Embed Size (px)

Citation preview

Investment Risk Management

Under New Regulatory Framework

Steven Yang Yu

Muqiu Liu

Redington Ltd

08 May 2015

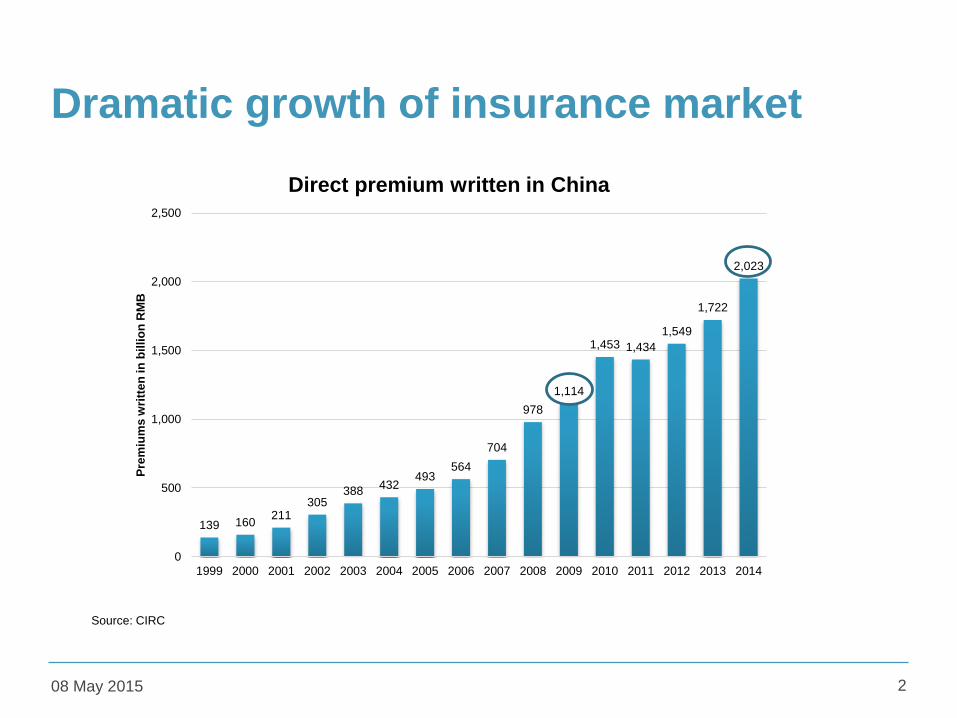

Dramatic growth of insurance market

08 May 2015 2

139 160211

305388

432493

564

704

978

1,114

1,453 1,434

1,549

1,722

2,023

0

500

1,000

1,500

2,000

2,500

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Pre

miu

ms

wri

tte

n in

bil

lio

n R

MB

Direct premium written in China

Source: CIRC

4th largest globally

08 May 2015 3

1,259

532

330278 255 247

169 145 125 101

0

200

400

600

800

1,000

1,200

1,400

Pre

miu

ms

wri

tte

n in

bil

lio

n U

.S.

do

lla

rs

Direct premium written by countries 2013

Ping An Insurance is one of the 9 Globally Systematically Important Insurers (G-SIIs) in the world!

