Embed Size (px)

Citation preview

Operations Strategies and Risk Management for Individuals

Sachin SachdevaIndependent Risk Management ConsultantGlobal Association of Risk Professionals

October 2016

2

The views expressed in the following material are the

author’s and do not necessarily represent the views of

the Global Association of Risk Professionals (GARP),

its Membership or its Management.

1

Options Strategies and Risk

Management for Individuals

Terminology

Basic Positions(Covered Calls, Protective Puts and Synthetic Options)

Advanced Techniques(Spreads and Straddles)

2

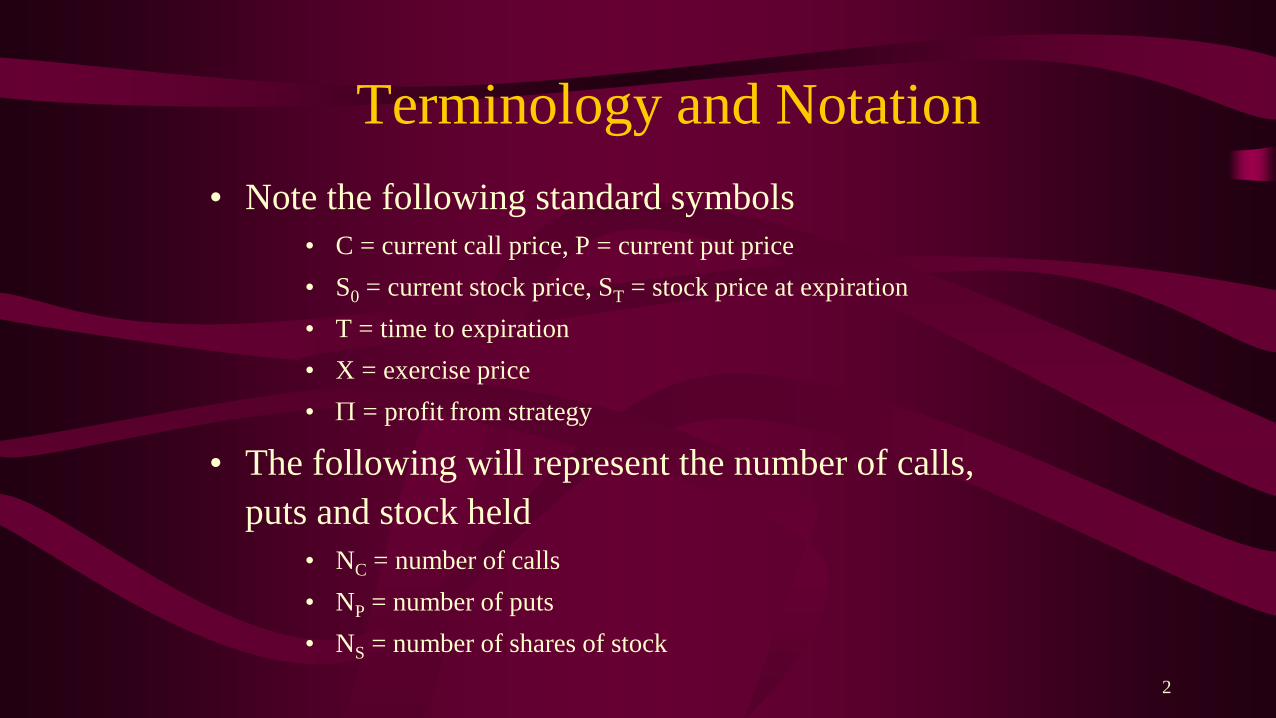

Terminology and Notation

• Note the following standard symbols

• C = current call price, P = current put price

• S0 = current stock price, ST = stock price at expiration

• T = time to expiration

• X = exercise price

• P = profit from strategy

• The following will represent the number of calls,

puts and stock held

• NC = number of calls

• NP = number of puts

• NS = number of shares of stock

3

Terminology and Notation

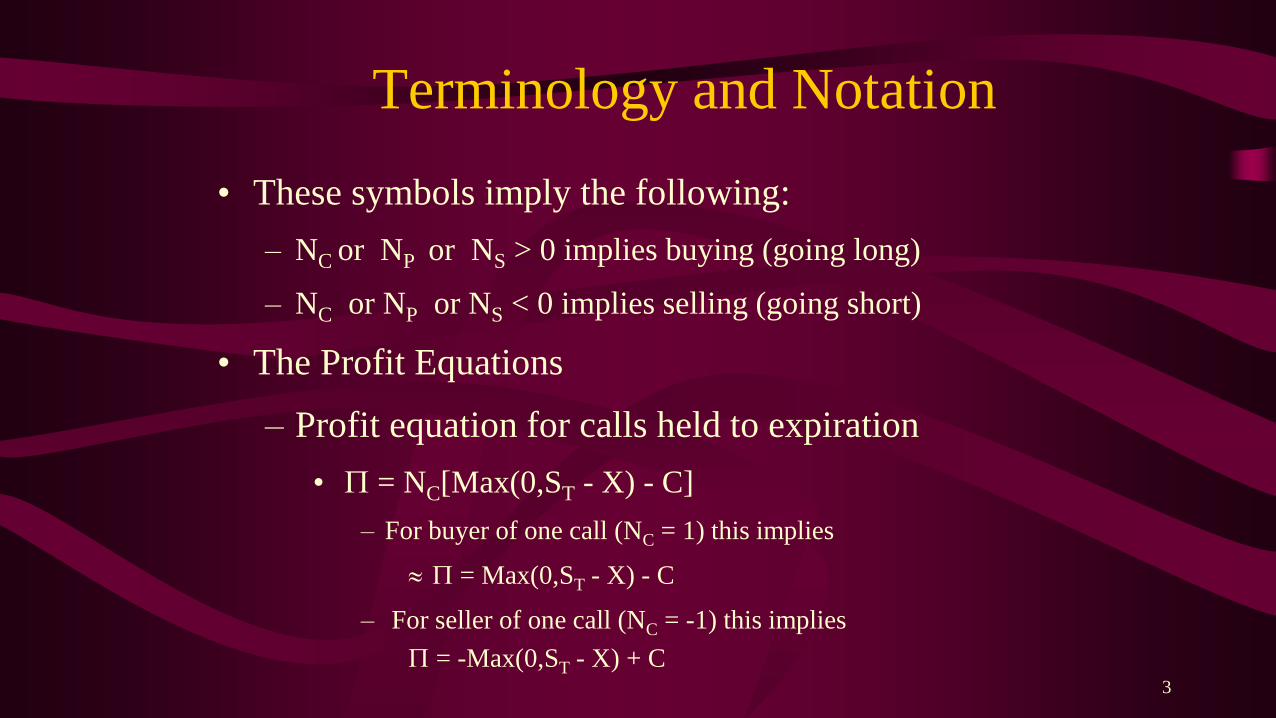

• These symbols imply the following:

– NC or NP or NS > 0 implies buying (going long)

– NC or NP or NS < 0 implies selling (going short)

• The Profit Equations

– Profit equation for calls held to expiration

• P = NC[Max(0,ST - X) - C]

– For buyer of one call (NC = 1) this implies

P = Max(0,ST - X) - C

– For seller of one call (NC = -1) this implies

P = -Max(0,ST - X) + C

4

Terminology and Notation

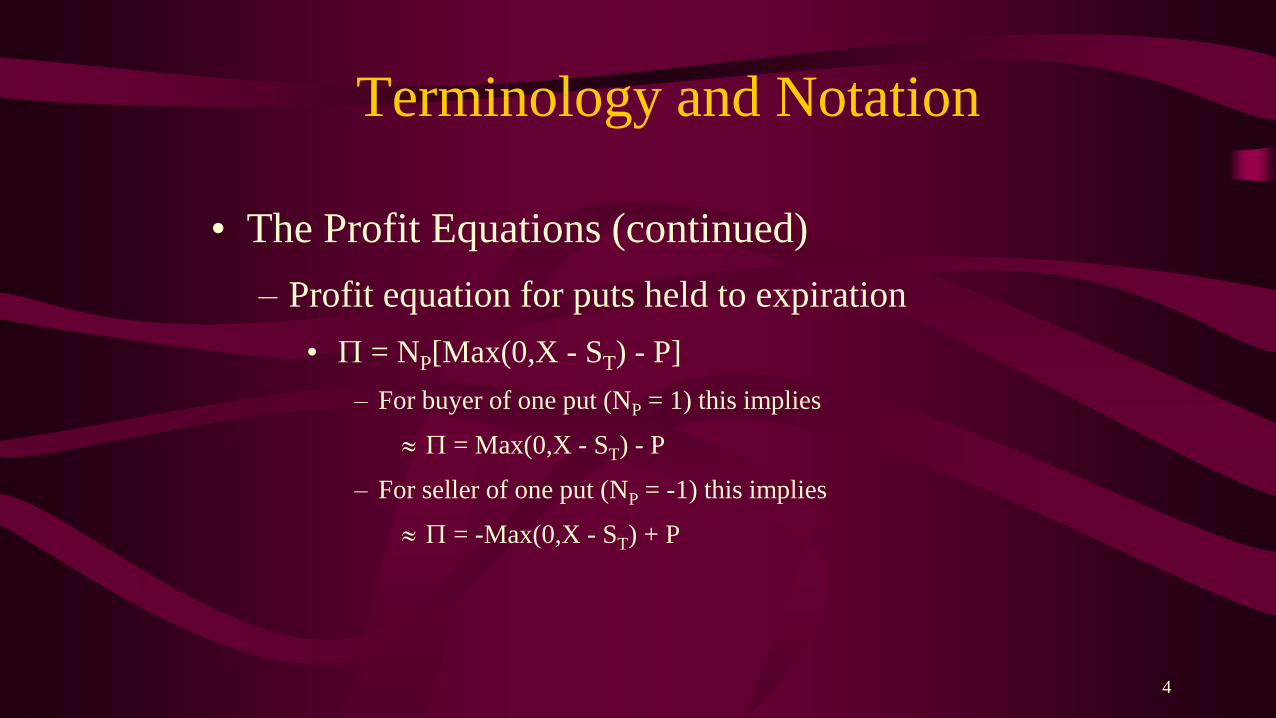

• The Profit Equations (continued)

– Profit equation for puts held to expiration

• P = NP[Max(0,X - ST) - P]

– For buyer of one put (NP = 1) this implies

P = Max(0,X - ST) - P

– For seller of one put (NP = -1) this implies

P = -Max(0,X - ST) + P

5

Terminology and Notation

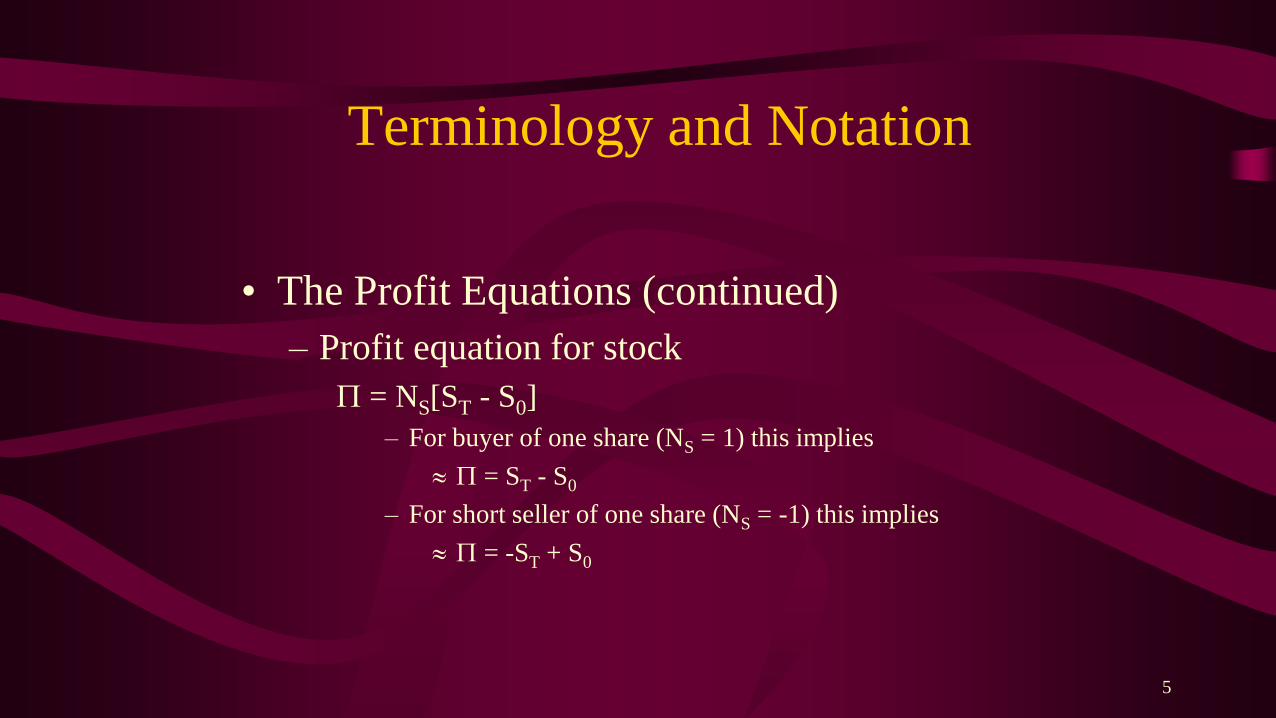

• The Profit Equations (continued)

– Profit equation for stock

P = NS[ST - S0]

