Embed Size (px)

Citation preview

LET'S TALK ABOUT OUR FUTURE.NOW !

Because we shouldn't wait until the damage has been done.

POWER TO THE PEOPLE

occupyfrankfurt.de/eurocrisis

TABLE OF CONTENTS

3 SUMMARY

4 CLARIFICATION

5 ANALYSIS

8 DATA

12 DIAGRAM OF THE EUROCRISIS IN ONE SLIDE ! 13 END SCENARIOS

15 EXPLANATIONS

28 START ASKING QUESTIONS…

2

3

The following review of the economic and fiscal situation of the Euro-zone attempts to make a realistic assessment. Our aim is to educate people about the importance of Europe's current situation and to allow them to form their own opinion.

This review does not represent the views or demands of the Occupy movement.

It does, however, point to approaches that could be adopted via the grass-roots democratic process of the Occupy movement (for example, reform of the banking system, debt write-offs for Greece, Portugal, Ireland and more).

This assessment also knowingly ignores the causes of the debt crisis and looks to the future. The damage has been done. Now the crucial question is how to undo it.

• The proposed policy of "muddling through" (the attempt to pay for old debts with new ones/ the "everything will be ok" mantra) conceals half the truth and neglects important aspects.

• Politicians have missed several opportunities to address the root cause of the debt crisis (e.g. bank restructuring 2009/Greece haircut in 2010) so that only third- and fourth-best solutions are left to deal with a protracted crisis of historic proportions.

• The entire world is looking to Germany for clear political and economic guidance of Europe. We are the only nation that has sufficient amounts of money left. As a society we have to democratically debate on who we are, what our vision of Europe is and how we get there. This process involves all our opinions.

• Policymakers do not recognize the complexity of and necessity for joint action. They listen to the representatives of big business and do not have the courage to engage in the dialogue with the population that is necessary to solve the crisis.

Our conclusions are as follows:

SUMMARY

4

We admit that our review does not paint a positive picture.

Critics will say that this pessimistic view will contribute to a deterioration of the situation, because it will worry people (and the "markets") and thus reduce consumption… and they're right.

Economic cycles are subject to human decisions that are influenced by emotions and psychology. The "animal spirits", as J. M. Keynes called the phenomenon – have the potential to reinforce a downward spiral. As Roosevelt summarized this relationship in 1933, "The only thing we have to fear, is fear itself".

Have a look at the overview and explanatory texts and form your own opinion!

However, the same critics will not mention what will happen if we continue as before, refusing to confront the problem, only buying more time with more debt, and failing to tell people the truth: in the course of the next one or two years we will be faced with a shambles that was once the European economic and financial system.

CLARIFICATION

If we all stand up now, stick together, are honest and show solidarity with one another throughout Germany and Europe,

then we have the power to make difficult decisions for coping with the crisis, so that we eventually will see the beginning

of a sustainable economic recovery.

BECAUSE

BUT!!!

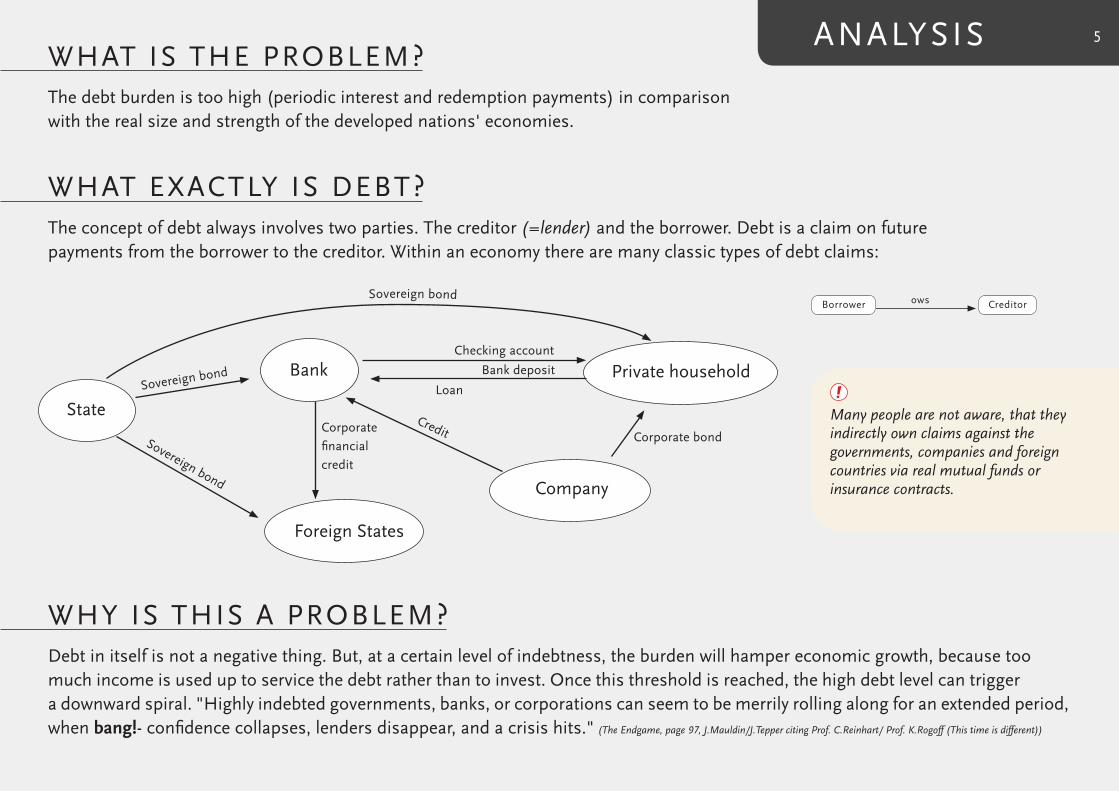

The debt burden is too high (periodic interest and redemption payments) in comparison with the real size and strength of the developed nations' economies.

The concept of debt always involves two parties. The creditor (=lender) and the borrower. Debt is a claim on future payments from the borrower to the creditor. Within an economy there are many classic types of debt claims:

Debt in itself is not a negative thing. But, at a certain level of indebtness, the burden will hamper economic growth, because too much income is used up to service the debt rather than to invest. Once this threshold is reached, the high debt level can trigger a downward spiral. "Highly indebted governments, banks, or corporations can seem to be merrily rolling along for an extended period, when bang!- confidence collapses, lenders disappear, and a crisis hits."

State

Bank Private household

Company

Foreign States

Sovereign bond

Sovereign bond

Sovereign bond

Credit

Loan

Checking account

Bank deposit

Corporate bond

WHY IS THIS A PROBLEM?

Many people are not aware, that they indirectly own claims against the governments, companies and foreign countries via real mutual funds or insurance contracts.

WHAT IS THE PROBLEM?

WHAT EXACTLY IS DEBT?

ANALYSIS

owsBorrower Creditor

!

Corporate financial credit

(The Endgame, page 97, J.Mauldin/J.Tepper citing Prof. C.Reinhart/ Prof. K.Rogoff (This time is different))

5

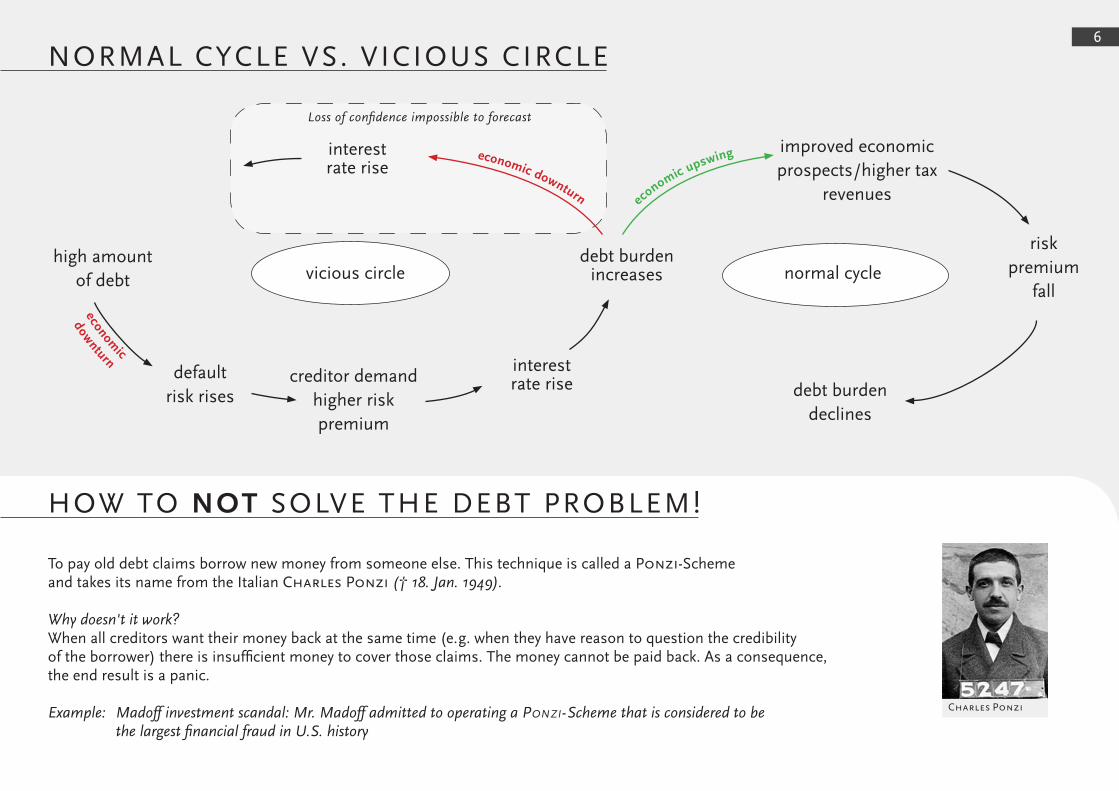

NORMAL CYCLE VS. VICIOUS CIRCLE

vicious circle normal cyclehigh amount

of debt

default risk rises

creditor demandhigher riskpremium

interestrate rise

interestrate rise

improved economic prospects/higher tax

revenues

riskpremium

fall

debt burdendeclines

debt burdenincreases

economic

downturn

economic downturn economic upswing

HOW TO NOT SOLVE THE DEBT PROBLEM!

