Embed Size (px)

Citation preview

A Presentation By:Shruti Gupta

&Shivam Bansal

"GST"

One of the biggest taxation reforms in India -- the Goods and Service Tax (GST) -- is all set to integrate State economies and boost overall growth.

GST will create a single, unified Indian market to make the economy stronger.

(Goods and Services Tax in India is set to be implemented from 01/04/2016.)

The implementation of GST will lead to the abolition of other taxes such as octroi, Central Sales Tax, State-level sales tax, entry tax, stamp duty, telecom licence fees, turnover tax, tax on consumption or sale of electricity, taxes on transportation of goods and services, et cetera, thus avoiding multiple layers of taxation that currently exist in India.

Introduction:

By CA. Vinay Bhushan

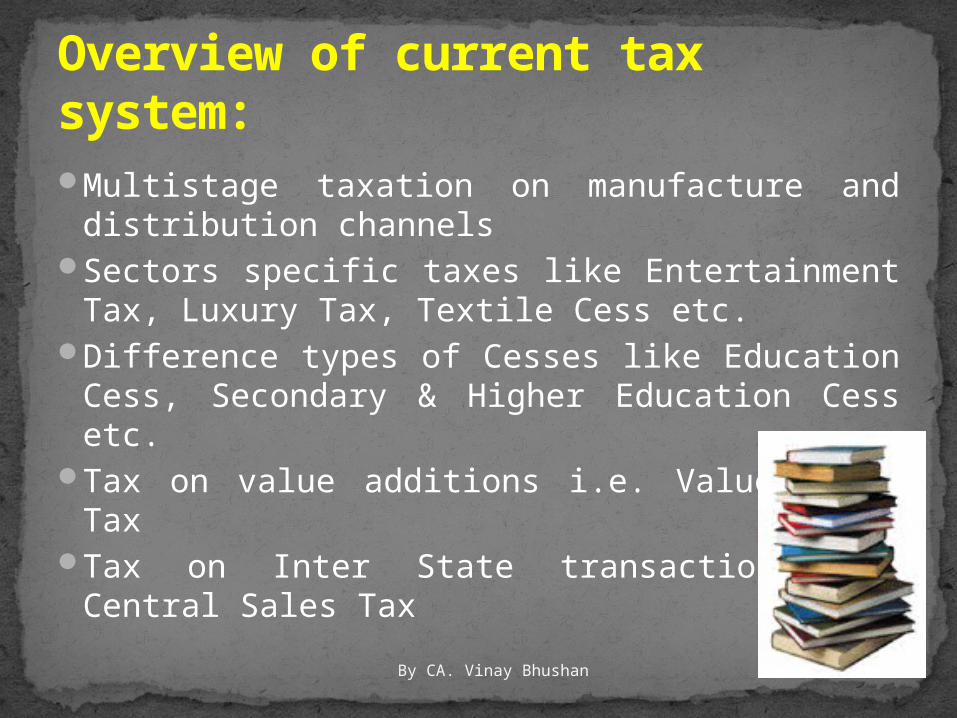

Multistage taxation on manufacture and distribution channels

Sectors specific taxes like Entertainment Tax, Luxury Tax, Textile Cess etc.

Difference types of Cesses like Education Cess, Secondary & Higher Education Cess etc.

Tax on value additions i.e. Value Added Tax Tax on Inter State transaction i.e. Central

Sales Tax

Overview of current tax system:

Manufacture Sector - Multiple Taxes:

Manufacturing Sector

Value Added Tax { 0%, 4%, 12.5%}

Central Sales Tax {2%}

Central Excise Duty {8%}

Educations Cesses {3%}

R & D Cess {5%}

Other local taxes like Entry Tax, Octroi, State Cesses etc. are also applicable

Service Sector - Multiple Taxes

ServiceSector

Education Cess {2%}

Secondary & Higher Education Cess {1%}

Service Tax {10%}

Confusion and MistrustComplex and lacking in stabilityHidden tax on exports, no state tax

on importsHigh transaction costs

DRAWBACKS OF CURRENT SYSTEM

Goods and Services Tax -- GST -- is a comprehensive tax levy on manufacture, sale and consumption of goods and services at a national level.

