Embed Size (px)

Citation preview

Egyp

tGlobal Research

Egypt Economic Review

Economy

December 2008Surviving the World Financial Turmoil ...

Global EgyptTel: 20 (2) 37609526Fax: 20 (2) 37609506

Address: 7 Abdel Hadi Saleh St.,El-Nasr Tower, Giza,

Postal code: 12311Egypt

Global Research

Omar M. El-Quqa, CFAExecutive Vice [email protected] No:(965) 2295 1110

Faisal Hasan, CFAHead of [email protected] No:(965) 2295 1270

Mahmoud SoheimManager-Egypt [email protected] No: (202) 37609526

Ahmed Abu Hussein, CFAFinancial [email protected] No: (202) 37609526

Cherine Fayez Farkouh, CFAFinancial [email protected] No: (202) 37609526

Radwa WeshahyFinancial [email protected] No: (202) 37609526

Global Investment House � Egypt Economic Review - December 2008

Economy ...................................................................................................................................................... 2

The Banking Sector ....................................................................................................................................... 8

Real Estate Sector ....................................................................................................................................... �2

Steel Sector ................................................................................................................................................. 24

Cement Sector ............................................................................................................................................. 28

Fertilizers Sector ......................................................................................................................................... 33

Telecom Sector ........................................................................................................................................... 38

Stock Market ............................................................................................................................................... 44

Table of Contents

Economy

Global Investment House 3 Egypt Economic Review - December 2008

Egypt - Economy

Economic Performance 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 *Real GDP ^ (LE bn) 390.7 407.0 425.2 454.3 486.5 798.� Real GDP Growth Rate (%) 3.2% 4.�% 4.5% 6.8% 7.�% 7.2%Per capita GDP (US$) �,�6� �,��7 �,247 �,460 �,65� 2,�42Inflation (%) 3.2% �0.3% ��.4% 4.2% ��.0% ��.7%Unemployment (%) ��.0% �0.3% ��.2% �0.6% 8.9% 8.4%Population (mn) 69.2 70.5 7�.9 73.6 77.5 77.5Government FinanceTotal Revenues and Grants (LE mn) 89,�46 �0�,88� ��0,865 �5�,266 �80,2�5 2�8,500Total Expenditures (LE mn) �27,320 �45,987 �6�,6�0 207,8�� 222,029 277,432Cash Surplus/(Deficit) (LE mn) -38,�74 -44,�07 -50,747 -56,545 -4�,8�5 -58,932Overall Fiscal Surplus/(Deficit) (LE mn) -43,559 -45,877 -5�,643 -50,386 -54,698 -59,234Government DebtGross Domestic Public Debt (LE mn) 323,�97 388,377 469,039 470,264 493,879 537,68�Gross External Debt (LE mn) �77,438 �85,385 �67,474 �69,868 �70,865 �77,336Balance of PaymentTrade Balance (US$ mn) -6,6�5 -7,834 -�0,359 -��,986 -�5,8�7 -23,4�5Total Exports (US$ mn) 8,205 �0,453 �3,833 �8,455 22,0�8 29,356Total Imports (US$ mn) -�4,820 -�8,286 -24,�93 -30,44� -37,834 -52,77�Current Account (US$ mn) �,943 3,4�8 2,9�� �,752 2,696 888Current Account/Nominal GDP (US$ mn) 2.4% 4.3% 3.3% �.6% 2.�% 0.5%Capital & Financial Account (US$ mn) -2,734 -5,0�6 3,378 3,5�� �,�34 7,�37Overall balance (US$ mn) 546 -�58 4,478 3,253 5,282 5,420Money Supply Money Supply - M� (LE mn) 67,2�2 77,606 89,685 �09,274 �3�,290 �70,579Quasi Money (LE mn) 3�7,050 357,305 404,�99 45�,082 53�,398 596,085Total Domestic Liquidity (M2) (LE mn) 384,262 434,9�� 493,884 560,356 662,688 766,664^ Using 2001/02 prices for the period 2002/03 to 2006/07 and prices of 2006/07 for 2007/08* Preliminary

Source: Central Bank of Egypt, Ministry of Finance, The Egyptian Exchange (EGX) and Global Research

4 Egypt Economic Review - December 2008Global Investment House

Egypt - Economy

» The Egyptian economy maintained its robust GDP growth during the previous three years, at around 7% annually.

» GDP is expected to grow by 6%, double the world average growth.

» This strong growth enabled Egypt to be an attractive FDI destination, rising by �9.4% in FY 2007/08, reaching US$�3.2bn.

» The challenge facing the Egyptian economy was the rising inflation rate, reaching 2�.5% in September 2008.

» Inflationary pressures generated from surging food and fuel prices worldwide. With the ease of these prices internationally, the inflation is believed to be brought down.

GDP Composition by Economic Activity in FY 2007/08

Natural Gas9.1%

Insurance3.6%

Agriculture,Forstry & Fishing

13.2%

Oil6.9%

Oil & OtherManufacturing

Ind.16.3%

Const. &Building

4.3%

Transport &Warehousing

4.1%Communications3.2%

Suez Canal3.4%

Wholesale &Retail Trade

11.2%

FinancialServices

3.7%

Tourism3.7%

Real Estate2.7%

GeneralGovernment

8.4%

Others6.2%

Real GDP Growth

3.2%

4.1%4.5%

6.8%7.1% 7.2%

-

100

200

300

400

500

600

700

800

900

LE bn

2002/03 2003/04 2004/05 2005/06 2006/07 2007/08

0%

1%

2%

3%

4%

5%

6%

7%

8%

Real GDP (LE bn) Real GDP Growth Rate (%)

Source: Central Bank of Egypt (CBE) and Global Research

Global Investment House 5 Egypt Economic Review - December 2008

Egypt - Economy

Global financial crisis will not affect Egypt financially » The exposure of the Egyptian financial institutions in the world’s financial credit market is minimal. » Local banks have abundant liquidity, with an average loan to deposits ratio of 54% compared to

approximately 80% as an international norm.

