Embed Size (px)

Citation preview

Investor Presentation

January 2014

George Rossolatos, Co-CEO

Avante Logixx Inc. TSXV: XX OTC:ALXXF www.avantelogixx.com

INDEX

Section 1: Introduction

Section 2: History

Section 3: Where We Are Today

Section 4: Where We’re Going: Strategy and Outlook

Appendix A: Trading Comparables

FORWARD LOOKING INFORMATION

This presentation may contain "forward-looking statements" within the meaning of applicable securities legislation.

Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as "plans",

"expects" or "does not expect", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates" or

"does not anticipate", or "believes" or variations of such words and phrases or state that certain actions, events or results

"may", "could", "would", "might" or "will be taken", "occur" or "be achieved". Forward-looking statements are subject to

known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or

achievements of Avante to be materially different from those expressed or implied by such forward-looking statements.

Although Avante has attempted to identify important factors that could cause actual results to differ materially from those

contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or

intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could

differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-

looking statements. Avante does not undertake to update any forward-looking statements, except in accordance with

applicable securities laws.

DISCLAIMER

This presentation is for information purposes only and is not intended to, and should not be construed to constitute, an offer

to sell or the solicitation of an offer to buy, Avante’s securities. This presentation and its contents should not be construed,

under any circumstances, as investment, tax or legal advice. Any person viewing or accepting delivery of this presentation

acknowledges the need to conduct their own thorough investigation into Avante’s business and its activities before

considering any investment in Avante’s securities. Among other things, investors should review Avante’s public filings which

are available in Canada at www.sedar.com

Section 1

INTRODUCTION

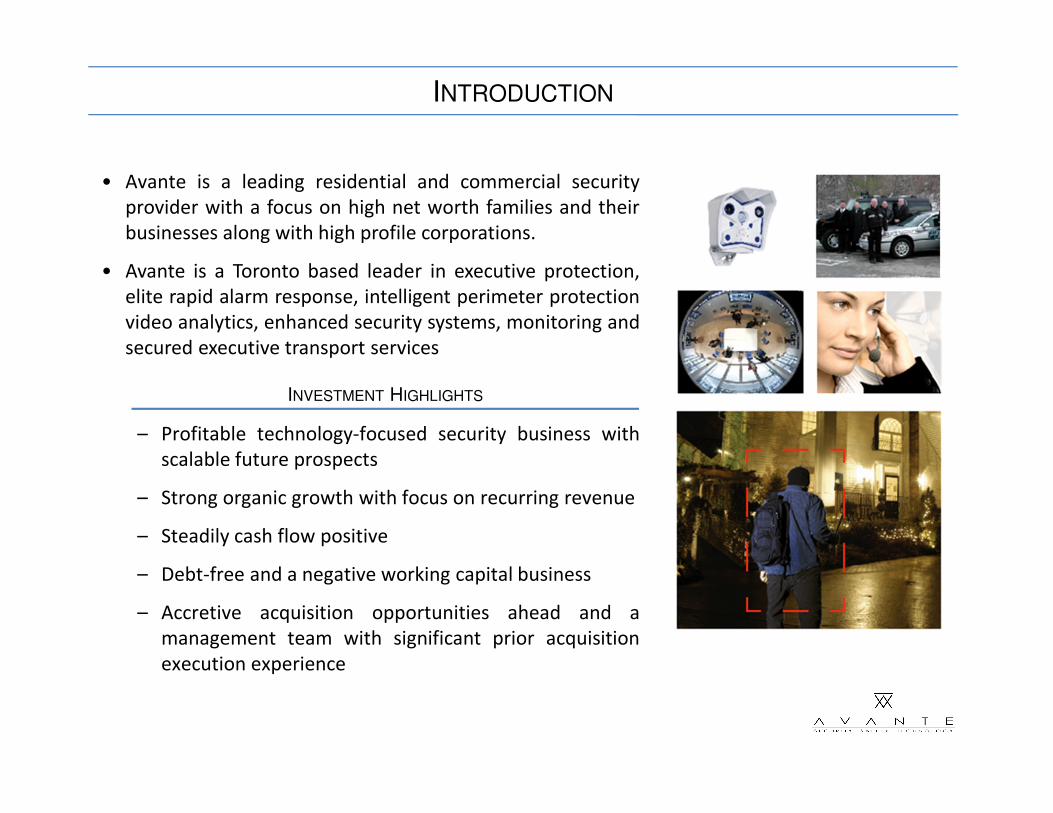

INTRODUCTION

• Avante is a leading residential and commercial security

provider with a focus on high net worth families and their

businesses along with high profile corporations.

