Embed Size (px)

Citation preview

Political Economy of Sovereign Wealth Fundsin the Oil Exporting Countries of the ArabRegion and especially the Gulf

Sara Bazoobandi and Jeffrey B. Nugent

ERF Workshop on Sovereign Wealth FundsWorld Bank, Washington D.C.September 9-10, 2016

Sovereign Wealth Funds (SWFs)Important institution for achieving multiple objectives: 1. Financial wealth fund for life after oil (future generations

and intergenerational equity)2. Means of investing in Physical and Human capital so as to

live up to the “Hartwick Rule” given that Oil exports sell off natural capital

3. Stabilizing expenditures in the face of fluctuating oil revenues, lowering excessive cyclicality and volatility

4. Supporting cooperation with other states and reducing conflict

5. Diversifying Assets to reduce income and credit risks and dependence on oil

6. Attracting foreign technology and investment for economic growth

7. Complement and coordinate public investment strategies and use of exisiting infrastructure within the region

Potentially SWFs seem like ideal institution for oil exporters to Avoid the “Oil Curse”• Save and invest for future, instead of excess cons.• Reduce volatility and procyclicality, a source of “oil curse”, in form of slower growth

• Badly needed industrial diversification away from dependence on oil

• Link economies to international financial markets• Especially important in all respects now, given a possibly long period of low oil prices and budgetary problems of MENA oil exporters in satisfying social contract and the gradual depletion of oil and gas reserves in some of them

Creation and Growth of Arab SWFs:Political Economy

• Early ones created before statehood, fostered monarchies, foreign role large

• Later ones: by high oil prices, copy cat, helpful for succession • Oil and Gas related SWFs :Over $4.2 trillion in 2015. Especially

rapid growth during 2000‐2008 and then again 2010‐2013 with high and increasing oil prices

• With high oil prices and global financial crisis 2008, these funds started to buy significant shares in banks and companies of west

• Seen as threat in the West, especially since the SWFs are government‐owned and non‐ transparent

• Some SWFs have responded positively since then

Three Phases of Growth: Rising Oil Prices

1. 1970s, 1980s Based on UK and US Model Very conservative But complementary institutions lacking. Poor budgeting

2. Norway 1990 (The Gold Standard of SWFs)3. 2000‐20084. 2010‐2013 5. Explosion of new Arab SWFs in those last two

periods. Seen as “modernist”, tied in to world finance, Some copy‐cat, rivalries even within royal families

In Practice: Political Economy of SWFs has often impeded such achievements • The sovereigns have wanted secrecy, not transparency,

leading to absence of assessment, sometimes corruption and inefficiency. Even after bringing in high quality staff, locals feel need to make decisions

• As conditions have changed, priorities among objectives have understandably changed, but making for inefficiencies

• Need for Maintaining the Social Contract between sovereign and citizenry has diverted attention from private sector to public sector and consumption, not investment (but this is not through or the fault of SWFs)

• Sovereigns as managers have had multiple responsibilities:tending to divert SWF to other objectives (from business to foreign affairs): – QIA under Sheikh Hamad bin Jassim Al Thani who was both

head , Prime Minister and Foreign Minister

Sheikh Hamad bin Jassin Al‐Thani Foreign Minister, Prime Minister, CEO QIA

Political Economy Shortcomings (cont.)• Unwillingness to delegate, final decisions often made by non‐

specialist kings and princes: lack of cooperation, trust between them and specialists (Clark, Dixon and Monk (2013)

• Lack of checks and balances: sometimes resulted in major mistakes, blocked proper assessments, and appropriate attribution of blame

• Lack of transparency: led to distrust of SWFs and failure to get enough of oil funds into SWFs and from SWFs into appropriate investments: (Algeria)

• Low scores on Open Budget and Resource Governance Indexes • Insufficient use of rules about putting oil revenues into SWFs and

for the use of the profits on their investments and control of government expenditures when oil prices high. This has weakened ability to accumulate assets, lower volatility,

• Interlinking of SWFs with Private Funds of Rulers and Insider elites has made for monopolistic regulations rather than ones fostering competition to assure international competitiveness

Political Economy Shortcomings (Cont.)

