Embed Size (px)

DESCRIPTION

Citation preview

M O R G A N S T A N L E Y R E S E A R C H

Morgan Stanley & Co. International plc

O c t o b e r 1 4 , 2 0 1 0

## Consumer Discretionary

## Consumer Staples

## Energy/Utilities

## Financials

## Healthcare

## Industrial/Business Services

## Materials

## Media

## Property

## Retail

## Technology

## Telecommunications

## Transportation

North America

Europe UK strategy – time to think about

inflation … Investors should focus on the longer-term impact of QE and the implications for higher inflation, which should be good news for equities vs. bonds, argues Graham Secker (Page 3)

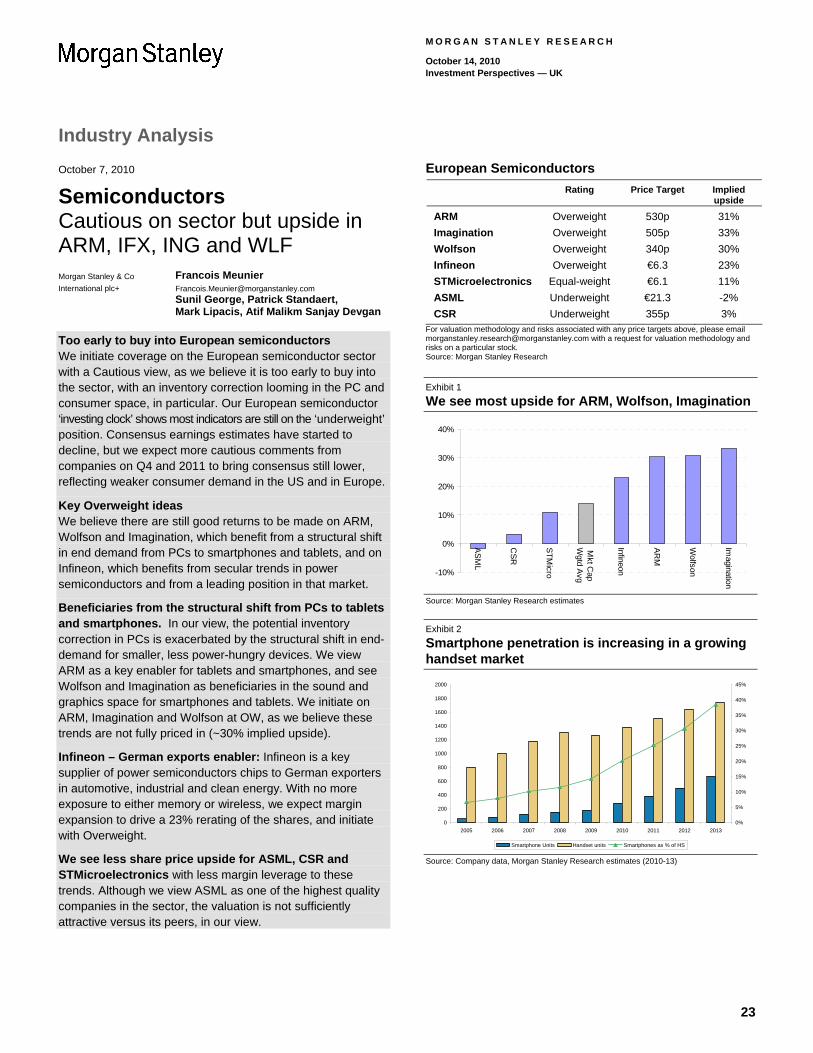

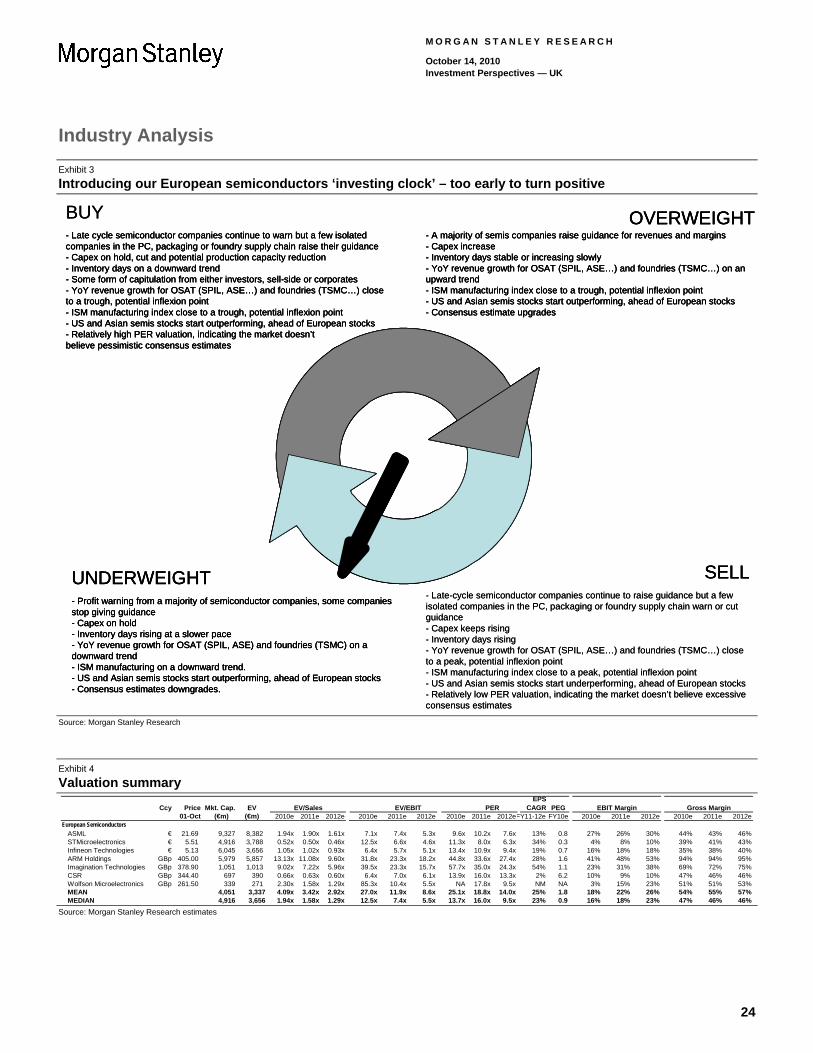

Semiconductors – too early to turn positive: Francois Meunier initiates coverage with a Cautious view, arguing that it is too early to buy into the sector, especially with an inventory correction looming in the PC and consumer space (Page 23).

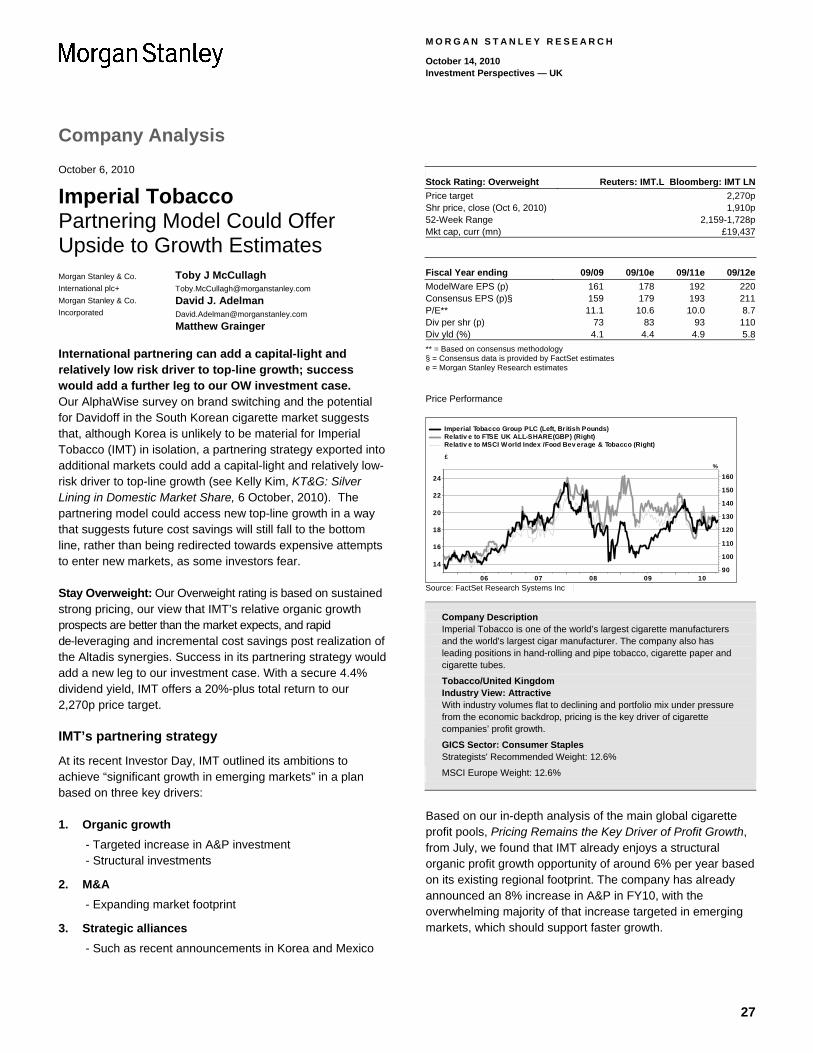

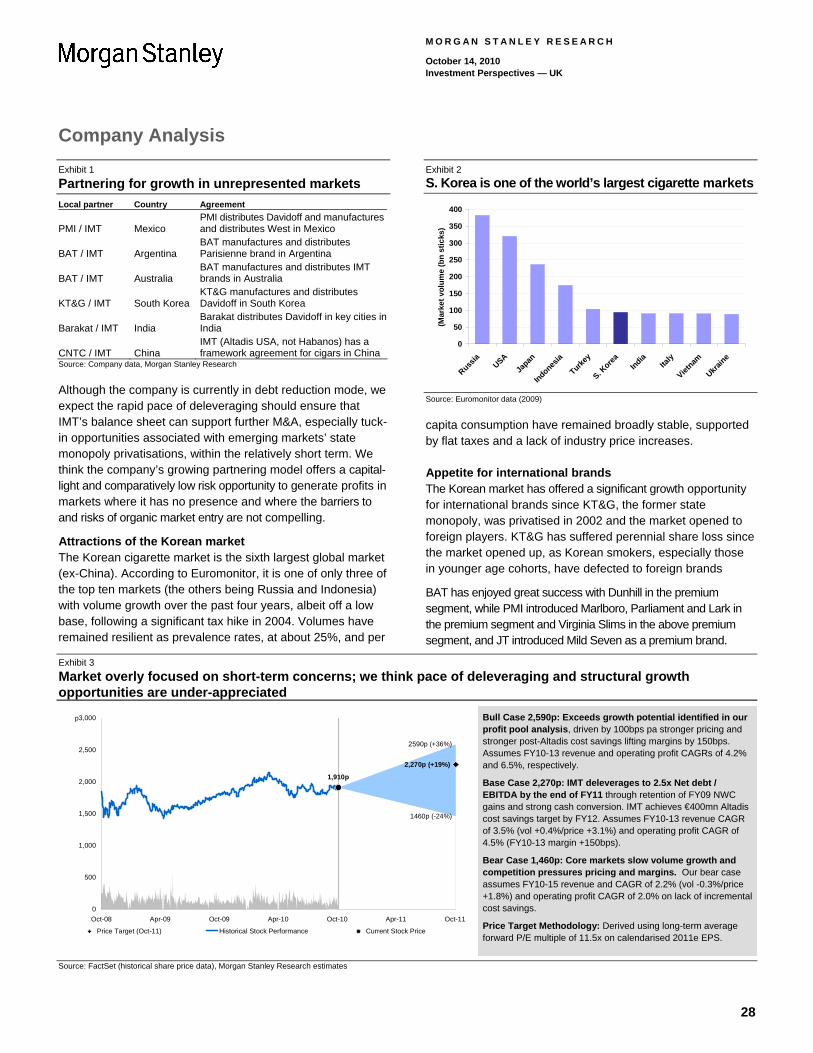

Imperial Tobacco – the merits of partnering: Toby McCullagh argues that international partnering can add a capital-light and relatively low risk driver to Imperial’s top-line growth and a further leg to his Overweight thesis (Page 27).

UK INVESTMENT PERSPECTIVES

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. Customers of Morgan Stanley in the US can receive independent, third-party research on companies covered in Morgan Stanley Equity Research, at no cost to them, where such research is available. Customers can access this independent research at www.morganstanley.com/equityresearch or can call 1-800-624-2063 to request a copy of this research. For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report. + = Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Strategy and Economics UK

3 UK Strategy Time to Think about Inflation… and Equities Outperforming Bonds Graham Secker

7 UK Economics Spending Review: Further Lines of Attack for Critics Melanie Baker, Anthony O’Brien, Cath Sleeman

9 UK Interest Rate Strategy UK Rates: Time to Deliver Anthony O’Brien, Melanie Baker, Cath Sleeman

Global 11 European Credit Strategy

Deleveraging and the Debt/Equity Clock Andrew Sheets, Phanikiran Naraparaju, Carlos Egea, Serena Tang, Jonathan Graber

15 US Economics Roadmap to Sustainable Growth Richard Berner, David Greenlaw

17 US Credit Strategy Tale of Two Markets Rizwan Hussain, Maya Abdurahmanova

19 Commodity Strategy Natural Gas – Fundamentally Oversupplied Hussein Allidina, Stephen Richardson, Tai Liu

Industry & Company Analysis

21 Airlines Short Haul: Long Opportunity Penelope Butcher, Suzanne Todd, Menno Sanderse

23 Initiation Semiconductors Cautious on Sector but Upside in ARM, IFX, ING and WLF Francois Meunier, Sunil George, Patrick Standaert, Mark Lipacis, Atif Malikm Sanjay Devgan

2

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Table of Contents (continued)

(continued…)

27 Imperial Tobacco Partnering Model Could Offer Upside to Growth Estimates Toby McCullagh, David Adelman, Matthew Grainger