To pay old debt claims borrow new money from someone else. This technique is called a Ponzi-Scheme and takes its name from the Italian Charles Ponzi († 18. Jan. 1949).

Why doesn't it work?When all creditors want their money back at the same time (e.g. when they have reason to question the credibility of the borrower) there is insufficient money to cover those claims. The money cannot be paid back. As a consequence, the end result is a panic.

Example: Madoff investment scandal: Mr. Madoff admitted to operating a Ponzi-Scheme that is considered to be the largest financial fraud in U.S. history

Charles Ponzi

Loss of confidence impossible to forecast

6

Middle waye.g. Merkozy 2011

Debt Cute.g. Russian Bankruptcy 1998

Ordinary insolvency proceeding

Everybody suffers from losses which are very high.Downward spiral and deflation.e.g. severe recession/Depression 1930

Too much debt

Release from debt burden but loss for creditor.

Problem: Losses can be high and are concen-trated in the banking system. -> banking crisis and recession

ECB prints moneyto buy Italian and

Spanish debt

+ Economic growth

Is that possible? -> Hyperinflation-> Currency reform-> Savers and the working class lose most

risk

risk

risk

Haircut on Greece andPortuguese Debt

HOW TO SOLVE THE DEBT PROBLEM? 7

Print 'a little bit' of money and use it to pay debte.g. US, UK 2011

Inflation 2–5%

The pressure to print new money to support the economy does not subside. Prices and income rise but at some point prices rise much more than incomes. -> Inflation 20–40%

risk

HOW HIGH IS THE DEBT BURDEN IN EUROPE?

What matters is not only government debt, but also the level of private debt.

Between 1970–2008, ~50% of all countries with a ratio of external debt to GNP equal to or lower than 60% have defaulted or restructered* **

!

Source: Debt Levels Alone Don’t Tell the Whole Story NYT, September 23, 2011

* "This time is different", page 24, Prof. K.Reinhart/Prof. K.Rogoff ** External Debt/GNP ratios are smalller compared to Total Debt/GDP ratios but in most cases are > 50% for developed nations

DATA

DATA 8

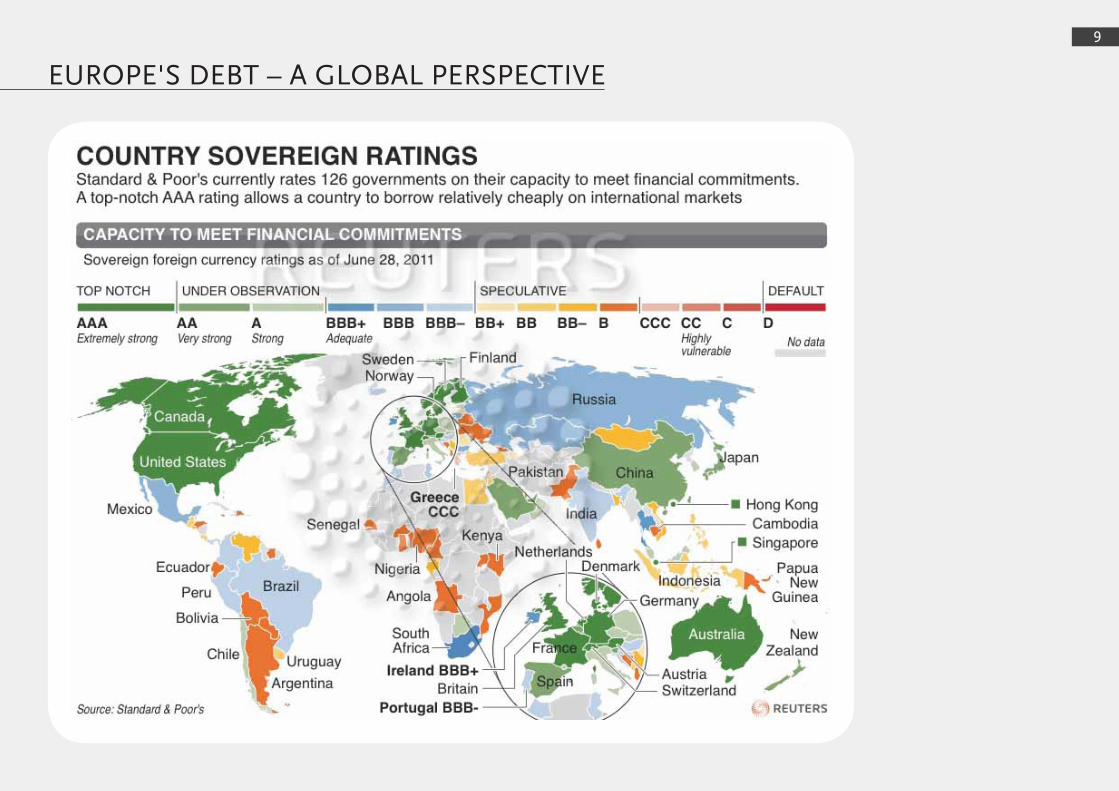

EUROPE'S DEBT – A GLOBAL PERSPECTIVE

9

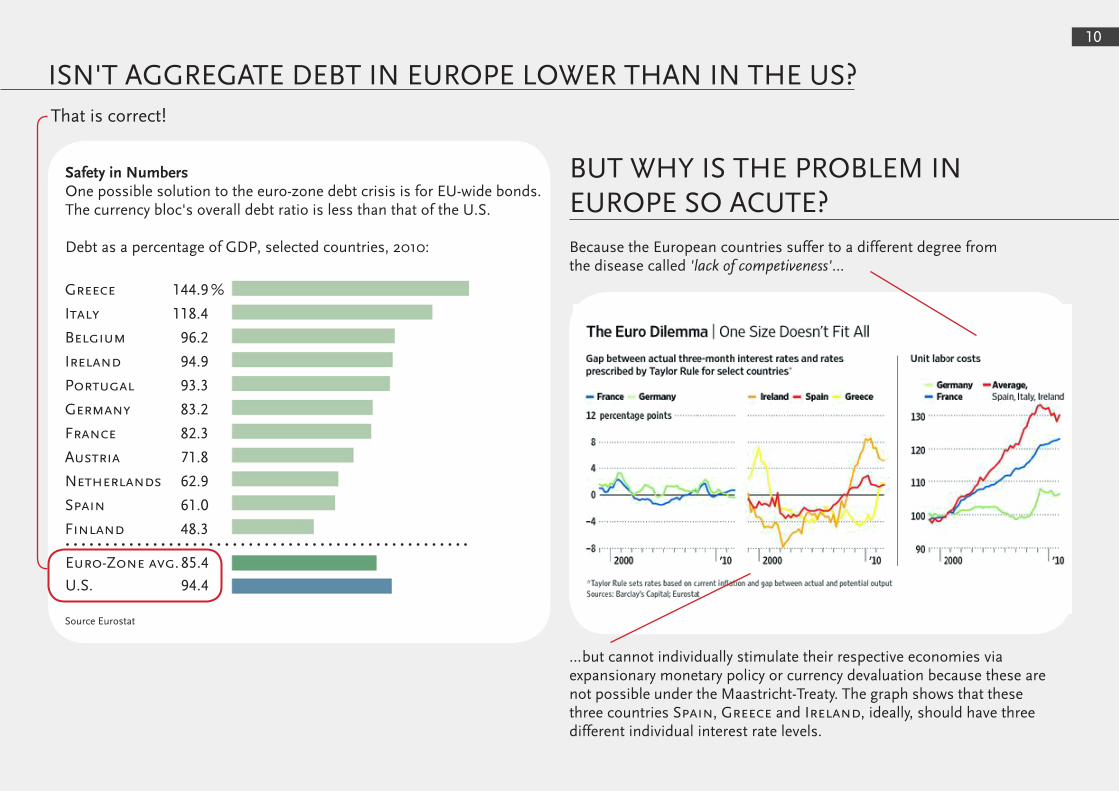

ISN'T AGGREGATE DEBT IN EUROPE LOWER THAN IN THE US?

BUT WHY IS THE PROBLEM IN EUROPE SO ACUTE?

That is correct!

Because the European countries suffer to a different degree from the disease called 'lack of competiveness'…

Safety in NumbersOne possible solution to the euro-zone debt crisis is for EU-wide bonds. The currency bloc's overall debt ratio is less than that of the U.S.

