Embed Size (px)

Citation preview

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 1

MICRO Research paper presentation

On

P2P Lending

A “Financial Intermediary in Social Democracy”-Indian Scenario

By:

Prashanth Ravada

January - 2017

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 2

Financial Institutions with higher credit flow to Micro-Sector; A Scheme for Promotion of Innovation and Rural Entrepreneurship and Agro Industry (ASPIRE); Scheme of Fund for Regeneration of Traditional Industries (SFURTI), Performance & Credit Rating Scheme (PCR) to create an ecosystem of SMEs for easier/ cheaper access to credit for the rated enterprises, and initiative of “Startup India campaign,” backed by positive business sentiments, Improved Customer confidence to earn and expense, and more over enact of corrective measure under phase of “DEMONETIZATION” through regulatory are a few Means, to correct and boost Economic Growth.

.

Significant development could be sighted in financial markets, its instruments and associated intermediaries driven largely by deregulation, technological advancement and rapid globalization resulting financial intermediation has also undergone remarkable changes, more so in developed countries but also in emerging economies like India, where Market participants who historically sought finance / investments through private equity & traditional banks, are now obtaining capital from Peer-To-Peer model (P2P lending.)

The P2P lending model uses online technology platforms to connect investors with individuals and businesses in search of capital. The model is attractive to borrowers as it allows them to access money at lower interest rates when compared to traditional credit providers. As has evolved into a distinct asset class, this model also provides a new investment opportunity for Retail Investors. P2P service providers typically earn money by charging a service fee on each facilitated loan and with the use of technology application process decreases transaction costs, making it more efficient and user-friendly than conventional lending.

Indian Economy is in the phase of correction posing robust growth trend, with sound economic policy & regulatory initiatives comprising “Make-in-India” appealing and attracting Investments from both Domestic and International Markets. With allocation of Rs 10K crore through the Micro Units Development Refinance Agency (MUDRA Bank), start of “JanDhan” a Central initiative targeting every Indian with provide of Savings bank a/c on its successful grass roots and a step forward for Financial Inclusion., introduction of the Goods and Service Tax (GST) Bill, Prime Minister’s Employment Generation Programme (PMEGP) to facilitate

Latest RBI’s initiative by extend of 11 new licenses in the Payments and Small Bank category, which indeed pose to be of ‘Challenger banks’, as they take on traditional banks with core objective to sustain Financial Inclusion, by expand of access to financial services in Emerging Markets comprising of Rural and Semi-Urban areas with traditional banking activities by accept deposits and lend to underserved sections of customers, including Small business units, Small & Marginal Farmers, Micro & Small Industries, and entities in Unorganized sector through Technology platform.

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 3

Fig. P2P Loan Origination and Process flow

Fig. General Purpose of Loan across the Industry Segment along with Borrower Risk Categorization and IRR along with Principal Protection (Service provider specific)

Individuals register themselves on P2P service provider platform as Borrower or Lender by pay of registration fee. Registration includes providing information such as personal, professional, financial details which service provider verifies along with the relevant KYC duly submitted online at par with RBI’s guidelines.

All approved borrowers and lenders listing are then published on the site. Lenders can view borrower loan listing which includes information such as loan purpose, demand and need for lenders make offers to them, personal, professional and financial information that allows lenders to make an informed decision before lending to a borrower.

Borrowers can receive offers from multiple lenders and similarly, lenders can lend to multiple borrowers thereby diversify their risk along with the interest rates are determined by the borrowers and lenders and not service provider.

Once a borrower loan is 100% funded by investors the loan is disbursed.

Loan disbursals involve loan agreement between borrower and lender, money transfer from lender to borrower for the loan amount and EMI transfer from borrower to lender.