– For buyer of one share (NS = 1) this implies

P = ST - S0

– For short seller of one share (NS = -1) this implies

P = -ST + S0

6

Terminology and Notation

• Different Holding Periods

– T1<T2

• Assumptions

– No dividends

– No taxes or transaction costs

7

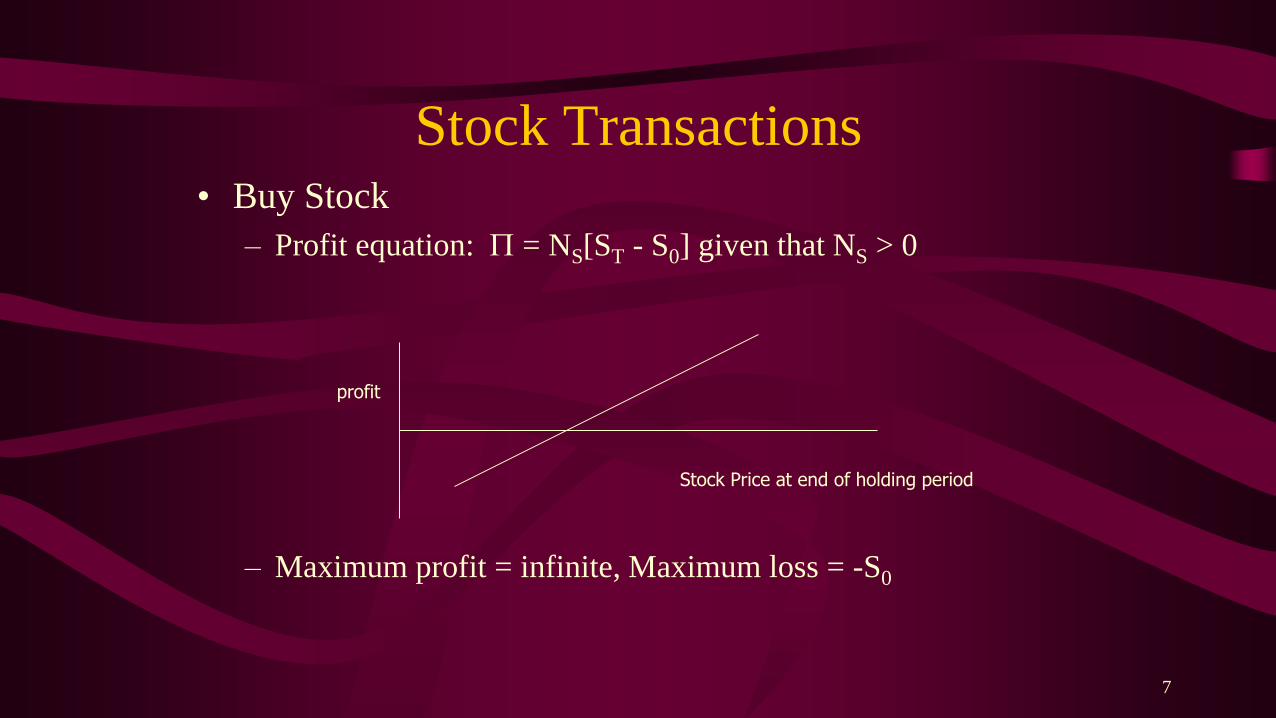

Stock Transactions• Buy Stock

– Profit equation: P = NS[ST - S0] given that NS > 0

– Maximum profit = infinite, Maximum loss = -S0

profit

Stock Price at end of holding period

8

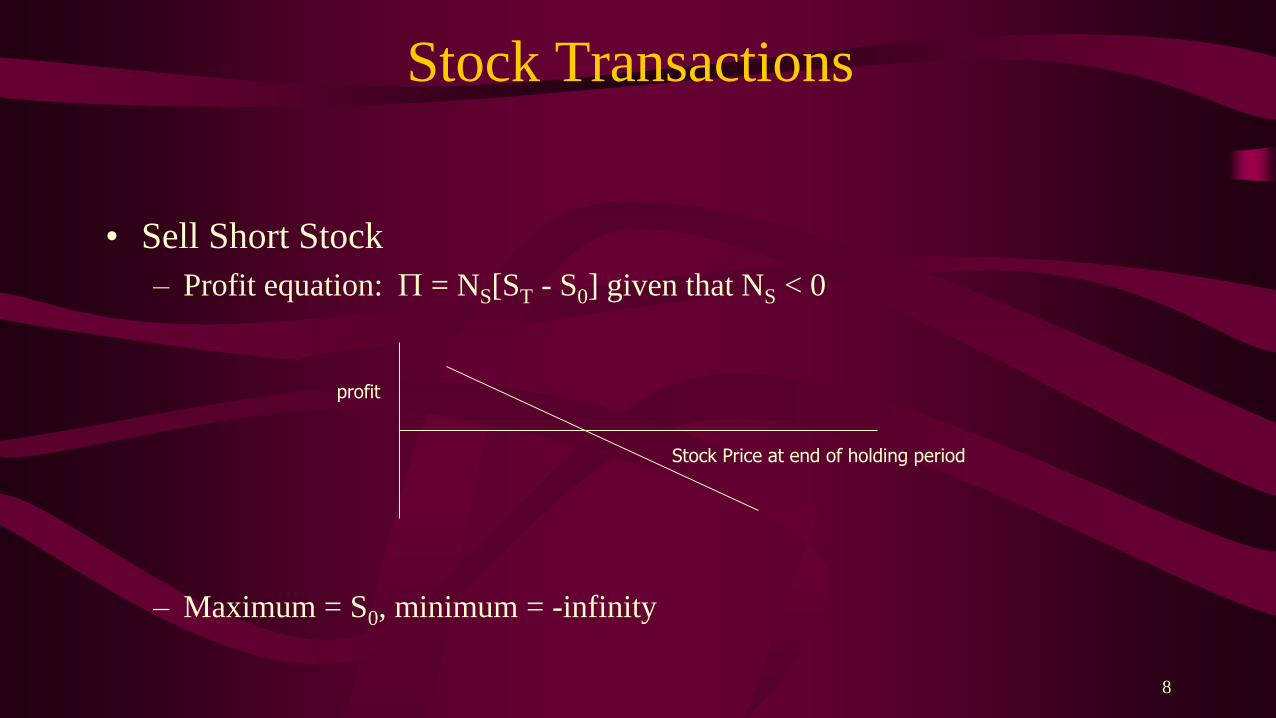

Stock Transactions

• Sell Short Stock

– Profit equation: P = NS[ST - S0] given that NS < 0

– Maximum = S0, minimum = -infinity

profit

Stock Price at end of holding period

9

Call Option Transactions

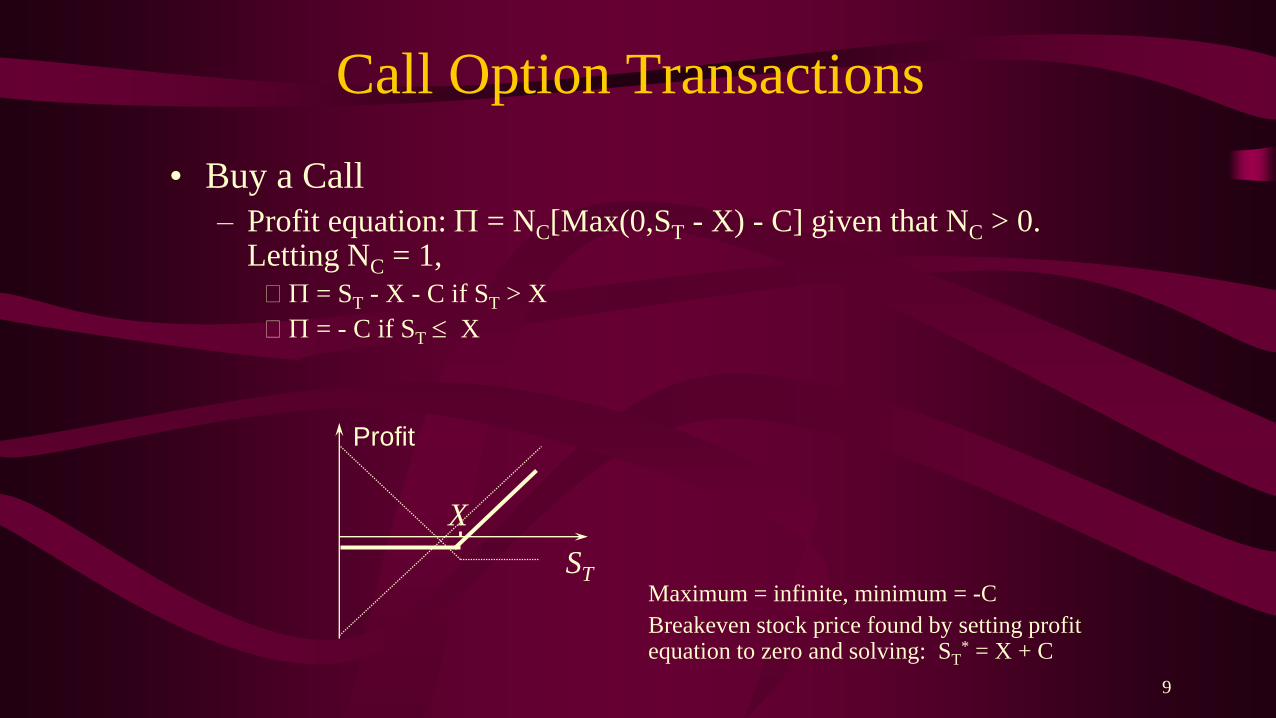

• Buy a Call

– Profit equation: P = NC[Max(0,ST - X) - C] given that NC > 0. Letting NC = 1,

P = ST - X - C if ST > X

P = - C if ST X

Maximum = infinite, minimum = -C

Breakeven stock price found by setting profit equation to zero and solving: ST

* = X + C

ST

X

Profit

10

Call Option Transactions

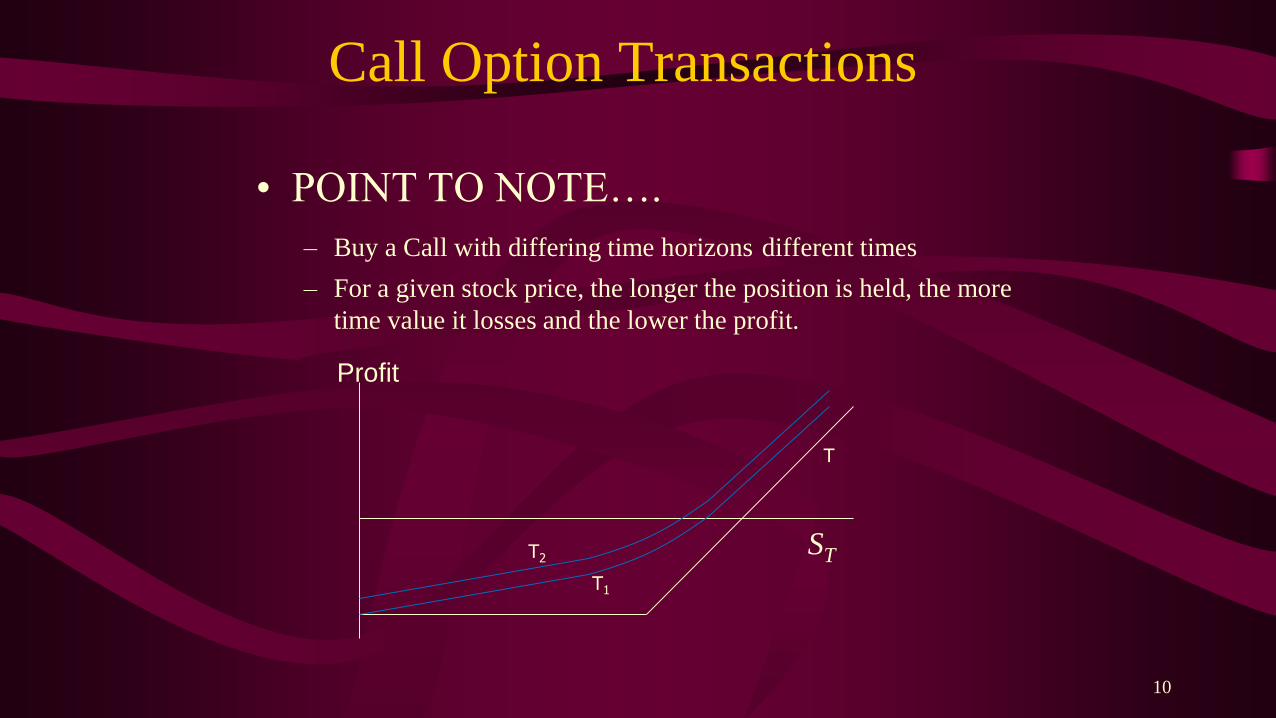

• POINT TO NOTE….

– Buy a Call with differing time horizons different times

– For a given stock price, the longer the position is held, the more

time value it losses and the lower the profit.