• Avante is a Toronto based leader in executive protection,

elite rapid alarm response, intelligent perimeter protection

video analytics, enhanced security systems, monitoring and

secured executive transport services

– Profitable technology-focused security business with

scalable future prospects

– Strong organic growth with focus on recurring revenue

– Steadily cash flow positive

– Debt-free and a negative working capital business

– Accretive acquisition opportunities ahead and a

management team with significant prior acquisition

execution experience

INVESTMENT HIGHLIGHTS

Section 2

HISTORY

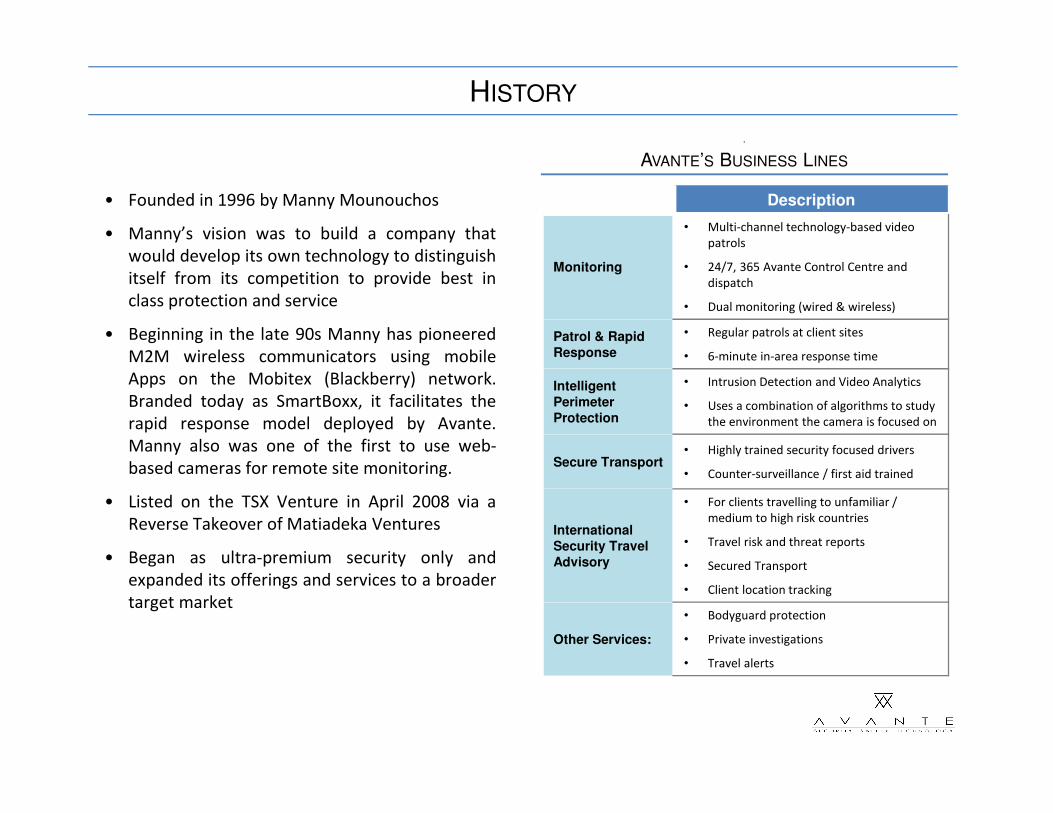

HISTORY

• Founded in 1996 by Manny Mounouchos

• Manny’s vision was to build a company that

would develop its own technology to distinguish

itself from its competition to provide best in

class protection and service

• Beginning in the late 90s Manny has pioneered

M2M wireless communicators using mobile

Apps on the Mobitex (Blackberry) network.

Branded today as SmartBoxx, it facilitates the

rapid response model deployed by Avante.

Manny also was one of the first to use web-

based cameras for remote site monitoring.

• Listed on the TSX Venture in April 2008 via a

Reverse Takeover of Matiadeka Ventures

• Began as ultra-premium security only and

expanded its offerings and services to a broader

target market

3

AVANTE’S BUSINESS LINES

v Description

Monitoring

• Multi-channel technology-based video

patrols

• 24/7, 365 Avante Control Centre and

dispatch

• Dual monitoring (wired & wireless)

Patrol & Rapid

Response

• Regular patrols at client sites

• 6-minute in-area response time

Intelligent

Perimeter

Protection

• Intrusion Detection and Video Analytics

• Uses a combination of algorithms to study

the environment the camera is focused on

Secure Transport• Highly trained security focused drivers

• Counter-surveillance / first aid trained

International

Security Travel

Advisory

• For clients travelling to unfamiliar /

medium to high risk countries

• Travel risk and threat reports

• Secured Transport

• Client location tracking

Other Services:

• Bodyguard protection

• Private investigations

• Travel alerts

PAST CHALLENGES

In the years leading up to 2010-2011, Avante’s SmartBoxx was gaining acceptance in the energy

management space as a demand response tool. Its GSM-based engineering made it unique

compared to other internet based solutions.

• Avante undertook a costly innovation development program to create energy management

technology for a new market – the utilities – that in hindsight exceeded its capabilities and its

financial wherewithal at the time

• By 2010-2011, the company was burning cash on account of:

– High capital spending to integrate its SmartBoxx into the utility and energy markets

– Loss of focus on core security business

• Technology development for the energy market was causing the company to exhaust its

financial resources:

– This technology spending consumed the company’s cash reserves with significant

dilution from requisite equity issues.

– The payoff from this technology development was distant and uncertain with the

prospect of a continued technology spend to keep up with the likes of GE, Honeywell

and others

AVANTE STRENGTHENS MANAGEMENT TEAM

• In June 2010, George Rossolatos joined Manny Mounouchos as Co-CEO to focus on corporate and operational

strategy & execution while Manny would focus on strategic sales and business development

• George made a concurrent investment in Avante and has since become the 2nd largest shareholder after Manny

• George’s role was to bring private equity discipline, capital markets expertise and a focus on profit and growth to

complement Manny’s skillset as an entrepreneur and innovator in advanced security solutions and services

• Prior to Avante, George founded Riverdale Capital with the intent of finding a business in which he could take a

senior operational role to drive value creation

• Prior to Riverdale, he co-founded private equity firm TorQuest Partners in 2002 with Brent Belzberg

– At TorQuest from 2002 to 2009, George and his partners raised and invested two funds of $180 million

and $550 million respectively

– TorQuest’s overall IRR from exited investments was in excess of 60%

• Previously, George worked as an investment professional at Harrowston Inc., a publicly traded private equity

fund

• Prior to Harrowston, he worked in a management role with Ernst & Young

• Recognized in 2007 as one of Canada’s Top 40 under 40

• CPA/CA (Ontario) and holds an MBA from the Kellogg School of Management (Marketing) at Northwestern

University

NEW MANAGEMENT STRATEGY

• The company’s strategic plan was reassessed and revamped significantly in the months that

followed.

• An experienced CFO (Raghu Sampath) was brought in to enhance Avante’s financial systems,

reporting and controls.

• Avante scaled back spending on non-core development and downsized the company by 30%

– Slow procurement and decision-making at enterprise customers left Avante to finance

these trials in a manner that was determined not to be cost effective for Avante’s

shareholders and capital requirements were very large

– Avante wrote down its technology development costs which allowed for a fresh start

with a clean balance sheet.

– Avante streamlined its costs and delivery models by seeking efficiencies in each

expense line of the P&L in a systematic and focused program.

• Beginning in 2011, the company refocused management attention and capital on its core

security business and began focusing on growth opportunities in which the company had a

competitive advantage. This ensured that Avante would pursue profitable security related

business with a focus on recurring revenue.

