Embed Size (px)

Citation preview

Enterprise Liquidity Risk: Overcoming the challengesPredictive analytics and advanced risk-monitoring systems are some of the tools available to financial institutions looking to minimize liquidity risk in an increasingly connected world.

Executive Summary“…The U.S. financial system experienced conditions that were among the most difficult and chaotic in its history. Waves of bank fail-ures culminated in the shutdown of the banking system (and of a number of other intermediaries and markets). On the other side of the ledger, exceptionally high rates of default and bank-ruptcy affected every class of borrower except the federal government.” 1

Even though the statement above very closely summarizes the financial crisis of 2008, it is not about that (the most severe financial crisis of recent times). It is an excerpt from a 1983 working paper by Federal Reserve Chairman Ben Bernanke, who was then a student studying the Great Depression of 1929.

Liquidity risk – the risk that a given security or asset cannot be traded quickly enough in the market to prevent a loss – is not a new phenom-enon in financial markets. In fact, liquidity risk has been a significant factor in most previous financial crises, from the Great Depression to the Latin American debt crisis. Each downturn has

thrown new challenges at the financial industry – leading to changes in regulations such as the Securities Act of 1933 and the Sarbanes Oxley Act, and altering the way banks and economies oper-ate. The most recent financial crisis is no different.

In this paper, we will provide a historical perspec-tive on the role that liquidity risk played in earlier financial crises. We will also discuss challenges that banks and financial institutions tradition-ally face when building operations, platforms and infrastructures to manage liquidity risk. We will then offer our point of view on how to bet-ter manage liquidity risk operations in light of new dynamics, such as the increasing interde-pendencies within the global financial system, the abundance of data, and new technologies that have added dimensions to an already complex liquidity problem. Finally, we will pro-vide recommendations for how banks can better manage these challenges.

Liquidity Risk – A Fundamental UnderstandingShakespeare’s play, “Merchant of Venice,” is a good primer for understanding the complex

cognizant 20-20 insights | december 2013

• Cognizant 20-20 Insights

cognizant 20-20 insights 2

financial concept of liquidity risk. In the play, Shylock loans money to Bassanio with Antonio’s ships at sea as collateral. Antonio’s ships are then rumored to have been wrecked at sea, leaving him unable to repay the loan. In financial terms, the asset that was used as collateral was impaired – presenting the risk that the outstanding liabil-ity would not be met. This is known as funding liquidity risk2 – one of two types of liquidity risk.

The other type of liquidity risk is market liquidity risk.3 This arises when the market is unwilling to buy your assets, or at least not at the price you want. To extend our analogy, if Antonio’s ships had arrived safely but the ships carried goods that were already abundant in Venice, Antonio would have been exposed to market liquidity risk, since nobody in the market would have wanted to buy the goods that those ships brought.

Both funding liquidity and market liquidity risks have played a key part in all financial crises. Understanding the role of liquidity risk in past financial crises is necessary in order for individu-als and institutions to prepare for the future.

Liquidity Risk and Past Financial CrisesCrash of 1929 and the Great Depression

The crash of 1929 and the Great Depression fol-lowed the speculative boom in the 1920s. From steel production to railway receipts, everything was rising.4 Hundreds of thousands of Americans invested in stock, many with borrowed money.5 A crucial factor contributing to the bullish stock market was the favorable commodity outlook in the 1920s, especially for wheat production. When wheat prices were at their peak in the U.S., France and Italy boasted about their own robust wheat production – sending wheat prices plummeting in the U.S. This sent shivers down the stock market. Panicked investors who had bought stocks with borrowed money now started selling – depressing the stock markets even further.

This led to massive defaults by individual borrowers, causing banks to suffer severe losses. Structural support like today’s FDIC insurance did not exist – prompting depositors to rush to their banks. This created a run on the banks – ultimately causing some to fail. The lack of a coordinated government effort further complicated matters. International trade came to a halt – affecting millions of workers.

Liquidity risk was at the heart of the Great Depression. Market liquidity risk caused wheat prices to fall; funding liquidity risk saw borrowed money flee the stock markets. Banks’ credit risk, coupled with their liquidity risk, exacerbated the downward spiral that lasted for a decade.

The Savings and Loans crisis of the 1980s, the Asian financial crisis of 1997, the Latin Ameri-can debt crisis of the 1980s and the 2008 Global financial crisis followed similar trajectories.

