption is that oligopoly firms realising their interdependence will pursue their common interest and will enter into the aggrementand work .

Howsoever, still we find that

fixing of price under oligopoly

market situation is very

difficult and involves a no. of

assumptions regarding

behaviour of oligopoly group

& reactions of rival firms to

price and output changes.

Many oligopolistic industries exhibit price rigidity or stability . Price rigidity may be due to following reasons:

(a): The oligopolistic industry has reached in a stage of maturity.

(b): Firms might have learnt by experience that price war is harmful & firms have found satisfactory price level.

(c): Firms have realised that they cannot increase their profit by lowering the price otherwise other firms will follow the price cut by the firm.

(d): A firm may compete by non-price competition rather than reducing the price.

quantity

$

D

P*

Q*

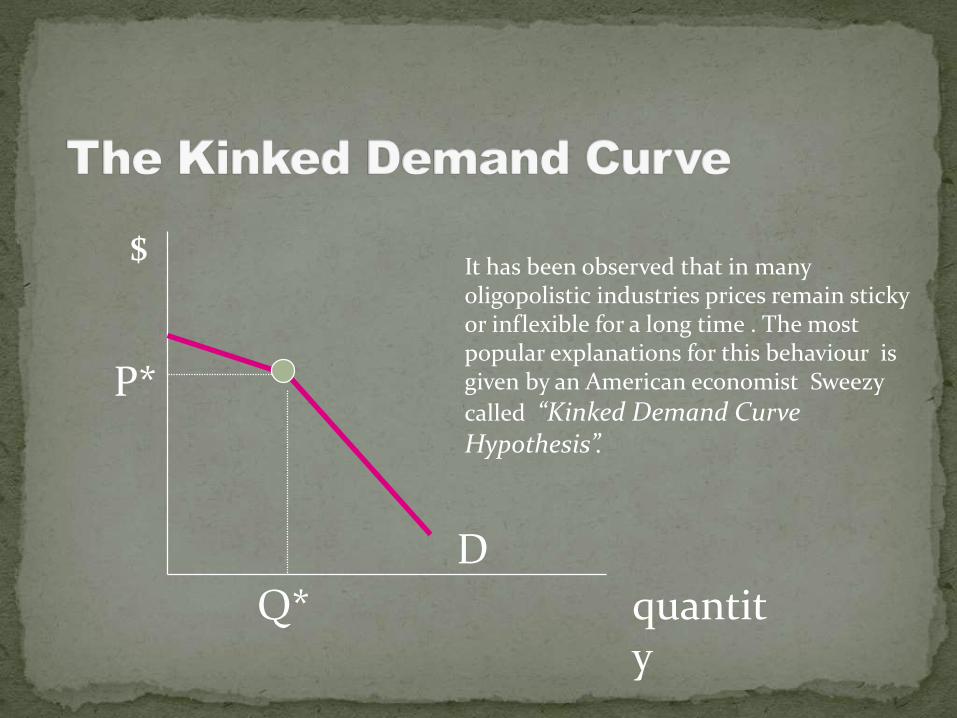

It has been observed that in many oligopolistic industries prices remain sticky or inflexible for a long time . The most popular explanations for this behaviour is given by an American economist Sweezy

called “Kinked Demand Curve Hypothesis”.

The kinked demand curve has following features:

The upper portion of demand curve is elastic.

The lower portion of demand curve is inelastic.

If the firm raises its price above P, it faces an elastic demand curve, payoff low

If the firm lowers its price below P, it faces an inelastic demand curve, payoff low

Different firms can have different MCs. As long as they fall with in the discontinuous MR, P will remain stable.

Output Effect < Price Effect for price movements with the discontinuous MR curve.

If MC increases enough, all firms raise their prices and the kink vanishes.

The question whether oligopoly affects economic welfare depends on whether or not they exercise market power over prices and production

In competition, the level of output produced is where P=MC or MB=MC. Hence, net benefits to society are maximized. Market prices as low as possible and respond to changes in market forces. This allows prices to help direct resource allocation.

Large firms with strong hold over the market are able to make huge profits.

Companies are capable of deciding prices as their own choice.

Dominant market players are able to make long-term profits.(As market don’t allow old business to increase their shares.)

High profits generated by companies can be used for innovation & development of products.