Source: Statista

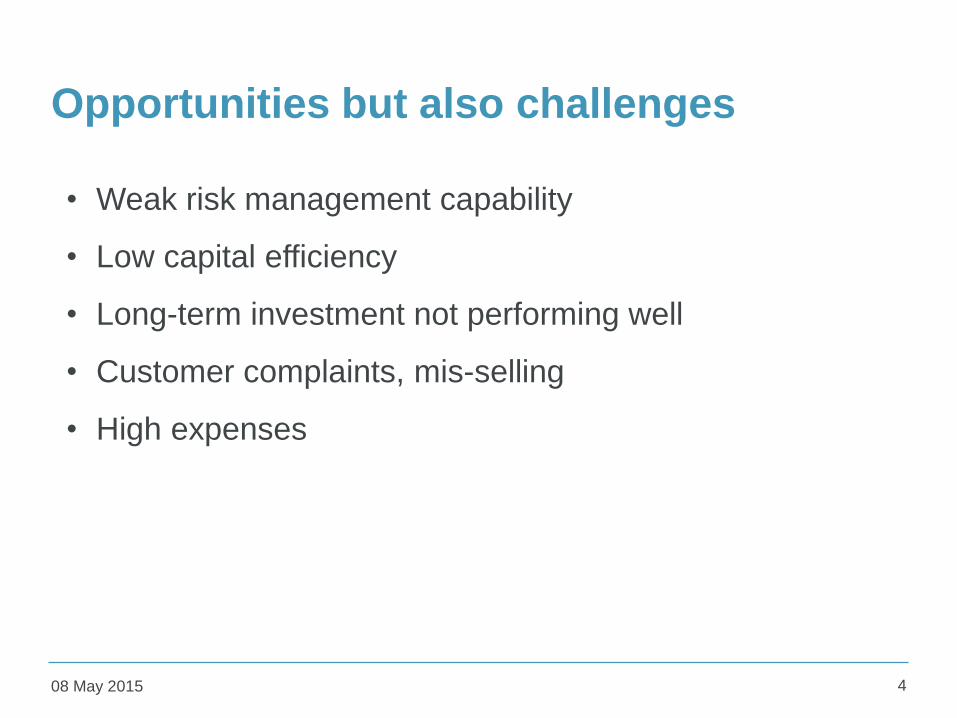

Opportunities but also challenges

08 May 2015 4

• Weak risk management capability

• Low capital efficiency

• Long-term investment not performing well

• Customer complaints, mis-selling

• High expenses

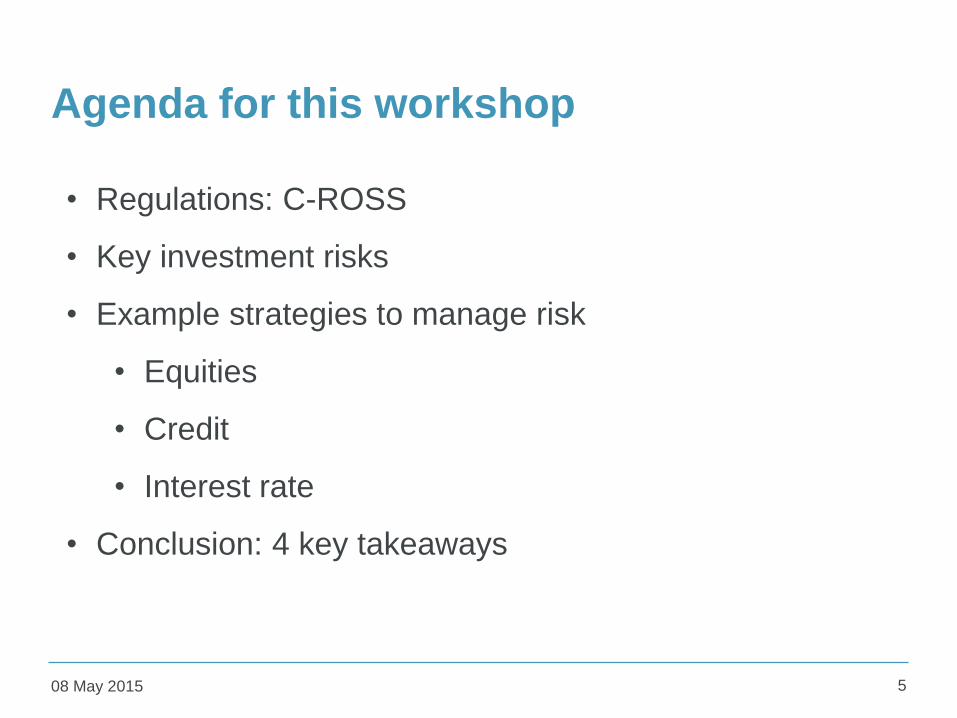

Agenda for this workshop

08 May 2015 5

• Regulations: C-ROSS

• Key investment risks

• Example strategies to manage risk

• Equities

• Credit

• Interest rate

• Conclusion: 4 key takeaways

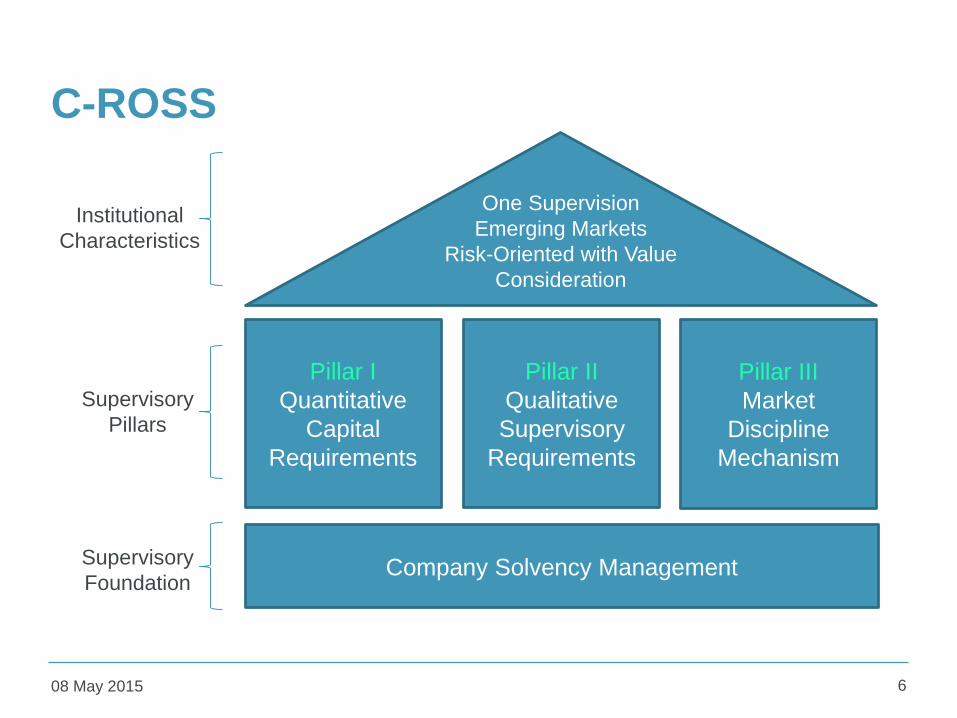

C-ROSS

08 May 2015 6

Pillar I

Quantitative

Capital

Requirements

Pillar II

Qualitative

Supervisory

Requirements

Pillar III

Market

Discipline

Mechanism

Company Solvency Management

One Supervision

Emerging Markets

Risk-Oriented with Value

Consideration

Institutional

Characteristics

Supervisory

Pillars

Supervisory

Foundation

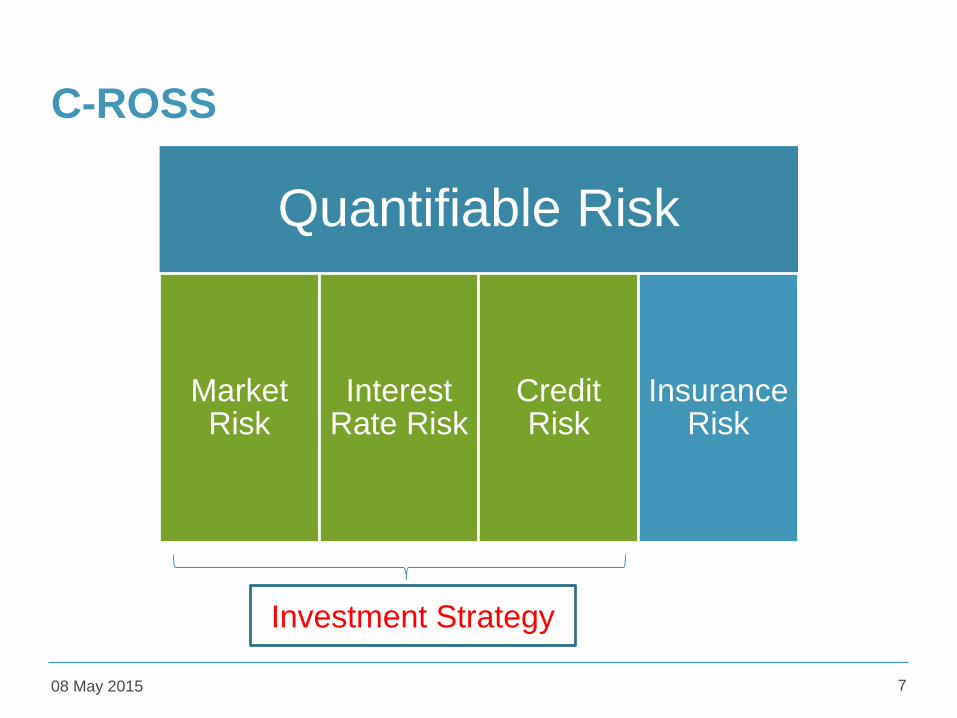

C-ROSS

08 May 2015 7

Quantifiable Risk

Market Risk

Interest Rate Risk

Credit Risk

Insurance Risk

Investment Strategy

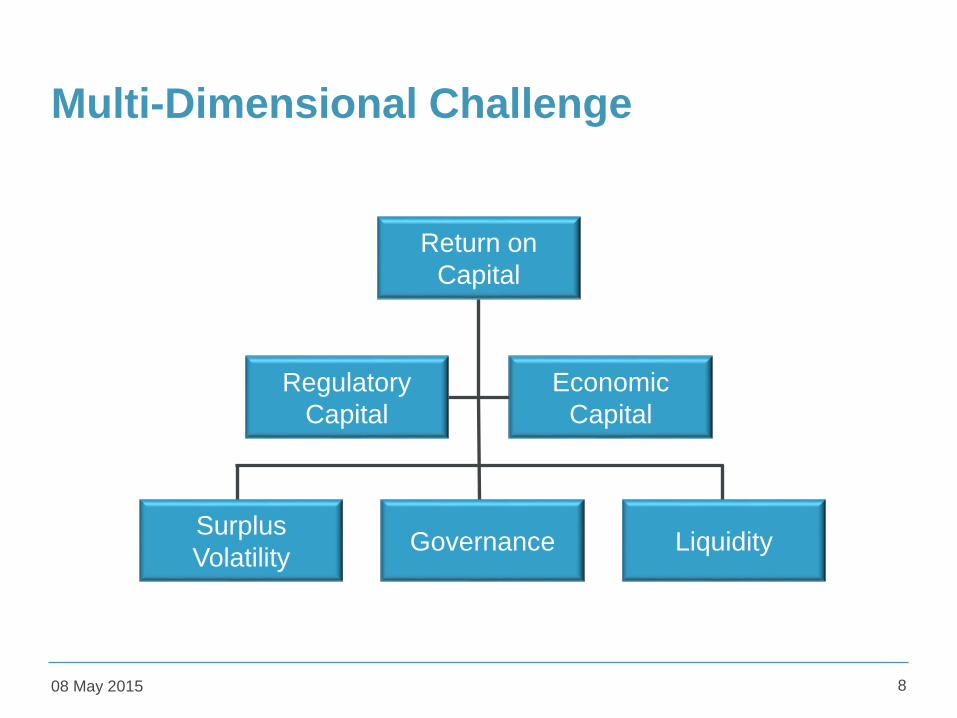

Multi-Dimensional Challenge

08 May 2015 8

Return on

Capital

Regulatory

Capital

Economic

Capital

GovernanceSurplus

VolatilityLiquidity

Investment Risk Management Framework

08 May 2015 9

Objective Measurement Quantification Action

ReturnExpected return > Shareholder

required return on capital

Expected return on capital 13.5%

-Required return on capital 12.0%

Margin (Expected return less required return) 1.5%

Risk / Capital Current capital > required capital

Economic basis

Current capital budget £1,150m

-Required capital (VaR

99.5%)£1,020m

Regulatory basis

Current capital budget £1,300Bring current capital in line

with required capitalRequired capital (VaR