T

T1

T2ST

Profit

11

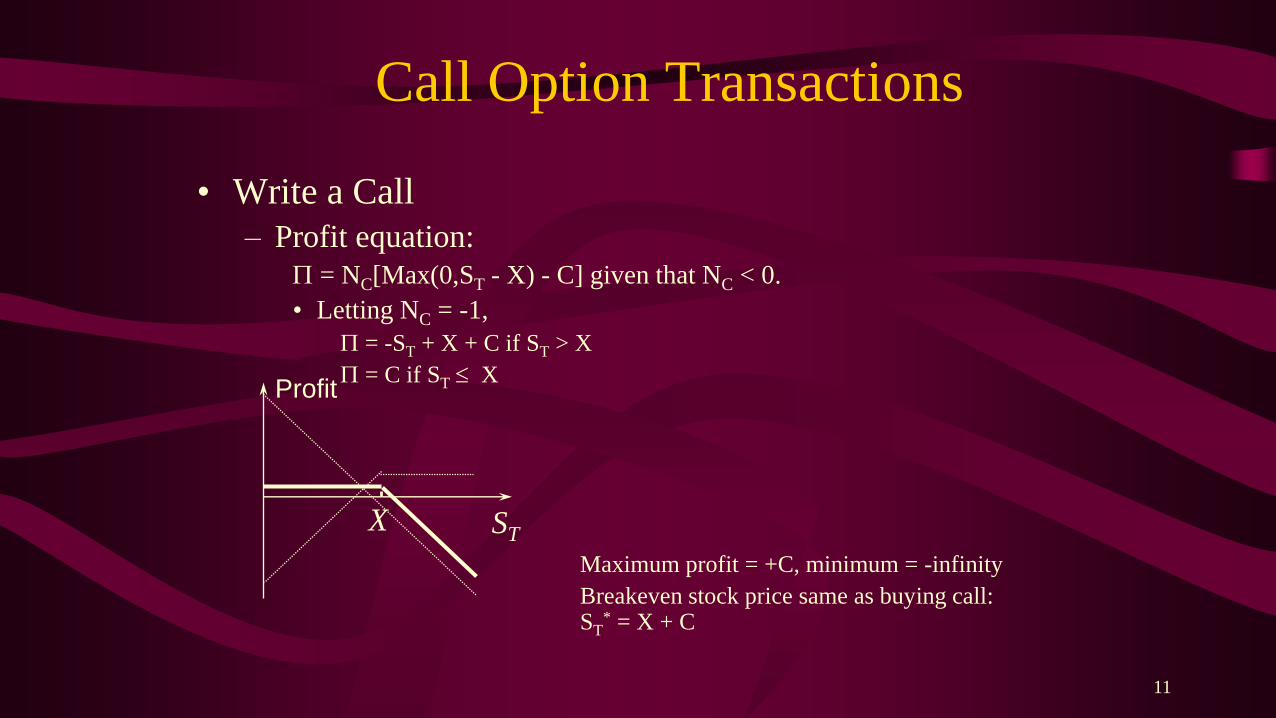

Call Option Transactions

• Write a Call

– Profit equation:

P = NC[Max(0,ST - X) - C] given that NC < 0.

• Letting NC = -1,

P = -ST + X + C if ST > X

P = C if ST X

Maximum profit = +C, minimum = -infinity

Breakeven stock price same as buying call: ST

* = X + C

Profit

STX

12

Put Option Transactions

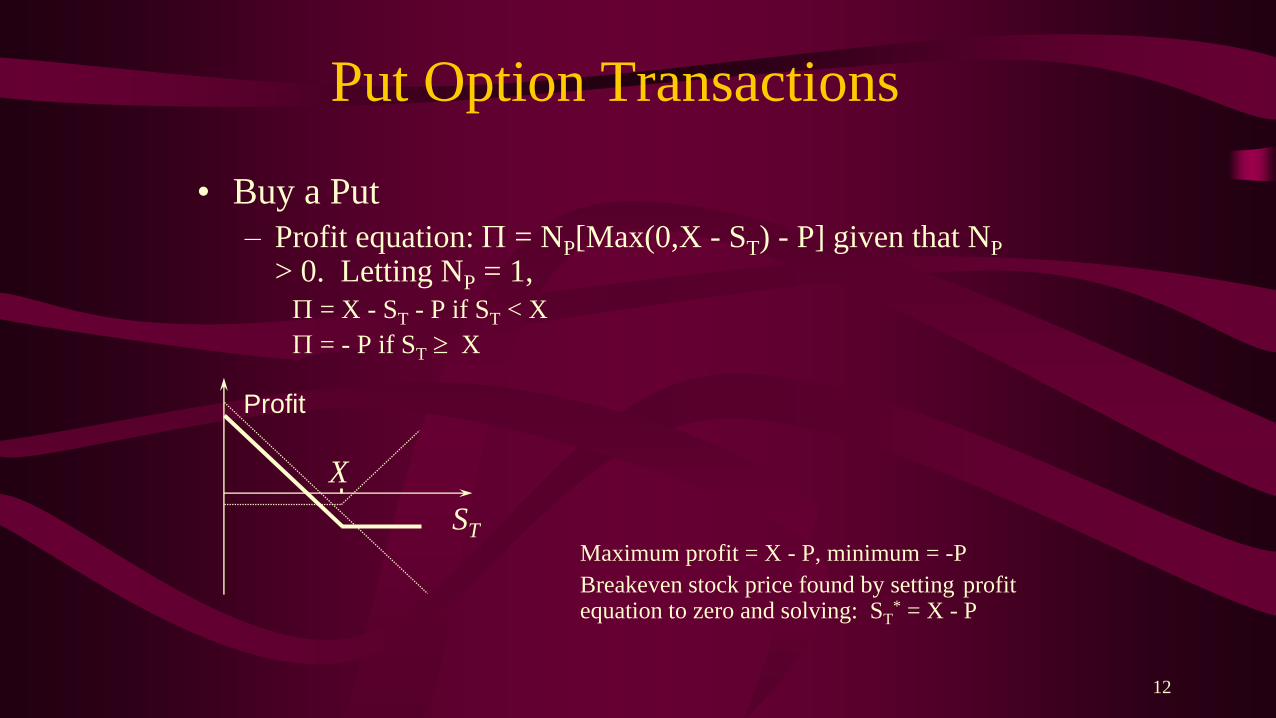

• Buy a Put

– Profit equation: P = NP[Max(0,X - ST) - P] given that NP

> 0. Letting NP = 1,

P = X - ST - P if ST < X

P = - P if ST X

Maximum profit = X - P, minimum = -P

Breakeven stock price found by setting profit equation to zero and solving: ST

* = X - P

Profit

ST

X

13

Put Option Transactions

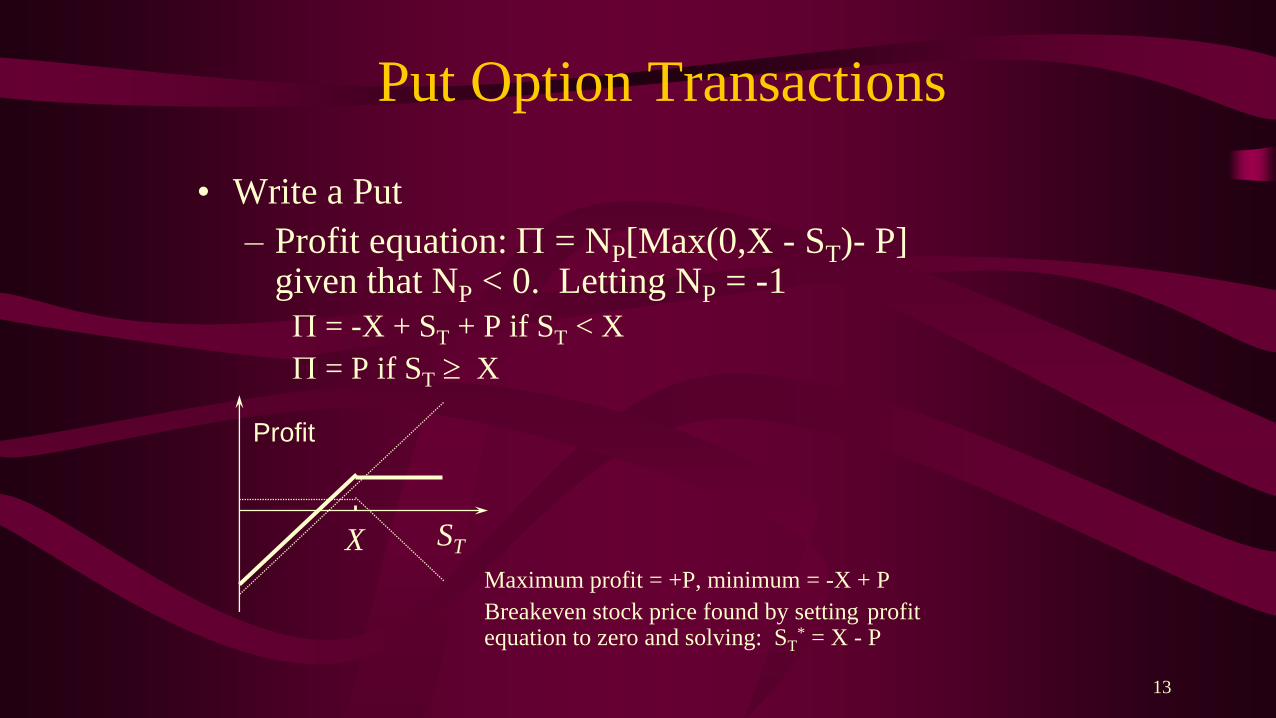

• Write a Put

– Profit equation: P = NP[Max(0,X - ST)- P] given that NP < 0. Letting NP = -1

P = -X + ST + P if ST < X

P = P if ST X

Maximum profit = +P, minimum = -X + P

Breakeven stock price found by setting profit equation to zero and solving: ST

* = X - P

Profit

STX

14

Holding Single Positions

– Buying a stock, taking a call or writing a put is a bullish strategy

– Short selling a stock, writing a call or taking a put is a bearish

strategy.

– If we were now to combine more than one instrument with

offsetting values this usually leads to hedging partial risk

15

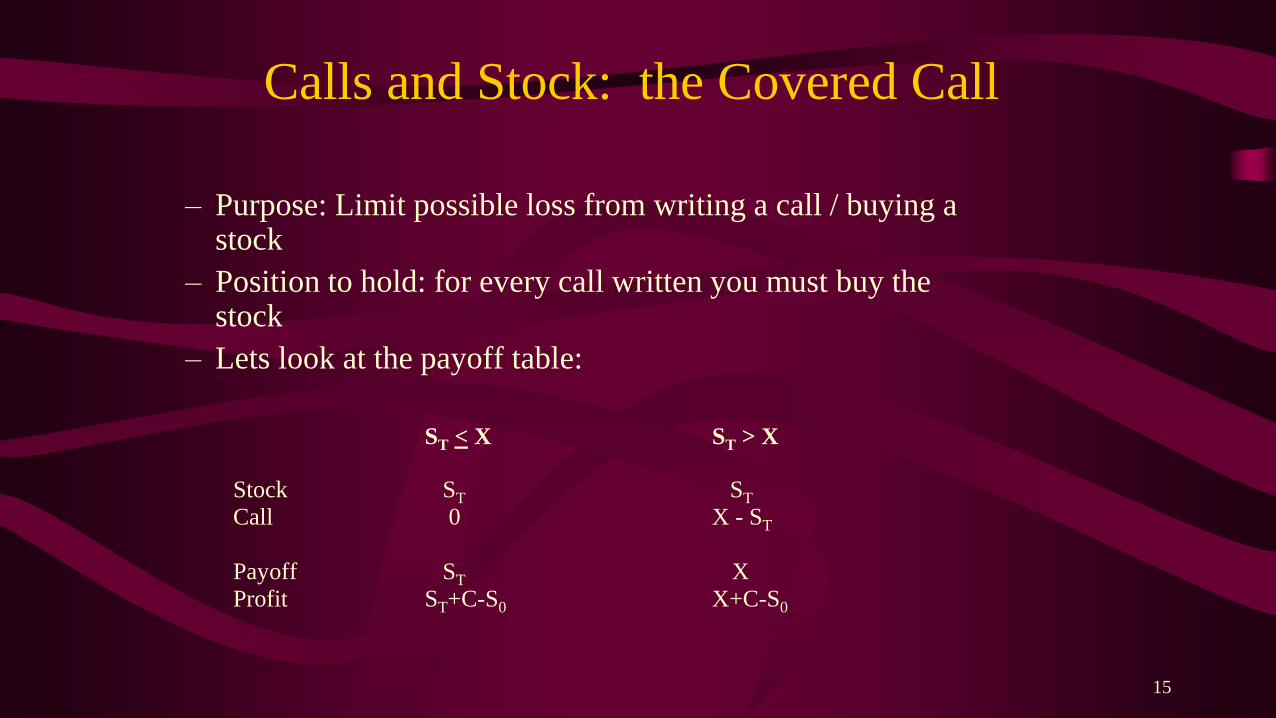

Calls and Stock: the Covered Call

– Purpose: Limit possible loss from writing a call / buying a stock

– Position to hold: for every call written you must buy the stock

– Lets look at the payoff table:

