Embed Size (px)

Citation preview

June Monetary Policy Review

Cape Town3 June 2015

2

Headlines

Evolving global conditions

Headline CPI likely to be sticky around 6% as petrol impact dissipates

Underlying inflation and expectations persistent

Output gap still negative, but potential growth lower

Risks to inflation high… Food, electricity, remuneration, currency

Monetary policy remains in a gradual tightening cycle

3

Overview of the presentation

I. The world economy

II. Growth and the GDP forecast

III. Inflation and the inflation outlook

I. The world economy

4

5

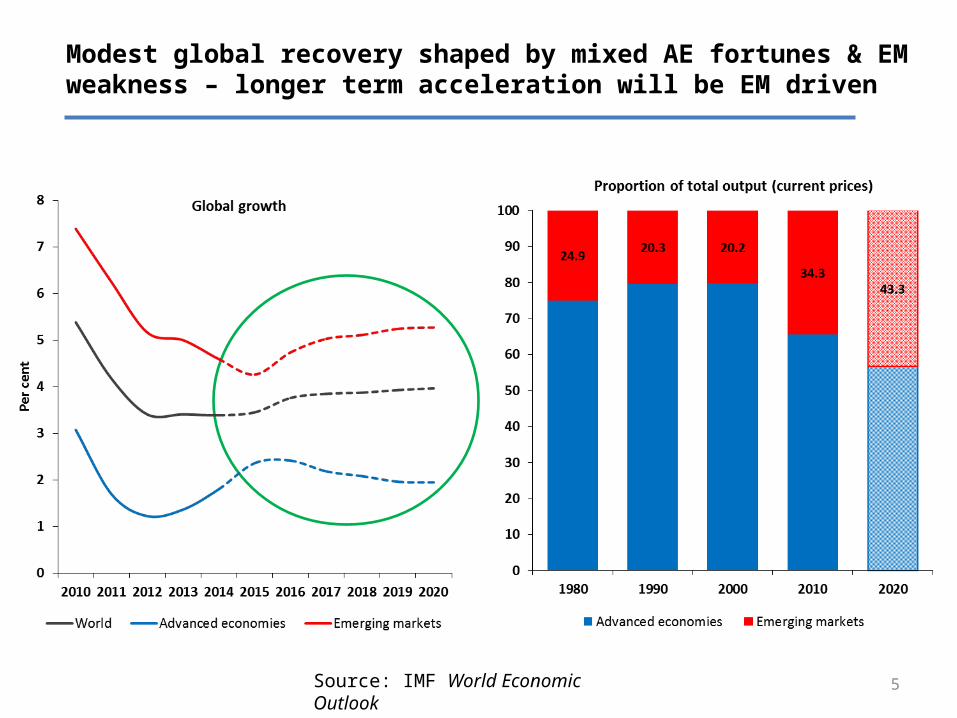

Modest global recovery shaped by mixed AE fortunes & EM weakness – longer term acceleration will be EM driven