Savings and Loan Crisis

The two decades following the end of World War II witnessed rising economic activity and the arrival of the baby boomer generation. Interest rates were rising, luring savings deposits. The economy was growing and more people were taking out mortgages. By the mid to late 1970s, the economy was slowing, whereas interest rates and inflation continued to rise. Soon, the U.S. economy hit a stage that later came to be known as stagflation – a combination of stagnating growth and rising inflation.6 This meant that fewer people qualified for mortgages, which lead to losses for many S&L institutions and caused 747 of 3,234 – or about 25% – of them to close their doors. The failed institutions represented a total book value of US$402 billion.7

Liquidity risk led to these institutions’ inability to generate income, and ultimately to a severe financial meltdown.

Asian Financial Crisis

In the case of the Asian financial crisis, South Asian countries such as Thailand, South Korea and Indonesia had maintained high interest rates to attract foreign capital. This caused heavy capital inflows into these countries, and increased their foreign debt-to-GDP ratios from 100% to 167% in the three years between 1993 and 1996. This worked well as long as U.S. interest rates remained low. However, once those rates started rising under Federal Reserve Chairman Alan Greenspan (who wanted to thwart inflation), these Asian countries witnessed massive capital outflows.

Market liquidity risk – the risk that the market would not want your assets, in this case Asian debt – was a key reason for the Asian financial crisis.

cognizant 20-20 insights 3

Latin American Debt Crisis

Countries such as Brazil, Argentina and Mexico borrowed heavily to carry out industrialization in the 1960s and 1970s. In less than a decade, Latin America’s debt grew by 400% – from US$75 billion in 1975 to US$315 billion in 1983. Interest payments grew in tandem to US$66 billion from US$12 billion in the same period. To compound the problem, in the 1970s and 1980s a global economic recession witnessed skyrocketing oil prices, raising U.S. interest rates. Depreciating Latin American currencies made debt repayment much more expensive.8 This led to a full-blown Latin American debt crisis and to what later came to be known as “the lost decade” for the region.

It was funding liquidity risk – a risk that left Latin America unable to service its debt – that was at the heart of this crisis.

Global Financial Crisis of 2008

Liquidity risk was one of the key factors in the financial crisis that lasted from 2008-2010. Subprime mortgages were aggressively sold to people who could not afford them. Availability of cheap mortgages jacked up demand for real estate, inflating prices.

While banks sliced and diced the mortgage secu-rities they owned, every bank had substantial amounts of these assets. Additionally, all banks were highly leveraged against these assets. When mortgage owners started defaulting, the financial markets witnessed an unprecedented downward spiral of asset pricing and ultimately the bursting of the asset bubble. The effect was pronounced – coming in the forms of market liquidity risk for the MBSs, CDOs and CMOs that nobody wanted to buy anymore… funding liquidity risk for the banks that were highly leveraged against these assets… and liquidity risk for mortgage owners. These three forces combined to initiate an economic meltdown.