Through a tax credit mechanism, this tax is collected on value-added goods and services at each stage of sale or purchase in the supply chain.

The system allows the set-off of GST paid on the procurement of goods and services against the GST which is payable on the supply of goods or services. However, the end consumer bears this tax as he is the last person in the supply chain.

What is GST?

It's been a long journey. Although the plan has been discussed for years, a formal announcement was made in the 2006 Budget by P Chidambaram, the then finance minister. Since then it has missed several deadlines. The BJP government is now hoping for a nationwide roll-out of GST from April 2016.

When was GST conceived and when will it be implemented?

Some States against GST: The governments of Madhya Pradesh, Chhattisgarh and

Tamil Nadu say that the information technology systems and the administrative infrastructure will not be ready by April 2010 to implement GST. States have sought assurances that their existing revenues will be protected.

The central government has offered to compensate States in case of a loss in revenues.

Some States fear that if the uniform tax rate is lower than their existing rates, it will hit their tax kitty. The government believes that dual GST will lead to better revenue collection for States.

However, backward and less-developed States could see a fall in tax collections. GST could see better revenue collection for some States as the consumption of goods and services will rise.

Why was it held up?

Almost 140 countries have already implemented the GST. Most of the countries have a unified GST system. Brazil and Canada follow a dual system where GST is levied by both the Union and the State governments.

France was the first country to introduce GST system in 1954.

Other nations have a similar tax structure

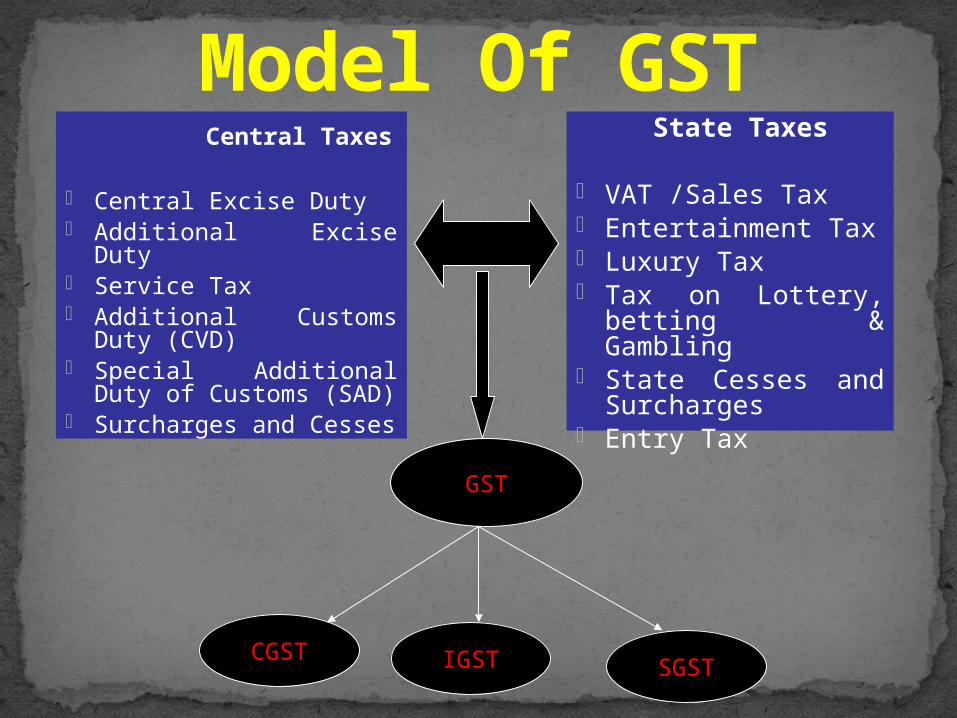

Model Of GST Central Taxes

- Central Excise Duty- Additional Excise Duty- Service Tax- Additional Customs Duty

(CVD)- Special Additional Duty

of Customs (SAD)- Surcharges and Cesses

State Taxes

- VAT /Sales Tax- Entertainment Tax- Luxury Tax- Tax on Lottery,

betting & Gambling- State Cesses and

Surcharges- Entry Tax

GST

CGST IGST SGST

It would be applicable to all transactions of goods and service.