Section 3

WHERE WE ARE TODAY

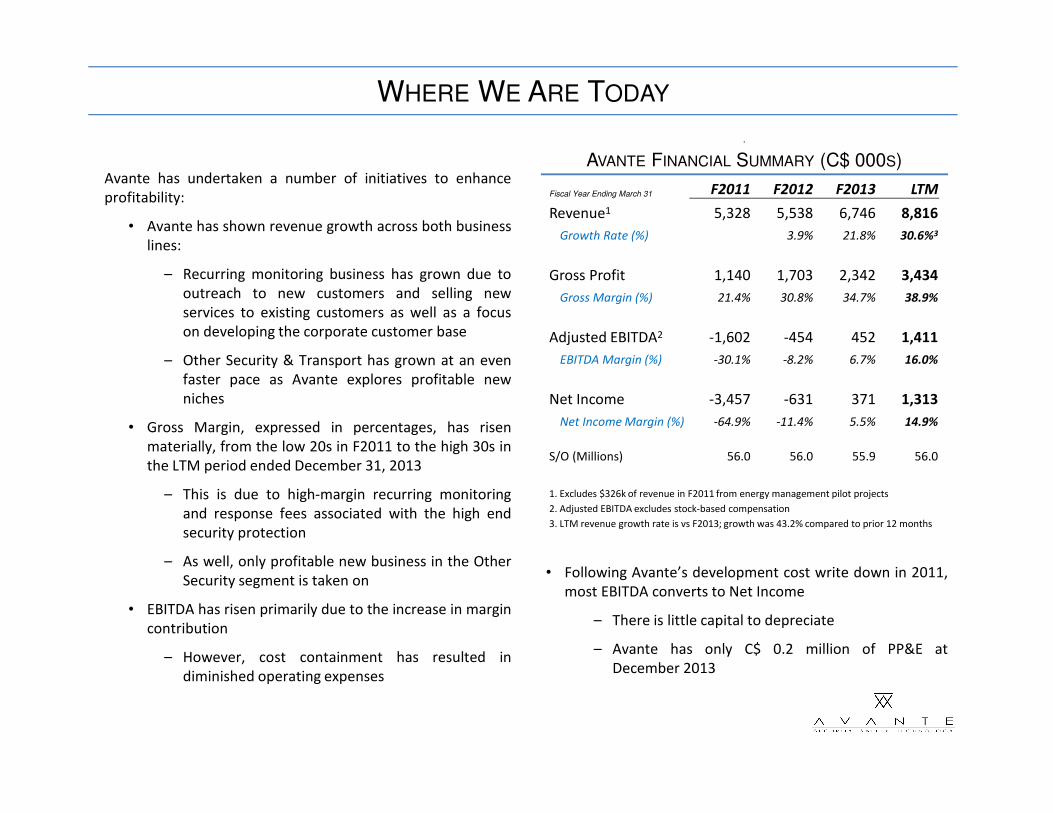

Fiscal Year Ending March 31 F2011 F2012 F2013 LTM

Revenue1 5,328 5,538 6,746 8,816

Growth Rate (%) 3.9% 21.8% 30.6%3

Gross Profit 1,140 1,703 2,342 3,434

Gross Margin (%) 21.4% 30.8% 34.7% 38.9%

Adjusted EBITDA2 -1,602 -454 452 1,411

EBITDA Margin (%) -30.1% -8.2% 6.7% 16.0%

Net Income -3,457 -631 371 1,313

Net Income Margin (%) -64.9% -11.4% 5.5% 14.9%

S/O (Millions) 56.0 56.0 55.9 56.0

1. Excludes $326k of revenue in F2011 from energy management pilot projects

2. Adjusted EBITDA excludes stock-based compensation

3. LTM revenue growth rate is vs F2013; growth was 43.2% compared to prior 12 months

WHERE WE ARE TODAY

3

AVANTE FINANCIAL SUMMARY (C$ 000S)Avante has undertaken a number of initiatives to enhance

profitability:

• Avante has shown revenue growth across both business

lines:

