Embed Size (px)

Citation preview

Negative Rates in a Multi Curve FrameworkCap Pricing and Volatility Transformation

Mattias Jonsson Ulrica Samark

May 11, 2016

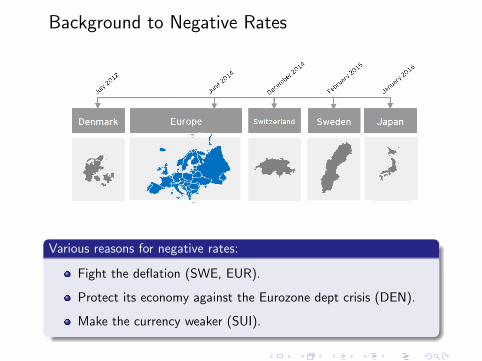

Background to Negative Rates

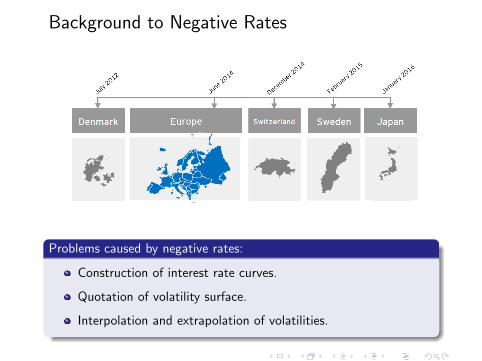

Background to Negative Rates

Various reasons for negative rates:

Fight the deflation (SWE, EUR).

Protect its economy against the Eurozone dept crisis (DEN).

Make the currency weaker (SUI).

Background to Negative Rates

Background to Negative Rates

Problems caused by negative rates:

Construction of interest rate curves.

Quotation of volatility surface.

Interpolation and extrapolation of volatilities.

Outline

1 Introduction to CapsCap ContractMarket Conventions

2 Objectives

3 TheoryShifted SABRMulti Curve FrameworkVolatility Transformation

4 Methods for Calibration

5 Results

6 Conclusions

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

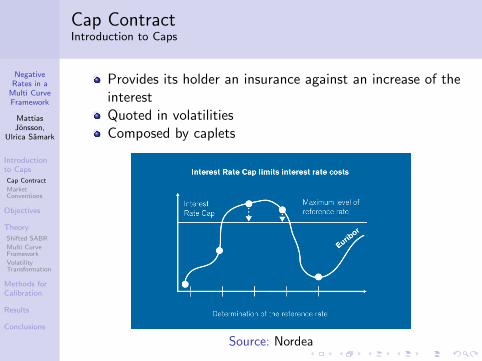

Cap ContractIntroduction to Caps

Provides its holder an insurance against an increase of theinterestQuoted in volatilitiesComposed by caplets

Source: Nordea

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

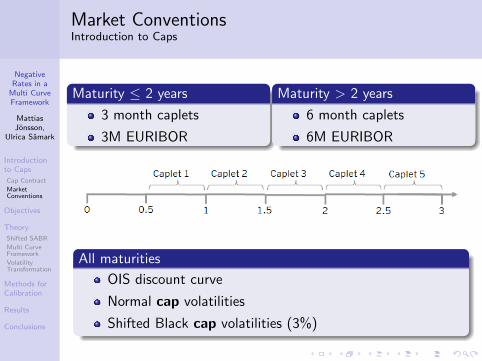

Market ConventionsIntroduction to Caps

Maturity ≤ 2 years

3 month caplets

3M EURIBOR

Maturity > 2 years

6 month caplets

6M EURIBOR

All maturities

OIS discount curve

Normal cap volatilities

Shifted Black cap volatilities (3%)

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

Market ConventionsIntroduction to Caps

Maturity ≤ 2 years

3 month caplets

3M EURIBOR

Maturity > 2 years

6 month caplets

6M EURIBOR

All maturities

OIS discount curve

Normal cap volatilities

Shifted Black cap volatilities (3%)