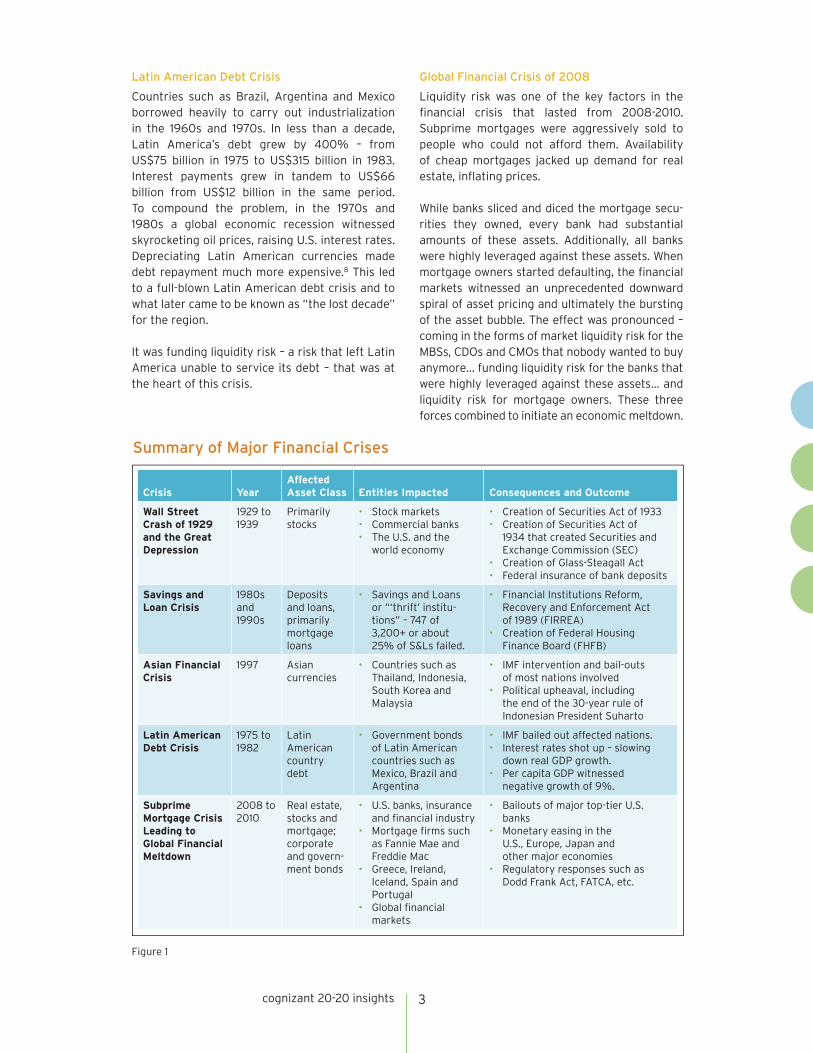

Summary of Major Financial Crises

Figure 1

Crisis YearAffected Asset Class Entities Impacted Consequences and Outcome

Wall Street Crash of 1929 and the Great Depression

1929 to 1939

Primarily stocks

• Stock markets• Commercial banks• The U.S. and the

world economy

• Creation of Securities Act of 1933• Creation of Securities Act of

1934 that created Securities and Exchange Commission (SEC)

• Creation of Glass-Steagall Act• Federal insurance of bank deposits

Savings and Loan Crisis

1980s and 1990s

Deposits and loans, primarily mortgage loans

• Savings and Loans or “‘thrift’ institu-tions” – 747 of 3,200+ or about 25% of S&Ls failed.

• Financial Institutions Reform, Recovery and Enforcement Act of 1989 (FIRREA)

• Creation of Federal Housing Finance Board (FHFB)

Asian Financial Crisis

1997 Asian currencies

• Countries such as Thailand, Indonesia, South Korea and Malaysia

• IMF intervention and bail-outs of most nations involved

• Political upheaval, including the end of the 30-year rule of Indonesian President Suharto

Latin American Debt Crisis

1975 to 1982

Latin American country debt

• Government bonds of Latin American countries such as Mexico, Brazil and Argentina

• IMF bailed out affected nations.• Interest rates shot up – slowing

down real GDP growth.• Per capita GDP witnessed

negative growth of 9%.

Subprime Mortgage Crisis Leading to Global Financial Meltdown

2008 to 2010

Real estate, stocks and mortgage; corporate and govern-ment bonds

• U.S. banks, insurance and financial industry

• Mortgage firms such as Fannie Mae and Freddie Mac

• Greece, Ireland, Iceland, Spain and Portugal

• Global financial markets

• Bailouts of major top-tier U.S. banks

• Monetary easing in the U.S., Europe, Japan and other major economies

• Regulatory responses such as Dodd Frank Act, FATCA, etc.