* Even though some SWFs have signed onto the Santiago Principles and the IFSWF, most have not lived up to them, leaving them with low scores on SWF Scoreboard, impeding performance* Much of this not the fault of the SWFs themselves but the broader institutional environment, Low OBS, Low scores of World Bank Governance indicators, Regulatory Quality, Rule of Law, V&A and Resource Governance Index* SWFs helped create and preserve Monarchies * Emphasis on Subsidies for fuel has undermined fund accumulation, distorted resource allocation, led to smuggling and lawlessness

Broader Political Problems in the GCC and Beyond

• Rivalries within the GCC and unequal power and resulting constraints, with Iran, drawn investments to other MENA Countries on political grounds, Religious minorities in oil areas

• Saudi Arabia with power over governance in Bahrain• Within UAE (a federation of Emirates in which each Emirate has

the rights to oil and gas) but Abu Dhabi the richest is called upon to bail out debts of ambitious and risk‐taking Dubai, its main rival for leadership within GCC

• Rivalries among members of ruling family for succession etc which has led to proliferation of SWFs especially in UAE and again almost always with great secrecy

• Civil, other Wars in Libya, Iraq, Sudan have impeded their SWFs

Some Achievements: Kuwait • Kuwait was the pioneer among SWFs in the world (at country level at least). KIB established in 1953 before state of Kuwait created

• It’s KIA also has generally been effective in investments . With its investment operation in London, KIA was able to finance the government during its invasion by Iraq and to pay off its debts after the Gulf War totalling over $100 billion

• Even so, Assets of about $600 billion in 2015 and Kuwait has also been an important funder of development in the region and beyond.

Achievements: Abu Dhabi• ADIA founded in 1976 has grown almost as rapidly as Norway’s to become perhaps the largest in Arab world with almost $800 billion by 2016

• ADIA has also played an important part in the agreement with the IMF and the West on the Santiago Principles for SWF behavior and a long time member of the IWG on SWFs

• It improved its scores substantially on SWF Scoreboard, nice organizational structure

Achievements: Algeria

• Desperate in 1990s after war for Independence, civil war, unrest, failed government programs, SWF set up Rev Regulation Fund (FRR) in 2000 and with certain rules on oil fund allocations.

• It’s assets grew rapidly to be the 2nd largest in Africa and the country’s debt was reduced sharply through 2010 But NOT SINCE THEN Assets have fall by 35% since 2013 Lack of transparency has undermined its use, led to huge fight between the Parliament and the executive. Unfortunate provision on secrecy

Achievements of Several Other Arab SWFs

• Mumtalakat (Bahrain), Mabadala (Abu Dhabi) – High Scores on Transparency, SWF Scoreboard

• Saudi Arabia’s SAMA For. Holding: not transparent but reportedly very conservative policies and risk management . – Royal family not the managers $686 Billion Assets by 2015, not

far below Norway’s $878 billion Will SA’s PIF become the pillar of its Vision 2030 with $1.3Trillion linking investments to attract FDI, tech, industries? A Fantasy of McKenzie?

• Qatar QIA established only in 2005; – more aggressive and strategic in investments (World Cup)

diversification though perhaps only of “trophy” type. Assets well over $250 billion by 2015 (though very non transparent)

Scandals and Setbacks: Do the SWFs and their leaders learn from these?