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

Market ConventionsIntroduction to Caps

Maturity ≤ 2 years

3 month caplets

3M EURIBOR

Maturity > 2 years

6 month caplets

6M EURIBOR

All maturities

OIS discount curve

Normal cap volatilities

Shifted Black cap volatilities (3%)

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

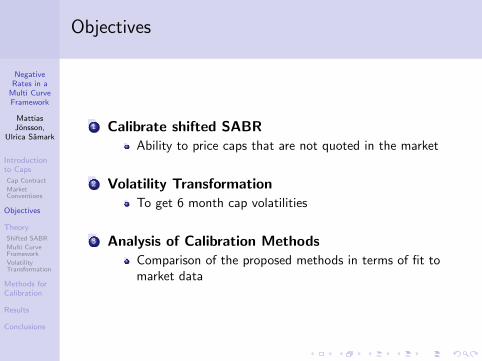

Objectives

1 Calibrate shifted SABRAbility to price caps that are not quoted in the market

2 Volatility TransformationTo get 6 month cap volatilities

3 Analysis of Calibration MethodsComparison of the proposed methods in terms of fit tomarket data

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

Objectives

1 Calibrate shifted SABRAbility to price caps that are not quoted in the market

2 Volatility TransformationTo get 6 month cap volatilities

3 Analysis of Calibration MethodsComparison of the proposed methods in terms of fit tomarket data

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

Objectives

1 Calibrate shifted SABRAbility to price caps that are not quoted in the market

2 Volatility TransformationTo get 6 month cap volatilities

3 Analysis of Calibration MethodsComparison of the proposed methods in terms of fit tomarket data

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

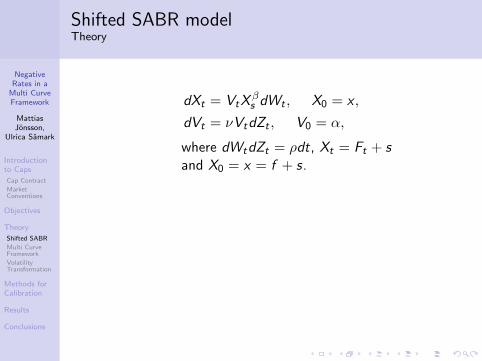

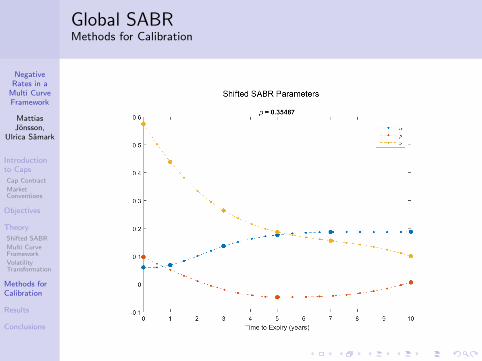

Shifted SABR modelTheory

dXt = VtXβs dWt , X0 = x ,

dVt = νVtdZt , V0 = α,

where dWtdZt = ρdt, Xt = Ft + sand X0 = x = f + s.

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

Shifted SABR modelTheory

dXt = VtXβs dWt , X0 = x ,

dVt = νVtdZt , V0 = α,

where dWtdZt = ρdt, Xt = Ft + sand X0 = x = f + s.

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

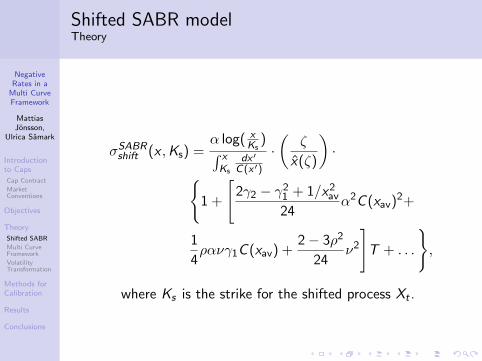

Shifted SABR modelTheory

σSABRshift (x ,Ks) =α log( x

Ks)∫ x

Ks

dx ′

C(x ′)

·(

ζ

x(ζ)

)·{

1 +

[2γ2 − γ2

1 + 1/x2av

24α2C (xav)2+

1

4ρανγ1C (xav) +

2 − 3ρ2

24ν2

]T + . . .

},

where Ks is the strike for the shifted process Xt .

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

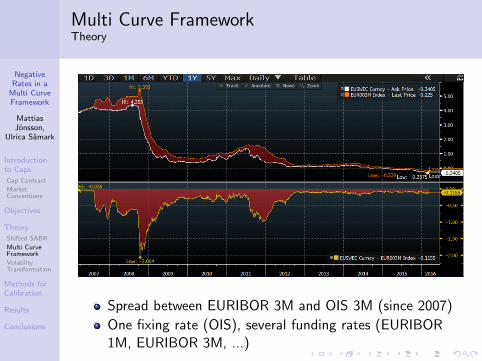

Multi Curve FrameworkTheory

Spread between EURIBOR 3M and OIS 3M (since 2007)

One fixing rate (OIS), several funding rates (EURIBOR1M, EURIBOR 3M, ...)

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

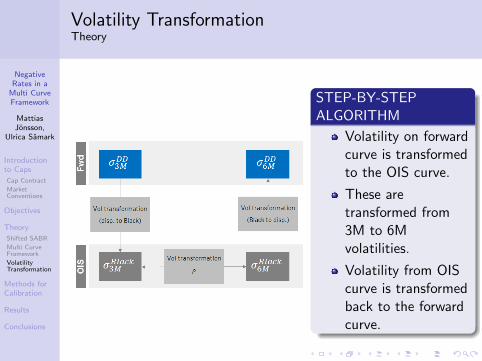

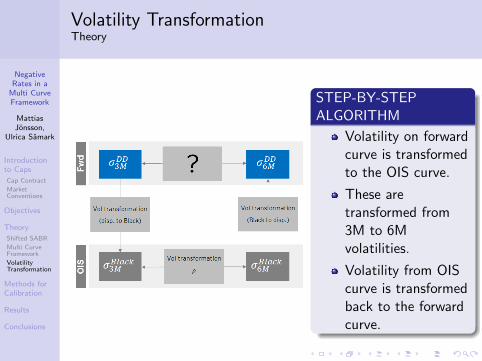

Volatility TransformationTheory

STEP-BY-STEPALGORITHM

Volatility on forwardcurve is transformedto the OIS curve.

These aretransformed from3M to 6Mvolatilities.

Volatility from OIScurve is transformedback to the forwardcurve.

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

Volatility TransformationTheory

STEP-BY-STEPALGORITHM

Volatility on forwardcurve is transformedto the OIS curve.

These aretransformed from3M to 6Mvolatilities.

Volatility from OIScurve is transformedback to the forwardcurve.