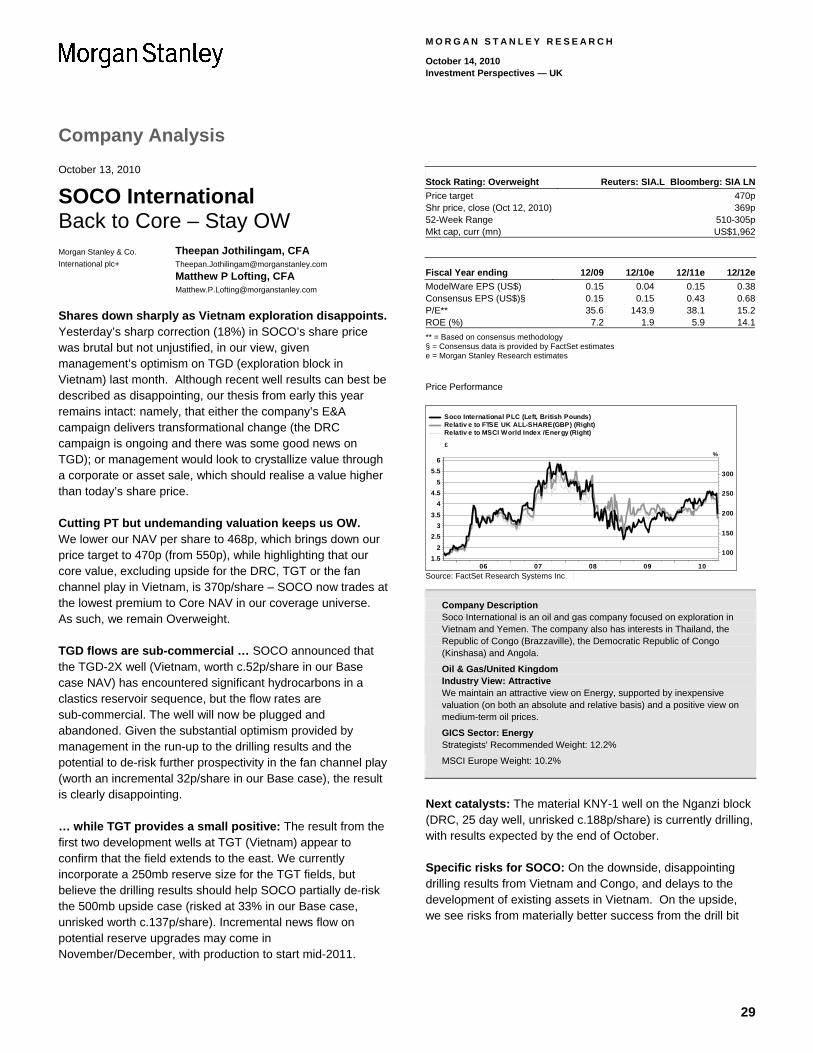

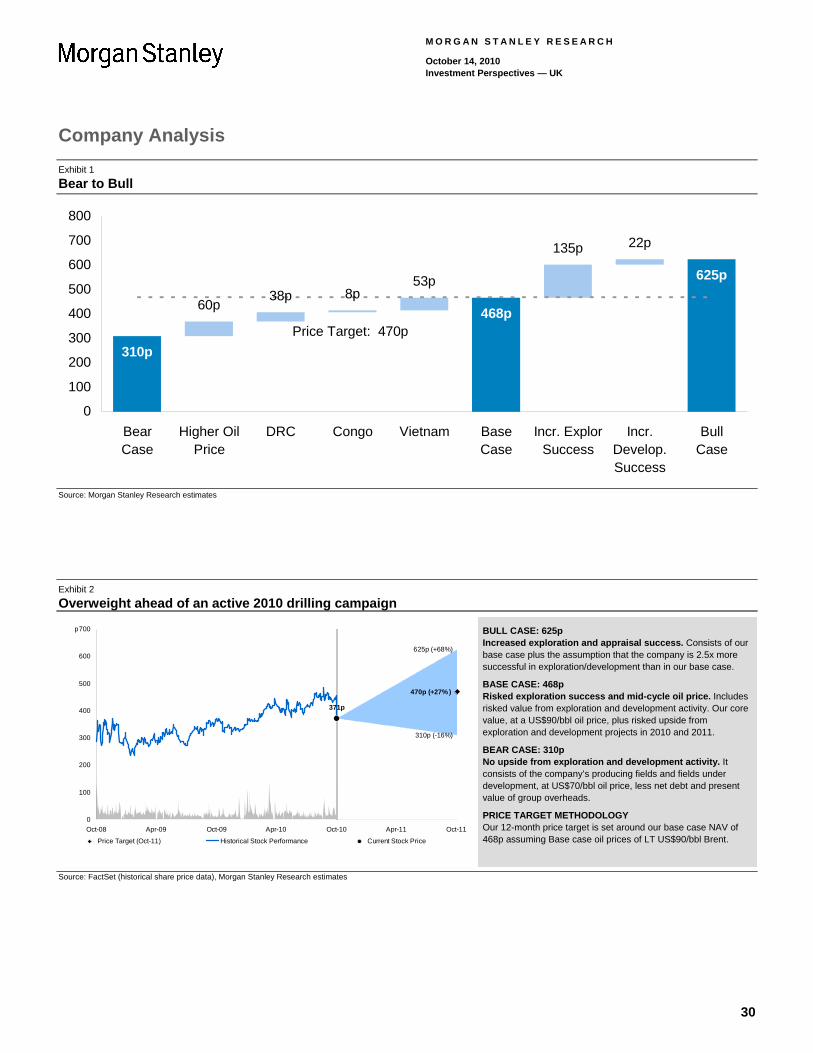

29 SOCO International Back to Core – Stay OW Theepan Jothilingam, Matthew P Lofting

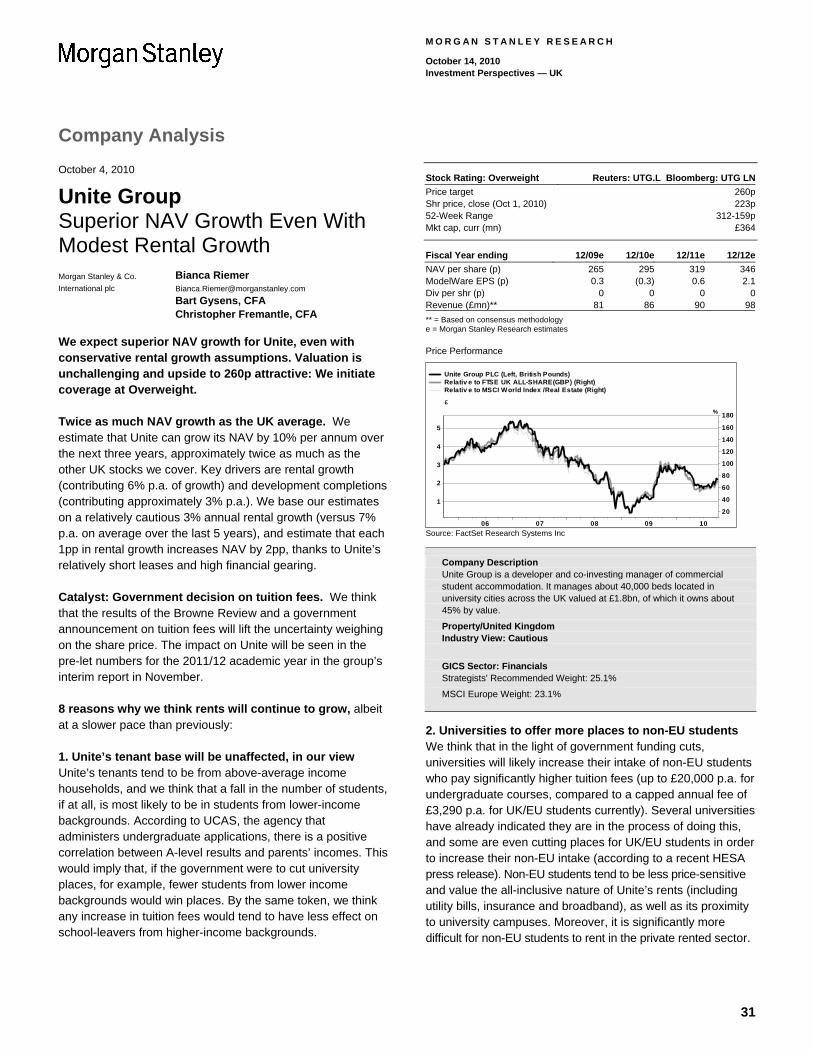

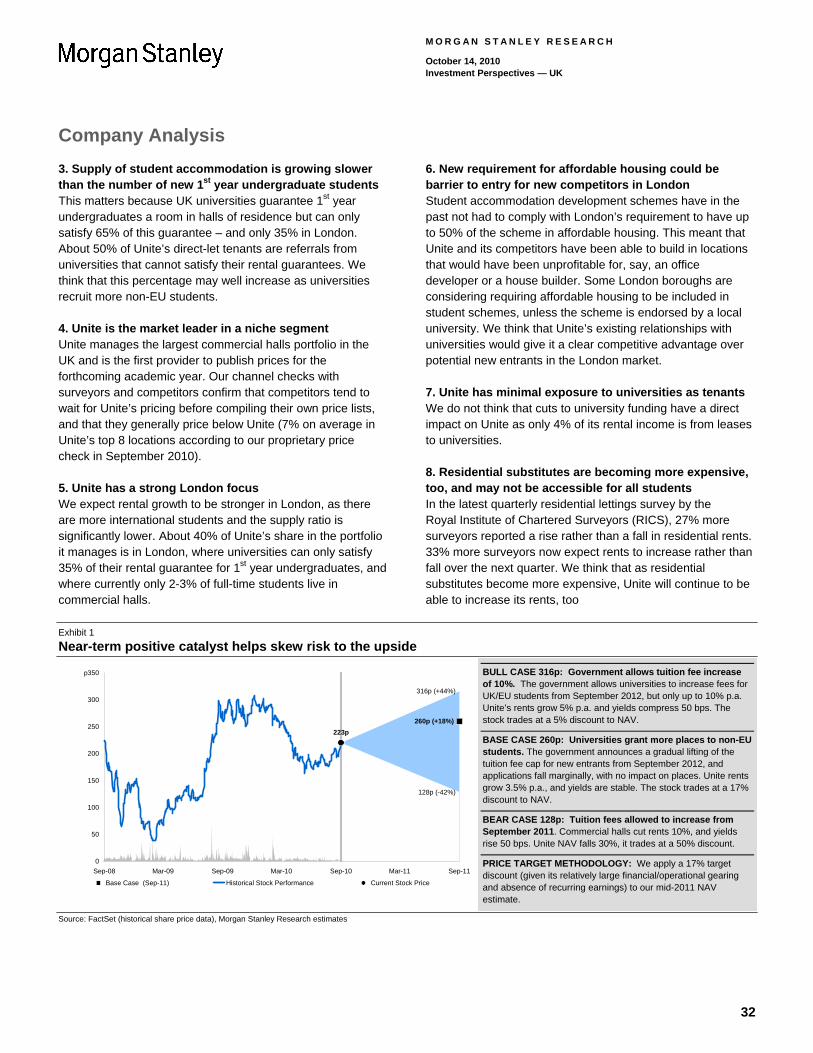

31 Initiation Unite Group Superior NAV Growth Even With Modest Rental Growth Bianca Riemer, Bart Gysens, Christopher Fremantle

