Embed Size (px)

Citation preview

ECONOMICEXPOSURETOEMERGINGMARKETS

PARADIGMSHIFTMOSCOW2012

Aparadigmshi,isaradicalchangeinpersonalbeliefs,complexsystemsororganizaMons,replacingtheformerwayofthinkingororganizingwitharadicallydifferentwayofthinkingororganizing.ThinkofaParadigmShiRasachangefromonewayofthinkingtoanother.

ThomasKuhn

2

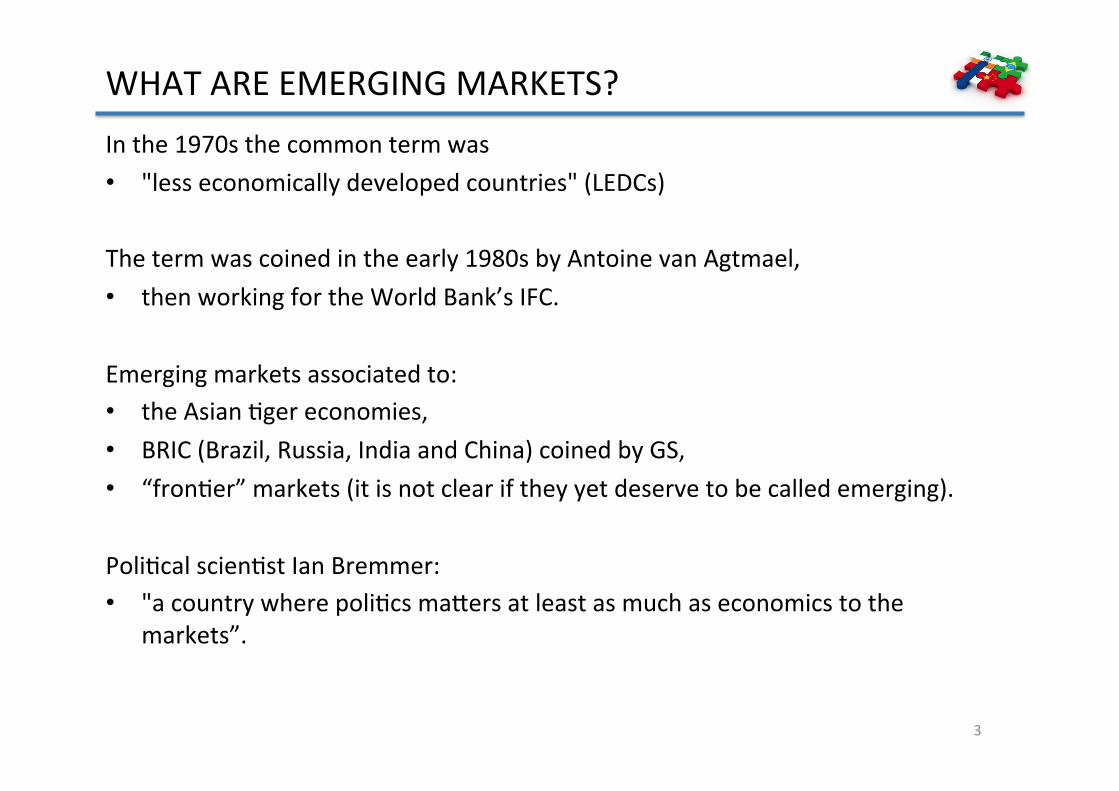

WHATAREEMERGINGMARKETS?Inthe1970sthecommontermwas• "lesseconomicallydevelopedcountries"(LEDCs)Thetermwascoinedintheearly1980sbyAntoinevanAgtmael,• thenworkingfortheWorldBank’sIFC.Emergingmarketsassociatedto:• theAsianMgereconomies,• BRIC(Brazil,Russia,IndiaandChina)coinedbyGS,• “fronMer”markets(itisnotcleariftheyyetdeservetobecalledemerging).PoliMcalscienMstIanBremmer:• "acountrywherepoliMcsmabersatleastasmuchaseconomicstothe

markets”.

3

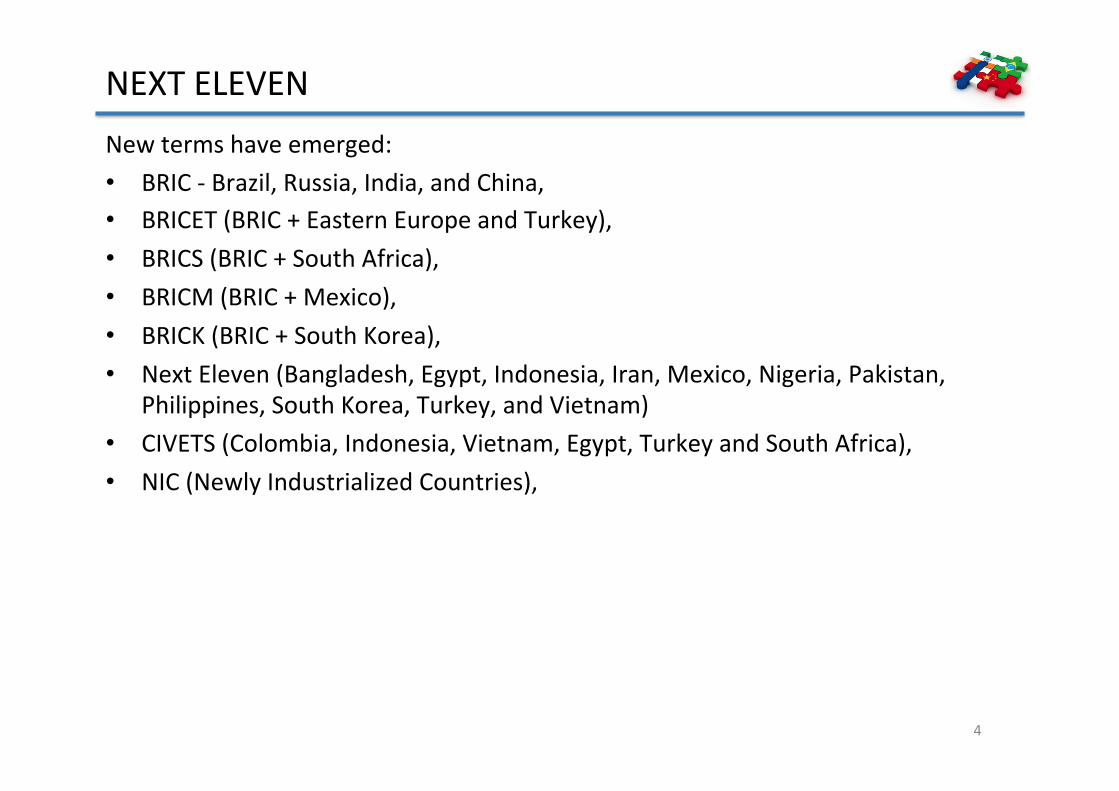

NEXTELEVENNewtermshaveemerged:• BRIC‐Brazil,Russia,India,andChina,• BRICET(BRIC+EasternEuropeandTurkey),• BRICS(BRIC+SouthAfrica),• BRICM(BRIC+Mexico),• BRICK(BRIC+SouthKorea),• NextEleven(Bangladesh,Egypt,Indonesia,Iran,Mexico,Nigeria,Pakistan,

Philippines,SouthKorea,Turkey,andVietnam)• CIVETS(Colombia,Indonesia,Vietnam,Egypt,TurkeyandSouthAfrica),• NIC(NewlyIndustrializedCountries),

4

WHOOWN“EMERGINGMARKETS”???ThebestguidestendtobeinvestmentinformaMonsourceslike• ISIEmergingMarkets,• theEconomist,• marketindexmakers(MorganStanleyCapitalInternaMonal),• raMngsagencies(S&P).

5

WHEREMONEYFLOW???90%ofEMmanagersuseMSCIindexes:

– SouthKoreaandTaiwan–30%,– Asia–52%,– LaMnAmerica–20%,– theBRICs–37.5%.

6

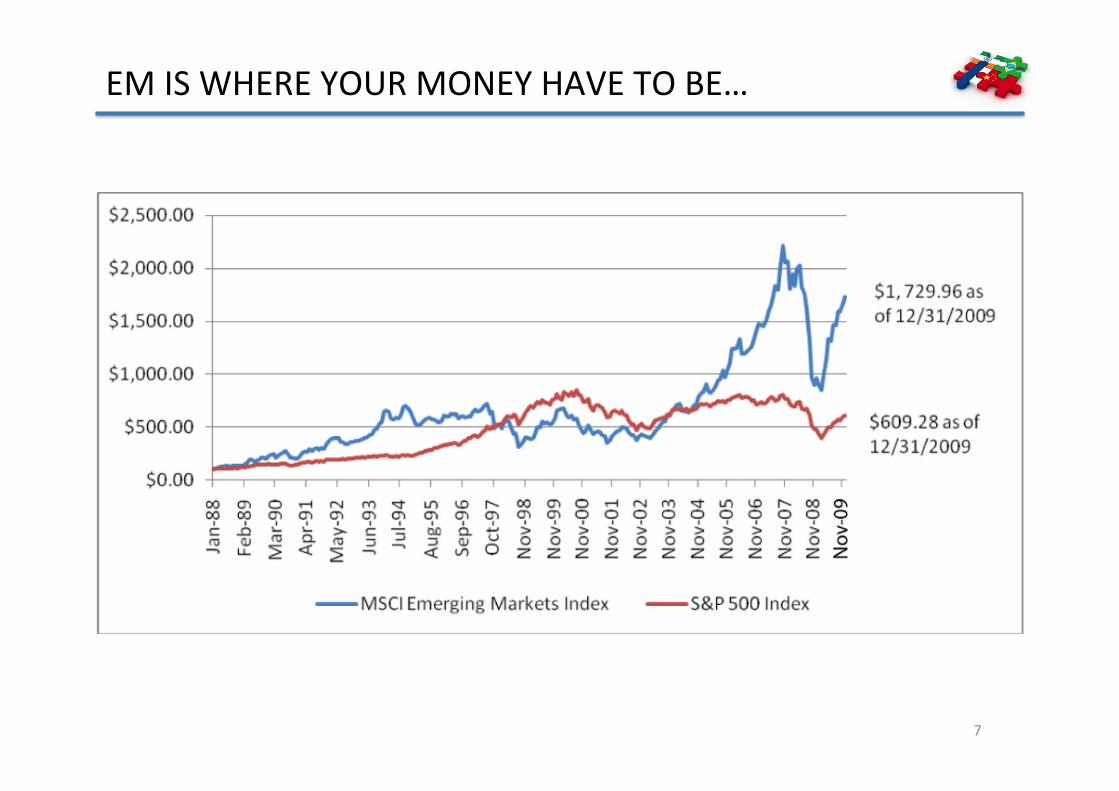

EMISWHEREYOURMONEYHAVETOBE…

7

WHEREISTHEBEEF?!EMgrewby270%throughlastdecade.ShortrunfluctuaMonsarecausedby:• P/EfluctuaMons.Whereas…Equitymarketlong‐termreturnisexplainedby:1. Earninggrowth,2. Dividends

ECONOMYGROWTHMATTERS!!!

8

WHATMAKESTHEMGROW?Whateconomistsagreewithis• suchcountriesareconsideredtobeinatransiMonalphasebetween

developinganddevelopedstatus.Whileresearchers,includingseveralprofessorsfromHarvardBusinessSchoolandYaleSchoolofManagement,havedescribedacMvityincountriessuchasIndiaandChina…

…itiss/llli1leunderstoodhowamarketemerges?