Helps in lowering average cost of production of goods.

Stable prices in market helps customers to plan and stabilize their expenditure.

There is only one dominating company,hencecustomers have no other choice.

Small business fail to establish themselves as a brand.

With presence of little competition ,dominant companies may not think of improving their products.

New firms can’t enter the market easily.

Firms cannot take independent decisions.

The micro-economic goal of fair wealth is not fulfilled as maximum profit is made by major players only.

Monopoly Oligopoly Meaning: One seller dominates the A small no .of sellers

entire market. dominate the industry.

Prices : High prices may be Moderate/fair charged. pricing.

Barriers A monopoly usually exist Barriers to entry are very entry : when barriers to entry are high because of economies

high. of scale.

Sources of Market making ability by Market making ability because

Power : virtue of being only viable of very few firms in the industry.seller in the industry.

Examples: Microsoft(OS),Google Health insurers,wireless carriers,beer,(web search),DeBeers, etc. media(TV,book publishing,movies)etc.

In monopoly, the level of output produced is where P>MC or MB>MC. Hence, net benefits to society are NOT maximized.

Market prices are higher and respond to changes in market forces. This allows prices to help direct resource allocation.

In oligopoly, the level of output is somewhere between the competitive and the monopolistic outcome. As the oligopolist produces closer to the competitive solution, the net benefits to society move closer to being maximized.

Duopoly Definition.

Duopoly exists when.

Best Response function.

Types of duopoly. Cournot Model.

Stackelberg Model.

Advantages.

Disadvantages.

Assumption.

Definition.

Definition.

Duopoly exists when.

Best Response function.

Types of duopoly. Cournot Model. Stackelberg Model.

Advantages.

Disadvantages.

Assumption.

An oligopoly with two firms.

OR

Control of a commodity or service in a given market by only two producers or suppliers.

No firm can gain by unilaterally changing its own output to improve its profit.

A point where the two firm’s best-response functions intersect.

Firm 1’s best-response function is

Similarly, Firm 2’s best-response function is (c2 is firm 2’s MC)

21

2112

1

2Q

b

caQrQ

12

1222

1

2Q

b

caQrQ

Cournot model Stackelberg model

1. Each firm chooses a quantity of output instead of a price.

2. In choosing an output, each firm takes its rival’s output as given.

The First firm’s best response function is:

y1*=30 – y2/2

The Second firm’s best response function is:

y2*=30 – y1/2

Taken together, these two best response functions can be used to find the equilibrium strategy combination for Cournot’s model.

The profit of one firm decreases as the output of the

other firm increases (other things equal).

The Nash equilibrium output for each firm is positive.

All strategy combinations that give the first firm the chosen level of profits is known as an indifference curve or iosprofit curve.

Profits are constant along the isoprofit curve.

y1* maximizes profits for the first firm given the second firm’s output of y2*.

Any strategy combinations below the indifference curve gives the first firm more profit than the Nash equilibrium.

The result above relates to the key assumption that the first firm’s profit increases as the second firm’s output decreases.

Q1

Q1M

r1

Q2C

Q1C

r2

Q2

Q1S

Q2S

Stackelberg Equilibrium

Note: Firm 1 is producing on Frim 2’s reaction function (maximizes its profits given the reaction of Firm 2)

Cournot equilibrium

123

Leader produces more than the Cournotequilibrium output. Larger market share, higher profits.

First-mover advantage.

Follower produces less than the Cournotequilibrium output. Smaller market share, lower profits.

Large firms having strong hold over the market are able to make huge profits as there are few players in the market.

Prevents new players from entering the market through several barriers of entry. Dominant market players usually make long-term profits in an oligopolistic environment.

High profits generated by the companies can be used for innovation and development of new products and processes.

Close competition between two firms.

Setting of prices may be advantageous for the firms, but if done unrealistically, it may prove to be a great disadvantage for consumers.

Creative ideas or plans of small businesses in the oligopolistic market fail to realize because they cannot overcome the control of major market players.

With the presence of little competition, dominant companies may not think of improving their products.

Two firms are producing and selling Homogeneous product.

The firms operate at zero cost of production.

Each firm has a aim of profit maximization.

Market demand is equally divided in the two firms.

Each firm demand curve is linear.

Each firm can not supply to entire market.