99.5%)£1,350

Liquidity

The company should hold enough

eligible assets to cover additional

liquidity requirements in an adverse

scenario

Available liquid asset £400m

-

5 year cashflows if lapse rate increases by 20% £250m

Asset allocation

target

benchmark

The current asset allocation is to be

kept within +/- 5% of the target

benchmark allocation

Government bonds 20% 36.2%

Allocate out of overweight

assets into relatively

underweight assets to

bring in line with target

benchmark allocations

Corporate bonds 10% 10.5%

Equity 35% 27.0%

Property 5% 6.3%

Other assets 30% 26.0%

On track Within 10% of target Off track

Equity Risk Management

08 May 2015

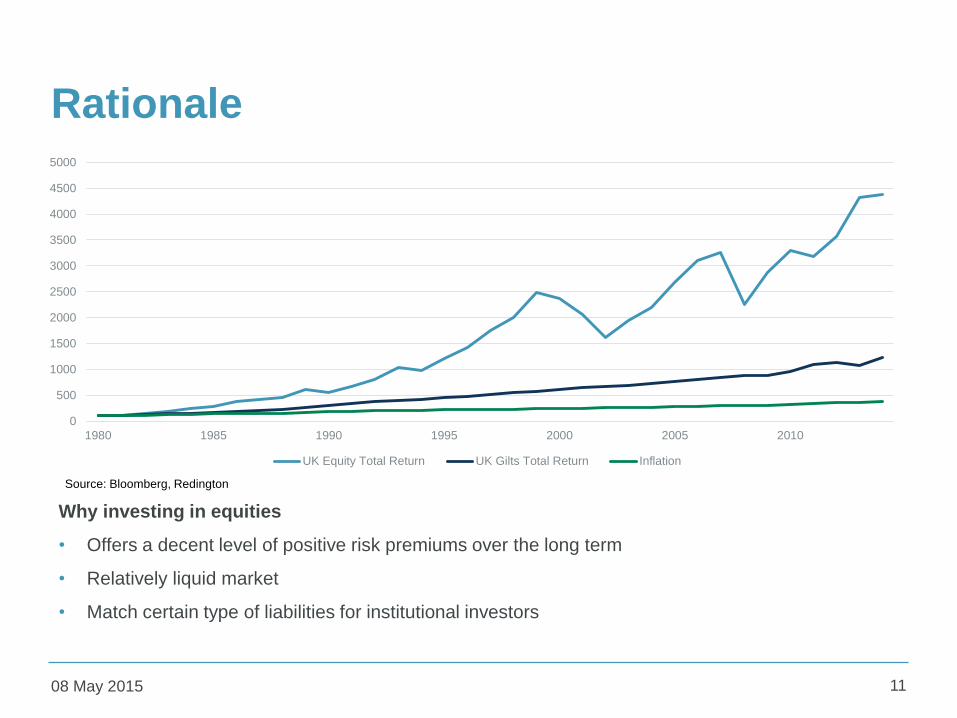

Rationale

08 May 2015 11

Why investing in equities

• Offers a decent level of positive risk premiums over the long term

• Relatively liquid market

• Match certain type of liabilities for institutional investors

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

1980 1985 1990 1995 2000 2005 2010

UK Equity Total Return UK Gilts Total Return Inflation

Source: Bloomberg, Redington

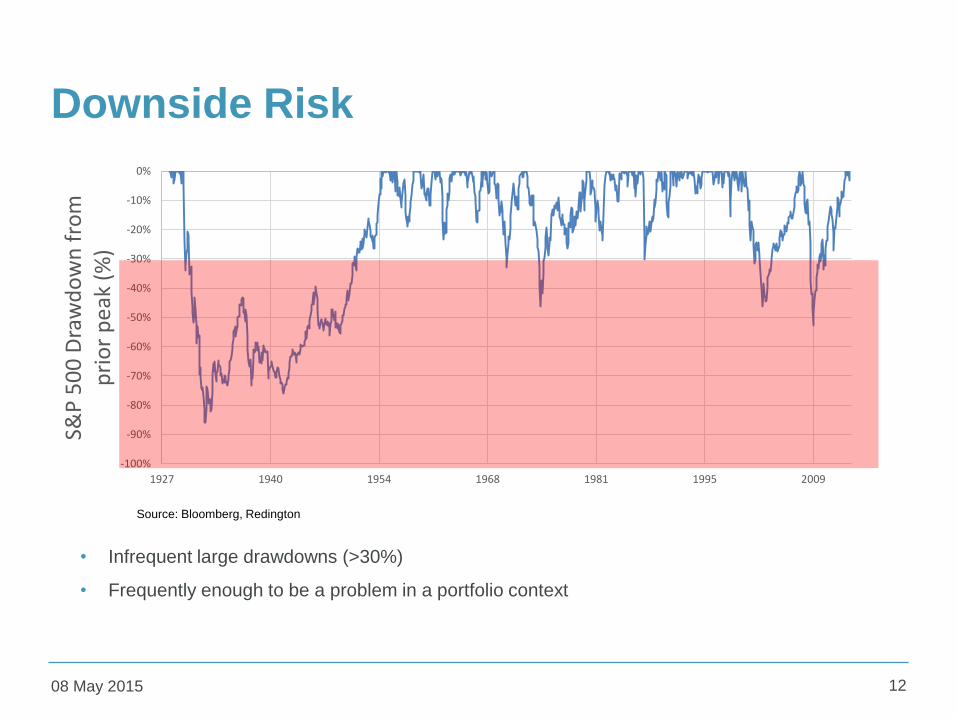

Downside Risk

• Infrequent large drawdowns (>30%)

• Frequently enough to be a problem in a portfolio context

08 May 2015 12

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

1927 1940 1954 1968 1981 1995 2009

S&P

50

0 D

raw

do

wn

fro

m

pri

or

pe

ak (

%)

Source: Bloomberg, Redington

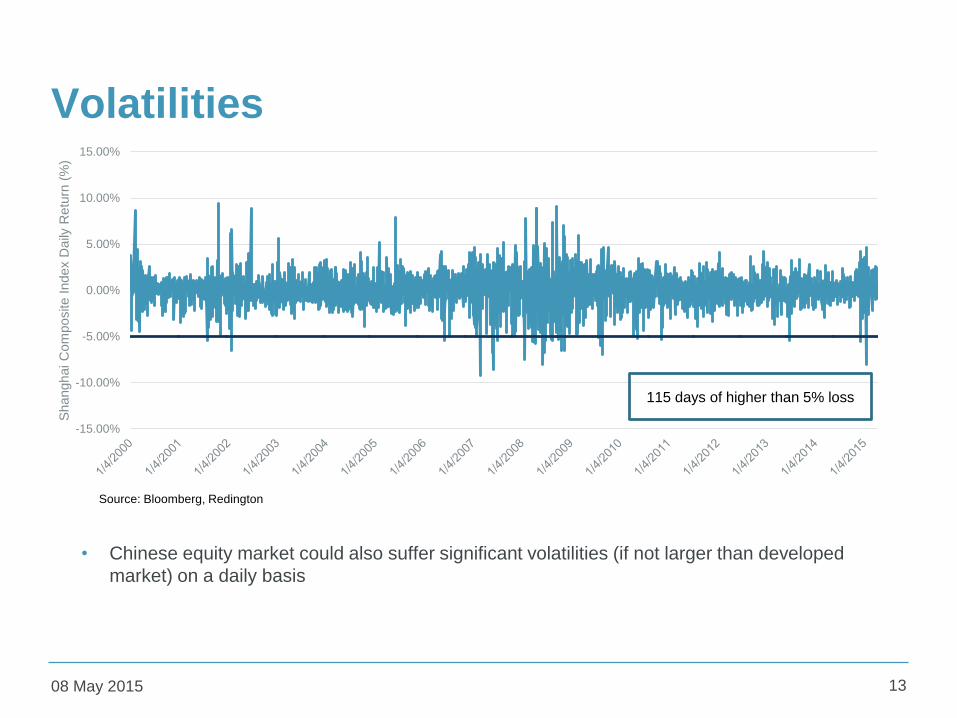

Volatilities

• Chinese equity market could also suffer significant volatilities (if not larger than developed

market) on a daily basis

08 May 2015 13

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Shanghai C

om

posite I

ndex D

aily

Retu

rn (

%)