Debt as a percentage of GDP, selected countries, 2010:

Greece 144.9 %

Italy 118.4

Belgium 96.2

Ireland 94.9

Portugal 93.3

Germany 83.2

France 82.3

Austria 71.8

Netherlands 62.9

Spain 61.0

Finland 48.3

Source Eurostat

Euro-Zone avg. 85.4

U.S. 94.4

…but cannot individually stimulate their respective economies via expansionary monetary policy or currency devaluation because these are not possible under the Maastricht-Treaty. The graph shows that these three countries Spain, Greece and Ireland, ideally, should have three different individual interest rate levels.

10

HOW DOES THIS EFFECT ME?

INTRODUCTION TO THE GRAPHIC

The current graphic assumes that the new concept of the leveraged efsf will be implemented.

Recent comments indicate that a leverage of more than 2–3x for insurance-type guarantees of newly issued Spanish and Italian government bonds has become less feasible. This seems to depend on the scope of the efsf's additional responsibilities. Our current analysis works on the 'optimistic' assumption that a 4–5x leverage is still possible. Despite this, the outcome of the analysis is perhaps not much more promising than assuming a lower leverage capability.

Most recent proposals suggest the imf will play a more important role by backstopping Italy and Spain with its asset reserve. Ultimately, the risk of providing these funds will be born by its member states of which the US has the greatest weight.

As you can see from graphic on page 10, the US has a higher debt burden on aggregate than the Eurozone area. The Tea Party and Occupy Wall Street movements have been gaining political momen-tum because they are sceptical towards reckless debt-ponzi-systems. Do you think the people of the United States will accept having to also pay for Europe's self-made problems?

Please note that quantifications of bank recapitalization needs can only be seen as guidelines. The real size depends on multiple factors. Estimates by experts vary by a wide range.

11

Abstract academic concepts such as high inflation and deflation have real and painful consequences for the daily lives of all of us and can last for a period of several years. The problem is that our generation and the generation of our parents have no experience with this situation and don't expext them to recur during our lifetime. Again, aren't we the people who are supposed to live in the prosperous time of the great moderation in which the volatility of cyclical business cycles has been smoothed away? Isn't the 21st century different from the previous centuries because we are smarter and have been inventing new technologies?

We discuss the real effects in what we call 'the possible future scenarios' that we think are realistic projections of the possible paths we could go through within the next three years. We name them provocatively: a) everything is ok b) (hyper-)inflation c) uncontrolled reset button d) controlled reset button

ACTIONS AT PRESENT

DECISION TO COME

global currency reform 2013gold price:$4k–8k

US recessionEU recession

France: AA

US recessionEU recession

France: AASpain+Italy no recovery

No US recessionNo EU recession

France: AAASpain+Italy recovery

+BUY BONDS / BUY TIME

WITH HELP OF IMF

MORE REFORMS

250bn euro x 4x

200bn euro

(HYPER-)INFLATION3% global growth

United States of Europe

"EVERYTHING IS OK"Severe recession (-5/-8% growth rate)

Attack on democracy from left and right

UNCONTROLLED RESET BUTTONRecession (-1/-5% growth rate)

New start finally possible

CONTROLLED RESET BUTTON

EFSFEuropean Financial Stability Facility printing money

EZB

IrelandPortugalGreeceBelgium

40 %40 %60–80 %40 %

Debit hair cut

HOPE FOR TAKE ACTION

Euro-BondSecondary market

50%50%50% 50%

No US recessionNo EU recession

France: AASpain+Italy recovery

'bad banks' 'good banks'

Banks and Insurances

/

+ North-South Euro ?+ 3rd bank recap/Marshall-Plan

500bn Euros?

Spain & Italy receive debt haircutSpain & Italy hope for generating budget surplus and economic growth

+ EU harmonization+ democratic integration+ transfer union europe

880bn euro

40%

14% 14% 51% 21%

60%

30%

40%60%

70%

+Debt haircut

EU

450bn euro

Spain+Italy no recovery

˜

DESCRIBTION OF END SCENARIOS

14%"EVERYTHING IS OK"

3% global growthUnited States of Europe

14%(HYPER-)INFLATION

global currency reform 2013gold price: $4–8k

13

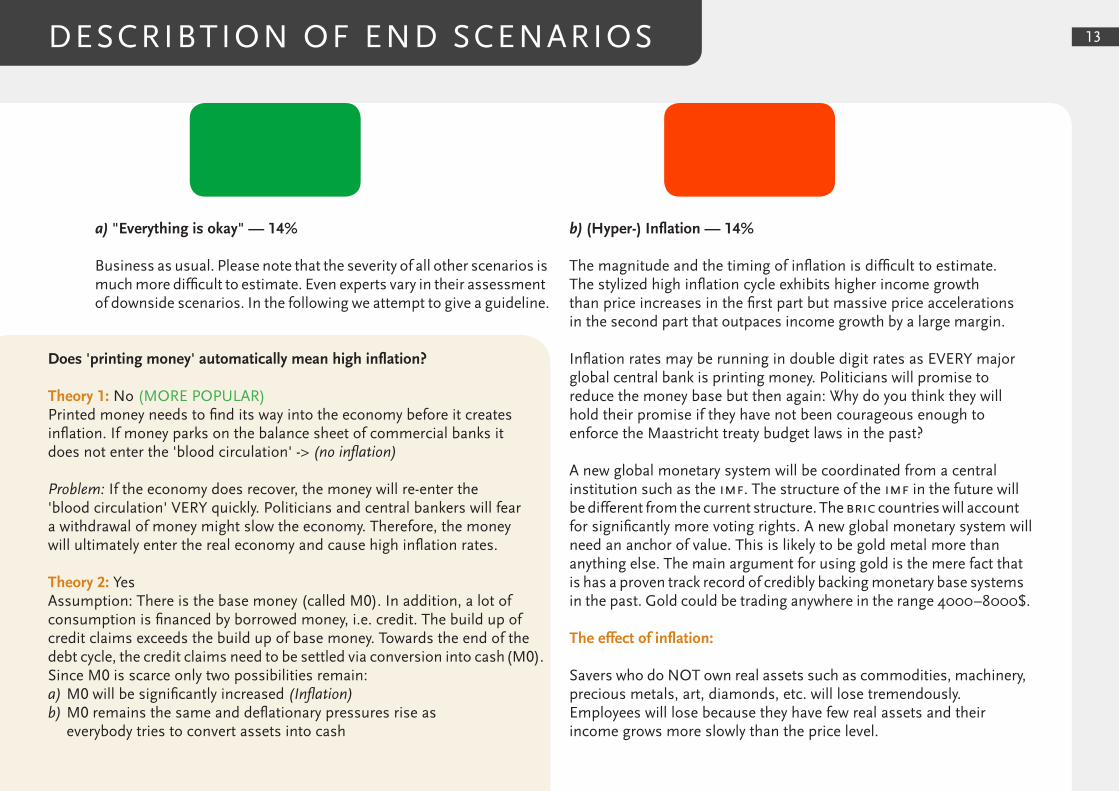

a) "Everything is okay" — 14%

Business as usual. Please note that the severity of all other scenarios is much more difficult to estimate. Even experts vary in their assessment of downside scenarios. In the following we attempt to give a guideline.

b) (Hyper-) Inflation — 14%

The magnitude and the timing of inflation is difficult to estimate. The stylized high inflation cycle exhibits higher income growth than price increases in the first part but massive price accelerations in the second part that outpaces income growth by a large margin.

Inflation rates may be running in double digit rates as EVERY major global central bank is printing money. Politicians will promise to reduce the money base but then again: Why do you think they will hold their promise if they have not been courageous enough to enforce the Maastricht treaty budget laws in the past?

A new global monetary system will be coordinated from a central institution such as the imf. The structure of the imf in the future will be different from the current structure. The bric countries will account for significantly more voting rights. A new global monetary system will need an anchor of value. This is likely to be gold metal more than anything else. The main argument for using gold is the mere fact that is has a proven track record of credibly backing monetary base systems in the past. Gold could be trading anywhere in the range 4000–8000$.

The effect of inflation:

Savers who do NOT own real assets such as commodities, machinery, precious metals, art, diamonds, etc. will lose tremendously. Employees will lose because they have few real assets and their income grows more slowly than the price level.

Does 'printing money' automatically mean high inflation?

Theory 1: No (MORE POPULAR)Printed money needs to find its way into the economy before it creates inflation. If money parks on the balance sheet of commercial banks it does not enter the 'blood circulation' -> (no inflation)

Problem: If the economy does recover, the money will re-enter the 'blood circulation' VERY quickly. Politicians and central bankers will fear a withdrawal of money might slow the economy. Therefore, the money will ultimately enter the real economy and cause high inflation rates.