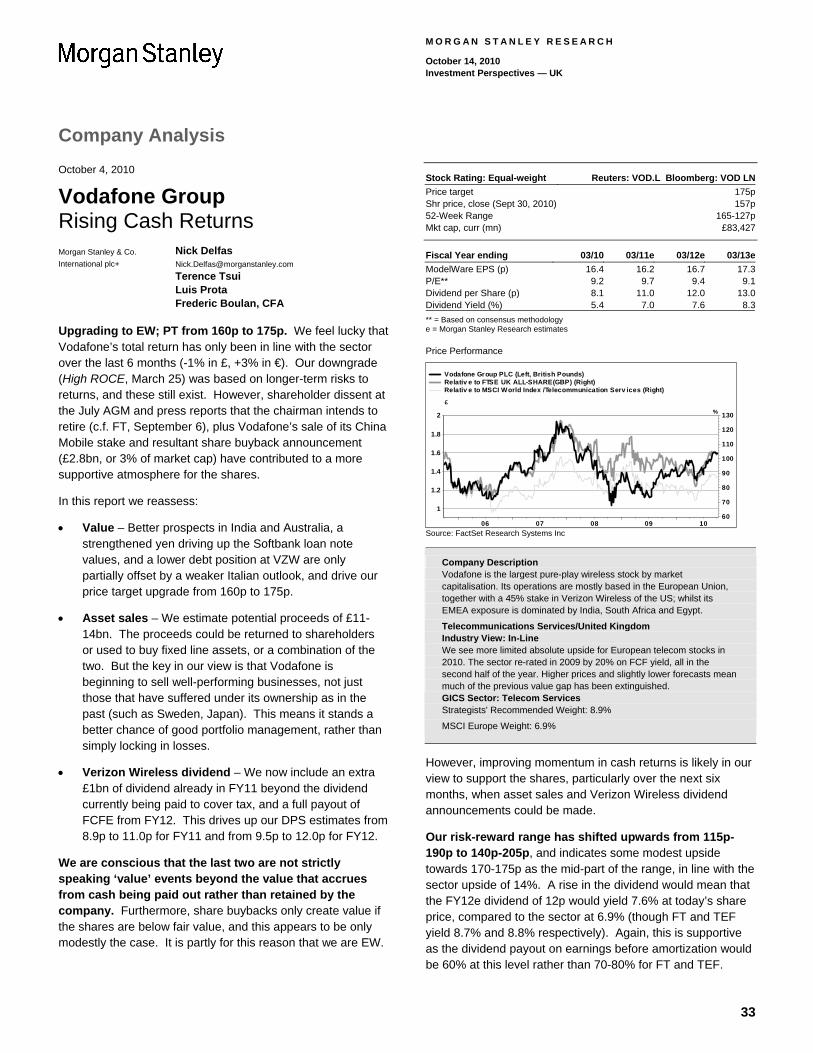

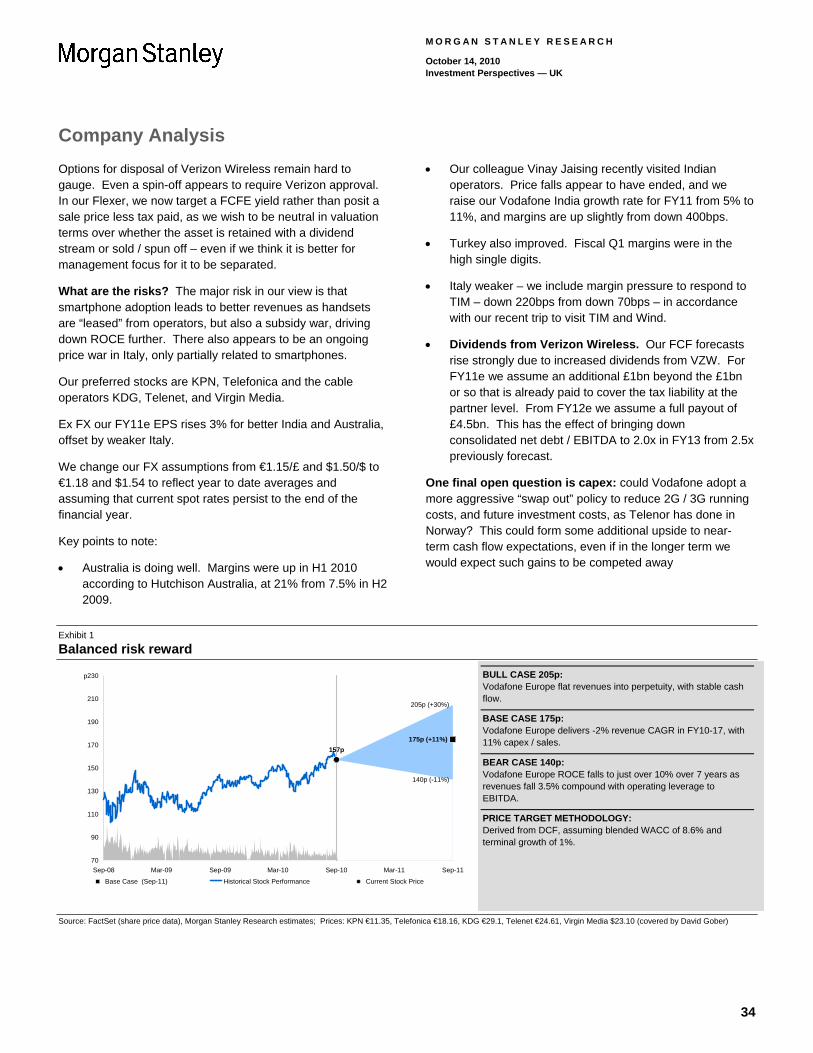

33 Vodafone Group Rising Cash Returns Nick Delfas, Terence Tsui, Luis Prota, Frederic Boulan

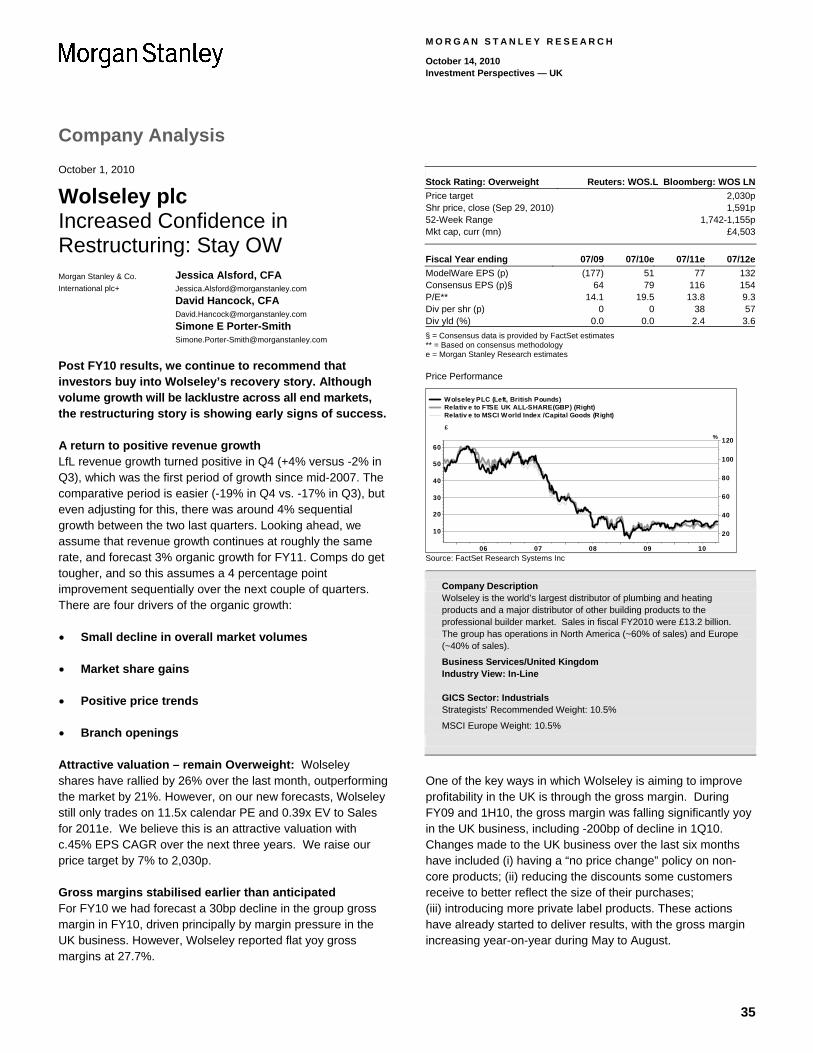

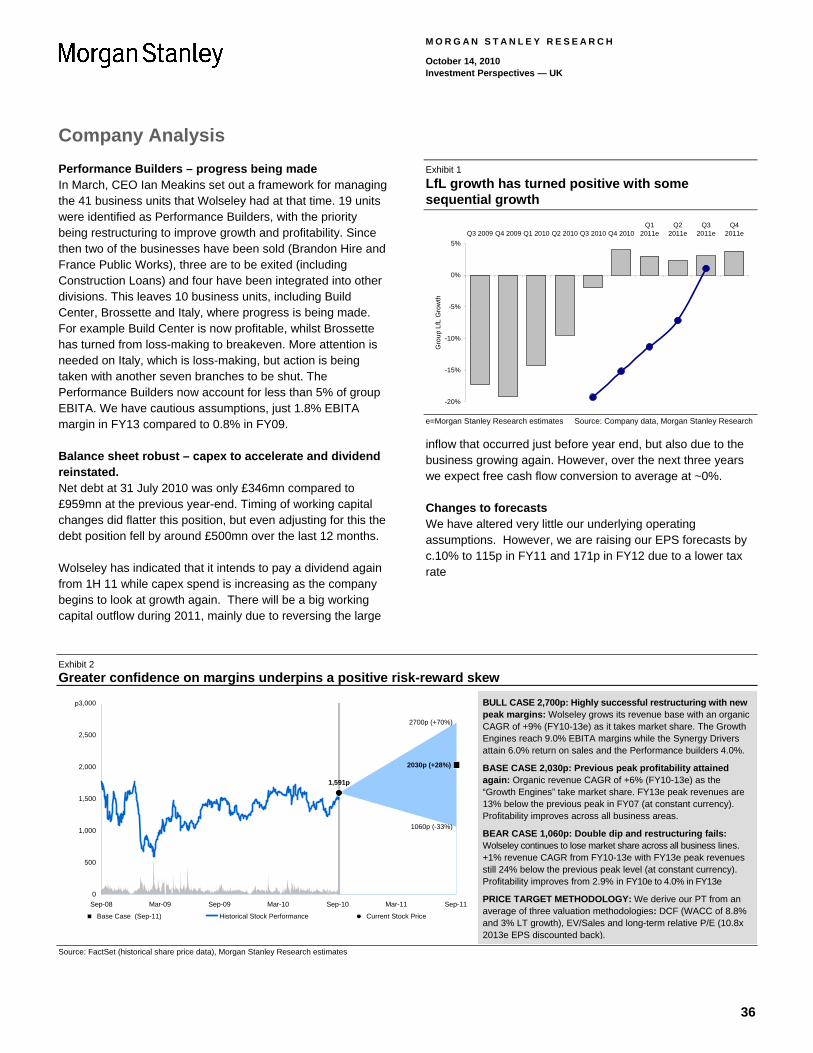

35 Wolseley plc Increased Confidence in Restructuring: Stay OW Jessica Alsford, David Hancock, Simone Porter-Smith

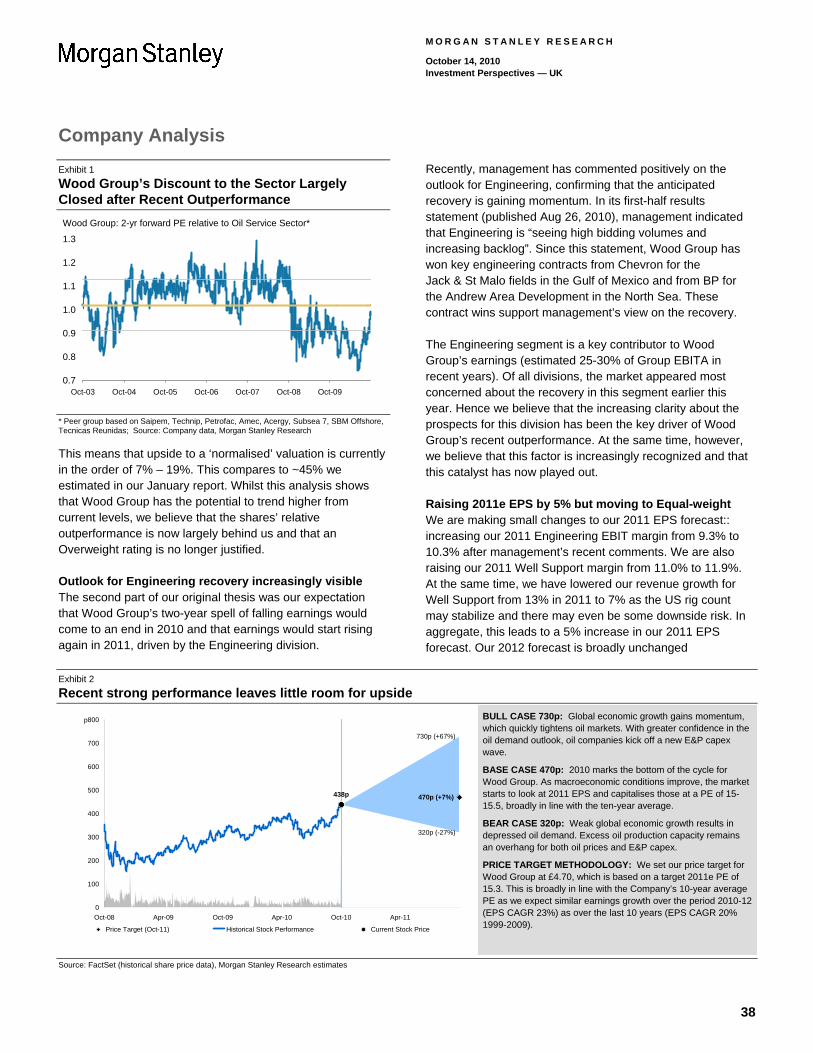

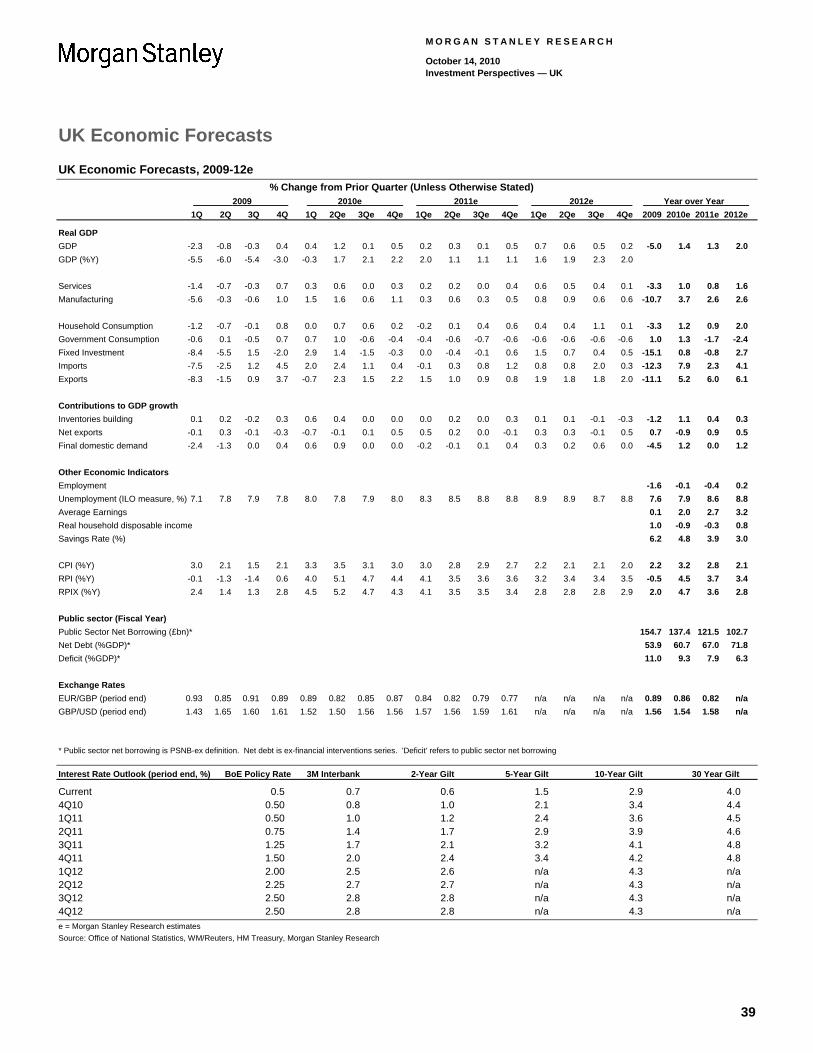

37 Wood Group Value Materialised; Downgrade to Equal-weight Martijn Rats, Robert Pulleyn

Portfolio and Valuations

39 UK Economic Forecasts

40 Indices, Sector and Stock Performance

41 UK Industry Valuations and Forecasts

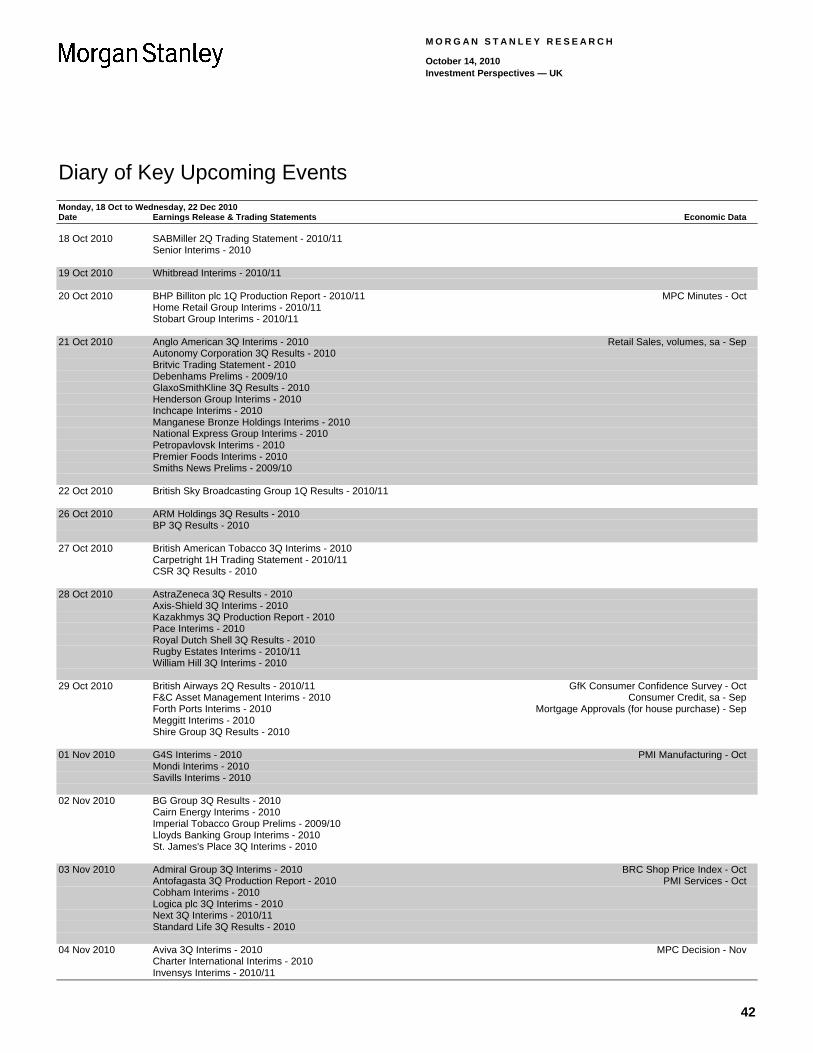

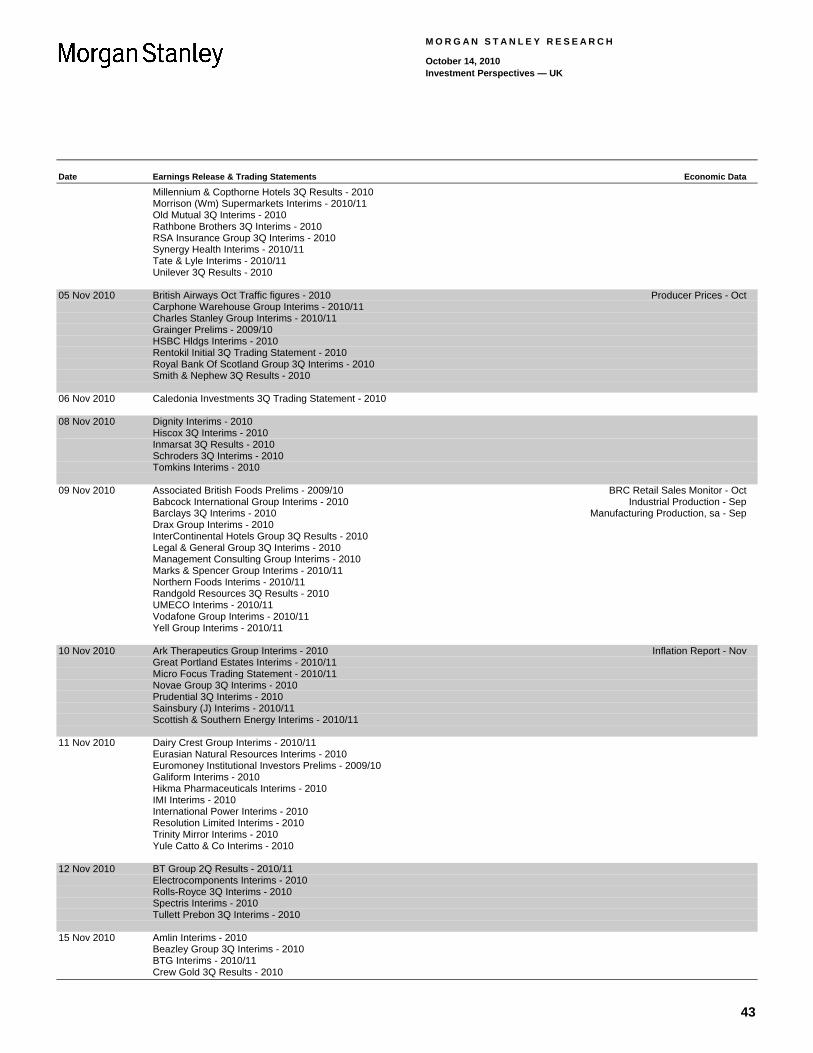

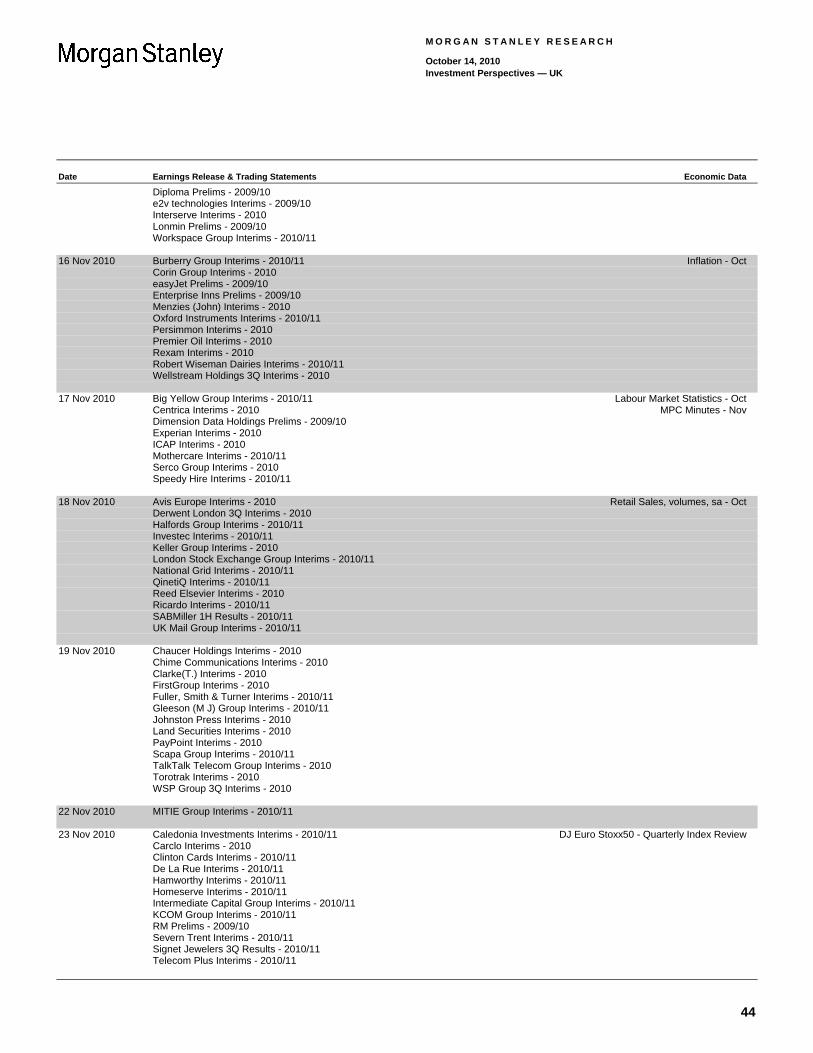

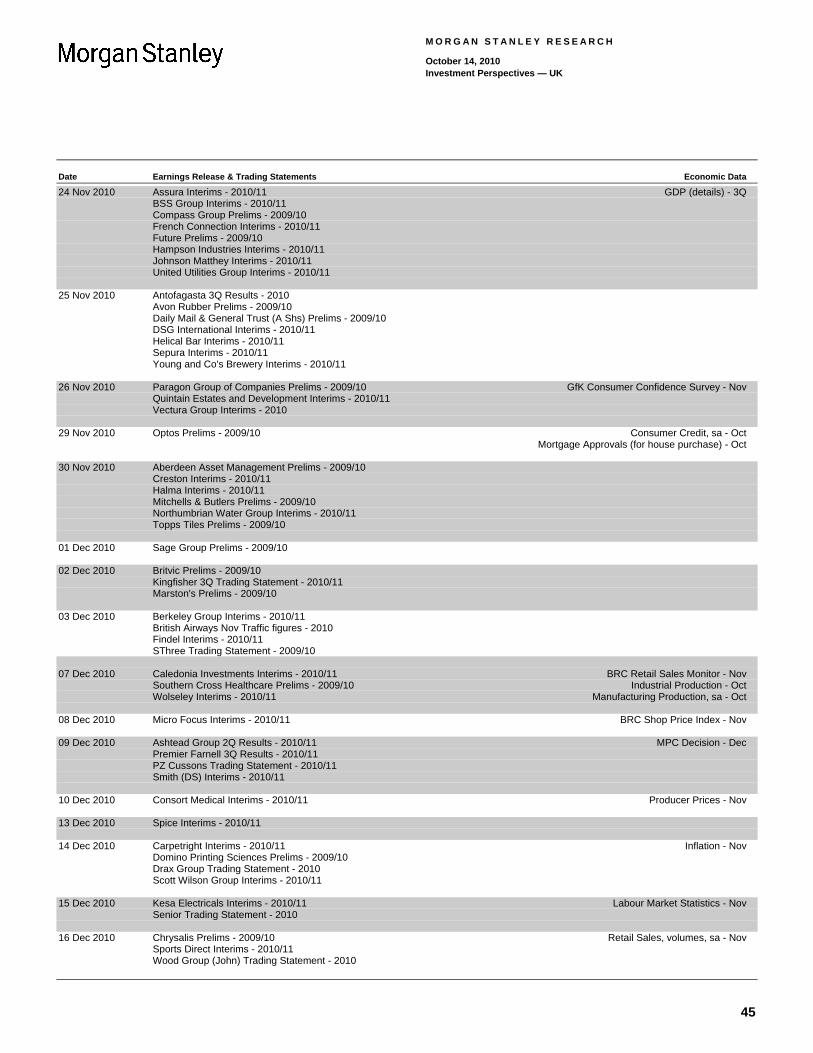

42 Diary of Key Upcoming Events

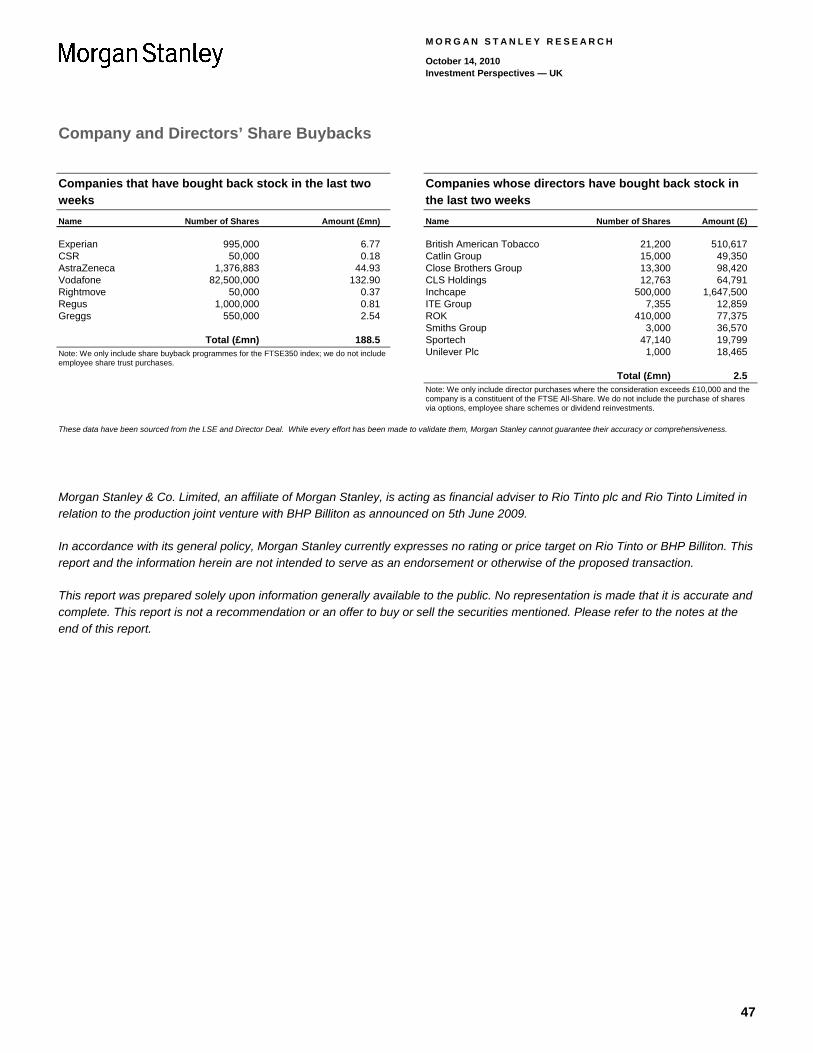

47 Company and Directors’ Share Buybacks

54 UK Stock Coverage List

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

October 12, 2010

UK Strategy Time to Think about Inflation… and Equities Outperforming Bonds Morgan Stanley & Co.

International Limited+

Graham Secker [email protected]

Looking to the longer-term ramifications of QE With pretty much every asset class apart from the US dollar rising in recent weeks, it appears that the market is busy preparing for a renewed bout of quantitative easing (QE) by the Fed. While a period of good performance is always nice, we believe investors should take this opportunity to focus on the more medium to longer-term ramifications of QE (and other forms of monetary stimulus). In this article we focus on the implications for asset allocation and, specifically, the possibility that this new QE programme coincides with a trough in US core inflation.