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 4

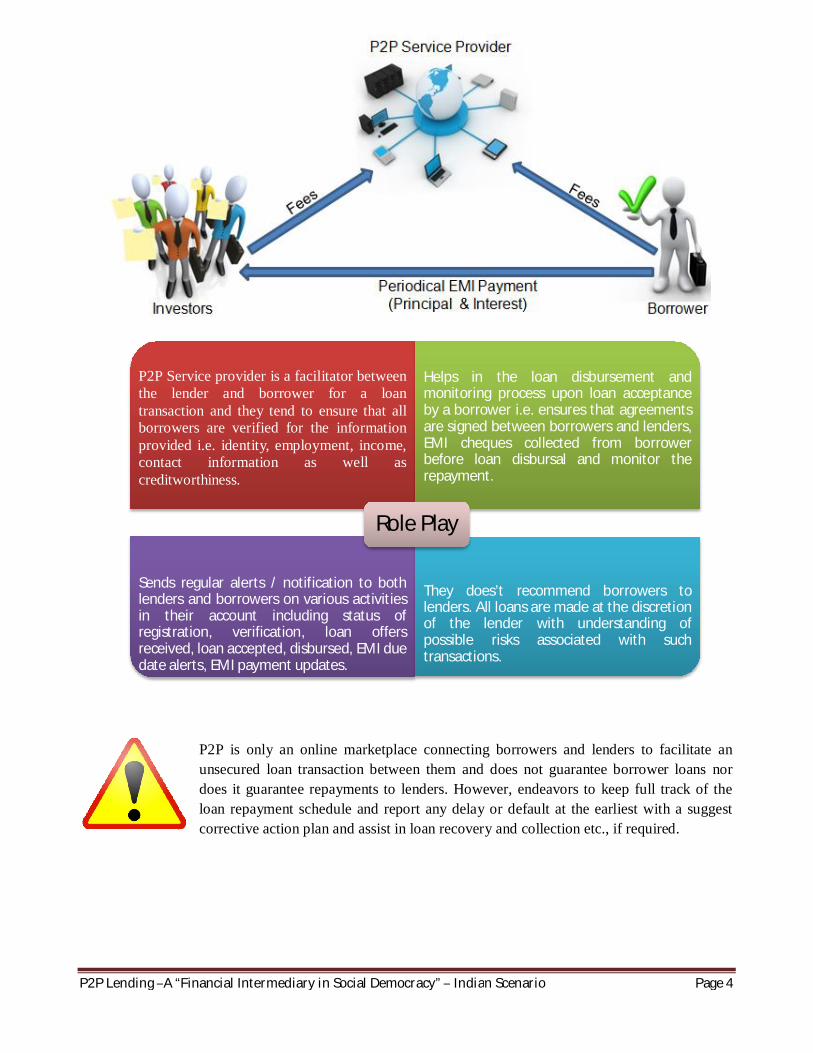

P2P Service provider is a facilitator betweenthe lender and borrower for a loantransaction and they tend to ensure that allborrowers are verified for the informationprovided i.e. identity, employment, income,contact information as well ascreditworthiness.

Helps in the loan disbursement andmonitoring process upon loan acceptanceby a borrower i.e. ensures that agreementsare signed between borrowers and lenders,EMI cheques collected from borrowerbefore loan disbursal and monitor therepayment.

Sends regular alerts / notification to bothlenders and borrowers on various activitiesin their account including status ofregistration, verification, loan offersreceived, loan accepted, disbursed, EMI duedate alerts, EMI payment updates.

They does’t recommend borrowers tolenders. All loans are made at the discretionof the lender with understanding ofpossible risks associated with suchtransactions.

Role Play

P2P is only an online marketplace connecting borrowers and lenders to facilitate an unsecured loan transaction between them and does not guarantee borrower loans nor does it guarantee repayments to lenders. However, endeavors to keep full track of the loan repayment schedule and report any delay or default at the earliest with a suggest corrective action plan and assist in loan recovery and collection etc., if required.