• ADIA example : A founding shareholder in BCCI in Luxemburg which then expanded into many countries in 1970s and 1980s. As it got into trouble in UK, US, France, Lux., its treasury was transferred to Abu Dhabi. Major scandals, including illicit entertainment . Major financial loss for ADIA– Result, at least at that time, it reinforced secrecy policy

• KIA investments in Spain including a Rio Tinto Explosives $5 billion loss and again sex scandal – Led to rebellion by Parliament and efforts to change rulers

Current Pressures: Learn from Mistakes? • Libya Investment Authority Very Low SWF Scoreboard scores, grew rapidly 2000‐8 but lost over $2 billion in ill‐fated Goldman Sachs and Societe Generale deals. Left it with only embarrassing option to sue these firms for not sufficiently teaching LIA about the options (admitting their own ignoran

• Oman’s SGRF An Exception of Positive response? Al‐Saidi PhD Dissertation disclosures 2012 – followed by SGRF actions – (a) 2014 Whistle‐Blowing Policy, – (b) 2015 applied for and received full membership in IFSWF, (c ) raised its transparency score

Challenges Ahead• With the shale and drilling revolutions underway, low oil prices could be long‐lasting

• With rising youth bulge and Female LFPR on rise, employment and diversification objectives of SWFs likely to continue to be more important

• Need for higher tech non‐oil private sector to attract nationals with higher wage rates and this likely to help in attracting FDI; these need to be internationally competitive

• Some countries running low on energy reserves• Therefore reforms are urgent!

Reforms NeededWithin the SWFs1. Improve Transparency and SWF Scoreboard Scores

a. This should increase accountability and assessment of investment programs

b. Should serve as a positive signal to other investors and to firms receiving funding to improve their performance 2. Move away from Monarchs as SWF heads and decision

makers, should reduce the subserviance of SWF goals to other objectives

3. Introduce more in the way of Whistleblower Protection to reduce likelihood of corruption

4. Join the IFSWF to get benefits of best practice tips, Perhaps develop a Regional Component of this

Reforms NeededBeyond the SWFs1. Improve the transparency between oil

companies and government: Join in EITI2. Improve budgeting procedures and openness:

Raise OBS scores. Increase comprehensiveness.3. Introduce Rules (as in Chile) based on oil price 4. Decrease Subsidies and Government Cons.5. Improve coordination between SWF

Investments in Region and Other Public Expenditures and Infrastructure

More Reforms Beyond the SWFs

5. Provide incentives to Firms and FDI to bring in higher technology 6. Lower artificially high Government Wage Rates to encourage nationals to private sector 7. Change Labor Laws so as to be somewhat tighter than they have been, avoid charges of abuses of foreign workers and improve likelihood of attracting high quality investors and nationals to the private sector8. Encourage entrepreneurship, FLFPR

Conclusion

• SWFs could play very important role in filling important objectives

• In some respects they already have, and some improvement over time is visible

• But, scandals, large losses, leave much room for improvement, especially considering that amount of oil rents has had no effect on Assets

• Low Oil Price Era makes SWF reforms more urgent. The needed reforms go well beyond SWFs themselves

Some Illustrative Evidence

• Cross‐SWF Regressions in 2008 and 2015 with Small SWF Sample (no More than 20 MENA, C.Asia but also including Norway’s for:– Transparency (Linaburg‐Maduell Index) – SWF Scoreboard and its Components (this index is rather minimal compromise, well far short of what was desired by west

– Assets Accumulated Huge Gaps between Institutional indexes between SWFs of Norway and Arab or other MENA countries

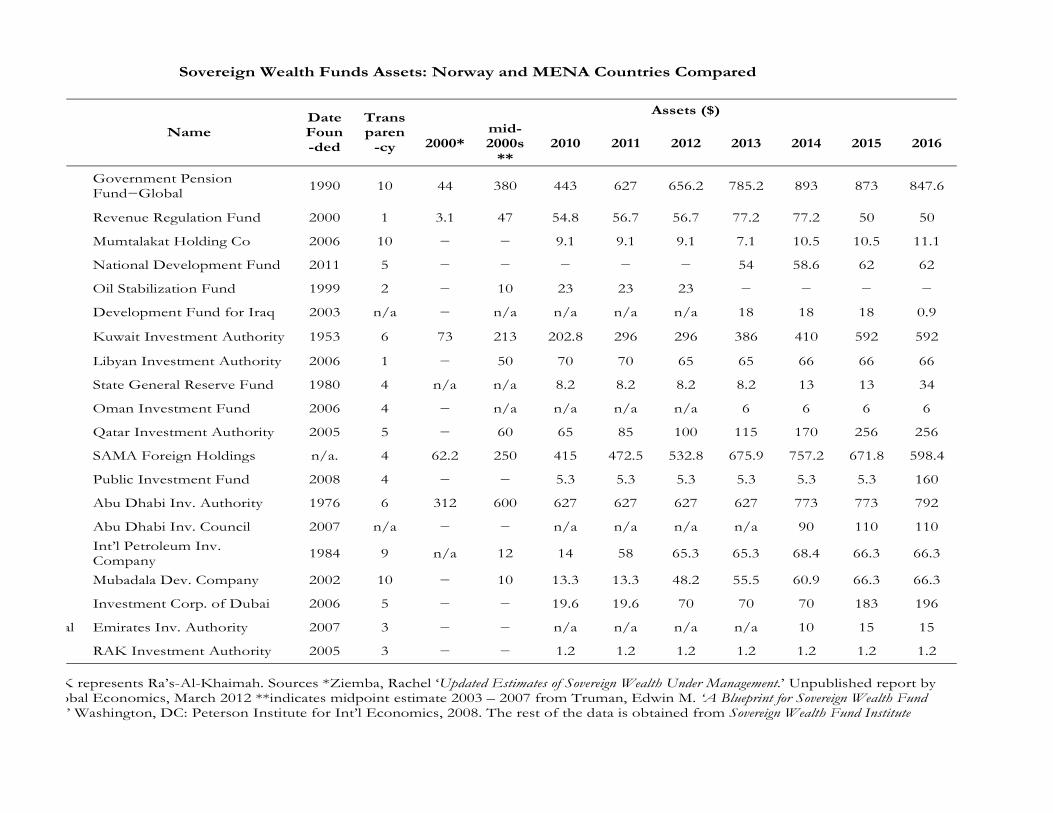

Sovereign Wealth Funds Assets: Norway and MENA Countries Compared

Name Date Foun-ded

Transparen

-cy

Assets ($)

2000*mid- 2000s

** 2010 2011 2012 2013 2014 2015 2016

Government Pension Fund−Global 1990 10 44 380 443 627 656.2 785.2 893 873 847.6

Revenue Regulation Fund 2000 1 3.1 47 54.8 56.7 56.7 77.2 77.2 50 50

Mumtalakat Holding Co 2006 10 − − 9.1 9.1 9.1 7.1 10.5 10.5 11.1

National Development Fund 2011 5 − − − − − 54 58.6 62 62

Oil Stabilization Fund 1999 2 − 10 23 23 23 − − − −

Development Fund for Iraq 2003 n/a − n/a n/a n/a n/a 18 18 18 0.9

Kuwait Investment Authority 1953 6 73 213 202.8 296 296 386 410 592 592

Libyan Investment Authority 2006 1 − 50 70 70 65 65 66 66 66

State General Reserve Fund 1980 4 n/a n/a 8.2 8.2 8.2 8.2 13 13 34

Oman Investment Fund 2006 4 − n/a n/a n/a n/a 6 6 6 6

Qatar Investment Authority 2005 5 − 60 65 85 100 115 170 256 256

SAMA Foreign Holdings n/a. 4 62.2 250 415 472.5 532.8 675.9 757.2 671.8 598.4

Public Investment Fund 2008 4 − − 5.3 5.3 5.3 5.3 5.3 5.3 160

Abu Dhabi Inv. Authority 1976 6 312 600 627 627 627 627 773 773 792

Abu Dhabi Inv. Council 2007 n/a − − n/a n/a n/a n/a 90 110 110 Int’l Petroleum Inv. Company 1984 9 n/a 12 14 58 65.3 65.3 68.4 66.3 66.3