9

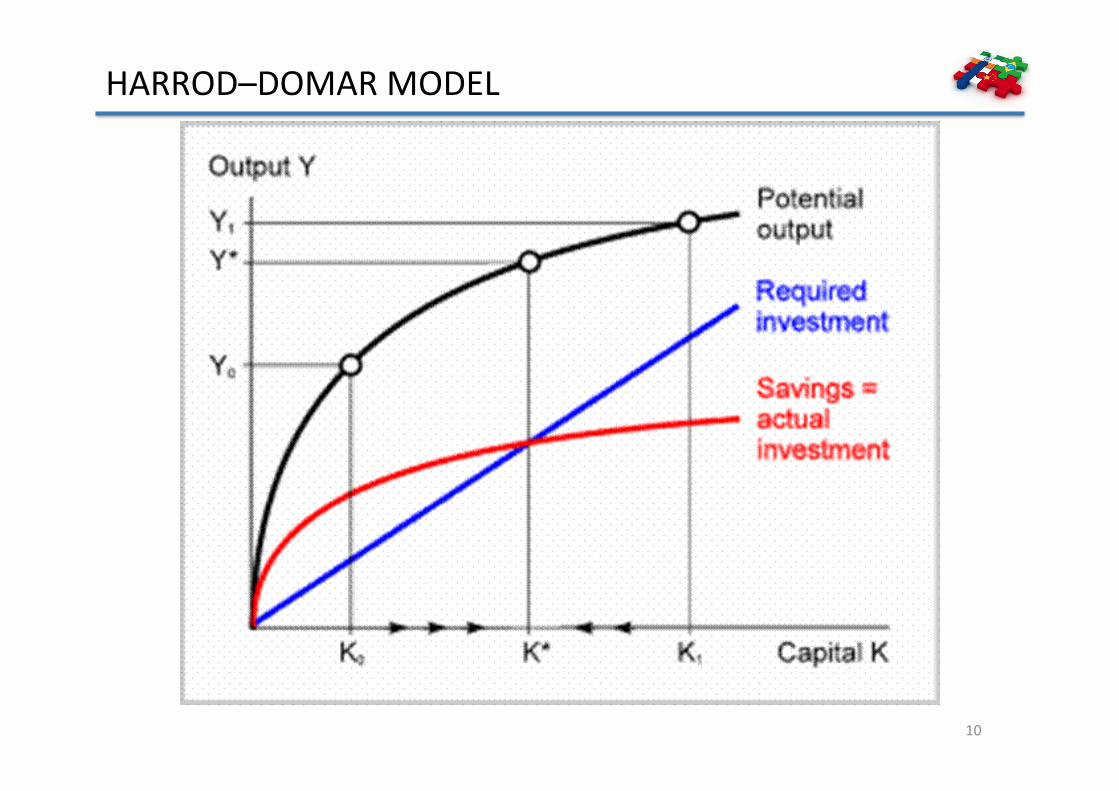

HARROD–DOMARMODEL

10

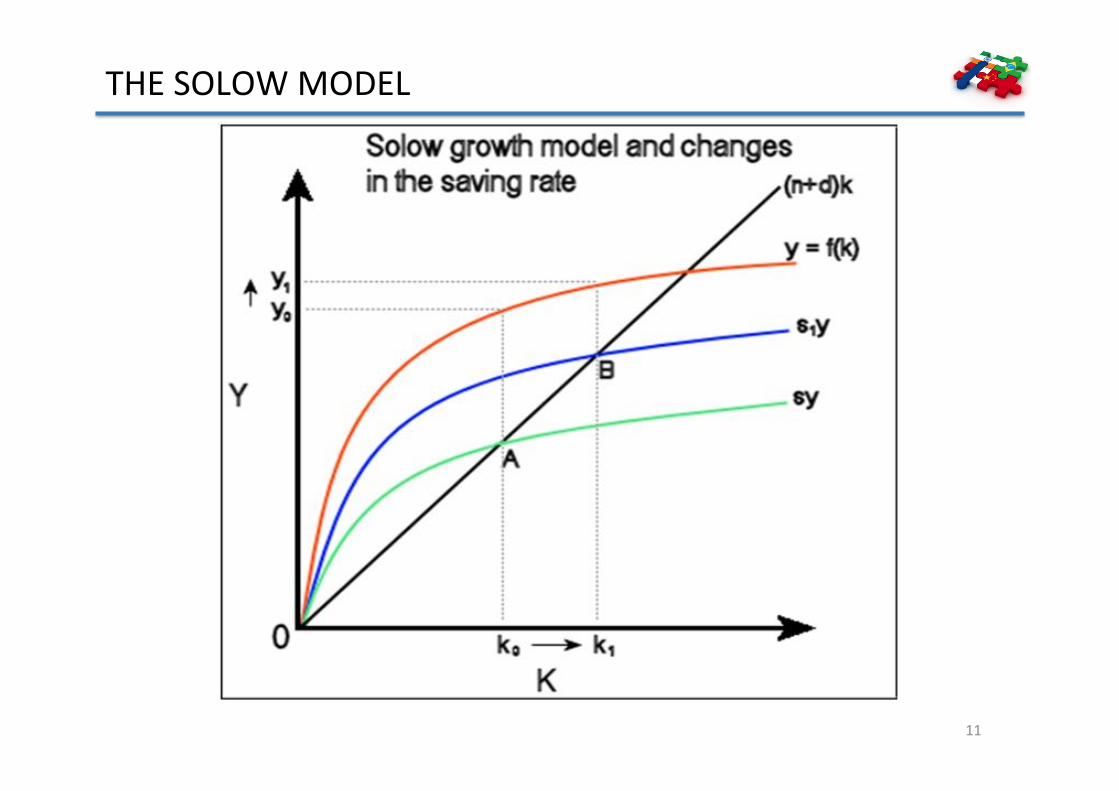

THESOLOWMODEL

11

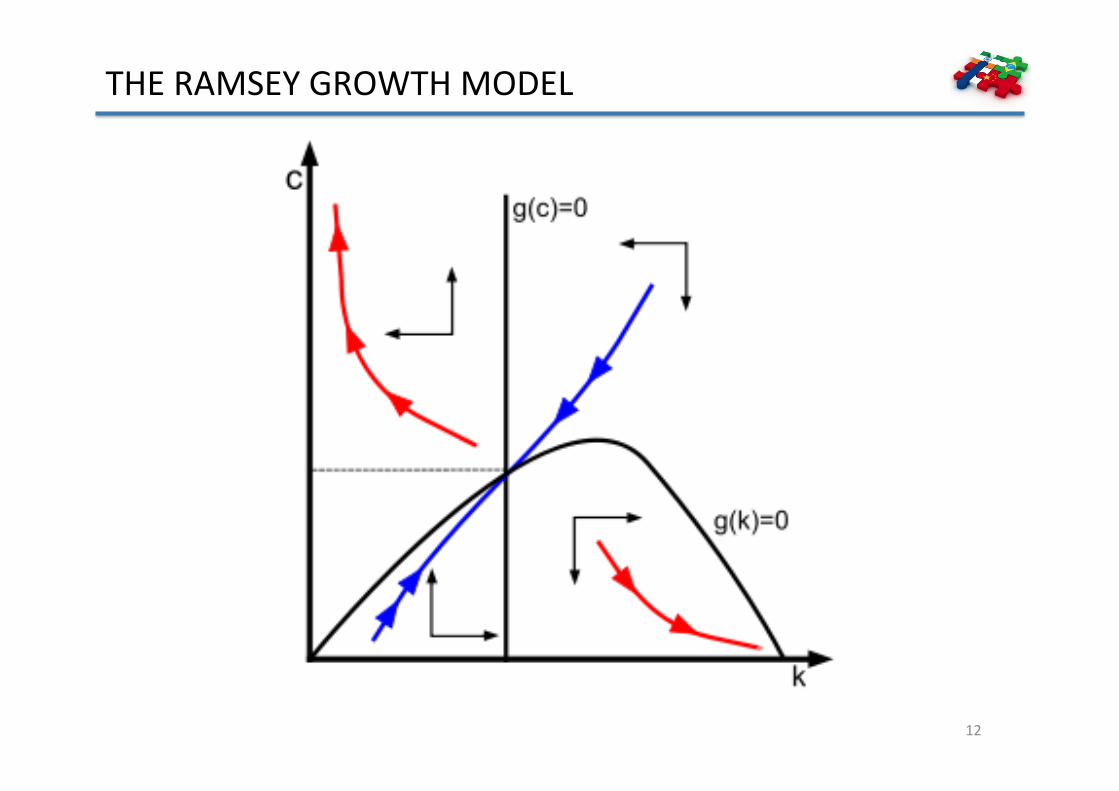

THERAMSEYGROWTHMODEL

12

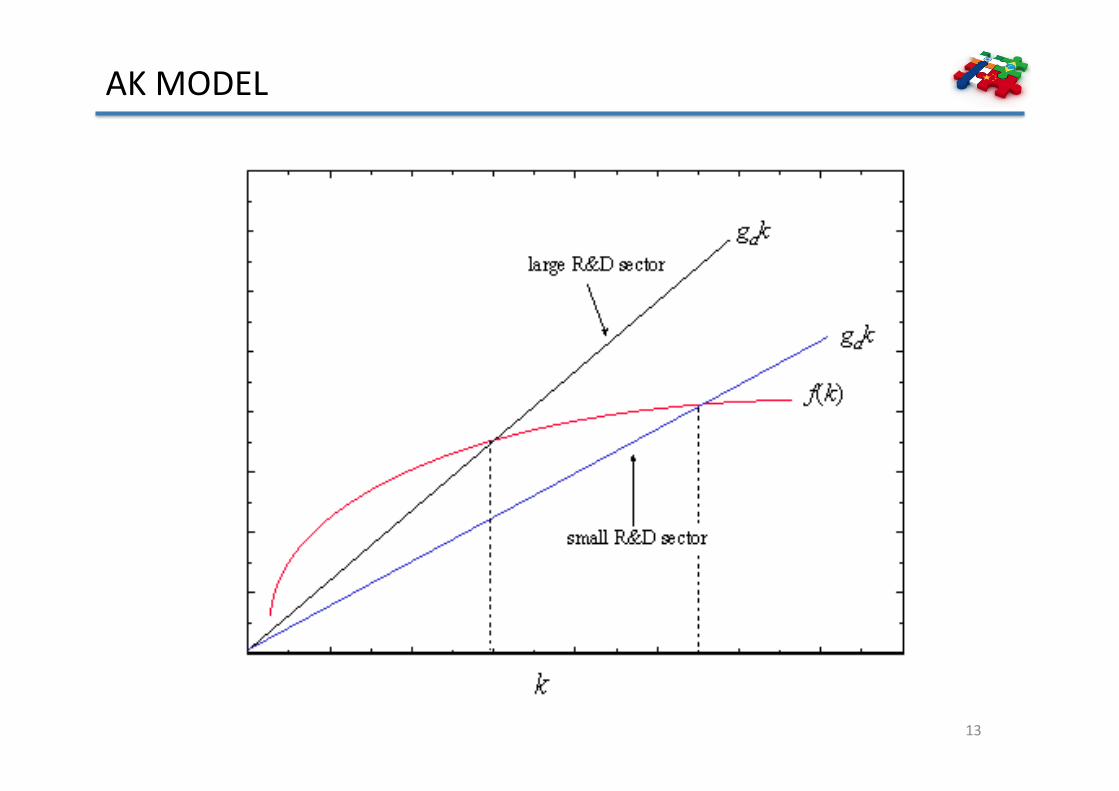

AKMODEL

13

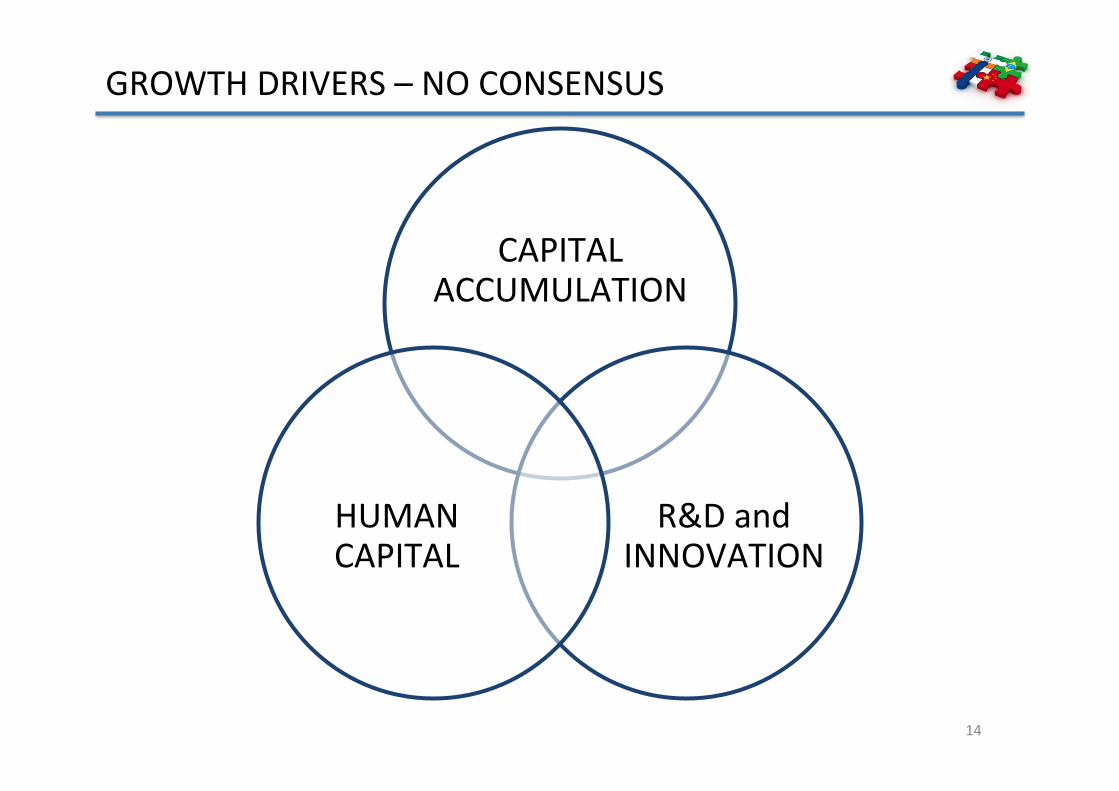

GROWTHDRIVERS–NOCONSENSUS

CAPITALACCUMULATION

R&DandINNOVATION

HUMANCAPITAL

14

Theywanted…Theyjustwereallowed…

15

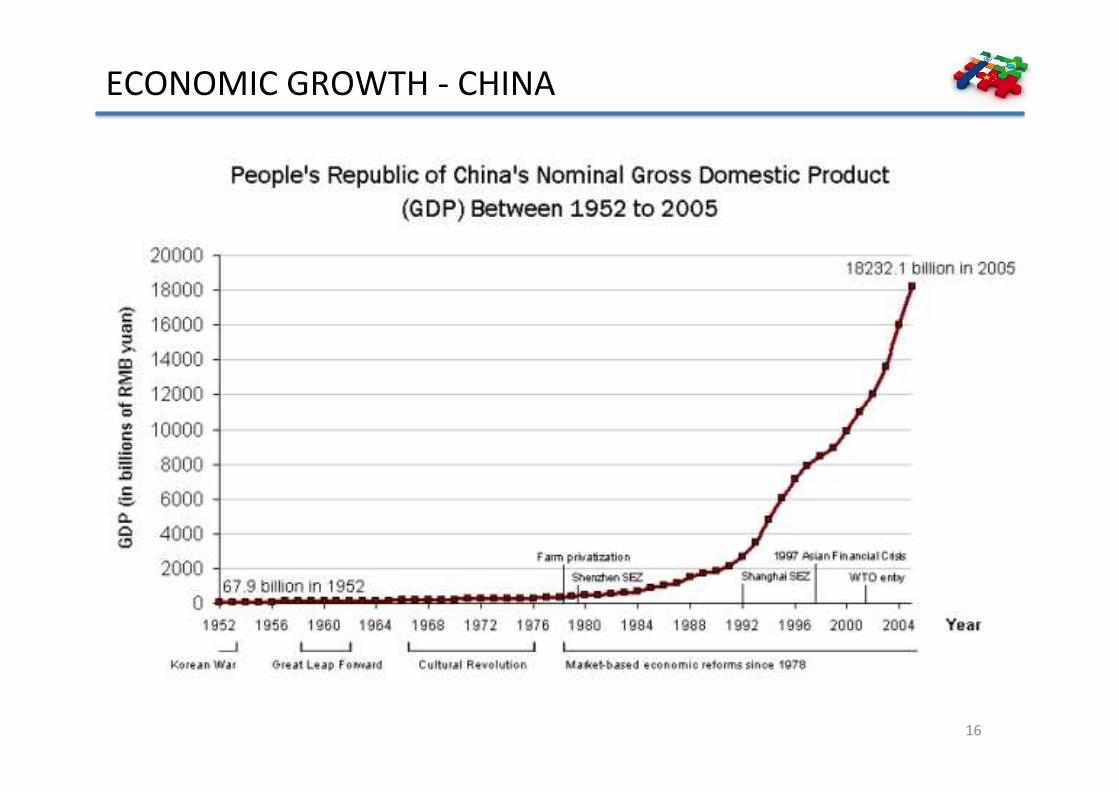

ECONOMICGROWTH‐CHINA

16

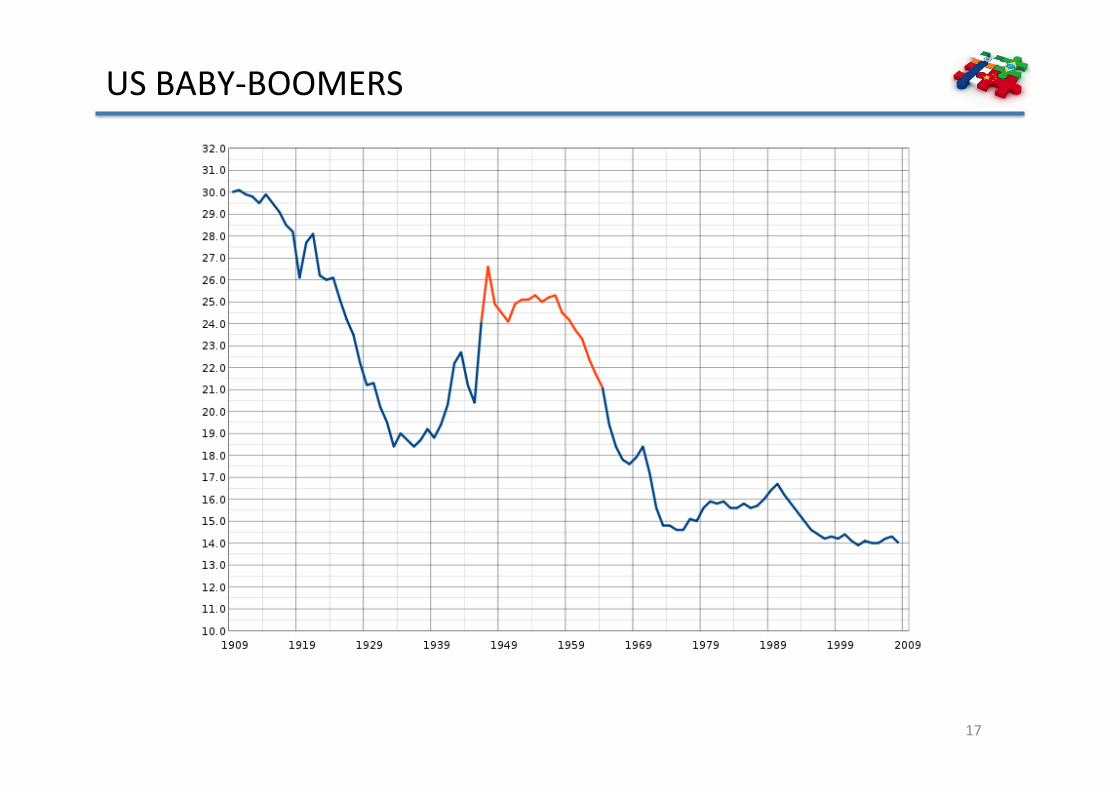

USBABY‐BOOMERS

17

WHO’SACULPRIT???