We expect moderate inflation rather than deflation When considering the link between asset allocation and inflation, the relative performance and valuation of equities versus bonds suggests to us that investors are predominantly concerned about deflationary risks. While we accept that deflation in Western economies is a possible outcome from here, we firmly believe that it is not a probable outcome in the medium term. At the same time, we do not predict a big inflation problem. Instead, we expect inflation to be a bit higher than one would naturally expect for a low rate of economic growth – i.e. a more benign version of stagflation.

Exhibit 1

When faced with a debt problem most countries tend to choose inflation – Japan was the exception

Source: National Statistics, Morgan Stanley Research

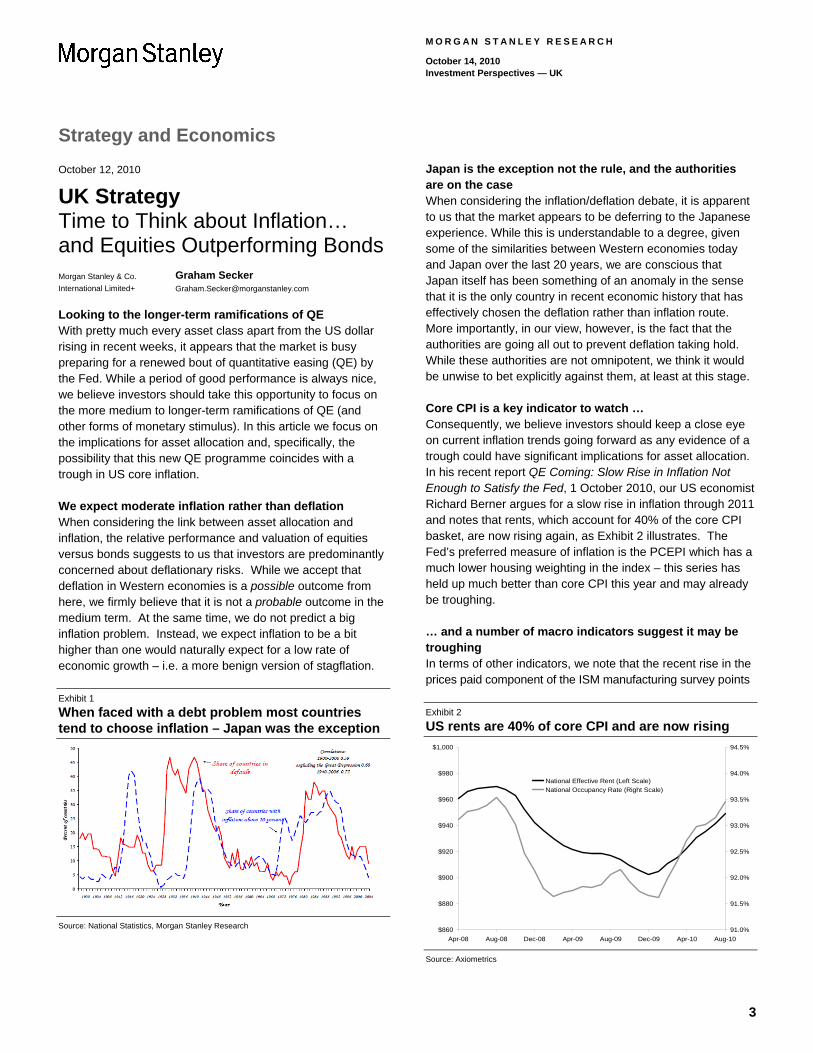

Japan is the exception not the rule, and the authorities are on the case When considering the inflation/deflation debate, it is apparent to us that the market appears to be deferring to the Japanese experience. While this is understandable to a degree, given some of the similarities between Western economies today and Japan over the last 20 years, we are conscious that Japan itself has been something of an anomaly in the sense that it is the only country in recent economic history that has effectively chosen the deflation rather than inflation route. More importantly, in our view, however, is the fact that the authorities are going all out to prevent deflation taking hold. While these authorities are not omnipotent, we think it would be unwise to bet explicitly against them, at least at this stage.

Core CPI is a key indicator to watch … Consequently, we believe investors should keep a close eye on current inflation trends going forward as any evidence of a trough could have significant implications for asset allocation. In his recent report QE Coming: Slow Rise in Inflation Not Enough to Satisfy the Fed, 1 October 2010, our US economist Richard Berner argues for a slow rise in inflation through 2011 and notes that rents, which account for 40% of the core CPI basket, are now rising again, as Exhibit 2 illustrates. The Fed’s preferred measure of inflation is the PCEPI which has a much lower housing weighting in the index – this series has held up much better than core CPI this year and may already be troughing.

… and a number of macro indicators suggest it may be troughing In terms of other indicators, we note that the recent rise in the prices paid component of the ISM manufacturing survey points

Exhibit 2

US rents are 40% of core CPI and are now rising

$860

$880

$900

$920

$940

$960

$980

$1,000

Apr-08 Aug-08 Dec-08 Apr-09 Aug-09 Dec-09 Apr-10 Aug-10

91.0%

91.5%

92.0%

92.5%

93.0%

93.5%

94.0%

94.5%

National Effective Rent (Left Scale)National Occupancy Rate (Right Scale)

Source: Axiometrics

3

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

to upside risks to CPI, as does the rise in capacity utilisation that is now underway in the US (and Germany and the UK too). Finally, we note that US yield curves remain steep at both the 10-2yr level and the 30-10yr level – arguably, the former suggests the growth outlook is okay while the latter, which is at a 30-year high, suggests inflation will return.

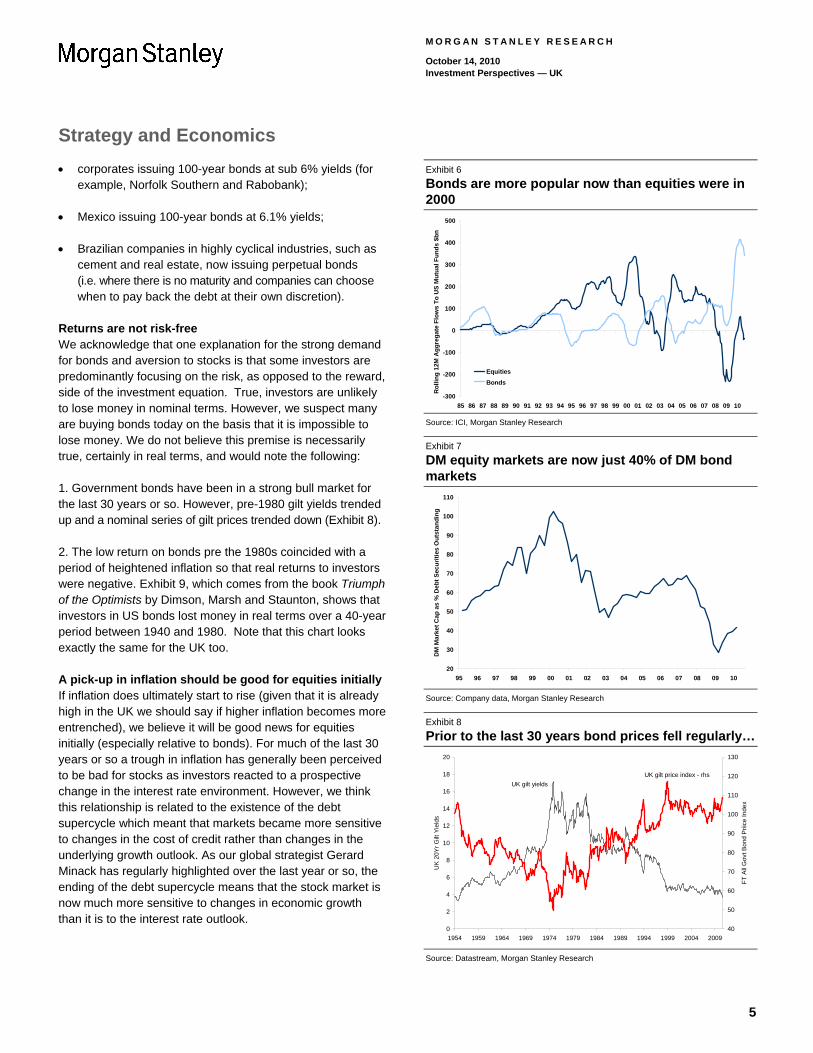

A trough in inflation would be an important signal for asset allocation If we do see the start of an uptrend in global inflation pressures over the next six months, this could have a profound impact on asset allocation. The huge amount of liquidity sloshing around the global financial system right now is predominantly sitting in bond funds. However, while this is understandable in a world worried about deflation, we think such a position is much harder to justify if investors start worrying about rising, not falling, inflation. As Exhibit 7 shows, developed equity markets have shrunk significantly in size compared to developed bond markets over the last decade or so. Consequently, a moderate outflow from bonds to equities is more meaningful now than it would have been 10 years ago.

When we consider asset allocation in this regard it is important to note that there is, in our opinion, a significant divergence in view between equity and fixed income investors at this time, with the latter significantly more bearish on growth and inflation than the former. Assuming this is indeed true, then it suggests that the investment implications of any uptick in inflation is more profound for bonds than stocks. In particular, we would highlight the traditional link between US core inflation and US bond yields, as highlighted in Exhibit 5 – yields always back up around a trough in core inflation.

Bonds are more popular now than equities were in 2000 In addition to bond investors’ bearish macro view as a starting point, we also note that bonds are far more popular as an asset class than equities are. The best chart we have come across to illustrate this point is Exhibit 6 – simply put, bonds are more popular today than equities were at the peak of the TMT bubble in 2000.

In addition, the market’s hunger for all things fixed income is reflected in recent bond news, such as:

corporates borrowing at record low interest rates (e.g. IBM issuing bonds at 1%, Microsoft borrowing at sub-1%);

Exhibit 3

The Fed’s preferred measure of inflation (PCEPI) is showing signs of troughing

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09

US

Infl

atio

n

Core CPI

PCEPI

Source: Haver, Morgan Stanley Research

Exhibit 4

Break-even inflation expectations are rising …

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

3.1

3.3

Oct 09 Nov 09 Dec 09 Jan 10 Feb 10 Mar 10 Apr 10 May 10 Jun 10 Jul 10 Aug 10 Sep 10 Oct 10

10-y

r B

reak

even

infl

atio

n e

xpec

tati

on

s

UK

US

Source: Bloomberg, Morgan Stanley Research

Exhibit 5

… and a trough in core CPI often coincides with a trough in treasury yields

0

2

4

6

8

10

12

14

16

Jan-80 Jan-83 Jan-86 Jan-89 Jan-92 Jan-95 Jan-98 Jan-01 Jan-04 Jan-07 Jan-10

(%) US 10-yr treasury yield

US core CPI

Source: Datastream, Morgan Stanley Research

4

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

corporates issuing 100-year bonds at sub 6% yields (for example, Norfolk Southern and Rabobank);

Mexico issuing 100-year bonds at 6.1% yields;

Brazilian companies in highly cyclical industries, such as cement and real estate, now issuing perpetual bonds (i.e. where there is no maturity and companies can choose when to pay back the debt at their own discretion).

Returns are not risk-free We acknowledge that one explanation for the strong demand for bonds and aversion to stocks is that some investors are predominantly focusing on the risk, as opposed to the reward, side of the investment equation. True, investors are unlikely to lose money in nominal terms. However, we suspect many are buying bonds today on the basis that it is impossible to lose money. We do not believe this premise is necessarily true, certainly in real terms, and would note the following:

1. Government bonds have been in a strong bull market for the last 30 years or so. However, pre-1980 gilt yields trended up and a nominal series of gilt prices trended down (Exhibit 8).

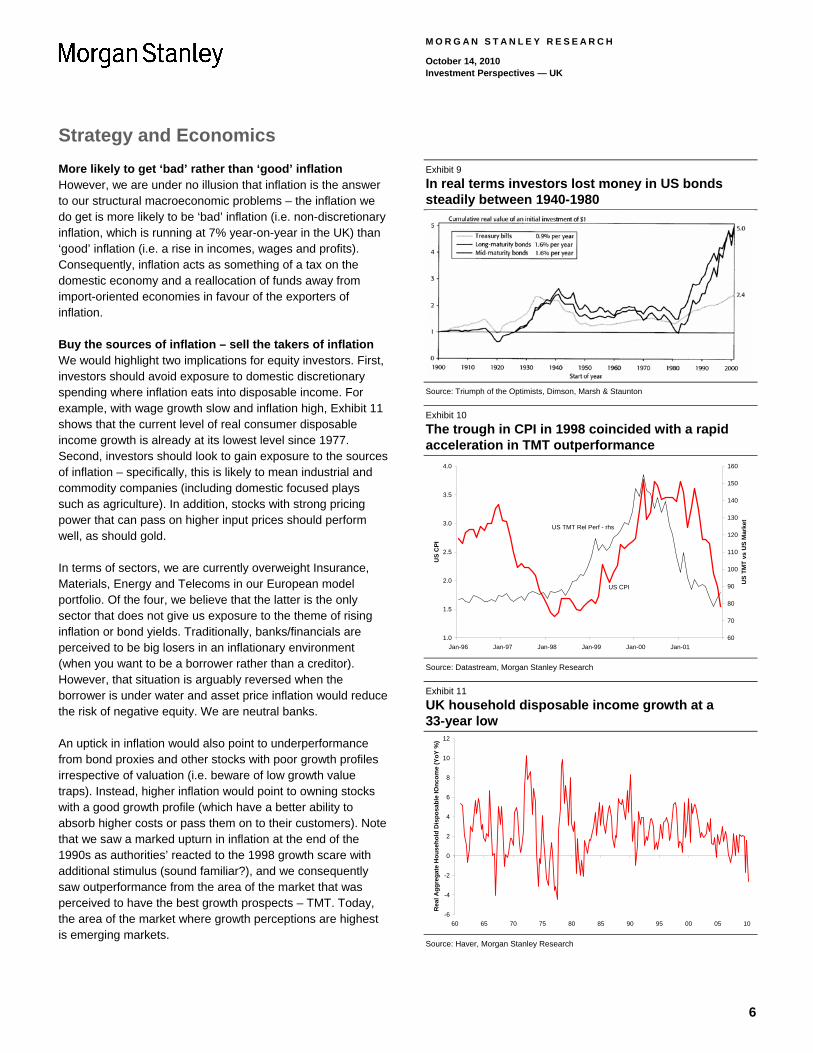

2. The low return on bonds pre the 1980s coincided with a period of heightened inflation so that real returns to investors were negative. Exhibit 9, which comes from the book Triumph of the Optimists by Dimson, Marsh and Staunton, shows that investors in US bonds lost money in real terms over a 40-year period between 1940 and 1980. Note that this chart looks exactly the same for the UK too.

A pick-up in inflation should be good for equities initially If inflation does ultimately start to rise (given that it is already high in the UK we should say if higher inflation becomes more entrenched), we believe it will be good news for equities initially (especially relative to bonds). For much of the last 30 years or so a trough in inflation has generally been perceived to be bad for stocks as investors reacted to a prospective change in the interest rate environment. However, we think this relationship is related to the existence of the debt supercycle which meant that markets became more sensitive to changes in the cost of credit rather than changes in the underlying growth outlook. As our global strategist Gerard Minack has regularly highlighted over the last year or so, the ending of the debt supercycle means that the stock market is now much more sensitive to changes in economic growth than it is to the interest rate outlook.

Exhibit 6

Bonds are more popular now than equities were in 2000

-300

-200

-100

0

100

200

300

400

500

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Ro

llin

g 1

2M A

gg

reg

ate

Flo

ws

To

US

Mu

tual

Fu

nd

s $b

n

.

Equities

Bonds

Source: ICI, Morgan Stanley Research

Exhibit 7

DM equity markets are now just 40% of DM bond markets

20

30

40

50

60

70

80

90

100

110

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

DM

Mar

ket

Cap

as

% D

ebt

Sec

uri

ties

Ou

tsta

nd

ing

Source: Company data, Morgan Stanley Research

Exhibit 8

Prior to the last 30 years bond prices fell regularly…

0

2

4

6

8

10

12

14

16

18

20

1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009

UK

20Y

r G

ilt Y

ield

s

40

50

60

70

80

90

100

110

120

130

FT

All

Gov

t B

ond

Pri

ice

Ind

ex

UK gilt price index - rhs

UK gilt yields

Source: Datastream, Morgan Stanley Research

5

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

More likely to get ‘bad’ rather than ‘good’ inflation However, we are under no illusion that inflation is the answer to our structural macroeconomic problems – the inflation we do get is more likely to be ‘bad’ inflation (i.e. non-discretionary inflation, which is running at 7% year-on-year in the UK) than ‘good’ inflation (i.e. a rise in incomes, wages and profits). Consequently, inflation acts as something of a tax on the domestic economy and a reallocation of funds away from import-oriented economies in favour of the exporters of inflation.

Buy the sources of inflation – sell the takers of inflation We would highlight two implications for equity investors. First, investors should avoid exposure to domestic discretionary spending where inflation eats into disposable income. For example, with wage growth slow and inflation high, Exhibit 11 shows that the current level of real consumer disposable income growth is already at its lowest level since 1977. Second, investors should look to gain exposure to the sources of inflation – specifically, this is likely to mean industrial and commodity companies (including domestic focused plays such as agriculture). In addition, stocks with strong pricing power that can pass on higher input prices should perform well, as should gold.

In terms of sectors, we are currently overweight Insurance, Materials, Energy and Telecoms in our European model portfolio. Of the four, we believe that the latter is the only sector that does not give us exposure to the theme of rising inflation or bond yields. Traditionally, banks/financials are perceived to be big losers in an inflationary environment (when you want to be a borrower rather than a creditor). However, that situation is arguably reversed when the borrower is under water and asset price inflation would reduce the risk of negative equity. We are neutral banks.

An uptick in inflation would also point to underperformance from bond proxies and other stocks with poor growth profiles irrespective of valuation (i.e. beware of low growth value traps). Instead, higher inflation would point to owning stocks with a good growth profile (which have a better ability to absorb higher costs or pass them on to their customers). Note that we saw a marked upturn in inflation at the end of the 1990s as authorities’ reacted to the 1998 growth scare with additional stimulus (sound familiar?), and we consequently saw outperformance from the area of the market that was perceived to have the best growth prospects – TMT. Today, the area of the market where growth perceptions are highest is emerging markets.