Mubadala Dev. Company 2002 10 − 10 13.3 13.3 48.2 55.5 60.9 66.3 66.3

Investment Corp. of Dubai 2006 5 − − 19.6 19.6 70 70 70 183 196

al Emirates Inv. Authority 2007 3 − − n/a n/a n/a n/a 10 15 15

RAK Investment Authority 2005 3 − − 1.2 1.2 1.2 1.2 1.2 1.2 1.2

K represents Ra’s-Al-Khaimah. Sources *Ziemba, Rachel ‘Updated Estimates of Sovereign Wealth Under Management.’ Unpublished report by obal Economics, March 2012 **indicates midpoint estimate 2003 – 2007 from Truman, Edwin M. ‘A Blueprint for Sovereign Wealth Fund ’ Washington, DC: Peterson Institute for Int’l Economics, 2008. The rest of the data is obtained from Sovereign Wealth Fund Institute

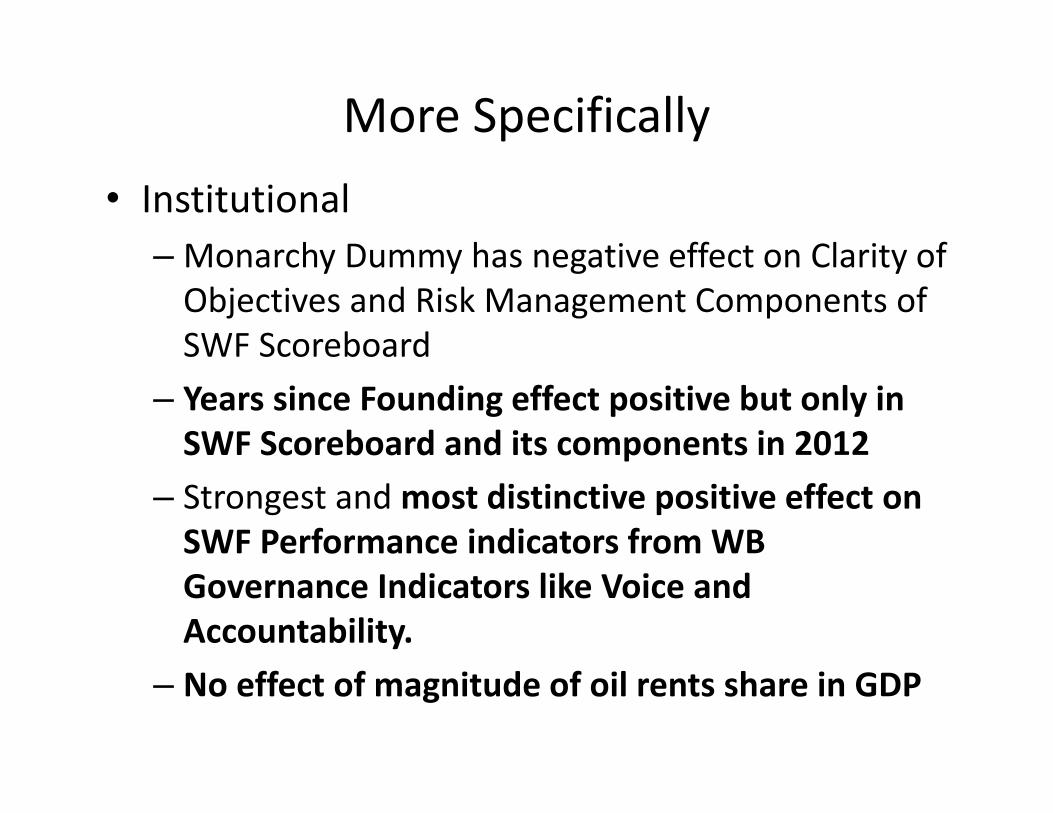

More Specifically• Institutional

–Monarchy Dummy has negative effect on Clarity of Objectives and Risk Management Components of SWF Scoreboard

– Years since Founding effect positive but only in SWF Scoreboard and its components in 2012

– Strongest and most distinctive positive effect on SWF Performance indicators from WB Governance Indicators like Voice and Accountability.

