Embed Size (px)

Citation preview

‘Sensibilité d’une rente viagère à l’extrapolationde la courbe des taux dans un contexte LTGA’,

JIRF 2015

Thierry Moudiki (ISFA, Université Lyon 1)

May 21st, 2015

Solvency II economic balance sheet, technical provisions

I Solvency II? QIS5? LTGA?I Simplified balance sheet

Assets Liabilities

Assets - Available capitalat - Solvency Capital Requirement (SCR)market - Risk Marginvalue - Best Estimate Liabilities

I ‘Fair’ valuation ∼ Assets marked to market + Liabilitiesmarked to model

I Technical provisions = Best Estimate Liabilities + RiskMargin

Best Estimate Liabilities (BEL) explained

BELt =∑T

E[D(t,T )CFT |Ft ⊗ Tt ]

I D(t,T ): stochastic discount factorI CFT : future cash-flowsI Ft ⊗ Tt : financial and technical information at tI Simple case: CFT deterministic/highly predictableI Difficult case: CFT depending on financial and technical

information

In the article:

I CFT : deterministic, mortality risk mutualizedI d(t,T ) := E[D(t,T )|Ft ] = ? = critical input

Solvency II term structure of discount factorsHow to derive d(t,T ) within Solvency II?

Liquid part

I Par swap ratesI Parallel shift for credit risk deduction (10 bps)I + Volatility adjustment (optional)I + Matching adjustment (optional)

Extrapolated part

I Last Liquid Point (LLP)I Ultimate Forward Rate (UFR)I Convergence speed (α) ∼ convergence period (years)I Bootstrap, interpolation, extrapolation: Smith-Wilson

Solvency II term structure of discount factors (cont’d)

Solvency II interpolation/extrapolation explained

Solvency II term structure of discount factors (cont’d)

UFR?

I Endogeneous UFR = f∞ = f∞(t)I Vasicek-Fong (1982): French Institute of Actuaries

d(t, s) =∑

mβm,se−mf∞(s−t)

I Nelson & Siegel (1987) or Svensson (1994): Central Banks

d(t, s) = exp (−(s − t) (f∞ + β1K1(t, s) + β2K2(t, s)))

I Exogeneous UFR = f∞ = constantI Smith-Wilson (2001): Solvency II

d(t, s) = e−f∞(s−t) +∑

mβmKm(t, s)

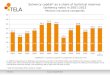

Solvency II term structure of discount factors (cont’d)I Problem with an endogeneous UFR: potential volatility

induced in liabilitiesI ECB data; calibration with Svensson method (Blue = AAA

Bonds, Red = All Bonds)

2004 2006 2008 2010 2012 2014

01

23

45

67

Calibration date

UF

R

Solvency II term structure of discount factors (cont’d)

The case for a fixed exogeneous UFR for insurance

I High demand on long-term swaps from pension funds,artificially driving long rates down?

I More stable liabilities valuationI UFR = Expected inflation + Expected real interest ratesI UFR = fixed since 5 years = 4.2% = 2% + 2.2%

Results from the article

Based on a fixed annuity valuation

I Fixed cash-flows depending on a mortality table (mutualizedmortality risk)

I Additional benefits cash-flows depending of implied forwardI Aggregated cash-flows discounted, using Smith-Wilson for,

interpolation and extrapolation (swap curve at 12/31/2011)

Results on the valuation

1. On interpolation with a ‘complicated’ (realistic, but not socommon) benchmark curve

2. On the dependence with UFR and convergence speed3. On the dependence with LLP and convergence speed

Results from the article (cont’d)On interpolation

Implied forwards on “A Curve where all cubic splines producenegative rates” (Hagan & West (2006))

Results from the article (cont’d)On interpolation (cont’d)

Results from the article (cont’d)Extrapolation: UFR/convergence speed dependence (fixedLLP = 20)

Results from the article (cont’d)Extrapolation: Cv. speed/LLP dependence (UFR = 4.2%)

Results from the article

A ‘Shiny App’ showing the impact of LLP, UFR and α on aannuity

I Just run the following commands in R (internet connexionrequired, tested on Safari and Chrome)

# Loading Shiny packagelibrary(shiny)# Run the app in your browser; execs code from my GistrunGist("ee4e7b9506a09e5d7cb8")

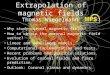

“Problem” with an exogeneous UFRI Hedging current UFR (increasing basis with low rates)?I Reasonable macroeconomic assumptions (2%+2.2%) ?

UFR implied vs market implied forwards rates on EUR swap curves

impl

ied

forw

ard

rate

s

0 5 10 15 20 25 30

0.00

0.01

0.02

0.03

0.04

20132014

Future work

I About the inclusion of insurer’s assets returns in a frameworkI On interpolation/extrapolation for valuationI On forecasting for the ORSA (Own Risk Solvency Assessment,

Solvency II pillar 2)I On low interest rates impacts