ST < X ST > X

Stock ST ST

Call 0 X - ST

Payoff ST X

Profit ST+C-S0 X+C-S0

16

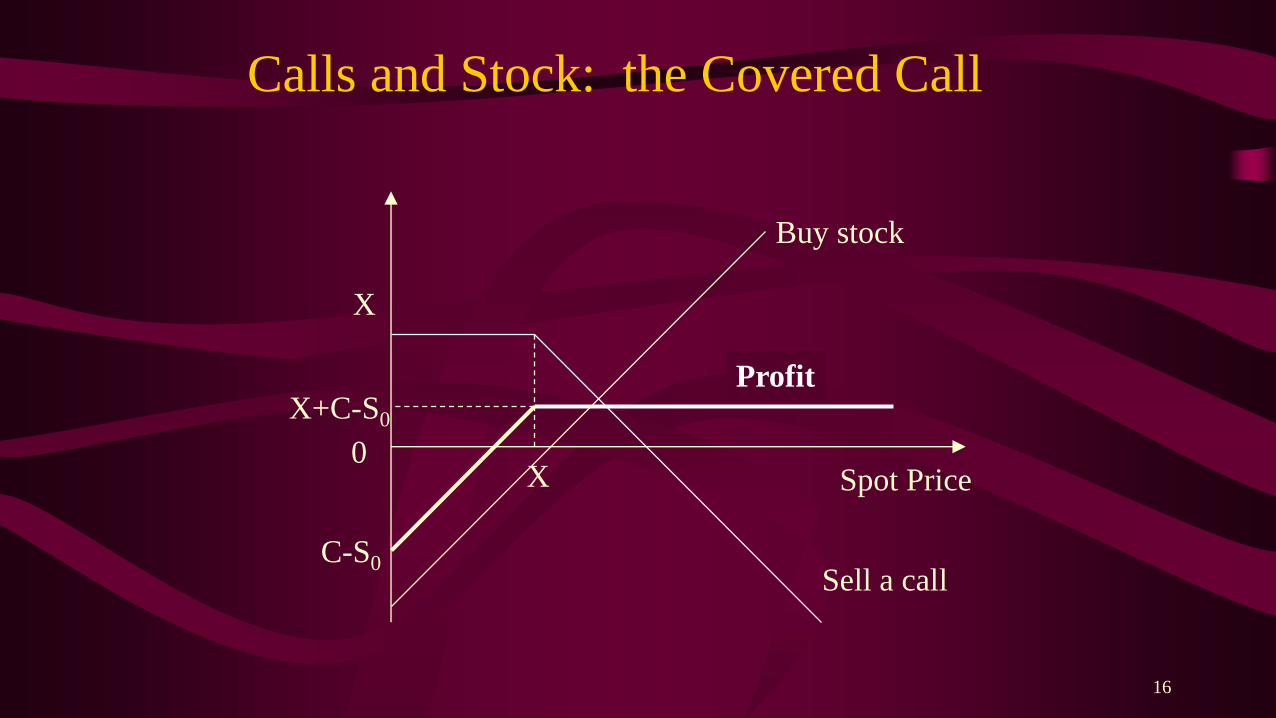

Calls and Stock: the Covered Call

Spot PriceX

X

C-S0

0

X+C-S0

Profit

Sell a call

Buy stock

17

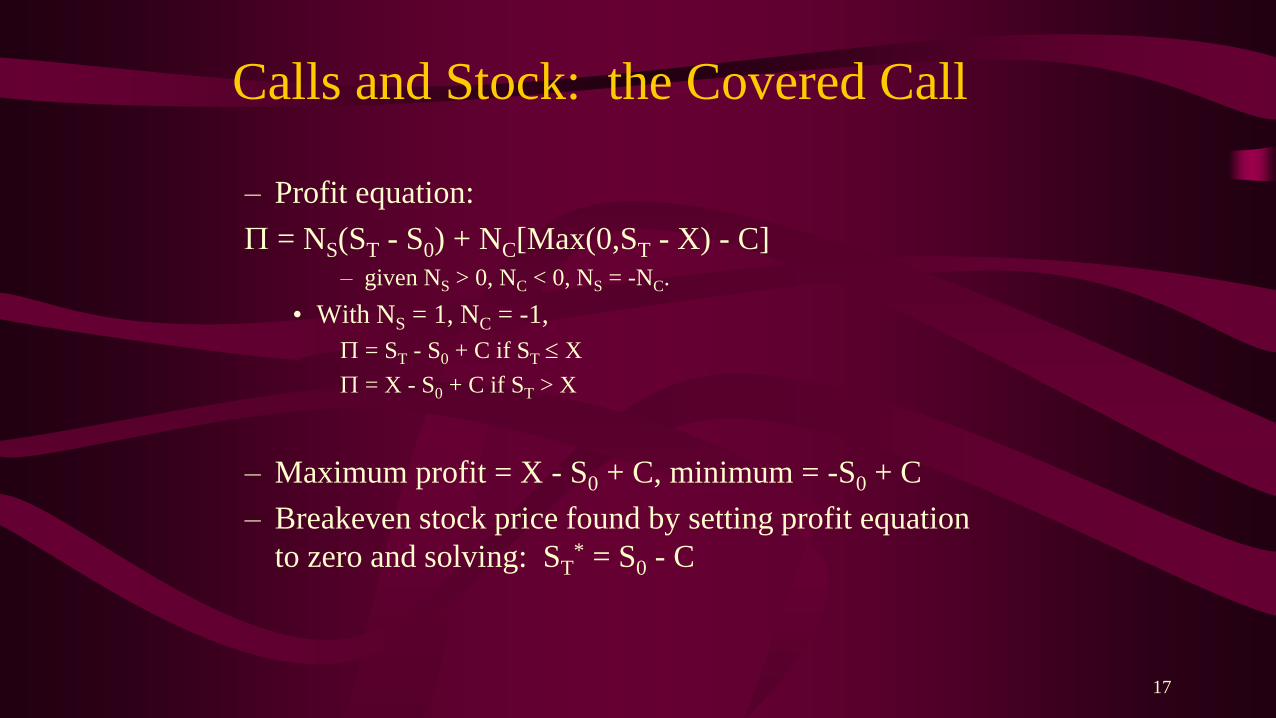

Calls and Stock: the Covered Call

– Profit equation:

P = NS(ST - S0) + NC[Max(0,ST - X) - C] – given NS > 0, NC < 0, NS = -NC.

• With NS = 1, NC = -1,

P = ST - S0 + C if ST X

P = X - S0 + C if ST > X

– Maximum profit = X - S0 + C, minimum = -S0 + C

– Breakeven stock price found by setting profit equation

to zero and solving: ST* = S0 - C

18

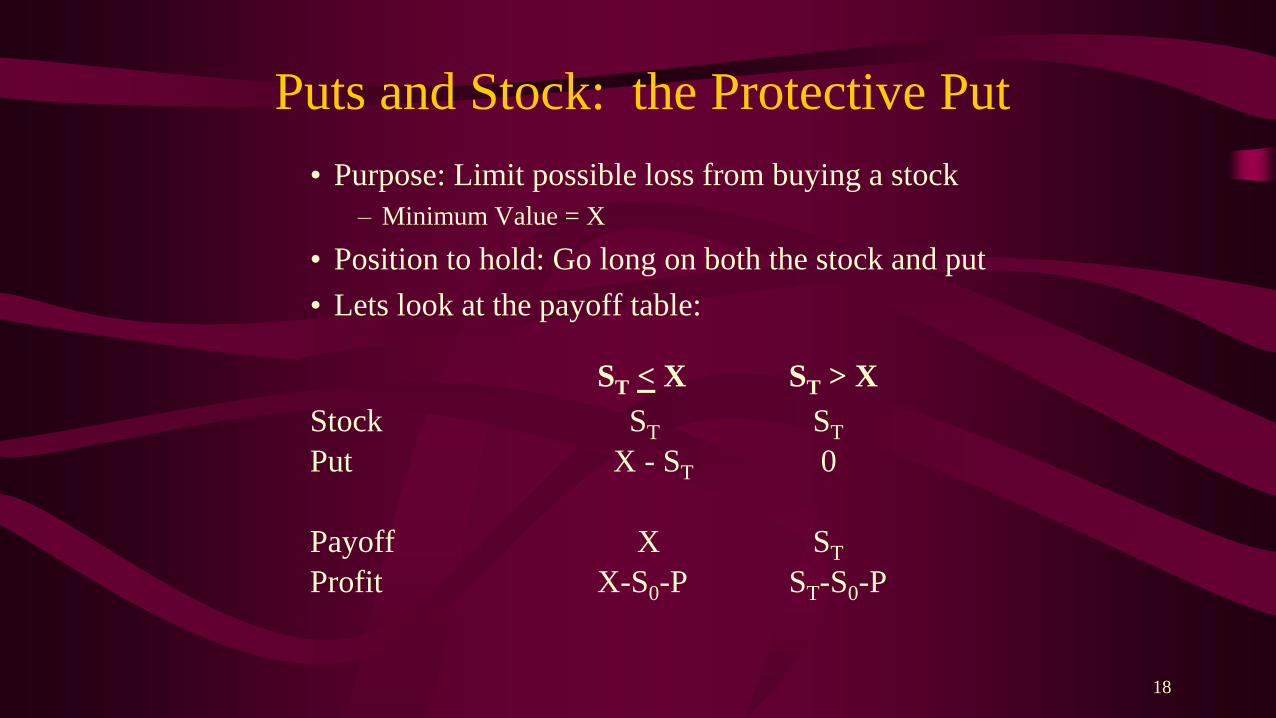

Puts and Stock: the Protective Put

• Purpose: Limit possible loss from buying a stock

– Minimum Value = X

• Position to hold: Go long on both the stock and put

• Lets look at the payoff table:

ST < X ST > X

Stock ST ST

Put X - ST 0

Payoff X ST

Profit X-S0-P ST-S0-P

19

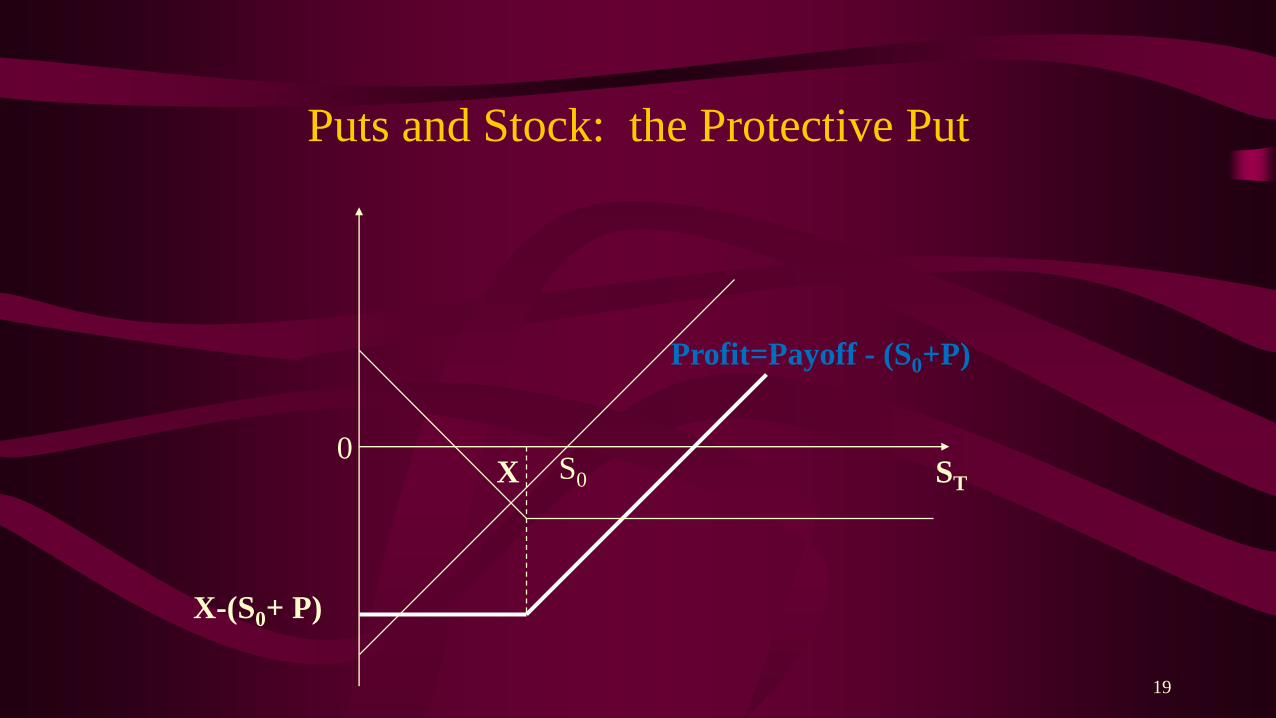

Puts and Stock: the Protective Put

STX

Profit=Payoff - (S0+P)

0S0

X-(S0+ P)

20

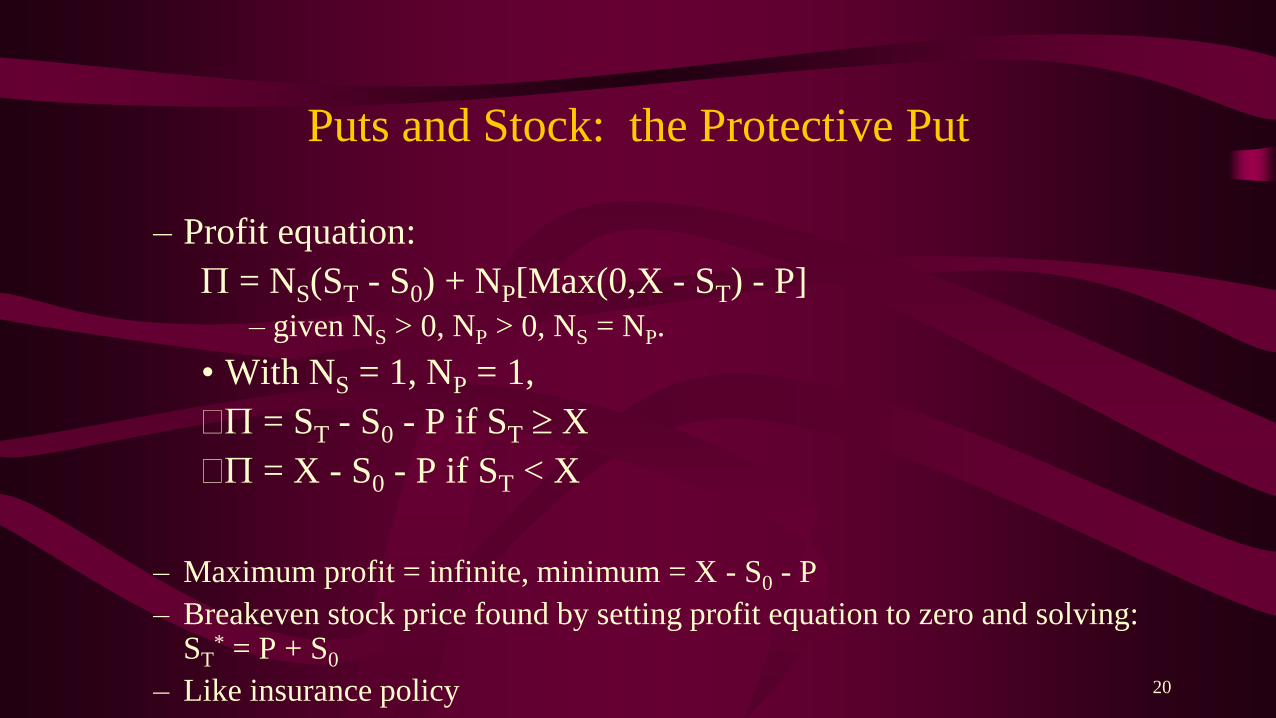

Puts and Stock: the Protective Put

– Profit equation:

P = NS(ST - S0) + NP[Max(0,X - ST) - P]

– given NS > 0, NP > 0, NS = NP.