18

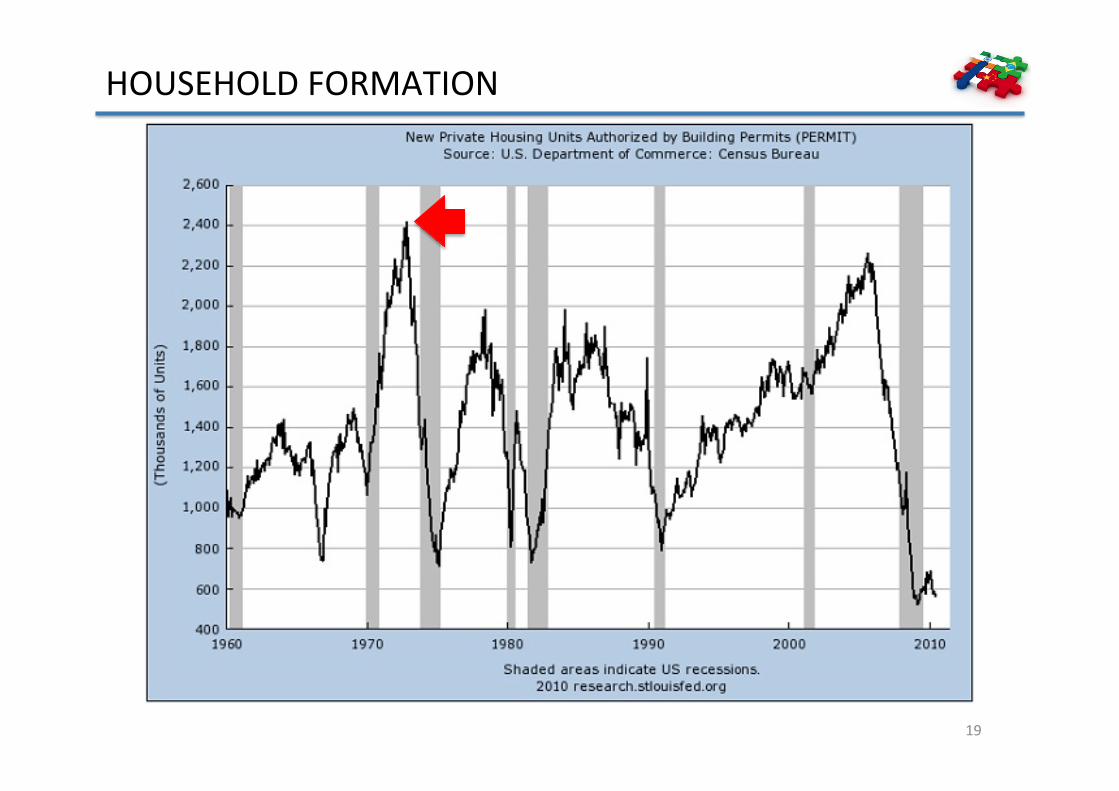

HOUSEHOLDFORMATION

19

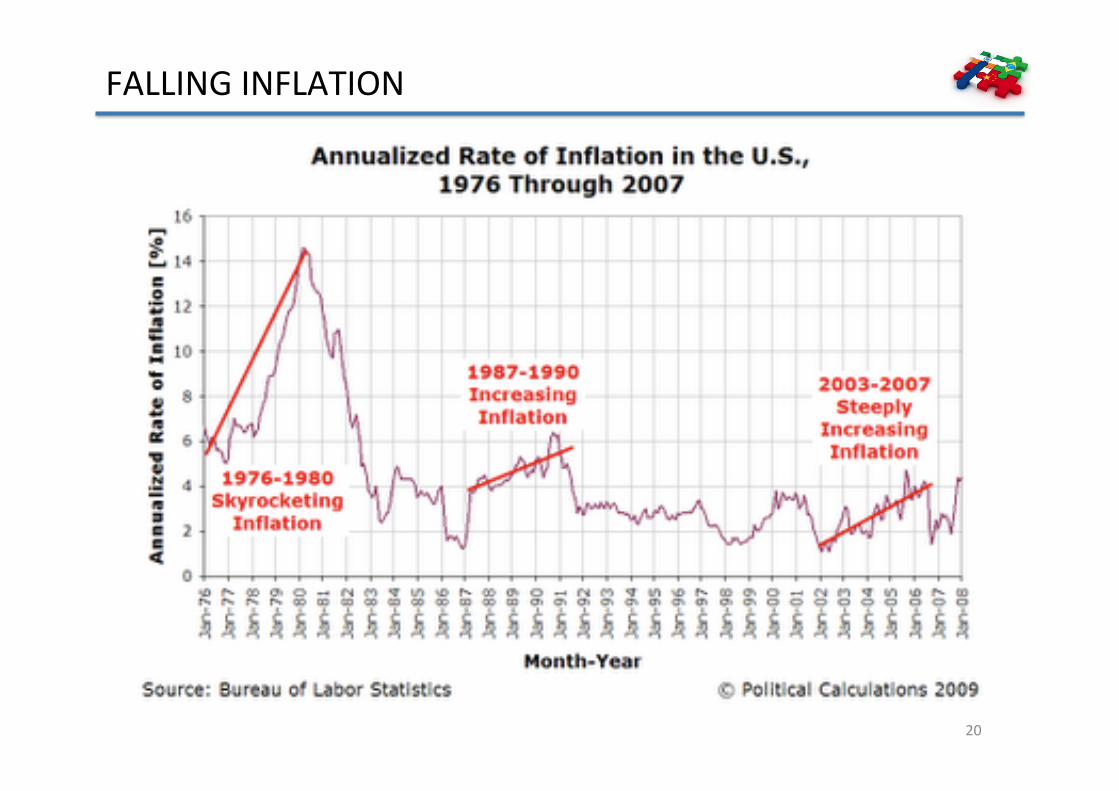

FALLINGINFLATION

20

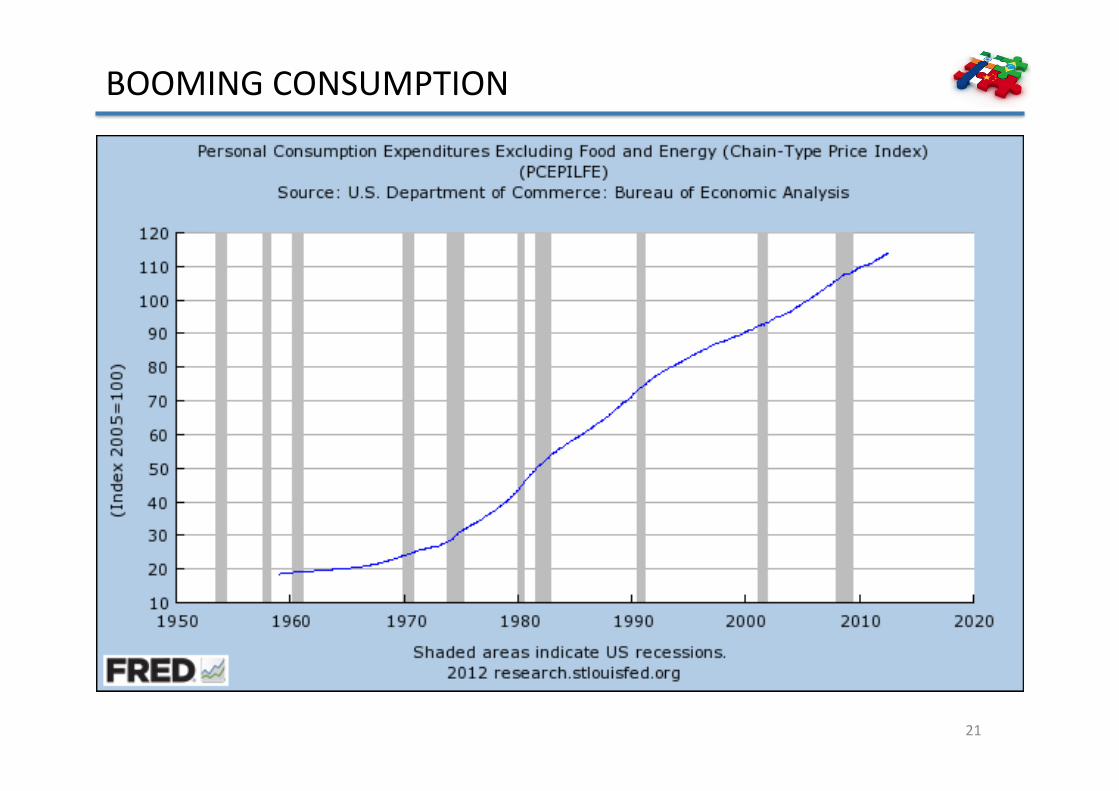

BOOMINGCONSUMPTION

21

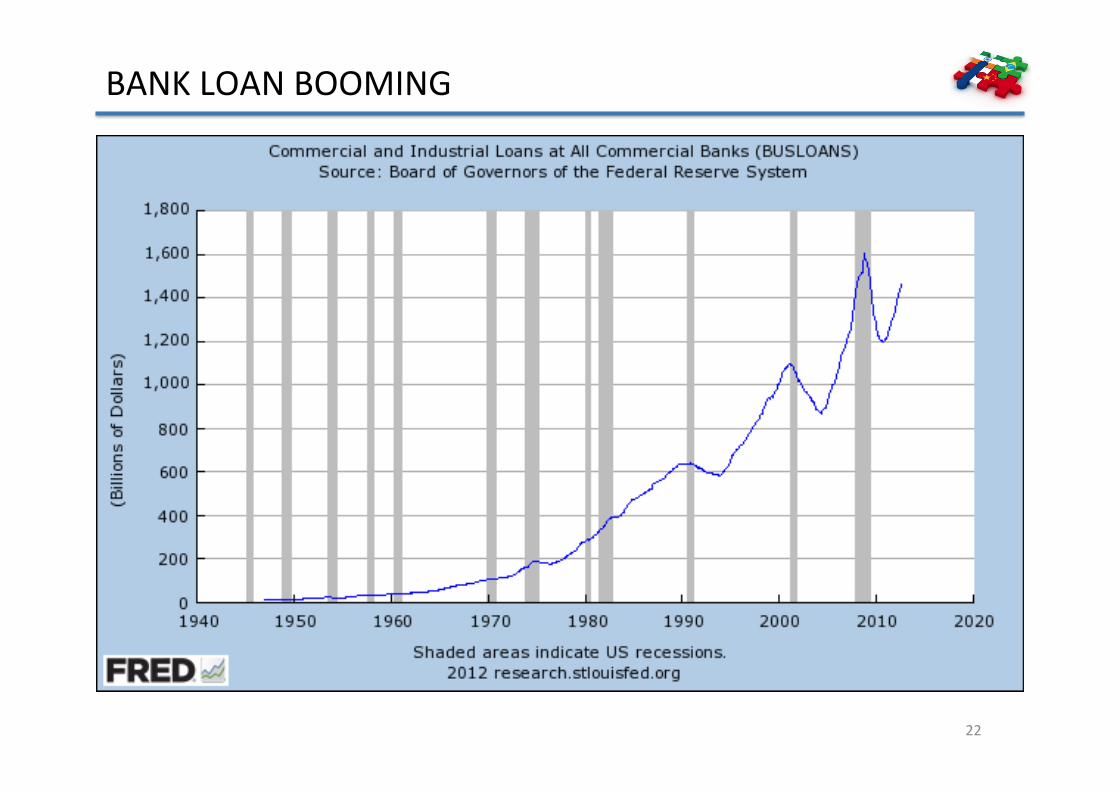

BANKLOANBOOMING

22

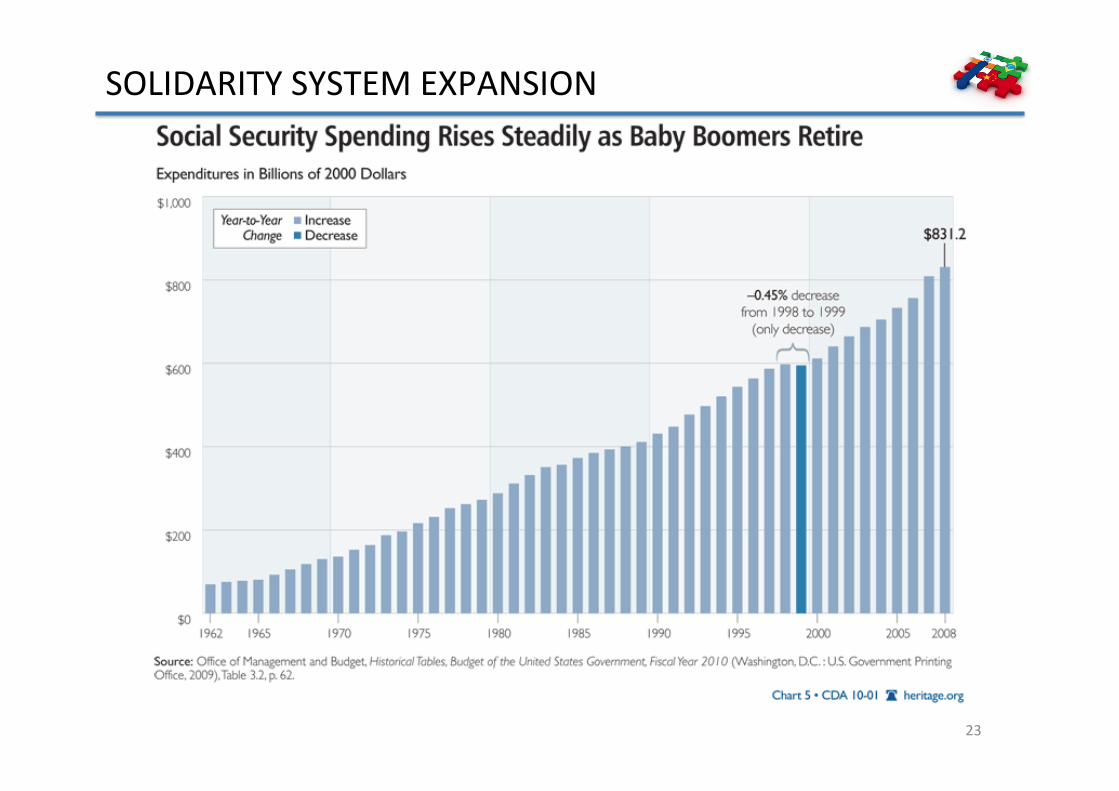

SOLIDARITYSYSTEMEXPANSION

23

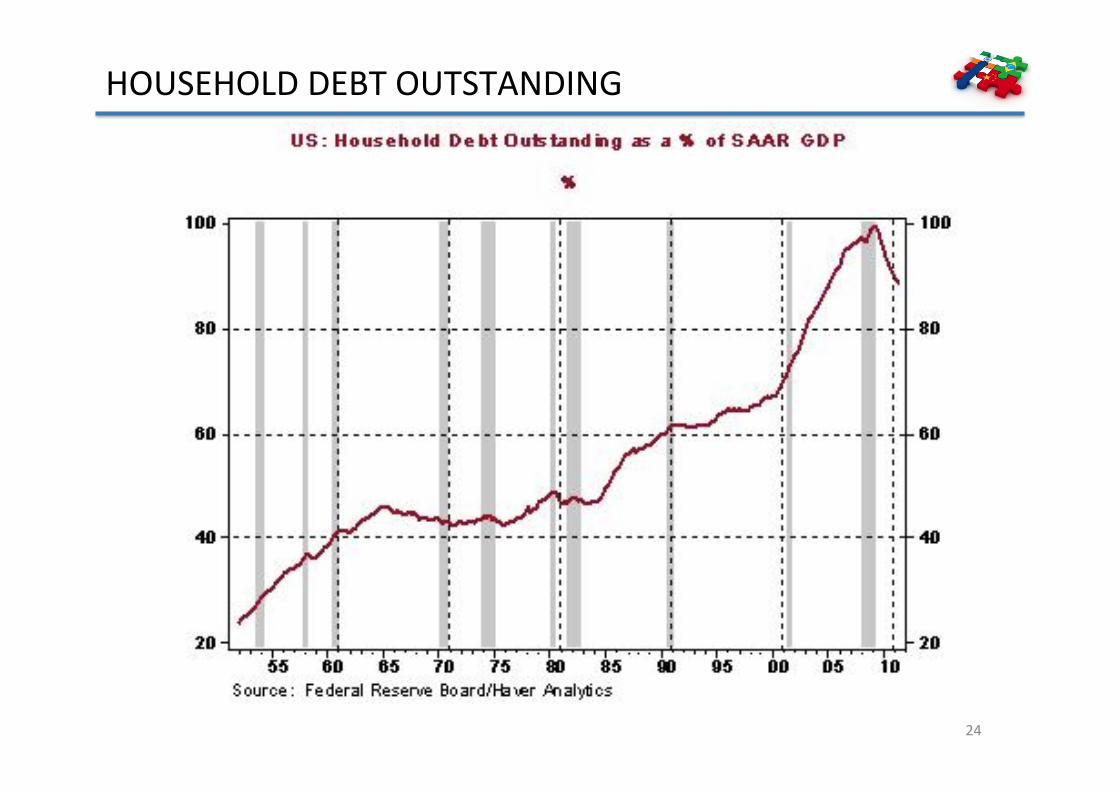

HOUSEHOLDDEBTOUTSTANDING

24

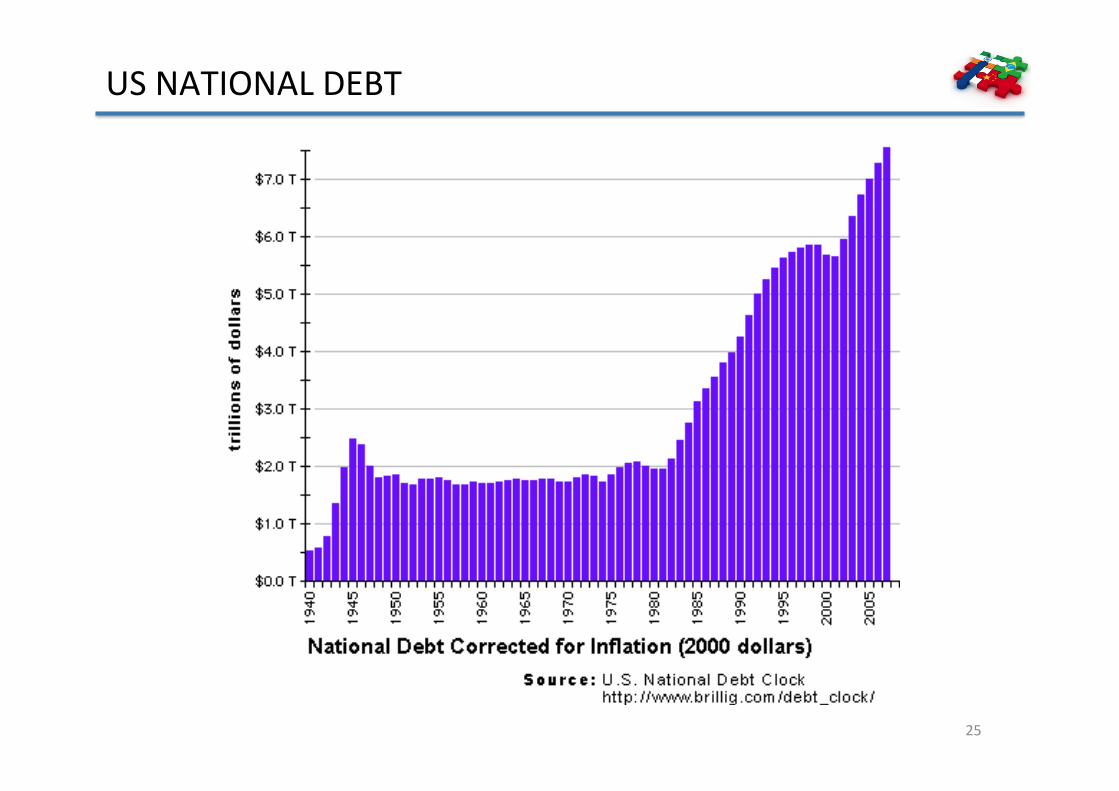

USNATIONALDEBT

25

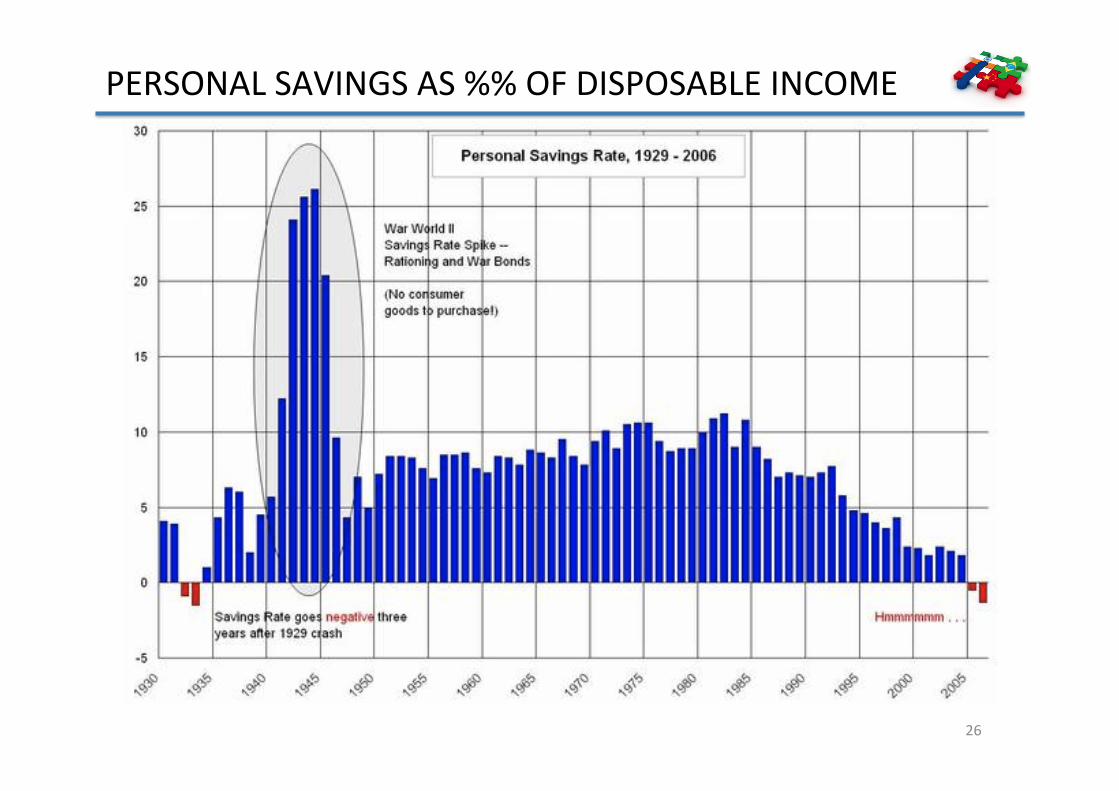

PERSONALSAVINGSAS%%OFDISPOSABLEINCOME

26

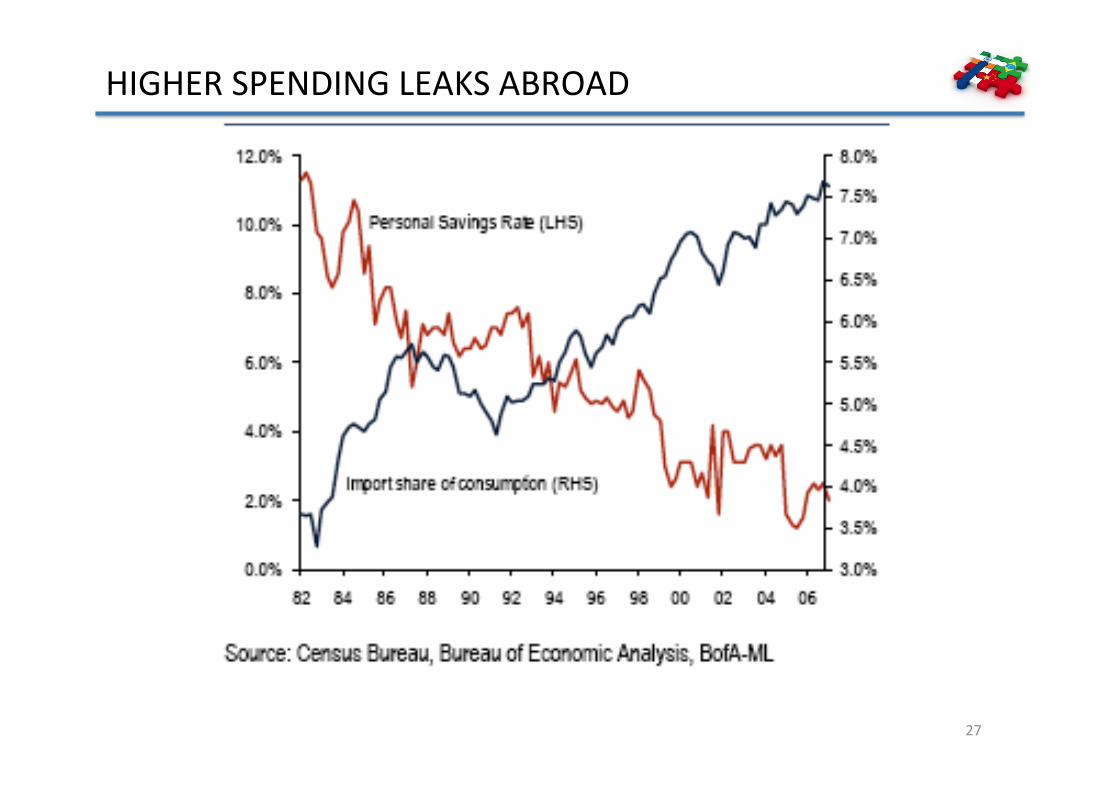

HIGHERSPENDINGLEAKSABROAD

27