It to be paid to the accounts of the Centre and the States separately.

The rules for taking and utilization of credit for the Central GST and the State GST would be aligned.

Cross utilization of ITC between the Central GST and the State GST would not be allowed except in the case of inter-State supply of goods.

GST - Salient Features

The Centre and the States would have concurrent jurisdiction for the entire value chain and for all taxpayers on the basis of thresholds for goods and services prescribed for the States and the Centre.

The taxpayer would need to submit common format for periodical returns, to both the Central and to the concerned State GST authorities.

Each taxpayer would be allotted a PAN-linked taxpayer identification number with a total of 13/15 digits.

Features

It will cover all types of person carrying on business activities, i.e. manufacturer, job-worker, trader, importer, exporter, all types of service providers, etc.

If a company is having four branches in four different states, all the four branches will be considered as TP under each jurisdiction of SGs.

All the dealers/ business entities will have to pay both the types of taxes on all the transactions.

A dealer must get registered under CGST as it will make him entitle to claim ITC of CGST thereby attracting buyers under B2B transactions.

Importers have to register under both CGST and SGST as well.

Taxable Person

The dealers registered under GST (Manufacturers, Wholesalers and retailers and service providers) will charge GST on the price of goods and services from their customers.

They will claim credits for the GST included in the price of their own purchases of goods and services used by them.

The sellers or service providers collect the tax from their customer, who may or may not be the ultimate customer, and before depositing the same to the exchequer, they deduct the tax they have already paid.

GST- HOW IT WORKS

Under GST registration, it is likely to be linked with the existing PAN.

The new business identification number was likely to be the 10-digit alphanumeric PAN, in addition to two digits for state code and one or two check numbers for disallowing fake numbers. The total number of digits in the new number was likely to be 13-14.

Registration under GST

“After making the calculations by including petrol and octroi in the GST as opposed to the states’ demand of keeping them out, the rate that has been arrived at is 11 per cent and 12 per cent for the Centre and states, respectively,” the official said.

What will be the rate of GST

1. GST is a transparent Tax and also reduce numbers of indirect taxes. With GST implemented a business premises can show the tax applied in the sales invoice. Customer will know exactly how much tax they are paying on the product they bought or services they consumed.

2. GST will not be a cost to registered retailers therefore there will be no hidden taxes and the cost of doing business will be lower. This in turn will help Export being more competitive.

3. GST can also help to diversification of income sources for Government other than income tax and petroleum tax.

Advantages GST:

4. Under Goods and Services Tax, the tax burden will be divided equally between Manufacturing and services. This can be done through lower tax rate by increase Tax base and reducing exemptions.

5. In GST System both Central GST and State GST will be charged on manufacturing cost and will be collected on point of sale. This will benefit people as prices will come down which in turn will help companies as consumption will increase.

6. Biggest benefit will be that multiple taxes like octroi, central sales tax, state sales tax, entry tax, license fees, turnover tax etc will no longer be present and all that will be brought under the GST. Doing Business now will be easier and more comfortable as various hidden taxation will not be present.

Advantages:

1. Critics say that GST would impact negatively on the real estate market. It would add up to 8 percent to the cost of new homes and reduce demand by about 12 percent.

2. Some Economist says that CGST, SGST and IGST are nothing but new names for Central Excise/Service Tax, VAT and CST and hence GST brings nothing new for which we should cheer.

Disadvantages

The Empowered Committee describes the GST as “a further significant improvement – the next logical step - towards a comprehensive indirect tax reforms in the country.” Indeed, it has the potential to be the single most important initiative in the fiscal history of India. It can pave the way for modernization of tax administration - make it simpler and more transparent and significant enhancement in voluntary compliance.

Conclusion: