Embed Size (px)

Citation preview

CHAPTER I

INTRODUCTION

Background of the Study

In the best-seller book of Art Williams entitled “Common Sense” (1993), he

pointed out that having background knowledge on financial literacy especially at an early

age is vital for it is most likely for a person who is financially literate to be successful in

managing his finances for the future. He also added that planning and investing is nothing

but a simple mathematical problem, all that a person need to become financially

independent eventually is to understand how money works.

Rooij, Lusardi, and Alssie (2007), found out that those who are exposed to

financial education in school or at a work place tend to save more. It means that the

earlier a person is educated with financial management, the more advanced with financial

background he may possess. Furthermore, Lusardi and Mitchell (2007) showed that those

who display low financial literacy are less likely to plan for the future and as a result,

gather much less wealth.

It was confirmed in the research work of Stango and Zinman (2007) that

individuals who incorrectly calculate interest rates out of stream of payments result to

borrowing more and acquiring lower amount of wealth. Agarwal et al. (2007) showed

that financial mistakes are prevalent among the young and elderly. When one lacks the

knowledge of financial management there is a greater chance to have difficulty in

managing his finances wisely in the near future. Therefore, the concept of financial

literacy goes far further than knowledge on financial matters, it also involves the way this

1

knowledge affects the behavior and attitudes of a person in making decisions (Leitao,

2012).

Economic system today is far more complex compared to the generation before,

where a simple awareness of how to sustain a savings account at banks was more than

sufficient. But at the present, consumers have to distinguish a wide array of financial

merchandises and services available in the contemporary financial market (Ramasawmy

et.al, 2013). Because of that, the need to improve financial literacy among individuals is

becoming increasingly significant. In fact countries such as the United State of America,

Japan, Canada, and United Kingdom introduced financial literacy subject in their

curriculum (http://en.wikipedia.org/wiki/Financial_literacy). In the Philippines, it is only

recently that the Department of Education and Hong Kong-based Prudential Corporation

Asia signed a memorandum of agreement to incorporate financial literacy on the Basic

Education Curriculum in 2012 (Horario, 2013).

Although Filipino’s rating in financial literacy has risen (Vallecera, 2013), it is

still relatively low. It has been found out that only 8% Filipinos who claim to be

specialist in financial management get more than 80% correct answers in financial

literacy quiz conducted by Sun Life of Canada (Dumlao, 2013).

Though there has been no evidence that a heightened financial literacy in an

individual can change his financial behavior such as saving, it is important to note that

saving will most likely make a person afford a good future. According to NEDA as cited

by Tiongzon (2011) on his article in the Philippine Daily Inquirer, savings rate in the

Philippines is one of the lowest around the world. The report place the savings rate

2

among Filipinos between 12 and 16 percent which is very far from 30 percent as

recommended by experts. This may be explained by the first world consumerism lifestyle

among Filipinos.

Statement of the Problem

This study was conceptualized in order gauge the level of awareness on financial

literacy among BSEd Social Studies majors.

Specifically, this study sought answers to the following questions:

1. What is the profile of BSEd Social Studies major students in terms of:

a. Age;

b. Gender;

c. Civil status;

d. Year level;

e. Place of residence (urban/rural);

f. Housing arrangement;

g. Benefactor; and

h. Average Weekly Allowance

2. How do the Social Science majors assess their knowledge in financial

literacy and their financial habits?

3. What is the financial attitude and behavior of the Social Studies majors?

4. Who influenced them in their financial management?

5. How do the Social Science majors fare in the basic financial literacy quiz?

3

Significance of the Study

This study may be meaningful and beneficial to the following:

To the students. It will help them realize how important it is to make wise

financial decisions and to be financially literate so that they will be able to improve their

present and long-term financial well-being.

To the teachers. It will be a great opportunity to reinforce their teaching

approach regarding topics about allocation of resources especially in economics related

subjects.

To curriculum-makers. This study will provide a database for the curriculum-

makers to design curriculum that will cater to the students’ need to be educated in terms

of financial management and related topics.

To future researchers. This study will serve as guide for future researchers to

conduct further researches that are related to financial literacy.

Scope and Delimitation of the Study

This study will look into the level of awareness of the BSEd students of Leyte

Normal University about financial literacy.

Due to financial and time constraints, this study is only limited to the BSEd

second year to fourth year Social Studies major of Leyte Normal University in the second

semester of school year 2013-2014.

4

Research Assumptions

This study will try the following assumptions:

1. Respondent’s age, gender, civil status, class standing, place of residence and

housing arrangement has nothing to do with the level of their financial literacy.

2. Majority of the Social Studies major students will have a high score in the

financial literacy quiz.

Theoretical Framework

The foundation of this study is anchored on Conventional Economic Approach

cited by Lusardi and Mitchell (2007).

Learning is evident when the behavior of the person has changed. Conventional

Economic Approach explains why a person’s chance to be financially independent in the

future is high if he is financially literate than those who are not. The approach implies

that a fully rational and well-informed individual consume less wealth for the future.

Conceptual Framework

This study was conceptualized in order to determine the level of awareness on

financial literacy among BSED Social Studies major students. Further, this study is

presented using the paradigm below.

5

Fig. 1. Paradigm showing the relationship between Independent, Intervening, and Dependent Variables

6

Independent Variable

(Background on Financial Literacy)

Intervening Variable

Part I: Demographic Profile

Part II: Self-assessment Regarding Financial Literacy

Part III: Financial Attitude and Behavior

Part IV: Influences Part V: Basic

Financial Literacy Quiz

Dependent Variable

(Level of Awareness on Financial

Literacy)

Definition of Terms

Basic Financial Literacy Quiz. These are the set of questions of cover topics

ranging from interest rates, interest compounding, inflation, time value of money, and

money illusions. (Lusardi et.al. 2007)

Benefactor. This term refers to a person that send the respondent to school.

Budgeting. This term refers to practical use of money for the future.

