Embed Size (px)

Citation preview

How to Become Financially IndestructibleBenefit from future volatility

Let’s face an uncomfortable truth:

At some point, you will face daunting economic challenges you never could have predicted.

How you’ll be affected will depend on which category you fall into…

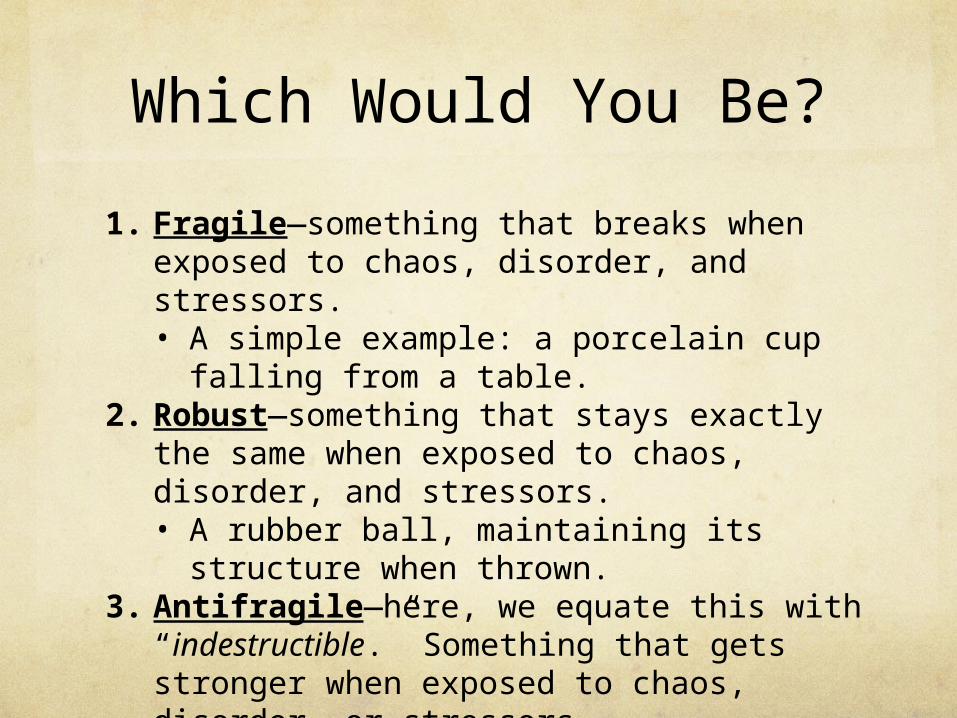

Which Would You Be?

1. Fragile—something that breaks when exposed to chaos, disorder, and stressors. • A simple example: a porcelain cup falling

from a table.2. Robust—something that stays exactly the

same when exposed to chaos, disorder, and stressors.• A rubber ball, maintaining its structure

when thrown.3. Antifragile—here, we equate this with

“indestructible.” Something that gets stronger when exposed to chaos, disorder, or stressors. • Your muscles, which rebuild themselves

even stronger after lifting weights.

The InspirationThe concept comes from Nassim Taleb’s best-seller Antifragile: Things that Gain from Disorder.

Ideas presented here are either loosely or directly based on Taleb’s ideas.

Photo: Sam Beebe, via Flickr

A Working Definition

Financial Antifragility:

Not only being protected from personal or systemic financial stressors, but positioning one’s self to actually benefit from them.

There are five key steps to living a

financially antifragile life.

1) Limit Your DownsideRemember, this isn’t about maximizing your returns in the short-run. It’s about surviving and thriving in the long-run.