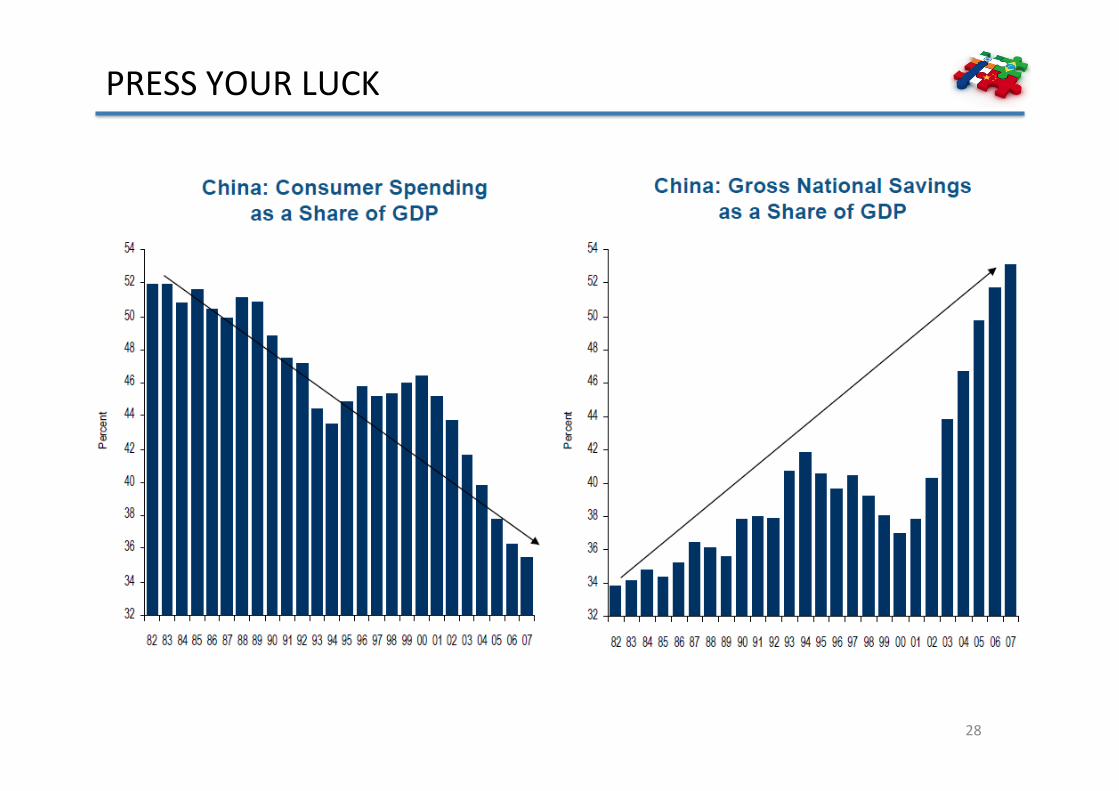

PRESSYOURLUCK

28

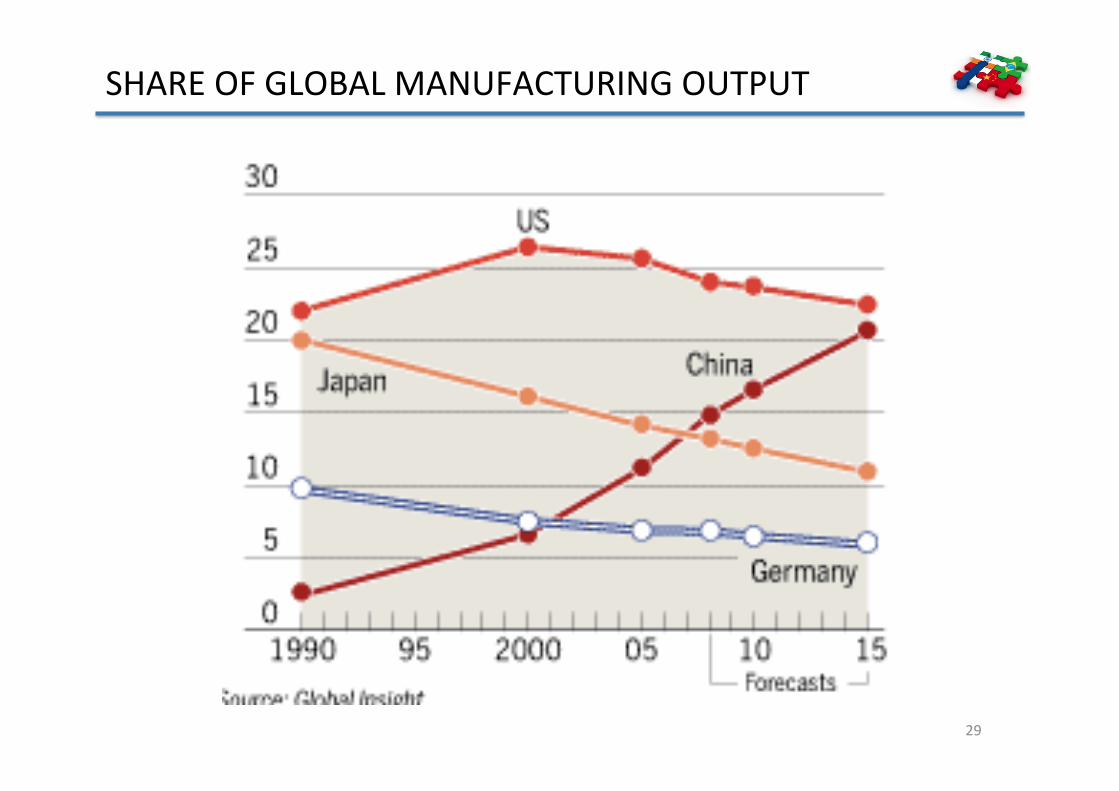

SHAREOFGLOBALMANUFACTURINGOUTPUT

29

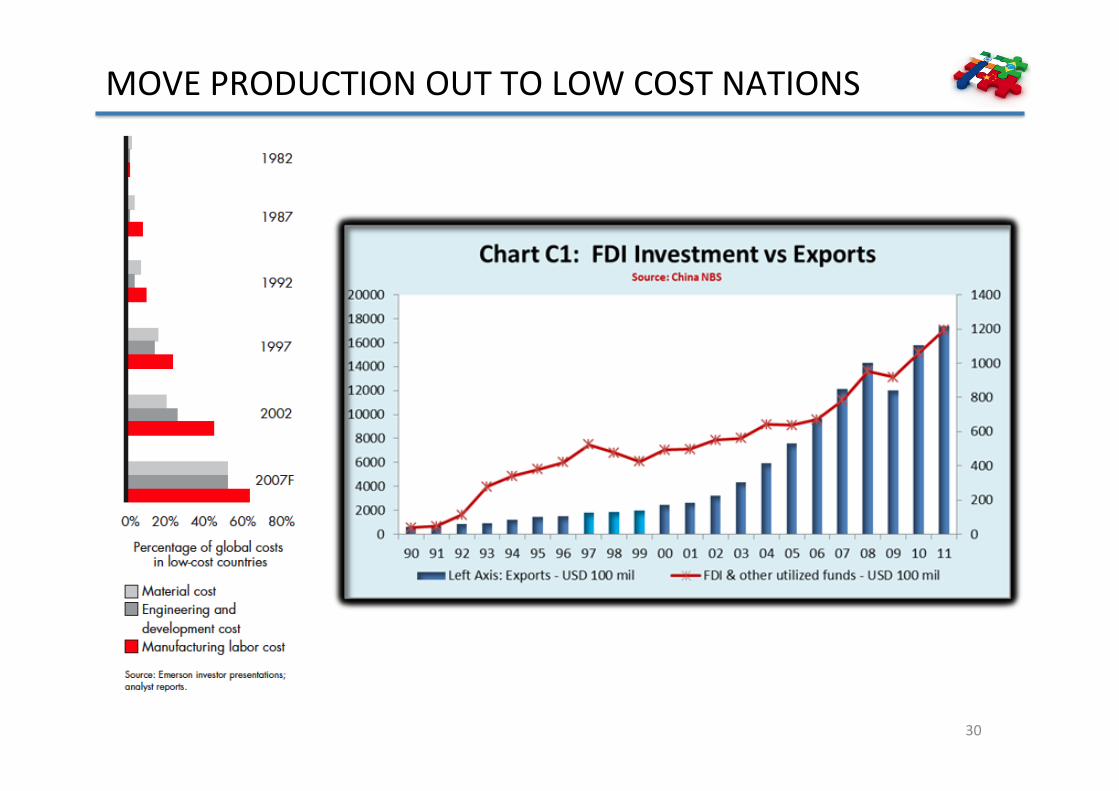

MOVEPRODUCTIONOUTTOLOWCOSTNATIONS

30

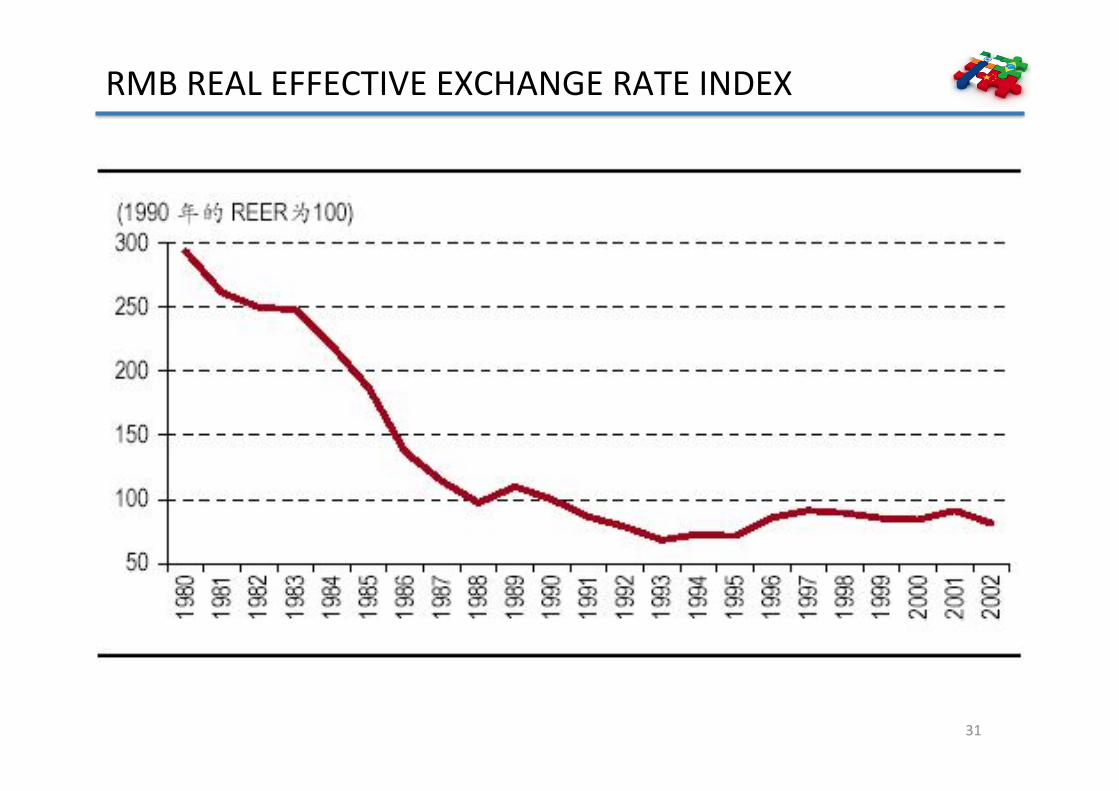

RMBREALEFFECTIVEEXCHANGERATEINDEX

31

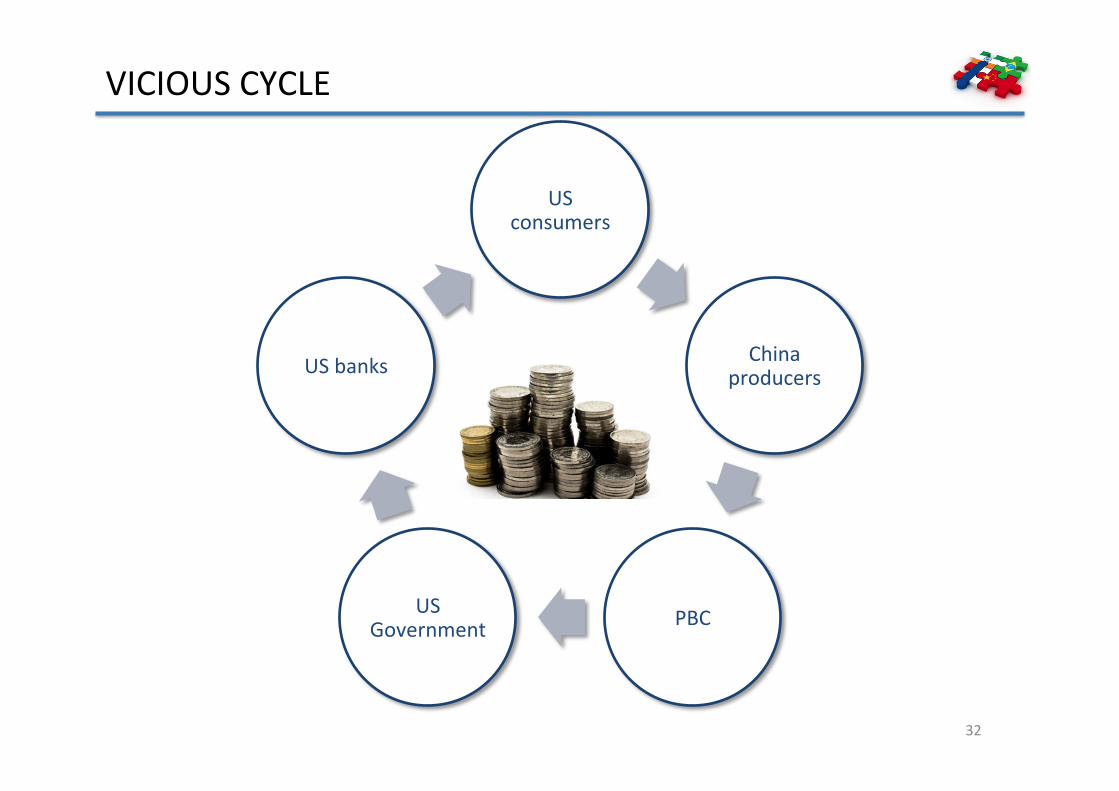

VICIOUSCYCLE

USconsumers

Chinaproducers

PBCUSGovernment

USbanks

32

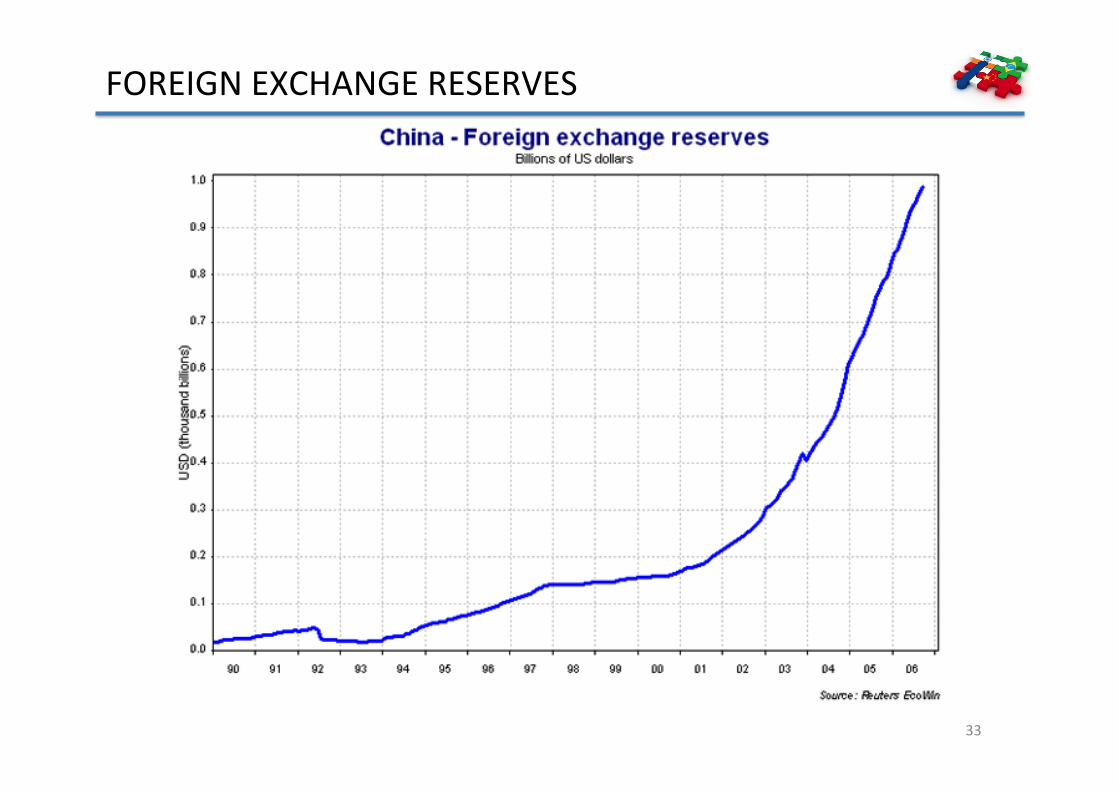

FOREIGNEXCHANGERESERVES

33

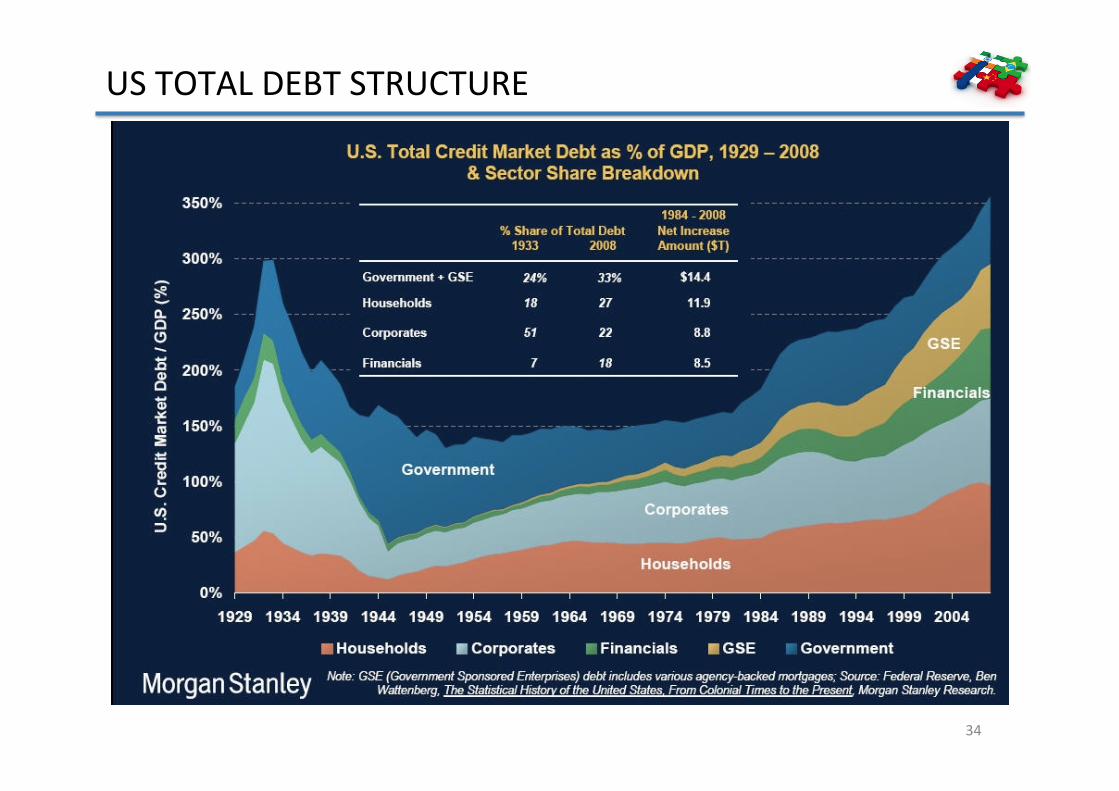

USTOTALDEBTSTRUCTURE

34

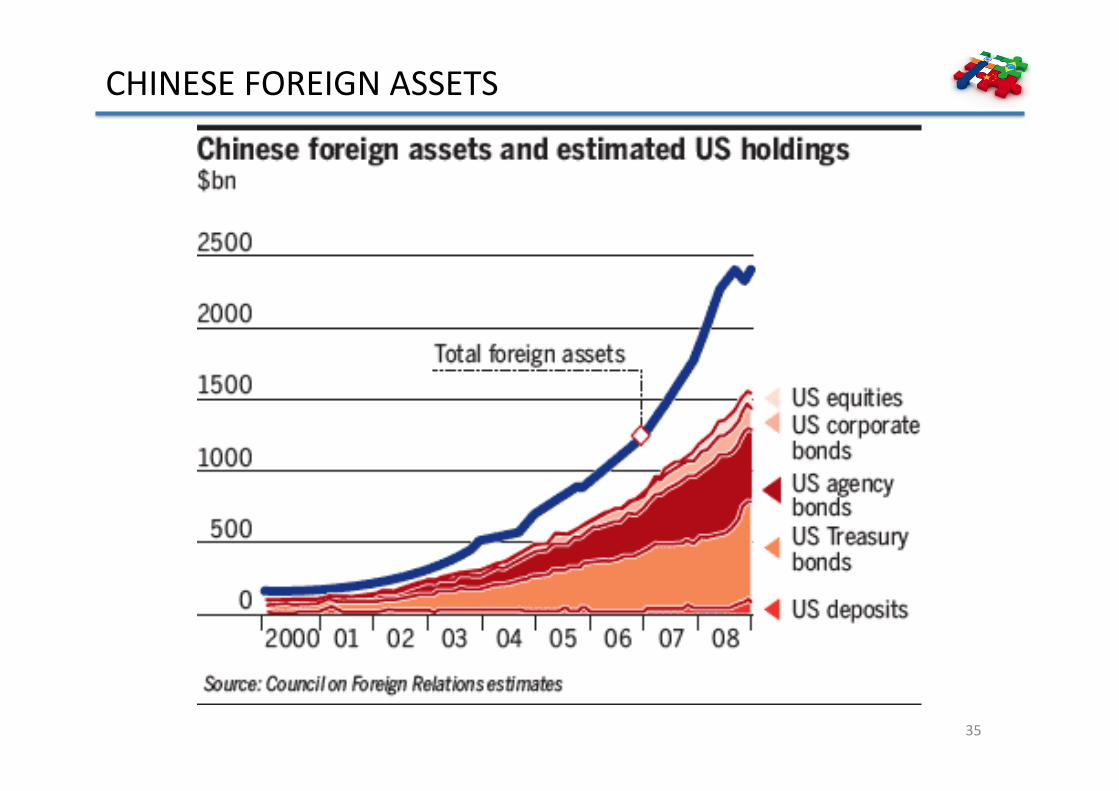

CHINESEFOREIGNASSETS

35

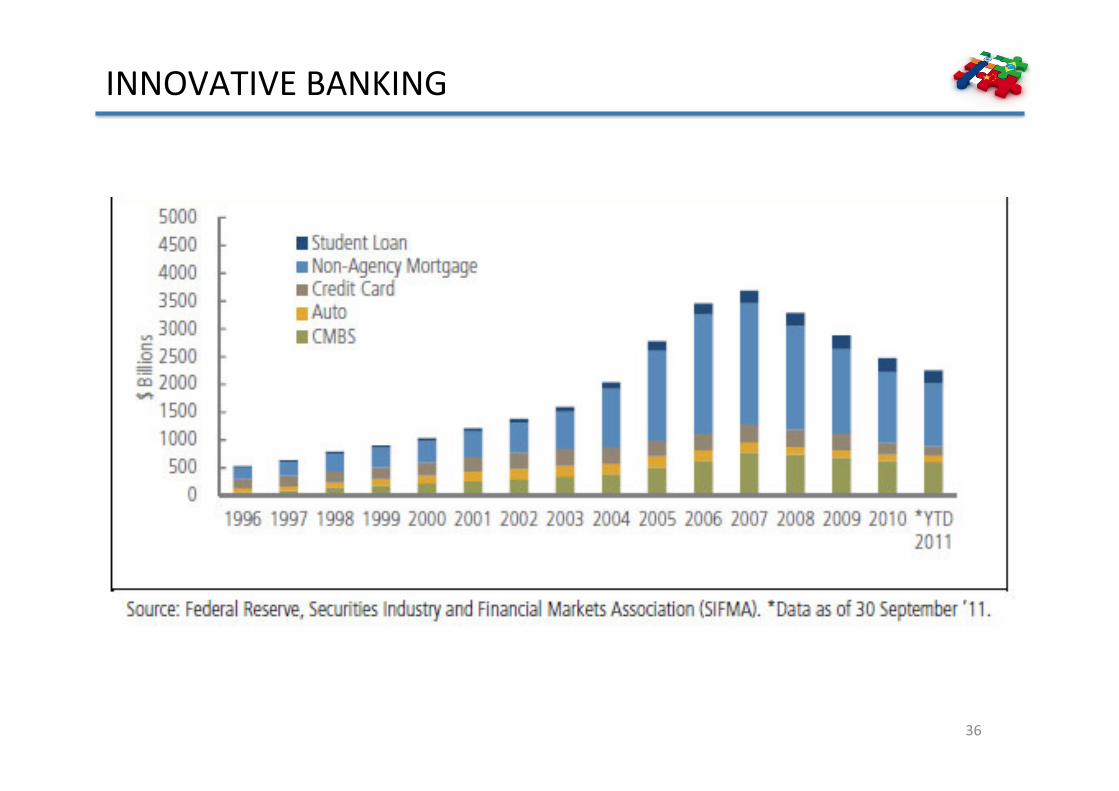