Exhibit 9

In real terms investors lost money in US bonds steadily between 1940-1980

Source: Triumph of the Optimists, Dimson, Marsh & Staunton

Exhibit 10

The trough in CPI in 1998 coincided with a rapid acceleration in TMT outperformance

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-96 Jan-97 Jan-98 Jan-99 Jan-00 Jan-01

US

CP

I

60

70

80

90

100

110

120

130

140

150

160

US

TM

T v

s U

S M

arke

t

US CPI

US TMT Rel Perf - rhs

Source: Datastream, Morgan Stanley Research

Exhibit 11

UK household disposable income growth at a 33-year low

-6

-4

-2

0

2

4

6

8

10

12

60 65 70 75 80 85 90 95 00 05 10

Rea

l Ag

gre

gat

e H

ou

seh

old

Dis

po

sab

le I

On

com

e (Y

oY

%)

Source: Haver, Morgan Stanley Research

6

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

October 8, 2010

UK Economics Spending Review: Further Lines of Attack for Critics Morgan Stanley & Co.

International plc+

Melanie Baker, CFA [email protected]

Anthony S O'Brien, Cath Sleeman

In the view of our Interest Rate Strategy Team, as long as the market perceives that the government is sticking to its plans, the October 20 Spending Review should not be a negative risk event for Gilts. However, fiscal spending plans have yet to be spelled out in much detail. The upcoming Spending Review will outline the departmental spending cuts and, we assume, provide additional detail on actual programme cuts within this.

This is of course a necessary step in maintaining fiscal credibility. However, the details of the Spending Review will provide more ‘lines of attack’ for critics who doubt that the plans can be achieved without considerable damage to the real economy and to public services. It will be particularly important therefore to see how much protection is given to spending that is likely to boost the UK’s longer-term growth potential. However, given the scale of the spending cuts planned, some compromise on that front seems inevitable, in our view.

A step that should be about shoring up credibility and that should provide more certainty about the path of government spending, could therefore also become a trigger for weaker confidence among households and businesses and doubt among investors about the ability of the economy to generate growth. That effect could be magnified if 3Q GDP growth – released only a few days after the Spending Review – disappoints (as we think it may well do; we forecast: 0.1%Q).

This Spending Review is different

The basics …: The path for public expenditure was set out in the 22 June Budget (see our budget review note). The Spending Review will lay out in more detail how this path will be achieved and will cover the years from 2011/12 to 2014/15. Designed to help multi-period planning, such spending reviews have occurred regularly since the late 1990s (the last in 2007).

… but this Spending Review is set to be a bit different.

Large budget cuts: The overall ‘spending envelope’ was set out in the June Budget. On the government’s own estimates, government spending is set to be cut by around £80 billion between 2010/11 and 2014/15)1. That is, some 6% of 2009 GDP over five years. The overall planned deficit reduction looks very ambitious when scaled against previous reductions. We assume there will not be major changes to the path for government spending and investment shown in the Budget.

It will go beyond departmental budgets: This Spending Review, as well as laying out departmental budgets, will also look at the bits of spending that cannot be ‘firmly fixed’, including social security, tax credits and public service pensions. It is therefore a very wide-ranging exercise. We assume that we are unlikely to learn exactly what these decisions will do for the size of the public sector workforce. We assume, however, that we will get a reasonable amount of detail about specific programme cuts.

Ambition goes beyond just cost-cutting: The Spending Review is not just seen by the government as an exercise in fiscal consolidation, but, according to the Spending Review Framework, as an opportunity to “think innovatively about the role of government in society”.

Big cuts for some departments

The scale of the departmental cuts, and the overall economic implications of the budget, will be affected by the split between cuts in welfare and departmental spending and the degree to which some sectors are protected.

Split between welfare, pensions and departmental spending: Welfare cuts will mean that less has to be cut from departmental expenditure. Since the June Budget Chancellor Osborne has announced a further £4 billion in welfare cuts2; this should ease departmental settlements (very) slightly. Further cuts in welfare could come (and have, with the recently announced cuts to Child Benefit). However, some of this will likely cover the upfront cost of far-reaching

1 Against baseline where departmental spending rises with inflation. 2 http://www.bbc.co.uk/news/uk-politics-11250639

7

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

planned reforms to the benefits system. Generalised public sector pension savings will help ease the burden on departmental budgets.

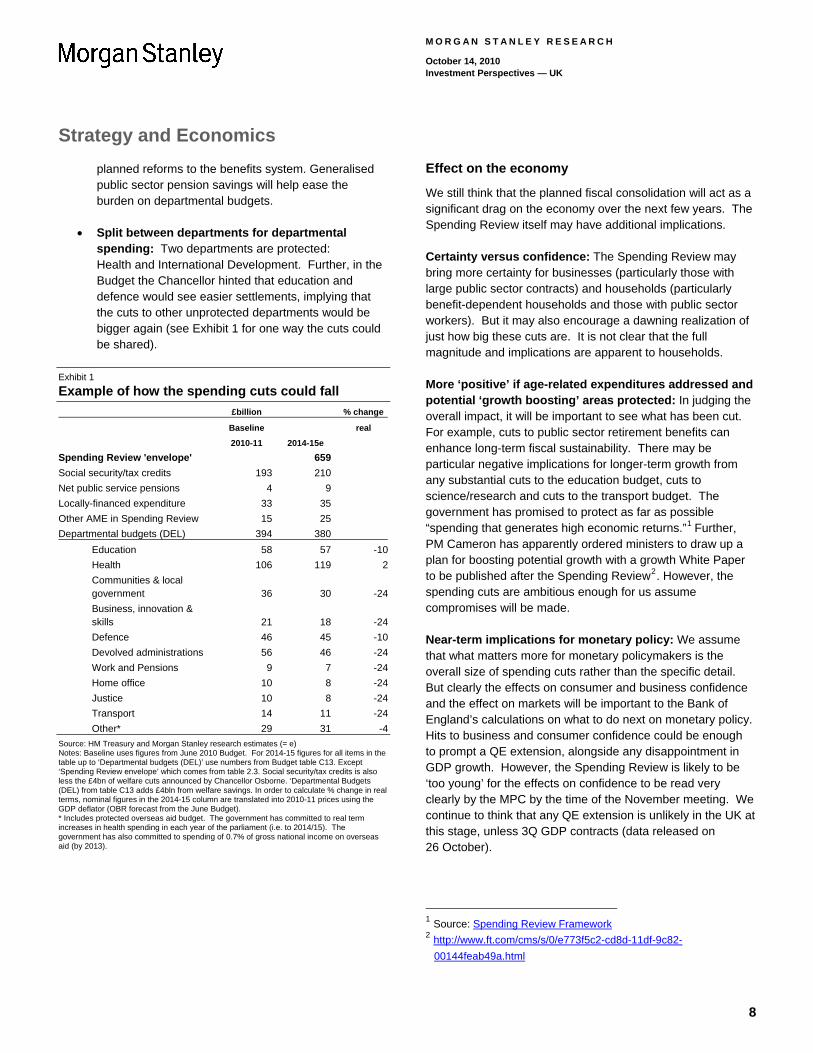

Split between departments for departmental spending: Two departments are protected: Health and International Development. Further, in the Budget the Chancellor hinted that education and defence would see easier settlements, implying that the cuts to other unprotected departments would be bigger again (see Exhibit 1 for one way the cuts could be shared).

Exhibit 1

Example of how the spending cuts could fall

£billion % change

Baseline real

2010-11 2014-15e

Spending Review 'envelope' 659

Social security/tax credits 193 210

Net public service pensions 4 9

Locally-financed expenditure 33 35

Other AME in Spending Review 15 25

Departmental budgets (DEL) 394 380

Education 58 57 -10

Health 106 119 2

Communities & local government 36 30 -24

Business, innovation & skills 21 18 -24

Defence 46 45 -10

Devolved administrations 56 46 -24

Work and Pensions 9 7 -24

Home office 10 8 -24

Justice 10 8 -24

Transport 14 11 -24

Other* 29 31 -4

Source: HM Treasury and Morgan Stanley research estimates (= e) Notes: Baseline uses figures from June 2010 Budget. For 2014-15 figures for all items in the table up to ‘Departmental budgets (DEL)’ use numbers from Budget table C13. Except ‘Spending Review envelope’ which comes from table 2.3. Social security/tax credits is also less the £4bn of welfare cuts announced by Chancellor Osborne. ‘Departmental Budgets (DEL) from table C13 adds £4bln from welfare savings. In order to calculate % change in real terms, nominal figures in the 2014-15 column are translated into 2010-11 prices using the GDP deflator (OBR forecast from the June Budget). * Includes protected overseas aid budget. The government has committed to real term increases in health spending in each year of the parliament (i.e. to 2014/15). The government has also committed to spending of 0.7% of gross national income on overseas aid (by 2013).

Effect on the economy

We still think that the planned fiscal consolidation will act as a significant drag on the economy over the next few years. The Spending Review itself may have additional implications.

Certainty versus confidence: The Spending Review may bring more certainty for businesses (particularly those with large public sector contracts) and households (particularly benefit-dependent households and those with public sector workers). But it may also encourage a dawning realization of just how big these cuts are. It is not clear that the full magnitude and implications are apparent to households.

More ‘positive’ if age-related expenditures addressed and potential ‘growth boosting’ areas protected: In judging the overall impact, it will be important to see what has been cut. For example, cuts to public sector retirement benefits can enhance long-term fiscal sustainability. There may be particular negative implications for longer-term growth from any substantial cuts to the education budget, cuts to science/research and cuts to the transport budget. The government has promised to protect as far as possible “spending that generates high economic returns.”1 Further, PM Cameron has apparently ordered ministers to draw up a plan for boosting potential growth with a growth White Paper to be published after the Spending Review2. However, the spending cuts are ambitious enough for us assume compromises will be made.

Near-term implications for monetary policy: We assume that what matters more for monetary policymakers is the overall size of spending cuts rather than the specific detail. But clearly the effects on consumer and business confidence and the effect on markets will be important to the Bank of England’s calculations on what to do next on monetary policy. Hits to business and consumer confidence could be enough to prompt a QE extension, alongside any disappointment in GDP growth. However, the Spending Review is likely to be ‘too young’ for the effects on confidence to be read very clearly by the MPC by the time of the November meeting. We continue to think that any QE extension is unlikely in the UK at this stage, unless 3Q GDP contracts (data released on 26 October).

1 Source: Spending Review Framework 2 http://www.ft.com/cms/s/0/e773f5c2-cd8d-11df-9c82-

00144feab49a.html

8

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

October 8, 2010

UK Interest Rate Strategy UK Rates: Time to Deliver Morgan Stanley & Co.

International plc+

Anthony S O'Brien Anthony.O'[email protected]

Melanie Baker, CFA, Cath Sleeman

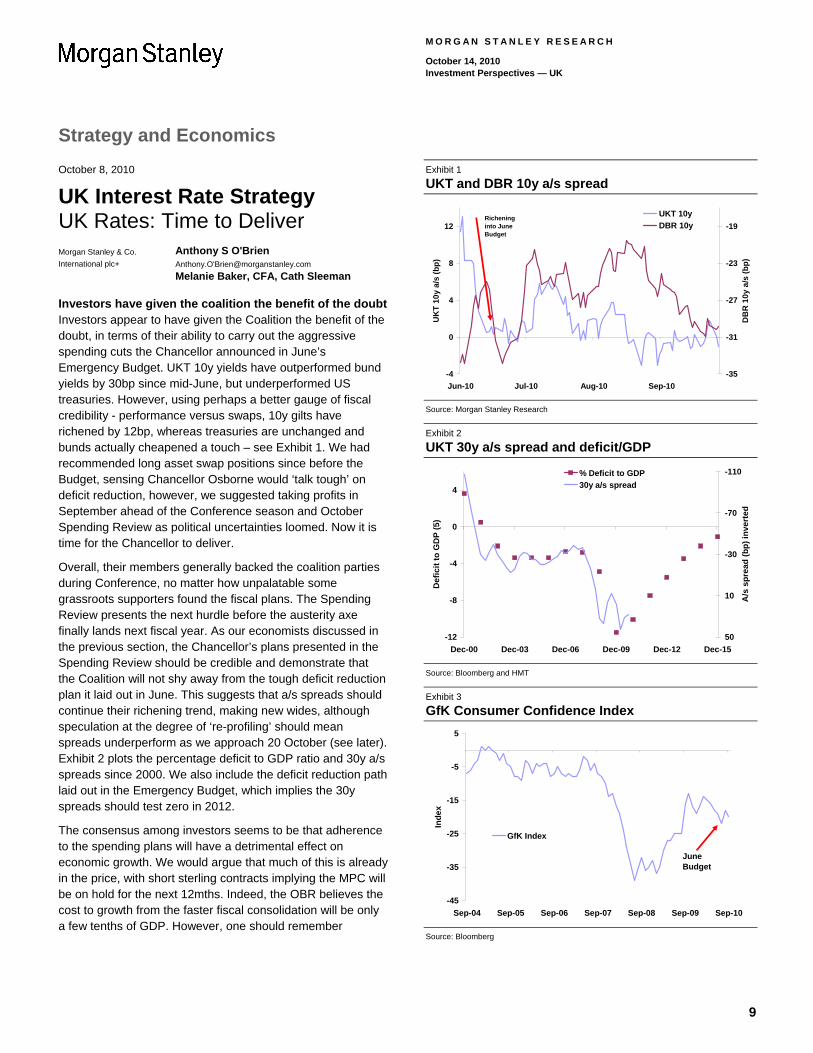

Investors have given the coalition the benefit of the doubt Investors appear to have given the Coalition the benefit of the doubt, in terms of their ability to carry out the aggressive spending cuts the Chancellor announced in June’s Emergency Budget. UKT 10y yields have outperformed bund yields by 30bp since mid-June, but underperformed US treasuries. However, using perhaps a better gauge of fiscal credibility - performance versus swaps, 10y gilts have richened by 12bp, whereas treasuries are unchanged and bunds actually cheapened a touch – see Exhibit 1. We had recommended long asset swap positions since before the Budget, sensing Chancellor Osborne would ‘talk tough’ on deficit reduction, however, we suggested taking profits in September ahead of the Conference season and October Spending Review as political uncertainties loomed. Now it is time for the Chancellor to deliver.

Overall, their members generally backed the coalition parties during Conference, no matter how unpalatable some grassroots supporters found the fiscal plans. The Spending Review presents the next hurdle before the austerity axe finally lands next fiscal year. As our economists discussed in the previous section, the Chancellor’s plans presented in the Spending Review should be credible and demonstrate that the Coalition will not shy away from the tough deficit reduction plan it laid out in June. This suggests that a/s spreads should continue their richening trend, making new wides, although speculation at the degree of ‘re-profiling’ should mean spreads underperform as we approach 20 October (see later). Exhibit 2 plots the percentage deficit to GDP ratio and 30y a/s spreads since 2000. We also include the deficit reduction path laid out in the Emergency Budget, which implies the 30y spreads should test zero in 2012.

The consensus among investors seems to be that adherence to the spending plans will have a detrimental effect on economic growth. We would argue that much of this is already in the price, with short sterling contracts implying the MPC will be on hold for the next 12mths. Indeed, the OBR believes the cost to growth from the faster fiscal consolidation will be only a few tenths of GDP. However, one should remember

Exhibit 1

UKT and DBR 10y a/s spread

-4

0

4

8

12

Jun-10 Jul-10 Aug-10 Sep-10

UK

T 1

0y

a/s

(b

p)

-35

-31

-27

-23

-19

DB

R 1

0y

a/s

(b

p)

UKT 10y

DBR 10y Richening into June Budget

Source: Morgan Stanley Research

Exhibit 2

UKT 30y a/s spread and deficit/GDP

-12

-8

-4

0

4

Dec-00 Dec-03 Dec-06 Dec-09 Dec-12 Dec-15

Def

icit

to

GD

P (

5)

-110

-70

-30

10

50

A/s

sp

read

(b

p)

inve

rte

d

% Deficit to GDP

30y a/s spread

Source: Bloomberg and HMT

Exhibit 3

GfK Consumer Confidence Index

-45

-35

-25

-15

-5

5

Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10

Ind

ex

GfK Index

June Budget

Source: Bloomberg

9

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

consumer confidence reached its lowest levels this year just after the Emergency Budget – see Exhibit 3. Confidence is heading lower again according to the GfK and if it hits a new low after the Spending Review, this would give the MPC much to consider so close to Christmas.

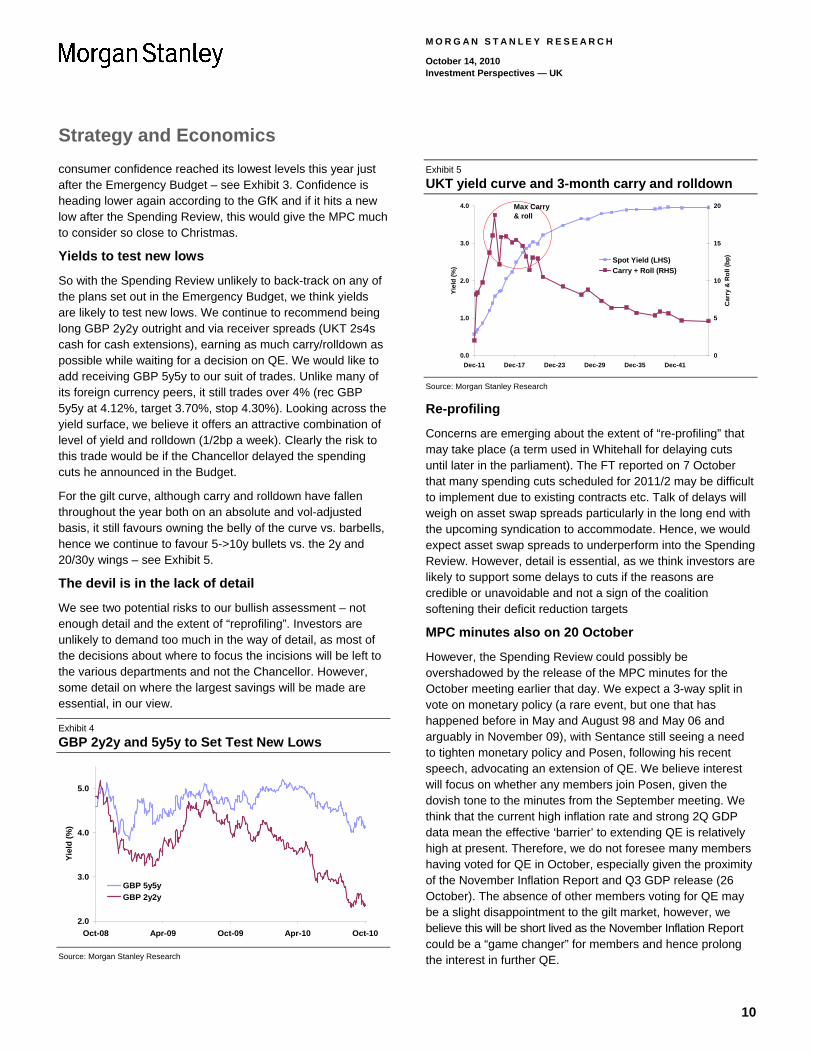

Yields to test new lows

So with the Spending Review unlikely to back-track on any of the plans set out in the Emergency Budget, we think yields are likely to test new lows. We continue to recommend being long GBP 2y2y outright and via receiver spreads (UKT 2s4s cash for cash extensions), earning as much carry/rolldown as possible while waiting for a decision on QE. We would like to add receiving GBP 5y5y to our suit of trades. Unlike many of its foreign currency peers, it still trades over 4% (rec GBP 5y5y at 4.12%, target 3.70%, stop 4.30%). Looking across the yield surface, we believe it offers an attractive combination of level of yield and rolldown (1/2bp a week). Clearly the risk to this trade would be if the Chancellor delayed the spending cuts he announced in the Budget.

