Embed Size (px)

Citation preview

Monetary

&

Fiscal Policy

What does the Eurozone need?

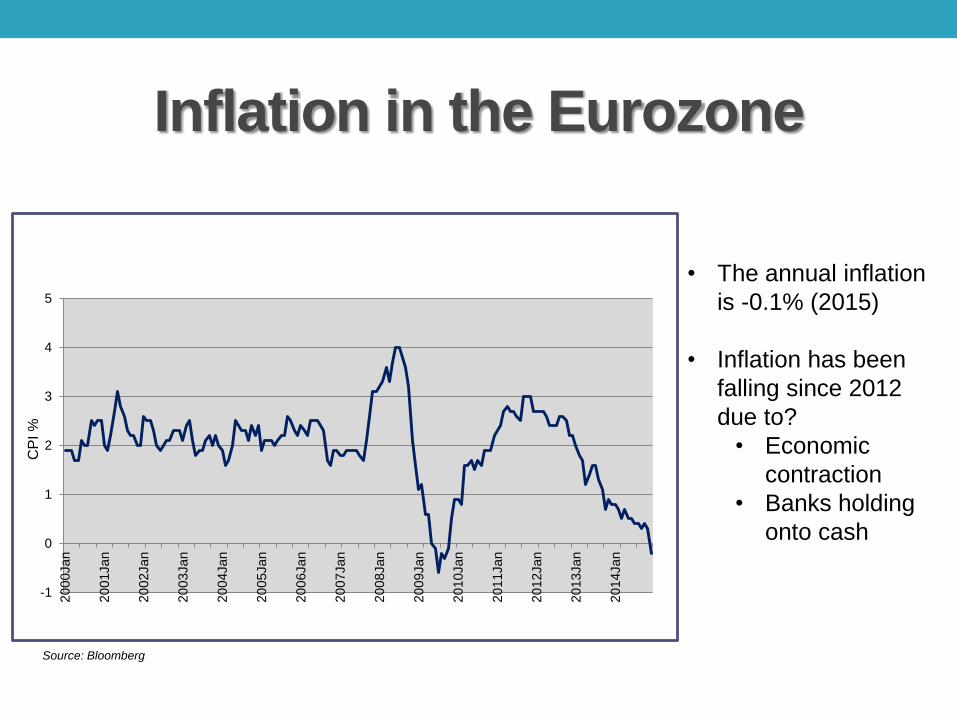

Inflation in the Eurozone

• The annual inflation

is -0.1% (2015)

• Inflation has been

falling since 2012

due to?