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 5

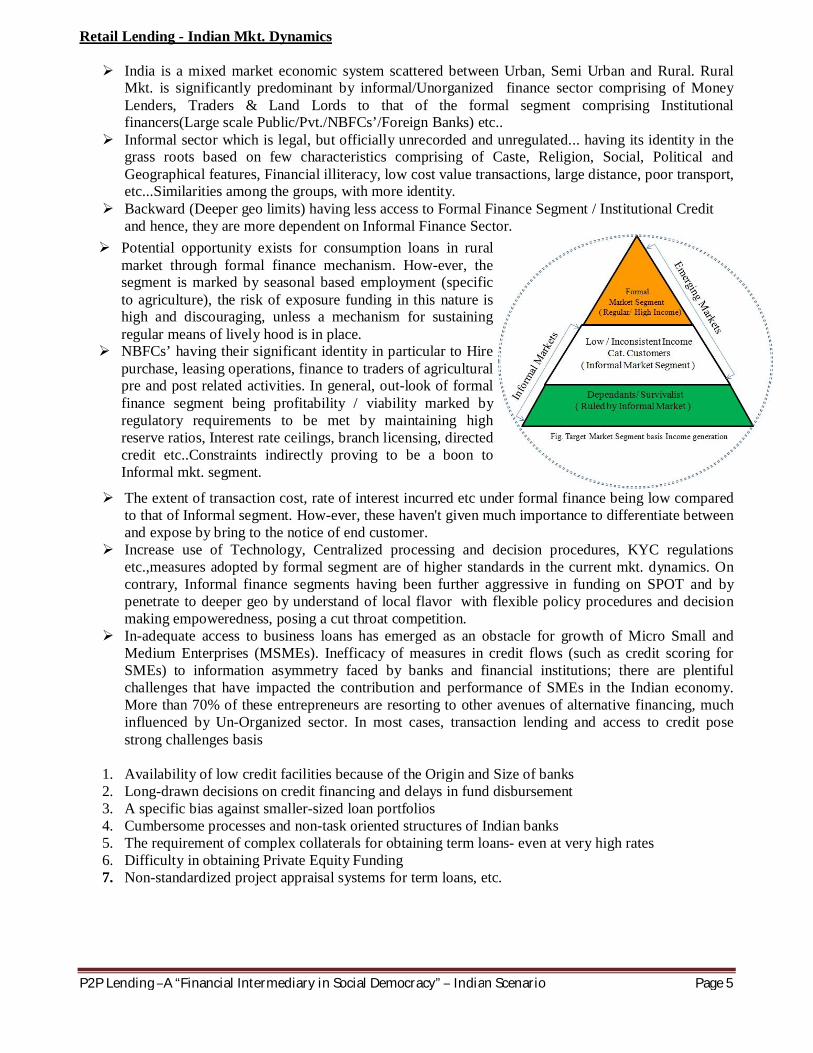

Retail Lending - Indian Mkt. Dynamics

India is a mixed market economic system scattered between Urban, Semi Urban and Rural. Rural Mkt. is significantly predominant by informal/Unorganized finance sector comprising of Money Lenders, Traders & Land Lords to that of the formal segment comprising Institutional financers(Large scale Public/Pvt./NBFCs’/Foreign Banks) etc..

Informal sector which is legal, but officially unrecorded and unregulated... having its identity in the grass roots based on few characteristics comprising of Caste, Religion, Social, Political and Geographical features, Financial illiteracy, low cost value transactions, large distance, poor transport, etc...Similarities among the groups, with more identity.

Backward (Deeper geo limits) having less access to Formal Finance Segment / Institutional Credit and hence, they are more dependent on Informal Finance Sector.

The extent of transaction cost, rate of interest incurred etc under formal finance being low compared

to that of Informal segment. How-ever, these haven't given much importance to differentiate between and expose by bring to the notice of end customer.

Increase use of Technology, Centralized processing and decision procedures, KYC regulations etc.,measures adopted by formal segment are of higher standards in the current mkt. dynamics. On contrary, Informal finance segments having been further aggressive in funding on SPOT and by penetrate to deeper geo by understand of local flavor with flexible policy procedures and decision making empoweredness, posing a cut throat competition.

In-adequate access to business loans has emerged as an obstacle for growth of Micro Small and Medium Enterprises (MSMEs). Inefficacy of measures in credit flows (such as credit scoring for SMEs) to information asymmetry faced by banks and financial institutions; there are plentiful challenges that have impacted the contribution and performance of SMEs in the Indian economy. More than 70% of these entrepreneurs are resorting to other avenues of alternative financing, much influenced by Un-Organized sector. In most cases, transaction lending and access to credit pose strong challenges basis

1. Availability of low credit facilities because of the Origin and Size of banks 2. Long-drawn decisions on credit financing and delays in fund disbursement 3. A specific bias against smaller-sized loan portfolios 4. Cumbersome processes and non-task oriented structures of Indian banks 5. The requirement of complex collaterals for obtaining term loans- even at very high rates 6. Difficulty in obtaining Private Equity Funding 7. Non-standardized project appraisal systems for term loans, etc.

