Embed Size (px)

Citation preview

Why sustainable budgets are important

BRAD KEITHLEYPRESIDENT, KEITHLEY CONSULTING, LLC

ANCHORAGE, ALASKA

BEFORE THE FISCAL POLICY SUBCOMMITTEEHOUSE FINANCE COMMITTEEJANUARY 9, 2014

How investors view Alaska (and citizens should)

“Right now, the state is on a path it can’t sustain. Growing spending and falling revenues are creating a widening fiscal gap. … Reasonable assumptions about potential new revenue sources suggest we do not have enough cash in reserves to avoid a severe fiscal crunch soon after 2023, and with that fiscal crisis will come an economic crash.”

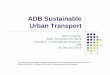

ISER Web Note 14 (2013)$0

$2

$4

$6

$8

$10

$12

$14

$16

2011 2015 2019 2023 2027 2031 2035 2039

Bill

ion

$

Fiscal Year

FY 2015 $6 BILLION AND GROWING:UNRESTRICTED GENERAL FUND

PF EARNINGS/CORPUS

CASH RESERVE

NATURAL GAS REV

NEW OIL REV

DOR OIL REV

NON OIL REV

UGF REVENUES

UGF SPENDING

2

What Alaskans (and investors) face ahead“Two options available to the state, in addition to reducing expenditures, are institution of a broad-based tax, and use of a portion of the earnings of the Permanent Fund. … It is anticipated that both options will be required in the non-OCS case. The value shown above assumes a personal income tax, similar to the tax that was eliminated in 1980, will be phased in between 2022 and 2026.”

Northern Economics and ISER, Potential National-Level Benefits of

Alaska OCS Development (Feb. 2011)

3

Sustainable budgets offer an alternative

“What can the state do to avoid a major fiscal and economic crisis? The answer is to save more and restrict the rate of spending growth. All revenues above the sustainable spending level … including Permanent Fund income, except the share that funds the dividend – would be channeled into savings.”

ISER Web Note 14 (2013)

Over time, earnings from the amounts saved are used to supplement other sources to maintain a sustainable level of overall revenues.

4

Turns a non-renewable resource (oil) into a renewable resource

(financial assets)

Why Alaskans should care

No one disputes that the current spending levels are unsustainable –reductions are inevitable ISER has demonstrated

repeatedly that taxes cannot make up the difference

The question is how best to manage the situation for all Alaskans, regardless of generation The best approach for all generations is to reduce current spending to

sustainable levels, save the difference and use the earnings from the savings to maintain revenue levels as other sources of revenue decline

Otherwise, future generations bear the brunt of both reduced spending and taxes, and still do not achieve equivalent services

5

How do Alaskans respond when faced with the choice

November 11, 2013 debate before the Anchorage Chamber of Commerce on adopting a sustainable budget model (MSY):

Arguing against a sustainable budget model, “Halcro … said some sort of broad-based sales tax is needed …. He also suggested siphoning off a percent of the earnings from the Permanent Fund.” Alaska Dispatch (Nov. 11, 2013)

Vote taken Favor MSY Opposed

Before 35% 35%

After 64% 26%

6

Policy is consistent with Constitutional mandate

Alaska Constitution, Art 8, Sec 4:“Fish, forests, wildlife, grasslands and all other replenishable resources belonging to the State shall be utilized, developed, and maintained on the sustained yield principle, subject to preferences among beneficial uses.”

7

The state’s financial resources similarly can sustain the state over the long term if not “fished out” by

the current generation.

What it requires currently … overall spending reductions

Calculation Year

General Fund Fiscal Burden

Source

MSY ActualSpend

FY2012 $6.2 $7.0 $.8Feb 2011, WebNote 7 & May 2011, WebNote 8March 2012, WebNote 10

FY2013 $6.4 $7.6 $1.2 August 2012, WebNote 13

FY2014 $5.5 $7.1 $1.6 Jan. 2013, WebNote 14

FY2015 $5.0 $5.6+ $.6+Total $23.1 $27.3+ $4.2+

8

Sustainability requires a “top down” look

What is important is the overall spending level Are we saving enough to build a sufficient nest egg to

maintain consistent spending in future years

Allocation within the overall spending level can be handled several ways Sequester (all spending reduced pro rata to fit within the

overall level) Priorities established between and within categories

But formulas and other spending trends need to fit within overall spending levels No programs are sustainable if one breaks the overall

budget

9

Everything needs a look

Education (K-12) spending as an example Overall state GF spending has

risen from $922 million to $1.92 billion (108%) in 10 years

Not sustainable at that level (already nearly 40% of current revenues)

Goal is to find and maintain a sustainable level to provide consistency and avoid a crash

David Teal, Leg Fin Director: Currently, “55 percent of ... available revenue is spent on these three items [education, Medicaid and retirement assistance]. By the time you get to 2022 its 105 percent of available revenue [based on FY2014 projections] being spent on these three items. Well ... you can't spend 105 percent of revenue ...”

10

Lessons from the front lines

Critical to remain aware of the overall goal Each program needs to fit in the overall sustainable

spending “box” Bottom up view of each program in isolation leads to

layering and budget growth

Need to prioritize for the long term Spending on football fields now, instead of saving to build

the nest egg, works to deprive future generations of coaches and teachers (wants v. needs)

Reducing spending doesn’t necessarily mean reducing funding to the core mission Education reductions can come from reduced capital

spending, increased focus on efficiencies; does not necessarily require reductions in overall operating budget

11

Recommendations for this coming legislative session

Cap UGF (operating and capital) spending this year at overall sustainable levels Should be on the downside of the $5.75 billion four year average

Enact HB 136 to provide information to the legislature and public each year on the overall sustainable budget level Enable legislature and public to understand the long term

implications of budgets

Closely examine and modify, if necessary, programs to ensure they are consistent with an overall sustainable budget Requires prioritization overall and within each program Also requires all revenue sources be tapped (e.g., UA system) And, provides a start on the additional $500 million reduction in

UGF spending required next year to offset PERS/TRS

12