• With NS = 1, NP = 1,

P = ST - S0 - P if ST X

P = X - S0 - P if ST < X

– Maximum profit = infinite, minimum = X - S0 - P

– Breakeven stock price found by setting profit equation to zero and solving: ST

* = P + S0

– Like insurance policy

21

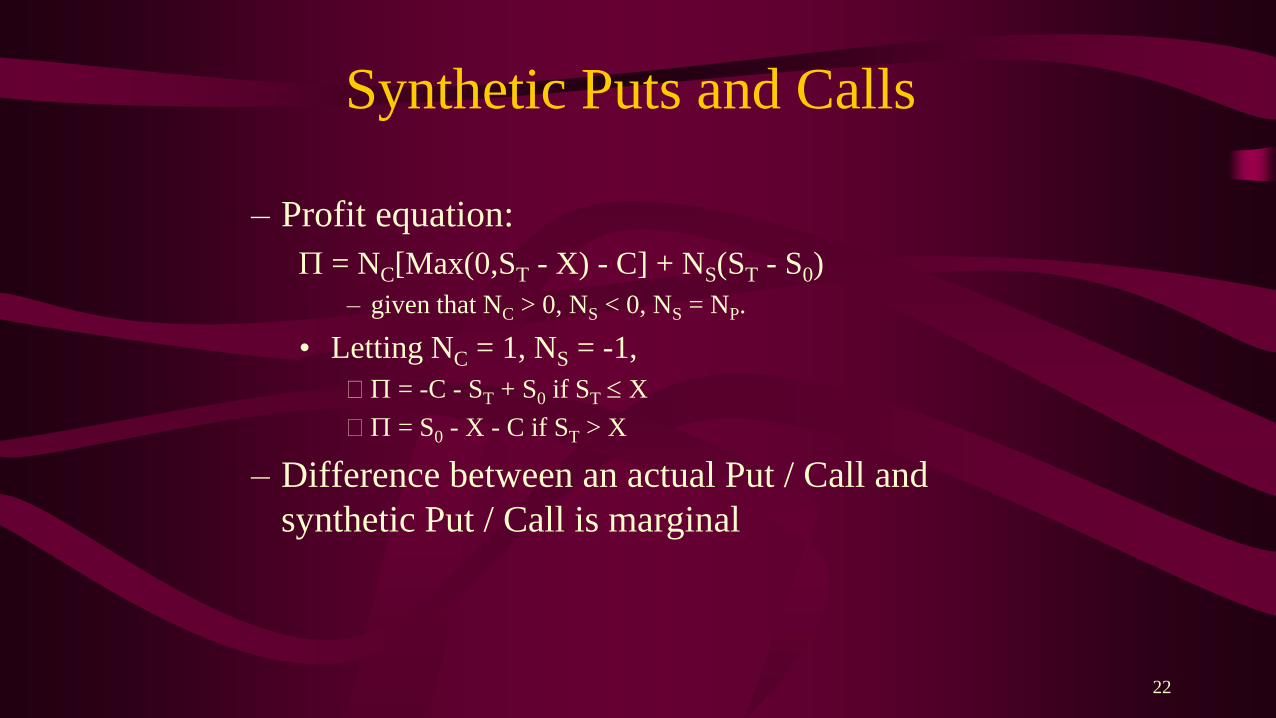

Synthetic Puts and Calls

– Rearranging put-call parity to isolate put price

– This implies put = long call, short stock, long risk-free

bond with face value X.

– This is a synthetic put.

– In practice most synthetic puts are constructed without

risk-free bond, i.e., long call, short stock.

Tr

0cXeSCP

22

Synthetic Puts and Calls

– Profit equation:

P = NC[Max(0,ST - X) - C] + NS(ST - S0)

– given that NC > 0, NS < 0, NS = NP.

• Letting NC = 1, NS = -1,

P = -C - ST + S0 if ST X

P = S0 - X - C if ST > X

– Difference between an actual Put / Call and

synthetic Put / Call is marginal

23

Option Spreads: Basic Concepts

• Holding Multiple Calls or Puts with differing exercise prices or time to expiration

• A Money Spread is taking one option and writing another at the same time with different exercise prices.

– The bull spread

– The bear spread

• A time spread is where one takes and writes options at the same time with differing expiration dates.

– The calendar spread

24

Option Spreads: Basic Concepts

• Why do Investors Use Option Spreads?

– Risk reduction

– To lower the cost of a long position

– Types of spreads

• bull spread

• bear spread

• time spread is based on volatility

25

Option Spreads: Basic Concepts

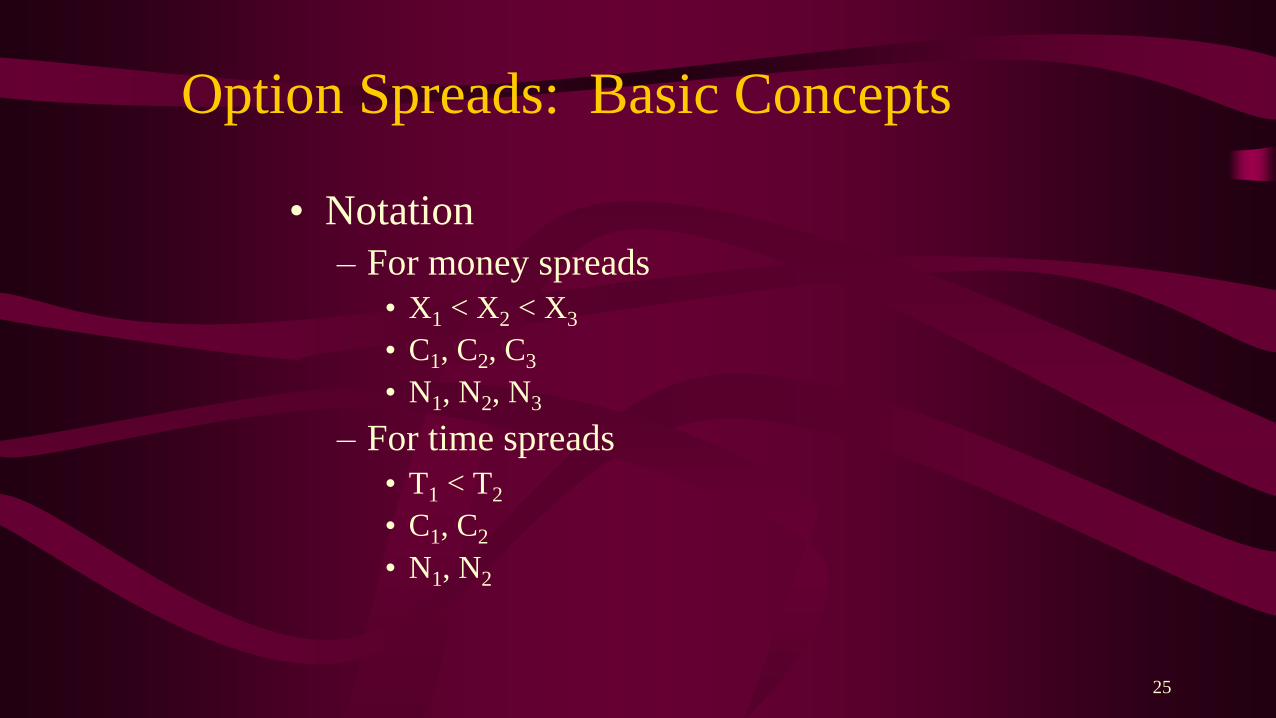

• Notation

– For money spreads

• X1 < X2 < X3

• C1, C2, C3

• N1, N2, N3

– For time spreads

• T1 < T2

• C1, C2

• N1, N2

26

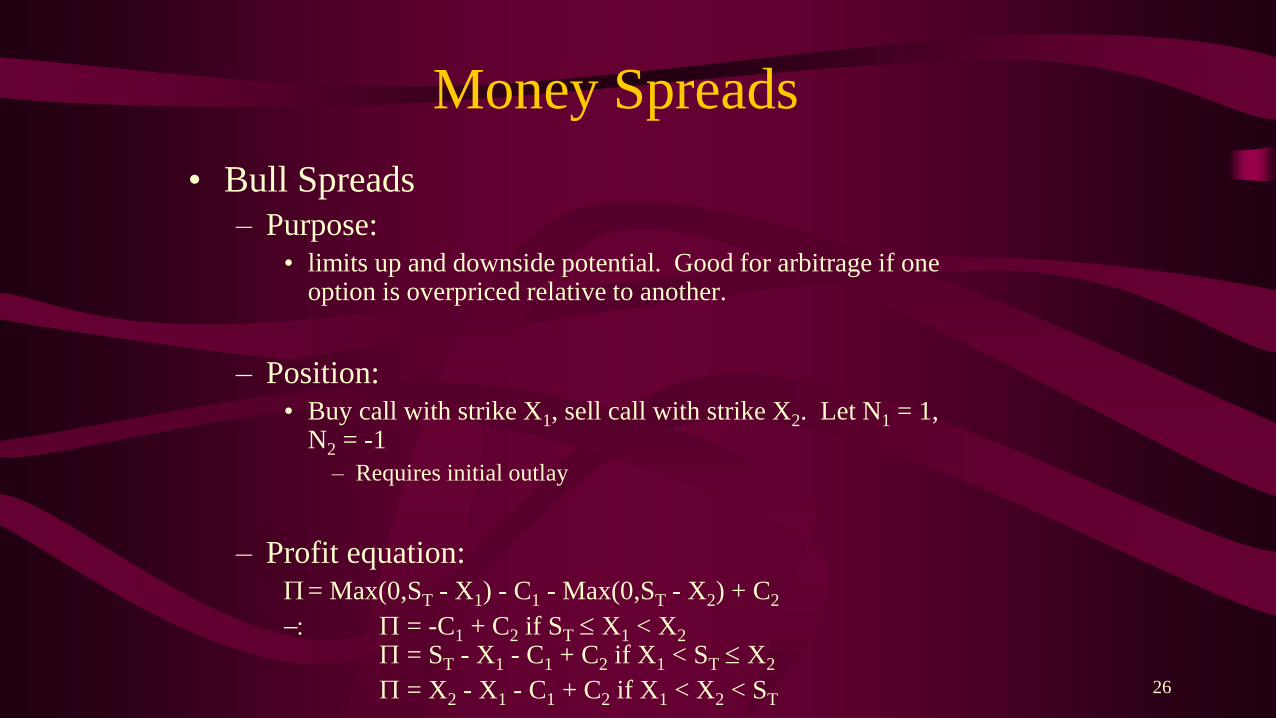

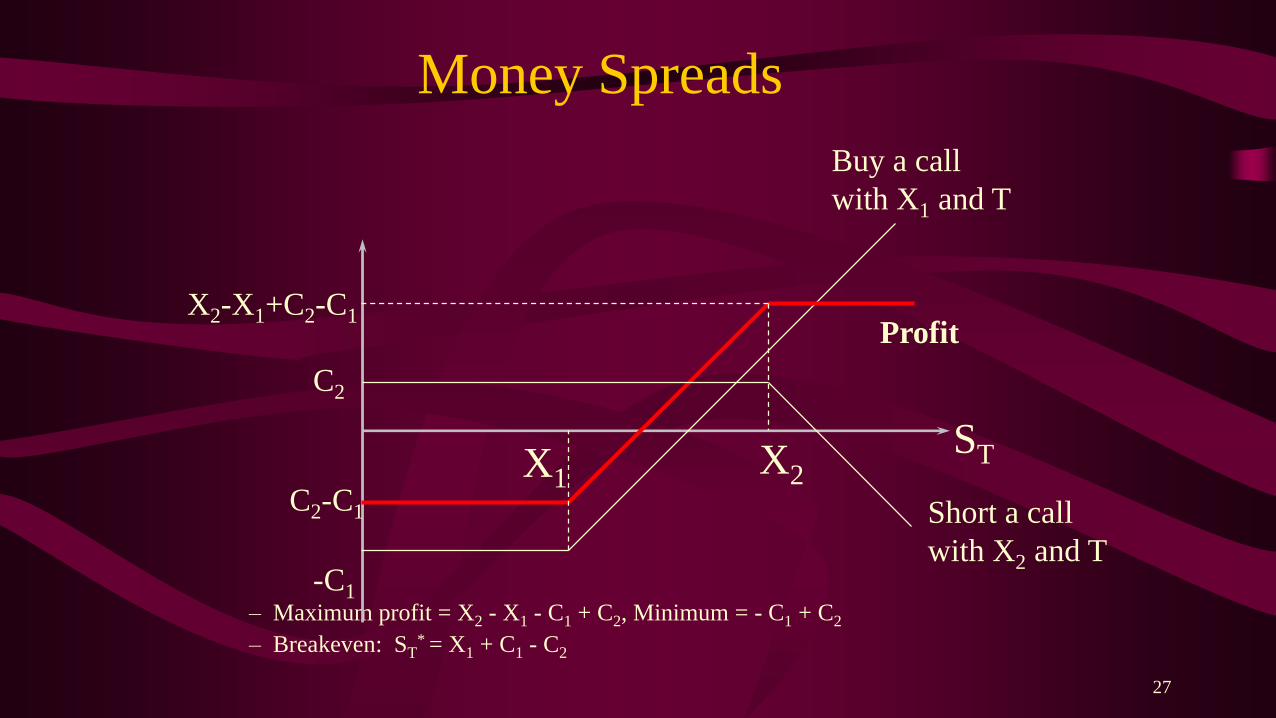

Money Spreads

• Bull Spreads

– Purpose:

• limits up and downside potential. Good for arbitrage if one option is overpriced relative to another.