Potential opportunity exists for consumption loans in rural market through formal finance mechanism. How-ever, the segment is marked by seasonal based employment (specific to agriculture), the risk of exposure funding in this nature is high and discouraging, unless a mechanism for sustaining regular means of lively hood is in place.

NBFCs’ having their significant identity in particular to Hire purchase, leasing operations, finance to traders of agricultural pre and post related activities. In general, out-look of formal finance segment being profitability / viability marked by regulatory requirements to be met by maintaining high reserve ratios, Interest rate ceilings, branch licensing, directed credit etc..Constraints indirectly proving to be a boon to Informal mkt. segment.

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 6

Emerging P2P Financial Intermediaries, their role in Indian Mkt. Dynamics Scenario

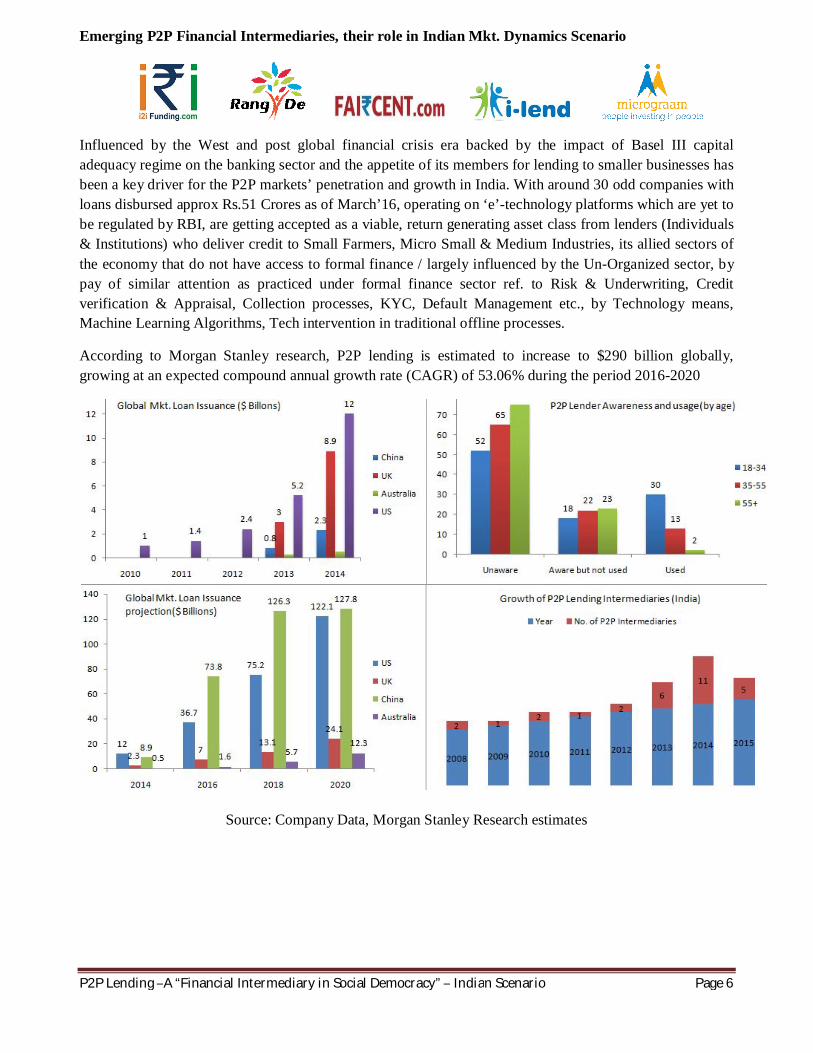

Influenced by the West and post global financial crisis era backed by the impact of Basel III capital adequacy regime on the banking sector and the appetite of its members for lending to smaller businesses has been a key driver for the P2P markets’ penetration and growth in India. With around 30 odd companies with loans disbursed approx Rs.51 Crores as of March’16, operating on ‘e’-technology platforms which are yet to be regulated by RBI, are getting accepted as a viable, return generating asset class from lenders (Individuals & Institutions) who deliver credit to Small Farmers, Micro Small & Medium Industries, its allied sectors of the economy that do not have access to formal finance / largely influenced by the Un-Organized sector, by pay of similar attention as practiced under formal finance sector ref. to Risk & Underwriting, Credit verification & Appraisal, Collection processes, KYC, Default Management etc., by Technology means, Machine Learning Algorithms, Tech intervention in traditional offline processes.

According to Morgan Stanley research, P2P lending is estimated to increase to $290 billion globally, growing at an expected compound annual growth rate (CAGR) of 53.06% during the period 2016-2020

Source: Company Data, Morgan Stanley Research estimates

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 7

Conventional banking carry an element of risk / mismatches between short term liabilities (Deposits) and long term assets (Asset Loans), which can make a bank vulnerable expose to large withdrawal of deposits / loan defaults to anticipate. On contrary, in P2P platforms as lenders are directly matched to borrowers and while a cluster of defaults would certainly hurt lenders, it would not necessarily bring down the lending company and trigger a wider financial crisis.

Evident and experienced, demand and use of mobile phone had a greater penetration in India in-line with the population growth by 80%, as its usage had tailor-made to the needs of a country with a large semi-literate population that is living on the borders of the poverty line though aren’t capable to handle a computer…but were capable enough to use & operate a mobile phone, and this being a key driving factor for the P2P platforms to sustain its objectives in a more tailored fashioned manner.