– Recurring monitoring business has grown due to

outreach to new customers and selling new

services to existing customers as well as a focus

on developing the corporate customer base

– Other Security & Transport has grown at an even

faster pace as Avante explores profitable new

niches

• Gross Margin, expressed in percentages, has risen

materially, from the low 20s in F2011 to the high 30s in

the LTM period ended December 31, 2013

– This is due to high-margin recurring monitoring

and response fees associated with the high end

security protection

– As well, only profitable new business in the Other

Security segment is taken on

• EBITDA has risen primarily due to the increase in margin

contribution

– However, cost containment has resulted in

diminished operating expenses

• Following Avante’s development cost write down in 2011,

most EBITDA converts to Net Income

– There is little capital to depreciate

– Avante has only C$ 0.2 million of PP&E at

December 2013

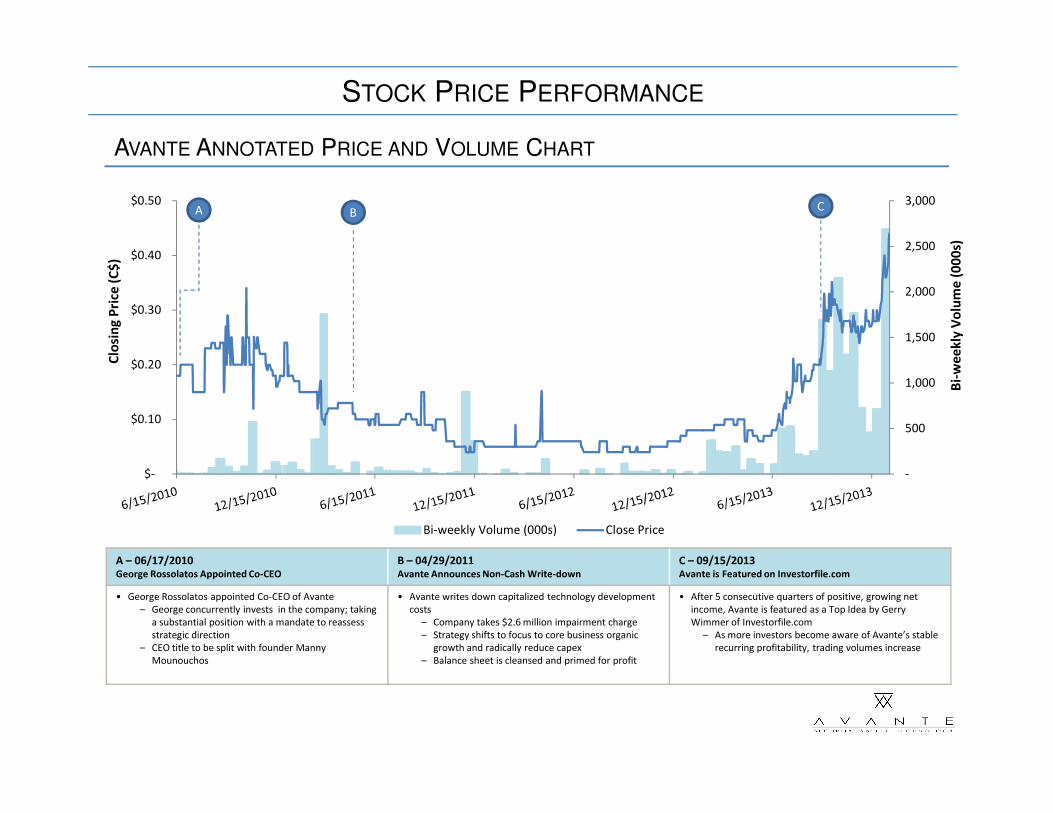

STOCK PRICE PERFORMANCE

AVANTE ANNOTATED PRICE AND VOLUME CHART

A – 06/17/2010George Rossolatos Appointed Co-CEO

B – 04/29/2011Avante Announces Non-Cash Write-down

C – 09/15/2013Avante is Featured on Investorfile.com

• George Rossolatos appointed Co-CEO of Avante

– George concurrently invests in the company; taking

a substantial position with a mandate to reassess

strategic direction

– CEO title to be split with founder Manny

Mounouchos

• Avante writes down capitalized technology development

costs

– Company takes $2.6 million impairment charge

– Strategy shifts to focus to core business organic

growth and radically reduce capex

– Balance sheet is cleansed and primed for profit

• After 5 consecutive quarters of positive, growing net

income, Avante is featured as a Top Idea by Gerry

Wimmer of Investorfile.com

– As more investors become aware of Avante’s stable

recurring profitability, trading volumes increase

A BC

Clo

sin

g P

rice

(C

$)

Bi-

we

ek

ly V

olu

me

(0

00

s)

-

500

1,000

1,500

2,000

2,500

3,000

$-

$0.10

$0.20

$0.30

$0.40

$0.50

Bi-weekly Volume (000s) Close Price

WHERE WE ARE TODAY

• Avante’s balance sheet has been steadily improving over the last 3 years

• As a negative working capital business, Avante’s balance sheet has grown more robust as

the business has grown, without any incremental working capital investment requirement

• Avante is debt-free and does not anticipate the need to borrow other than to potentially

finance acquisitions

• Cash of $1.5 million at 12/31/2013

BALANCE SHEET HIGHLIGHTS

F2012 F2013 F2014 YTDIn C$000s, unless otherwise noted

Basic Shares O/S (Millions) 55.9 55.9 56.0

Total assets 1,712 2,225 3,542

Total liabilities 1,935 2,044 2,286

Total liabilities (excl. deferred revenue) 708 639 797

Deferred revenue 1,227 1,405 1,489

Bank and other debt 0 0 0

Shareholders' equity -223 182 1,256

WHERE WE ARE TODAY

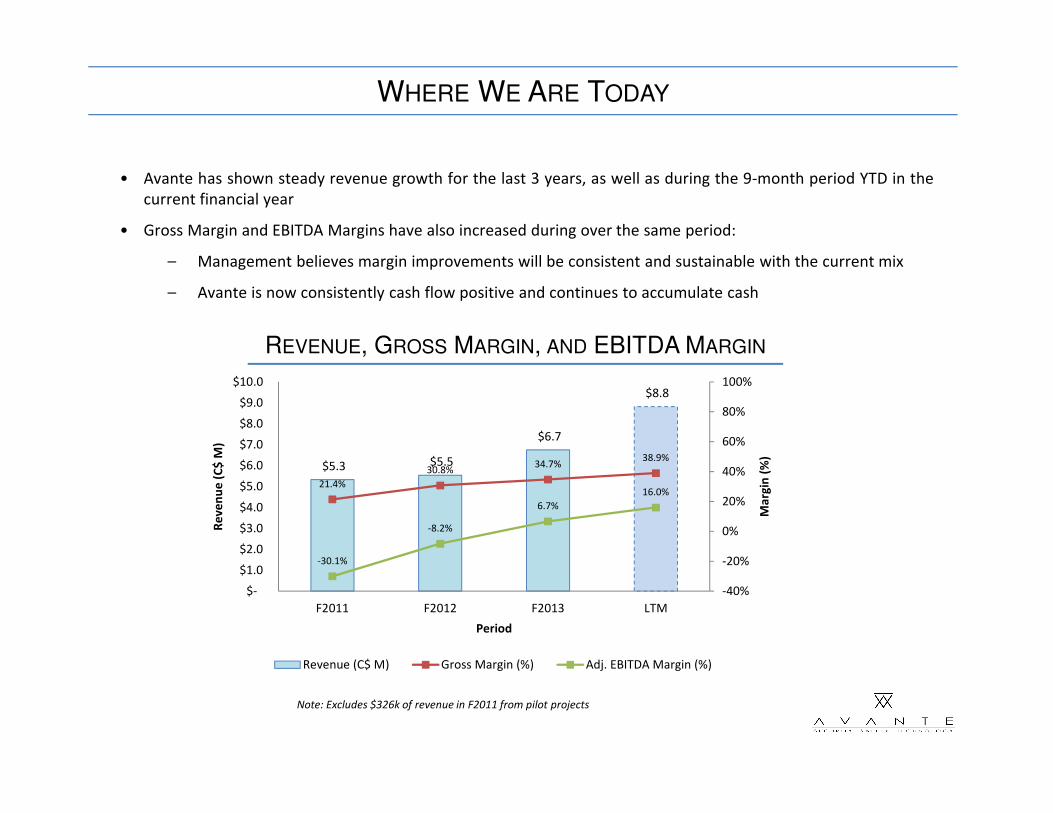

• Avante has shown steady revenue growth for the last 3 years, as well as during the 9-month period YTD in the

current financial year

• Gross Margin and EBITDA Margins have also increased during over the same period:

– Management believes margin improvements will be consistent and sustainable with the current mix

– Avante is now consistently cash flow positive and continues to accumulate cash

REVENUE, GROSS MARGIN, AND EBITDA MARGIN

Note: Excludes $326k of revenue in F2011 from pilot projects

$5.3 $5.5

$6.7

$8.8

21.4%

30.8%34.7%

38.9%

-30.1%

-8.2%

6.7%

16.0%

-40%

-20%

0%

20%

40%

60%

80%

100%

$-

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

$10.0

F2011 F2012 F2013 LTM

Ma

rgin

(%

)

Re

ve

nu

e (

C$

M)