Theory 2: YesAssumption: There is the base money (called M0). In addition, a lot of consumption is financed by borrowed money, i.e. credit. The build up of credit claims exceeds the build up of base money. Towards the end of the debt cycle, the credit claims need to be settled via conversion into cash (M0). Since M0 is scarce only two possibilities remain: a) M0 will be significantly increased (Inflation) b) M0 remains the same and deflationary pressures rise as everybody tries to convert assets into cash

DESCRIBTION OF END SCENARIOS

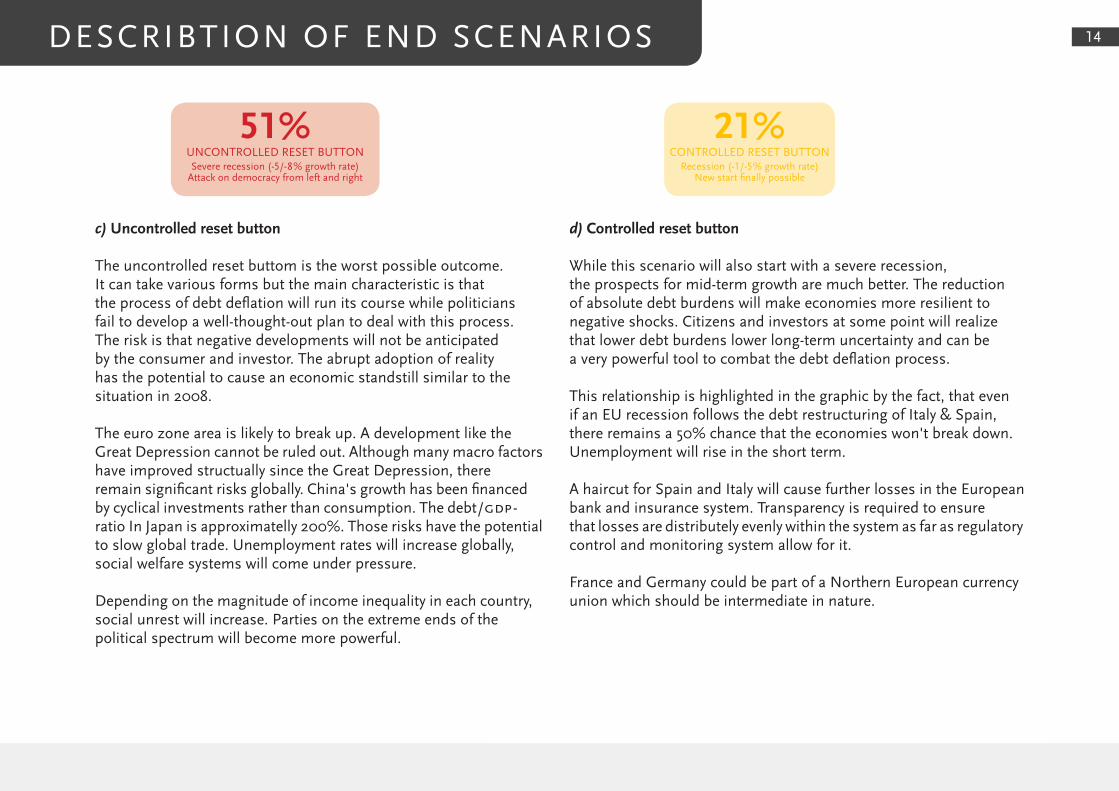

51%UNCONTROLLED RESET BUTTONSevere recession (-5/-8% growth rate)

Attack on democracy from left and right

21%CONTROLLED RESET BUTTON

Recession (-1/-5% growth rate)New start finally possible

14

c) Uncontrolled reset button

The uncontrolled reset buttom is the worst possible outcome. It can take various forms but the main characteristic is that the process of debt deflation will run its course while politicians fail to develop a well-thought-out plan to deal with this process. The risk is that negative developments will not be anticipated by the consumer and investor. The abrupt adoption of reality has the potential to cause an economic standstill similar to the situation in 2008.

The euro zone area is likely to break up. A development like the Great Depression cannot be ruled out. Although many macro factors have improved structually since the Great Depression, there remain significant risks globally. China's growth has been financed by cyclical investments rather than consumption. The debt/gdp- ratio In Japan is approximatelly 200%. Those risks have the potential to slow global trade. Unemployment rates will increase globally, social welfare systems will come under pressure.

Depending on the magnitude of income inequality in each country, social unrest will increase. Parties on the extreme ends of the political spectrum will become more powerful.

d) Controlled reset button

While this scenario will also start with a severe recession, the prospects for mid-term growth are much better. The reduction of absolute debt burdens will make economies more resilient to negative shocks. Citizens and investors at some point will realize that lower debt burdens lower long-term uncertainty and can be a very powerful tool to combat the debt deflation process.

This relationship is highlighted in the graphic by the fact, that even if an EU recession follows the debt restructuring of Italy & Spain, there remains a 50% chance that the economies won't break down. Unemployment will rise in the short term.

A haircut for Spain and Italy will cause further losses in the European bank and insurance system. Transparency is required to ensure that losses are distributely evenly within the system as far as regulatory control and monitoring system allow for it.

France and Germany could be part of a Northern European currency union which should be intermediate in nature.

THE ECB15

The ecb is allowed to purchase Spanish and Italian sovereign bonds in the secondary market through the Security Market Purchase programme (smp). As the ecb purchases the bonds it increases the size and the riskiness of its balance sheet. The transaction is not in accordance with the original Maastricht Treaty. This is why the smp is currently limited in size.

The ecb has government bonds on the asset side of the balance sheet. The liability side is made up of currency (the physical bank notes and coins) and bank reserves that commercial banks hold at the central bank. The structure of the government bond assets should represent the weighting of the proportional size of each member state (gdp data/citizens). The execution of the smp programme has skewed the asset mix towards riskier bonds from the Southern European area.

The ecb is a private entity which is owned by the individual European national central banks which also appoint members to the central body, the ecb Governing Council.

The ecb has no authority to 'print' money. Article 123 of the Treaty on the Functioning of the European Union does not allow the ecb to provide central governments with credit facilities.

As pointed out above, Germany is the only country which has enough 'money' to help the Eurozone buy time. In reality this means that it is Germany who, to the greatest extent, decides what the ecb will do.

German politicians promised their citizens before the introduction of the Euro that Germany's post war hard monetary policy would not be sacrified.

If our politicians decide that the ecb will be allowed to print, the ecb will have money to BUY TIME, but we will have passed the last milestone on the way to high inflation. From now on, the full control of inflation rates is no longer in our hands (see page 13).

Can the ecb go bankrupt?

printing money

Given that the ecb continues to buy assets with default risk, can the ecb go bankrupt? It depends on the angle from which you look at it and the answer to this is a political decision.

Yes:Like any private bank, the ecb can suffer losses if its assets decline in value to such an extent that the bank's equity capital is zero. In this case, the member states have to inject new capital according to their proportional share.

No: The ecb could use the printing press it has in its 'basement'. The amount of newly printed Euros represents fresh new equity capital.

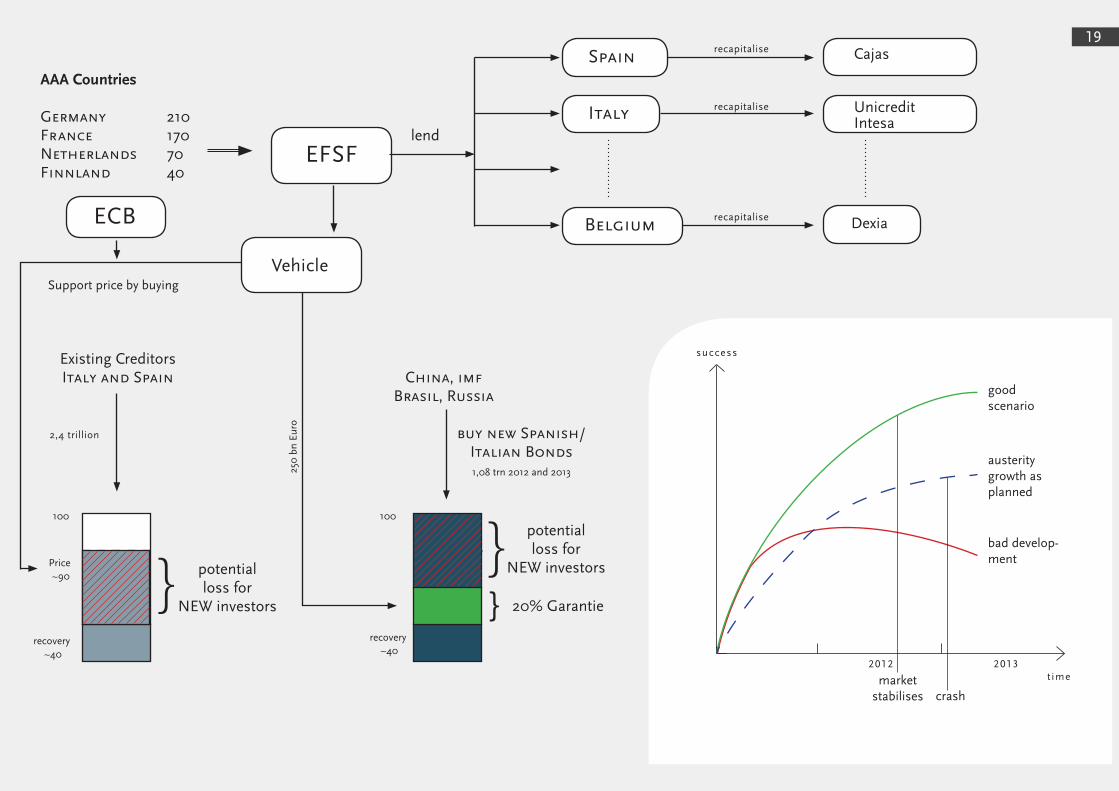

EFSF16

European Financial Stability Facility (efsf)

We assume that Greece, Ireland, Portugal and presumably Belgium will default in 2012 on their sovereign bonds and will receive a haircut.