Use of alternative credit scoring methods (Non Traditional data sources) comprising assessment of large data streams from online social networks, mobile phone records, community domicile based information, utility service bills and psychometrics etc., forming part of alternative means of evaluation to identity potential borrowers in cases where traditional credit information is scarce, enabling new lending and control over risk by these emerging intermediaries, where traditional finance sectors are lagging behind and serving the potential credit-worthy yet financially excluded population, and simultaneously contributing for financial inclusion.

P2P lending intermediary, a unique and new asset class on the Indian investment scene, is being considered by investors because of its higher returns at predictable risks. These platforms intended to create new investment opportunities for income-seeking investors, especially those who are ready to go an extra mile of earnings. Currently it is providing an opportunity to investors to earn a gross return of up to 18-26% p.a. by diversified portfolio as per their risk appetite as compared to the interest rates of 4%-7% on Savings and fixed deposits offered by traditional financial institutions, who inter alia charge 10-22/24% lending interest rates on various loans and basis risk lending matrix, take the advantage of spread between borrowing & lending rates.

Impact of Demonetization strategy tends to put an effort in formalizing the unorganized / informal finance sector which accounts for 45% of the India’s GDP to be streamlined/exit and by pose of opportunities for the Organized Finance sector to serve the increase demand in Short (or) Medium Term for business funding significantly from SMEs comprising Small Time Entrepreneurs’ and Business Owners. Given the context, P2P financial intermediaries tend to take lead role, basis their expertise in minimizing the risk spread by bringing borrowers and investors on same platform.

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 8

Risk Description Drivers Risk Category Investors Borrowers Driver description

Credit Risk

Is tempted to invest by the promise of an unrealistically high rate of return on investment.

Insufficient financial literacy of Investors and high complexity risk analysis is necessary to evaluate projects

Loses the capital invested in the event the borrower is unable to meet its repayment obligation.

Insufficient assessment of the creditworthiness service provider

Does not receive the funds back Borrower does not receive the funds collected from lenders Incomplete information ref. money

remittance provider authorization

Suffers loss because platform defaults Borrower could be held liable by the investor in the event of failure of the service provider platform

Lack of financial safeguards against platform default

Risk of Fraud

suffers loss when a borrower acts fraudulently

Insufficient background check on a borrower, by the platform

Uncertain about the reputation and the security of a P2P Lending platform

Borrower is uncertain about the reputation and the security of a P2P funding platform Non disclosure requirements of

platforms / Nil Regulatory control.