Period

Revenue (C$ M) Gross Margin (%) Adj. EBITDA Margin (%)

WHERE WE ARE TODAY

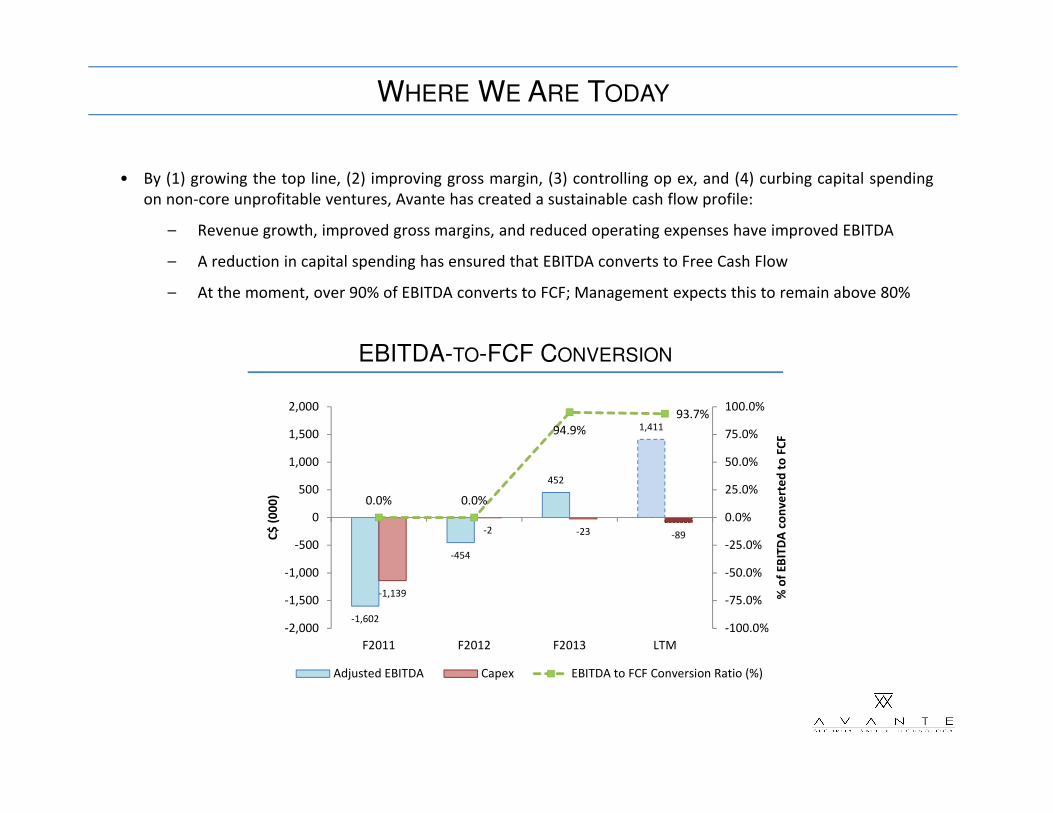

• By (1) growing the top line, (2) improving gross margin, (3) controlling op ex, and (4) curbing capital spending

on non-core unprofitable ventures, Avante has created a sustainable cash flow profile:

– Revenue growth, improved gross margins, and reduced operating expenses have improved EBITDA

– A reduction in capital spending has ensured that EBITDA converts to Free Cash Flow

– At the moment, over 90% of EBITDA converts to FCF; Management expects this to remain above 80%

EBITDA-TO-FCF CONVERSION

-1,602

-454

452

1,411

-1,139

-2 -23 -89

0.0% 0.0%

94.9%

93.7%

-100.0%

-75.0%

-50.0%

-25.0%

0.0%

25.0%

50.0%

75.0%

100.0%

-2,000

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

F2011 F2012 F2013 LTM

% o

f E

BIT

DA

co

nv

ert

ed

to

FC

F

C$

(0

00

)

Adjusted EBITDA Capex EBITDA to FCF Conversion Ratio (%)

WHERE WE ARE TODAY

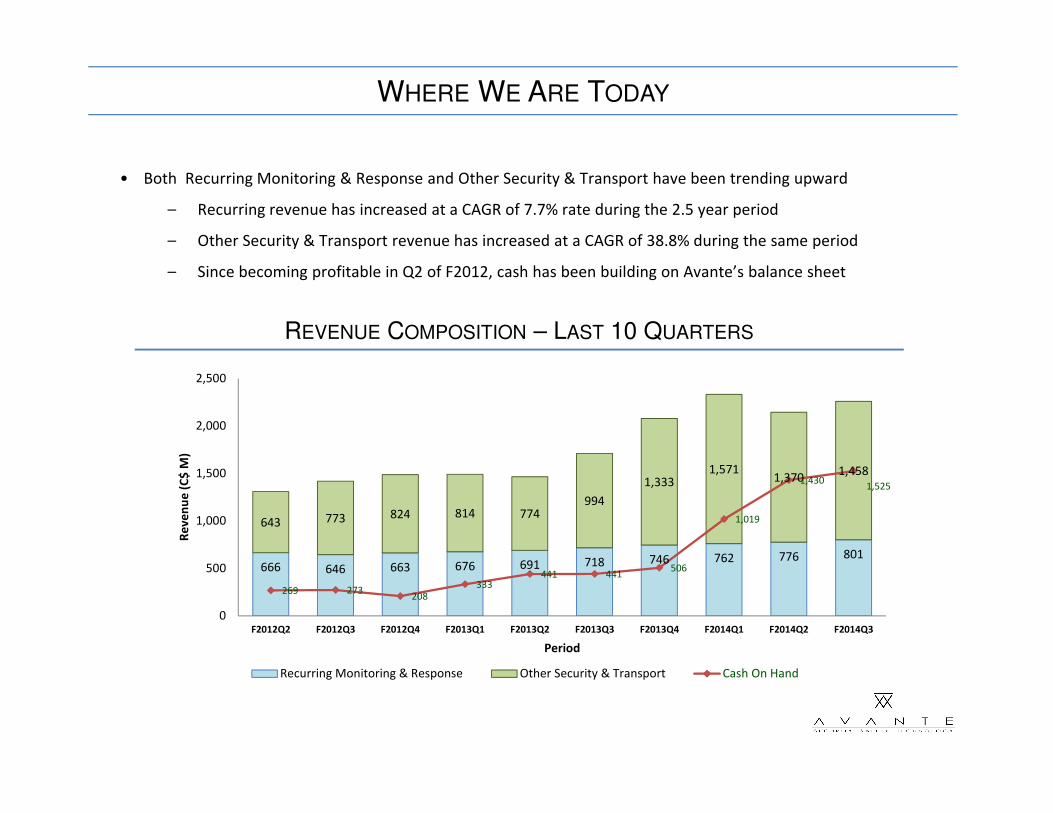

REVENUE COMPOSITION – LAST 10 QUARTERS

• Both Recurring Monitoring & Response and Other Security & Transport have been trending upward

– Recurring revenue has increased at a CAGR of 7.7% rate during the 2.5 year period

– Other Security & Transport revenue has increased at a CAGR of 38.8% during the same period

– Since becoming profitable in Q2 of F2012, cash has been building on Avante’s balance sheet

666 646 663 676 691 718 746 762 776 801

643 773 824 814 774994

1,3331,571

1,3701,458

269 273208

333441 441

506

1,019

1,4301,525

0

500

1,000

1,500

2,000

2,500

F2012Q2 F2012Q3 F2012Q4 F2013Q1 F2013Q2 F2013Q3 F2013Q4 F2014Q1 F2014Q2 F2014Q3

Re

ve

nu

e (

C$

M)

Period

Recurring Monitoring & Response Other Security & Transport Cash On Hand

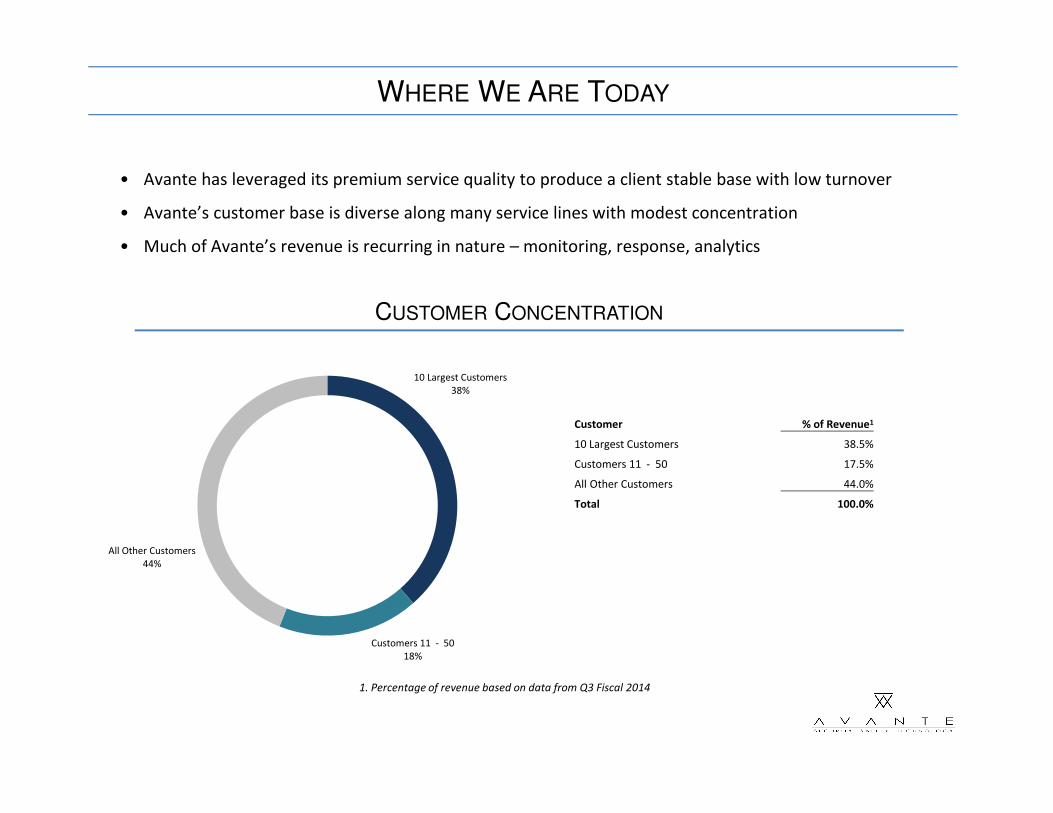

• Avante has leveraged its premium service quality to produce a client stable base with low turnover

• Avante’s customer base is diverse along many service lines with modest concentration

• Much of Avante’s revenue is recurring in nature – monitoring, response, analytics