In this case we consider the main objective of the efsf a) to guarantee newly issued Italian and Spanish government bonds so that foreign investors will buy them in the primary market and b) to provide funds for an adequate capitalisation of European banks.

We neglect a description of additional objectives of the efsf since we consider them less relevant. Operational features are of interest because they determine the credibility of the structure.

The basic concept of the efsf .

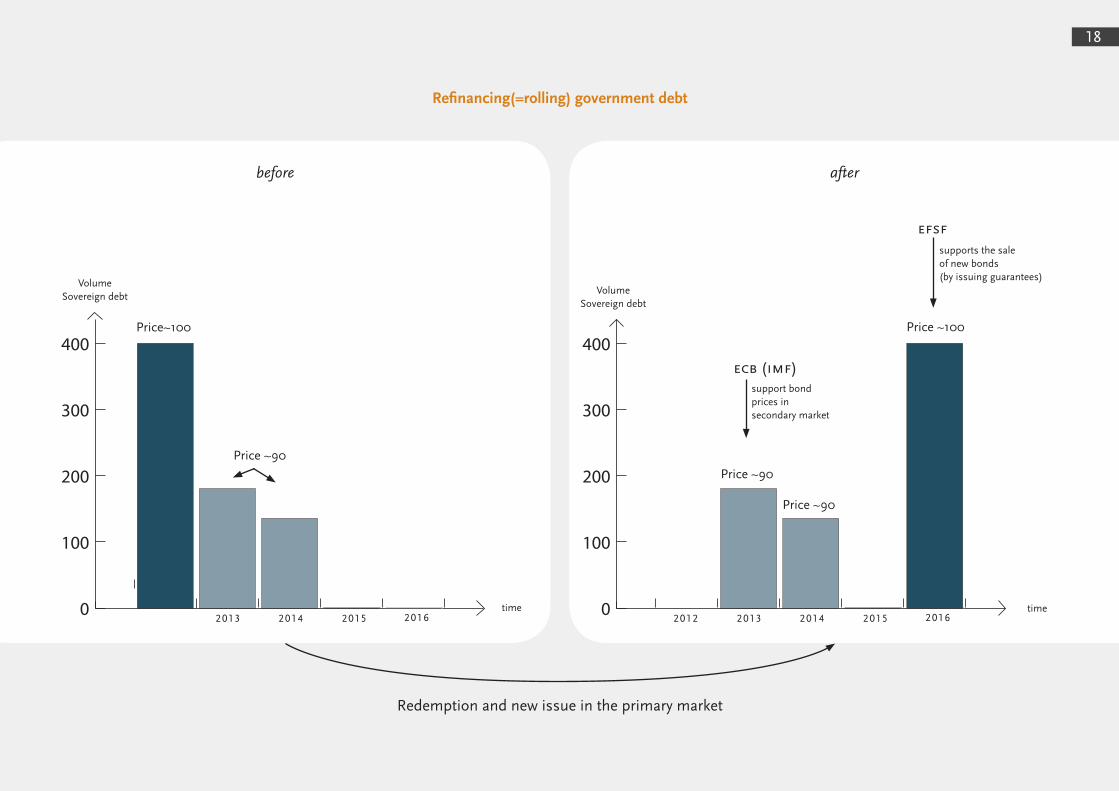

As pointed out above, the main problem is that investors refuse to lend Italy and Spain new money as their redemption payments come due: Italy and Spain are not able to refinance their debt (see graphic page 18).

The efsf is an attempt to convince foreign investors to buy newly-issued sovereign bonds of Italy and Spain in 2012, 2013 and perhaps 2014. To achieve this objective the efsf guarantees that if Spain or Italy default in the future, the first 20% of the losses will be borne by the efsf.

In order for the structure to succeed, the newly issued guaranteed bonds (bonds are always issued at a price close to 100) need to be attractive for investors. They are only attractive if the investor who buys the new bonds (with a 20% loss guarantee) at a price of 100 cannot lose more (if Spain/Italy default) than if they had bought the old bonds.

The Graphic on page 20 highlights this point. Assuming a certain recovery value for Spanish/Italian debt, the potential loss for an investor might be less if he can buy oustanding bonds at very low prices even if they don't have a loss absorption guarantee. This would likely cause a lack of demand for new bonds and would lead to a failure of refinancing.

In order to prevent this constellation from happening, the ecb will make the old bonds 'less attractive' by buying those bonds 'in the (secondary) market' and thereby pushing the prices of those oustanding bonds higher.

Why Leverage?

The original idea of the efsf was to guarantee losses up to the full 100% should Italy or Spain default. Table xyz on page 23 shows that a 450bn efsf (AAA guarantees) in this original idea would have only been able to guarantee 6 months of bond issues before the guarantee amount would have been used up. Clearly too little time for Italy and Spain to convince investors that sustainable reforms have been successfully implemented. In order to 'buy more time', the compromise was to guarantee fewer losses per bond, which would permit guaranteeing more bonds and gaining more time.

The 4–5x leverage allows the efsf to guarantee a higher volume of newly-issued bonds. The downside of this leverage is, that if Spain and Italy default, the actual loss for the German/French taxpayer (guarantees will turn into real cash payouts that will not come back) will be 4–5x higher and likely reach the full amount of 211bn Euro.

European Financial Stability Facility463bn

17

Guarantees of AAA-rated countries amount to approximately 450bn Euro.

Table

Germany 211 France 158 Netherlands 44 Austria 21 Finland 14 Slovakia 7.5 Cyprus/Luxembourg/Malta/Slovenia 7.5 = 450

The second objective of the efsf is to recapitalise financial institutions with valid business models. A minimum capital ratio, defined and called T1 capital ratio, has been set at 9%. Practically the efsf will not inject cash and therefore equity capital directly into individual banks but will lend to the member states which then use the proceeds to make the necessary injection.

Assuming a debt haircut on Greece, Portugal, Ireland and perhaps Belgium in 2012, the required equity capital injection will amount to from 150bn to 250bn Euro!

Who are the potential investors in European bonds and what are their objectives?

It is completely rational for bric countries to support the euro zone by investing in Spain and Italy using the efsf as a safety backstop for the following reasons:

The bric countries have built up wealth by retaining foreign currency reserves, which are denominated largely in US dollars. Due to the US debt problem, the value of the dollar is likely to deteriorate in the future. To compensate for this loss in purchasing power, the sovereign wealth funds seek to diversify away from the dollar. A strong euro helps to achieve this goal.

The brics could use their negotiation stake to achieve important geopolitical objectives:

• increasevotingpowerintheimf • improvetradeconditionsunderthewto legislation • buyphysicalassetsindevelopedcountries • minimizeforeignpolicyinterventionsintodomesticpolicyaffairs such as human right violations

However, supporting the efsf in order to achieve the aforementioned goals comes at a price: the risk of suffering significant losses due to debt defaults of either Spain or Italy. Foreign investors will try to make sure that Germany/France take care that the guarantee solution retains credibility. The most direct way to express this idea is to require an AAA-rated entity guarantee. The backstop of the efsf AAA rating is derived from France and Germany's rating strength.

Realistically, foreign investors might accept a rating downgrade of the efsf to AA, but this analysis is highly controversial and hypothetical. Recent demand for efsf bonds has been very low and indicates that relying on the functionality of an AA-rated efsf poses a very high degree of risk.

Refinancing(=rolling) government debt

before

Price~100 Price ~100

Price ~90Price ~90

Price ~90

VolumeSovereign debt

VolumeSovereign debt

time time2012

20122014 20142013 20132015 20152016 2016

after

0

100

200

300

400

0

100

200

300

400

Redemption and new issue in the primary market

ecb (imf)support bond prices in secondary market

supports the sale of new bonds (by issuing guarantees)