For the gilt curve, although carry and rolldown have fallen throughout the year both on an absolute and vol-adjusted basis, it still favours owning the belly of the curve vs. barbells, hence we continue to favour 5->10y bullets vs. the 2y and 20/30y wings – see Exhibit 5.

The devil is in the lack of detail

We see two potential risks to our bullish assessment – not enough detail and the extent of “reprofiling”. Investors are unlikely to demand too much in the way of detail, as most of the decisions about where to focus the incisions will be left to the various departments and not the Chancellor. However, some detail on where the largest savings will be made are essential, in our view.

Exhibit 4

GBP 2y2y and 5y5y to Set Test New Lows

2.0

3.0

4.0

5.0

Oct-08 Apr-09 Oct-09 Apr-10 Oct-10

Yie

ld (

%)

GBP 5y5y

GBP 2y2y

Source: Morgan Stanley Research

Exhibit 5

UKT yield curve and 3-month carry and rolldown

0.0

1.0

2.0

3.0

4.0

Dec-11 Dec-17 Dec-23 Dec-29 Dec-35 Dec-41

Yie

ld (

%)

0

5

10

15

20

Car

ry &

Ro

ll (b

p)

Spot Yield (LHS)

Carry + Roll (RHS)

Max Carry & roll

Source: Morgan Stanley Research

Re-profiling

Concerns are emerging about the extent of “re-profiling” that may take place (a term used in Whitehall for delaying cuts until later in the parliament). The FT reported on 7 October that many spending cuts scheduled for 2011/2 may be difficult to implement due to existing contracts etc. Talk of delays will weigh on asset swap spreads particularly in the long end with the upcoming syndication to accommodate. Hence, we would expect asset swap spreads to underperform into the Spending Review. However, detail is essential, as we think investors are likely to support some delays to cuts if the reasons are credible or unavoidable and not a sign of the coalition softening their deficit reduction targets

MPC minutes also on 20 October

However, the Spending Review could possibly be overshadowed by the release of the MPC minutes for the October meeting earlier that day. We expect a 3-way split in vote on monetary policy (a rare event, but one that has happened before in May and August 98 and May 06 and arguably in November 09), with Sentance still seeing a need to tighten monetary policy and Posen, following his recent speech, advocating an extension of QE. We believe interest will focus on whether any members join Posen, given the dovish tone to the minutes from the September meeting. We think that the current high inflation rate and strong 2Q GDP data mean the effective ‘barrier’ to extending QE is relatively high at present. Therefore, we do not foresee many members having voted for QE in October, especially given the proximity of the November Inflation Report and Q3 GDP release (26 October). The absence of other members voting for QE may be a slight disappointment to the gilt market, however, we believe this will be short lived as the November Inflation Report could be a “game changer” for members and hence prolong the interest in further QE.

10

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

October 8, 2010

European Credit Strategy Deleveraging and the Debt/Equity Clock Morgan Stanley & Co.

International plc

Andrew Sheets [email protected]

Phanikiran Naraparaju, Carlos Egea, Serena Tang, Jonathan Graber

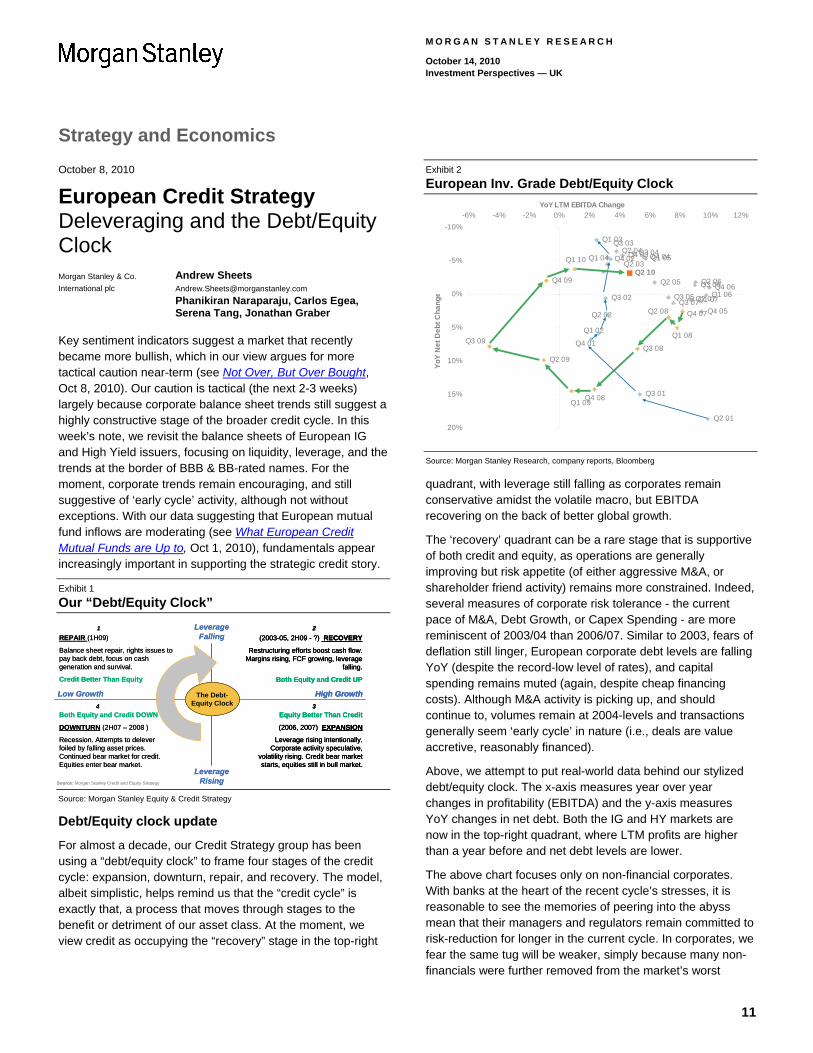

Key sentiment indicators suggest a market that recently became more bullish, which in our view argues for more tactical caution near-term (see Not Over, But Over Bought, Oct 8, 2010). Our caution is tactical (the next 2-3 weeks) largely because corporate balance sheet trends still suggest a highly constructive stage of the broader credit cycle. In this week’s note, we revisit the balance sheets of European IG and High Yield issuers, focusing on liquidity, leverage, and the trends at the border of BBB & BB-rated names. For the moment, corporate trends remain encouraging, and still suggestive of ‘early cycle’ activity, although not without exceptions. With our data suggesting that European mutual fund inflows are moderating (see What European Credit Mutual Funds are Up to, Oct 1, 2010), fundamentals appear increasingly important in supporting the strategic credit story.

Exhibit 1

Our “Debt/Equity Clock”

Source: Morgan Stanley Equity & Credit Strategy

Debt/Equity clock update

For almost a decade, our Credit Strategy group has been using a “debt/equity clock” to frame four stages of the credit cycle: expansion, downturn, repair, and recovery. The model, albeit simplistic, helps remind us that the “credit cycle” is exactly that, a process that moves through stages to the benefit or detriment of our asset class. At the moment, we view credit as occupying the “recovery” stage in the top-right

Exhibit 2

European Inv. Grade Debt/Equity Clock

Q2 10

Q1 10

Q4 09

Q3 09

Q2 09

Q1 09Q4 08

Q3 08

Q2 08

Q1 08

Q4 07

Q3 07Q2 07Q1 07

Q4 06Q3 06Q2 06

Q1 06

Q4 05

Q3 05

Q2 05

Q1 05Q4 04Q3 04Q2 04

Q1 04 Q4 03

Q3 03

Q2 03

Q1 03

Q4 02

Q3 02

Q2 02

Q1 02

Q4 01

Q3 01

Q2 01

-10%

-5%

0%

5%

10%

15%

20%

-6% -4% -2% 0% 2% 4% 6% 8% 10% 12%YoY LTM EBITDA Change

Yo

Y N

et

De

bt

Ch

an

ge

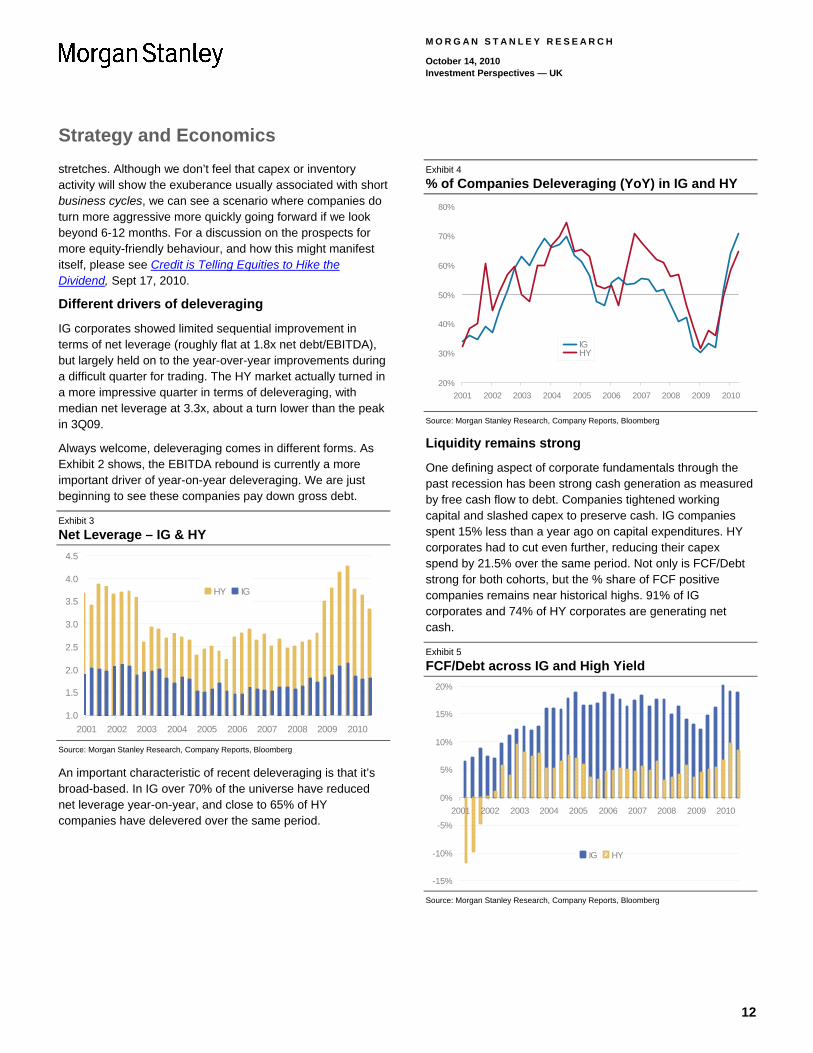

Source: Morgan Stanley Research, company reports, Bloomberg

quadrant, with leverage still falling as corporates remain conservative amidst the volatile macro, but EBITDA recovering on the back of better global growth.

The ‘recovery’ quadrant can be a rare stage that is supportive of both credit and equity, as operations are generally improving but risk appetite (of either aggressive M&A, or shareholder friend activity) remains more constrained. Indeed, several measures of corporate risk tolerance - the current pace of M&A, Debt Growth, or Capex Spending - are more reminiscent of 2003/04 than 2006/07. Similar to 2003, fears of deflation still linger, European corporate debt levels are falling YoY (despite the record-low level of rates), and capital spending remains muted (again, despite cheap financing costs). Although M&A activity is picking up, and should continue to, volumes remain at 2004-levels and transactions generally seem ‘early cycle’ in nature (i.e., deals are value accretive, reasonably financed).

Above, we attempt to put real-world data behind our stylized debt/equity clock. The x-axis measures year over year changes in profitability (EBITDA) and the y-axis measures YoY changes in net debt. Both the IG and HY markets are now in the top-right quadrant, where LTM profits are higher than a year before and net debt levels are lower.

The above chart focuses only on non-financial corporates. With banks at the heart of the recent cycle’s stresses, it is reasonable to see the memories of peering into the abyss mean that their managers and regulators remain committed to risk-reduction for longer in the current cycle. In corporates, we fear the same tug will be weaker, simply because many non-financials were further removed from the market’s worst

Low Growth

Leverage Falling

Leverage Rising

The Debt-Equity Clock4

1

High Growth

3

2

(2003-05, 2H09 - ?) RECOVERY

Restructuring efforts boost cash flow. Margins rising, FCF growing, leverage

falling.

Both Equity and Credit UP

Equity Better Than Credit

(2006, 2007) EXPANSION

Leverage rising intentionally. Corporate activity speculative,

volatility rising. Credit bear market starts, equities still in bull market.

Both Equity and Credit DOWN

WNTURNDO (2H07 – 2008 )

ecession. Attempts to delever iled by falling asset prices. ontinued bear market for credit.

ities enter bear market.

Source: Morgan Stanley Credit and Equity Strategy

EPAIR

RfoCEqu

R (1H09)

ance sheet repair, rights issues to ay back debt, focus on cash

neration and survival.

Credit Better Than Equity

Balpge

Low Growth

Leverage Falling

Leverage Rising

The Debt-Equity Clock4

1

High Growth

3

2

(2003-05, 2H09 - ?) RECOVERY

Restructuring efforts boost cash flow. Margins rising, FCF growing, leverage

falling.

Both Equity and Credit UP

Equity Better Than Credit

(2006, 2007) EXPANSION

Leverage rising intentionally. Corporate activity speculative,

volatility rising. Credit bear market starts, equities still in bull market.

High Growth

3

2

(2003-05, 2H09 - ?) RECOVERY

Restructuring efforts boost cash flow. Margins rising, FCF growing, leverage

falling.

Both Equity and Credit UP

Equity Better Than Credit

(2006, 2007) EXPANSION

Leverage rising intentionally. Corporate activity speculative,

volatility rising. Credit bear market starts, equities still in bull market.

Both Equity and Credit DOWN

WNTURNDO (2H07 – 2008 )

ecession. Attempts to delever iled by falling asset prices. ontinued bear market for credit.

ities enter bear market.

Source: Morgan Stanley Credit and Equity Strategy

EPAIR

RfoCEqu

R (1H09)

ance sheet repair, rights issues to ay back debt, focus on cash

neration and survival.

Credit Better Than Equity

Balpge

11

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

stretches. Although we don’t feel that capex or inventory activity will show the exuberance usually associated with short business cycles, we can see a scenario where companies do turn more aggressive more quickly going forward if we look beyond 6-12 months. For a discussion on the prospects for more equity-friendly behaviour, and how this might manifest itself, please see Credit is Telling Equities to Hike the Dividend, Sept 17, 2010.

Different drivers of deleveraging

IG corporates showed limited sequential improvement in terms of net leverage (roughly flat at 1.8x net debt/EBITDA), but largely held on to the year-over-year improvements during a difficult quarter for trading. The HY market actually turned in a more impressive quarter in terms of deleveraging, with median net leverage at 3.3x, about a turn lower than the peak in 3Q09.

Always welcome, deleveraging comes in different forms. As Exhibit 2 shows, the EBITDA rebound is currently a more important driver of year-on-year deleveraging. We are just beginning to see these companies pay down gross debt.

Exhibit 3

Net Leverage – IG & HY

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

HY IG

Source: Morgan Stanley Research, Company Reports, Bloomberg

An important characteristic of recent deleveraging is that it’s broad-based. In IG over 70% of the universe have reduced net leverage year-on-year, and close to 65% of HY companies have delevered over the same period.

Exhibit 4

% of Companies Deleveraging (YoY) in IG and HY

20%

30%

40%

50%

60%

70%

80%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

IGHY

Source: Morgan Stanley Research, Company Reports, Bloomberg

Liquidity remains strong

One defining aspect of corporate fundamentals through the past recession has been strong cash generation as measured by free cash flow to debt. Companies tightened working capital and slashed capex to preserve cash. IG companies spent 15% less than a year ago on capital expenditures. HY corporates had to cut even further, reducing their capex spend by 21.5% over the same period. Not only is FCF/Debt strong for both cohorts, but the % share of FCF positive companies remains near historical highs. 91% of IG corporates and 74% of HY corporates are generating net cash.

Exhibit 5

FCF/Debt across IG and High Yield

-15%

-10%

-5%

0%

5%

10%

15%

20%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

IG HY

Source: Morgan Stanley Research, Company Reports, Bloomberg

12

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

Exhibit 6

% of Companies FCF+ across IG and High Yield

40%

50%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

60%

70%

80%

90%

100%

IG

HY

Source: Morgan Stanley Research, Company Reports, Bloomberg

Are the gains to cash generation from these cuts at risk?

g

wly. The latter trend reflects business skepticism overy, but recovering order

demand has forced a reassessment: surveys show a record share of euro area manufacturers “view their inventories of finished products as insufficient right now” (Euroland

There is the risk that working capital consumes more cash as companies restock. Our European economists note that manufacturers have acted more aggressively on the workincapital management front this cycle compared to any of theprevious cycles, cutting inventories deeper and restocking more sloabout the durability of the rec

Economics: Chewing on Green Shoots, Aug 5, 2010). Despite the uptick in order demand, there is yet little pressure to expand operations organically. Capacity utilization in the eurozone sits at just 75.5% at the end of the second quarter, well below the 15-year average (~82%) and even the early 1990s nadir (76.7%).

Despite these potential stresses on free cash flow generation, projected figures are upbeat. Aggregating the estimates of our equity analysts for western European companies, 2011e FCF

FCF a 5%

nd near-

Trends by sector and rating

Digging a level deeper, we look at trends at the sector and rating level. Our one high-conviction sector trade has been overweight financials, especially sub-debt. Within non-financials, we’re pleased with the broad-based fundamental improvement across sectors, and find more value in contrasting individual credits, beyond the sector level. In Exhibits 7-8 we present the

evels, by sector and rating, of FCF/Debt, Cash/Debt,

absolute change of these metrics is reported in parentheses.