INNOVATIVEBANKING

36

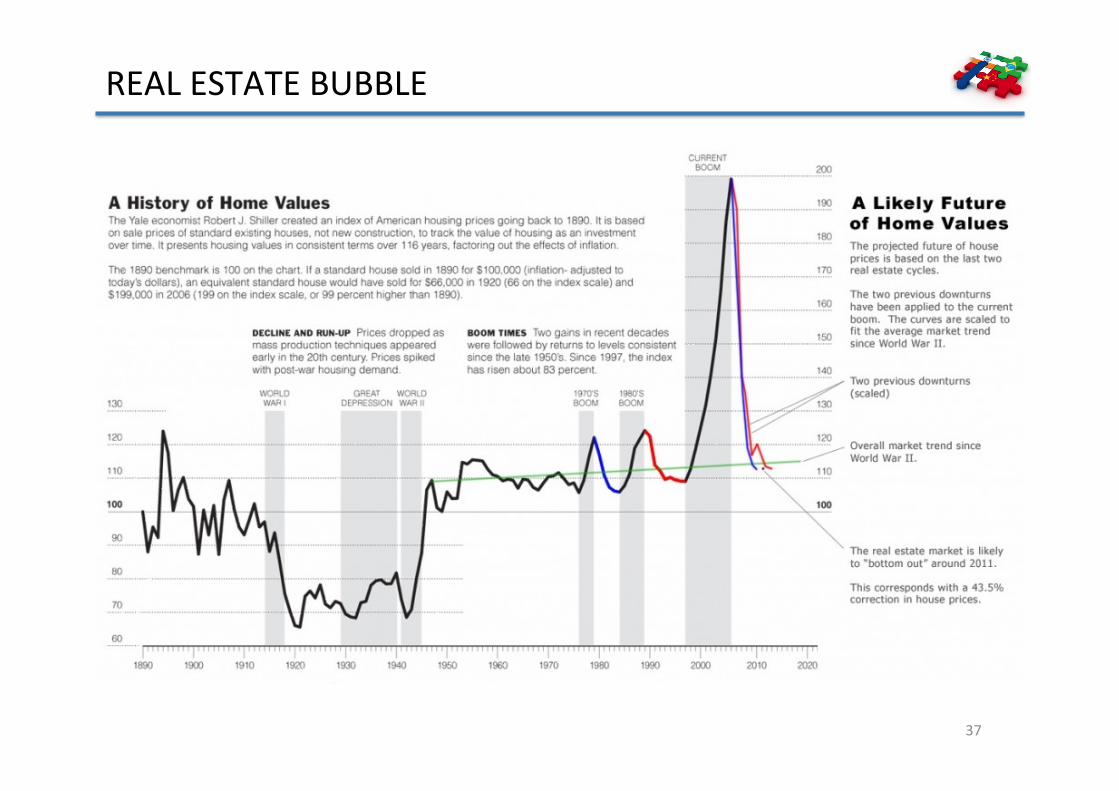

REALESTATEBUBBLE

37

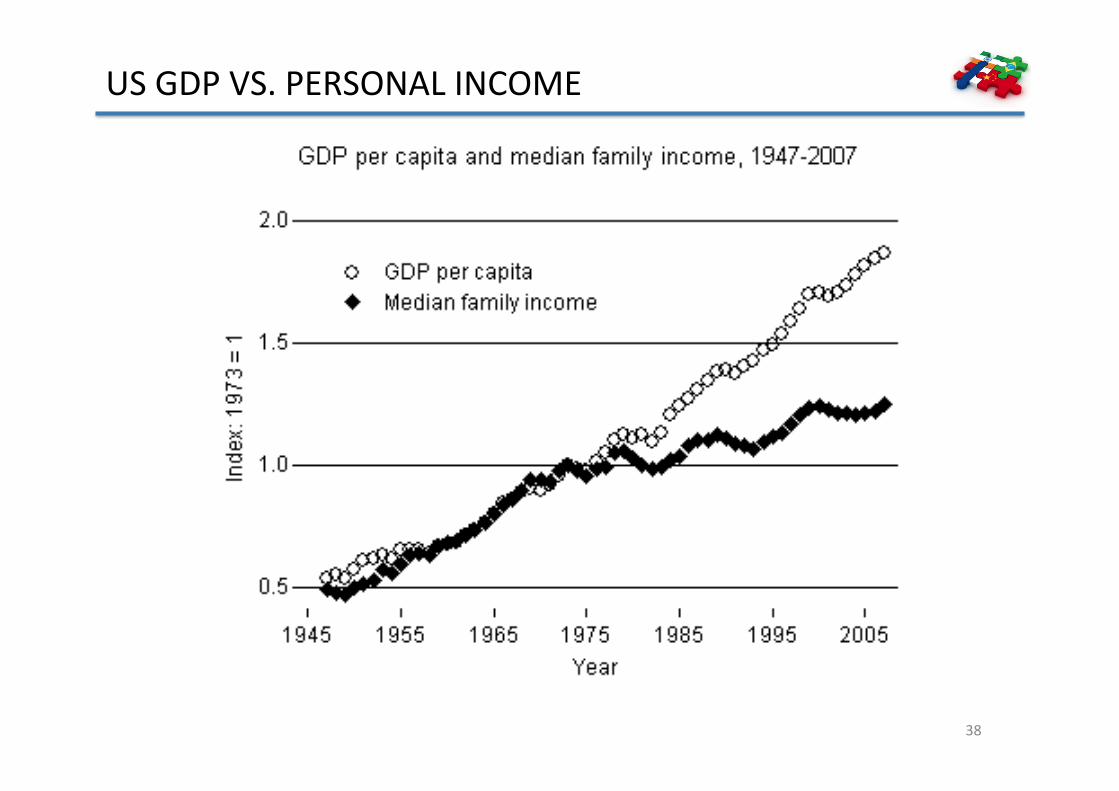

USGDPVS.PERSONALINCOME

38

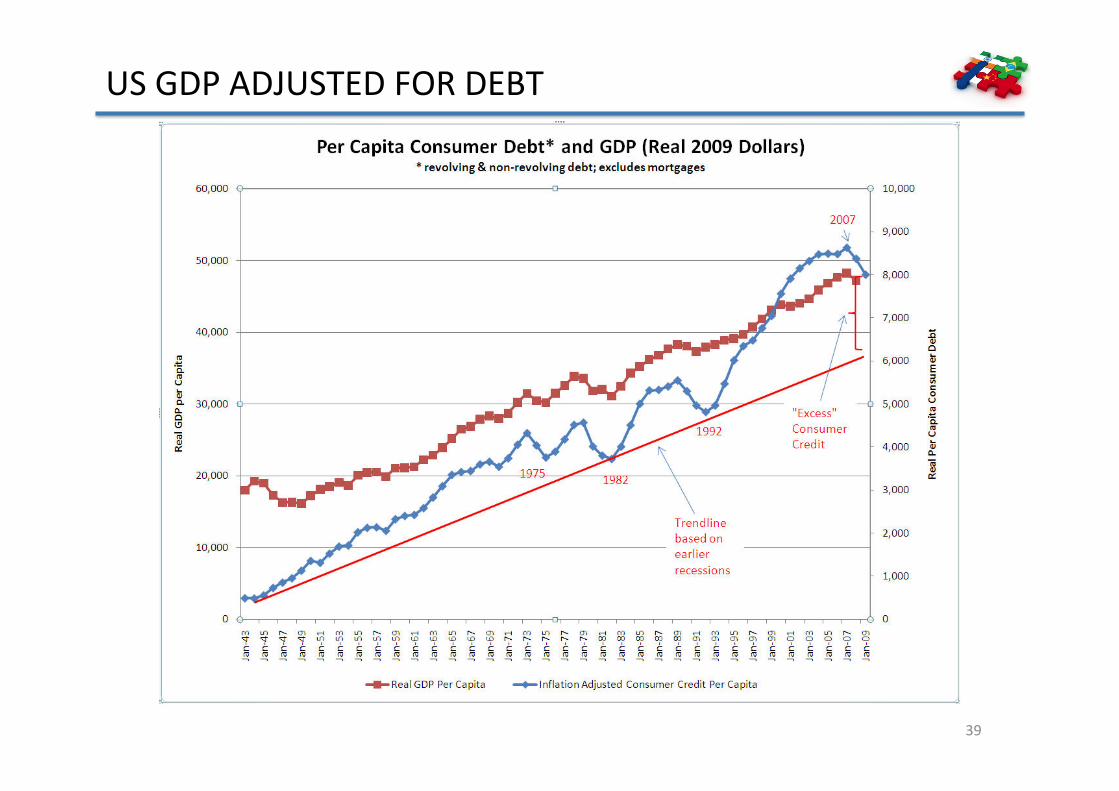

USGDPADJUSTEDFORDEBT

39

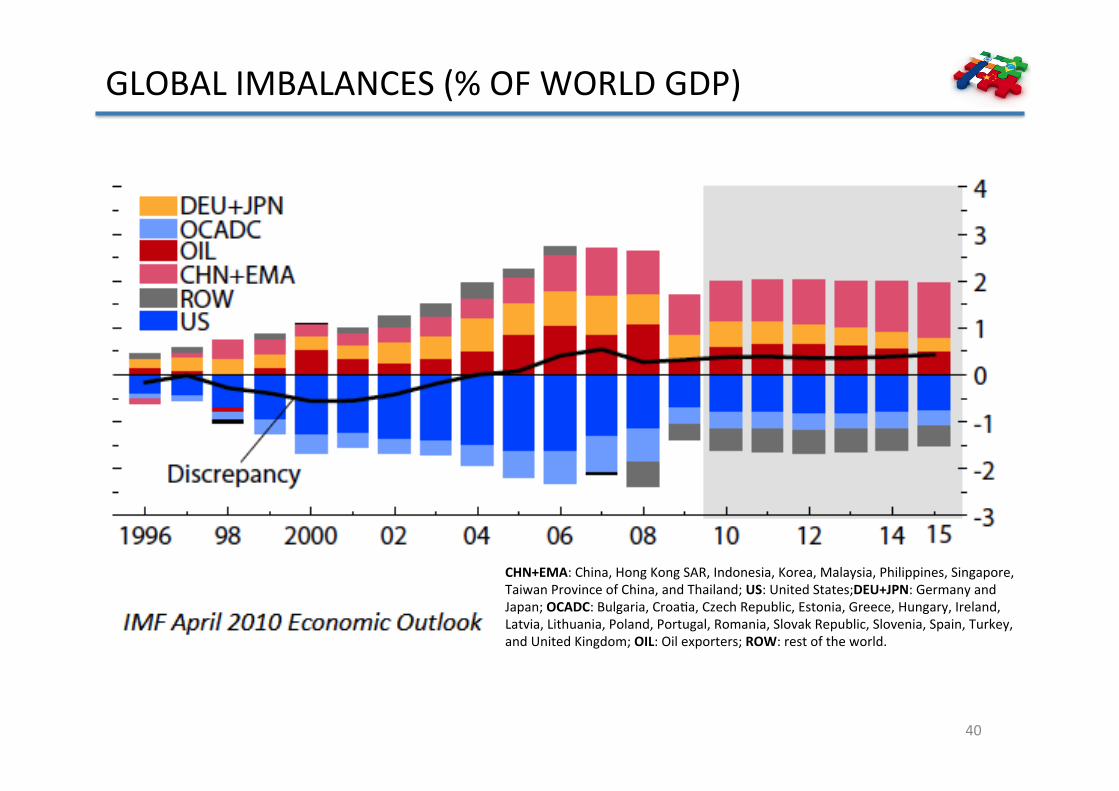

GLOBALIMBALANCES(%OFWORLDGDP)

40

CHN+EMA:China,HongKongSAR,Indonesia,Korea,Malaysia,Philippines,Singapore,TaiwanProvinceofChina,andThailand;US:UnitedStates;DEU+JPN:GermanyandJapan;OCADC:Bulgaria,CroaMa,CzechRepublic,Estonia,Greece,Hungary,Ireland,Latvia,Lithuania,Poland,Portugal,Romania,SlovakRepublic,Slovenia,Spain,Turkey,andUnitedKingdom;OIL:Oilexporters;ROW:restoftheworld.