efsf

18

AAA Countries

EFSF

ECB

Italy

Spain

UnicreditIntesa

Cajas

Belgium Dexiarecapitalise

recapitalise

recapitalise

Support price by buying

Existing CreditorsItaly and Spain

2,4 trillion

potential loss for

NEW investors}

}}

recovery ~40

recovery ~40

Price ~90

100

250

bn

Euro

100

China, imfBrasil, Russia

buy new Spanish/ Italian Bonds1,08 trn 2012 and 2013

potential loss for

NEW investors

20% Garantie

lendGermany 210 France 170Netherlands 70Finnland 40

Vehicle

market stabilises crash

good scenario

austerity growth as planned

bad develop-ment

2013t ime

success

2012

19

20

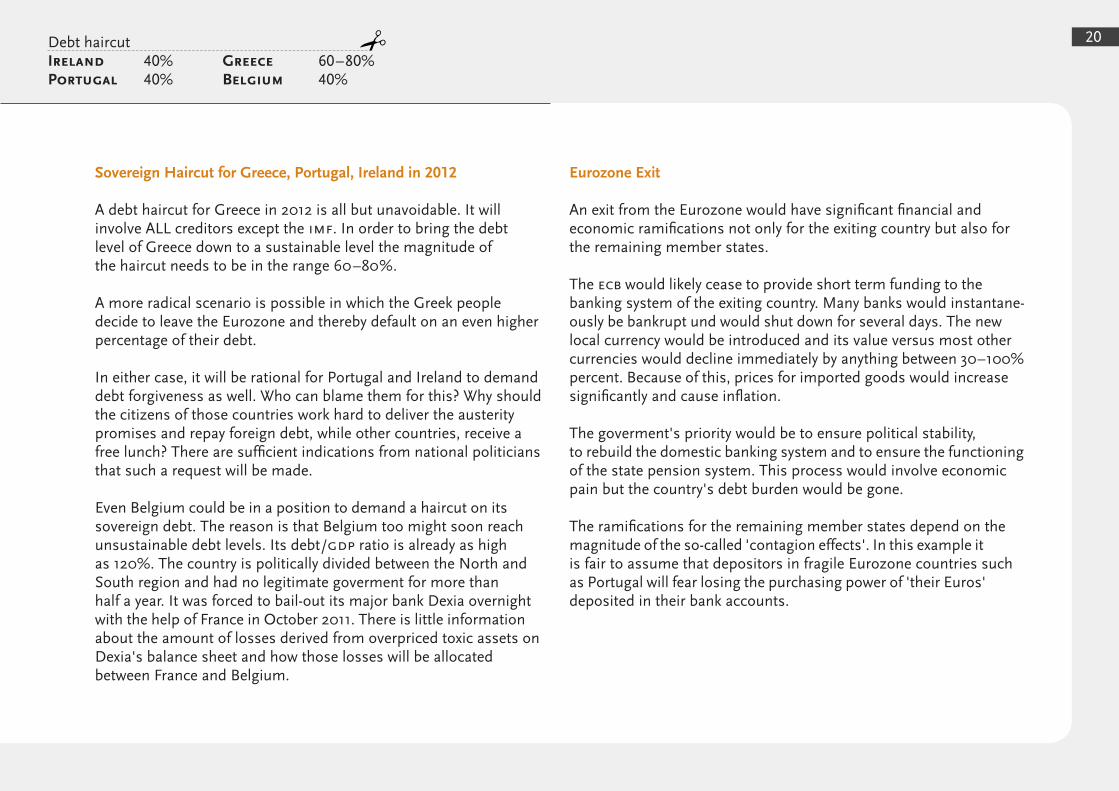

Sovereign Haircut for Greece, Portugal, Ireland in 2012

A debt haircut for Greece in 2012 is all but unavoidable. It will involve ALL creditors except the imf. In order to bring the debt level of Greece down to a sustainable level the magnitude of the haircut needs to be in the range 60–80%.

A more radical scenario is possible in which the Greek people decide to leave the Eurozone and thereby default on an even higher percentage of their debt.

In either case, it will be rational for Portugal and Ireland to demand debt forgiveness as well. Who can blame them for this? Why should the citizens of those countries work hard to deliver the austerity promises and repay foreign debt, while other countries, receive a free lunch? There are sufficient indications from national politicians that such a request will be made.

Even Belgium could be in a position to demand a haircut on its sovereign debt. The reason is that Belgium too might soon reach unsustainable debt levels. Its debt/gdp ratio is already as high as 120%. The country is politically divided between the North and South region and had no legitimate goverment for more than half a year. It was forced to bail-out its major bank Dexia overnight with the help of France in October 2011. There is little information about the amount of losses derived from overpriced toxic assets on Dexia's balance sheet and how those losses will be allocated between France and Belgium.

Debt haircutIreland 40% Portugal 40%

Greece 60–80% Belgium 40%

Eurozone Exit

An exit from the Eurozone would have significant financial and economic ramifications not only for the exiting country but also for the remaining member states.

The ecb would likely cease to provide short term funding to the banking system of the exiting country. Many banks would instantane-ously be bankrupt und would shut down for several days. The new local currency would be introduced and its value versus most other currencies would decline immediately by anything between 30–100% percent. Because of this, prices for imported goods would increase significantly and cause inflation.

The goverment's priority would be to ensure political stability, to rebuild the domestic banking system and to ensure the functioning of the state pension system. This process would involve economic pain but the country's debt burden would be gone.

The ramifications for the remaining member states depend on the magnitude of the so-called 'contagion effects'. In this example it is fair to assume that depositors in fragile Eurozone countries such as Portugal will fear losing the purchasing power of 'their Euros' deposited in their bank accounts.

21

Why is it necessary to reform the banking system?

The main objective of a well-functioning banking system is to efficiently allocate savings from savers to entrepreneurs who need the money to invest into projects that offer an attractive risk/reward relationship. Standard neoclassical economic theory postulates that this process automatically promotes the economy and society. The economic allocation of resources is considered to be efficient (a discussion about what the correct economic theory is/should be is beyond the scope of this publication).

The main duty of a 'banker' would be to correctly assess the credit-worthiness of the borrowers. The classic banking business is therefore simple, transparent and boring.

The current status of the banking system has few things in common with the classic banking system.

Over the last 20 years, a wave of global and European deregulatory measures has led the banking system to decouple not only from the real economy but also from ethical values/standards. Most important were the abolition of the Glass-Steagall-Act, the lowering of equity capital requirements for banks, the introduction of short-term-orientated stock-based management reward systems and broad approvals with respect to size and transparency of derivatives trading.

As a consequence, bank capital structures have become much more risky, both for the bank's shareholders and, because of the size of the banking system, also for the society. A banking system has evolved which continuously exploits this weakness to put poltitics in a stranglehold in two ways:

1) If the banks do not get bailed out, the financial system will collapse because of chain-reaction effects

2) If banks do not get bailed out, a recession is unavoidable because banks will need to reduce lending and thereby blocking the 'blood circulation' of the economy ("Credit Crunch").

This incentive structure represents what every student of economics and business administration learns/in his or her first semester 101 econ course: The bad incentive structure called Moral Hazard!

Moral Hazard means that it is rational for banks to take on big risks: If everything works out, banks earn decent profits and reward shareholders, management and employees generously. 'If things go wrong' the bank goes bankrupt and the society is asked to step in and 'pay the bill'. And paying the bill doesn't just involve direct capital injections! Any government intervention that supports the market comes at a cost or has high opportunity costs.

The concept of Moral Hazard is abstract and it is hard to comprehend the severity of this problem. The damage to the society only becomes clear when the unavoidable crisis finally confronts us in our daily lives.

The current state of the banking system is unfair, unjust and damaging to our economy!

The Swedish model for a successful reform of the banking systemBanks and Insurances 'bad banks' 'good banks'

/

22

A fair, stable and robust banking system has the following characteristics:

1) Balance sheets are transparent and can be analysed (This should be obvious but in reality this is not the case!)

2) Banks are small enough so that they are allowed to fail without causing chain-reaction effects

3) Limited size and transparency of interbanking interdependencies

4) Robust balance sheets based on strong equity capital buffer

The Swedish reform of its banking system during the domestic crisis between 1991–1993 is the instruction manual for a successful and consequent reorganization of the banking system. The measures taken by the Swedish parliament still serve as the key guidelines today. Those measures cannot be applied on a 1-to-1 basis to the banking system in 2011: While the Swedish crisis was an isolated banking crisis which was not subject to negative external feedback loops, the current banking crisis is global in nature. European Economic Papers 360, Lars Jonung

The key elements of a successful reform of the banking system

1) Decisive policy action legitimated by broad parliamentary approval across political parties to achieve credibility

2) Guarantee to bank creditors (see below)

3) Early and decisive policy response in the context of a well-thought-out holistic plan

4) Sufficient liquidity provision by the central bank

5) Temporary nationalization of insolvent banks/layoff of senior management/creation of good/bad banks

6) Separation of retail banking and investment banking (Re-implementation of Glass-Steagall-Act)

7) Break-up of Too-big-to-fail institutions

8) Enforcement of the Sarbanes-Oxley-Act: No legal loophole for directors who personally sign official financial company reports

9) Banking recapitalisation via debt-equity-swaps. In special cases senior unsecured creditors (excluding depositors) may need to accept a haircut. This measure is controversial and needs to be part of point 3). Interbanking links via senior unsecured credit are extensive and lie at the heart of the financial system's 'chain'

10) Enforcement of mark-to-marked accounting rules

11) Exchange based derivate trading and limitation of the volume of derivative trading as a function of the underlying notional outstanding

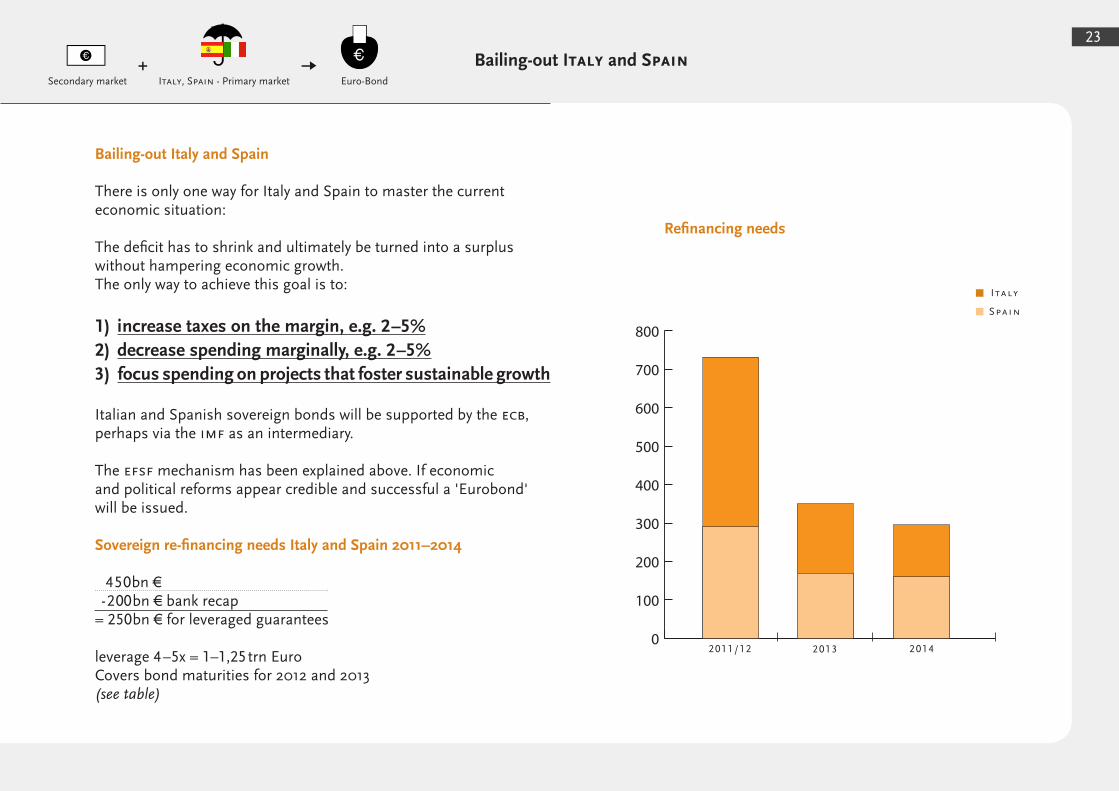

Refinancing needs

23

Bailing-out Italy and Spain

There is only one way for Italy and Spain to master the current economic situation:

The deficit has to shrink and ultimately be turned into a surplus without hampering economic growth.The only way to achieve this goal is to:

1) increase taxes on the margin, e.g. 2–5%2) decrease spending marginally, e.g. 2–5%3) focus spending on projects that foster sustainable growth

Italian and Spanish sovereign bonds will be supported by the ecb, perhaps via the imf as an intermediary.

The efsf mechanism has been explained above. If economic and political reforms appear credible and successful a 'Eurobond' will be issued.

Sovereign re-financing needs Italy and Spain 2011–2014

450bn € -200bn € bank recap= 250bn € for leveraged guarantees

leverage 4–5x = 1–1,25trn EuroCovers bond maturities for 2012 and 2013(see table)

+Secondary market Euro-BondItaly, Spain - Primary market

880bn euro

Bailing-out Italy and Spain

Spain

Italy

2011/12 201420130

100

200

300

400

500

600

700

800

24

Sovereign Haircut for Italy and Spain

This path is currently not the policy option favoured by European politicians. This is why we assign only a 30% probability to this path. It doesn't mean we don't think it's the right way to go.

The decision to accept haircuts on Italy and Spain is difficult to make for politicians, because political advisors and bank lobbyists will claim that this will be 'the end of the world'. It surely won't, but it will not be easy either.

The main argument in favor of haircuts is:

The sober realization and acceptance that there is no other longterm solution. Tackling debt problems with more debt makes the ultimate breakdown only more painful and dangerous.

It is better to make a clear break, even if it hurts everybody in the short term, and be able to start on a fair and transparent basis again, rather than to kick the can down the road and thereby to continuously suffer from moral hazard problems.

"One step back and two steps ahead" in the European integration process must be a policy option if we all agree and accept that mistakes have been made in the past (conceptually flawed model of Eurozone). The intermediate process can involve the creation of a North-South Euro system (Germany und France in North Euro) that could last for a period of 5–15 years before more radical integration models can be applied again.

Only few people ask what a crash scenario could look like in for example two years, if additional debt financed support programmes

fail and Spain and Italy have to declare bankruptcy because austerity and economic restructurings have failed.

Imagine if, as discussed on page 25, one of the following things happens:

1) Many more hidden losses are discovered in the Spanish banking system than those which were officially disclosed. These would bring the Spanish economy down to its knees

2) Government statistics turn out to be incorrect (e.g. Greece)3) Spanish and Italian citizens vote for parties that block austerity

programmes (could you blame them for doing so?)

Is this unrealistic?

How will Germans react, if they suffer austerity measures just to buy time and then get screwed anyway?

Isn't it better to openly communicate the view NOW that solidarity has its limits and cannot be fully based on mere beliefs about promises that lack credibility?

Wouldn't it be better to save the money for a programme to build up Europe AFTER a clear and transparent break has been made? Something like a Marshall plan? Clearly, it will not be as easy and painless as it sounds, but isn't it at least worth an intensive society-wide discussion?

Debt hair cut30% Sovereign Haircut for Italy and Spain

25

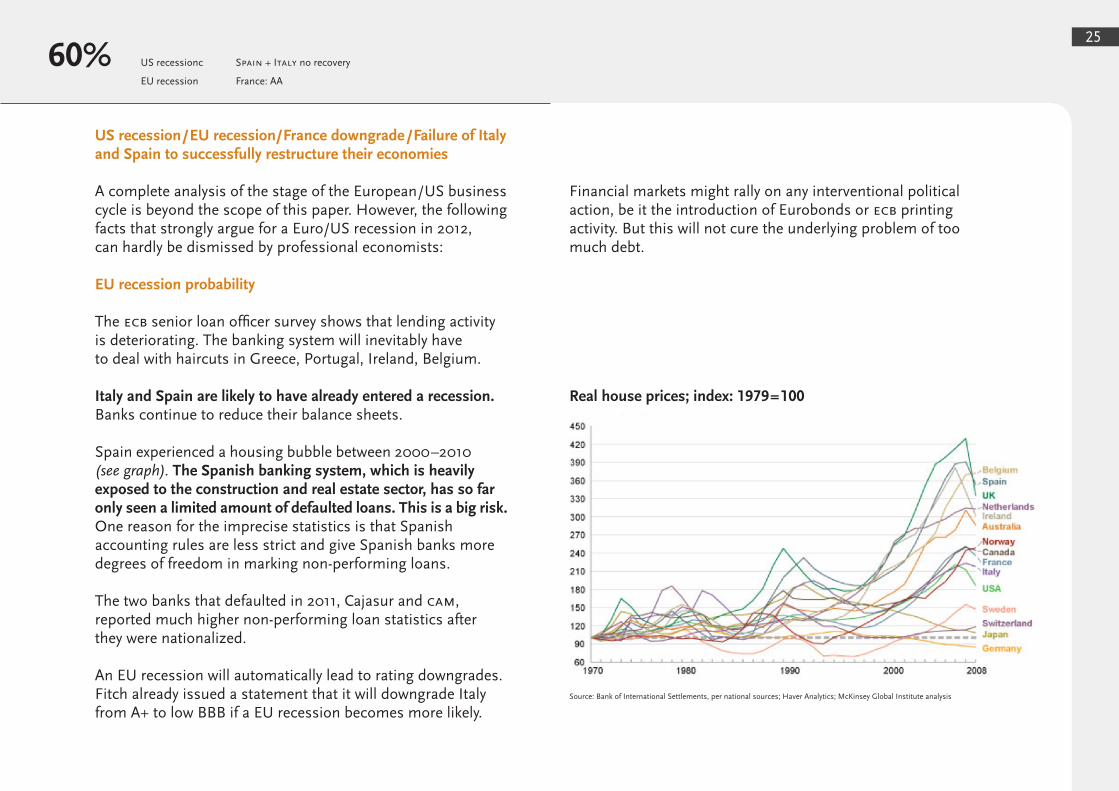

US recession/EU recession/France downgrade/Failure of Italy and Spain to successfully restructure their economies

A complete analysis of the stage of the European/US business cycle is beyond the scope of this paper. However, the following facts that strongly argue for a Euro/US recession in 2012, can hardly be dismissed by professional economists:

EU recession probability

The ecb senior loan officer survey shows that lending activity is deteriorating. The banking system will inevitably have to deal with haircuts in Greece, Portugal, Ireland, Belgium.

Italy and Spain are likely to have already entered a recession. Banks continue to reduce their balance sheets.

Spain experienced a housing bubble between 2000–2010 (see graph). The Spanish banking system, which is heavily exposed to the construction and real estate sector, has so far only seen a limited amount of defaulted loans. This is a big risk. One reason for the imprecise statistics is that Spanish accounting rules are less strict and give Spanish banks more degrees of freedom in marking non-performing loans.

The two banks that defaulted in 2011, Cajasur and cam, reported much higher non-performing loan statistics after they were nationalized.

An EU recession will automatically lead to rating downgrades. Fitch already issued a statement that it will downgrade Italy from A+ to low BBB if a EU recession becomes more likely.

Financial markets might rally on any interventional political action, be it the introduction of Eurobonds or ecb printing activity. But this will not cure the underlying problem of too much debt.

Real house prices; index: 1979=100

60% US recessionc

EU recession

Spain + Italy no recovery

France: AA

Source: Bank of International Settlements, per national sources; Haver Analytics; McKinsey Global Institute analysis

26

Will an EU integration and harmonization work?

Every politician and banking analyst will tell you that in order for the future 'United States of Europe' to function properly, the euro zone will need to integrate politically and harmonize economically. But what does that mean?