Source: IMF World Economic Outlook

6

The advanced economy recovery is chiefly a US-UK story…

8

China’s economy is slowing and rebalancing…

9

…with important consequences for commodity prices

10

Chinese monetary policy easing as inflation falls & GDP slows

11

Global monetary conditions continue to support financing in EMs

12

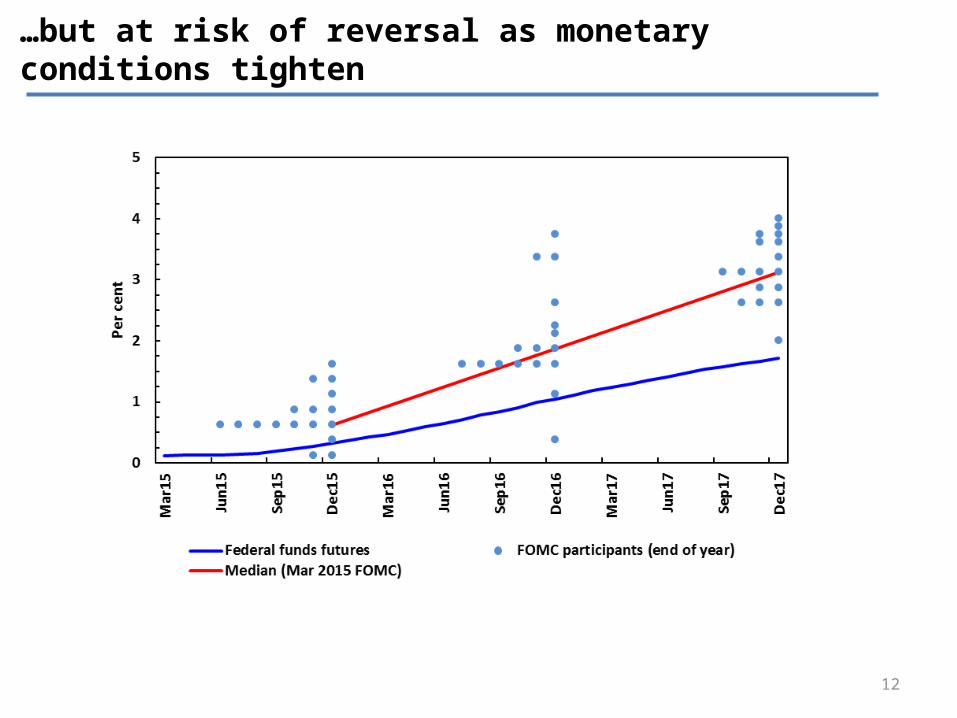

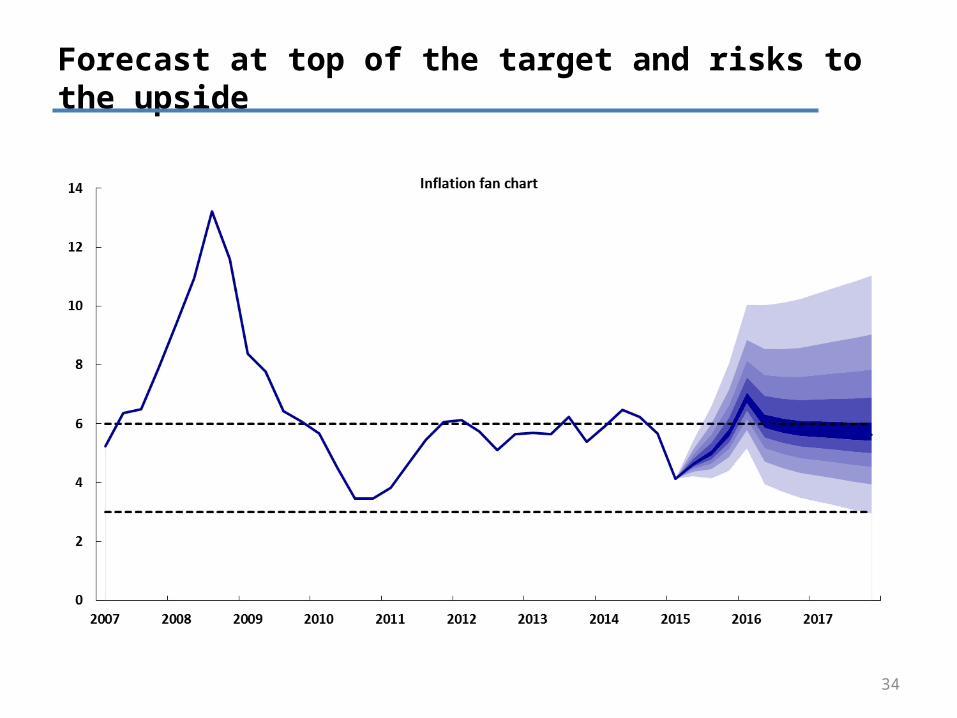

…but at risk of reversal as monetary conditions tighten

13

II. Growth and the GDP forecast

14

SA growth forecasts closer to 2%, with pick up late in the period

Nov13

Jan14

Mar1

4

May

14Ju

l14Se

p14