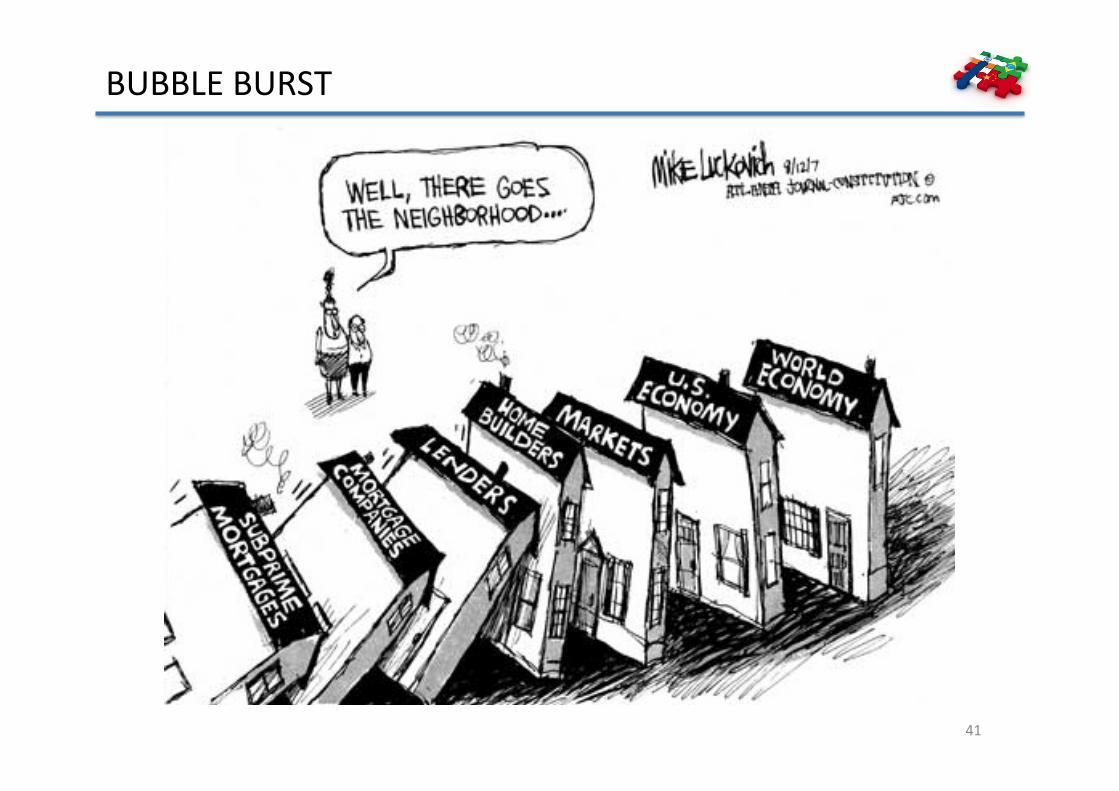

BUBBLEBURST

41

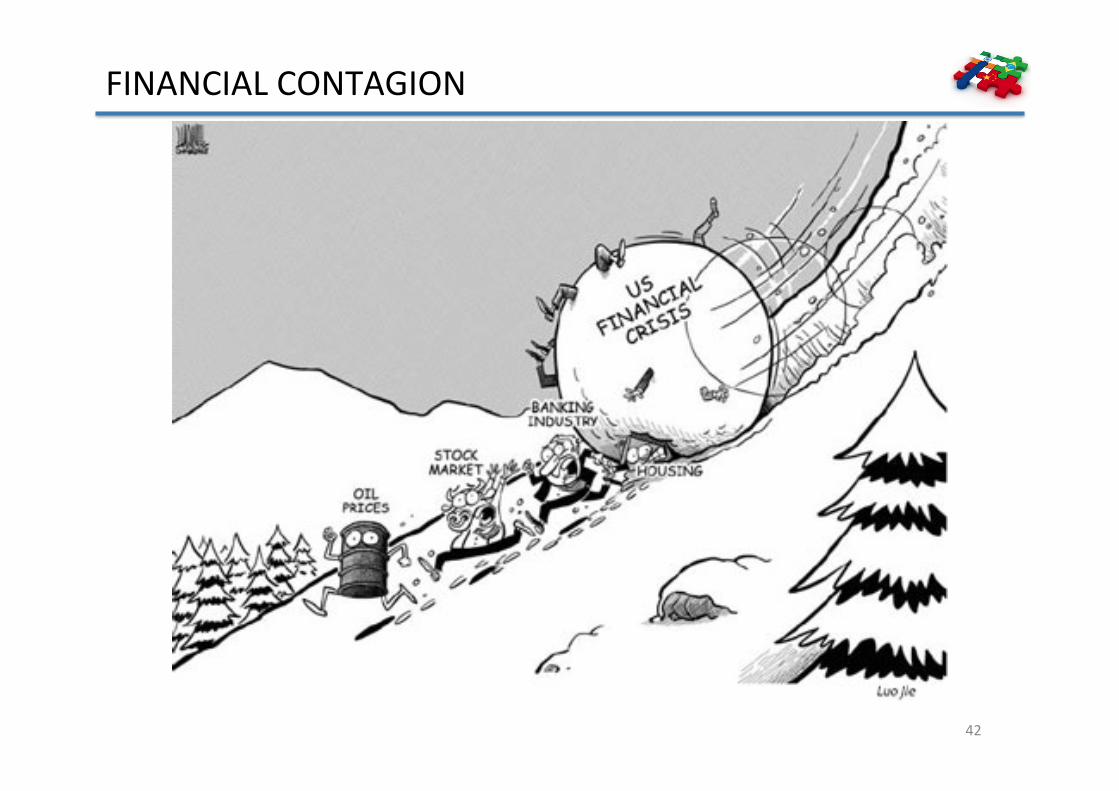

FINANCIALCONTAGION

42

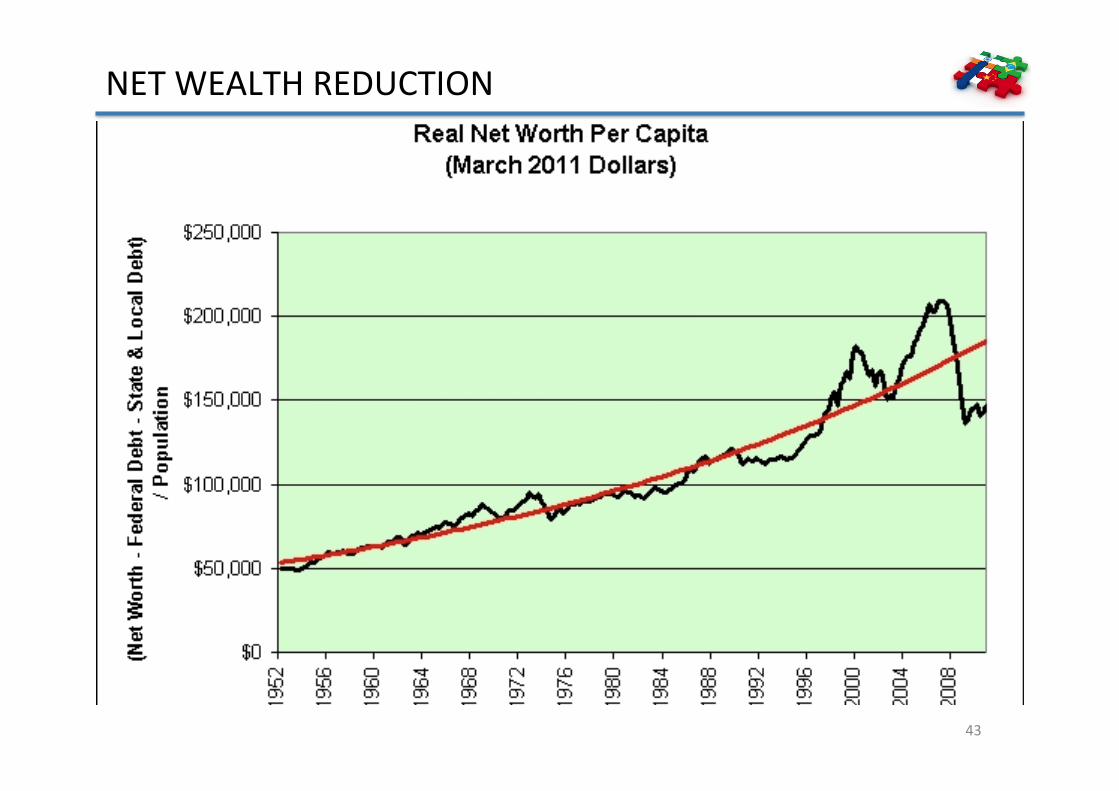

NETWEALTHREDUCTION

43

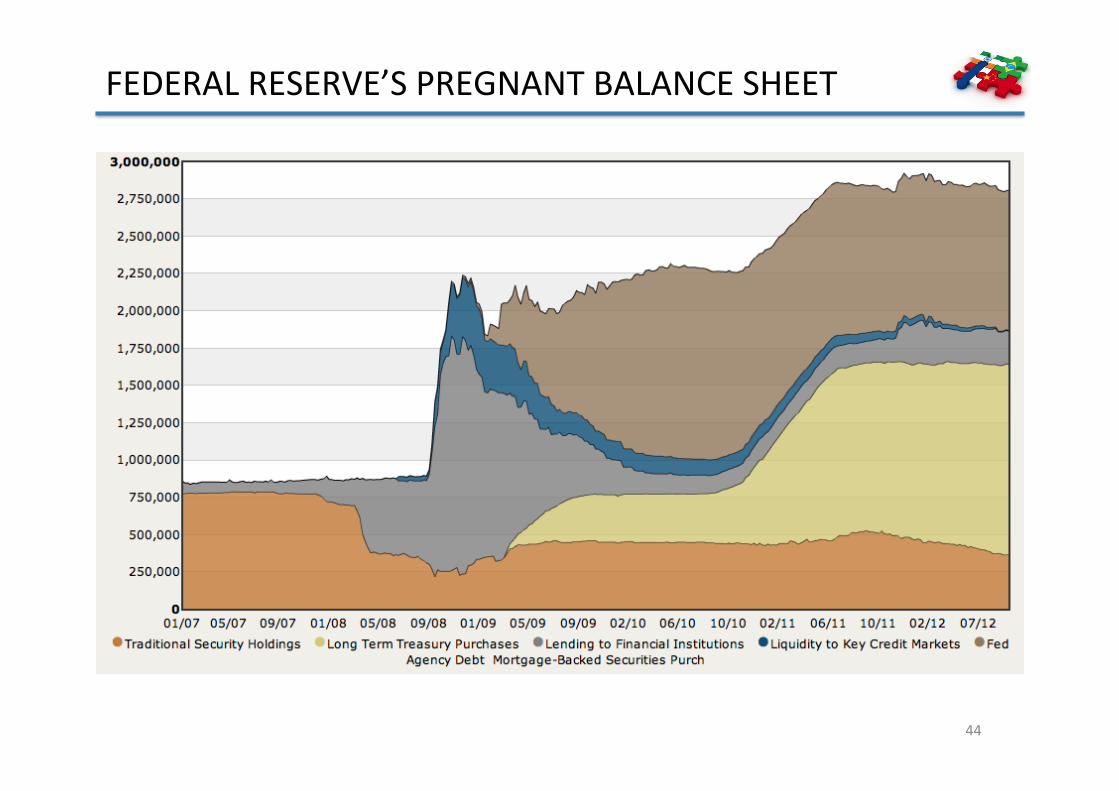

FEDERALRESERVE’SPREGNANTBALANCESHEET

44

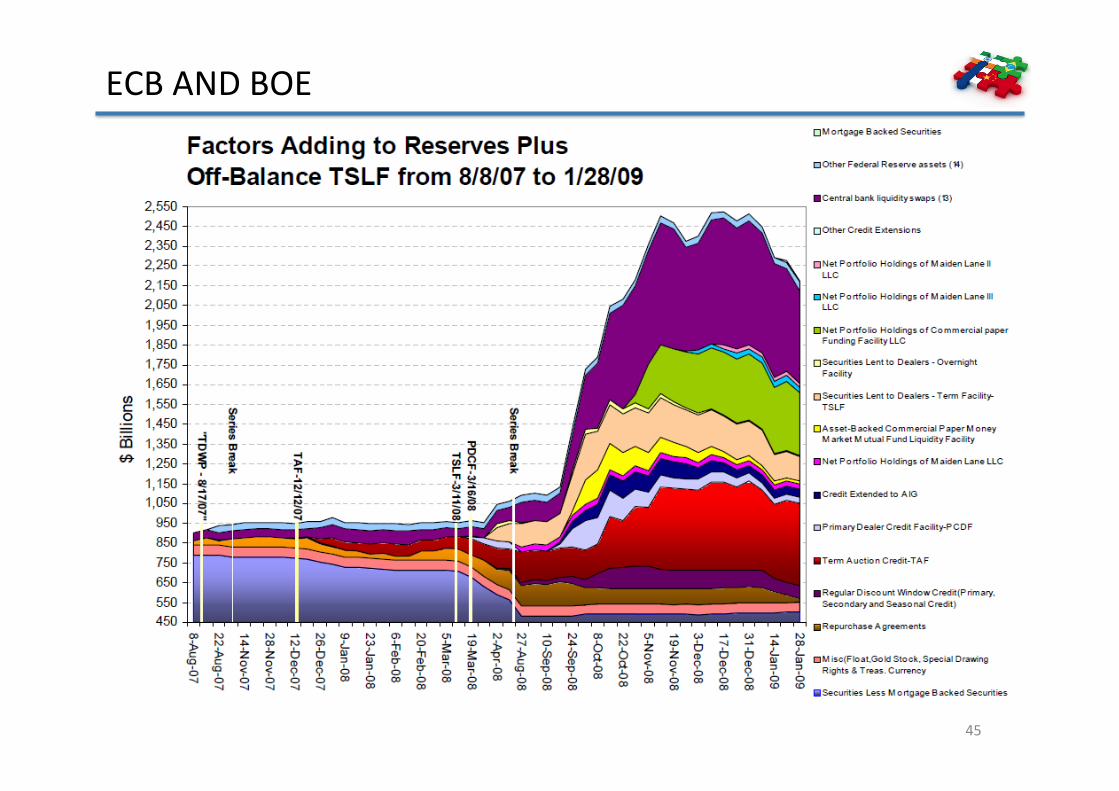

ECBANDBOE

45

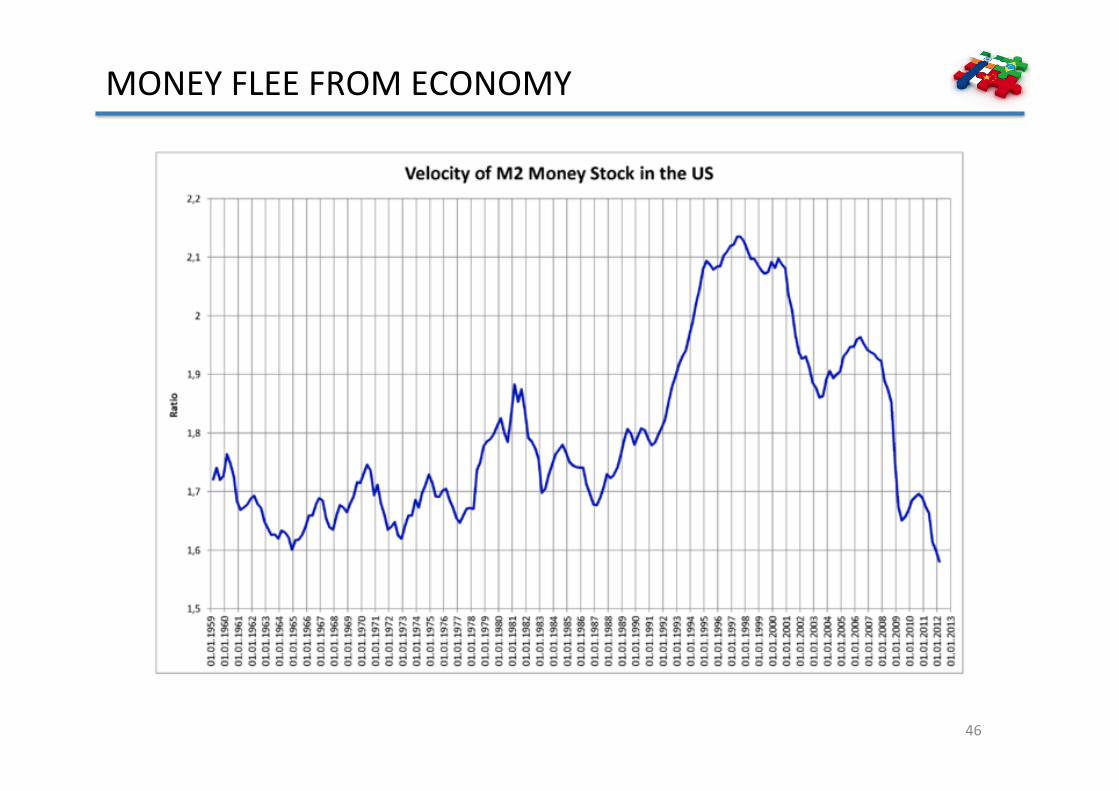

MONEYFLEEFROMECONOMY

46

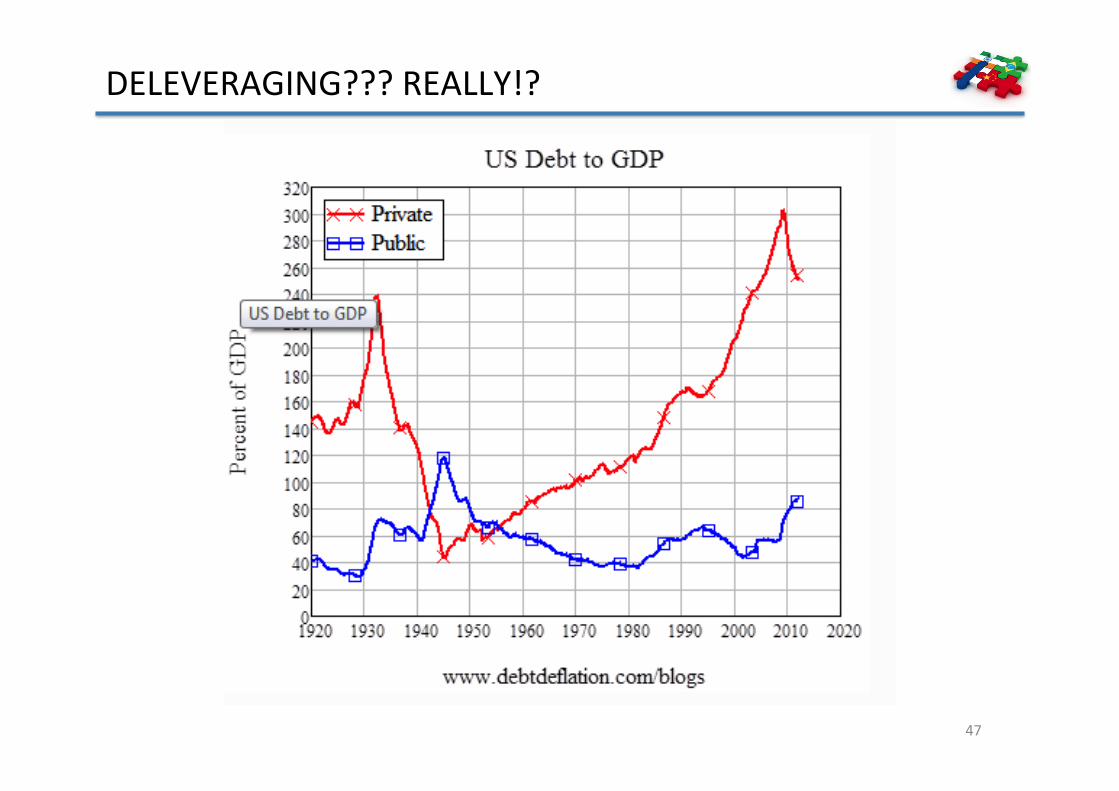

DELEVERAGING???REALLY!?