Exhibit 7

should be just 4% off 2009 levels, and 2012eimprovement. As the debt/equity clock turns, FCF is likely to once again turn lower as companies (or their acquirers) find other uses for the cash. But for now, high levels of cash andcash flow remain highly supportive of credit quality, aterm default risk.

current lInterest Coverage and Net Leverage. The year-on-year

European IG Sector Scorecard FCF/Debt Cash to Debt Int Cov Net Leverage

Autos 120% (101%) 186% (107%) - -0.5 (-2.2)Chemicals 21% (3%) 41% (15%) 7.6 (-1.1) 1.1 (-0.7)Cons. Disc. 43% (19%) 21% (5%) 11.0 (1.6) 1.5 (0.2)Cons. Stap. 22% (10%) 18% (3%) 5.7 (0.9) 2.3 (-0.3)Energy 0% (-17%) 30% (0%) 33.1 (12.3) 0.8 (-0.1)Health Care 34% (-4%) 44% (-18%) 13.1 (1.6) 0.6 (0.2)Industrials 19% (-3%) 32% (5%) 7.3 (1.8) 1.6 (-0.2)Materials 14% (2%) 14% (-9%) 8.8 (1.7) 2.0 (0.3)Media 22% (0%) 28% (3%) 8.8 (2.7) 1.6 (-0.3)Telecom 15% (3%) 16% (0%) 7.4 (1.1) 2.3 (-0.2)Utilities 8% (5%) 9% (-3%) 5.5 (0.3) 3.7 (0.7)Market 19% (4%) 21% (1%) 7.3 (1.2) 1.8 (-0.3)

Source: Morgan Stanley Research, Company Reports, Bloomberg

IG fundamental trends look pretty consistent across the

year

board. IG Autos have performed exceptionally well at the industrial co level, enjoying the benefits of various national auto stimulus plans. Chemicals also show impressive deleveraging on the back of an EBITDA rebound thanks to global demand. Materials are also faring better than the headline; ex-MTNA, the sector has delevered half a turn on year. As we’ve mentioned before, we like Materials namesfor their exposure to global growth.

Exhibit 8

European HY Sector Scorecard FCF/Debt Cash to Debt Int Cov Net Leverage

Autos 25% (18%) 49% (28%) - 1.1 (-1.1)(0.4) 2.5 (-0.5)

7) 1.6 (-1.0)Cons. Stap. 14% (4%) 9% (4%) 3.7 (-0.6) 3.2 (-0.3)Energy 14% (21%) 17% (-1%) 3.0 (-0.5) 4.9 (-1.6)Industrials 1% (4%) 24% (-6%) 2.7 (0.2) 4.7 (0.0)Materials 6% (-4%) 26% (4%) 2.4 (0.0) 3.4 (-1.9)Media 9% (5%) 7% (2%) 2.1 (-0.5) 5.3 (0.6)Telecom 9% (6%) 3% (-3%) 4.5 (1.0) 2.6 (0.0)Market 8% (3%) 20% (4%) 3.0 (0.1) 3.3 (-0.8)

Chemicals 11% (-2%) 30% (0%) 3.8 Cons. Disc. 13% (13%) 30% (11%) 4.8 (1.

Source: Morgan Stanley Research, Company Reports, Bloomberg

Please note that all important disclosures including personal holdings disclosures and Morgan Stanley disclosures appear on the Morgan Stanley public website at www.morganstanley.com/researchdisclosures.

HY fundamental trends exhibit a little more dispersion. HY Media is faring the worst in terms of net leverage, and its interest coverage is the lowest among the sectors. Autos,

wn the most progress in deleveraging, reflective of a cyclical rebound. The deleveraging in the Energy sector is due entirely to Petroplus returning to profitability.

Consumer Discretionary, and Materials have sho

13

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

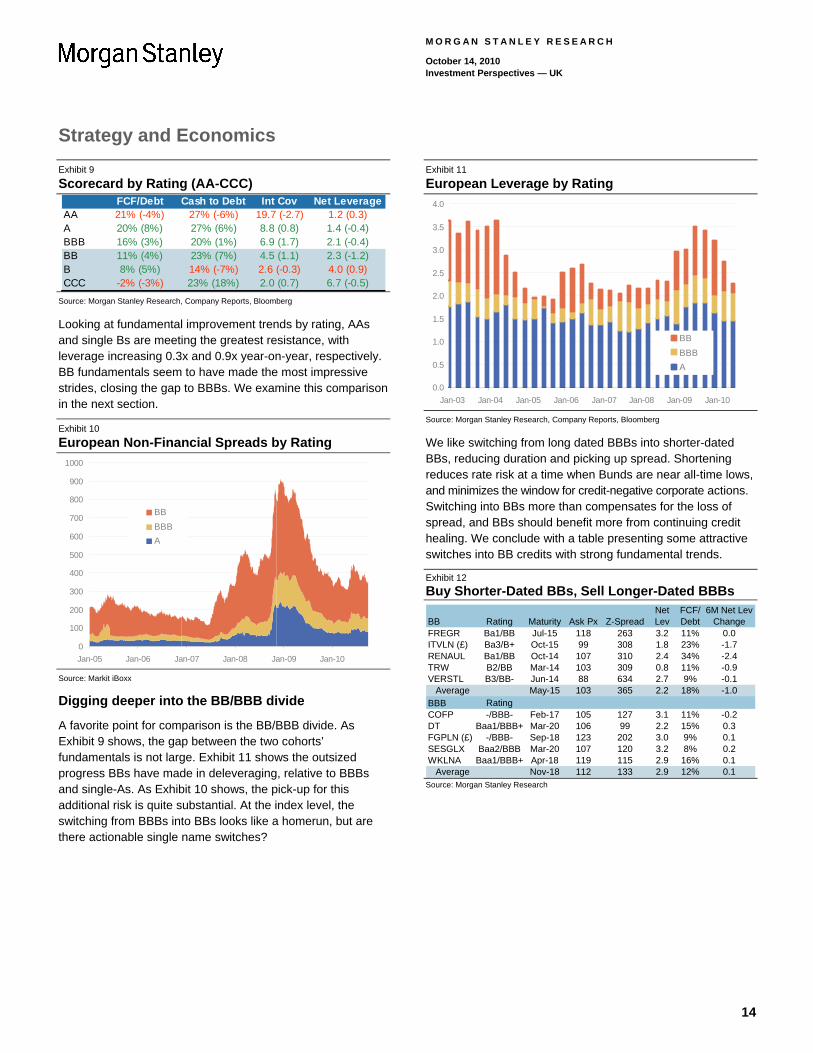

Exhibit 9

Scorecard by Rating (AA-CCC) FCF/Debt Cash to Debt Int Cov Net Leverage

AA 21% (-4%) 27% (-6%) 19.7 (-2.7) 1.2 (0.3)A 20% (8%) 27% (6%) 8.8 (0.8) 1.4 (-0.4)BBB 16% (3%) 20% (1%) 6.9 (1.7) 2.1 (-0.4)BB 11% (4%) 23% (7%) 4.5 (1.1) 2.3 (-1.2)B 8% (5%) 14% (-7%) 2.6 (-0.3) 4.0 (0.9)CCC -2% (-3%) 23% (18%) 2.0 (0.7) 6.7 (-0.5)

Source: Morgan Stanley Research, Company Reports, Bloomberg

Looking at fundamental improvement trends by rating, AAs and single Bs are meeting the greatest resistance, with leverage increasing 0.3x and 0.9x year-on-year, respectively. BB fundamentals seem to have made the most impressive strides, closing the gap to BBBs. We examine this comparison in the next section.

Exhibit 10

European Non-Financial Spreads by Rating

0

100

200

300

400

500

600

700

800

900

1000

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

BB

BBB

A

Source: Markit iBoxx

Digging deeper into the BB/BBB divide

A favorite point for comparison is the BB/BBB divide. As Exhibit 9 shows, the gap between the two cohorts’ fundamentals is not large. Exhibit 11 shows the outsized progress BBs have made in deleveraging, relative to BBBs and single-As. As Exhibit 10 shows, the pick-up for this additional risk is quite substantial. At the index level, the switching from BBBs into BBs looks like a homerun, but are there actionable si

Exhibit 11

European Leverage by Rating

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

BB

BBB

A

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Source: Morgan Stanley Research, Company Reports, Bloomberg

We like switching from long dated BBBs into shorter-dated BBs, reducing duration and picking up spread. Shorteningreduces rate risk at a time when Bunds are near all-time lows, and minimizes the window for credit-negative corporate actionsSwitching into BBs more than compensates for the loss of spread, and BBs should benefit more from continuing credit healing. We conclude with a table presenting some attractive switches into BB credits with strong fundamental trends.

Exhibit 12

.

Buy Shorter-Dated BBs, Sell Longer-Dated BBBs

BB Rating Maturity Ask Px Z-SpreadNet Lev

FCF/Debt

6M Net Lev Change

FREGR Ba1/BB Jul-15 118 263 3.2 11% 0.0ITVLN (£) Ba3/B+ Oct-15 99 308 1.8 23% -1.7RENAUL Ba1/BB Oct-14 107 310 2.4 34% -2.4TRW B2/BB Mar-14 103 309 0.8 11% -0.9VERSTL B3/BB- Jun-14 88 634 2.7 9% -0.1

Average May-15 103 365 2.2 18% -1.0BBB RatingCOFP -/BBB- Feb-17 105 127 3.1 11% -0.2DT Baa1/BBB+ Mar-20 106 99 2.2 15% 0.3FGPLN (£) -/BBB- Sep-18 123 202 3.0 9% 0.1SESGLX Baa2/BBB Mar-20 107 120 3.2 8% 0.2WKLNA Baa1/BBB+ Apr-18 119 115 2.9 16% 0.1

12% 0.1 Average Nov-18 112 133 2.9Source: Morgan Stanley Research

ngle name switches?

14

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

October 8, 2010

US Economics Roadmap to Sustainable Growth Morgan Stanley & Co.

Incorporated

Richard Berner [email protected]

David Greenlaw [email protected]

r

at 1.4% measured by the core personal price index, or somewhat below the Fed’s

that inflation is bottoming, the rise we expect to 1.6% next year is unlikely to satisfy the Fed. With the Fed missing on both aspects of its dual mandate, and other policies caught in political gridlock, it’s appropriate for the Fed to ease policy further.

Yield outlook depends on policy. Our interest rate strategy team and we believe that ten-year Treasury yields will likely decline slightly further, to 2.25% or so. The Fed wants to depress real yields to support growth while boosting inflation expectations, so the composition of yields between real and inflation compensation matters more than the level of nominal rates. With ten-year real (TIPS) yields at 50 bp, down 70 bp from July, real yields are clearly headed in the right direction.

will depend on how low officials think real ields must go and how long they need to stay there to

keep the

n. of

alf of

ome of their aberrant Q2 gain. Quirky seasonal factors for petroleum imports will likely defer that improvement until Q4, but a one-point annualized contribution to growth from net exports in H2 should partly offset the near-record 1.9% H1 drag from net exports.

Second, personal income is growing again. Even with modest job gains, increases in the workweek have sustained real wage and salary income growth at a 2%

al rate in the past three months. Ongoing e and the

reinstatement of unemployment insurance benefits are providing enough wherewithal to sustain the 2% pace of consumer spending we expect in H2.

Third, lower mortgage rates are promoting a modest refinancing wave, despite the inability of many current borrowers to qualify under current GSE guidelines. We estimate that the recent decline in mortgage rates will reduce interest payments and provide a $10-15 billion windfall to borrowers. That will accelerate the decline in the household debt service ratio — already down from 14% in Q3 07 to 12.1% in Q2 — to a sustainable 11-12% range by late this year, with ongoing benefits to consumer discretionary income and creditworthiness. As evidence of consumers’ new capacity to borrow, nonrevolving

in a row in

e

flat

y in such outlays and cuts in

ended in Q1 10.

Will QE2 work? We think there’s modestly good news ahead: The combination of easier financial conditions and strong overseas growth should help trigger a return to sustainable, slightly above-trend growth in 2011. QE is no panacea, of course, and its bang per buck will be small, but it will help. QE will work through several channels: It will lower financing costs, boost risky asset prices and household wealth, and continue to weaken the dollar. Freddie Mac reported this week that 30-year conventional mortgage rates

any lenders are offering rates between 3.875% and 4.25%. Since Fed Chairman Bernanke’s Jackson Hole speech, popular stock price gauges have risen by 10%. That reversed the second-quarter decline and puts household equity wealth up 5.6% ($960 billion) so far this year. And the dollar on a broad, trade-weighted basis has declined by 5.2%.

Those developments will help support credit-sensitive spending, foster a stable-to-lower saving rate, and help net exports. At the margin, lower mortgage rates will promote refinancing and make housing more affordable. Corporate America is borrowing at historically low rates. Standard

QE coming soon. It’s virtually certain that today’s below-trend growth and too-low inflation will spur aggressive furtheasset purchases from the Fed. Growth has slipped to 2-2½% in the second half of this year, and slack in the economy is beginning to rise; the unemployment rate edged up from 9.5% in July to 9.6% in September, and a further increase is likely. Core inflation stands consumption unofficial target of 1¾-2%. While we strongly believe

But the trough ysupport growth. It seems likely that the Fed will funds rate near zero until 2012.

Consensus is too pessimistic on growth, inflatioDespite our subdued outlook, we think the consensus view1-2% growth and declining inflation is too dour. We see fourfactors that will sustain growth at 2-2½% in the second hthis year:

First, we think net exports will rebound in H2 as export growth persists and imports retrace s

annuimprovements in proprietors’ incom

consumer credit rose for the fourth monthAugust.

Finally, lingering fiscal stimulus in the form of rising infrastructure spending will boost near-term growth. Outlays for highways, bridges and other state and local infrastructure jumped at a 20.1% annual rate in the thremonths ended in August, and double-digit gains in such spending are likely at least through the mid-term elections.That will keep overall state and local spending growthin H2. In contrast, the delastate and local spending trimmed an average 0.3 percentage point from GDP in each of the three quarters

declined to 4.27%, and m

15

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

models suggest that the rise in wealth, if sustained, will 4%) in consumer spending. uggests that a sustained 5%

mon mission channel mearect impact and will be

ited. Tougher mor riteria have limited the umber of eligible borro with

ans

d.

low imports dramatically. As mentioned above, if

ce,

of rs do

ing quarters.” Chetan Ahya onth

ber have been robust.”

econd alternative to resolve this ‘trilemma,’ or as

S imports tribution

ied the Q2 import se

nd,

the

ek

te If n

rag

rst

prompt an extra $44 billion (0.Likewise, our empirical work sdepreciation in the real trade-weighted dollar will over three years boost net exports by about 1% of GDP. However, blockages in thethat the di

etary policy trans n

surge and dampened recovery in domestic output. Becauthat inventory leverage works both ways, a slowing in inventory accumulation will depress import growth going forward. Consequently, we think that import growth henceforth will re-sync with the pace of US domestic demapromoting a deceleration in imports and ultimately a much-needed rebalancing of the US economy.

Needed: Job and income growth. Ultimately, the sustainability of the recovery will hinge in significant part on the continued revival of job and income growth. On that score, the moderation in the pace of private job gains andsignificant declines in state and local government jobs are

th a concer

from QE on domestic demlim tgage origination cn wers, and originators faced “putbacks” from the GSEs (Fannie and Freddie) on prior loare understandably skittish to extend credit to less-than-pristine borrowers.

Strong growth abroad will lift US net exports. The influence of strong global growth on US demand and output is a key factor that differentiates us from pessimists. US net exports are poised to add to growth over the next year. While growth in developed market economies is tepid, a modest reacceleration in emerging market growth, especially in capital spending, will help US exports. The surge in non-oil imports has ended, and stable import penetration means imports will grow only slightly faster than domestic demanIn turn, a sharp moderation in US demand and inventories should ssustained, the dollar’s decline will augment those gains.

Global growth slowed in the spring, casting doubt on its potential support for US growth. But even with a slower pathree global factors are likely to boost US exports: a shift in the mix of US exports toward faster-growing EM economies and Canada, a global capex upswing, and the Russian drought and export ban that will boost agricultural exports.

Moreover, the slowing in global growth may be ending. Qing Wang notes that “while there has been no clear indicationre-acceleration in Chinese growth, forward-looking indicatosuch as PMIs and the MS China Business Condition Index point to re-acceleration in the comobserves that in India “the volatile IP number showed a mon month deceleration in June but July data released in mid-September came right back with a 6% (MoM) rise. Key domestic demand indicators such as auto sales for August and Septem

Finally, US QE may indirectly promote faster US growth through an international channel: The Fed’s actions are strengthening currencies abroad and forcing policymakers tochoose whether to accept currency strength, adopt easier policies, or implement capital controls. Many central banks inboth EM and DM economies (e.g., Australia, Canada) are choosing the simpossible trinity, meaning they are choosing faster growthwell as global rebalancing.

Import slowdown has begun. A spring surge in Uthwarted what we expected to be a moderate confrom global to US growth earlier this year. But we think the 33.5% annualized Q2 import surge was only a temporary development. Swings in inventories magnif

bo n. The good news is that a rising work wehas through most of this year promoted healthy gains in paychecks; the bad news is that private hours stalled in September and growth must improve to restart that process. More ominously, state and local payrolls skidded by a monthlyaverage of 54,000 in the summer. As noted below, a further revival in revenues will be needed to stabilize and ultimately revive state and local government hiring.

Coming resolution to tax uncertainty. Policy gridlock in Washington has created economic uncertainty and a drag on growth. If this gridlock is not resolved soon, expectations of fiscal drag will become reality, perhaps trimming three-quarters of a percentage point from growth in 2011. The faof the expiring tax cuts is a key uncertainty for the outlook. the tax cuts expire, households will be hit with $175 billion ihigher taxes on January 1. We now expect that Congress and the Administration will resolve that uncertainty by early next year with a one-year extension of all tax provisions.

Fiscal drag: Less than feared. Three sources of fiscal dcould hold back growth: Stimulus enacted in 2009 under the American Recovery and Reconstruction Act (ARRA) will continue to fade, unemployment benefits may not be extended, and state and local governments could cut spending further. However, we expect that Congress will extend UI benefits at least for a while. And rising tax receipts mean that the drag from state and local restraint should be modest. Total state and local tax revenue gained 1.7% year/year in Q2, a third straight small gain after the wodecline on record last year. The combination of a modest rebound in revenues and Federal stimulus funds for infrastructure seems likely to support renewed spending growth.

16

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

October 8, 2010

US Credit Strategy Tale of Two Markets Morgan Stanley & Co.

Incorporated

Rizwan Hussain [email protected]

Maya Abdurahmanova, CFA [email protected]

Despite buoyant primary markets, the tone in secondary markets hasn’t been as consistently positive. With earnings season commencing, companies will soon offer

e

e tal

ry

ew

– as

’s

ancials. Primary markets remain the path of least resistance to add non-financial credit risk,

greater confirmation or denial of the strength and staying power of a sustained US rebound. Meanwhile, high-grade credit markets just finished the seventh biggest month of thpast decade in new issues, and yet corporate excess returns were strongly positive, ringing in their third best month of thyear. We hope that goes some way in severing the menassociation many still have between sizeable primary issuance and subsequent credit underperformance. Primaissuance confirming secondary market spreads was certainly at work, and admittedly the technical backdrop remained favorable.

Recent conversations with investors suggest that many remain frustrated with the lack of opportunity away from nissues. Many argue that thin, illiquid markets are barely providing an opportunity to meaningfully add risk (or for that matter, shed it), leaving the new issue space virtually the only game in town. Only when new issue markets slow downin earnings season now – does the focus seem to (perhaps reluctantly) shift back to existing issues in the hunt for value.