WHERE WE ARE TODAY

CUSTOMER CONCENTRATION

1. Percentage of revenue based on data from Q3 Fiscal 2014

Customer % of Revenue1

10 Largest Customers 38.5%

Customers 11 - 50 17.5%

All Other Customers 44.0%

Total 100.0%

10 Largest Customers

38%

Customers 11 - 50

18%

All Other Customers

44%

Section 4

WHERE WE’RE GOING: STRATEGY & OUTLOOK

WHERE WE’RE GOING: STRATEGY AND OUTLOOK

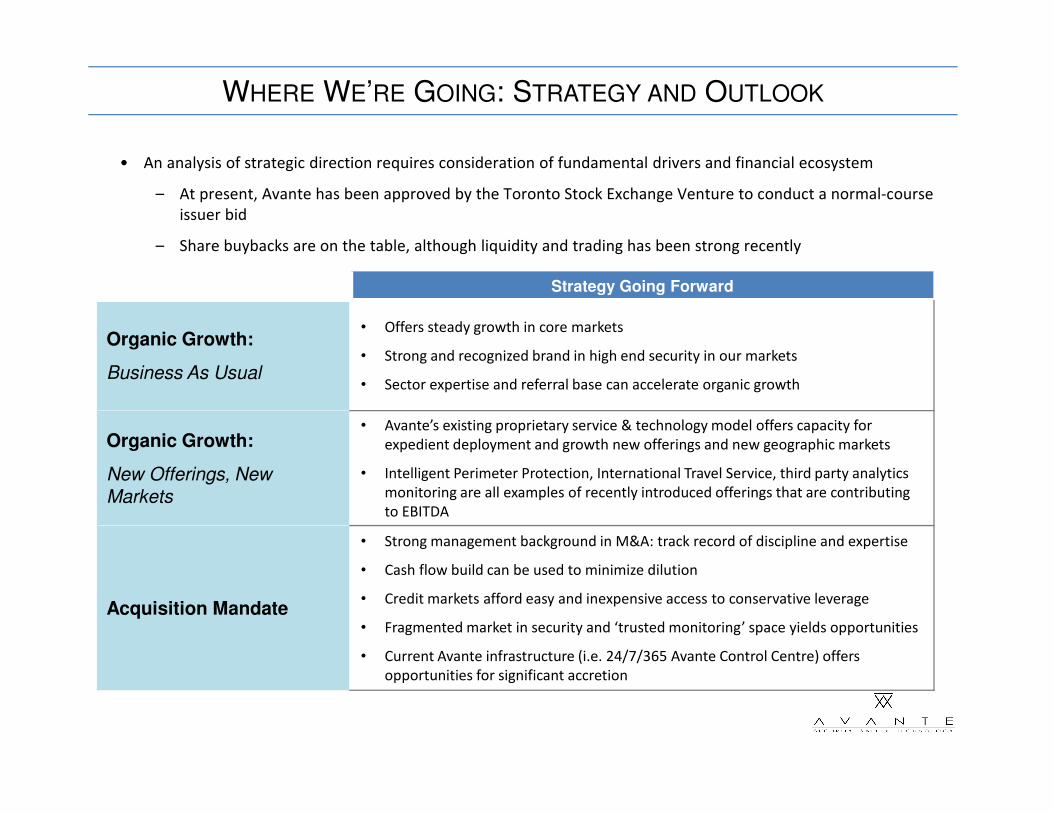

• An analysis of strategic direction requires consideration of fundamental drivers and financial ecosystem

– At present, Avante has been approved by the Toronto Stock Exchange Venture to conduct a normal-course

issuer bid

– Share buybacks are on the table, although liquidity and trading has been strong recently

Strategy Going Forward

Organic Growth:

Business As Usual

• Offers steady growth in core markets

• Strong and recognized brand in high end security in our markets

• Sector expertise and referral base can accelerate organic growth

Organic Growth:

New Offerings, New Markets

• Avante’s existing proprietary service & technology model offers capacity for

expedient deployment and growth new offerings and new geographic markets

• Intelligent Perimeter Protection, International Travel Service, third party analytics

monitoring are all examples of recently introduced offerings that are contributing

to EBITDA

Acquisition Mandate

• Strong management background in M&A: track record of discipline and expertise

• Cash flow build can be used to minimize dilution

• Credit markets afford easy and inexpensive access to conservative leverage

• Fragmented market in security and ‘trusted monitoring’ space yields opportunities

• Current Avante infrastructure (i.e. 24/7/365 Avante Control Centre) offers

opportunities for significant accretion

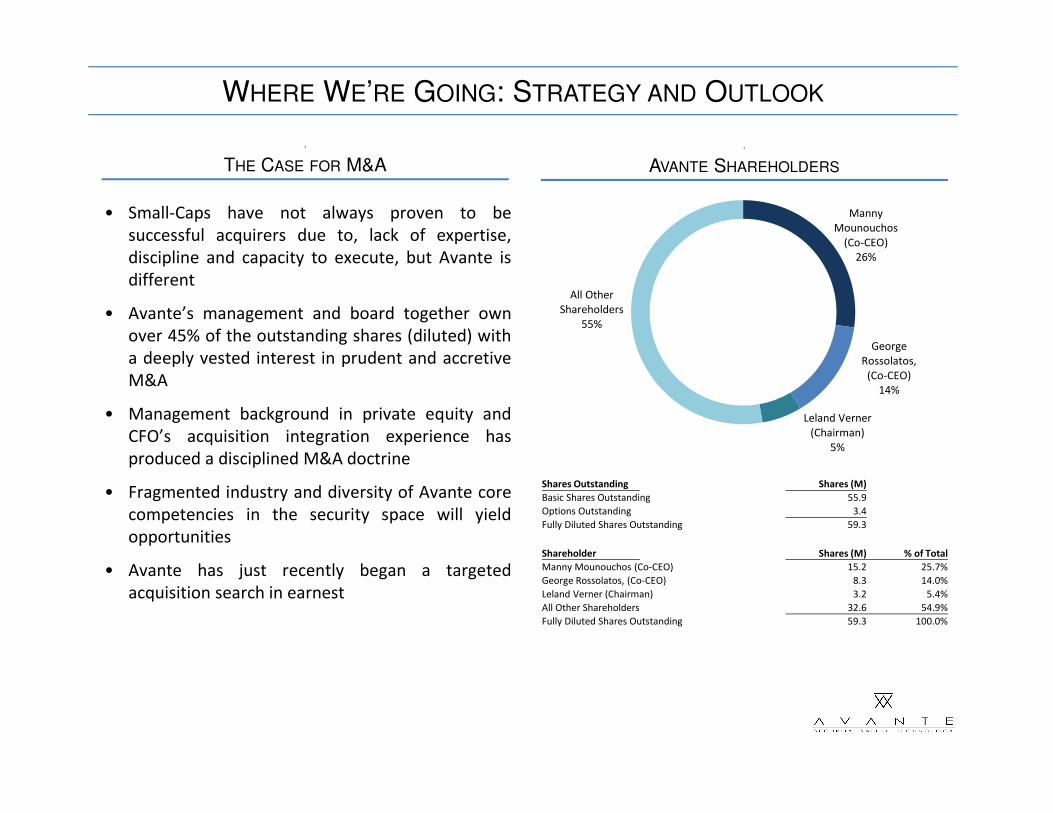

Shares Outstanding Shares (M)

Basic Shares Outstanding 55.9

Options Outstanding 3.4

Fully Diluted Shares Outstanding 59.3

Shareholder Shares (M) % of Total

Manny Mounouchos (Co-CEO) 15.2 25.7%

George Rossolatos, (Co-CEO) 8.3 14.0%

Leland Verner (Chairman) 3.2 5.4%

All Other Shareholders 32.6 54.9%

Fully Diluted Shares Outstanding 59.3 100.0%

WHERE WE’RE GOING: STRATEGY AND OUTLOOK

• Small-Caps have not always proven to be

successful acquirers due to, lack of expertise,

discipline and capacity to execute, but Avante is

different

• Avante’s management and board together own

over 45% of the outstanding shares (diluted) with

a deeply vested interest in prudent and accretive

M&A

• Management background in private equity and

CFO’s acquisition integration experience has

produced a disciplined M&A doctrine

• Fragmented industry and diversity of Avante core

competencies in the security space will yield

opportunities

• Avante has just recently began a targeted

acquisition search in earnest

3

AVANTE SHAREHOLDERS

Manny

Mounouchos

(Co-CEO)