– No effect of magnitude of oil rents share in GDP

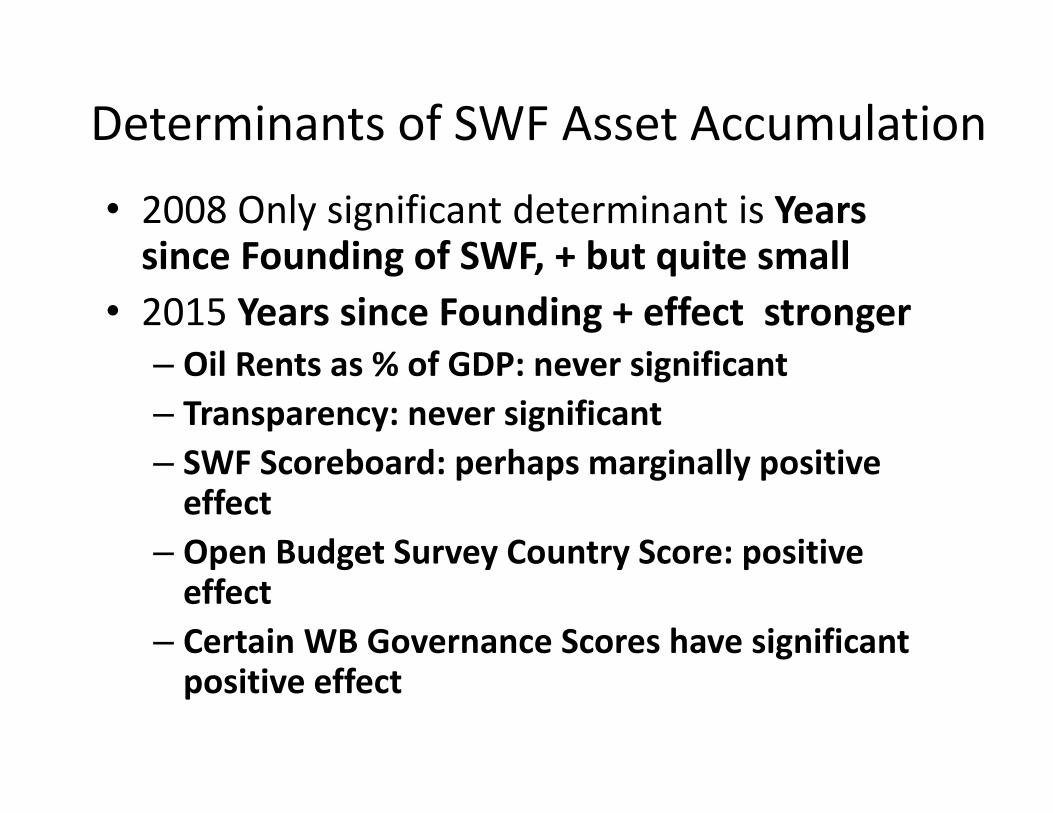

Determinants of SWF Asset Accumulation• 2008 Only significant determinant is Years since Founding of SWF, + but quite small

• 2015 Years since Founding + effect stronger– Oil Rents as % of GDP: never significant – Transparency: never significant– SWF Scoreboard: perhaps marginally positive effect

– Open Budget Survey Country Score: positive effect

– Certain WB Governance Scores have significant positive effect

Appendix: Linaburg‐Maduell Transparency Index

Point Principles of the Linaburg‐Maduell Transparency Index

+1 Fund provides history including reason for creation, origins of wealth, and government ownership structure

+1 Fund provides up‐to‐date independently audited annual reports

+1 Fund provides ownership percentage of company holdings, and geographic locations of holdings

+1 Fund provides total portfolio market value, returns, and management compensation

+1 Fund provides guidelines in reference to ethical standards, investment policies, and enforcer of guidelines

+1 Fund provides clear strategies and objectives

+1 If applicable, the fund clearly identifies subsidiaries and contact information

+1 If applicable, the fund identifies external managers

+1 Fund manages its own web site

+1 Fund provides main office location address and contact information such as telephone and fax