Investors personal data may be stolen or misused Borrowers face the risk that personal data

may be stolen or misused Lack of document handling processes of platform provider

Unable to identify conflicts of interests of the platform, its shareholders, managers and key employees

Insufficient information disclosure requirements of platforms on potential conflicts of interests

Misled pricing structure or information about other terms and conditions applicable to the parties

Insufficient contract information disclosure requirements

Not been provided the information necessary to assess a certain project [and/or the reputation of the borrower]

Lack of Customer due diligence process on borrower by a platform; Insufficient information regarding the ability or willingness of lenders to pay the committed amounts

Uncertain about his rights to withdraw or to cancel an investment prior to its maturity

Insufficient termination rights for the lender/Misleading explanations on applicable termination rights

Not in a position to assess a certain platform’s reputation and probity

Lack of information disclosure requirements of platforms on potential conflicts of interests

- Borrowers may not receive committed funds because lenders are not able or willing to pay as agreed

Insufficient assessment of the creditworthiness/risks by the platform

Legal Risk

Investor is uncertain about his rights and obligations vis-a-vis the parties involved

Borrower is uncertain about his rights and obligations vis-à-vis the parties involved

Inappropriate or misleading information about the contractual rights and obligations of the contracting parties

Lender faces an inappropriate complaints handling mechanism on a platform

Borrowers can be affected by inappropriate complaints handling mechanism on a platform too

Unclear complaints handling rights and regulations of market participants

Lender's funds might not be transferred to the Borrower -

Missing requirement for platforms to follow money remittance provider authorization