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

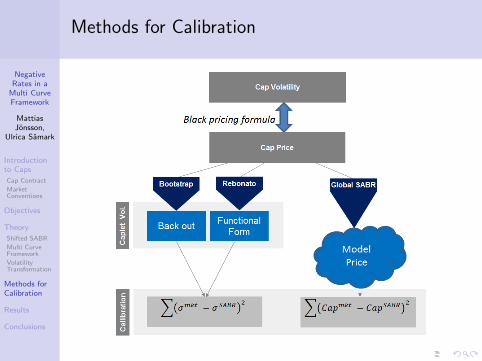

Methods for Calibration

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

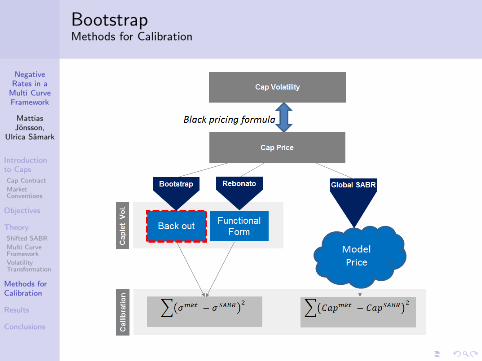

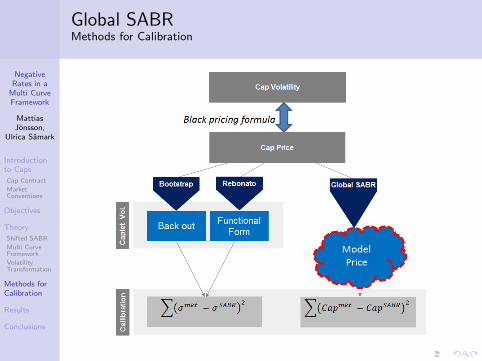

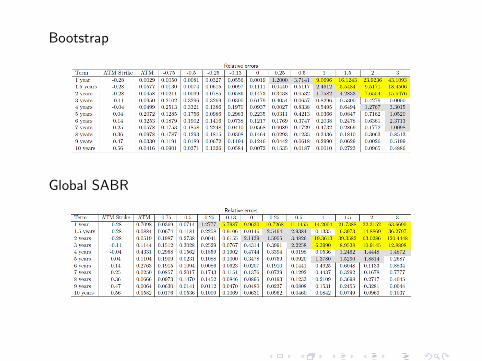

BootstrapMethods for Calibration

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

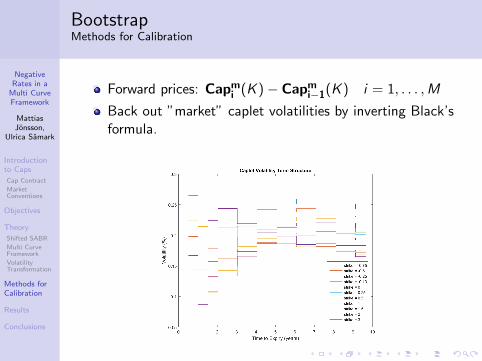

BootstrapMethods for Calibration

Forward prices: Capmi (K ) − Capmi−1(K ) i = 1, . . . ,M

Back out ”market” caplet volatilities by inverting Black’sformula.

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

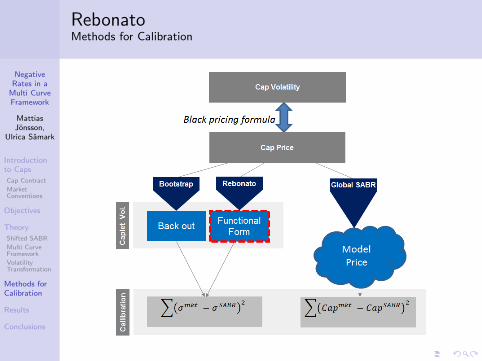

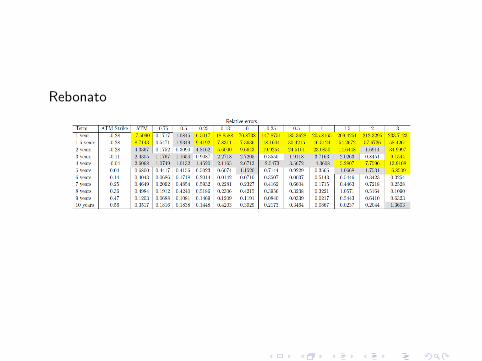

RebonatoMethods for Calibration

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

RebonatoMethods for Calibration

Fit a functional form to get caplet volatilities

σ(s) =[a + b(T − s)

]exp

[− c(T − s)

]+ d .

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

Global SABRMethods for Calibration

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

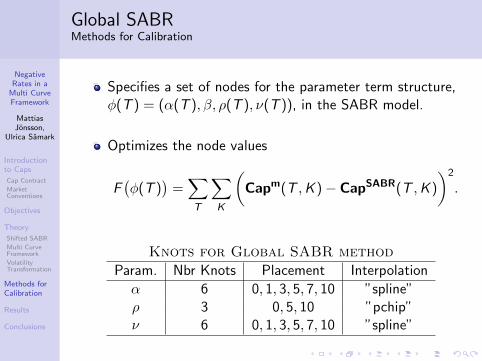

Global SABRMethods for Calibration

Specifies a set of nodes for the parameter term structure,φ(T ) = (α(T ), β, ρ(T ), ν(T )), in the SABR model.