– Position:

• Buy call with strike X1, sell call with strike X2. Let N1 = 1, N2 = -1

– Requires initial outlay

– Profit equation:

P= Max(0,ST - X1) - C1 - Max(0,ST - X2) + C2

: P = -C1 + C2 if ST X1 < X2

P = ST - X1 - C1 + C2 if X1 < ST X2

P = X2 - X1 - C1 + C2 if X1 < X2 < ST

27

Money Spreads

– Maximum profit = X2 - X1 - C1 + C2, Minimum = - C1 + C2

– Breakeven: ST* = X1 + C1 - C2

X1X2

ST

-C1

C2

Short a call

with X2 and T

Buy a call

with X1 and T

ProfitX2-X1+C2-C1

C2-C1

28

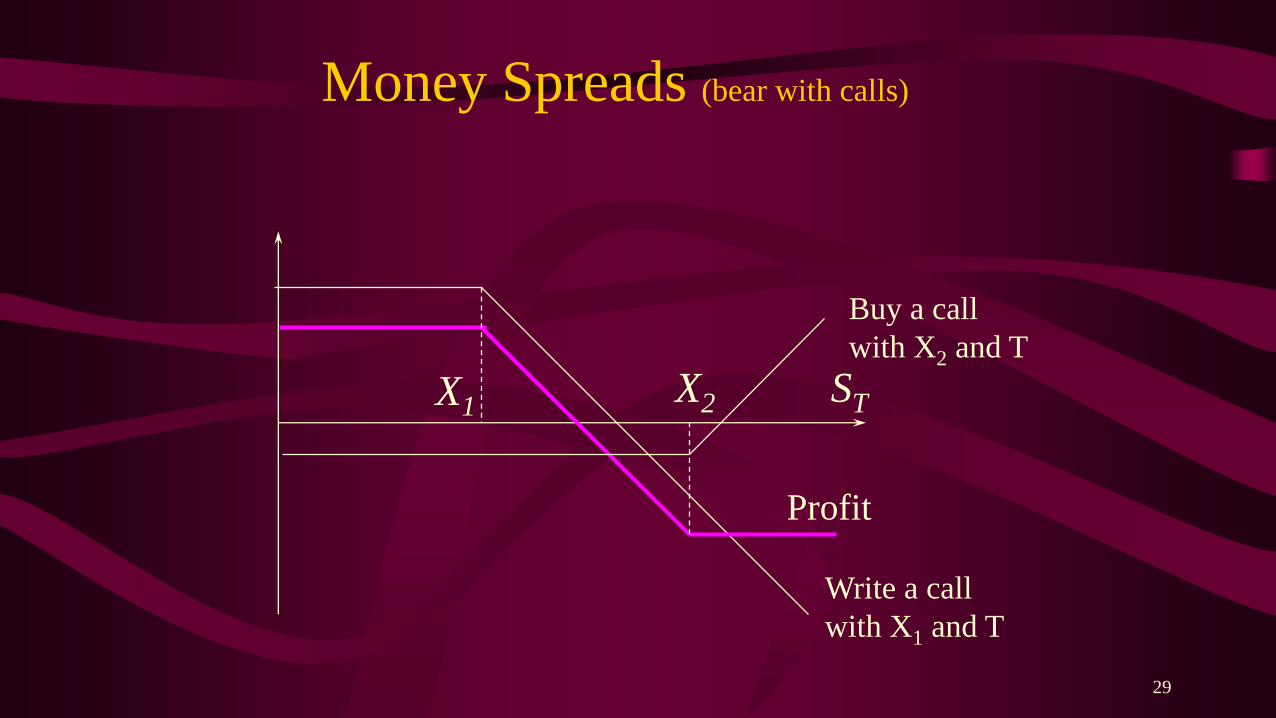

Money Spreads

• Bear Spread using calls

– Purpose:

• Benefit from speculation of a stock price fall, but

with limited up / downward potential

– Position:

• Take a call with X2 and writing another with X1

• Note: Call bought costs less than call written

29

Money Spreads (bear with calls)

X1X2

Profit

ST

Buy a call

with X2 and T

Write a call

with X1 and T

30

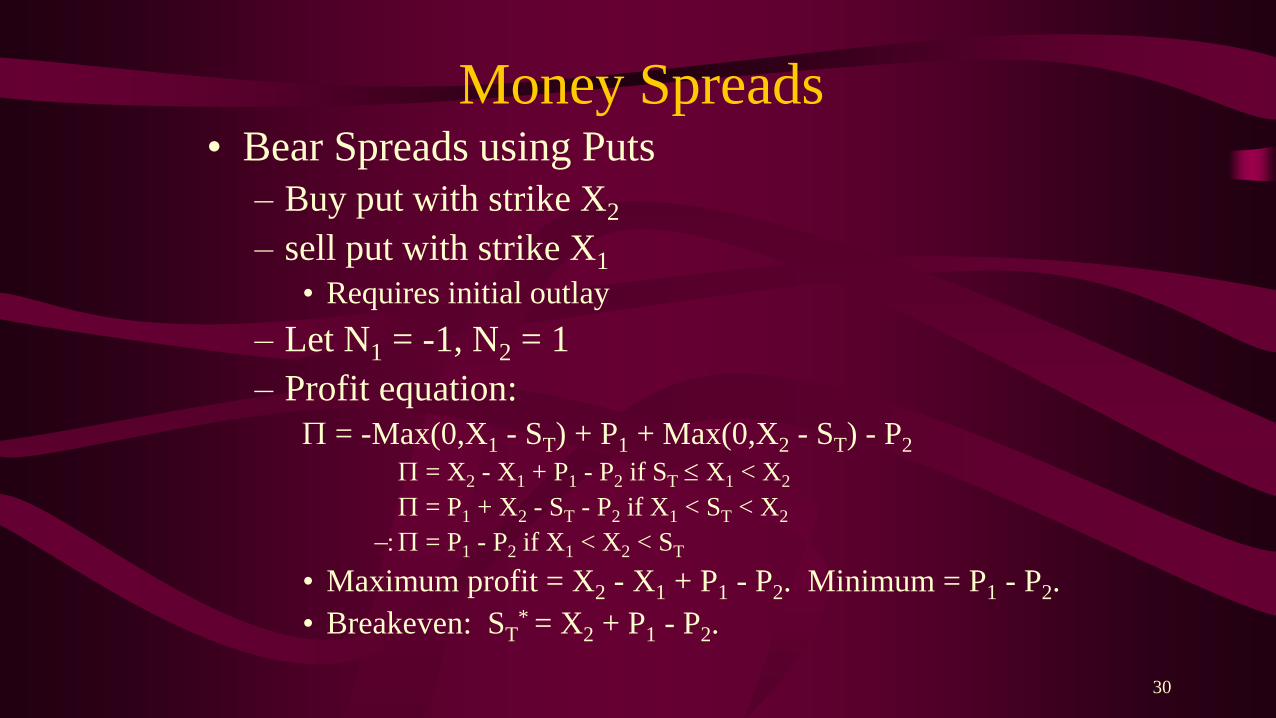

Money Spreads• Bear Spreads using Puts

– Buy put with strike X2

– sell put with strike X1

• Requires initial outlay

– Let N1 = -1, N2 = 1

– Profit equation:

P = -Max(0,X1 - ST) + P1 + Max(0,X2 - ST) - P2

P = X2 - X1 + P1 - P2 if ST X1 < X2

P = P1 + X2 - ST - P2 if X1 < ST < X2

:P = P1 - P2 if X1 < X2 < ST

• Maximum profit = X2 - X1 + P1 - P2. Minimum = P1 - P2.

• Breakeven: ST* = X2 + P1 - P2.

31

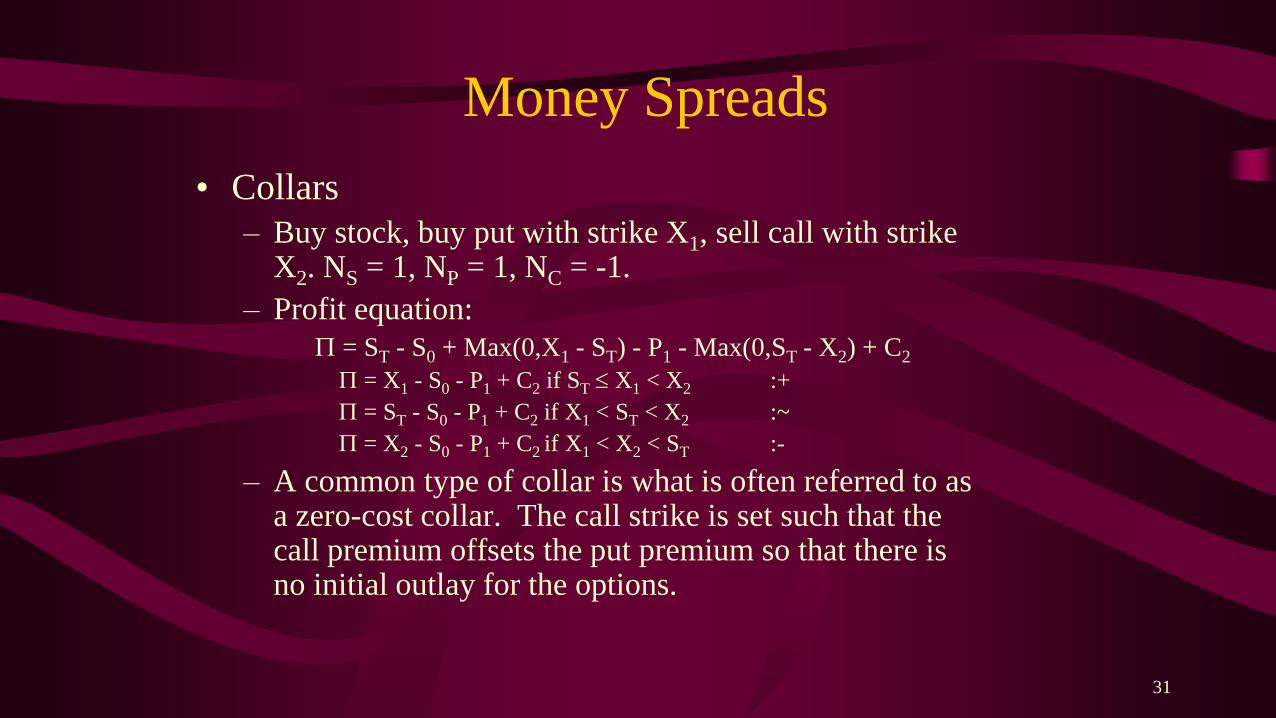

Money Spreads

• Collars

– Buy stock, buy put with strike X1, sell call with strike X2. NS = 1, NP = 1, NC = -1.

– Profit equation:

P = ST - S0 + Max(0,X1 - ST) - P1 - Max(0,ST - X2) + C2

P = X1 - S0 - P1 + C2 if ST X1 < X2 :+

P = ST - S0 - P1 + C2 if X1 < ST < X2 :~

P = X2 - S0 - P1 + C2 if X1 < X2 < ST :-

– A common type of collar is what is often referred to as a zero-cost collar. The call strike is set such that the call premium offsets the put premium so that there is no initial outlay for the options.