Nov14

Jan15

Mar1

5

May

151.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

3.1

3.3

3.5

Growth forecasts over time

2015 real GDP

2016 real GDP

2017 real GDP

Date of forecast

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8Growth fan chart

15

Lower potential but output gap still negative

16

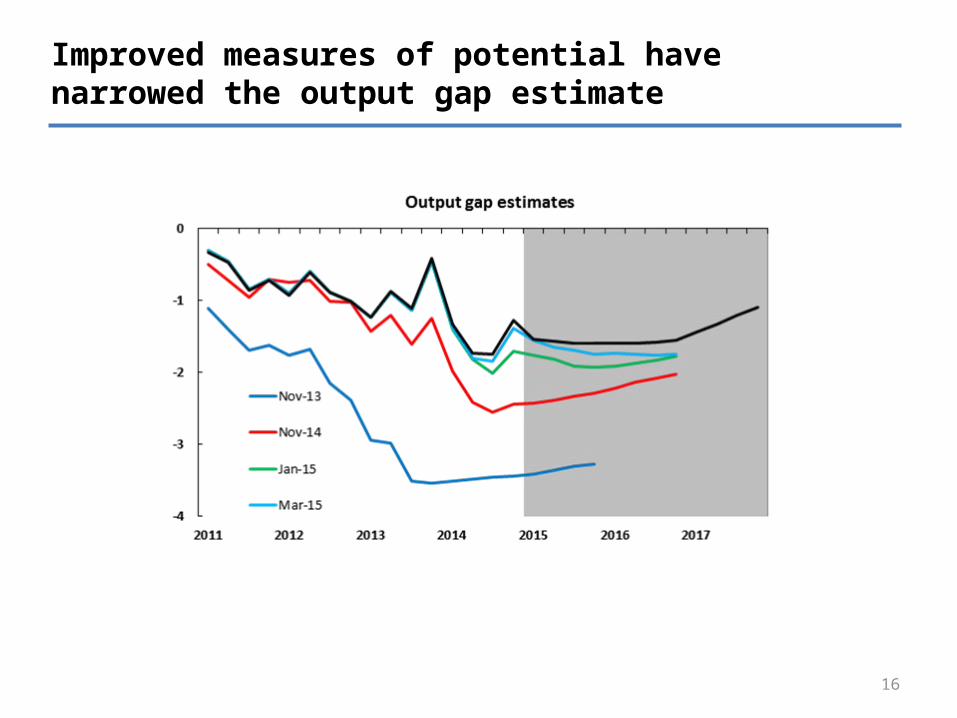

Improved measures of potential have narrowed the output gap estimate

17

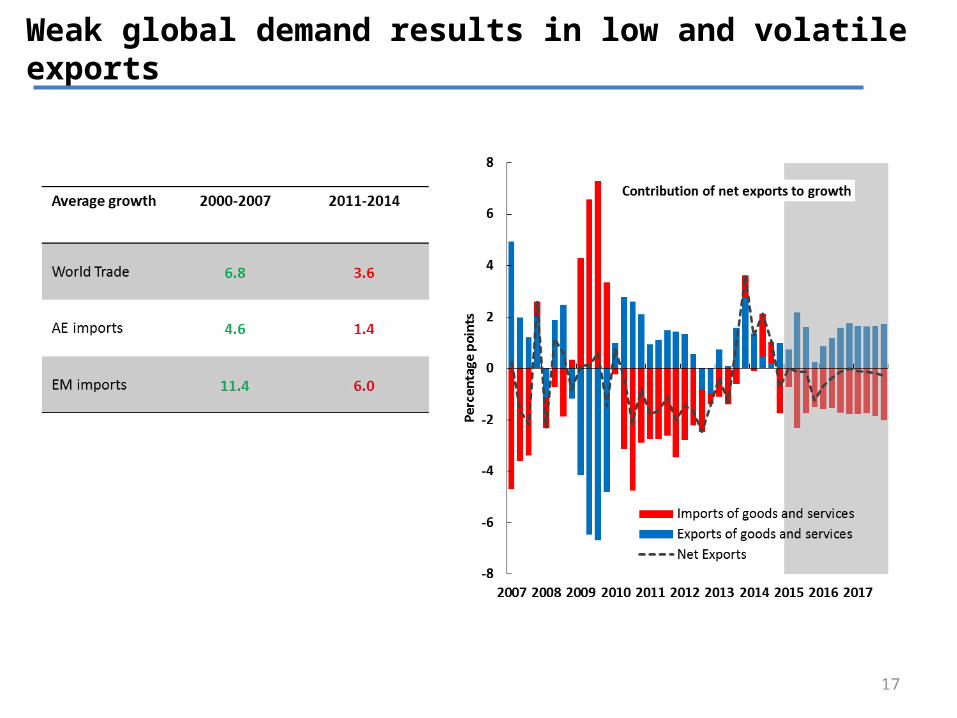

Weak global demand results in low and volatile exports

18

… and inflation diluting competitiveness gains…

19

… while commodity prices decline … CSC over?