cognizant 20-20 insights 4

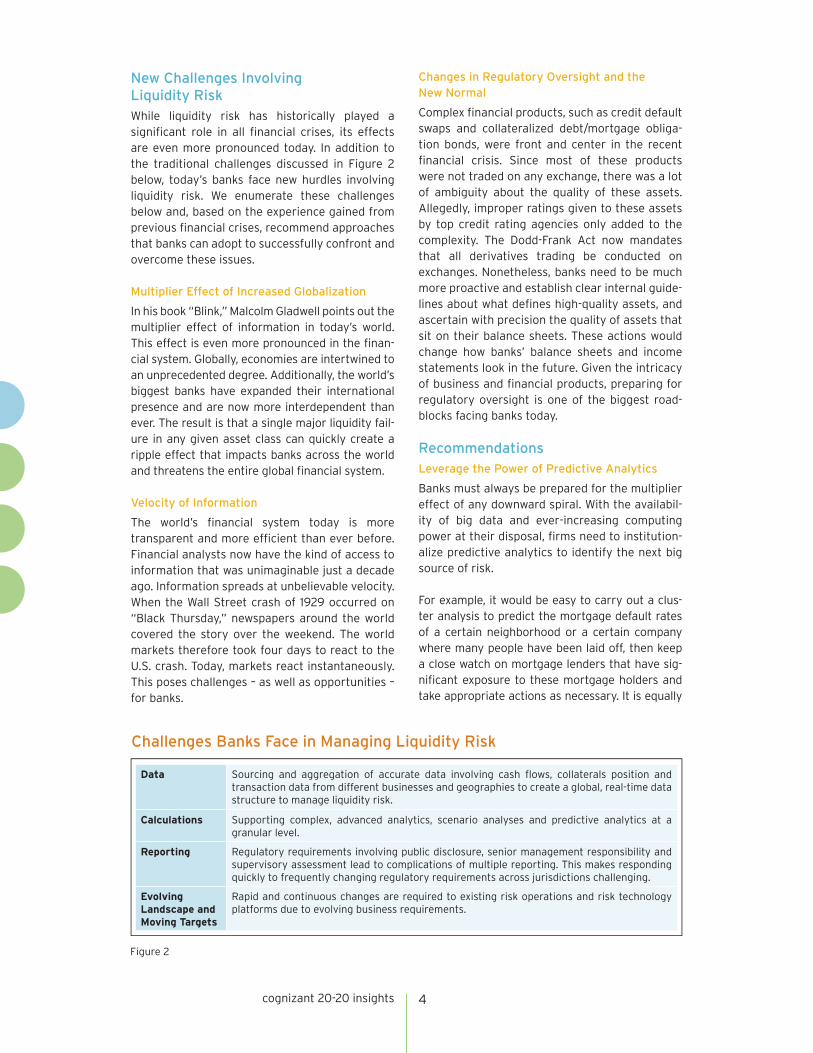

New Challenges Involving Liquidity Risk While liquidity risk has historically played a significant role in all financial crises, its effects are even more pronounced today. In addition to the traditional challenges discussed in Figure 2 below, today’s banks face new hurdles involving liquidity risk. We enumerate these challenges below and, based on the experience gained from previous financial crises, recommend approaches that banks can adopt to successfully confront and overcome these issues.

Multiplier Effect of Increased Globalization

In his book “Blink,” Malcolm Gladwell points out the multiplier effect of information in today’s world. This effect is even more pronounced in the finan-cial system. Globally, economies are intertwined to an unprecedented degree. Additionally, the world’s biggest banks have expanded their international presence and are now more interdependent than ever. The result is that a single major liquidity fail-ure in any given asset class can quickly create a ripple effect that impacts banks across the world and threatens the entire global financial system.

Velocity of Information

The world’s financial system today is more transparent and more efficient than ever before. Financial analysts now have the kind of access to information that was unimaginable just a decade ago. Information spreads at unbelievable velocity. When the Wall Street crash of 1929 occurred on “Black Thursday,” newspapers around the world covered the story over the weekend. The world markets therefore took four days to react to the U.S. crash. Today, markets react instantaneously. This poses challenges – as well as opportunities – for banks.

Changes in Regulatory Oversight and the New Normal

Complex financial products, such as credit default swaps and collateralized debt/mortgage obliga-tion bonds, were front and center in the recent financial crisis. Since most of these products were not traded on any exchange, there was a lot of ambiguity about the quality of these assets. Allegedly, improper ratings given to these assets by top credit rating agencies only added to the complexity. The Dodd-Frank Act now mandates that all derivatives trading be conducted on exchanges. Nonetheless, banks need to be much more proactive and establish clear internal guide-lines about what defines high-quality assets, and ascertain with precision the quality of assets that sit on their balance sheets. These actions would change how banks’ balance sheets and income statements look in the future. Given the intricacy of business and financial products, preparing for regulatory oversight is one of the biggest road-blocks facing banks today.

Recommendations Leverage the Power of Predictive Analytics

Banks must always be prepared for the multiplier effect of any downward spiral. With the availabil-ity of big data and ever-increasing computing power at their disposal, firms need to institution-alize predictive analytics to identify the next big source of risk.

For example, it would be easy to carry out a clus-ter analysis to predict the mortgage default rates of a certain neighborhood or a certain company where many people have been laid off, then keep a close watch on mortgage lenders that have sig-nificant exposure to these mortgage holders and take appropriate actions as necessary. It is equally

Challenges Banks Face in Managing Liquidity Risk

Figure 2

Data Sourcing and aggregation of accurate data involving cash flows, collaterals position and transaction data from different businesses and geographies to create a global, real-time data structure to manage liquidity risk.