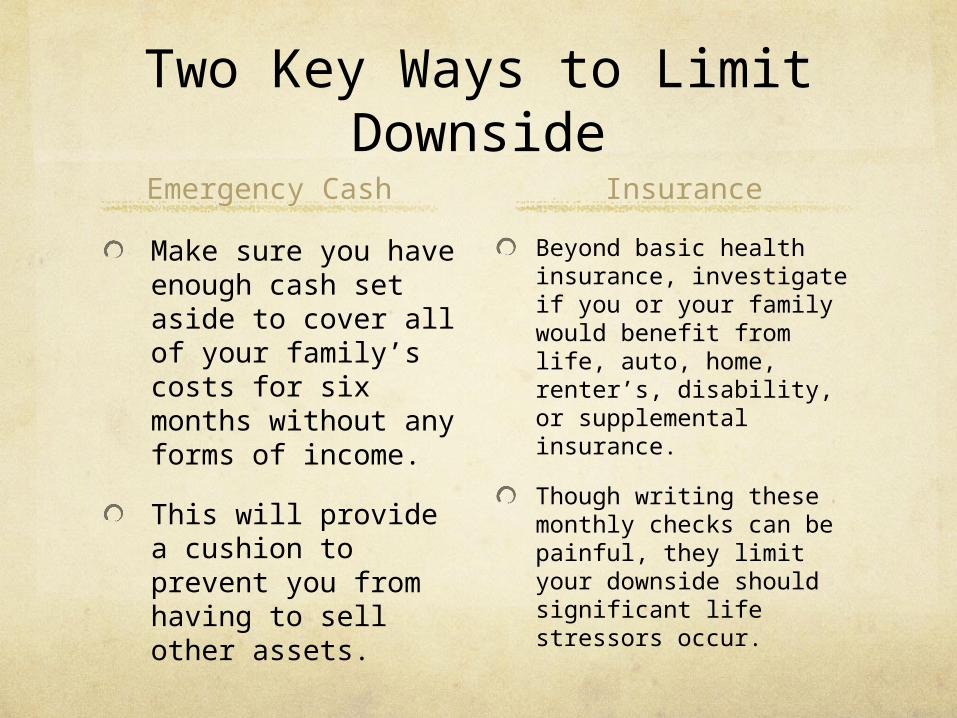

Two Key Ways to Limit Downside

Emergency Cash

Make sure you have enough cash set aside to cover all of your family’s costs for six months without any forms of income.

This will provide a cushion to prevent you from having to sell other assets.

Insurance

Beyond basic health insurance, investigate if you or your family would benefit from life, auto, home, renter’s, disability, or supplemental insurance.

Though writing these monthly checks can be painful, they limit your downside should significant life stressors occur.

2) Avoid DebtIn times of uncertainty and distress, nothing is more constraining than the burden of debt.

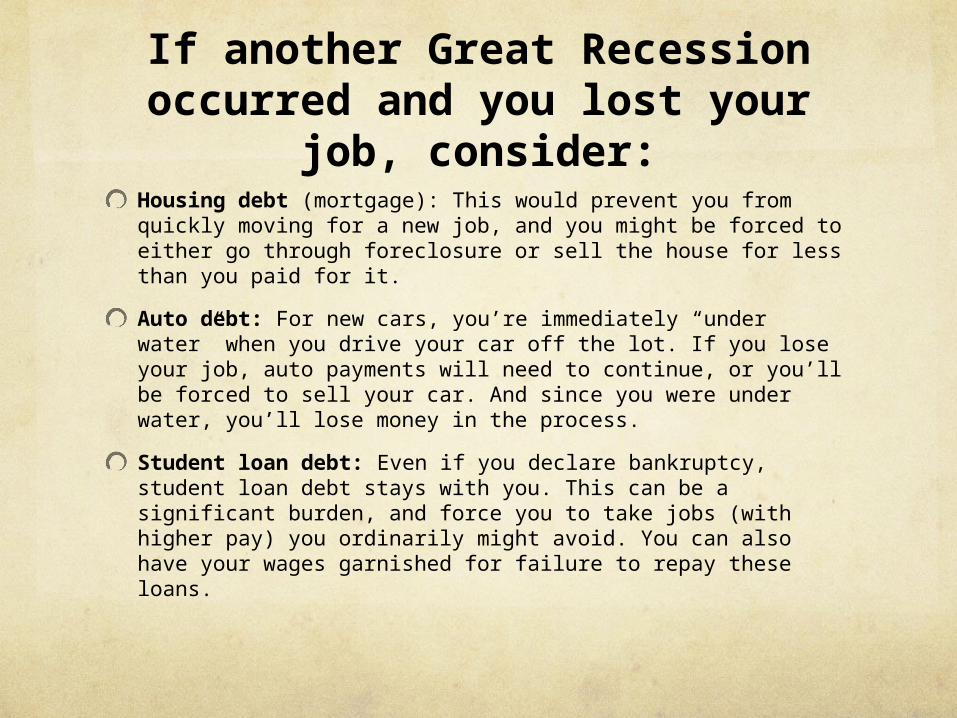

If another Great Recession occurred and you lost your

job, consider:Housing debt (mortgage): This would prevent you from quickly moving for a new job, and you might be forced to either go through foreclosure or sell the house for less than you paid for it.