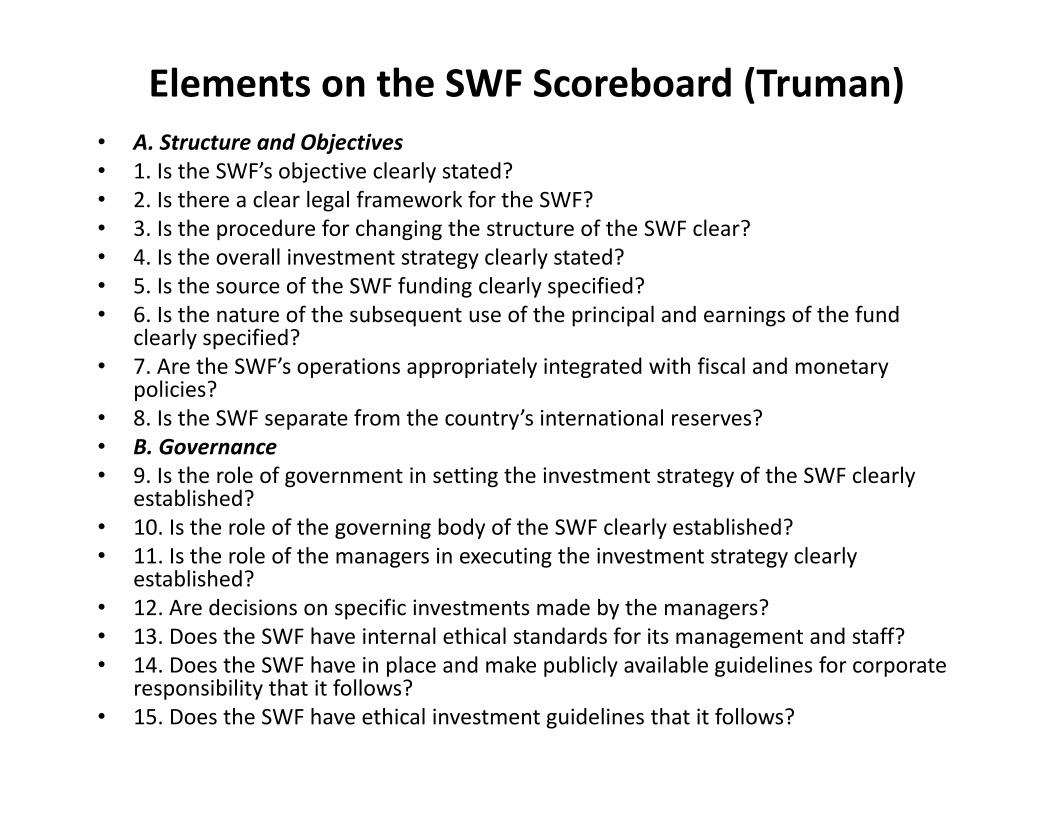

Elements on the SWF Scoreboard (Truman)• A. Structure and Objectives• 1. Is the SWF’s objective clearly stated?• 2. Is there a clear legal framework for the SWF?• 3. Is the procedure for changing the structure of the SWF clear?• 4. Is the overall investment strategy clearly stated?• 5. Is the source of the SWF funding clearly specified?• 6. Is the nature of the subsequent use of the principal and earnings of the fund

clearly specified?• 7. Are the SWF’s operations appropriately integrated with fiscal and monetary

policies?• 8. Is the SWF separate from the country’s international reserves?• B. Governance• 9. Is the role of government in setting the investment strategy of the SWF clearly

established?• 10. Is the role of the governing body of the SWF clearly established?• 11. Is the role of the managers in executing the investment strategy clearly

established?• 12. Are decisions on specific investments made by the managers?• 13. Does the SWF have internal ethical standards for its management and staff?• 14. Does the SWF have in place and make publicly available guidelines for corporate

responsibility that it follows?• 15. Does the SWF have ethical investment guidelines that it follows?