• Economic

contraction

• Banks holding

onto cash

-1

0

1

2

3

4

5

20

00Jan

20

01Jan

20

02Jan

20

03Jan

20

04Jan

20

05Jan

20

06Jan

20

07Jan

20

08Jan

20

09Jan

20

10Jan

20

11Jan

20

12Jan

20

13Jan

20

14Jan

CP

I %

Source: Bloomberg

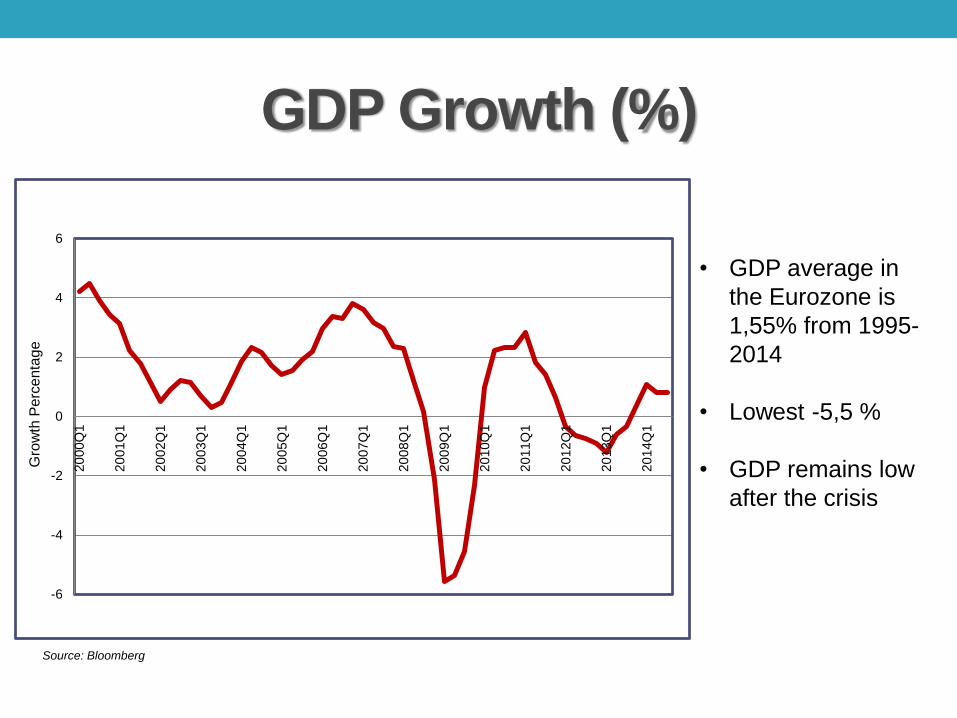

GDP Growth (%)