Compounding. The ability of a deposit to generate earnings, which are then

redeposit in order to generate their own earnings.

(www.investopedia.com/terms/i/compounding.asp)

Financial Literacy. It is the combination of awareness, knowledge, skills,

attitude and behavior necessary to make sound financial decisions and ultimately

achieved and individual’s financial well-being (OECD’s definition).

Financial Management. Means the efficient and effective way of managing

money of an individual.

Housing Arrangement. It describes where the respondents live in, whether on-

campus or off-campus.

Inflation Rate. The rate at which the general level of prices for goods and

services are rising, and subsequently, purchasing power is falling.

(www.investopedia.com/terms/i/inflation.asp)

Interest Rate. The amount of profit, expressed as a percentage of deposit.

7

Nominal Value of Money. The stated value of money in numerical term.

True Value. Is obtained by removing the effect of price level changes from the

nominal value of time (www.investopedia.com/terms/r/real-value.asp).

8

CHAPTER II

RELATED LITERATURE AND STUDIES

Navigating in today’s world financial system needs a person to be equipped with

adequate financial knowledge that will help him avoid financial disarray.

In the United Kingdom, the government is trying to enhance the financial

capabilities of its people especially those who have less income and people with learning

disabilities (www.ifie.org/index.php/resources-clearinghouse/49).

In Australia, they developed the National Financial Literacy Strategy to provide a

national direction to improve financial literacy among its citizens. They also established a

National Consumer and Financial Literacy Taskforce in 2004, which recommended the

establishment of the Financial Literacy Foundation in 2005. After three years, the

functions of the Foundation were transferred to the Australian Securities and Investments

Commission (ASIC). The Australian Government also runs a range of programs to

improve the financial literacy of its Indigenous population, particularly those living in

remote communities (Clitheroe, 2004).

Financial literacy between adults and among teens and young adults vary through

their behavioral patterns. In the United States, adults have low sense of accountability. It

was observed that 28% of adults failed to pay their bills on time. However, even 65% of

adults wanted to be more financially literate, only few undertake the steps to refine their

financial skills. Only 64% of adults are convinced that financial practice is more

significant than physical practice, yet behind this percentage, only 18% possesses, to

incorporate the former as a part of their routine. Like adults, teens and young adults are

also experiencing the same thing. Between 16-18 years old individuals, 77% of them

9

believe that they are “financially savvy” yet only 35% are able to do some bank

statement activities and only 31% of then knows how credit card interest and fees work.

According to Annamaria Lusardi in her speech before the U.S. Senate Committee

on Health, Education, Labor and Pension last April 24, 2013, one of the reasons why

American government or any government around the world should launch financial

literacy efforts among their schools has something to do with equality. Studies show that

in terms of gender, more men are financially literate than women. According to Charles

Schwab & Co., Inc as cited by Llewellyn (2012) more men than women knows how

credit card interest and fees work.

Financial education programs in the United States of America were implemented

over years. Some of its States designed approaches like financial counseling that

improves and advices financial decision-making among Americans (Agarwal, et.al.

2011). Assembly Bill 166 of California obliged the state to integrate financial literacy in

the existing curriculum. In anent to this, Assembly Bill 391 or Common Cents

Curriculum Act was enacted in 2013 which require developing a one-semester

instructional program entitled consumer economics for post-secondary education before

July 1, 2015 (http//:www.ncsl.org/research/financial-services-and-commerce/financial-

literacy-2013-legislation.asp).

In Singapore, their government had made financial literacy program for their

schools. Since financial education seems to be a large issue to most students, the

National Institute of Education or NIE handed over an educational training for teachers

through the Citi-NIE financial literacy hub for teachers being funded by a grant from Citi

Foundation. These training workshops for teachers enable them to be equipped in

10

engaging pedagogy and idea to incorporate financial literacy in their curriculum. It also

provides an understanding in regards to different factors that motivate students to acquire

financial literacy skills and knowledge. To support this school task force, mentoring is

given. Schools benefits from the hubs mentoring model where trainers are guided and

empowered a group of teachers called the tasked force to made plans on how to

implement financial education in their curriculum. Currently there is an ongoing research

into the effectiveness of the program implemented (www.singaporeqp.com)

In Romania, United Nations Development Project (UNDP) disclosed that of about

9 million of the Romanian Citizens aged 18-45 years old only 14% of them are totally

financial literate and 65% find it difficult to cover their daily needs. That is why UNDP

came up a project that aims to facilitate the financial education of Romanian citizens

which would contribute to Romania’s economic and social development. The impact

analysis of the project will be evaluated by pretest and posttest and also through an in-

depth questionnaire on financial literacy. The outcome of the project and the result of the

impact analysis will be provided to the government as a policy recommendation on a

financial awareness of the Romania’s citizens (www.undp.ro/projects.php?

project_id=72).

In Peru, the state has offered financial training with credit, microfinance

institutions as a way to better management for their loans repayments and avoid debt.

According to Chong, Karlan and Valdivia, (2010), one way to deliver financial literacy

and to minimize educational cost is by using of Information and Communication

Technologies or ICT’S such as radio and television and social networking sites as

mediums of financial education for Peruvian citizens.

11

In Bangladesh, financial literacy project was launched last May 20, 2013 to bring

large communities under banking services. Top official said that the concept of financial

literacy spread across the world following the global financial crisis to ensure financial

stability. Financial literacy program since then, has been designed by giving importance

on the needs of the people, who still remain unbanked, including school and college-

going students, women, poor rural and urban people, and aged citizens. The project also

aims at bringing under the financial services the people who thinks they do not need to

go to banks. Bangladesh Bank is working for making a web link under this project to

provide information about what people will have to do for getting the services

(www.dhakatribune.com).

In Philippines, according to the survey on financial literacy among Filipinos

conducted by Citi Bank, they found out that there is improvement in the Filipinos when it

comes in financial matters. Filipinos are now said to be more financially literate. They are

learning the basics in budgeting, planning and savings. Survey shows that nine out of 10

Filipinos create a budget on a monthly basis, 65% shows importance to stick with their

budget and 63% are on track on their retirement plans. This survey also found the

average financial literacy score across Asia has pushed past the 50 point marked at 53.2

%, it only shows a positive financial future for Filipinos. When it comes to savings, 44%

reported that they save a portion of their salary and 57% believe that they have enough

insurance for themselves and their families (Vallecera, 2013). Last February 7 and 8,

2012 a National Summit was held with a gathering of about 100 partner-educators,

representatives of various cooperatives under the umbrella of the National Confederation

12

of Cooperatives (NATCCO). Through Aflauton Program, member cooperatives will help

educate children in financial management (Samson, 2012).

It has been the state’s ideal goal to improve economic development among

Filipino people (see Article XII of the 1987 Constitution), that is the reason why senator

Juan Edgardo Angara filed the senate bill 201 also known as Financial Literacy Act of

2013 where it pushes the inclusion of entrepreneurial and financial literacy education as

an integral part of secondary education which will be a great help towards the financial

literacy of the students (Torres, 2013).

13

CHAPTER III

METHODOLOGY

This section contains a discussion of the research design, research locale, research

respondents, research instrument, data collection technique, data analysis, statistical

treatment and methods of scoring.

Research Design

The quantitative survey method of research was utilized in this study since this

study intends to determine the level of awareness on financial literacy among BSEd

Social Studies major students. It looked into the extent the self-assessment of the

respondents regarding financial habits, and attitudes and behavior. It also determined

where the students get influence as regards financial literacy.

Research Locale

This study was conducted within the premises of Leyte Normal University. It is

one of the universities in Eastern Visayas that is strategically located at P. Paterno Street,

Tacloban City. Whatever results gathered do not necessarily reflect the level of

awareness of the whole population of the LNU students.

Research Respondents

The respondents of the study were the population of BSEd Social Science majors

in Leyte Normal University, Tacloban City during the second semester of school year

2013-2014. The total population of Social Studies majors from 2nd year to 4th year is 89

students excluding the researchers.

14

Sampling Procedure

The researchers utilized purposive sampling procedure in conducting the study.

The main goal was to focus solely on BSEd Social Studies major students in order to

determine their level of awareness on financial literacy.

Research Instrument

As the primary tool for the data gathering, the investigation used a survey

questionnaire. Some questions were obtained from different research questionnaires

outside the country while some questions were modified by the researchers taking into

consideration the local realities. The survey results were tabulated, analyzed and the level

of awareness on financial literacy among the respondents gauged.

The survey questionnaire is composed of 45 items. The questionnaire is divided

into five parts namely: Part I: Demographic Profile, Part II: Self-assessment Regarding

Financial Literacy and Habits, Part III: Financial Attitude and Behavior, Part IV:

Influences, and Part V: Basic Financial Literacy Questions.

Part I: Demographic Profile

This part of the questionnaire was designed to capture the profile of each

respondent. It includes the class standing, gender, civil status, place of residence,

benefactor, and housing arrangement of the respondents.

Part II: Self-assessment Regarding Financial Literacy and Habits

This part of questionnaire measures the respondent’s self-awareness on financial

literacy. It includes their personal understanding on financial literacy. This part was also

determined if the respondent has attended any lectures or seminars on financial literacy, if

15

he has a budget and whether he is saving or not. The second and third item in this part of

the questionnaire was obtained from the Senior Honor Thesis of Llewellyn (2012).

Part III: Financial Attitude and Behavioral Statements

This part determines the respondent’s attitude and behavior in managing his

finances. This part of the questionnaire was acquired from Financial Literacy Survey

Report, 2012 of Janke and Trechter.

Part IV: Influences

This part determined how much did respondents learn about financial

management from the influencers such as; parents, friends, school, books, media, job, life

experiences, internet, informal seminars or class, and financial planners. It also included

how often the respondents are being influenced or how often the respondent discusses

financial matters with the influencers (enumerated above). This part of the questionnaire

was acquired from Financial Literacy Survey Report, 2012 of Janke and Trechter.

Part V: Basic Financial Literacy Questions

This part attempts to assess the basic financial literacy of the respondent that

cover topics ranging from interest compounding to the effects of inflation, discounting

and nominal versus true value of money. This part of the questionnaire was adopted from

the working paper of Van Rooij, et al. (2007).

Data Collection Technique

The questionnaires were administered personally by the researchers to the

respondents. They were asked to answer the questions honestly. The researchers

immediately retrieved the questionnaires. The results gathered were the basis for data

analysis.

16

Data Analysis/ Statistical treatment

The data which were collected from the various respondents were classified,

tabulated and subjected to statistical analysis in order to formulate objective

interpretation in terms of research findings, conclusions and recommendations. Specified

instruments were used to gather data and appropriate statistical tools were employed.

This was a fact-finding study with an adequate and accurate interpretation of the data. It

described the status of awareness on financial literacy among BSEd Social Science

majors in Leyte Normal University, Tacloban City during the second semester of school

year 2013-2014.

Relative Frequency (%) = n/N x 100

Where:

% = Relative Frequency of Percentage

n = Number of Responses/Question

N = Total Number of Respondents

The researchers also utilized the weighted mean formula in giving interpretation

to the gathered data in the Part II item 1, Part II item 6, Part III, Part IV item A, and Part

IV item B of the questionnaire.

Weighted Mean = ∑ fx / N

17

Where:

f = the frequency or the number of responses on each question or

indicator

x = each indicator or scale

N = the total number of respondents

∑ = the summation or total

METHODS OF SCORING

The following are the ranges to interpret the data gathered using the qualitative

description adopted in this study.

Part II item 1 of the questionnaire

Attainment of Objectives Qualitative Description

Range:

4.50 – 5.00 Very High

3.50 – 4.49 High

2.50 – 3.49 Moderate

1.50 – 2.49 Low

1.00 – 1.49 Very Low

18

Part II item 6 of the questionnaire

Attainment of Objectives Qualitative Description

Range:

3.50 – 4.00 Very Prepared

2.50 – 3.49 Prepared

1.50 – 2.49 Somewhat Prepared

1.00 – 1.49 Not Prepared

Part III of the questionnaire

Attainment of Objectives Qualitative Description

Range:

4.50 – 5.00 Very True of Me

3.50 – 4.49 True of Me

2.50 – 3.49 Sometimes Not True of Me

1.50 – 2.49 Not True of Me Most of the Time

1.00 – 1.49 Not at All True of Me

19

Part IV item A of the questionnaire

Attainment of Objectives Qualitative Description

Range:

4.50 – 5.00 A Lot

3.50 – 4.49 Enough

2.50 – 3.49 Not so Much

1.50 – 2.49 Little

1.00 – 1.49 None

Part IV item B of the questionnaire

Attainment of Objectives Qualitative Description

Range:

4.50 – 5.00 Weekly

3.50 – 4.49 Twice per Month

2.50 – 3.49 Every Few Months

1.50 – 2.49 Once per Year

1.00 – 1.49 Never

20

CHAPTER IV

PRESENTATION, ANALYSIS, AND INTERPRETATION OF DATA

The data gathered using the researcher-modified survey questionnaire are herein

presented, analyzed, and interpreted.

Table 1 shows the summarized tabular presentation of the respondents’ profile. It

can be gleaned that majority of the respondents, in fact 60 or 70.6% have reached legal

age. The row for gender signifies that most Social Studies specializers are female.

Though the researchers found that there is a difference between the mean score of males

and females in the basic financial literacy quiz, the difference is not statistically

significant which means that gender of individual has nothing to do with financial

literacy. Respondents were mostly single at 82 out of 85 or 96.5%. Responses from those

who live in the rural areas comprise of 40 respondents or 46.9% of the sample, while 34

or 40% of the respondents came from the urban areas. It is also worth noting that 11 or

almost 13% of the respondents either answered don’t know or didn’t respond at all to the

question related to their place of residence. Further, most of the respondents are either

living on the homes with their parents at 38 out of 85 or 44.7% or renting on boarding

houses at 35 out of 85 or 41.2%. Sixty-two (62) or 72.9% of the respondents are being

financed in school by their parents while 9 of them or 10.6% are scholars. Seven (7) or

(8.2%) of the respondents are being sent to school by their relatives while 2 or 2.4% of

them answered others. Lastly, almost half of the respondents at 42 out of 85 or 49.4%

have 101 to 500 pesos average weekly allowance while a significant number of

21

respondents at 30 or 35.3% who are enjoying their average weekly allowance that reaches

501 to 1000 pesos.

Table 1 Respondents’ Profile

Age17 18 19 20 21 24 27 28 No Response

f % f % f % f % f % f % f % f % f %

2nd Year 7 8.2 21 24.7 0 0 2 2.3 0 0 0 0 0 0 0 0 9 10.6

3rd Year 0 0 4 4.7 9 10.6 2 2.3 1 1.2 0 0 1 1.2 0 0 2 2.4

4th Year 0 0 1 1.2 2 2.3 8 9.5 7 8.2 1 1.2 0 0 1 1.2 7 8.2

Number of Respondents 7 8.2 26 30.6 11 12.9 12 14.1 8 9.4 1 1.2 1 1.2 1 1.2 18 21.2

GenderMale Female No Response

f % f % f %

2nd Year 7 8.2 31 36.5 1 1.2

3rd Year 7 8.2 12 14.2 0 0

4th Year 7 8.2 20 23.5 0 0

Number of Respondents 21 24.6 63 74.2 1 1.2

Civil StatusSingle Married No Response

f % f % f %

2nd Year 39 45.9 0 0 0 0

3rd Year 19 22.4 0 0 0 0

4th Year 24 28.2 1 1.2 2 2.3

Number of Respondents 82 96.5 1 1.2 2 2.3

CommunityRural Urban Don’t Know No Response

f % f % f % f %

2nd Year 18 21.2 17 20.0 2 2.4 2 2.4

3rd Year 8 9.3 7 8.2 0 0 4 4.7

4th Year 14 16.4 10 11.8 1 1.2 2 2.4

Number of Respondents 40 46.9 34 40.0 3 3.6 8 9.5

Housing ArrangementDormitory Off-campus Rent Off-campus Own Live w/ Family Others No Response

f % f % F % f % f % f %

2nd Year 2 2.4 19 22.3 2 2.4 16 18.7 0 0 0 0

3rd Year 0 0 6 7.1 0 0 9 10.6 1 1.2 3 3.4

4th Year 2 2.4 10 11.8 0 0 13 15.3 0 0 2 2.4

Number of Respondents 4 4.8 35 41.2 2 2.4 38 44.6 1 1.2 5 5.8

BenefactorParents Relatives Working Student Scholar Others No Response

f % f % F % f % f % f %

2nd Year 28 32.9 2 2.4 0 0 8 9.4 1 1.2 0 0

3rd Year 15 17.6 1 1.2 1 1.2 1 1.2 1 1.2 0 0

4th Year 19 22.4 4 4.7 1 1.2 0 0 0 0 3 3.4

Number of Respondents 62 72.9 7 8.3 2 2.4 9 10.6 2 2.4 3 3.4

Weekly Allowance0-100 101-500 501-1000 1001 - above No Response

f % f % F % f % f %

2nd Year 3 3.4 25 29.4 7 8.2 4 4.7 0 0

3rd Year 2 2.4 11 12.9 6 7.1 0 0 0 0

4th Year 2 2.4 6 7.1 17 20.0 1 1.2 1 1.2

Number of Respondents 7 8.2 42 49.4 30 35.3 5 5.9 1 1.2

Table 2

22

Respondents’ Self-Assessment on their Understanding on Financial Literacy

Self-assessment f %

Very High 10 11.8

High 27 31.8

Moderate 40 47.0

Low 4 4.7

Very low 0 0

Don’t Know 3 3.5

No Response 1 1.2

Total 85 100

Table 2 shows that 40 or 47% of the respondents assessed themselves to have

moderate understanding on financial literacy. Almost one-third of them at 27 or 32%

claimed that they highly understand what financial literacy is. Those who have very high

confidence on their knowledge on financial literacy stand at 10 or 12%.

Table 3

Distribution of Respondents’ Answer for the Question, “Did Anyone Ever Explain How to Manage Your Finances?”

Did Anyone Ever Explain How To Manage

Your Finances?F %

Yes 61 71.8

No 22 25.9

No Response 2 2.3

Total 85 100

Table 3 illustrates that most of the respondents answered yes in the question “did

anyone ever explain how to manage your finances?” It is also worthy to note that more

23

than a quarter of them at 22 or 26% answered no while 2 or 2.3% of them didn’t respond

to the question.

When asked if the respondents are setting a budget before spending, majority of

them said yes.

Table 4

Distribution of Respondents’ Answer to the Question “Do You Regularly Set a Budget Before Spending?”

Do you set a budget? F %

Yes

I set a unwritten budget but don’t stick to it

5 5.9

I set an unwritten budget and stick to it

33 38.8

I set a written budget but don’t stick to it

11 12.9

I have a written budget and I stick to it

21 24.7

No 14 16.5

No Response 1 1.2

Total 85 100

It can be glanced on Table 4 that 70 or 82.3% of the respondents answered that

they regularly set a budget before spending. Thirty-three (33) or 38.8% of those who

regularly set budget said that theirs were unwritten but they stick to it. A number of the

respondents at 21 or 24.7% said that theirs were written budget and they stick to it.

Sixteen (16) or 18.8% of the respondents said that they set budget but they fail to stick to

it.

24

Meanwhile, 14 or 16.47% of all the respondents are not setting a budget at all

while 1 or 1.2% of them refused to answer.

Table 5

Distribution of the Respondents’ Responses for the Question “Do You Save?”

Do You Save? F %

Yes 70 82.4

No 15 17.6

Total 85 100

Table 5 shows that majority at 70 or 82% of those who responded the survey is

saving money. It is also worth noting that some respondents at 15 or 18% are not saving.

Table 6

Distribution of Respondents’ Responses for the Question “Who is Handling Your Savings?”

Who handles their savings?

F %

Themselves 63 90.0

Friends 2 2.9

Parents 2 2.9

Bank 3 4.3

Total 70 100

It can be gleaned in Table 6 that only 3 or 4.28% of the respondents who said that

they save entrust their money in the bank while majority of them at 63 or 90% keep it

themselves. It is also interesting to note that 2 or 2.86% respondents entrust their money

to their friends while the same number make their parents as overseer of their cash.

25

Table 7

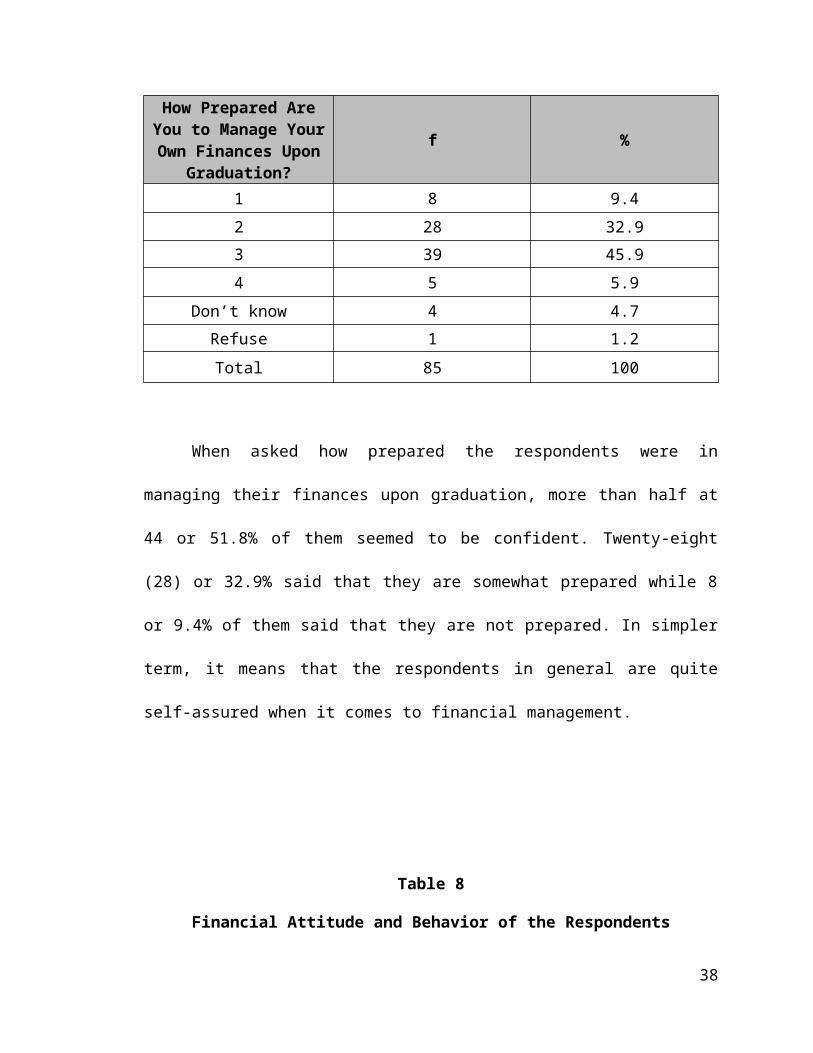

Distribution of the Respondents’ Answer in the Question “How Prepared Are You to Manage Your Own Finances Upon Graduation (On a 4-point Scale)?”