- Borrowers’ project ideas could potentially be copied

Lack or insufficient project ideas’ safeguard clauses

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 9

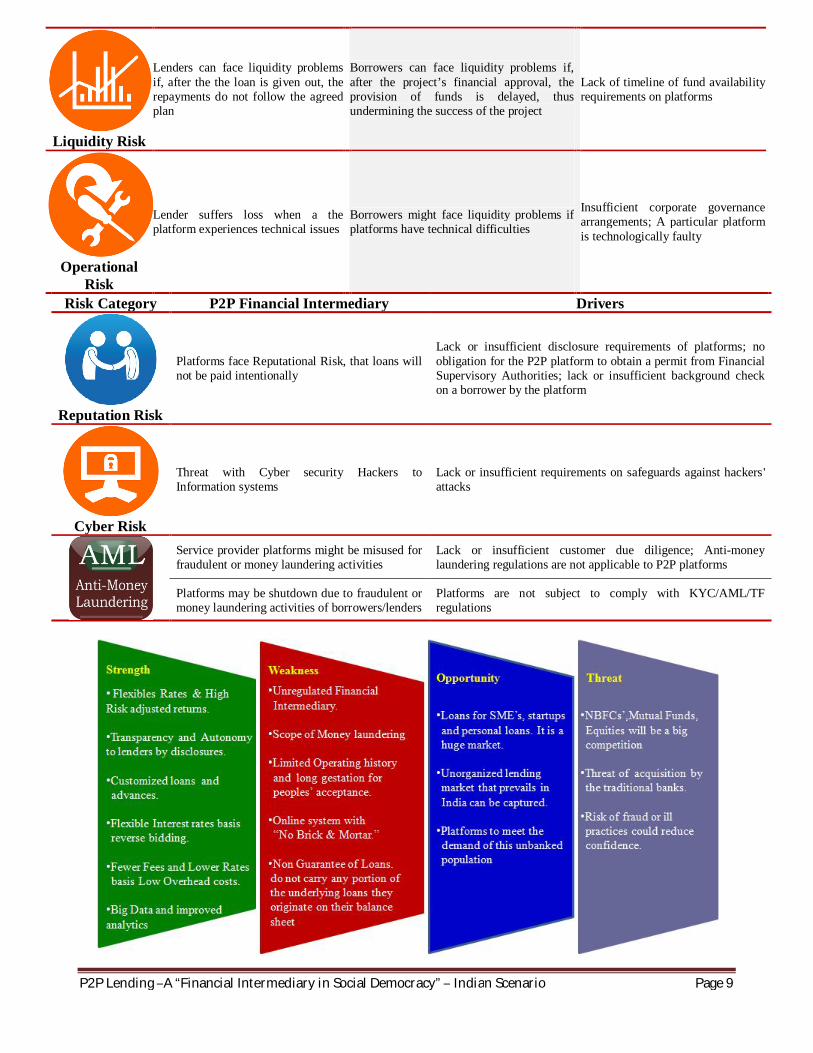

Liquidity Risk

Lenders can face liquidity problems if, after the the loan is given out, the repayments do not follow the agreed plan

Borrowers can face liquidity problems if, after the project’s financial approval, the provision of funds is delayed, thus undermining the success of the project

Lack of timeline of fund availability requirements on platforms

Operational Risk

Lender suffers loss when a the platform experiences technical issues Borrowers might face liquidity problems if

platforms have technical difficulties Insufficient corporate governance arrangements; A particular platform is technologically faulty

Risk Category P2P Financial Intermediary Drivers

Reputation Risk

Platforms face Reputational Risk, that loans will not be paid intentionally

Lack or insufficient disclosure requirements of platforms; no obligation for the P2P platform to obtain a permit from Financial Supervisory Authorities; lack or insufficient background check on a borrower by the platform

Cyber Risk

Threat with Cyber security Hackers to Information systems

Lack or insufficient requirements on safeguards against hackers' attacks

Service provider platforms might be misused for fraudulent or money laundering activities

Lack or insufficient customer due diligence; Anti-money laundering regulations are not applicable to P2P platforms

Platforms may be shutdown due to fraudulent or money laundering activities of borrowers/lenders

Platforms are not subject to comply with KYC/AML/TF regulations

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 10

The website of the platform should contain information of borrowers and Investors. Information about the risks for lenders – including risk of total / partial loss of capital invested; lack of liquidity – must also be provided on the platform’s website. All information to be clear, understandable and not misleading. Moreover, Lenders should only be permitted to invest after confirming acknowledgment of this information.

Disclosures

In case of lending contributors comprising of Institutional Investors (White-Label Partnership) comprising Banks, Hedge Funds or other business entities that lend money through P2P platform, such means to be handled in accordance with the guide lines set by the RBI. Set investment limits for lenders by permit invest to maximum amount, within a certain period of time or depending on his income or wealth. To ensure adherence to these investment limits, the platform to seek lenders confirmation to comply with the statutory limit. P2P platforms to disclose detailed information to extent a risk assessment has been performed. Any information gained is made available to lenders, so as to strengthen the ability of lenders for informed decisions.

KYC

Platforms to conduct an effective, proper and clearly defined due diligence procedure on any investment opportunity, possibly above a certain threshold, before posting on platform’s website. Furthermore, any results of due diligence procedures performed in relation to a project to be disclosed.

On anticipate of risk that individuals acting under false identity through use of P2P platforms to collect money for fake offerings, would require background checks. Platforms should therefore be obliged to request identification & addresses, information about financial status/creditworthiness and potential criminal records from borrowers/lenders. Furthermore, platform to restrict access to its website on reason to believe that a borrower/ lender might potentially act fraudulently

Platforms to establish lender protection services. For this, platforms to obtain data regarding creditworthiness of borrowers & lenders. Furthermore, platforms would in any event be obliged to provide disclaimers regarding the credit/counterparty risk on the platform. This risk driver could also be mitigated if P2P lending platforms were required to cooperate with a bank/credit bureau/rating agencies, either in the way that the bank processes the assessments on a professional basis.

Platforms, their shareholders, managers or key employees to be prohibited from having or acquiring financial interests in a borrower’s business. In any case, platforms should be obliged to implement measures to identify and manage potential conflicts of interest. Furthermore, these measures should be unambiguously disclosed on their websites.

Platforms to clearly describe the rights and obligations of the parties, the financing process and all costs and other features applicable to contracting parties. In addition, a draft contract should be made available on the website to both borrowers and lenders, and customers should confirm their acknowledgment of the terms and conditions prior to the conclusion of any contracts.