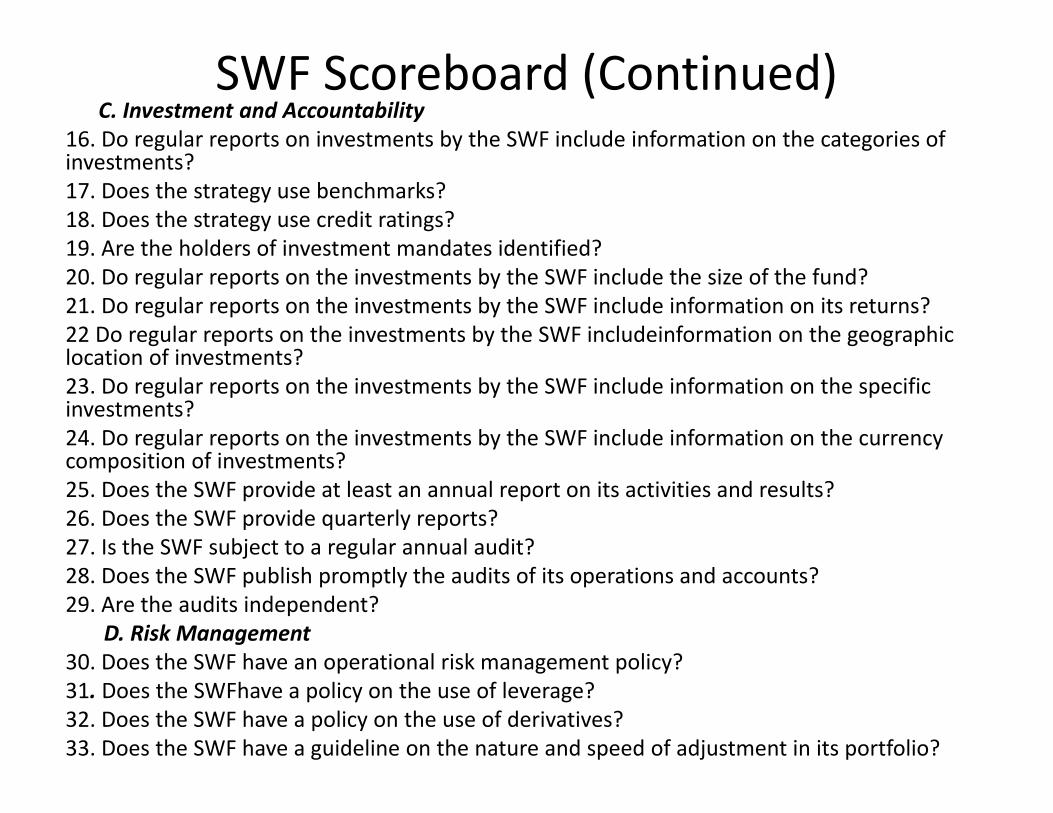

SWF Scoreboard (Continued)C. Investment and Accountability

16. Do regular reports on investments by the SWF include information on the categories of investments?17. Does the strategy use benchmarks? 18. Does the strategy use credit ratings? 19. Are the holders of investment mandates identified?20. Do regular reports on the investments by the SWF include the size of the fund?21. Do regular reports on the investments by the SWF include information on its returns?22 Do regular reports on the investments by the SWF includeinformation on the geographic location of investments?23. Do regular reports on the investments by the SWF include information on the specific investments?24. Do regular reports on the investments by the SWF include information on the currency composition of investments?25. Does the SWF provide at least an annual report on its activities and results?26. Does the SWF provide quarterly reports?27. Is the SWF subject to a regular annual audit?28. Does the SWF publish promptly the audits of its operations and accounts? 29. Are the audits independent?

D. Risk Management30. Does the SWF have an operational risk management policy? 31. Does the SWFhave a policy on the use of leverage?32. Does the SWF have a policy on the use of derivatives?33. Does the SWF have a guideline on the nature and speed of adjustment in its portfolio?