How Prepared Are You to Manage Your Own

Finances Upon Graduation?

f %

1 8 9.4

2 28 32.9

3 39 45.9

4 5 5.9

Don’t know 4 4.7

Refuse 1 1.2

Total 85 100

When asked how prepared the respondents were in managing their finances upon

graduation, more than half at 44 or 51.8% of them seemed to be confident. Twenty-eight

(28) or 32.9% said that they are somewhat prepared while 8 or 9.4% of them said that

they are not prepared. In simpler term, it means that the respondents in general are quite

self-assured when it comes to financial management.

Table 8

Financial Attitude and Behavior of the Respondents

Attitude and BehaviorWeighted

MeanBefore I buy something, I carefully consider whether I can afford it. 4.4

I tend to live for today and let tomorrow take care of itself. 2.3

26

I find it more satisfying to spend money than to save it for the long term. 2.3

I am prepared to risk my own money when saving or making investment. 3

I keep close personal watch on my financial affairs. 3.47

I set long term financial goals and strive to achieve them. 3.19

Money is there to be spent. 2.71

Table 8 shows the attitude and behavior of the respondents with regard to their

finances. In the scale of 1 to 5 (1=not all true of me, 2=not true of me most of the time,

3=sometimes not true of me, 4=true of me, and 5=very true of me), the respondents have

rated each item in the part III of the questionnaire in accordance whether the item

describe their attitude and behavior or not.

Forty-five (45) or 53% of the respondents answered 5 in item number 1.

Meanwhile, 29 or 34% of the respondents rated themselves 4. The mean rating that

respondents gave themselves for item number 1 is 4.4 which implies that it is true that

before they buy something, they carefully consider whether they can afford it or not.

For the second item, the mean rating of all the respondents is 2.3. With that rating,

it is safe to say that most of the time; they tend to be more concerned about their financial

future. This explains why 70 or 82 % of the respondents are setting budget before

spending and the same percentage of respondents save money for future.

In the third item, the respondents rated themselves 2.3 which implies that most of

the time, they save money for the long term. The mean rating for the responses of the

fourth item is 3 which imply that sometimes, it is not true of them that they risk their own

money when saving or making an investment. This clarifies the fact that of those who

said that they save, 63 or 90% of them keep the money themselves. In the fifth item, the

27

mean response is 3.47. It implies that sometimes, it is not true of them that they keep

personal watch over their finances. This may explain why 38 or 44.7% of those who

responded that they set budget before spending sets an unwritten budget. In the sixth

item, the mean score of the respondents is 3.19 which imply that sometimes it is not true

that they set long term financial goals and strive to achieve them. In the last item, the

mean score of the respondents is 2.71. With that score, it is safe to say that sometimes, it

is not true that the respondents think that money is there to be spent.

Table 9

Ratings Given by the Respondents to the Influencers

Influencers Weighted Mean

Parents 4.43

Friends 3.12

School 3.67

Books 3.01

Media 3.07

Job 2.41

Life Experiences 4.21

Internet 2.98

Informal Seminar/Class 2.81

Financial Planner (Professional) 2

Table 9 shows how the respondents rated the influence of each influencer. The

highest influencers with regard to financial management are the parents with the mean

score of 4.43 meaning they learned “enough” from them. Second is through life

experiences with the mean score of 4.21 meaning they learned “enough” from it. The

third is the school with the mean score of 3.67 meaning they learned also “enough” from

it. Influences of friends ranked fourth with mean score of 3.12 meaning they learned “not

28

so much” from them. Fifth place is through media with the mean score of 3.07 meaning

they learned “not so much from it. Books ranked sixth with the mean score of 3.01

meaning they learned “not so much from it. Although internet is considered the biggest

repository of knowledge, it only ranked seventh with the mean score of 2.98 meaning

they learned “not so much” followed by informal class/seminar with the mean score of

2.81 meaning they learned “not so much” from it. Ninth is through job with the mean

score of 2.41 meaning they learned “little” from it. The mean score given by the

respondents to the financial planner is 2 meaning they learned “none” which implies that

there are only few of the respondents who are subscribing to the services of the

professionals/financial planners.

Table 10

Distribution of the Respondents’ Answer on the Question: “How Often Were You Being Influenced by the Following Influencers?”

Influencers1 2 3 4 5

f % f % f % f % f %

Parents 2 2.4 3 3.516

18.8

15

17.6

47

55.3

Friends14

16.5

14

16.5

24

28.2

16

18.8

13

15.3

School11

12.9

7 8.236

42.4

8 9.413

15.3

29

Books18

21.1

18

21.1

26

30.6

8 9.4 6 7.1

Media15

17.6

10

11.8

26

30.6

12

14.1

12

14.1

Job26

30.6

13

15.3

14

16.5

8 9.4 7 8.2

Life Experiences 3 3.5 910.6

19

22.4

16

18.8

33

38.8

Internet13

15.3

7 8.222

25.9

12

14.1

21

24.7

Informal Seminar/Class21

24.7

17

2020

23.5

7 8.2 6 7.1

Financial Planner (Professional)27

28.2

16

18.8

17

20.0

6 7.1 3 3.5

It can be gleaned on Table 10 that respondents tend to talk about their finances to

their parents two times per month. Forty-seven (47) or 55.3% from the total respondents

rated 5 for parents meaning they are influenced “weekly.” Fifteen (15) or 17.6% from the

total respondents rated 4 for parents meaning they are influenced “twice per month.”

Sixteen (16) or 18.8% from the total respondents rated 3 for parents meaning they are

influenced “every few months.” Three (3) or 3.5% from the total respondents rated 2 for

parents meaning they are influenced “once per year.” Two (2) or 2.4% from the total

respondents rated 1 for parents meaning they are “never” influenced. Thirteen (13) or

15.3% from the total respondents rated 5 for friends meaning they are influenced

“weekly.” Sixteen (16) or 18.8% from the total respondents rated 4 for friends meaning

they are influenced “twice per month.” Twenty-four (24) or 28.8% from the total

respondents rated 3 for friends meaning they are influenced “every few months.”