Source: Bloomberg, Redington

115 days of higher than 5% loss

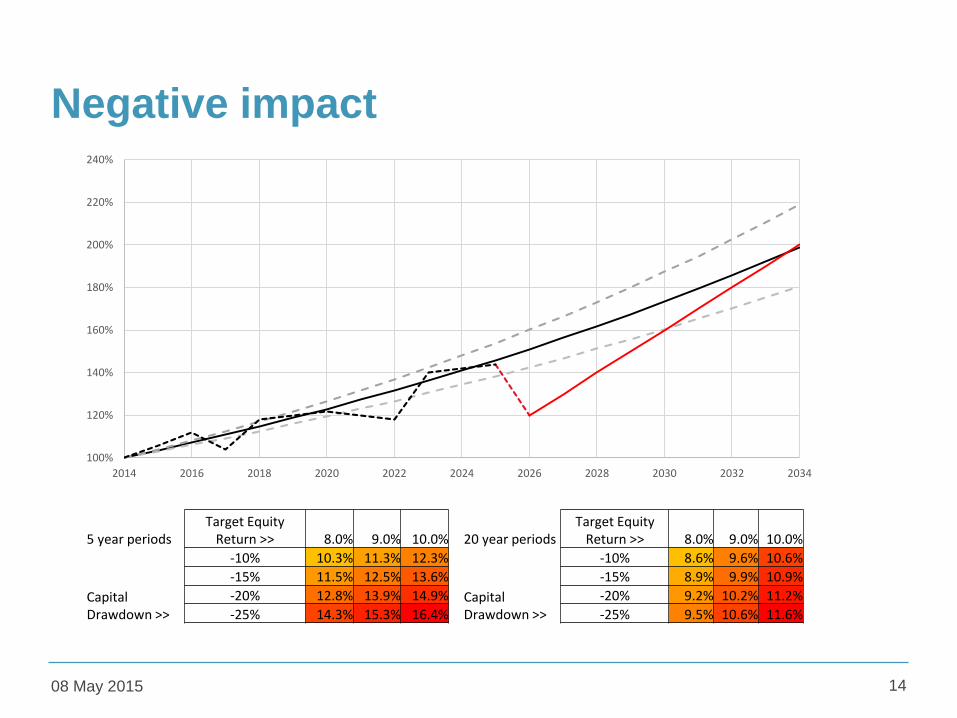

Negative impact

08 May 2015 14

100%

120%

140%

160%

180%

200%

220%

240%

2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034

5 year periodsTarget Equity

Return >> 8.0% 9.0% 10.0%

Capital Drawdown >>

-10% 10.3% 11.3% 12.3%

-15% 11.5% 12.5% 13.6%

-20% 12.8% 13.9% 14.9%

-25% 14.3% 15.3% 16.4%

20 year periodsTarget Equity

Return >> 8.0% 9.0% 10.0%

Capital Drawdown >>

-10% 8.6% 9.6% 10.6%

-15% 8.9% 9.9% 10.9%

-20% 9.2% 10.2% 11.2%

-25% 9.5% 10.6% 11.6%

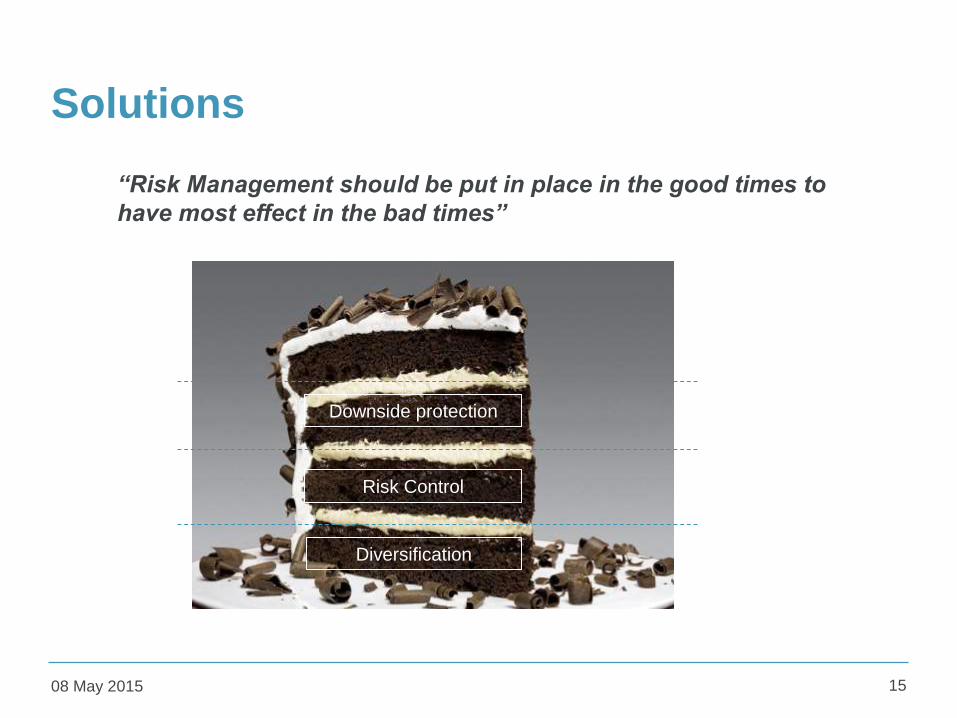

Solutions

08 May 2015 15

Diversification

Downside protection

Risk Control

“Risk Management should be put in place in the good times to

have most effect in the bad times”

5.00%

5.50%

6.00%

6.50%

7.00%

7.50%

8.00%

1.5% 3.5% 5.5% 7.5% 9.5% 11.5% 13.5% 15.5% 17.5% 19.5%

EX

pe

cte

d R

etu

rn

Risk (measured by standard deviation of annual returns)

Efficient Frontier

1. Diversification

08 May 2015 16

Concentrated equity

portfolio

50% DM Equity

10% EM Equity

30% Alternatives

40% DM Equity

0% EM Equity

60% Alternatives

50% DM Equity

30% EM Equity

20% Alternatives

20% DM Equity

80% EM Equity

0% Alternatives

Source: Redington

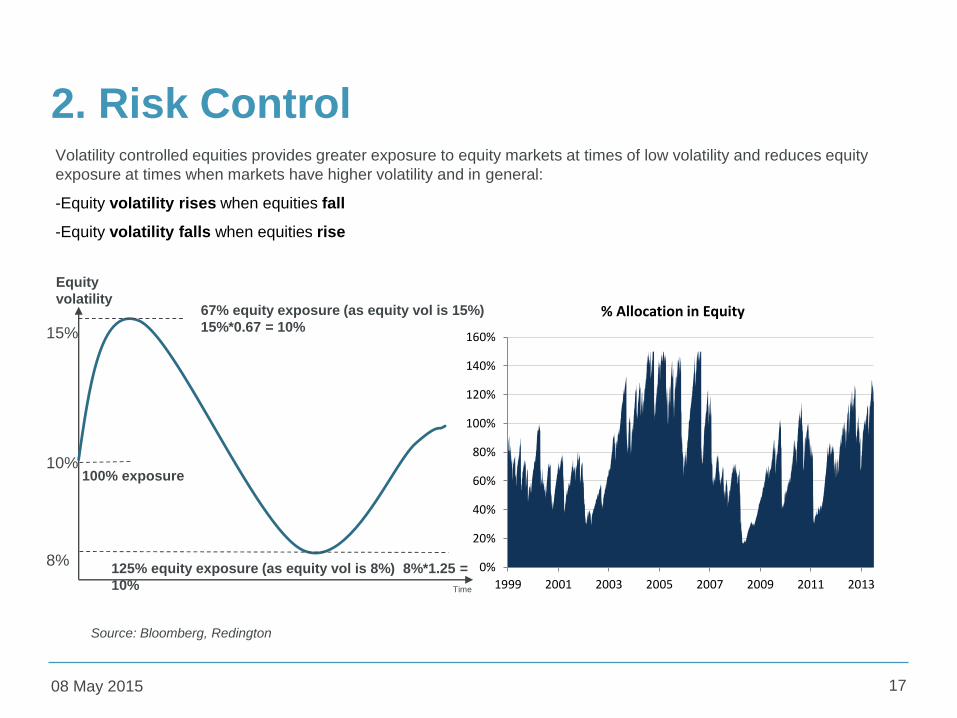

2. Risk Control

08 May 2015 17

Source: Bloomberg, Redington

Volatility controlled equities provides greater exposure to equity markets at times of low volatility and reduces equity

exposure at times when markets have higher volatility and in general:

-Equity volatility rises when equities fall

-Equity volatility falls when equities rise

Equity

volatility

100% exposure

67% equity exposure (as equity vol is 15%)

15%*0.67 = 10%

125% equity exposure (as equity vol is 8%) 8%*1.25 =

10% Time

0%

20%

40%

60%

80%

100%

120%

140%

160%

1999 2001 2003 2005 2007 2009 2011 2013

% Allocation in Equity

15%

10%

8%

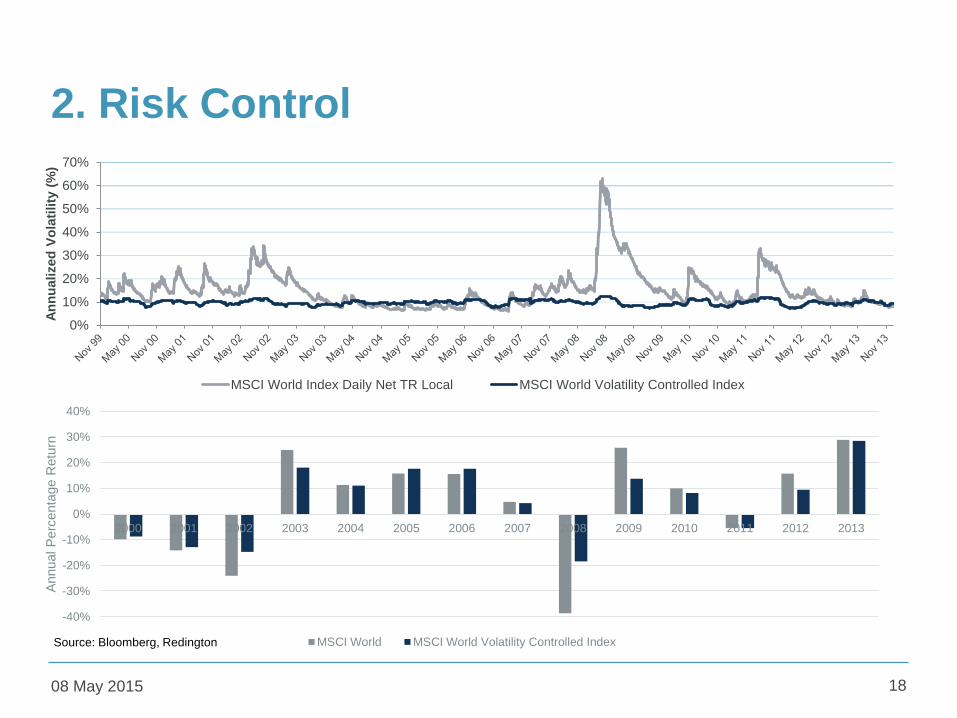

2. Risk Control

08 May 2015 18

0%

10%

20%

30%

40%

50%

60%

70%

An

nu

alized

Vo

lati

lity

(%

)