47

PARADIGMSHIFTS

48

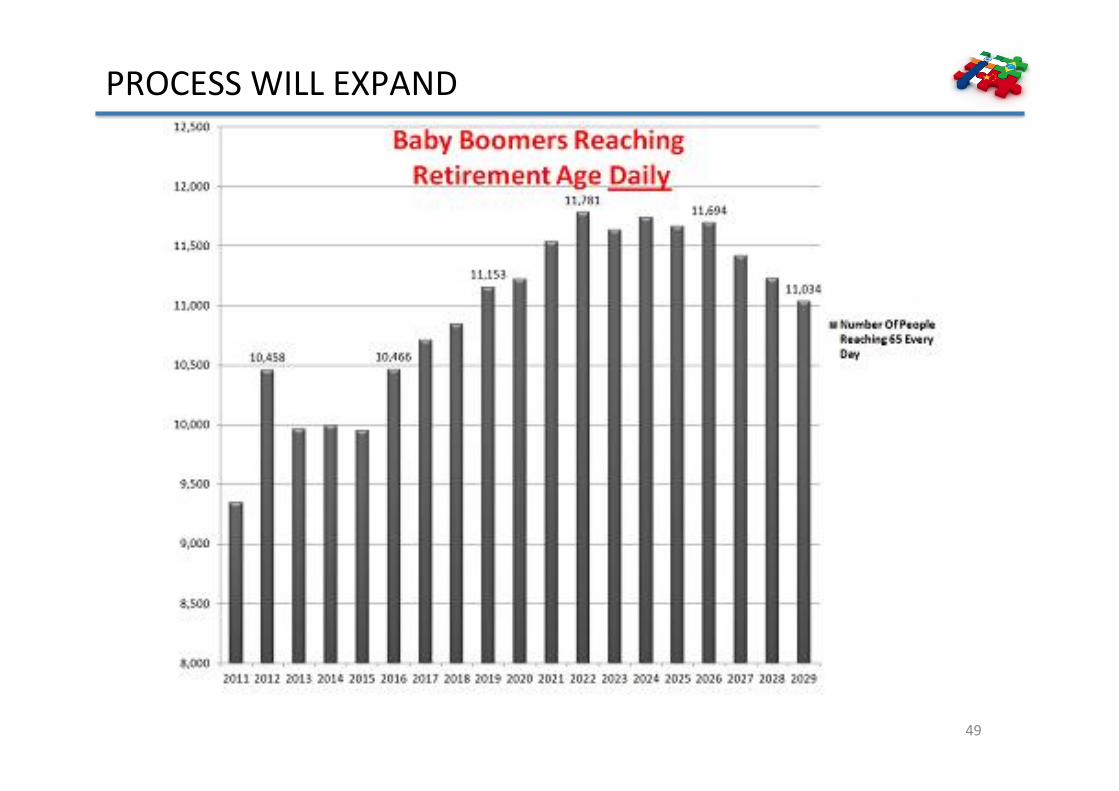

PROCESSWILLEXPAND

49

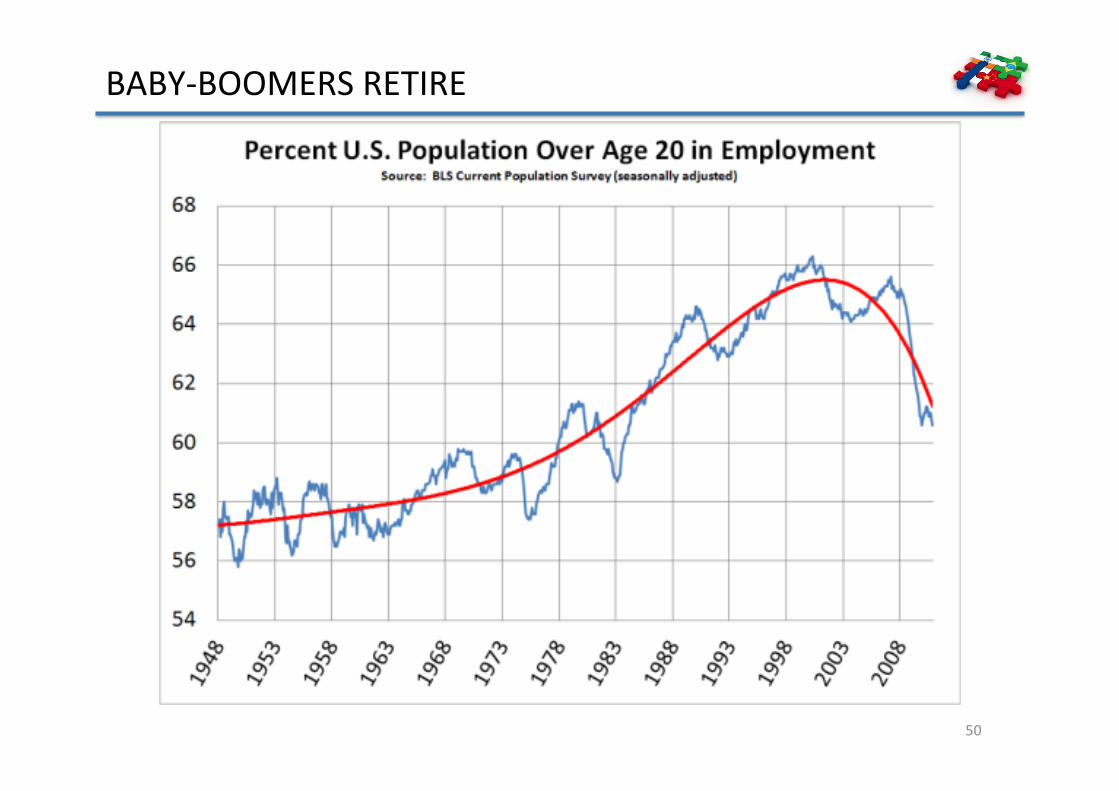

BABY‐BOOMERSRETIRE

50

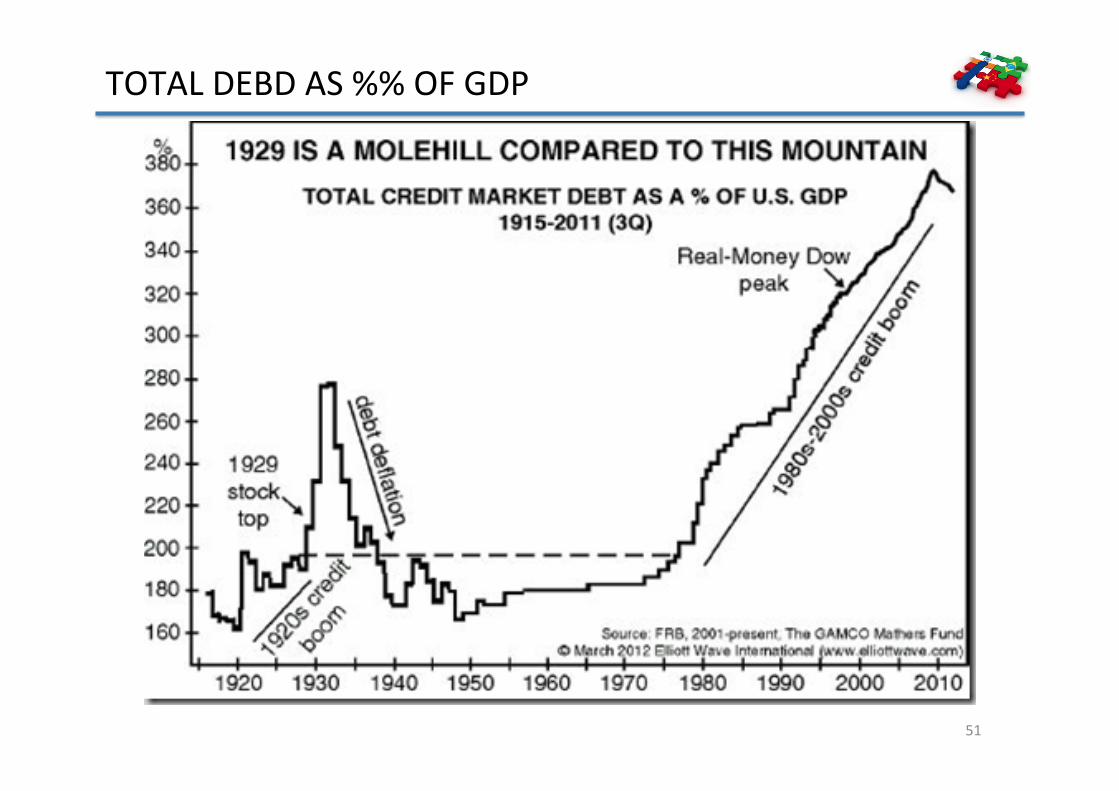

TOTALDEBDAS%%OFGDP

51

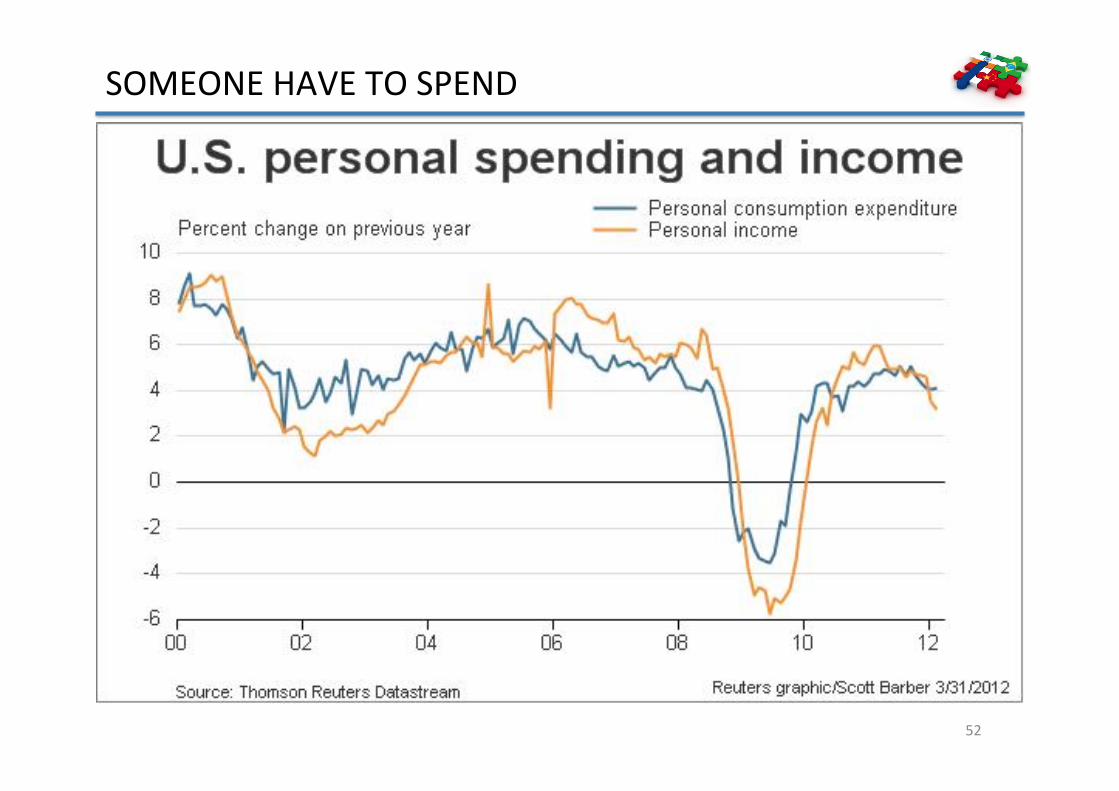

SOMEONEHAVETOSPEND

52

EMWILL???

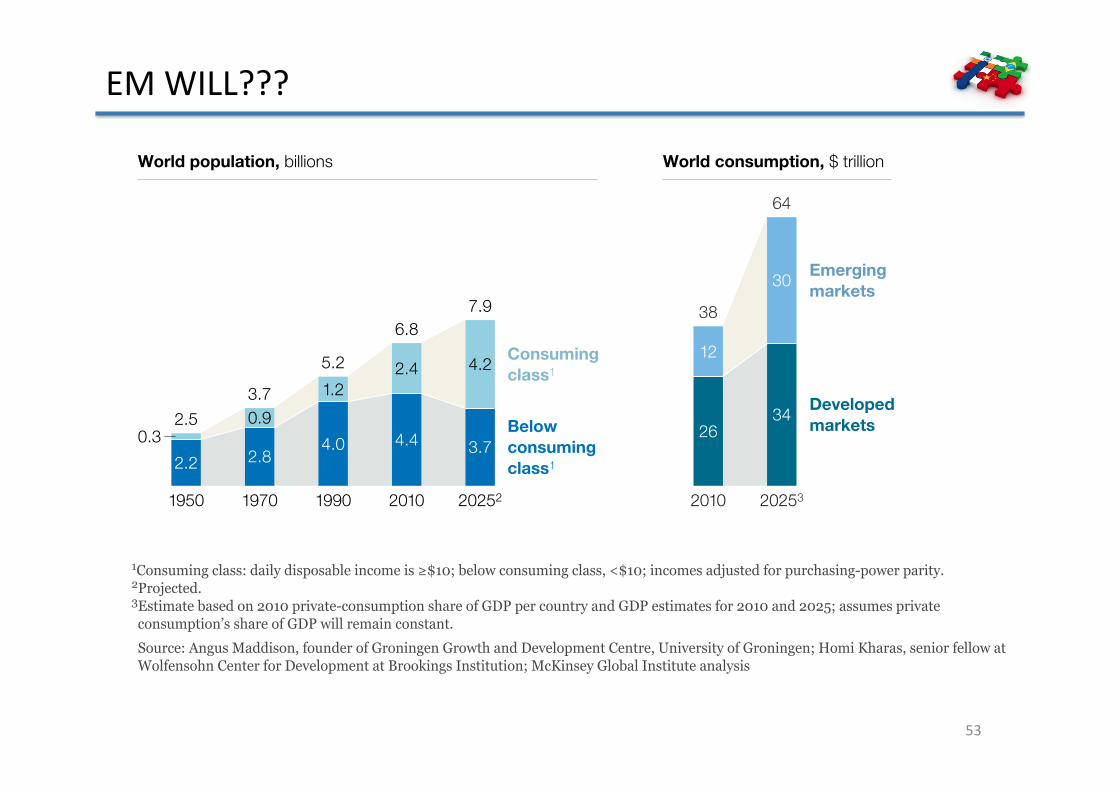

!

Exhibit 2 By 2025, the consuming class will swell to 4.2 billion people. Consumption in emerging markets will account for $30 trillion—nearly half of the global total.

Compendium$30 trillion decathlonExhibit 2 of 5

World population, billions World consumption, $ trillion

Consuming class1

Below consuming class1

0.3

1950

2.5

2.2

1970

3.70.9

2.8

1990

5.2

1.2

4.0

2010

6.8

2.4

4.4

20252

7.9

4.2

3.7

2010

38

12

26

20253

64

30

34

Emerging markets

Developed markets

!"#$%&'($)*+,-%%.*/-(,0*/(%1#%-2,3*($+#'3*(%*!4!56*23,#7*+#$%&'($)*+,-%%8*94!56*($+#'3%*-/:&%;3/*<#=*1&=+>-%($)?1#73=*1-=(;0@AB=#:3+;3/@*CD%;('-;3*2-%3/*#$*A5!5*1=(E-;3?+#$%&'1;(#$*%>-=3*#<*FGB*13=*+#&$;=0*-$/*FGB*3%;('-;3%*<#=*A5!5*-$/*A5AH6*-%%&'3%*1=(E-;3*+#$%&'1;(#$I%*%>-=3*#<*FGB*7(,,*=3'-($*+#$%;-$;@

* J#&=+3.*K$)&%*L-//(%#$8*<#&$/3=*#<*F=#$($)3$*F=#7;>*-$/*G3E3,#1'3$;*"3$;=38*M$(E3=%(;0*#<*F=#$($)3$6*N#'(*O>-=-%8*%3$(#=*<3,,#7*-;*P#,<3$%#>$*"3$;3=*<#=*G3E3,#1'3$;*-;*Q=##R($)%*S$%;(;&;(#$6*L+O($%30*F,#2-,*S$%;(;&;3*-$-,0%(%

"#$%&'()*"++),"('-)./0')."1.)/(2",/3"%#(-)/#4)/,')

*"++"#1)3%)(2'#4)3%),'/+"5')3.'&6)7.'(')#'*)

$%#(8&',()./0')$%&')%9)/1')"#)3.')4"1"3/+)',/6)

:+,'/4;-)&%,')3./#)./+9)%9)/++)1+%</+)=#3',#'3))

8(',()/,')"#)'&',1"#1)&/,>'3(6)?,/5"+"/#)(%$"/+@

#'3*%,>)2'#'3,/3"%#-)/()'/,+;)/()ABCB-)*/()3.')

('$%#4)."1.'(3)"#)3.')*%,+46):#4)/),'$'#3)D$E"#(';)

(8,0';)%9)8,</#):9,"$/#)$%#(8&',()"#)CF)$"3"'()"#)

3'#)4"99','#3)$%8#3,"'()9%8#4)3./3)/+&%(3)GB)2',$'#3)

%*#'4)=#3',#'3@$/2/<+')2.%#'()%,)(&/,32.%#'(6)

:()'@$%&&',$')/#4)&%<"+'@2/;&'#3)(;(3'&()

(2,'/4)3%)'0'#)3.')&%(3),'&%3')./&+'3(-)'&',1"#1)

$%#(8&',()/,')(./2"#1-)#%3)H8(3)2/,3"$"2/3"#1)"#-)

3.')4"1"3/+),'0%+83"%#)/#4)+'/29,%11"#1)4'0'+%2'4@

&/,>'3)#%,&(-)$,'/3"#1)#'*)$./&2"%#()+">'))

?/"48-)&I'(/-)/#4)7'#$'#36

7.')2,'9','#$'()%9)'&',1"#1@&/,>'3)$%#(8&',()

/+(%)*"++)4,"0')1+%</+)"##%0/3"%#)"#)2,%48$3)4'("1#-)

&/#89/$38,"#1-)4"(3,"<83"%#)$./##'+(-)/#4))

(822+;)$./"#)&/#/1'&'#3-)3%)#/&')H8(3)/)9'*)/,'/(6)

J%&2/#"'()9/"+"#1)3%)28,(8')$%#(8&',()"#)3.'(')

#'*)&/,>'3()*"++)(K8/#4',)$,8$"/+)%22%,38#"3"'()

3%)<8"+4)2%("3"%#()%9)(3,'#13.)3./3-)."(3%,;)(81@

1'(3(-)$%8+4)<')+%#1)+/(3"#16)=#)C!)&/H%,)2,%48$3)

$/3'1%,"'()"#)3.')L#"3'4)M3/3'(-)3.')&/,>'3))

+'/4',)"#)CNAF),'&/"#'4)3.')#8&<',@%#')%,)#8&<',@)

3*%)2+/;',)9%,)3.'),'(3)%9)3.')$'#38,;6F

Ten crucial capabilities O%,)4'0'+%2'4@&/,>'3)$%&2/#"'(-)*"##"#1)$%#@)

(8&',()"#)3.'(')#'*)."1.@1,%*3.)&/,>'3()

,'K8",'()/),/4"$/+)$./#1')"#)&"#4@('3-)$/2/<"+"3"'(-)

F))7.'(')$%&2/#"'()"#$+84')

E,/93)O%%4()PQ/<"($%R-)*."$.)

+'4)"#)<"($8"3(S)T'+)D%#3')

O%%4(-)"#)$/##'4)9,8"3S)/#4)