We have explored some of the statistics around secondary trading this year, as well as how it has and hasn’t changed over the past nine months. While this content may be a bit more backward-looking than we typically offer, we believe there are lessons to be learned from a broader portfolio-management perspective. In summary:

Similar to market experience ahead of the US banking system stress tests of last year, trading volumes did decline in advance of a similar exercise in Europe this summer, but more importantly, are now tracking last yearlevels.

The top 20 most actively traded credits have consistently accounted for about 40% of overall trading volume in the last two years. This remains a source of frustration overall in secondary markets today, but it is not a new dynamic.

Meanwhile, the top 20 most actively traded issuers remain highly skewed towards fin

and financials will remain prone to be a source of funds should volatility rise from here.

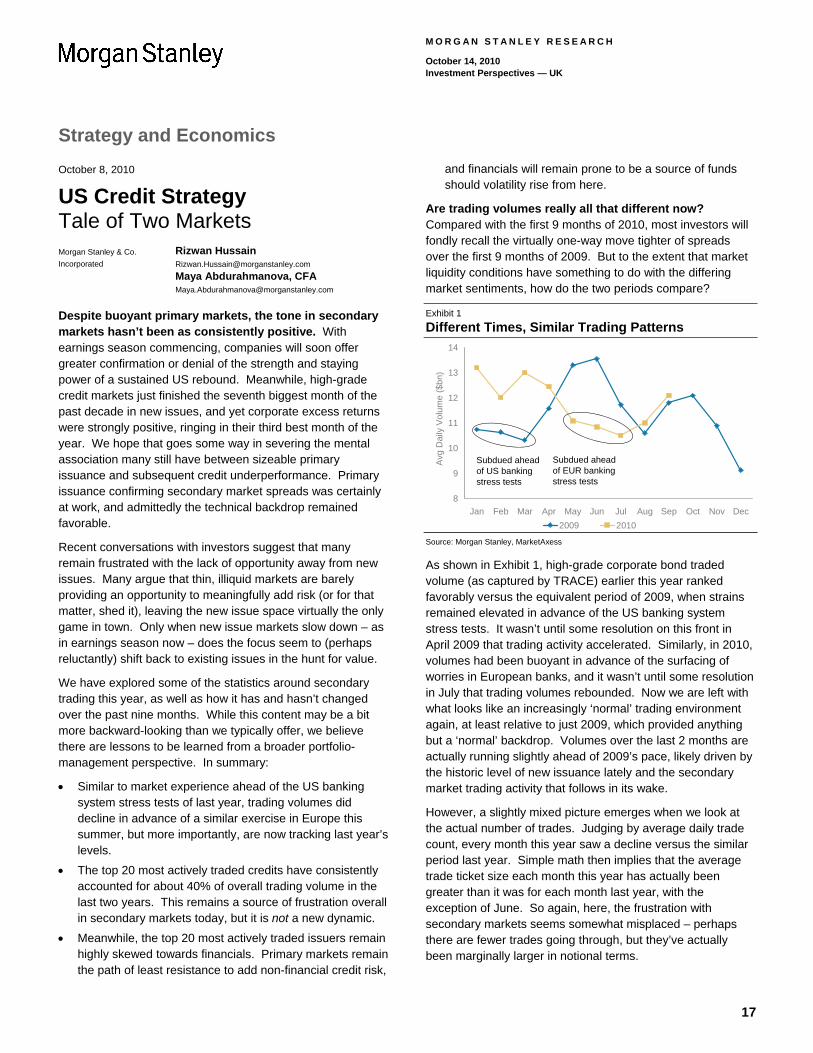

Are trading volumes really all that different now? Compared with the first 9 months of 2010, most investors will fondly recall the virtually one-way move tighter of spreads over the first 9 months of 2009. But to the extent that market liquidity conditions have something to do with the differingmarket sentiments, how do the two periods compare?

Exhibit 1

Different Times, Similar Trading Patterns

8

9

10

11

12

13

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Avg

Dai

ly V

olu

me

($bn

)

14

2009 2010

Subdued ahead of US banking stress tests

Subdued ahead of EUR banking stress tests

Source: Morgan Stanley, MarketAxess

As shown in Exhibit 1, high-grade corporate bond traded

in

th

g

y

ok at e

rhaps

rginally larger in notional terms.

volume (as captured by TRACE) earlier this year ranked favorably versus the equivalent period of 2009, when strains remained elevated in advance of the US banking system stress tests. It wasn’t until some resolution on this frontApril 2009 that trading activity accelerated. Similarly, in 2010, volumes had been buoyant in advance of the surfacing of worries in European banks, and it wasn’t until some resolutionin July that trading volumes rebounded. Now we are left wiwhat looks like an increasingly ‘normal’ trading environment again, at least relative to just 2009, which provided anythinbut a ‘normal’ backdrop. Volumes over the last 2 months are actually running slightly ahead of 2009’s pace, likely driven bythe historic level of new issuance lately and the secondarmarket trading activity that follows in its wake.

However, a slightly mixed picture emerges when we lothe actual number of trades. Judging by average daily tradcount, every month this year saw a decline versus the similar period last year. Simple math then implies that the averagetrade ticket size each month this year has actually been greater than it was for each month last year, with the exception of June. So again, here, the frustration with secondary markets seems somewhat misplaced – pethere are fewer trades going through, but they’ve actuallybeen ma

17

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

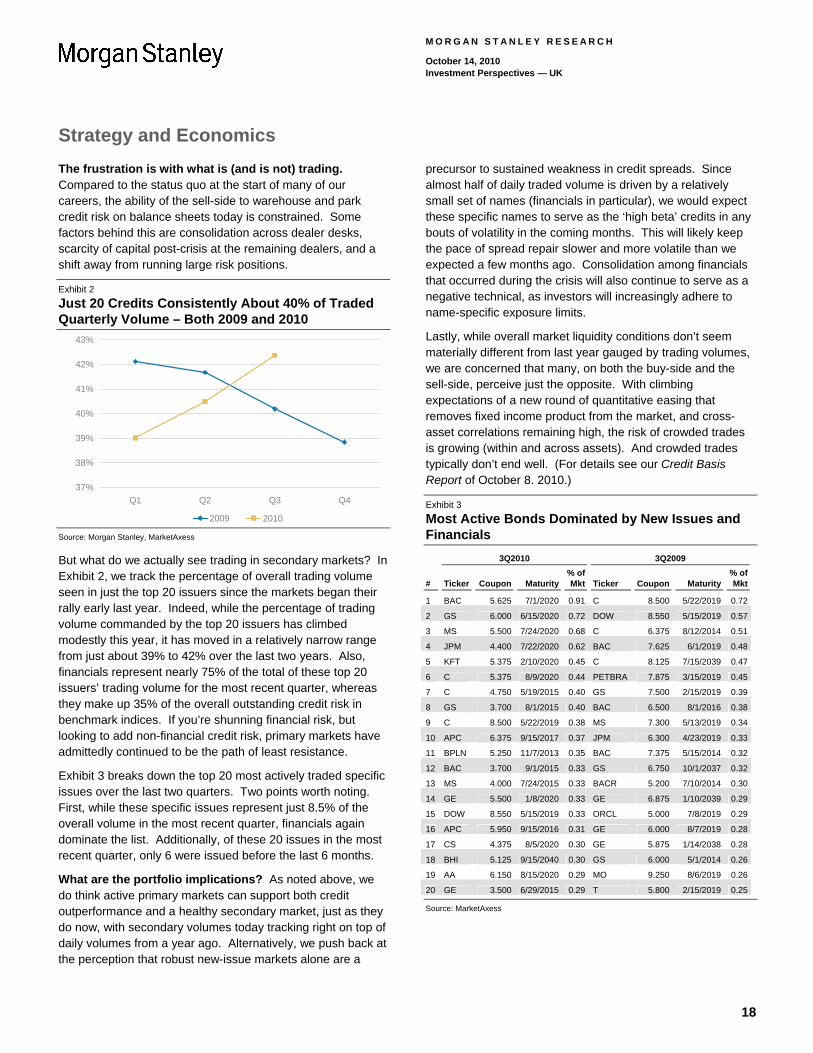

The frustration is with what is (and is not) trading. rt of many of our arehouse and park onstrained. Some ross dealer desks,

l pos aining dealers, and a from runnin

Exhibit 2

Compared to the status quo at the stacareers, the ability of the sell-side to wcredit risk on balance sheets today is cfactors behind this are consolidation acscarcity of capitashift away

t-crisis at the remg large risk positions.

Just 20 Credits Consistently About 40% of Traded Quarterly Volume – Both 2009 and 2010

37%

38%

39%

40%

41%

42%

43%

Q1 Q2 Q3 Q4

2009 2010 Source: Morgan Stanley, MarketAxess

But what do we actually see trading in secondary markets? InExhibit 2, we track the percentage of overall trading volumseen in just the top 20 issuers since the markets began their rally early last year. Indeed, while the percentage of trading volume commanded by the top 20 issuers has climbed modestly this year, it has moved in a relatively narrow range from just about 39% to 42% over the last two years. Also,

e

e

ific

r, only 6 were issued before the last 6 months.

driven by a relatively xpect

a to

pecific exposure limits.

’t seem materially different from last year gauged by trading volumes, we are concerned that many, on both the buy-side and the sell-side, perceive just the opposite. With climbing expectations of a new round of quantitative easing that removes fixed income product from the market, and cross-asset correlations remaining high, the risk of crowded trades is growing (within and across assets). And crowded trades typically don’t end well. (For details see our Credit Basis Report of October 8. 2010.)

Exhibit 3

financials represent nearly 75% of the total of these top 20 issuers’ trading volume for the most recent quarter, whereas they make up 35% of the overall outstanding credit risk in benchmark indices. If you’re shunning financial risk, but looking to add non-financial credit risk, primary markets havadmittedly continued to be the path of least resistance.

Exhibit 3 breaks down the top 20 most actively traded specissues over the last two quarters. Two points worth noting.First, while these specific issues represent just 8.5% of theoverall volume in the most recent quarter, financials again dominate the list. Additionally, of these 20 issues in the most recent quarte

What are the portfolio implications? As noted above, we do think active primary markets can support both credit outperformance and a healthy secondary market, just as they do now, with secondary volumes today tracking right on top of daily volumes from a year ago. Alternatively, we push back at the perception that robust new-issue markets alone are a

precursor to sustained weakness in credit spreads. Since almost half of daily traded volume is small set of names (financials in particular), we would ethese specific names to serve as the ‘high beta’ credits in any bouts of volatility in the coming months. This will likely keep the pace of spread repair slower and more volatile than we expected a few months ago. Consolidation among financials that occurred during the crisis will also continue to serve asnegative technical, as investors will increasingly adhere name-s

Lastly, while overall market liquidity conditions don

Most Active Bonds Dominated by New Issues and Financials

3Q2010 3Q2009

# Ticker Coupon Maturity% of Mkt Ticker Coupon Maturity

% of Mkt

1 BAC 5.625 7/1/2020 0.91 C 8.500 5/22/2019 0.72

2 GS 6.000 6/15/2020 0.72 DOW 8.550 5/15/2019 0.57

3 MS 5.500 7/24/2020 0.68 C 6.375 8/12/2014 0.51

4 JPM 4.400 7/22/2020 0.62 BAC 7.625 6/1/2019 0.48

5 KFT 5.375 2/10/2020 0.45 C 8.125 7/15/2039 0.47

6 C 5.375 8/9/2020 0.44 PETBRA 7.875 3/15/2019 0.45

7 C 4.750 5/19/2015 0.40 GS 7.500 2/15/2019 0.39

8 GS 3.700 8/1/2015 0.40 BAC 6.500 8/1/2016 0.38

9 C 8.500 5/22/2019 0.38 MS 7.300 5/13/2019 0.34

10 APC 6.375 9/15/2017 0.37 JPM 6.300 4/23/2019 0.33

11 BPLN 5.250 11/7/2013 0.35 BAC 7.375 5/15/2014 0.32

12 BAC 3.700 9/1/2015 0.33 GS 6.750 10/1/2037 0.32

13 MS 4.000 7/24/2015 0.33 BACR 5.200 7/10/2014 0.30

14 GE 5.500 1/8/2020 0.33 GE 6.875 1/10/2039 0.29

15 DOW 8.550 5/15/2019 0.33 ORCL 5.000 7/8/2019 0.29

16 APC 5.950 9/15/2016 0.31 GE 6.000 8/7/2019 0.28

17 CS 4.375 8/5/2020 0.30 GE 5.875 1/14/2038 0.28

18 BHI 5.125 9/15/2040 0.30 GS 6.000 5/1/2014 0.26

19 AA 6.150 8/15/2020 0.29 MO 9.250 8/6/2019 0.26

20 GE 3.500 6/29/2015 0.29 T 5.800 2/15/2019 0.25

Source: MarketAxess

18

M O R G A N S T A N L E Y R E S E A R C H

October 14, 2010 Investment Perspectives — UK

Strategy and Economics

October 11, 2010

Commodity Strategy Natural Gas – Fundamentally Oversupplied

Hussein Allidina, CFA Morgan Stanley & Co.

Through 2011, oversupply will likely continue. We see 2011 natural gas prices averaging $4.00/mmBtu, as the US balance is fundamentally oversupplied and is likely to remain so through 2011. NYMEX futures are trading at ~$4.00/mmBtu, very different from the ~$14.00/mmBtu we saw in mid-2008. The root of today’s depressed price environment lies with elevated production, driven by robust horizontal drilling activity — the latest EIA data, covering July 2010, show US dry gas production averaging ~58.5 bcf/d, up 1.5 bcf/d year over year. The three key drivers of our bearish price outlook for 2011 are (1) the momentum of rig activity in

ed response of production to the

Incorporate

Stephen Richardson [email protected]

Tai Liu

recent months; (2) the lagglaying down of rigs; and (3) today’s elevated gas inventory.

Exhibit 1

We Are Bearish on 2011 Natural Gas ($/mmBtu) 2010 2011 201Forecast $4.36 $4.00 Forward $4.41 $4.57 $5.2

Note: Prices as of Oct. 8, 2010.

2 $5.50

5

Source: Bloomberg, Morgan Stanley Commodity Research estimates

Horizontal rig activity has rebounded strongly, averaging near 580 rigs, after hitting a trough of near 300 rigs in mid-2009. According to Smith Bits, some 880 rigs are activelydrilling for gas today (both horizontal and vertical). As a comparison, rig activity bottomed at ~610 in July 2009. W

e

0

expect the surge in rig activity and higher-productivity horizontal rigs to lift production in the months ahead.

In our base case, we assume rig activity declines to ~70by end-2010, and thereafter falls to ~630 by mid-2011. Under these assumptions, we see US gas production averaging ~59.4 bcf/d in 2010 and ~60.2 bcf/d in 2011. If actual rig activity turns out to be materially different from our assumptions (i.e., most likely we are too optimistic on the decline), we will have to adjust our production forecasts.

Due to a confluence of events, producers have continued to drill in the current low-gas-price environment. Unless

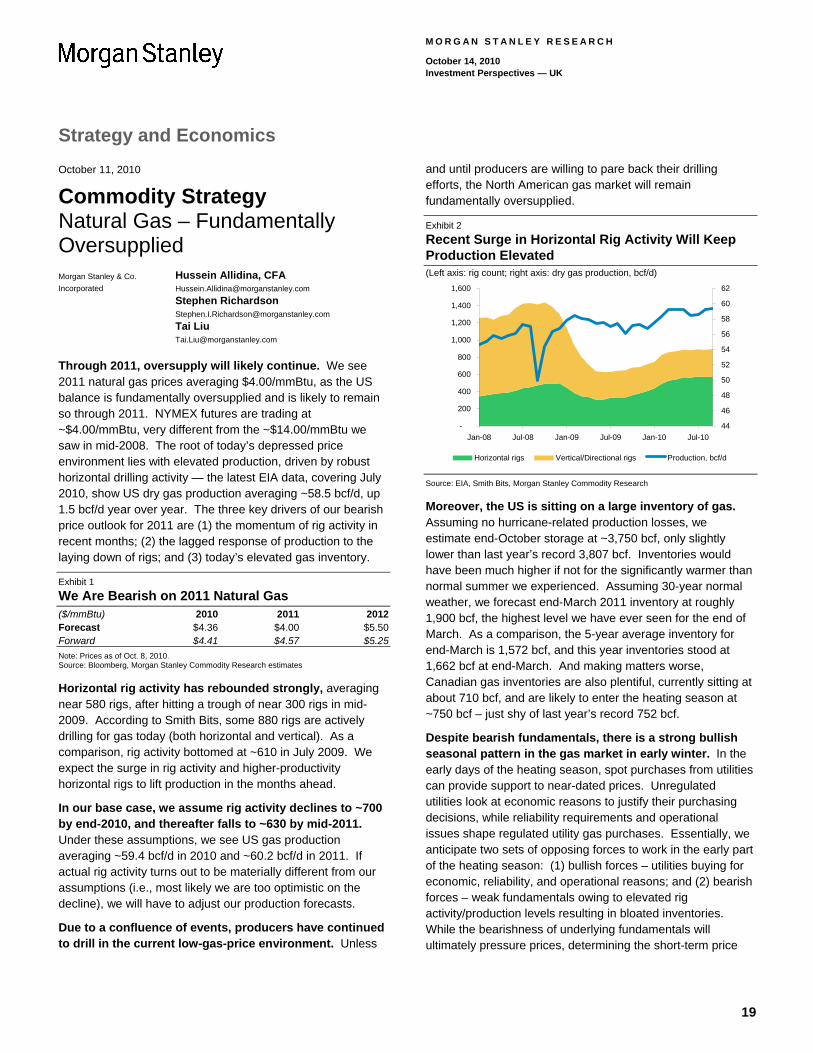

and until producers are willing to pare back their drilling efforts, the North American gas market will remain fundamentally oversupplied.

Exhibit 2

Recent Surge in Horizontal Rig Activity Will Keep Production Elevated (Left axis: rig count; right axis: dry gas production, bcf/d)

-

200

400

600

800

1,000

Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10

44

46

50

52

54

56

1,200

1,400

1,600

60

62

48

58

Horizontal rigs Vertical/Directional rigs Production, bcf/d

Source: EIA, Smith Bits, Morgan Stanley Co

mmodity Research

October storage at ~3,750 bcf, only slightly wer than las record 3,807 bcf. Inventories would

een much higher if r the significantly warmer than u e u -ywe ca M 011 inv y l

9 cf, th er f da As ar aver v o

rch i 7 r inve s6 cf at M ing mat o

ian g e tifu r n 710 b r the h g

y 5 f.

be e re is o sl p n t in e

ys o h pot pu e ivide ces. Unreg

look o e justify n, w ts an er

hap u l urchas sate tw ts es to w n eatin a rces – esic, r l l reas an weak f als o lev rig

on levels resulting in bloated inventories. While the bearishness of underlying fundamentals will ultimately pressure prices, determining the short-term price

Moreover, the US is sitting on a large inventory of gas.Assuming no hurricane-related production losses, we estimate end-lohave b

t year’snot foncenormal s mmer we experi d. Ass ming 30 ear normal