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 11

Platform to ensure that lenders are aware of their rights to cancel a contract prior to its maturity. Platforms should offer a true, clear and complete explanation of the termination rights applicable under statutory law and, where necessary, pursuant to their contractual terms. A platform would accordingly be required to disclose on its website the exact point in time at which it would no longer be possible to terminate an investment prior to maturity.

Furthermore, platforms are required to offer lender the right to withdraw commitment, provided that the funding goal/target amount hasn’t been reached and the borrower hasn’t yet received the money.

To set up an appropriate complaints handling mechanism (Grievance Redress Mechanism). A clear and flexible open policy on complaints handling should also be explicitly described in the terms and conditions of the platform.

On un eve scenario of Platforms handling money from lenders or borrowers,Sec.45(I) of RBI, same to be required to be segregate and reported in books of accounts and disclose to Regulatory, as in the current scenario, same being prohibited considering the platforms being likely to be assigned NBFC – Intermediary status.

Platforms are required to be authorized by an affiliate authority (RBI). These further to include check of natural persons who manage platform meet appropriate standards for competence, capability, integrity and financial soundness. Relevant disclosures with ref. to be updated on Web portal.

Business Continuity Plan/Committee (BCP) to be set up for measure of performance, risk assessment and arrangements to be envisaged by setting up a compensation scheme, insurance coverage for default, or similar provisions and by ensure that loans would continue to be administered even if platform goes out of business.

Platforms to take reasonable care in establish and maintain systems and controls that are appropriate to business, including timely transfer of agreed funds. Must also disclose all risks, including risk that pledged money may not be paid when it is due, in a way that is fair, clear and not misleading.

Provide of “Principal Protection Fund” (PPF) to all investors who lend through P2P lending platform with no extra charges. For which service providers to set aside X% of the disbursed loans towards PPF, which allows its Investors to enjoy up to 100% protection against loan defaults, so as to further build and develop a Financial Healthy Economic System to sustain.

IT risks for lenders and borrowers may arise in particular from the unavailability of systems, networks, or data, or from a loss of data integrity. Mitigating these risks requires a sound IT Organization frame work.

Platforms to be complied and include in the scope of the Anti-Money Laundering Directive as set by the regulatory (RBI). Plat forms to take reasonable care to establish and maintain appropriate controls in that sense (including when using a payment service provider)

P2P Lending –A “Financial Intermediary in Social Democracy” – Indian Scenario Page 12

P2P lending financial intermediaries though not a significant player in terms of overall market share and willn’t fundamentally disrupt/displace banks' core function as lenders in mass market., but tend to play an active role in the financial system of our economy, as they complement the role of service provider and are aimed to serve Customers under facilitator mode, while pose little Systemic Risk, their importance to some key sectors and other areas of the Economy Warrant RBI’s interest and oversight. With their low operating cost backed by technology, minimal regulatory, data-driven models, and specializing in channelize low cost borrowings and higher earning interest attracting Individual investors / Institutional investments helping to meet funding needs of larger population including under-served, these tend to extend their share in the Nation’s Economic growth by promote of Financial Inclusion through technology enabled platforms and by spread of Financial Literacy, Service, by extend opportunities of growth, days coming by in both Retail and MSME business segment offerings, as currently forming part of ‘Traditional Lenders,’ share.

PricewaterhouseCoopers, Peer Pressure: How Peer-to-Peer Lending Platforms are Transforming the Consumer Lending Industry, PWC.COM (February 2015)

Peter Man beck and Marc Franson, The Regulation of Marketplace Lending: A Summary of the Principal Issues

Morgan Stanley Research “Global Marketplace Lending: Disruptive Innovation in Financials" (May 19, 2015).

Opinion of the European Banking Authority (EBA) on lending based Crowd funding.

Practice Pointers on: P2P Lending Basics: How It Works, Current Regulations and Considerations

R Gandhi: “Regulating financial innovation - P2P lending platforms design Challenges” at the Mint Marketplace Lending Summit, Mumbai, 17 May 2016.

Status of Micro Finance in India 2015-16 – NABARD MSME at a Glance 2016 – Govt. of India. General Web search.