U,"1+';-)"#)$.'*"#1)18&6

53

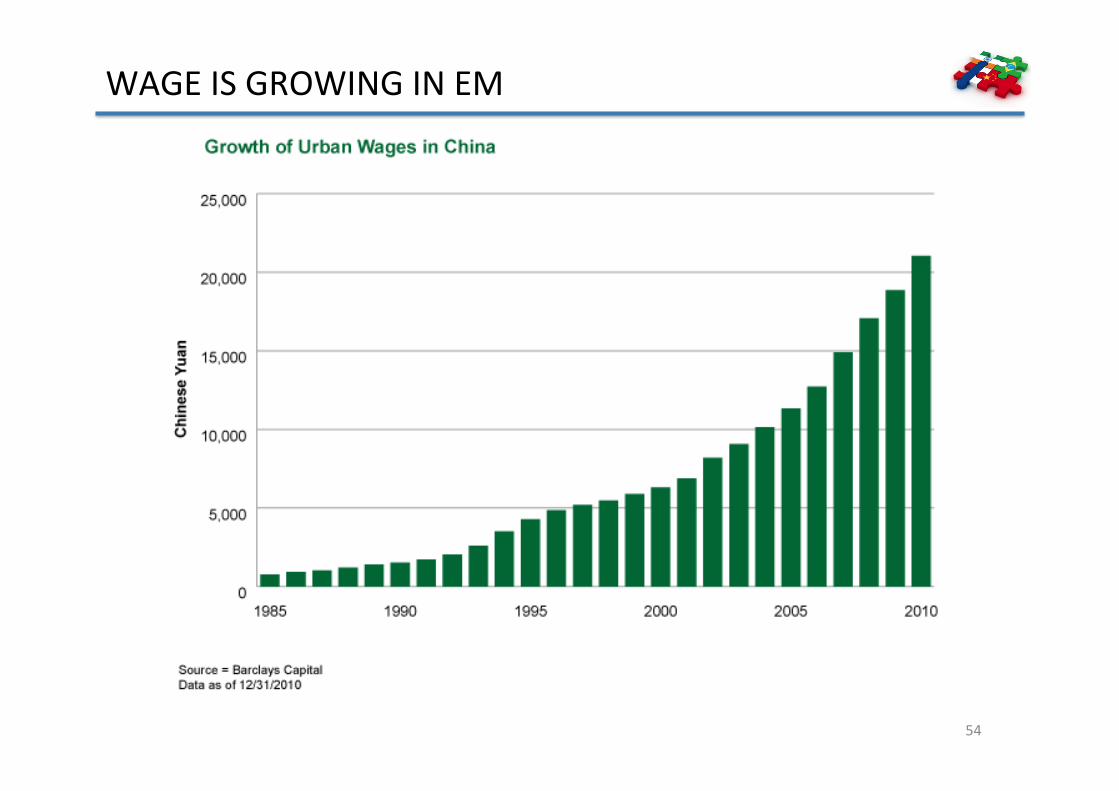

WAGEISGROWINGINEM

54

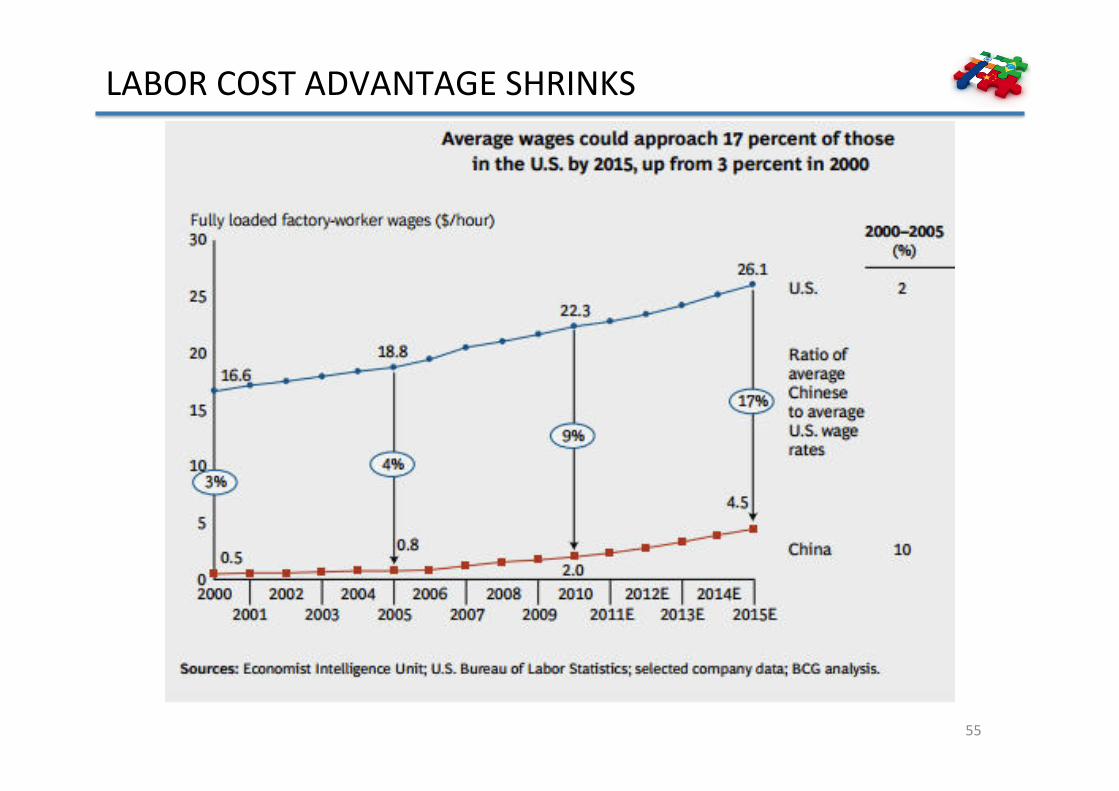

LABORCOSTADVANTAGESHRINKS

55

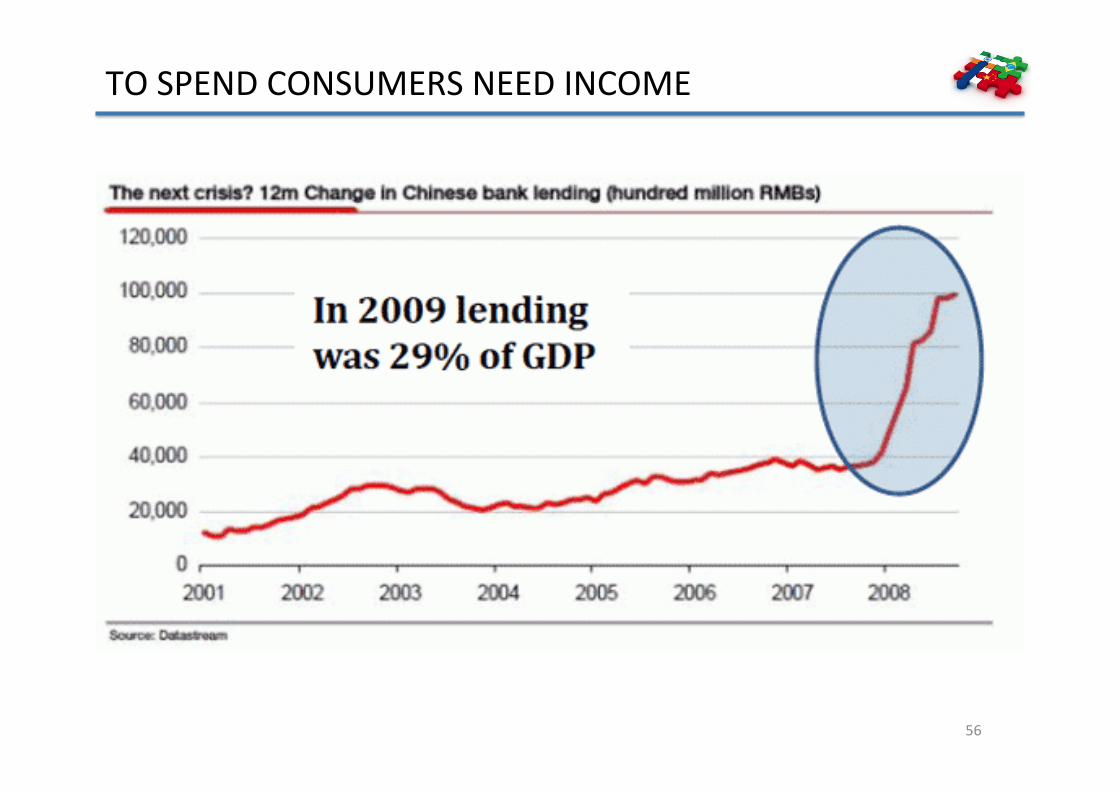

TOSPENDCONSUMERSNEEDINCOME

56

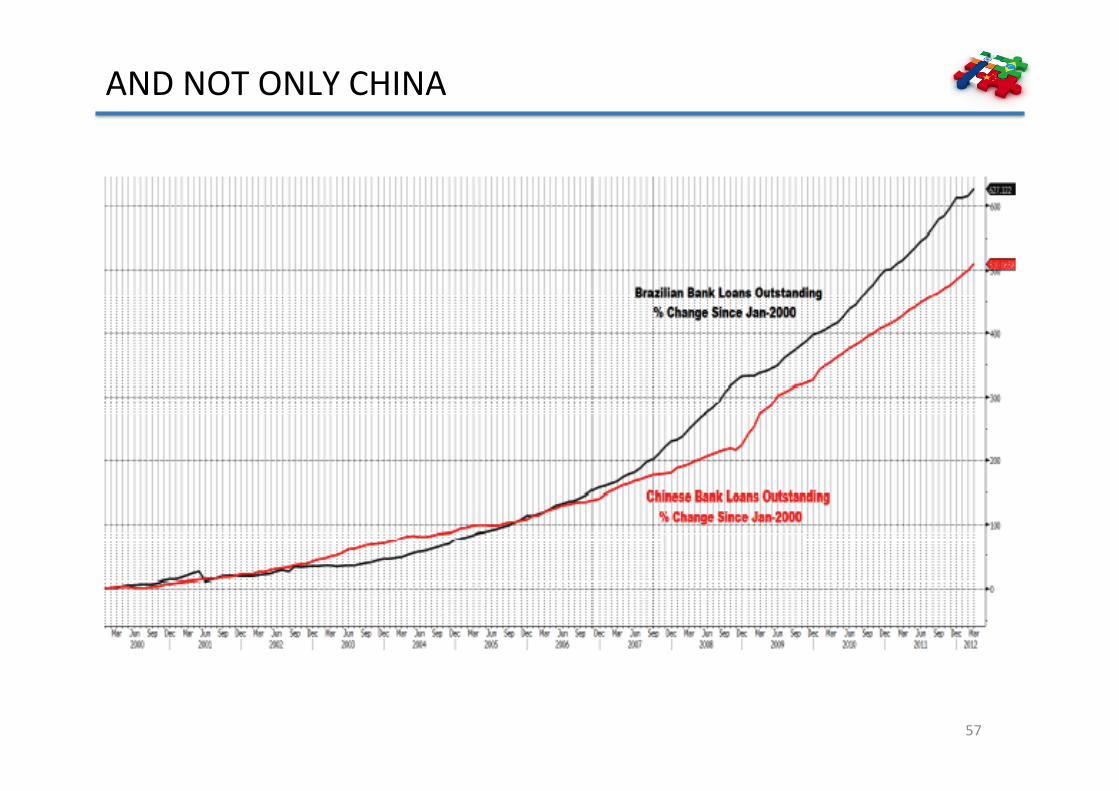

ANDNOTONLYCHINA

57

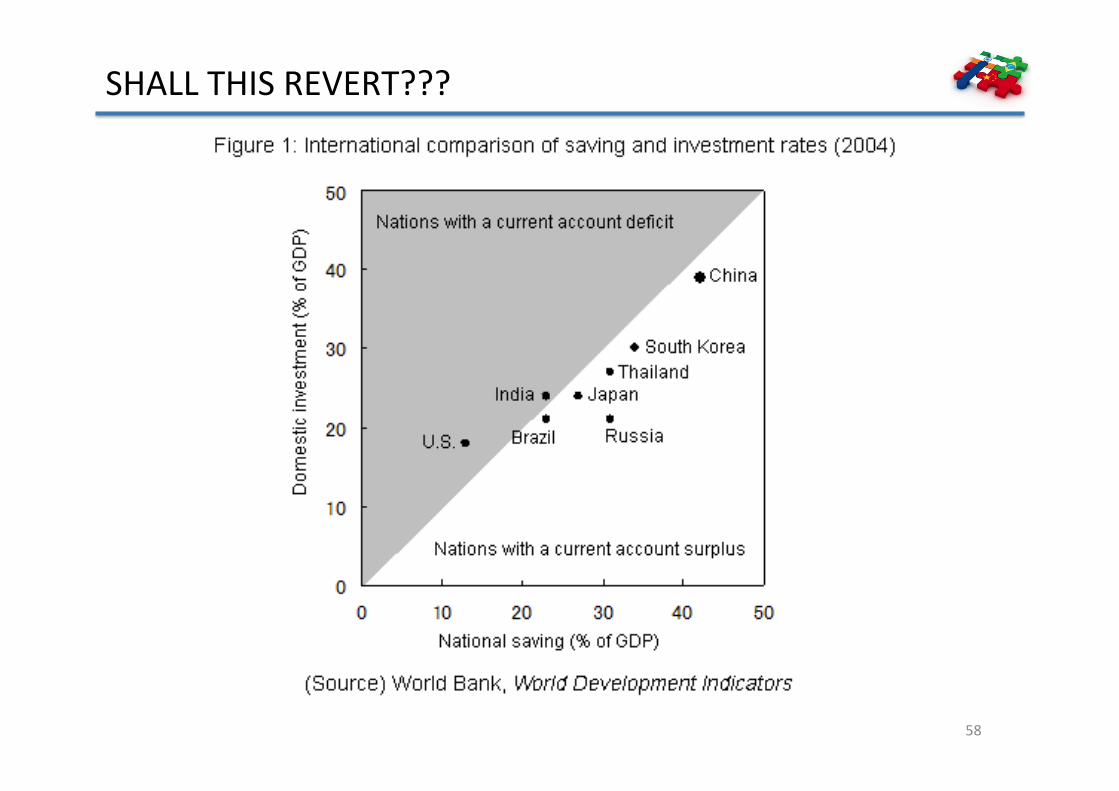

SHALLTHISREVERT???

58

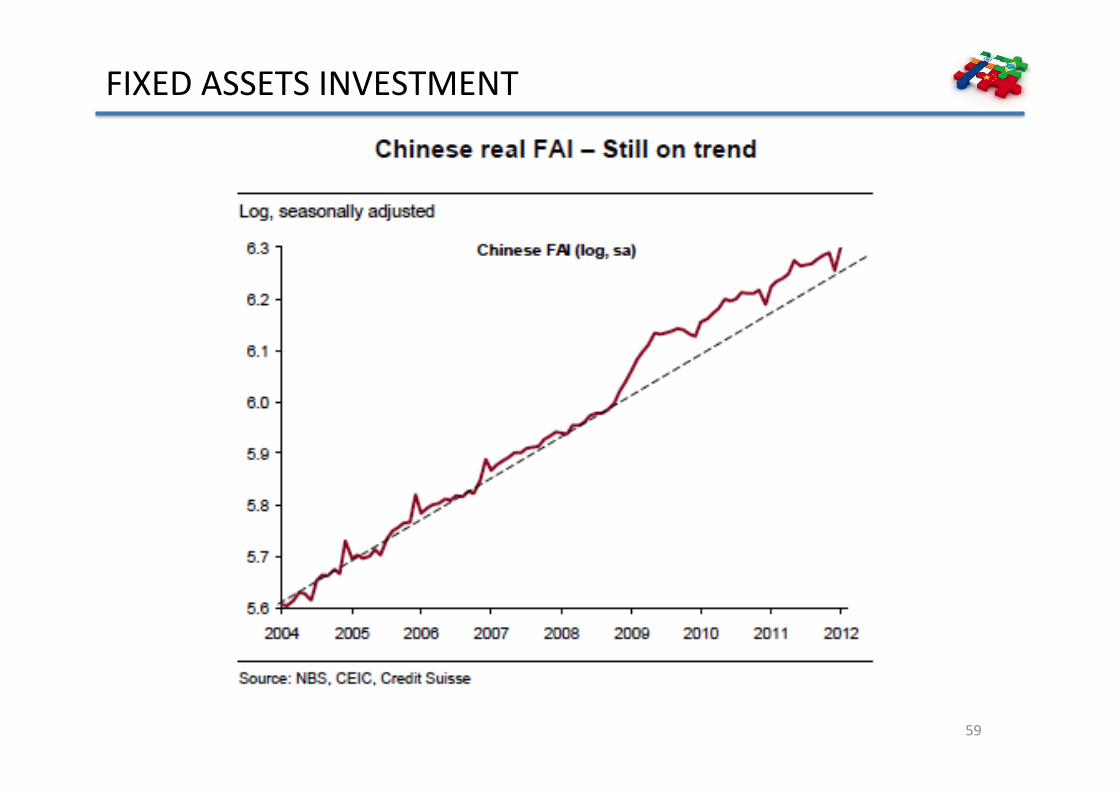

FIXEDASSETSINVESTMENT

59

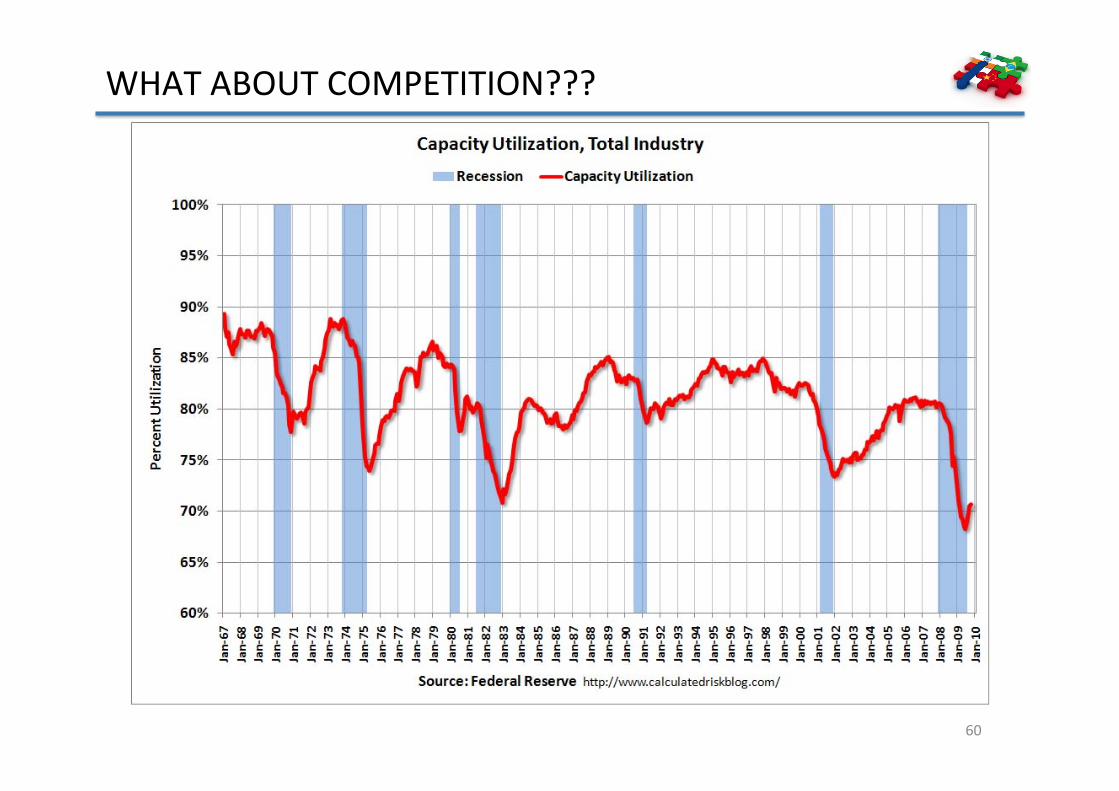

WHATABOUTCOMPETITION???

60

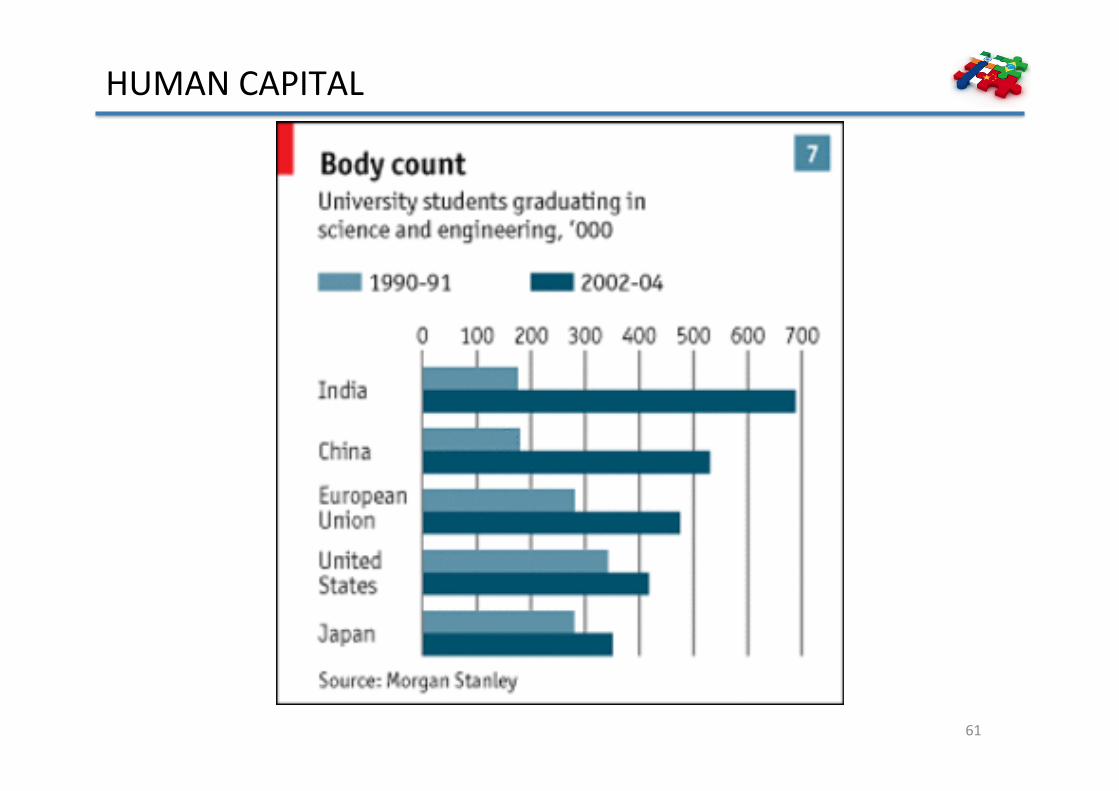

HUMANCAPITAL

61

WHATABOUTEXPECTEDRETURN???

62

HFMANAGERJONATHANBINDER:“investorswillnotnecessarilythinkof"G10"(orG7)versus"emergingmarkets”.“Instead,peopleshouldlookatthecountriesthat• arefiscallyresponsibleversus• countriesthatarenot.”

63

ONEPOTENTIALSCENARIO–RENTIERNATION

64

THANKYOUFORYOURATTENTION!!!

65

OlegShenker,CFARedValueCapitalPartnersManagingPartner+7(985)2310342