32

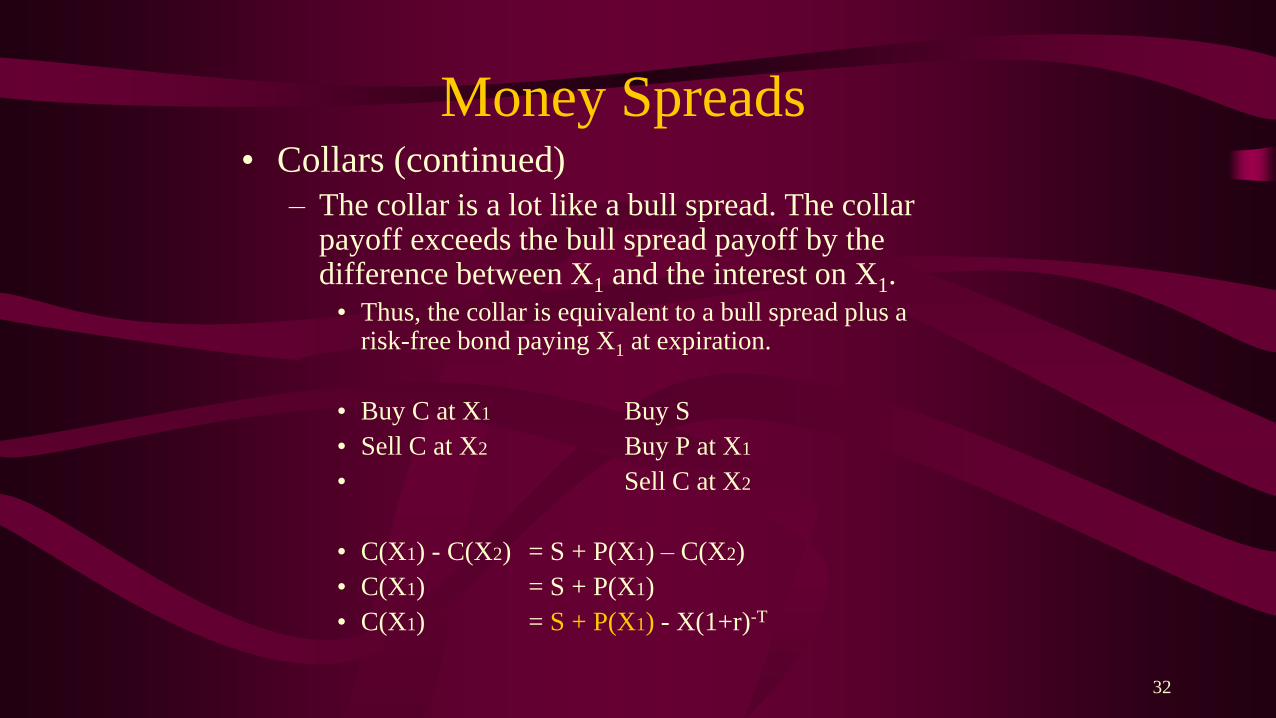

Money Spreads• Collars (continued)

– The collar is a lot like a bull spread. The collar payoff exceeds the bull spread payoff by the difference between X1 and the interest on X1.

• Thus, the collar is equivalent to a bull spread plus a risk-free bond paying X1 at expiration.

• Buy C at X1 Buy S

• Sell C at X2 Buy P at X1

• Sell C at X2

• C(X1) - C(X2) = S + P(X1) – C(X2)

• C(X1) = S + P(X1)

• C(X1) = S + P(X1) - X(1+r)-T

33

Money Spreads

• Butterfly Spreads

– Purpose:

• Speculate that large stock price movements are unlikely

– Position:

• Buy call with strike X1, buy call with strike X3, sell two calls with strike X2. Let N1 = 1, N2 = -2, N3 = 1.

– Profit equation:

P = Max(0,ST - X1) - C1 - 2Max(0,ST - X2) + 2C2 + Max(0,ST - X3) - C3

:P = -C1 + 2C2 - C3 if ST X1 < X2 < X3

< :P = ST - X1 - C1 + 2C2 - C3 if X1 < ST X2 < X3

> :P = -ST +2X2 - X1 - C1 + 2C2 - C3 if X1 < X2 < ST X3

:P = -X1 + 2X2 - X3 - C1 + 2C2 - C3 if X1 < X2 < X3 < ST

34

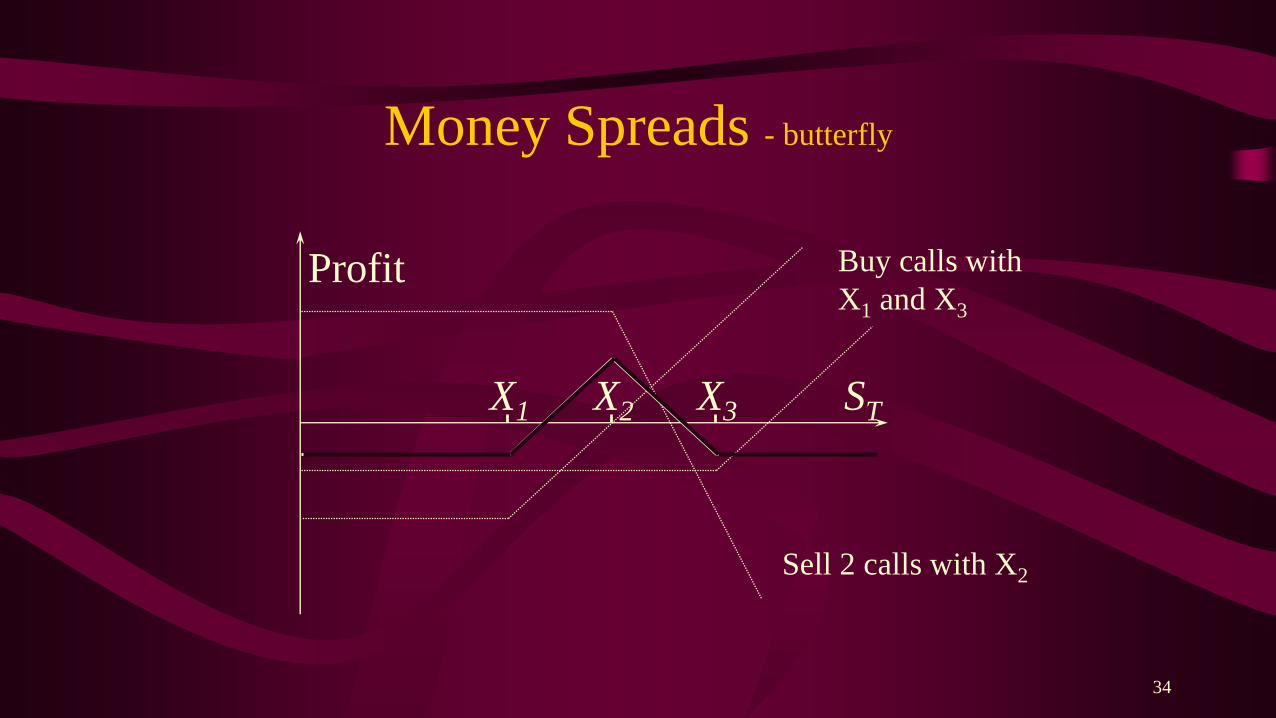

Money Spreads - butterfly

X1 X3

Profit

STX2

Buy calls with

X1 and X3

Sell 2 calls with X2

35

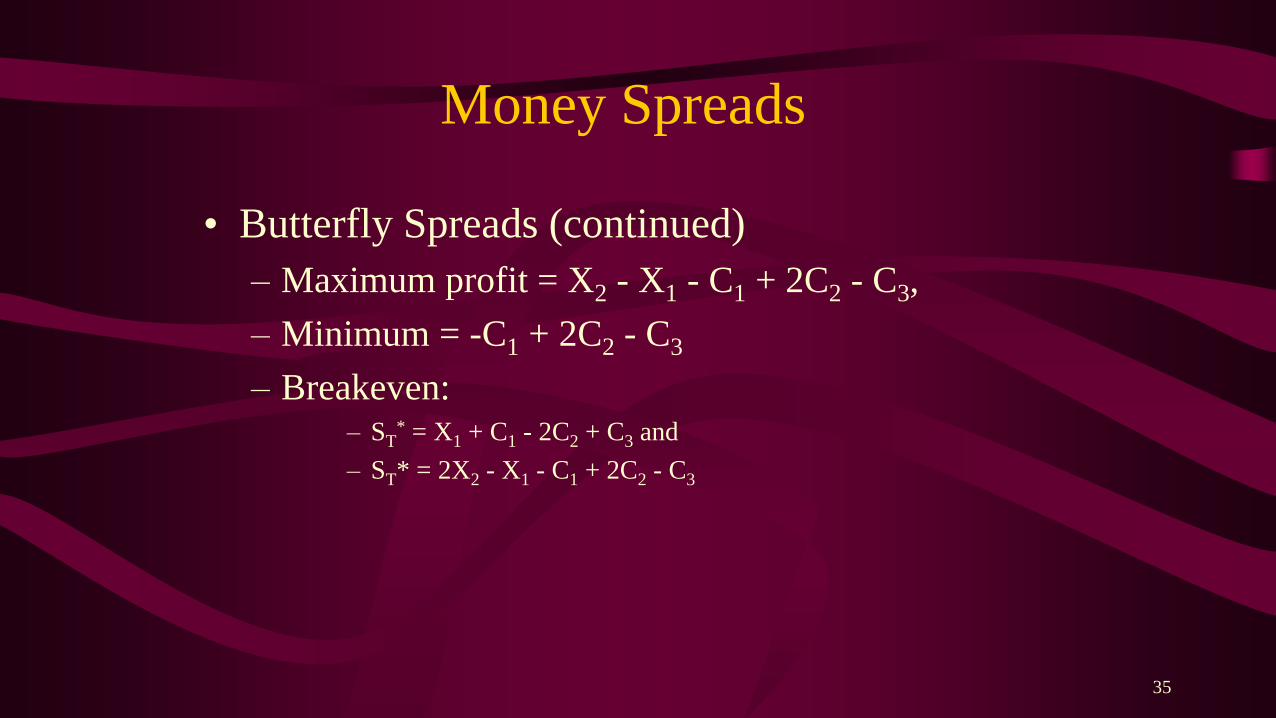

Money Spreads

• Butterfly Spreads (continued)

– Maximum profit = X2 - X1 - C1 + 2C2 - C3,

– Minimum = -C1 + 2C2 - C3

– Breakeven: – ST

* = X1 + C1 - 2C2 + C3 and

– ST* = 2X2 - X1 - C1 + 2C2 - C3

36

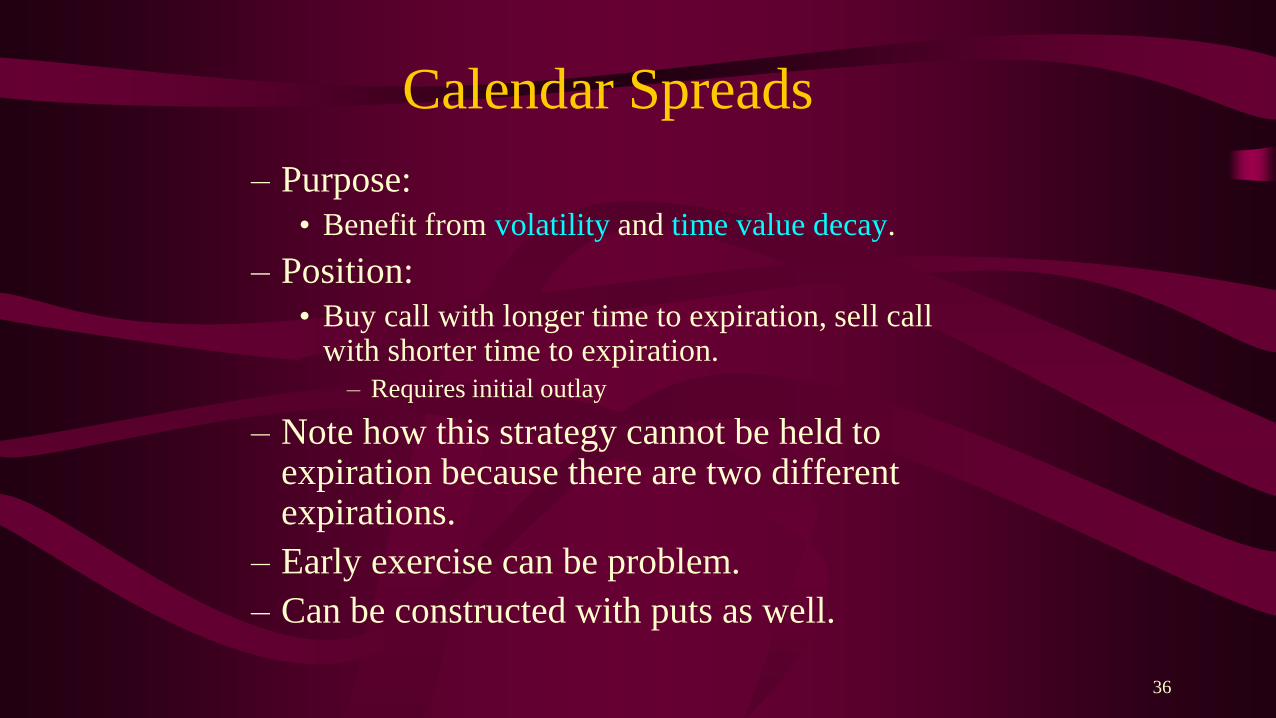

Calendar Spreads

– Purpose:

• Benefit from volatility and time value decay.

– Position:

• Buy call with longer time to expiration, sell call with shorter time to expiration.

– Requires initial outlay

– Note how this strategy cannot be held to expiration because there are two different expirations.

– Early exercise can be problem.

– Can be constructed with puts as well.