Optimizes the node values

F(φ(T )

)=∑T

∑K

(Capm(T ,K ) − CapSABR(T ,K )

)2

.

Knots for Global SABR method

Param. Nbr Knots Placement Interpolation

α 6 0, 1, 3, 5, 7, 10 ”spline”ρ 3 0, 5, 10 ”pchip”ν 6 0, 1, 3, 5, 7, 10 ”spline”

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

Global SABRMethods for Calibration

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

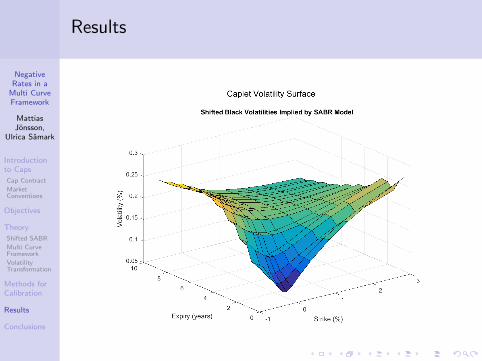

Results

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

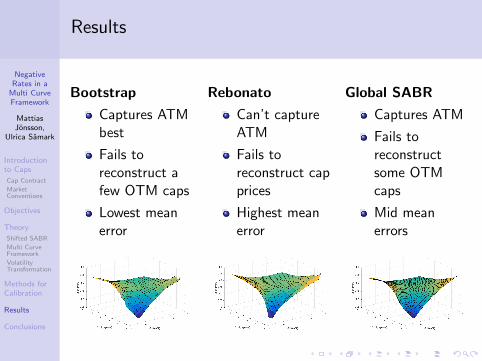

Results

Bootstrap

Captures ATMbest

Fails toreconstruct afew OTM caps

Lowest meanerror

Rebonato

Can’t captureATM

Fails toreconstruct capprices

Highest meanerror

Global SABR

Captures ATM

Fails toreconstructsome OTMcaps

Mid meanerrors

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

Conclusions

The calibration of shifted SABR works well.

The developed algorithm for volatility transformationworks fine.

The best performing method is Bootstrap.

NegativeRates in a

Multi CurveFramework

MattiasJonsson,

Ulrica Samark

Introductionto Caps

Cap Contract

MarketConventions

Objectives

Theory

Shifted SABR

Multi CurveFramework

VolatilityTransformation

Methods forCalibration

Results

Conclusions

Further Research

Develop a framework for estimating correlations betweenforward rates.

Refine node selection algorithm in global SABR.

Investigate if normal volatilities could be used, and developa similar transformation technique.

Don’t be negative, just shift andkeep on smiling!

Calibration Errors

Bootstrap

Global SABR

Calibration Errors

Rebonato

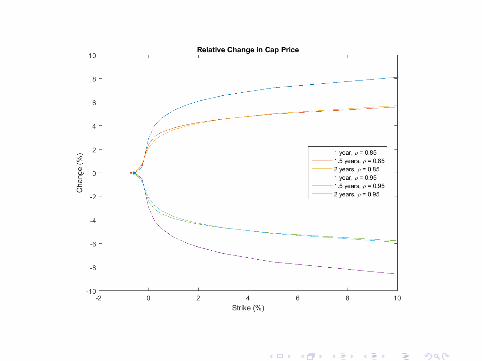

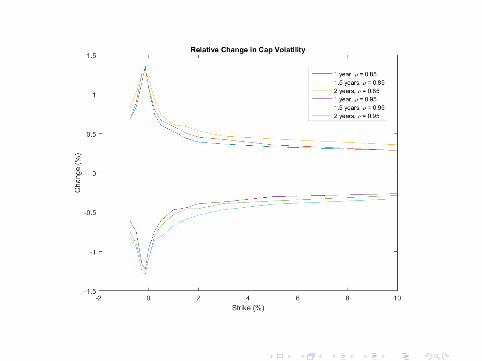

Sensitivity of Correlation

Sensitivity of Correlation