Fourteen (14) or 16.5% from the total respondents rated 2 for friends meaning they are

influenced “once per year.” Also, fourteen (14) or 16.5% from the total respondents rated

1 for friends meaning they were “never” influenced. Thirteen (13) or 15.3% from the

total respondents rated 5 for school meaning they are influenced “weekly.” Eight (8) or

30

9.4% from the total respondents rated 4 for school meaning they are influenced “twice

per month.” Thirty-six (36) or 42.4% from the total respondents rated 3 for school

meaning they are influenced “every few months.” Seven (7) or 8.2% from the total

respondents rated 2 for school meaning they are influenced “once per year.” Eleven (11)

or 12.9% from the total respondents rated 1 for school meaning they are “never”

influenced. Six (6) or 7.1% from the total respondents rated 5 for books meaning they are

influenced “weekly.” Eight (8) or 9.4% from the total respondents rated 4 for books

meaning they are influenced “twice per month.” Twenty-six (26) or 30.6% from the total

respondents rated 3 for books meaning they are influenced “every few months.” Eighteen

(18) or 21.2% from the total respondents rated 2 for books meaning they are influenced

“once per year.” Also, eighteen (18) or 21.2% from the total respondents rated 1 for

books meaning they are “never” influenced. Twelve (12) or 14.1% from the total

respondents rated 5 for media meaning they are influenced “weekly.” Twelve (12) or

14.1% from the total respondents rated 4 for media meaning they are influenced “twice

per month.” Twenty-six (26) or 30.6% from the total respondents rated 3 for media

meaning they are influenced “every few months.” Ten (10) or 11.8% from the total

respondents rated 2 for media meaning they are influenced “once per year.” Also, 15 or

17.6% from the total respondents rated 1 for media meaning they are “never” influenced.

Seven (7) or 8.2% from the total respondents rated 5 for job meaning they are influenced

“weekly.” Eight (8) or 9.4% from the total respondents rated 4 for job meaning they are

influenced “twice per month.” Fourteen (14) or 16.5% from the total respondents rated 3

for job meaning they are influenced “every few months.” Thirteen (13) or 15.3% from the

total respondents rated 2 for job meaning they are influenced “once per year.” Also,

31

Twenty-six (26) or 30.6% from the total respondents rated 1 for job meaning they are

“never” influenced. Thirty-three (33) or 38.8% from the total respondents rated 5 for life

experiences meaning they are influenced “weekly.” Sixteen (16) or 18.8% from the total

respondents rated 4 for life experiences meaning they are influenced “twice per month.”

Nineteen (19) or 22.4% from the total respondents rated 3 for life experiences meaning

they are influenced “every few months.” Nine (9) or 10.6% from the total respondents

rated 2 for life experiences meaning they are influenced “once per year.” Also, three (3)

or 3.5% from the total respondents rated 1 for life experiences meaning they are “never”

influenced. Twenty-one (21) or 24.7% from the total respondents rated 5 for internet

meaning they are influenced “weekly.” Twelve (12) or 14.1% from the total respondents

rated 4 for internet meaning they are influenced “twice per month.” Twenty-two (22) or

25.9% from the total respondents rated 3 for internet meaning they are influenced “every

few months.” Seven (7) or 8.2% from the total respondents rated 2 for internet meaning

they are influenced “once per year.” Thirteen (13) or 15.3% from the total respondents

rated 1 for internet meaning they are “never” influenced. Six (6) or 7.1% from the total

respondents rated 5 for informal seminar/class meaning they are influenced “weekly.”

Seven (7) or 8.2% from the total respondents rated 4 informal seminar/class meaning they

are influenced “twice per month.” Twenty (20) or 23.5% from the total respondents rated

3 for informal seminar/class meaning they are influenced “every few months.” Seventeen

(17) or 20% from the total respondents rated 2 for informal seminar/class meaning they

are influenced “once per year.” Twenty-one (21) or 24.7% from the total respondents

rated 1 for informal seminar/class meaning they are “never” influenced. Three (3) or

3.5% from the total respondents rated 5 for financial planner (professional) meaning they

32

are influenced “weekly.” Six (6) or 7.1% from the total respondents rated 4 financial

planner (professional) meaning they are influenced “twice per month.” Fourteen (14) or

17% from the total respondents rated 3 for financial planner (professional) meaning they

are influenced “every few months.” Sixteen (16) or 18.8% from the total respondents

rated 2 for financial planner (professional) meaning they are influenced “once per year.”

Twenty-four (24) or 28.2% from the total respondents rated 1 for financial planner

(professional) meaning they are “never” influenced.

Table 11

Distribution of the Respondents’ Answer on the Question: “What Did You Learned About Finances in Your Home While Growing Up?”

Learned in Home f %

Work for what you receive 43 50.6Being honest in all dealings 45 52.9

Keeping Records 18 21.2Interest Rates 19 22.3

Giving to Charities 8 9.4Saving 64 75.3

Credit Cards 10 11.8Loans/Debt 20 23.5

Renter’s/Homeowner’s Insurance 5 5.9Life Insurance 16 18.8

Wills 17 20.0Credit 27 31.8Taxes 20 23.5

Investing 20 23.5Budgeting 56 65.9

In table 11, three quarters of the respondents responded that they learned about

saving when they were growing up while 56 or 66% of them said that they learned

budgeting in their houses. Work for what you receive ranked third with 40 or 56% of the

respondents who chose it. Fourth in the rank is being honest in all dealings with 45 or

53%. Twenty-seven (27) or 32% of the respondent answered that they learned about

credit when they were young. Meanwhile, twenty (20) or 24% of the respondents learned

about investing and the same percentage of respondents learned taxes and loans/debt.