Do you think that in two year’s time, when Italy and Spain suffer from the implementation of austerity measures, the Spanish people will accept having German/French technocrats dictate the conditions under which they live? Do you think that the Germans actually want to play this role? Why do you think it will work in the future under much more strained relationships when it has not worked in the past when the problem comprised simple 3% budget violations?

Why do you think that political unity will be successful in the future? Do you think just because 'there is no alternative', European nations will accept a centralized authority when the European parliament has not been able to gain broad acceptance over the course of 15 years?

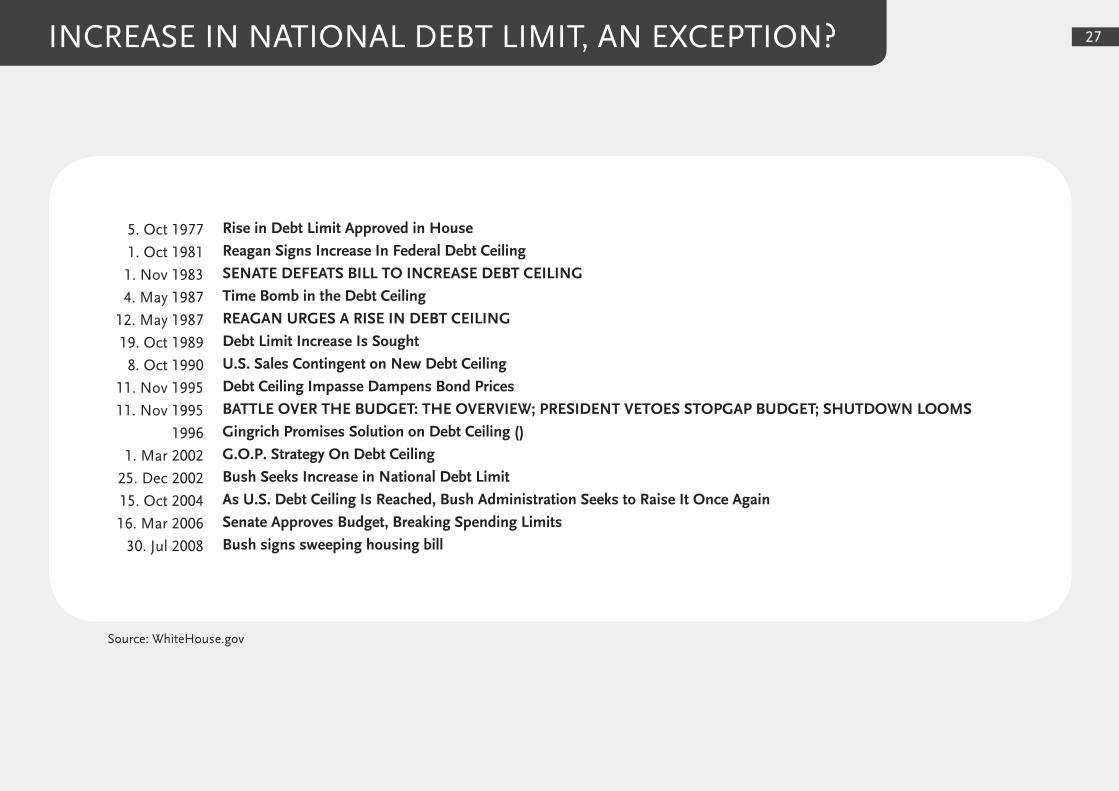

The United States of America is considered to be one of the most homogeneous economic spaces due to its geographic and cultural characterisics, its national identity and history. The US has proven to be the longest-lasting democratic nation in the world. The United States has incorporated a debt limit into their constitution. The United States has violated the debt limit more than 50 times since 1970 (see graphic on page 27). The United States has created a higher debt burden than the European Union (see graphic on page 10) on aggregate and still cannot agree on a solution in the interest of the country because each political party aims to win elections in 2013!

The euro zone has 17 member states with parliaments that are composed of up to 6 different political parties!

Probability of a US recession in 2012

The US has seen the most dismal post-war economic recovery despite historically high stimulative government initiatives. Official US debt volume stands at 15trn USD and there does not seem to be the political will to tackle the problem ahead of the election. Monetary policy options are almost exhausted with the Federal Fund rate at 0% and with two monetary base expansions, which seem to have a decreasing marginal impact. Stimulative tax cut programms are politically controversial to say the least. ecri weekly leading indicators are deep in negative territory. A serious negative reversal at this time is likely to be the final confirmation of the start of a new recession.

The senior loan officer survey partly indicates tightening credit standards as US banks are forced to delever their balance sheets and reduce their exposure to the European banking system. Bank of America 5-year cds spreads reached the highest level ever on November 24th @ 480 basis points.

This paper is not meant to disregard positive economic developments. But the overall evidence indicates a high recession probability.

If the US sneezes then the global economy will catch a cold. This description of the global economic interdependences still holds true in the year 2011.

We think that a rating downgrade of France in 2012 to the AA category has a probability of more than 80% irrespective of economic developments.

Rise in Debt Limit Approved in House

Reagan Signs Increase In Federal Debt Ceiling

SENATE DEFEATS BILL TO INCREASE DEBT CEILING

Time Bomb in the Debt Ceiling

REAGAN URGES A RISE IN DEBT CEILING

Debt Limit Increase Is Sought

U.S. Sales Contingent on New Debt Ceiling

Debt Ceiling Impasse Dampens Bond Prices

BATTLE OVER THE BUDGET: THE OVERVIEW; PRESIDENT VETOES STOPGAP BUDGET; SHUTDOWN LOOMS

Gingrich Promises Solution on Debt Ceiling ()

G.O.P. Strategy On Debt Ceiling

Bush Seeks Increase in National Debt Limit

As U.S. Debt Ceiling Is Reached, Bush Administration Seeks to Raise It Once Again

Senate Approves Budget, Breaking Spending Limits

Bush signs sweeping housing bill

5. Oct 1977

1. Oct 1981

1. Nov 1983

4. May 1987

12. May 1987

19. Oct 1989

8. Oct 1990

11. Nov 1995

11. Nov 1995

1996

1. Mar 2002

25. Dec 2002

15. Oct 2004

16. Mar 2006

30. Jul 2008

INCREASE IN NATIONAL DEBT LIMIT, AN EXCEPTION? 27

Source: WhiteHouse.gov

28

• Doyouthinkpoliticiansarecapableofcomprehendingthe complexity of the problem?

• Whydoyoutrustpoliticianswhohavealreadypromisedthefinal bailout package several times but keep coming back to the taxpayer to beg for a new one?

• DoyoutrustpoliticianswhoattemptedtocircumventtheGermanBundestag in deciding about the expected loss of up to 211bn Euros?

• Whatdoyouthink:Doesn'titseemoddthattheultimateendscenariothat politicians strive for has such a low probability of success? Shouldn’t politicians incorporate this expectation into their decision making process?

• Doyouthinkitislikelythatiftheentiremonetarysystemcollapsesin 3 years time, politicians will argue that this was due to unexpected 'external shocks' that no one could have foreseen?

• Wouldn'tithavebeenbettertoletGreecedefault?Theytoldus that the system would not have been able to absorb the shock.

• Butdidn'twerescueGreece?YetIreland/Portugal/Spain/Belgium/Italy have deteriorated to the extent that even Germany was not able to place an entire new sovereign bond issue, and meanwhile, Greece still suffers from all the debt burden!

• Isn’titstrangethatallfinancialcompaniesandinvestorsaround the world beg and force our parliament to spend enormous amounts of money? Why should these people advise our politicians at all?

• WhodoyouthinkadvisesourexpertsintheBundestag?Wouldn’tyou like to know with which experts the politicians meet? Shouldn’t they disclose this information publicly? Shouldn't the politicians discuss in more detail with the public the advantages and disadvantages of the various courses of action proposed? Shouldn't the politicians listen to those experts who foresaw the crisis for the correct reasons? So, what's going on here?!

• Giventhemagnitudeandseverityofthishistoricdecision,shouldn’twe expect each member of the Bundestag to be informed equally well? Shouldn’t they decide based upon their personal individual conscience instead of merely executing the advice of banker-influenced expert committees?

• Shouldn’tweexpectthemtobesmartenoughtodecidethisontheir own?

• Shouldn’twelistentopeoplewhosawthiscrisiscomingforthecorrect reasons? Who are they? Do you want to know? D.J. Benzemer (2009) 'No one saw this coming: Understanding Financial Crisis through Accounting Models'

• Iftheefsf idea has to be withdrawn due to impracticability despite months of negotiations, what does this tell you?

• Whomadetheproposalifitisobviousthatitdoesnotwork?

• Isn’titoddthattheEUistryingtofinanceborrowerswhoseemtohave lost creditworthiness by constructing a structured vehicle called efsf, which seems to be some sort of cdo, and trying to put an AAA label on it? Where have we seen this before?

START ASKING QUESTIONS…

![Quo vadis Europa? Assessing the impact of the Eurocrisis ... · [DRAFT VERSION – DO NOT QUOTE!] Quo vadis Europa? Assessing the impact of the Eurocrisis on the voting alignments](https://img.pdfslide.us/doc/110x75/5afddb537f8b9a444f8e0fd3/quo-vadis-europa-assessing-the-impact-of-the-eurocrisis-draft-version-do.jpg)