Auto debt: For new cars, you’re immediately “under water” when you drive your car off the lot. If you lose your job, auto payments will need to continue, or you’ll be forced to sell your car. And since you were under water, you’ll lose money in the process.

Student loan debt: Even if you declare bankruptcy, student loan debt stays with you. This can be a significant burden, and force you to take jobs (with higher pay) you ordinarily might avoid. You can also have your wages garnished for failure to repay these loans.

In the end, you may not be able to totally avoid debt. If that’s the case, repay it as

soon as possible.

3) Live FrugallyThe less you need to be happy, the freer you are!

One of the key tenets of Antifragility is that smaller is

beautiful—but also less fragile.

• If you need more things in your life to make you happy, that will require more money, which inherently makes you more fragile.

• By living frugally, you get an unmatched one-two punch that leads to financial independence and antifragility:

1. You have more money left over to save and invest, which brings you closer to self-reliance.

2. You don’t need to save nearly as much, as you know you don’t need all the bells and whistles of life to be happy.

4) Have

Redundancies in

PlacePlanning for things to go wrong means that you’re prepared when they do.

Efficiency vs. Redundancy

The business world is focused on making things as efficient as possible. Taleb argues that this can be a mistake.

Nature doesn’t work that way—things that survive have many redundancies. The ideally “efficient” body would have one kidney, one lung, and so on.

Therefore, it is somewhat counter-intuitive to have redundancies in place. It often means spending money for things that we may never use.

Are Your Redundancies In Place?

If you lost your job tomorrow:

Do you have a different employer in your field you are familiar with that you could call?

Is there another field you’d like to get into that you’ve already started tinkering with?

Have you done the requisite research to see what it would take to make such moves?

An Example From Real-Life

I genuinely enjoy my job. But my wife and I are constantly working to make sure Plans B, C, and D are in place:

Plan B: We were both teachers in a former life. Neither of us plan to go back into the classroom. However, we keep our credentials up-to-date should we need to apply.

Plan C: We’ve always had a farming itch. We now spend our winters on a farm to learn more about it. We have also borrowed plots of land and picked the brains of those at farmer’s markets to get an idea for what it would take to succeed if we wanted to start our own farm.

Plan D: We will likely be building a very small home in Costa Rica this winter. Should we need to, we could move there and live on very little money for many years before it became absolutely necessary to re-enter the workforce.

5) Use Convex

Optionality to Your

Benefit

Tinker with ideas that have limited downside and unlikely—but unlimited—upside.