Calculations Supporting complex, advanced analytics, scenario analyses and predictive analytics at a granular level.

Reporting Regulatory requirements involving public disclosure, senior management responsibility and supervisory assessment lead to complications of multiple reporting. This makes responding quickly to frequently changing regulatory requirements across jurisdictions challenging.

Evolving Landscape and Moving Targets

Rapid and continuous changes are required to existing risk operations and risk technology platforms due to evolving business requirements.

cognizant 20-20 insights 5

Our Recommendations

Figure 3

Comprehensive Evaluation of Operational and Technology Assets

Rather than adopting a piecemeal approach, financial institutions must conduct a holistic evaluation of their processes, platforms and assets to optimally leverage them for developing liquidity risk solutions.

Data Consolida-tion and Data Quality

Firms require a centralized liquidity warehouse solution that creates a virtual layer for aggregating disparate data sources. Additionally, firms need to address data-quality issues, including data accuracy, completeness and consistency.

Collaboration Across Groups and Integra-tion with Other Platforms (Risk, Transfer Pricing)

Firms need operations and technology teams supporting treasury, finance, credit, market and liquidity risks to work closely with one another to identify process reusability and leverage best practices.

A liquidity risk framework must be integrated with Fund Transfer Pricing capabilities for liquidity cost attribution and collateral management platforms to account for the impact of increasing demand for collaterals, and for prospective liquidity pressures from margin calls.

Flexible Reporting Reporting must be flexible to enable different jurisdictions, legal entities and branches to define their respective reporting requirements within an overall framework of firm-wide reporting.

Model Governance Firms need to develop advanced analytical models with superior model governance, testing and model risk management. Also critical is to ensure that all models are up-to-date, that clear linkages between data, models and reports exist, and that all models are tested with requisite scenarios.

important – and possible – to deploy predictive analytics at asset-class levels. And it is possible to triangulate factors that led to Detroit’s bankruptcy, for example, and extrapolate the data to predict what other municipalities may face a similar fate.

Predictive analytics will play a seminal role in helping banks mitigate risk going forward. Testament to this fact is the emergence of the Chief Analytics Officer (CAO) – an increasingly important position for institutions that approach their information as a corporate asset that can lessen risk, increase trust and add more value.

Leverage Social Media to Improve Risk- Monitoring

Today’s banks need to constantly monitor their assets and the online “chatter” that surrounds these resources both on and off the street. For example, using consumers’ feedback on social media, it is possible to track their level of satisfaction with utilities such as toll roads and airports, which are revenue sources for revenue obligation bonds. This information can then be used to predict the revenue potential of a munici-pality’s revenue bonds and its ultimate credit rating. Similarly, a company’s stock performance can be predicted based on consumers’ responses on social media.

Banks will also need to beef up their risk-moni-toring systems to keep up with the advancing speed of information spread. For example, it is not difficult to imagine a scenario where local economic trouble at the city level in a European country threatens a European bank that in turn threatens its counterparties, which could be a U.S. bank’s European subsidiary – putting the U.S. bank’s capital adequacy at risk. A vigilant, quick-to-respond risk-monitoring system that can spot such risks early on and ensure banks’ speedy response will help institutions mitigate the challenge of information spread.

Strengthen Internal Guidelines on Asset Quality and Stress Testing

Banks need to establish robust internal guidelines to identify and ascertain the true quality of their assets – and not just because the Dodd Frank Act mandates this. Conducting periodic stress tests and simulating scenarios of unexpected events will be critical to avoiding future shocks like the recent financial crisis. If scenarios involving world recession and sharp oil price rises had been simu-lated, Latin American countries would probably have issued less debt. Banks and developed coun-tries would have surely loaned them less money. The financial crisis of 2008 could have been averted if simulation of “fat tail” events had been carried out.

cognizant 20-20 insights 6

Footnotes1 Bernanke, Ben. Excerpt adapted from “Non-monetary Effects of the Financial Crisis in the Propagation

of the Great Depression.” http://www.nber.org/papers/w1054.pdf?new_window=1.

2 “Market Liquidity and Funding Liquidity,” by Markus Brunnermeier and Lasse H. Pederson. http://pages.stern.nyu.edu/~lpederse/papers/Mkt_Fun_Liquidity.pdf.

3 Ibid.

4 “Broad Facts of USA Crisis.” The Daily News (Perth, WA: 1882 - 1950). November, 1929. p. 6 Edition: HOME FINAL EDITION. http://trove.nla.gov.au/ndp/del/article/85141129.