• GDP average in

the Eurozone is

1,55% from 1995-

2014

• Lowest -5,5 %

• GDP remains low

after the crisis

-6

-4

-2

0

2

4

6

20

00Q

1

20

01Q

1

20

02Q

1

20

03Q

1

20

04Q

1

20

05Q

1

20

06Q

1

20

07Q

1

20

08Q

1

20

09Q

1

20

10Q

1

20

11Q

1

20

12Q

1

20

13Q

1

20

14Q

1

Gro

wth

Pe

rce

nta

ge

Source: Bloomberg

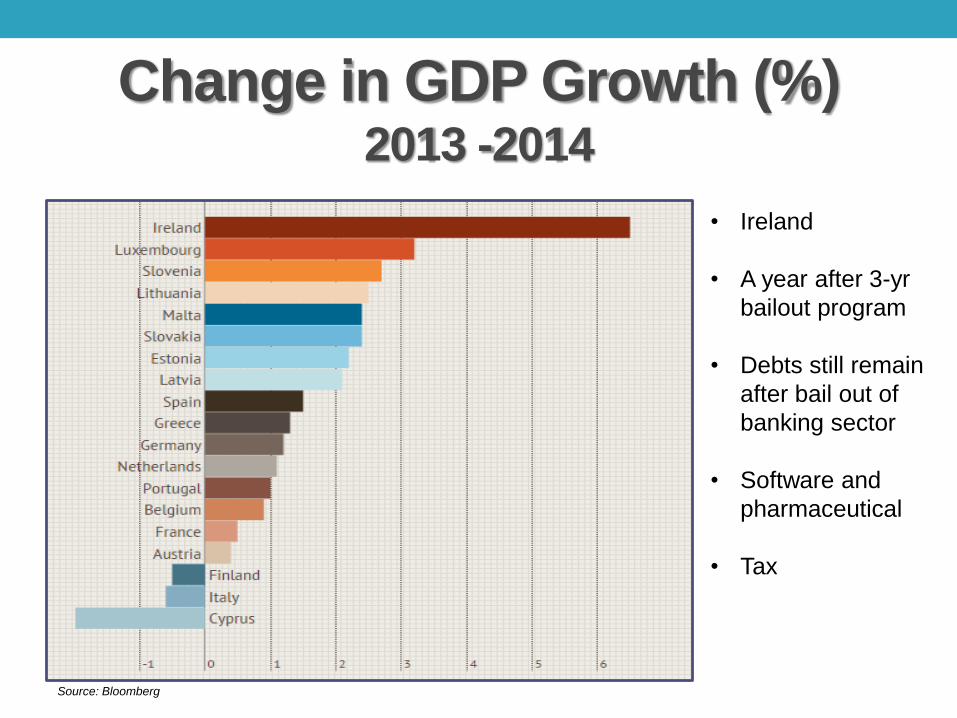

Change in GDP Growth (%) 2013 -2014

• Ireland

• A year after 3-yr

bailout program

• Debts still remain

after bail out of

banking sector

• Software and

pharmaceutical

• Tax

Source: Bloomberg

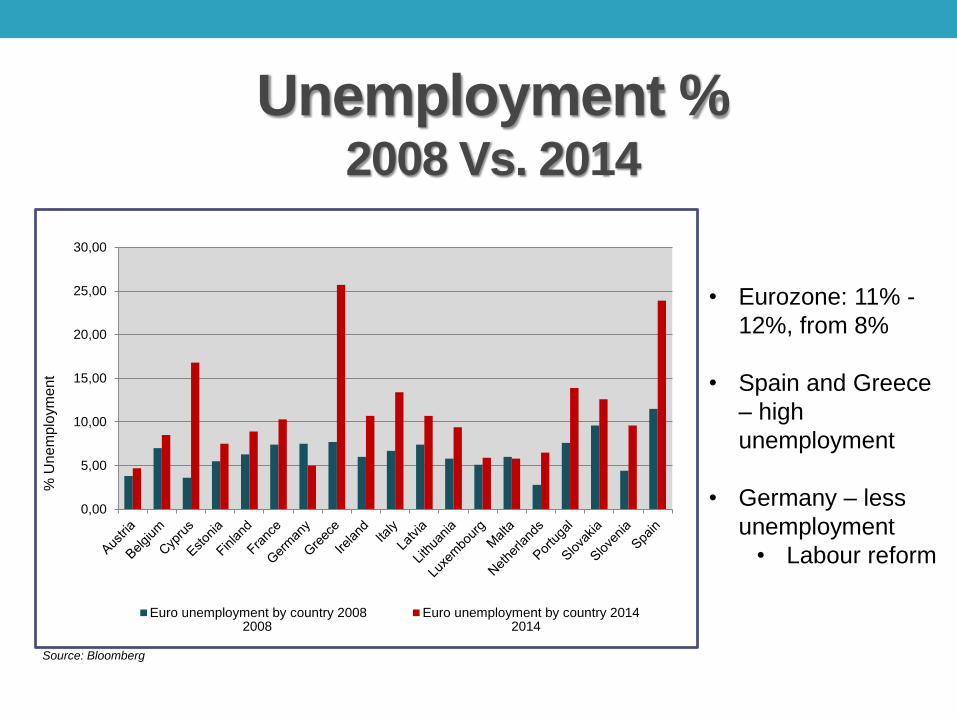

Unemployment % 2008 Vs. 2014

• Eurozone: 11% -

12%, from 8%

• Spain and Greece

– high

unemployment

• Germany – less

unemployment

• Labour reform

0,00

5,00

10,00

15,00

20,00

25,00

30,00

Euro unemployment by country 2008 Euro unemployment by country 2014

% U

nem

plo

ym

ent

2008 2014

Source: Bloomberg

Government Imbalance

• Deficit

• Spain, Greece

• Germany

zero/near zero

balance

Source: European Commission

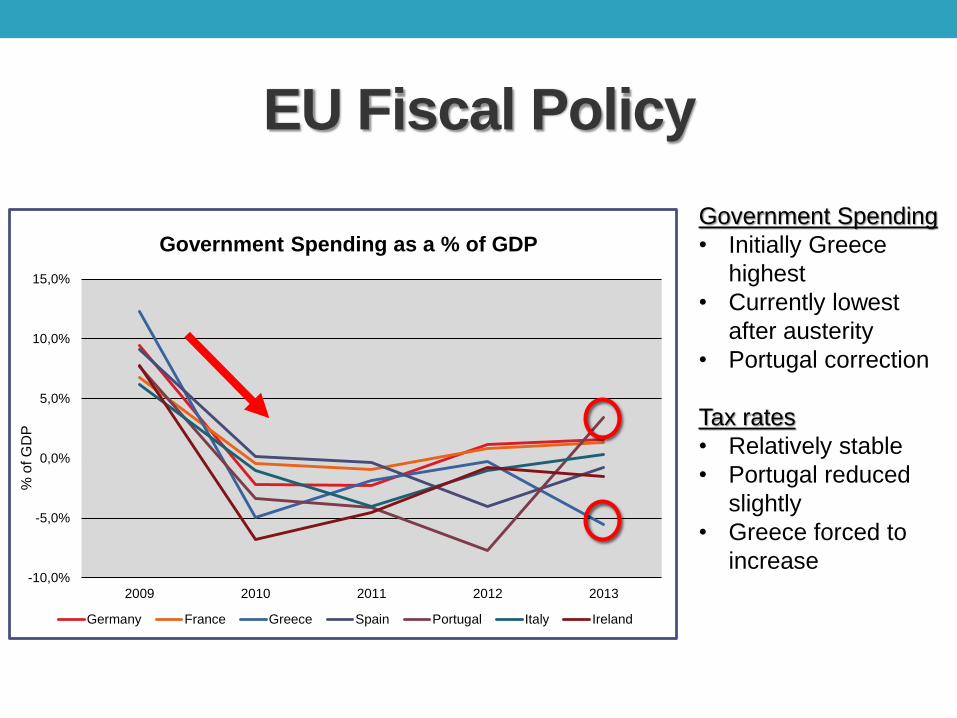

EU Fiscal Policy

Government Spending

• Initially Greece

highest

• Currently lowest

after austerity

• Portugal correction

Tax rates

• Relatively stable

• Portugal reduced

slightly

• Greece forced to

increase-10,0%

-5,0%

0,0%

5,0%

10,0%

15,0%

2009 2010 2011 2012 2013

Germany France Greece Spain Portugal Italy Ireland

Government Spending as a % of GDP

% o

f G

DP

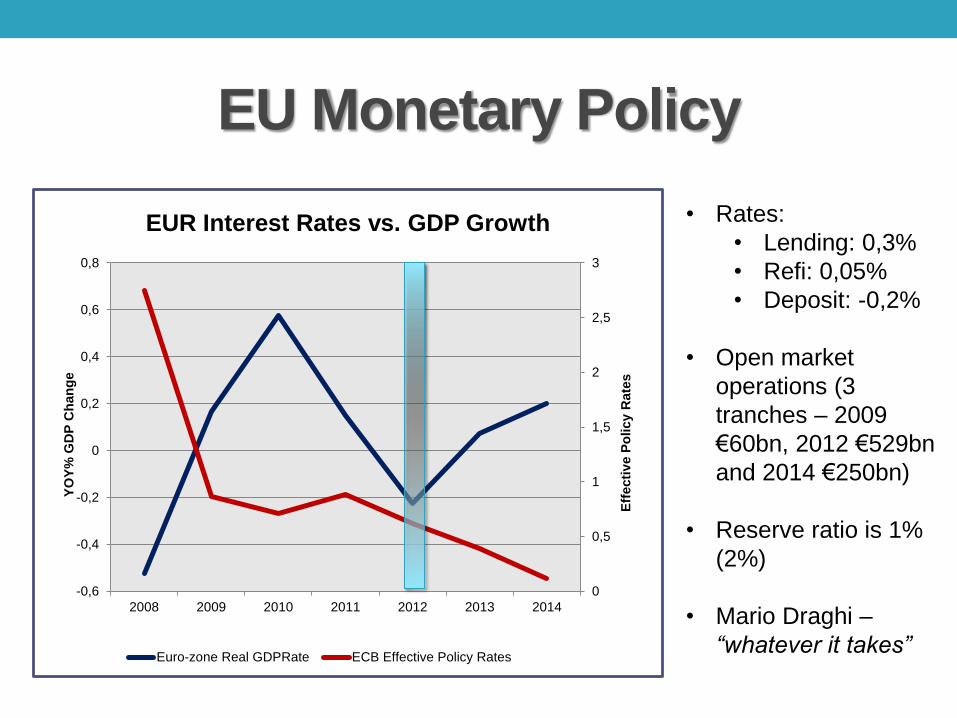

EU Monetary Policy

• Rates:

• Lending: 0,3%

• Refi: 0,05%

• Deposit: -0,2%

• Open market

operations (3

tranches – 2009

€60bn, 2012 €529bn

and 2014 €250bn)

• Reserve ratio is 1%

(2%)

• Mario Draghi –

“whatever it takes”

0

0,5

1

1,5

2

2,5

3

-0,6

-0,4

-0,2

0

0,2

0,4

0,6

0,8

2008 2009 2010 2011 2012 2013 2014

Eff

ecti

ve P

olicy R

ate

s

YO

Y%

GD

P C

han

ge

EUR Interest Rates vs. GDP Growth

Euro-zone Real GDPRate ECB Effective Policy Rates

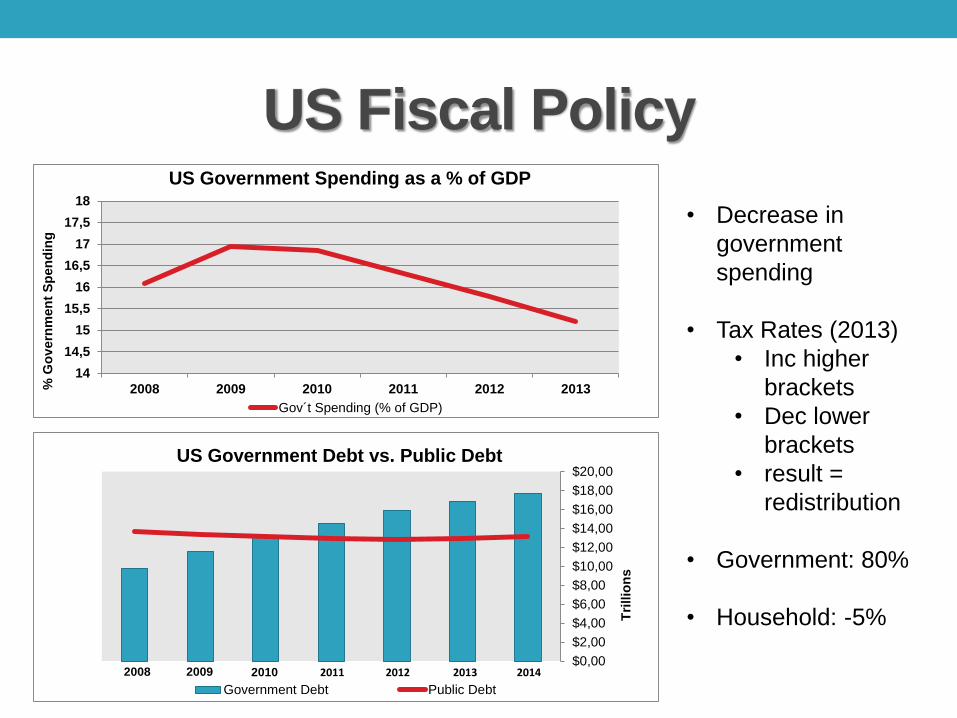

US Fiscal Policy

• Decrease in

government

spending

• Tax Rates (2013)

• Inc higher

brackets

• Dec lower

brackets

• result =

redistribution

• Government: 80%

• Household: -5%

14

14,5

15

15,5

16

16,5

17

17,5

18

2008 2009 2010 2011 2012 2013% G

ov

ern

men

t S

pen

din

g

US Government Spending as a % of GDP

Gov´t Spending (% of GDP)

$0,00

$2,00

$4,00

$6,00

$8,00

$10,00

$12,00

$14,00

$16,00

$18,00

$20,00

Tri

llio

ns

US Government Debt vs. Public Debt

Government Debt Public Debt

2008 2009 2010 2011 2012 2013 2014

US Monetary Policy

• Stable low US rates

• Introduction of QE in

2008

• Total QE spend:

$4,5T

• GDP growth

recovered since the

crisis

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

-3,00

-2,00

-1,00

0,00

1,00

2,00

3,00

2008 2009 2010 2011 2012 2013 2014

US Interest Rates vs. GDP Growth

Real GDP (yoy %) Policy Rates

Inte

rest

GD

P G

row

th %

QE1 Dec08-March10 QE2 Nov10-June11 QE3 Sept12-Oct14

TS 0,3 0,6 0,9

MBS & AD 1,35 0,79

0

0,2

0,4

0,6

0,8

1

1,2

1,4

1,6

1,8

$T

rillio

n

Quantitative Easing

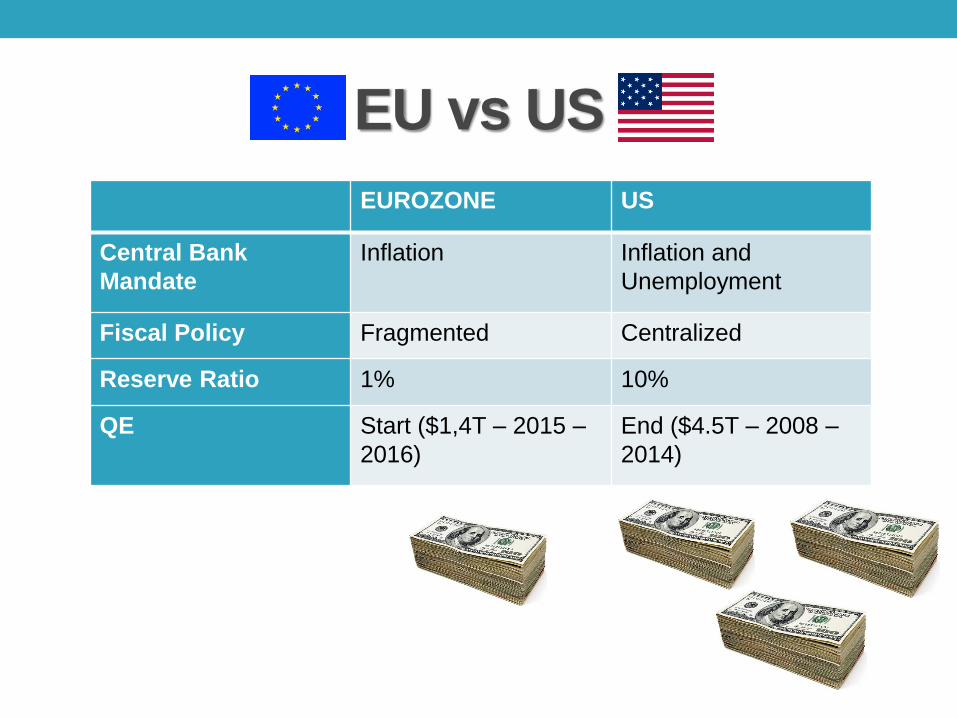

EU vs US

EUROZONE US

Central Bank

Mandate

Inflation Inflation and

Unemployment

Fiscal Policy Fragmented Centralized

Reserve Ratio 1% 10%

QE Start ($1,4T – 2015 –

2016)

End ($4.5T – 2008 –

2014)

Unemployment vs Inflation

• US policies have

been effective:

• CPI

• Unemployment

• Rates

-4

-2

0

2

4

6

8

10

12

14

EUR Unemployment Rate (%) US Unemployment Rate (%)

EU CPI US CPI

Pe

rce

nta

ge

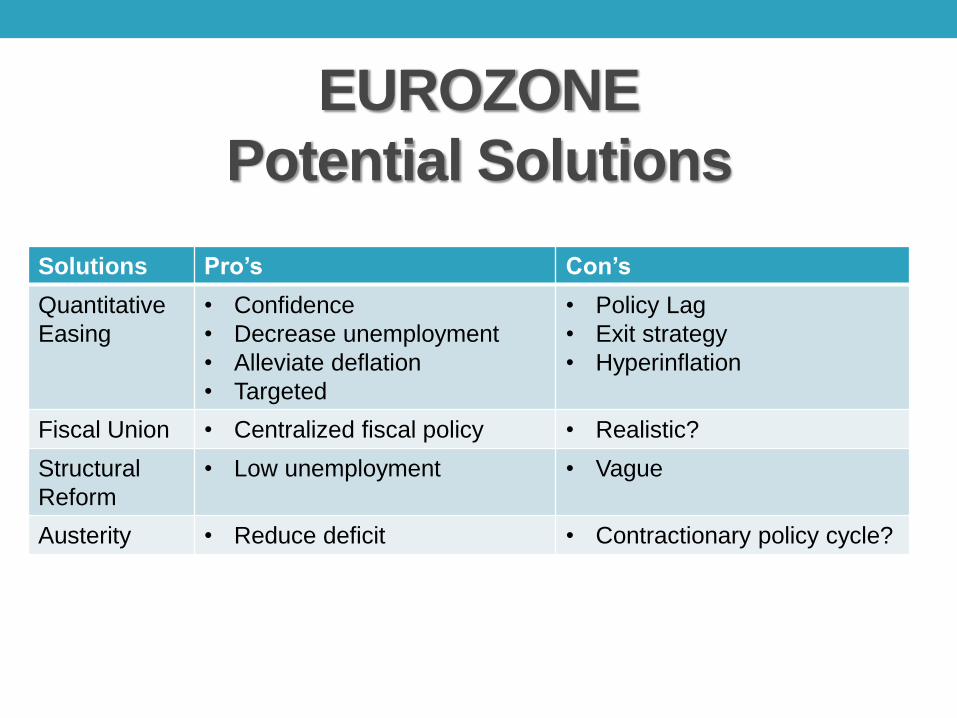

EUROZONE

Potential Solutions

Solutions Pro’s Con’s

Quantitative

Easing

• Confidence

• Decrease unemployment

• Alleviate deflation

• Targeted

• Policy Lag

• Exit strategy

• Hyperinflation

Fiscal Union • Centralized fiscal policy • Realistic?

Structural

Reform

• Low unemployment • Vague

Austerity • Reduce deficit • Contractionary policy cycle?

Our Recommendation

Quantitative Easing with Targeted Structural Reforms• Cautious in implementation

• Exit planningo Method

o Timing

• Structural reforms implemented alongsideo Labour market

o Innovation

Our Recommendation

Quantitative Easing

• Cautious in implementation

• Exit planning

o Method

o Timing

• Structural reforms implemented alongside

o EG: Spanish labour market rules

o Innovation

o Benefits