Commodity price assumptions down 37% in two years

21

Shortages in energy intensive economy hit hard

22

…curtailing investment (outside electricity sector)

23

Household consumption still underpins growth forecast

24

…while debt to GDP burdens weigh against further leverage

25

And net job creation tailing off

26

III. Inflation and the inflation outlook

27

World inflation unusually low due to weak demand… falling food & oil prices

28

South African inflation running ahead

29

The inflation respite from cheap oil was brief

30

Higher inflation propelled by a series of supply shocks…

31

…as well as high unit labour cost growth

32

Not unhinging expectations, but fostering convergence

33

Convergence around the top of the target range

Hassan, Shakill, Siobhan Redford, and Franz Ruch. 2015. Dispersion of Inflation Expectations. SA Reserve Bank, Working Paper (forthcoming).

34

Forecast at top of the target and risks to the upside

35

World food prices low, but currency and drought keeping SA prices buoyant

Depreciation to the USD sustained but EMs still exposed

36

37

South Africa’s current account deficit narrowing slowly

38

Unit labour costs expected to moderate somewhat, with risks

20042005

20062007

20082009

20102011

20122013

20142015

20162017

0

3

6

9

12

15

Core inflation Unit labour cost

39

Electricity prices have the potential to shock

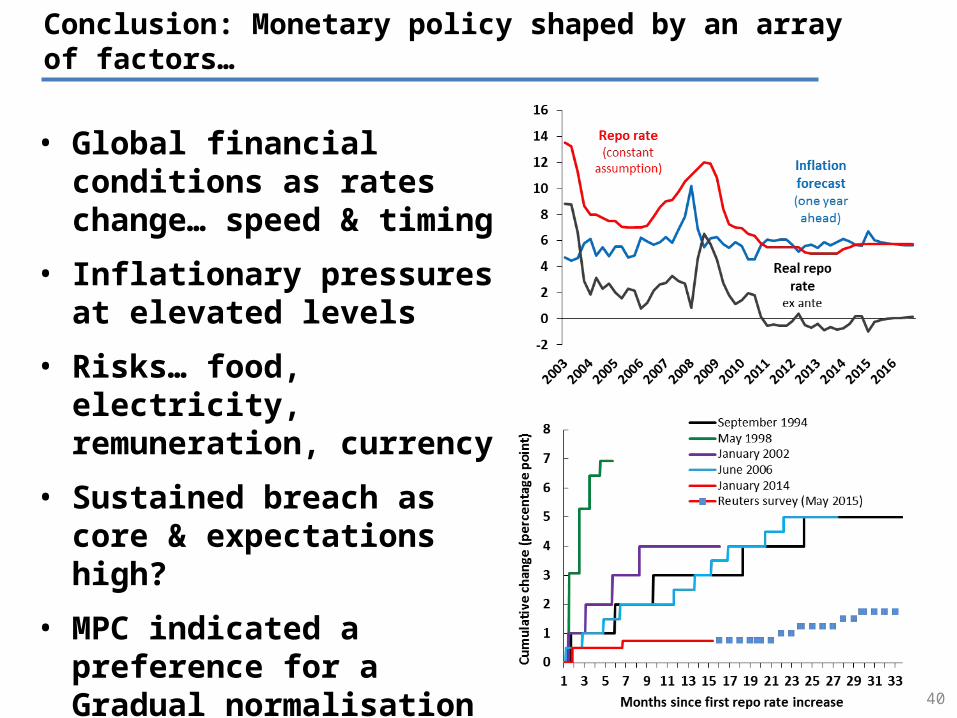

Conclusion: Monetary policy shaped by an array of factors…

• Global financial conditions as rates change… speed & timing

• Inflationary pressures at elevated levels

• Risks… food, electricity, remuneration, currency

• Sustained breach as core & expectations high?

• MPC indicated a preference for a Gradual normalisation path in keeping with or flexible IT framework

40