5 Lambert, Richard. “Crashes, Bangs, and Wallops.” Financial Times. http://www.ft.com/intl/cms/s/0/7173bb6a-552a-11dd-ae9c-000077b07658.html#axzz2huDIa15i.

6 “Savings and Loan Industry, U.S.”, EH.net Encyclopedia, edited by Robert Whaples. http://eh.net/ency clopedia/article/mason.savings.loan.industry.us.

7 “Financial Audit: Resolution Trust Corporation's 1995 and 1994 Financial Statements.” U.S. General Accounting Office. http://www.gao.gov/archive/1996/ai96123.pdf.

8 Schaeffer, Robert. “Understanding Globalization: The Social Consequences of Political, Economic, and Environmental Change.” Rowman & Littlefield Publishers. January, 2009.

Referenceswww.wikipedia.org.

Gladwell, Malcolm. “Blink: The Power of Thinking Without Thinking.” Back Bay Books; Little, Brown. January, 2005.

Shakespeare, William. “The Merchant of Venice.”

ConclusionLiquidity risk has been and will continue to be an important factor in all financial crises. The traditional challenges that banks face in building liquidity risk operations, platforms and infrastructure can be effectively managed by making a holistic assessment of existing operational and technology assets, consolidating existing information, and building a flexible and robust architecture.

In addition to traditional challenges, banks face the added complexities of the multiplier effect

caused by increased globalization, the velocity of information and changes in regulatory over-sight. In preparing for future crises, banks need to employ the power of predictive analytics, leverage social media, and establish comprehensive inter-nal guidelines on asset quality and stress testing.

Currently, different banks are at different stages of adopting these measures; some have deployed short-term remedies. Over the long term, institutions would do well to adopt a proactive approach and devise an appropriate overall risk-management strategy.

World Headquarters

500 Frank W. Burr Blvd.Teaneck, NJ 07666 USAPhone: +1 201 801 0233Fax: +1 201 801 0243Toll Free: +1 888 937 3277Email: [email protected]

European Headquarters

1 Kingdom StreetPaddington CentralLondon W2 6BDPhone: +44 (0) 207 297 7600Fax: +44 (0) 207 121 0102Email: [email protected]

India Operations Headquarters

#5/535, Old Mahabalipuram RoadOkkiyam Pettai, ThoraipakkamChennai, 600 096 IndiaPhone: +91 (0) 44 4209 6000Fax: +91 (0) 44 4209 6060Email: [email protected]

© Copyright 2013, Cognizant. All rights reserved. No part of this document may be reproduced, stored in a retrieval system, transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the express written permission from Cognizant. The information contained herein is subject to change without notice. All other trademarks mentioned herein are the property of their respective owners.

About Cognizant

Cognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process outsourcing services, dedicated to helping the world’s leading companies build stronger businesses. Headquartered in Teaneck, New Jersey (U.S.), Cognizant combines a passion for client satisfaction, technology innovation, deep industry and business process expertise, and a global, collaborative workforce that embodies the future of work. With over 50 delivery centers worldwide and approximately 166,400 employees as of September 30, 2013, Cognizant is a member of the NASDAQ-100, the S&P 500, the Forbes Global 2000, and the Fortune 500 and is ranked among the top performing and fastest growing companies in the world.

Visit us online at www.cognizant.com or follow us on Twitter: Cognizant.

About the AuthorsMrugesh Kulkarni is a Senior Manager – Consulting in the capital markets domain at Cognizant Business Consulting. With over 12 years of experience in capital markets, consulting and technology, Mrugesh has worked in areas such as business/IT strategy, project roadmaps, portfolio analysis, and requirements management for large investment banking clients and has supported multiple sales and business development initiatives. He has an MBA from the Indian Institute of Management, Lucknow and a BE from Mumbai University. Mrugesh is a member of the Global Association of Risk Professionals and has completed the FRM certification. He can be reached at [email protected].

Hrishit Pandit is a Senior Consultant in Cognizant Business Consulting’s Banking and Financial Services practice. He has over 10 years of experience in banking, asset management, and wealth advisory and has held various positions at Goldman Sachs, ICICI Bank, and HSBC Bank in the US, Middle East, South Asia, and Africa. Hrishit has an MBA from Kelley School of Business, Indiana University, a PGDBA from Narsee Monjee Institute, Mumbai, and a Bachelor of Engineering from MS University of Baroda, India. He can be reached at [email protected].