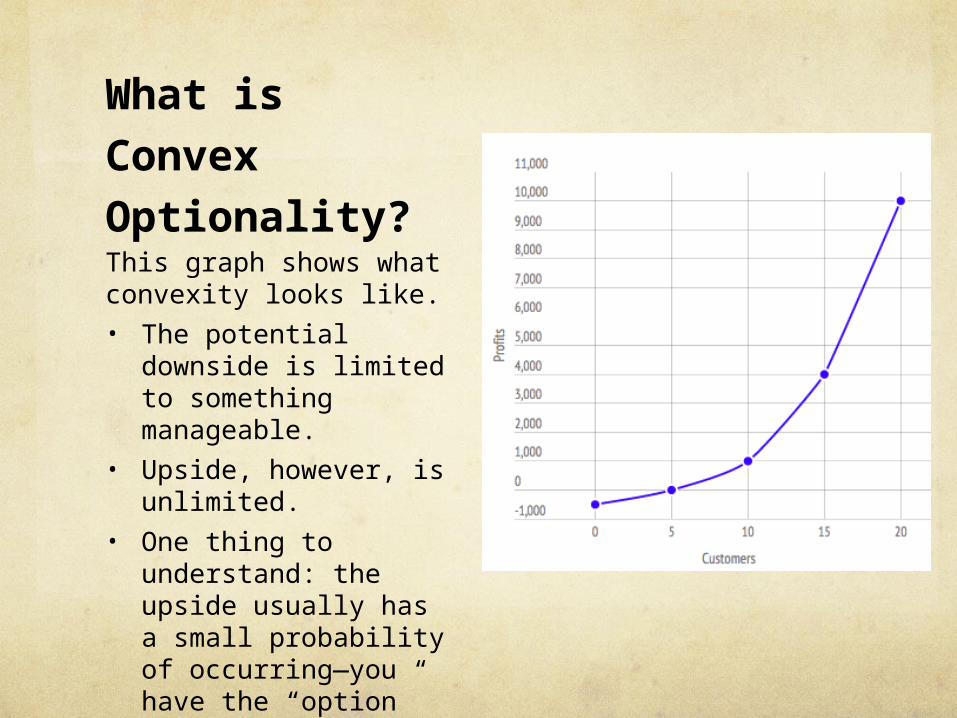

What is Convex Optionality?This graph shows what convexity looks like.• The potential downside

is limited to something manageable.

• Upside, however, is unlimited.

• One thing to understand: the upside usually has a small probability of occurring—you have the “option” of continuing or trying something else.

The Barbell Approach

Taleb defines this as: “A dual strategy: one safe and one speculative, deemed more robust than a ‘monomodal’ strategy.”

For working adults, this means having one stable income while tinkering with a passion on the side.

Though the chances of one “tinkering experiment” being wildly successful are small, your chances go up markedly with repeated attempts.

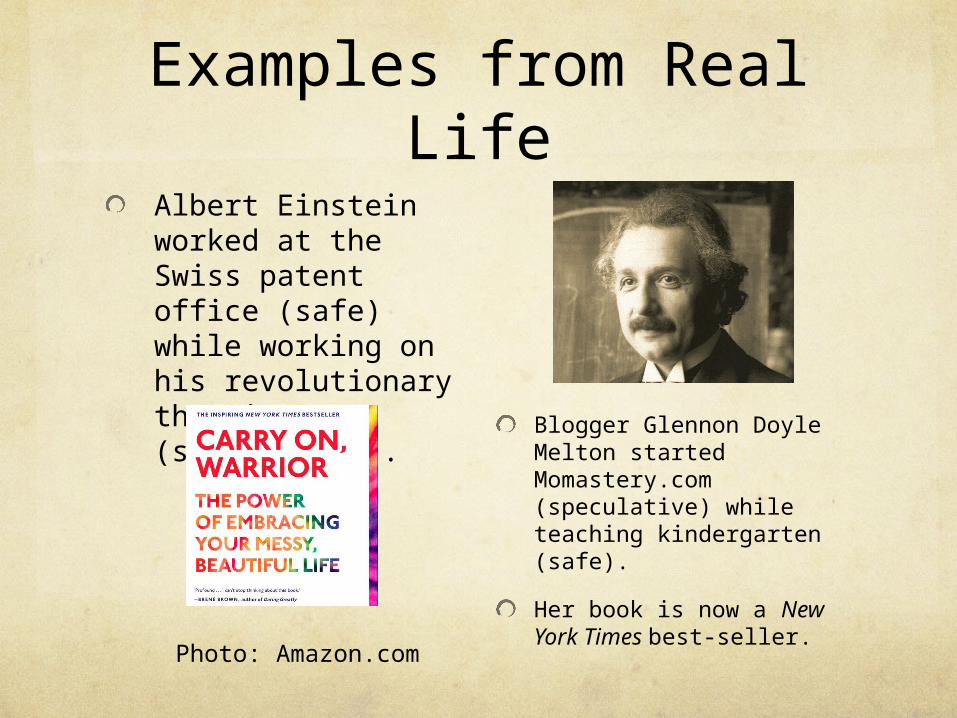

Examples from Real Life

Albert Einstein worked at the Swiss patent office (safe) while working on his revolutionary theories (speculative). Blogger Glennon Doyle

Melton started Momastery.com (speculative) while teaching kindergarten (safe).

Her book is now a New York Times best-seller.Photo: Amazon.com

A Quick Review1. Limit Your

Downside2. Avoid Debt3. Live Frugally4. Have

Redundancies5. Embrace Convex

Optionality

If you find that it’s too late in the game to adopt this

strategy, check out…

The $60K Social Security Bonus Most Retirees Completely Overlook