37

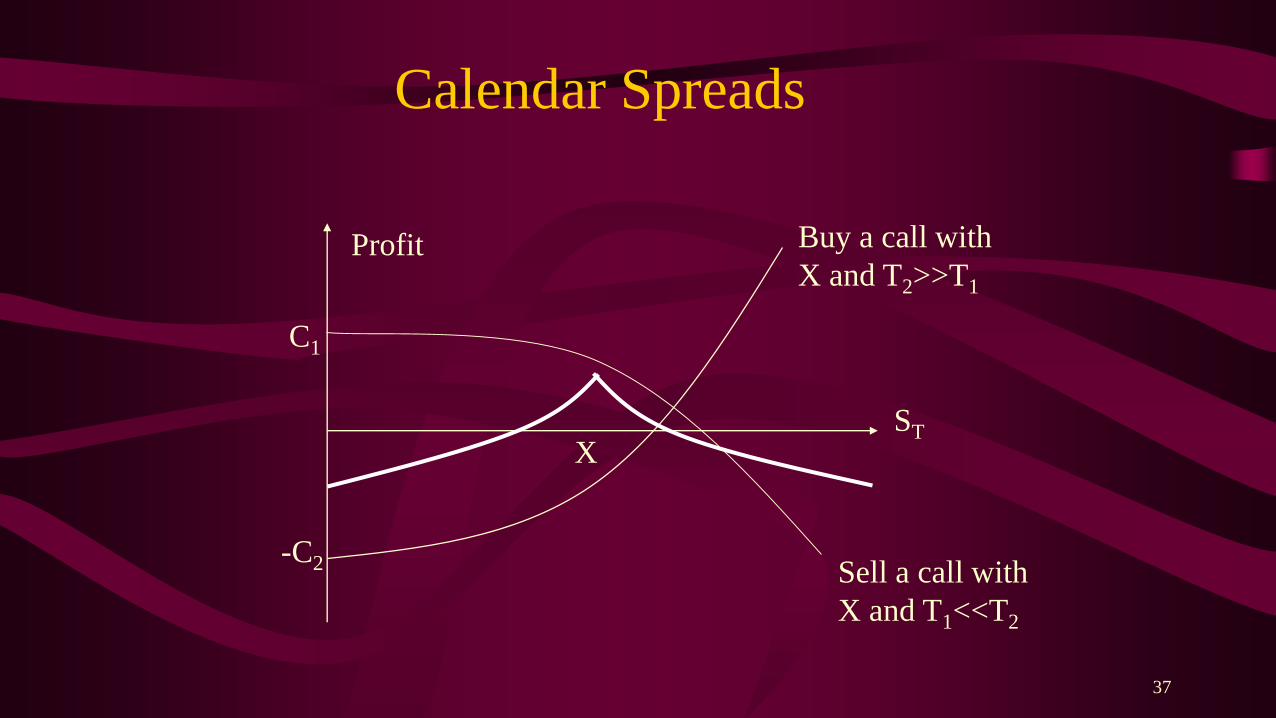

Calendar Spreads

Profit

X

Sell a call with

X and T1<<T2

Buy a call with

X and T2>>T1

ST

C1

-C2

38

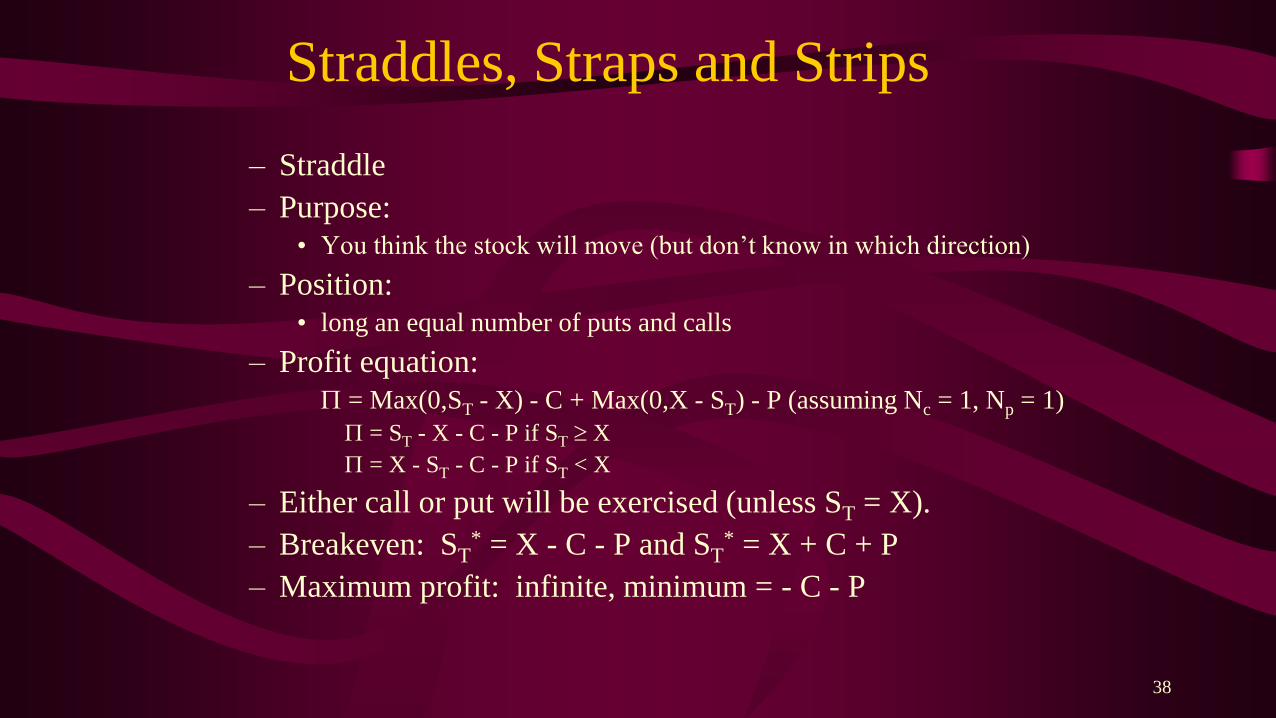

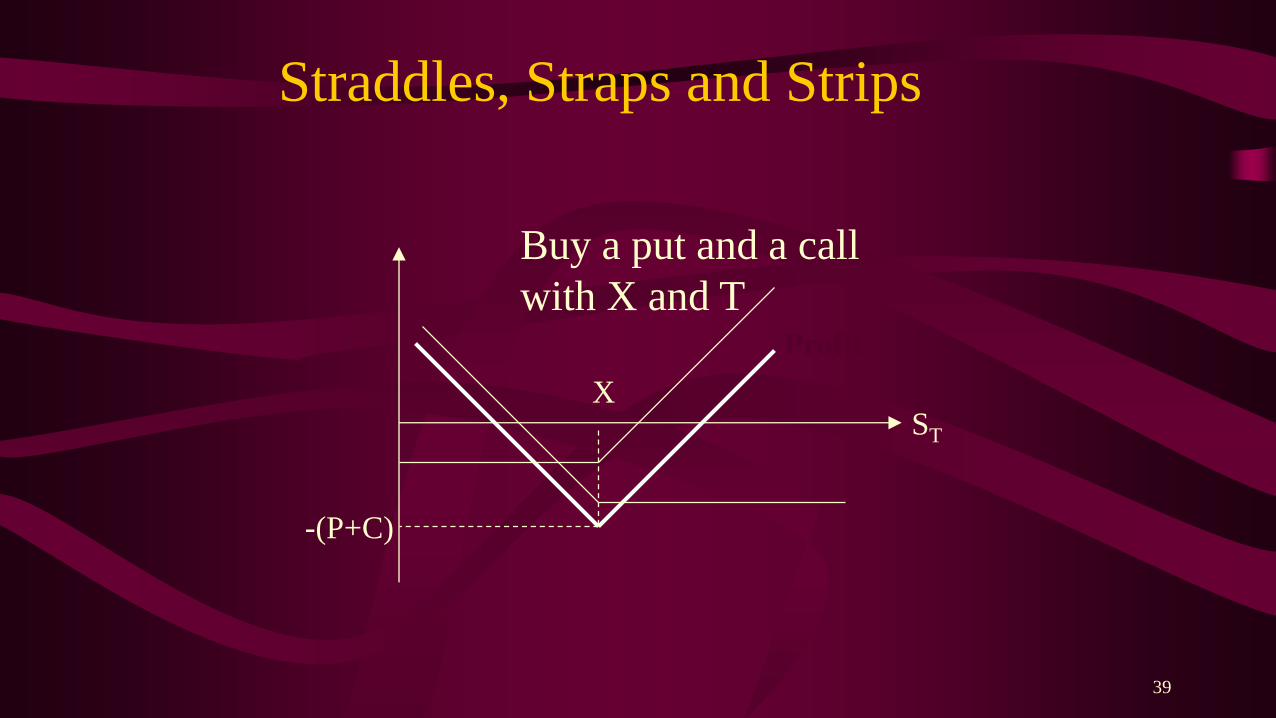

Straddles, Straps and Strips

– Straddle

– Purpose:

• You think the stock will move (but don’t know in which direction)

– Position:

• long an equal number of puts and calls

– Profit equation:

P = Max(0,ST - X) - C + Max(0,X - ST) - P (assuming Nc = 1, Np = 1)

P = ST - X - C - P if ST X

P = X - ST - C - P if ST < X

– Either call or put will be exercised (unless ST = X).

– Breakeven: ST* = X - C - P and ST

* = X + C + P

– Maximum profit: infinite, minimum = - C - P

39

Straddles, Straps and Strips

Profit

XST

-(P+C)

Buy a put and a call

with X and T

40

Straddles, Straps and Strips

• Applications of Straddles

– Based on perception of volatility greater than

priced by market

• A Short Straddle

– Unlimited loss potential

– Based on perception of volatility less than

priced by market

41

Straddles, Straps and Strips

• Straps

– Purpose:

• Doubles up bet on stock going up

– Position:

• two long calls and one long put.

– Profit equation:

P = 2Max(0,ST - X) - 2C + Max(0,X - ST) - P (assuming Nc = 2, Np = 1)

: P = 2ST - 2X - 2C - P if ST X

: P = X - ST - 2C - P if ST < X

– Breakeven: ST* = X + C + P/2; ST*=X-2C-P

– Maximum profit = infinite, minimum = -2C - P

42

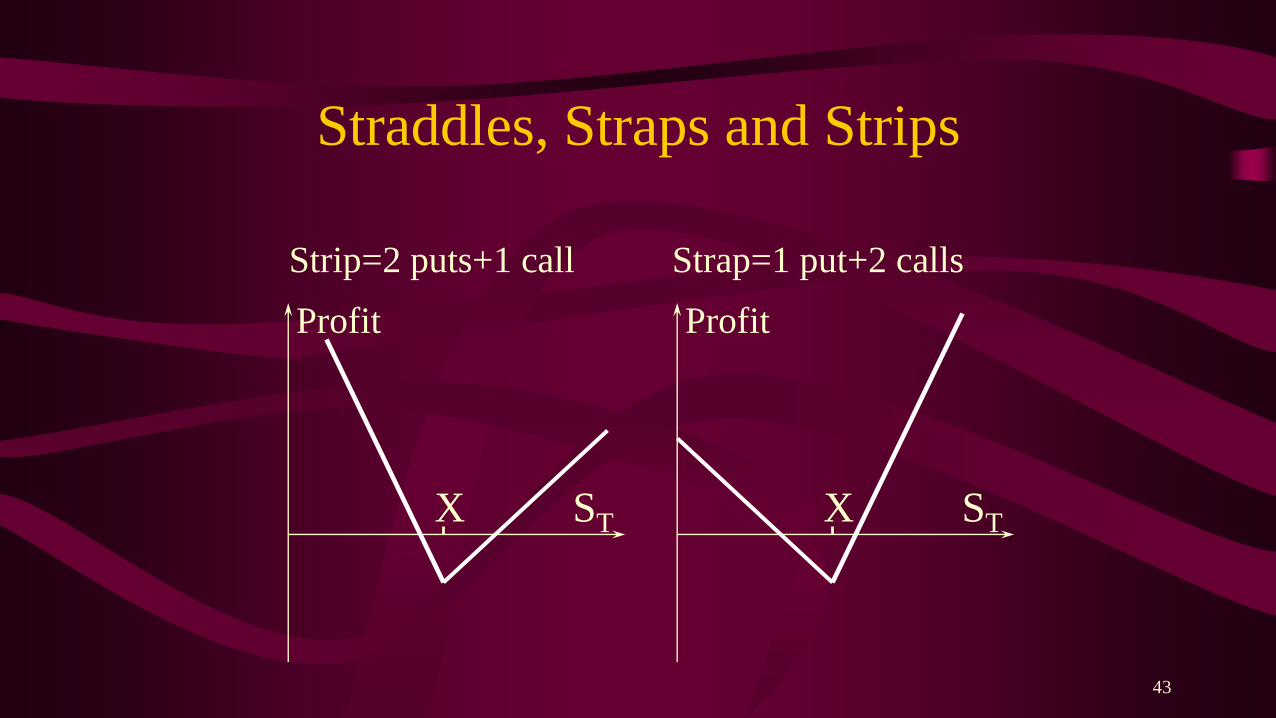

Straddles, Straps and Strips

• Strips

– Purpose:

• Doubles up bet on stock going down

– Position:

• two long puts and one long call.

– Profit equation:

P = Max(0,ST - X) - C + 2Max(0,X - ST) - 2P (assuming Nc = 1, Np = 2)

: P = ST - X - C - 2P if ST X

: P = 2X - 2ST - C - 2P if ST < X

– Breakeven: ST* = X - P - C/2; ST*=X+C+2P

– Maximum profit = infinite, minimum = -2P - C

43

Straddles, Straps and Strips

Profit

X ST

Profit

X ST

Strip=2 puts+1 call Strap=1 put+2 calls

C r e a t i n g a c u l t u r e o f r i s k a w a r e n e s s ®

Global Association ofRisk Professionals

111 Town Square Place14th FloorJersey City, New Jersey 07310U.S.A.+ 1 201.719.7210

2nd FloorBengal Wing9A Devonshire SquareLondon, EC2M 4YNU.K.+ 44 (0) 20 7397 9630

www.garp.org

About GARP | The Global Association of Risk Professionals (GARP) is a not-for-profit global membership organization dedicated to preparing professionals and organizations to make better informed risk decisions. Membership represents over 150,000 risk management practitioners and researchers from banks, investment management firms, government agencies, academic institutions, and corporations from more than 195 countries and territories. GARP administers the Financial Risk Manager (FRM®) and the Energy Risk Professional (ERP®) Exams; certifications recognized by risk professionals worldwide. GARP also helps advance the role of risk management via comprehensive professional education and training for professionals of all levels. www.garp.org.

4 | © 2014 Global Association of Risk Professionals. All rights reserved.