26%

George

Rossolatos,

(Co-CEO)

14%

Leland Verner

(Chairman)

5%

All Other

Shareholders

55%

3

THE CASE FOR M&A

WHERE WE’RE GOING: STRATEGY AND OUTLOOK

• Avante has a number of initiatives which are intended to improve shareholder value:

Liquidity

– Avante has obtained a US Listing – OTC:ALXXF. It is believed that this will:

• Enhance liquidity

• Provide a larger universe of investors who can trade the stock

• Ensure that there is more exposure in the event of a financing

M&A

– Avante is proactively searching for accretive M&A opportunities

• Acquisitions will be considered opportunistically but must align with core

competencies

Enhanced Marketing/Branding Focus

– Given Avante’s growth and the dynamics of the company’s fixed costs, incremental

revenue is increasingly converting to cash flow

• This is an opportune time to focus on a enhanced marketing / branding effort to

increase awareness and potentially drive accelerated organic growth

Appendix A

TRADING COMPARABLES

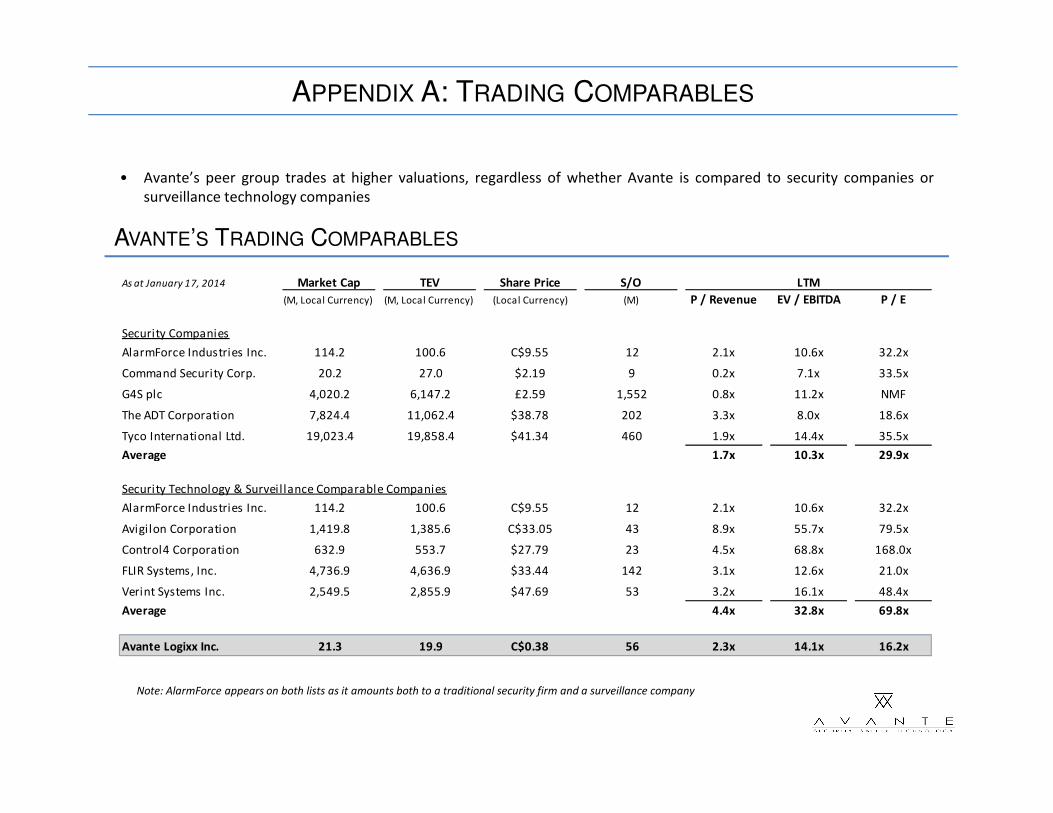

APPENDIX A: TRADING COMPARABLES

• Avante’s peer group trades at higher valuations, regardless of whether Avante is compared to security companies or

surveillance technology companies

AVANTE’S TRADING COMPARABLES

Note: AlarmForce appears on both lists as it amounts both to a traditional security firm and a surveillance company

As at January 17, 2014 Market Cap TEV Share Price S/O LTM

(M, Local Currency) (M, Local Currency) (Local Currency) (M) P / Revenue EV / EBITDA P / E

Security Companies

AlarmForce Industries Inc. 114.2 100.6 C$9.55 12 2.1x 10.6x 32.2x

Command Security Corp. 20.2 27.0 $2.19 9 0.2x 7.1x 33.5x

G4S plc 4,020.2 6,147.2 £2.59 1,552 0.8x 11.2x NMF

The ADT Corporation 7,824.4 11,062.4 $38.78 202 3.3x 8.0x 18.6x

Tyco International Ltd. 19,023.4 19,858.4 $41.34 460 1.9x 14.4x 35.5x

Average 1.7x 10.3x 29.9x

Security Technology & Surveil lance Comparable Companies

AlarmForce Industries Inc. 114.2 100.6 C$9.55 12 2.1x 10.6x 32.2x

Avigilon Corporation 1,419.8 1,385.6 C$33.05 43 8.9x 55.7x 79.5x

Control4 Corporation 632.9 553.7 $27.79 23 4.5x 68.8x 168.0x

FLIR Systems, Inc. 4,736.9 4,636.9 $33.44 142 3.1x 12.6x 21.0x

Verint Systems Inc. 2,549.5 2,855.9 $47.69 53 3.2x 16.1x 48.4x

Average 4.4x 32.8x 69.8x

Avante Logixx Inc. 21.3 19.9 C$0.38 56 2.3x 14.1x 16.2x

AVANTE LOGIXX KEY TAKEAWAYS

• Underfollowed Canadian based (TSX-V XX) security and technology company that’s

recently been turned around and now transitioning from a inward cost reduction

focus to an outward focused growth strategy

• Profitable with strong organic growth story with current and new offerings

• Attractive recurring revenue focused with negative working capital dynamic

• Strong balance sheet with no debt and significant cash accumulating each quarter

• Extremely high cash conversion with little capex requirements

• Fragmented market with acquisition opportunities and expertise to execute

• Favorable valuation comps especially given quarter by quarter trend lines

Investor Presentation

January 2014

George Rossolatos, Co-CEO

Avante Logixx Inc. TSXV: XX OTC:ALXXF www.avantelogixx.com