33

Next is the interest rate with 19 or 22% of the respondents who checked it. Eighteen (18)

or 21% of the respondents reported that they learned about keeping records while they

were young. When asked about wills, only 17 or 20% of the respondents said that they

learned it while they were young. Sixteen (16) or 19% of the respondents said they were

thought about life insurance. Ten (10) or 12% of the respondents learned about credit

cards while they were growing up in their homes. Eight (8) or 9% of the respondents

responded that they were taught about giving to charities while the least common to them

is renters’/homeowner’s insurance with only 5 or 6% of the respondents said they were

taught about it by their parents.

Table 12

Distribution of the Respondents’ Answer on the Question: “Where Do You Expect to Increase Your Financial Knowledge?”

Influencer f %Others 11 12.9

Financial planner or counselor 17 20.0Life experiences 54 63.5

Job 22 25.9Media 21 24.7Book 24 28.8

School 38 44.7Friends 21 24.7Parents 59 69.4

Table 12 shows that most 59 or 69% of the respondents are expecting to increase

their financial knowledge through the help of their parents. Second in the rank is through

life experiences where 52 or 61% of the respondents said they are expecting to widen

their financial knowledge through it. Meanwhile, 38 or 45% of the respondents are

expectant to learn more about finances through school while 24 or 28% of them are

through books. Twenty-two (22) or 26% of them believed that their financial knowledge

will escalate through their job. Learning from media and friends are both in the sixth spot

34

where 21 or 25% of the respondents reported it as their answer. Seventeen (17) or 20% of

the respondents are expecting that they will enhance their financial knowledge through

financial planner or counselor. Eleven (11) or 13% of the respondent responded to the

question with the response of “others.”

Table 13

Distribution of the Respondents’ Answer on the Question: “How Will You Describe How Finances Were Handled Your Family?”

How finances are handled in their family? f %

My parents included me in some financial decisions

29 34.1

We didn’t talk much about finances but I learned from their examples

24 28.2

My parents explicitly taught me about finances 24 28.2

Within the family we openly discussed our finances

40 47.0

My parents usually argued about finances 24 28.2

It can be gleaned on Table 13 that 40 or 47% of the respondents said that within

their family, they openly discussed matters about finances. Twenty-nine (29) or 34% of

those who responded reported that their parents include them in some financial decisions.

Twenty-four (24) or 28% of the respondents stated that though they didn’t talk about

finances in their homes they learn money management through their parents’ examples.

The same number of respondents described that their parents explicitly taught them about

finances and those who recounted that their parents usually argue about money.

Table 14

Distribution of Respondents’ Responses for the Question “Compared to Your Parents, You are:”

35

Compared to their parents, respondents are:

f %

Much more likely to save 15 17.6

Somewhat more likely to save 27 31.8

About as likely to save/spend 28 32.9

Somewhat more likely to spend 10 11.8

Much more likely to spend 4 4.7

No Response 1 1.2

Total 85 100

It can be observed in Table 14 that comparing to their parents, 28 or 33% of the

respondents responded that they are about as likely to save/spend while 27 or 32% of all

the respondents stated that they are somewhat more likely to save. Fourteen (14) or 17%

said that compared to their parents, they are much more likely to save. Ten (10) or 12%

responded that they are somewhat more likely to spend. Four (4) or 5% of the

respondents assumed that they are much more likely to spend as compared to their

parents. One percent (1%) did not respond to the question.

Table 15

Scores Obtained by the Respondents from Basic Financial Literacy Quiz

Basic Financial Literacy Questions

2nd Year(39 Respondents)

3rd Year(19 Respondents)

4th Year(27 Respondents)

Total(85

Respondents)

N % N % N % N %

Interest Rates 15 38.46 17 89.47 13 48.15 45 52.94

Interest Compounding 6 15.38 4 21.05 4 14.81 14 16.47

36

Inflation 7 17.95 6 31.58 14 51.85 27 31.76

Time Value of Money 6 15.38 10 52.63 17 62.96 33 38.82

Money Illusions 15 38.46 14 73.68 17 62.96 46 54.12

Table 15 shows that 45 or 52.94% of the total number of respondents got the

correct answer on the interest rate question. Meanwhile, only 14 or 16.47% on the

interest compounding, 27 or 31.76% on the question related to inflation. Thirty-three

(33) or 38.82% of the total number of respondents were able to answer the question for

the Time Value of Money while on Money Illusion, 46 or 54.12% got the correct answer.

Table 16

Mean Percentage for Basic Financial Literacy Quiz per Year Level

Year Level Mean (in %)

2nd 25.13

3rd 53.68

4th 48.15

Table 16 shows that the highest mean percentage score among year levels are

those of the third year students with 46 or 53.68%. Next are the fourth year students with

forty-one (41) or 48.15%. While the lowest mean percentage score are those of the

second year students with twenty-one 21 or 25.13%. The table also shows that financial

illiteracy among the BSED Social Studies major student is so prevalent especially among

2nd year students. The researchers compared the mean score of the 2nd year and those of

37

the consolidated mean of 3rd and 4th year respondents and found that year-level based

difference in the survey data is statistically significant. It means that, part of the first

research assumption is nullified. In other words, being exposed to economic-related

courses affects the financial literacy of an individual.

Table 17

Mean Percentage for Basic Financial Literacy Quiz per Item

Basic Financial Literacy Questions Mean (in %)

Interest Rates 52.94

Interest Compounding 16.47

Inflation 31.76

Time Value of Money 38.82

Money Illusions 54.12

It can be gleaned in Table 17 that financial literacy levels among Social Studies

majors are low. Forty-five (45) or 52.94% of the respondents answered correctly the

question related to interest rates. The number of respondents who were able to answer the

interest compounding related question is only 14 or 16.47%. For the question related to

inflation, less than one third of the total number of respondents got the correct answer.

For the item related to time value of money, only 33 or 38.8% answered the item

correctly. Lastly, 46 or 54.12% of the respondents answered correctly the questions

related to money illusion.

38