MSCI World Index Daily Net TR Local MSCI World Volatility Controlled Index

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Annual P

erc

enta

ge R

etu

rn

MSCI World MSCI World Volatility Controlled IndexSource: Bloomberg, Redington

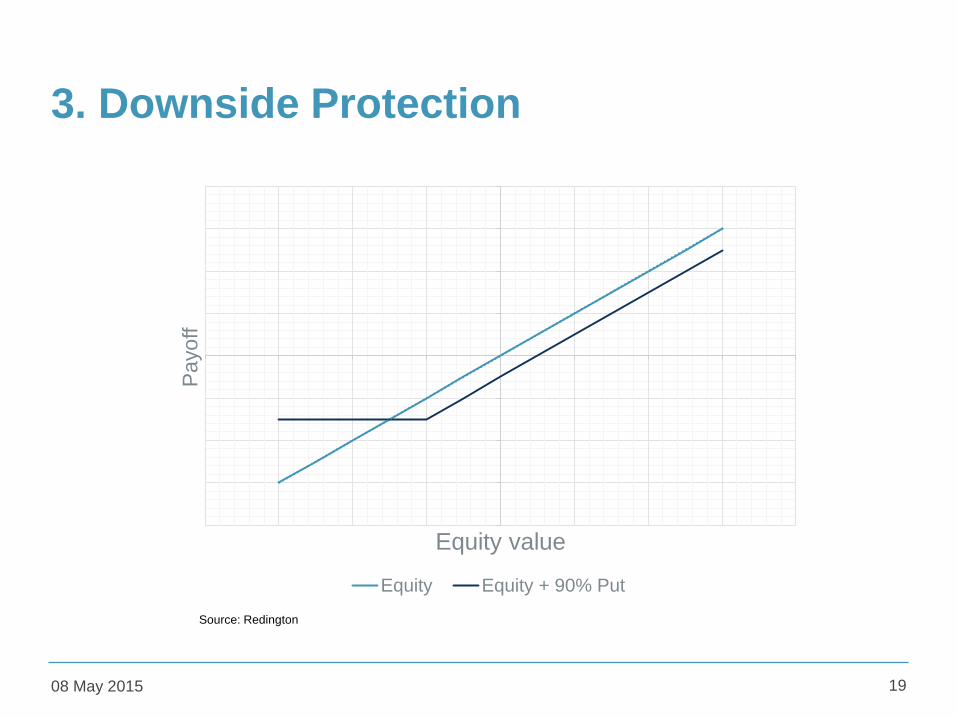

3. Downside Protection

08 May 2015 19

Payoff

Equity value

Equity Equity + 90% Put

Source: Redington

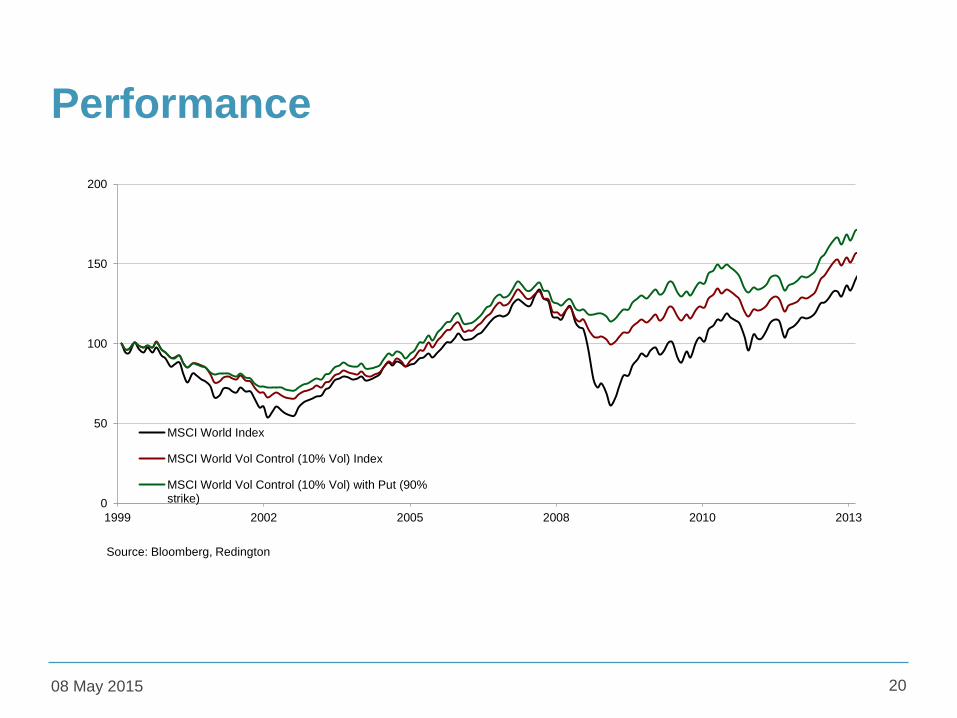

Performance

08 May 2015 20

0

50

100

150

200

1999 2002 2005 2008 2010 2013

MSCI World Index

MSCI World Vol Control (10% Vol) Index

MSCI World Vol Control (10% Vol) with Put (90%strike)

Source: Bloomberg, Redington

Credit Optimization

08 May 2015

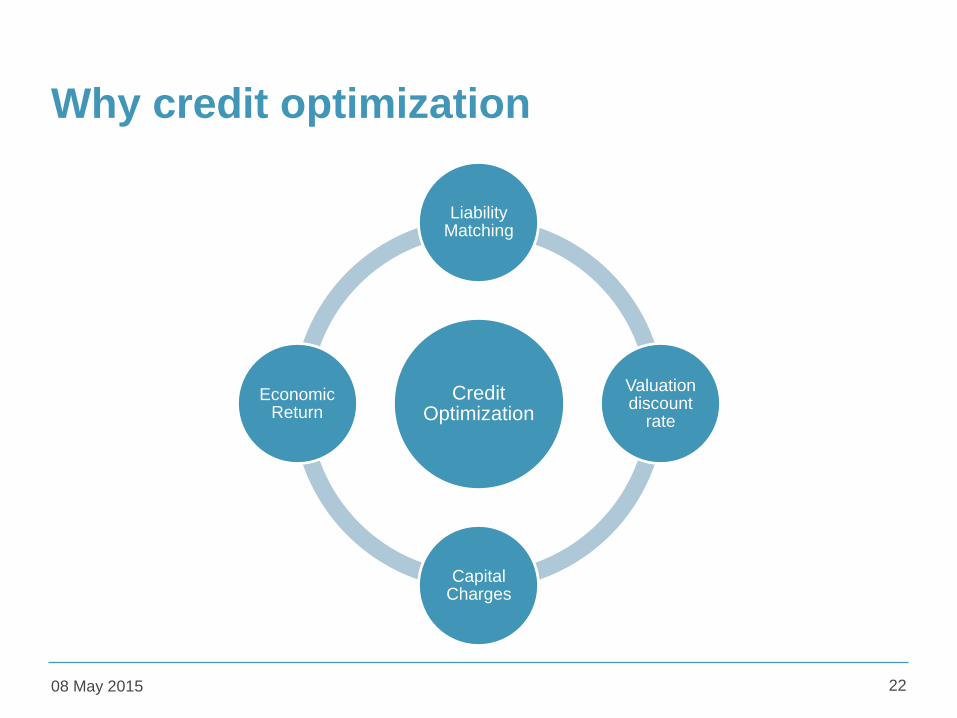

Why credit optimization

08 May 2015 22

Credit Optimization

Liability Matching

Valuation discount

rate

Capital Charges

Economic Return

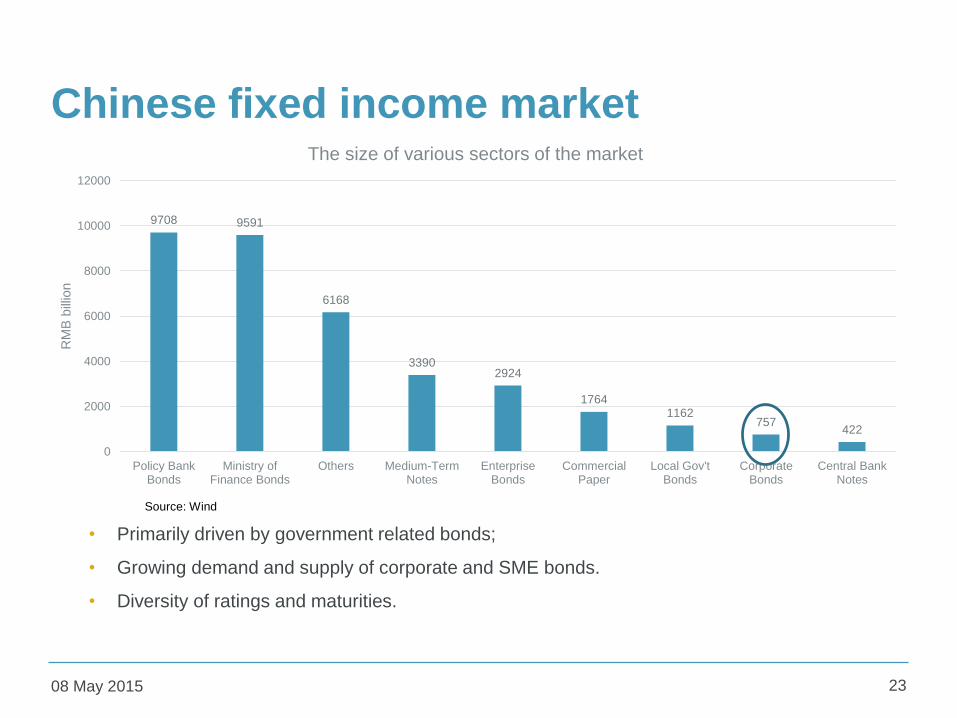

Chinese fixed income market

08 May 2015 23

• Primarily driven by government related bonds;

• Growing demand and supply of corporate and SME bonds.

• Diversity of ratings and maturities.

9708 9591

6168

33902924

17641162

757422

0

2000

4000

6000

8000

10000

12000

Policy BankBonds

Ministry ofFinance Bonds

Others Medium-TermNotes

EnterpriseBonds

CommercialPaper

Local Gov'tBonds

CorporateBonds

Central BankNotes

RM

B b

illio

n

The size of various sectors of the market

Source: Wind

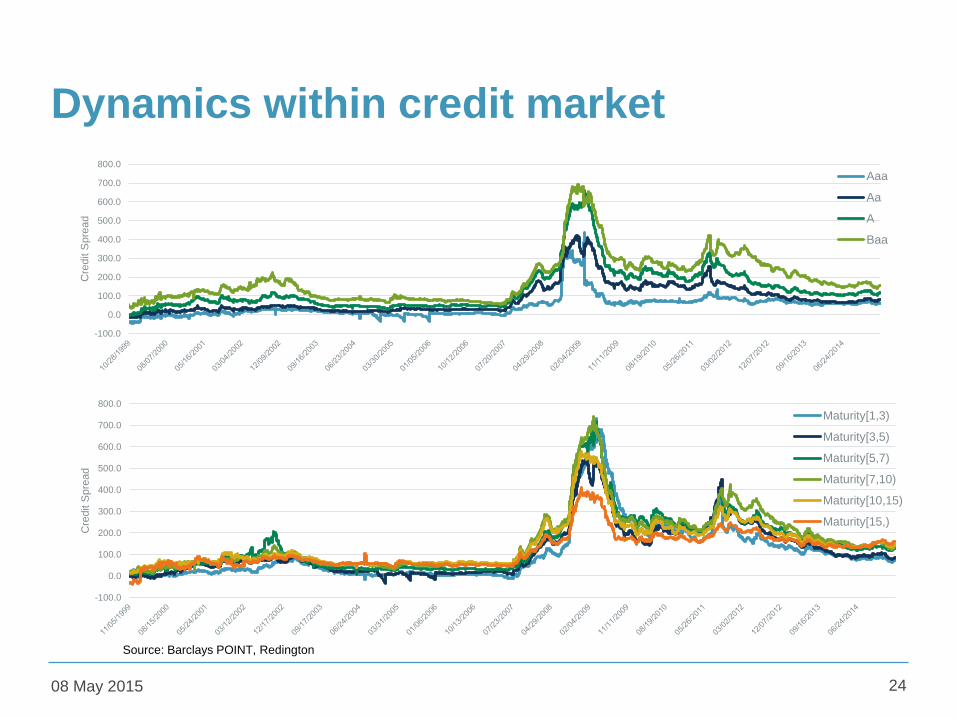

Dynamics within credit market

08 May 2015 24

-100.0

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

Cre

dit S

pre

ad

Aaa

Aa

A

Baa

-100.0

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

Cre

dit S

pre

ad

Maturity[1,3)

Maturity[3,5)

Maturity[5,7)

Maturity[7,10)

Maturity[10,15)

Maturity[15,)

Source: Barclays POINT, Redington

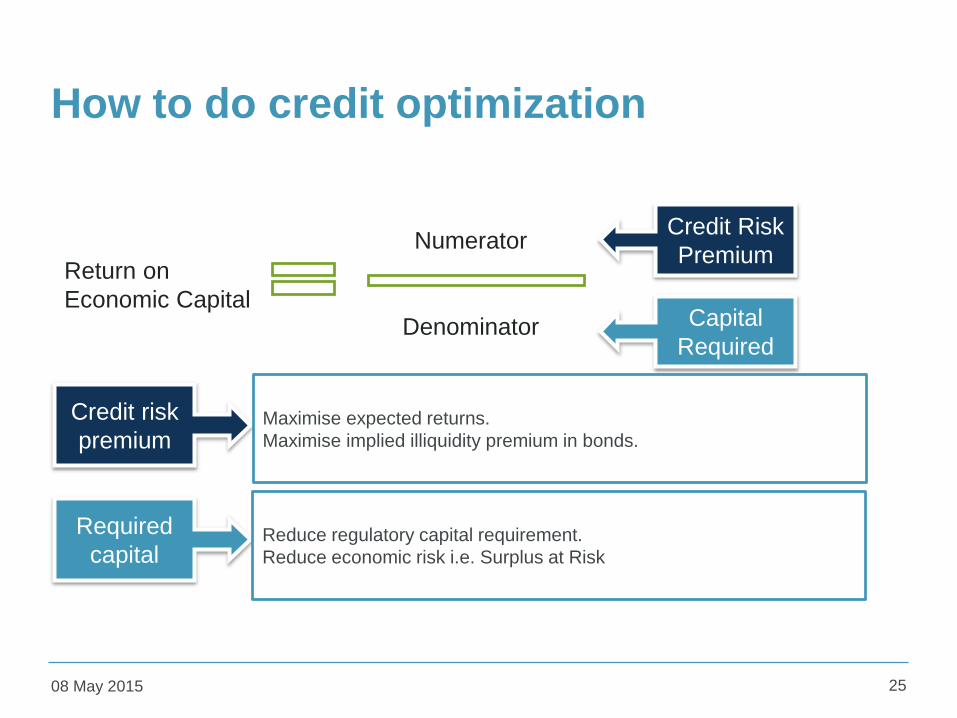

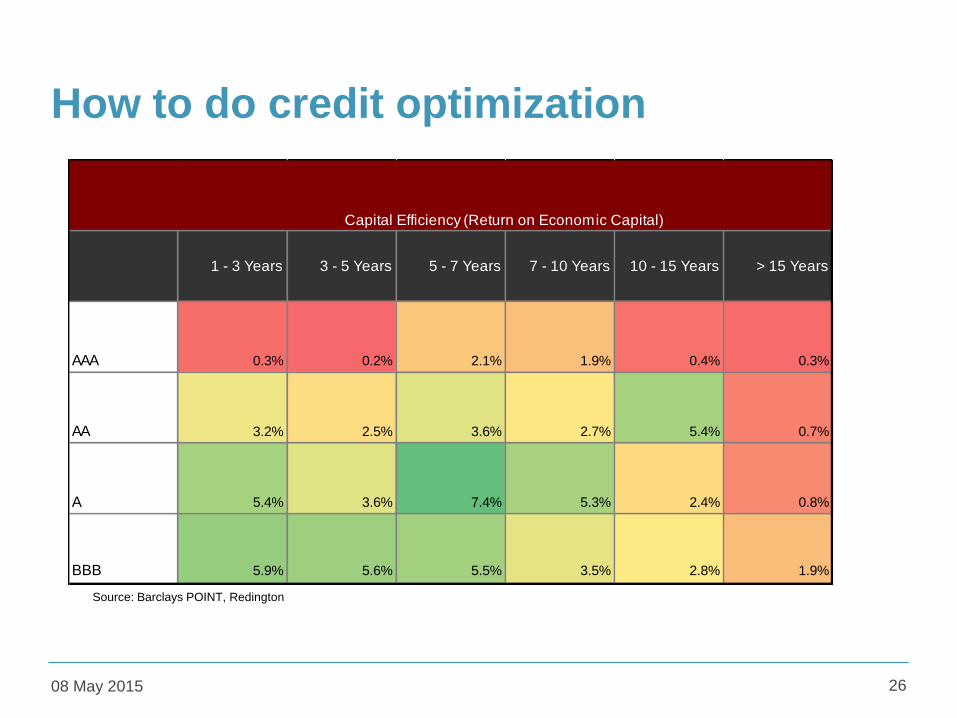

How to do credit optimization

08 May 2015 25

Return on

Economic Capital

Credit risk

premium

Required

capital

Numerator

Denominator

Credit Risk

Premium

Capital

Required

Maximise expected returns.

Maximise implied illiquidity premium in bonds.

Reduce regulatory capital requirement.

Reduce economic risk i.e. Surplus at Risk

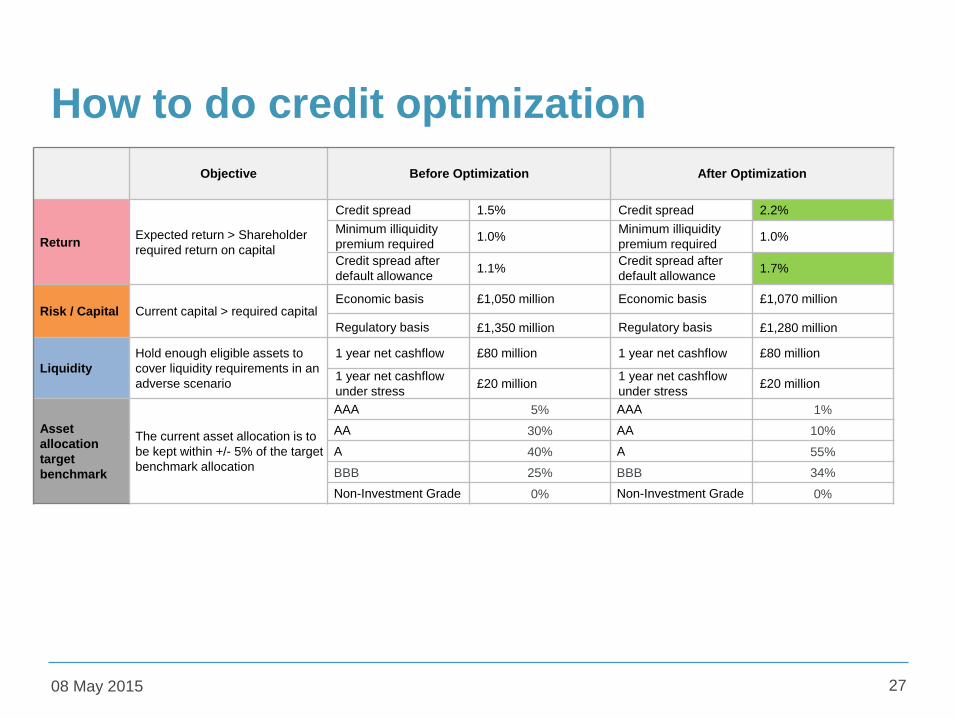

How to do credit optimization

08 May 2015 26

Source: Barclays POINT, Redington

1 - 3 Years 3 - 5 Years 5 - 7 Years 7 - 10 Years 10 - 15 Years > 15 Years

AAA 0.3% 0.2% 2.1% 1.9% 0.4% 0.3%

AA 3.2% 2.5% 3.6% 2.7% 5.4% 0.7%

A 5.4% 3.6% 7.4% 5.3% 2.4% 0.8%

BBB 5.9% 5.6% 5.5% 3.5% 2.8% 1.9%

Capital Efficiency (Return on Economic Capital)

How to do credit optimization

08 May 2015 27

Objective Before Optimization After Optimization

ReturnExpected return > Shareholder

required return on capital

Credit spread 1.5% Credit spread 2.2%

Minimum illiquidity

premium required1.0%

Minimum illiquidity

premium required1.0%

Credit spread after

default allowance1.1%

Credit spread after

default allowance1.7%

Risk / Capital Current capital > required capitalEconomic basis £1,050 million Economic basis £1,070 million

Regulatory basis £1,350 million Regulatory basis £1,280 million

Liquidity

Hold enough eligible assets to

cover liquidity requirements in an

adverse scenario

1 year net cashflow £80 million 1 year net cashflow £80 million

1 year net cashflow

under stress£20 million

1 year net cashflow

under stress£20 million

Asset

allocation

target

benchmark

The current asset allocation is to

be kept within +/- 5% of the target

benchmark allocation

AAA 5% AAA 1%

AA 30% AA 10%

A 40% A 55%

BBB 25% BBB 34%

Non-Investment Grade 0% Non-Investment Grade 0%

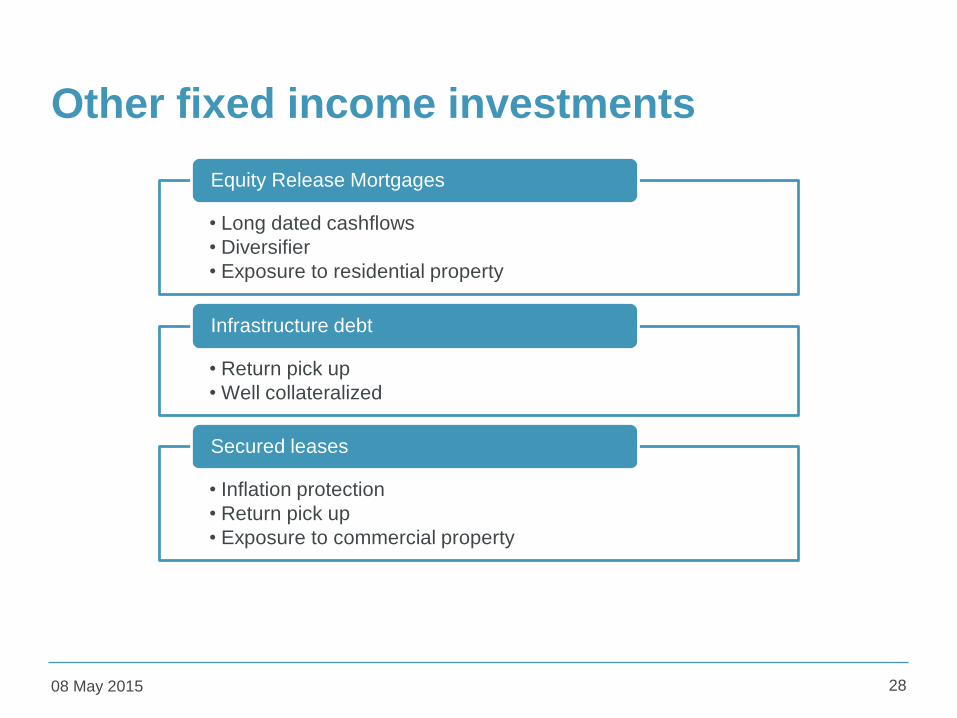

Other fixed income investments

08 May 2015 28

• Long dated cashflows

• Diversifier

• Exposure to residential property

Equity Release Mortgages

• Return pick up

• Well collateralized

Infrastructure debt

• Inflation protection

• Return pick up

• Exposure to commercial property

Secured leases

Managing Interest Rate Risk

08 May 2015

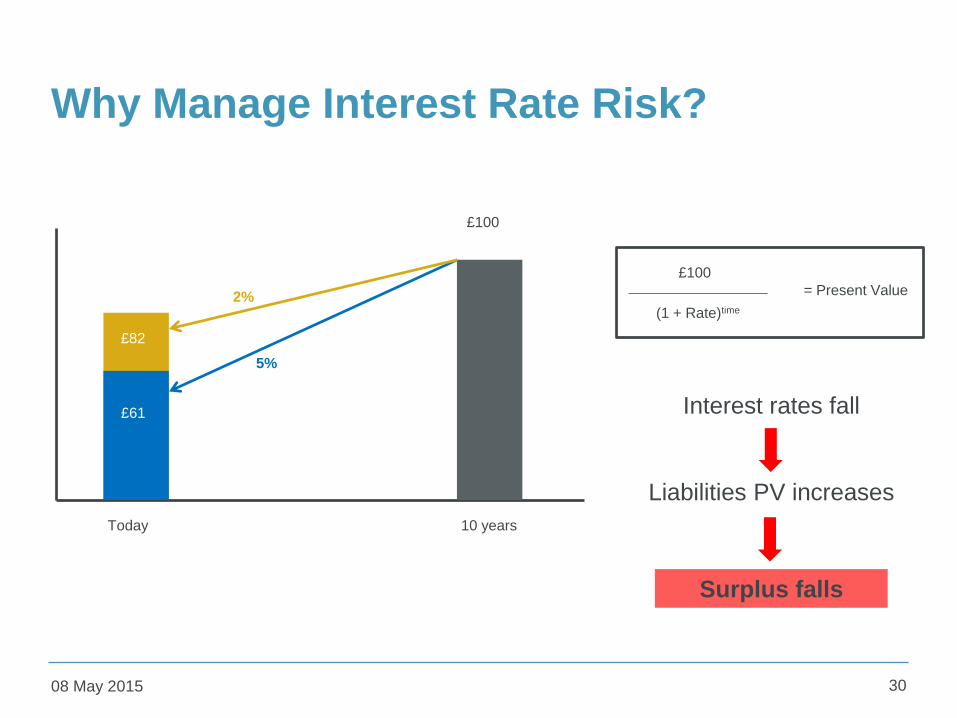

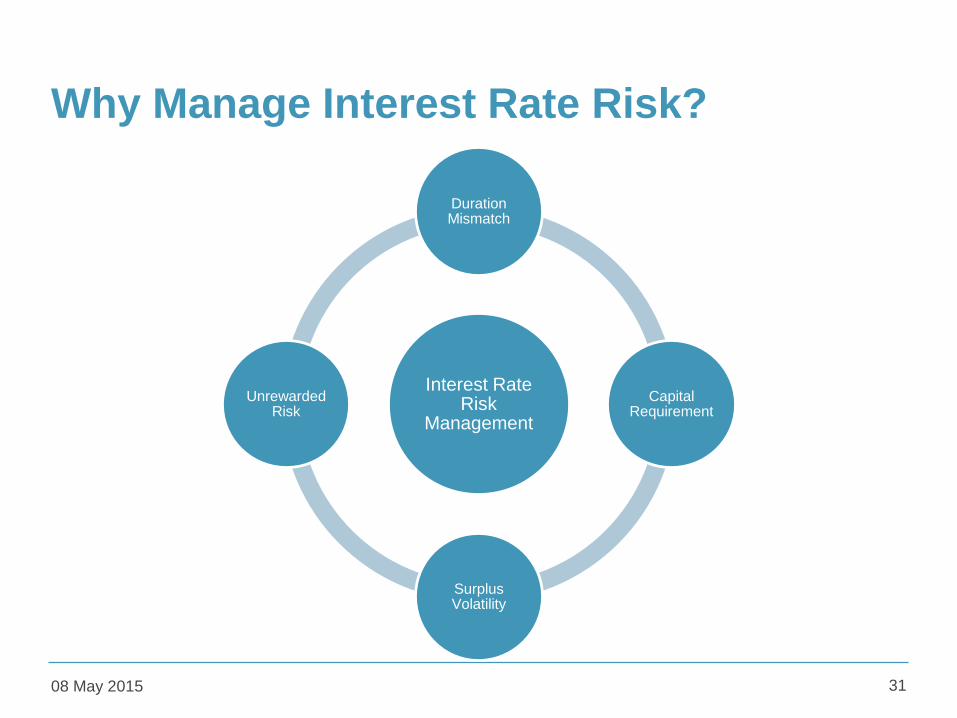

Why Manage Interest Rate Risk?

08 May 2015 30

Interest rates fall

Liabilities PV increases

Surplus falls

10 years

£100

£61

£82

Today

2%

5%

£100

(1 + Rate)time

= Present Value

Why Manage Interest Rate Risk?

08 May 2015 31

Interest Rate Risk

Management

Duration Mismatch

Capital Requirement

Surplus Volatility

Unrewarded Risk

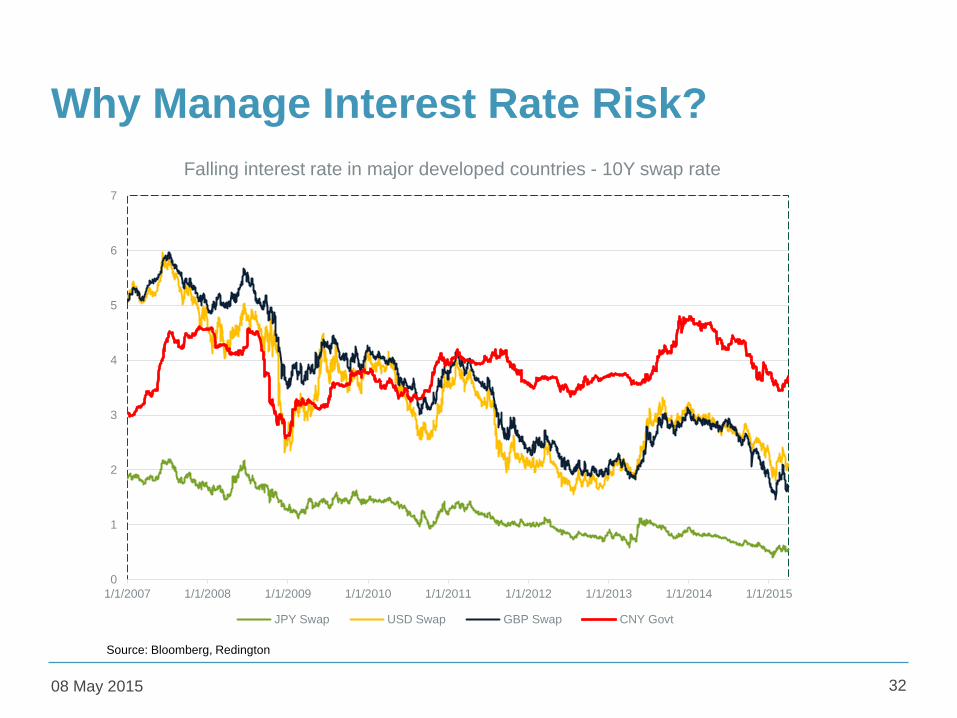

Why Manage Interest Rate Risk?

08 May 2015 32

0

1

2

3

4

5

6

7

1/1/2007 1/1/2008 1/1/2009 1/1/2010 1/1/2011 1/1/2012 1/1/2013 1/1/2014 1/1/2015

Falling interest rate in major developed countries - 10Y swap rate

JPY Swap USD Swap GBP Swap CNY Govt

Source: Bloomberg, Redington

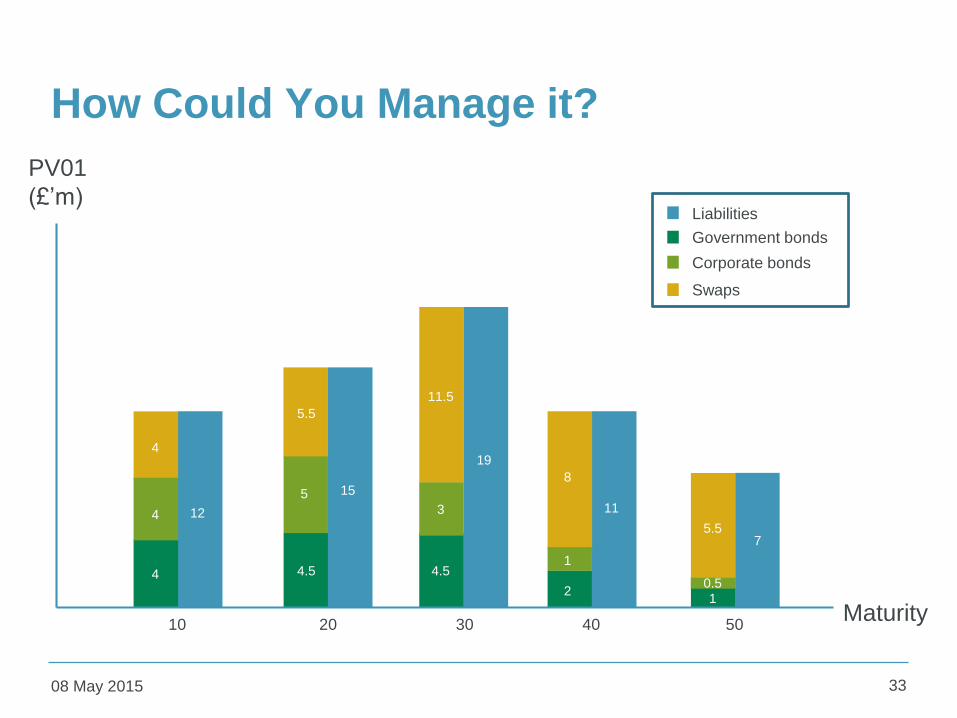

How Could You Manage it?

08 May 2015 33

PV01

(£’m)

Maturity5040302010

Liabilities

Swaps

Government bonds

Corporate bonds

12

4

4

4

15

4.5

5

5.5

4.5

19

3

11.5

8

15

2

11

1

5.5

10.5

7

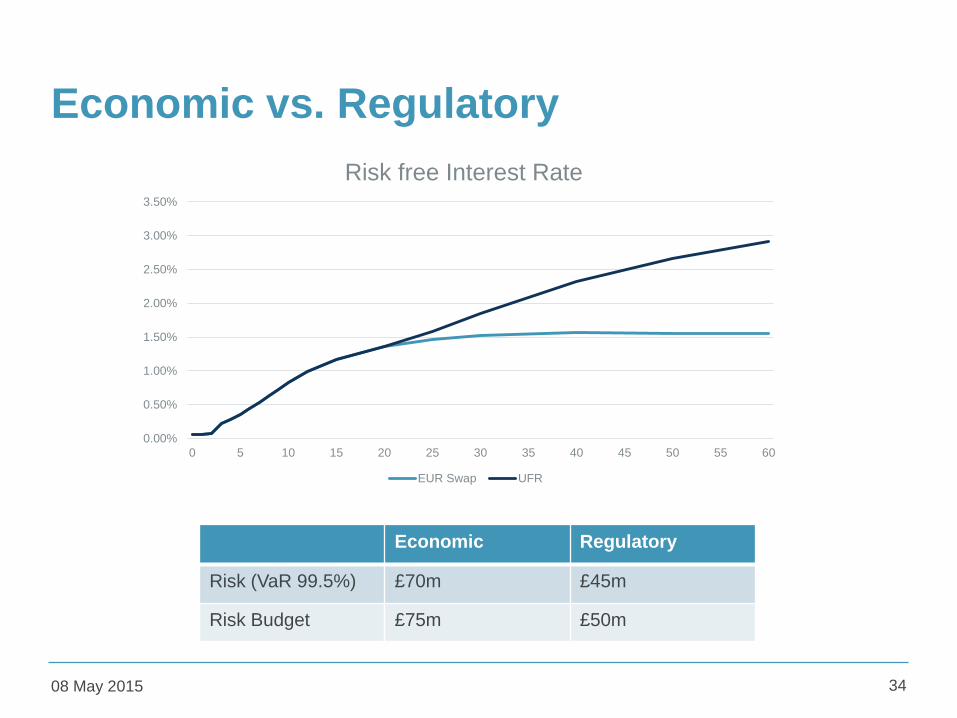

Economic vs. Regulatory

08 May 2015 34

Economic Regulatory

Risk (VaR 99.5%) £70m £45m

Risk Budget £75m £50m

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

0 5 10 15 20 25 30 35 40 45 50 55 60

Risk free Interest Rate

EUR Swap UFR

Conclusion: 4 key takeaways

• Strong need of risk/capital management practices

• Investment strategy in the context of ALM

• People, system and process

• Constant learning and dynamically adapt to changes

08 May 2015 35

08 May 2015 36

Expressions of individual views by members of the Institute and

Faculty of Actuaries and its staff are encouraged.

The views expressed in this presentation are those of the

presenter.

Questions Comments