What will be the economic threats? » Lower exports proceeds, on the back of expected drop in prices, which is anticipated to be more severely

affected than quantities. Negatively affecting the Balance of Payment.

» Lower return from Suez Canal, due to reduced global trade activity.

» Lower proceeds generated from tourism, due to slower expected economic performance in Europe.

Economic Outlook

6 Egypt Economic Review - December 2008Global Investment House

Egypt - Economy

Could any benefit emerge from this situation?

» Reduction in international oil, food and metal prices will :

• Make imports cheaper, relieving some pressure from the Balance of Payment.

• Save huge expenditures for the government budget, especially on subsidies, which have surged by 56% between 2006/07 and 2007/08.

• Lower the inflation rate, which was 20.2% in October 2008 down from 23.6% in August 2008.

» More attention should be directed to SMEs because 80% of employment in Egypt work in SMEs and their products are directed to the local market , therefore they are protected from global recession.

» Currently, SMEs are targeted by Banks, as they are believed to drive economic growth in the coming period.

Economic Snapshot

Global Investment House 7 Egypt Economic Review - December 2008

How Egypt economy is expected to perform against the world economy?

» IMF projected that Egypt GDP will grow by 6% in 2009, which is double the world expected GDP growth.

» And almost in line with the emerging and developing

countries forecasted average GDP growth. » This should attract more FDIs from around the

world. » Future FDI inflows are expected in more

manufacturing sectors benefiting from low labor cost, abundance of several raw materials, as well as Egypt’s geographical location.

» Transportation, education and health care are

projected to attract FDIs too.

4.5

6.87.1 7.2

6.0 6.0

6.56.8 6.9

4.94.5

5.1 5.0

3.9

3.0

4.2

4.8 4.8 4.7

3.2

4.1

3.6

2

3

4

5

6

7

8

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

%

Egypt World

3.2

4.14.5

6.87.1

6.0 6.06.5

6.8 6.96.3

7.57.1

7.9 8.0

6.9 6.9 6.97.2

6.9 6.1 6.7

2

3

4

5

6

7

8

9

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

%

Egypt Emerging & developing countries

Economic Snapshot Egypt - Economy

Source: IMF

The Banking Sector

Global Investment House 9 Egypt Economic Review - December 2008

The Banking Sector

» Significant banking reforms since 2004.

» Attractive sector dynamics led to international and regional acquisitions over Egyptian banks.

» Domestic Liquidity (M2) growing by a CAGR of �4.8% over the 5-year period starting 2002/03 to 2007/08.

» Potential lending opportunities to fund future projects, stemmed by accelerated GDP growth, even with slight deviation than expected, as a result of the current global conditions.

*provisional

Source: Central Bank of Egypt Source: Central Bank of Egypt

Domestic Liquidity Growth

-

100

200

300

400

500

600

700

800

900

2002/03 2003/04 2004/05 2005/06 2006/07 2007/08*

LE bn

M1 Quasi Money

Loans to Deposits Development

70.6%64.2%

59.3% 57.0% 54.4% 53.7%

0

100

200

300

400

500

600

700

800

2002/03 2003/04 2004/05 2005/06 2006/07 2007/08

LEbn

0%

10%

20%

30%

40%

50%

60%

70%

80%

Loans and Discount Balances Deposits Loans to Deposits

�0 Egypt Economic Review - December 2008Global Investment House

The Banking Sector

» Extremely low loans/deposits ratio of around 54%, compared to a rough estimate of 80% worldwide, providing enough room for extending loans.

» Pressure exerted on banks by the CBE to extend loans to SMEs, as prospective stimulant for economic growth.

» Banks with international parent lenders are not likely to be negatively affected by global turmoil due to independent operations.

» Investments by Egyptian banks, not covering risky instruments like derivatives and securitized bonds, have saved them from the world’s financial turmoil.

» Still a lot of unexploited segments in the banking sector, i.e. mortgage and SMEs lending .

» Huge unfulfilled demand from the retail sector, with a low penetration rate of approximately 30%.

» Ample liquidity characterizing the banking sector in contrast to the credit crunch prevailing in USA.

Global Investment House �� Egypt Economic Review - December 2008

Market Players

Sector/ Company RIC FYE # Shares Free Float CMP MC FC PE PBV DY%

000s as of 20/11/08 LE 000s LE 000s Trailing Forward

30/06/08 LE 2007 2008

Banks

Egyptian Gulf Bank ($) EGBE Dec. �50,�92 5�.�3% �.95 292,875 �49,747 22.7� �8.8� 2.�0 7.69%

CIB COMI Dec. 292,500 9�.35% 29.94 8,757,450 7,999,93� 7.68 6.�4 �.64 3.34%

Credit Agricole Bank CIEB Dec. 287,000 20.98% 8.60 2,468,200 5�7,828 4.7� 4.92 �.30 ��.63%

Housing and Development Bank HDBK Dec. 67,000 2�.47% 22.50 �,507,500 323,660 7.99 6.42 �.70 6.67%

NSGB NSGB Dec. 302,94� 22.83% �5.60 4,725,879 �,078,9�8 7.0� 5.6� 0.93 �.60%

Export Development Bank of Egypt EXPA June �00,000 23.29% 8.02 802,000 �86,786 2.58 6.0� 0.63 �2.47%

Sector Average 7.60 6.22 1.54

Source: EGX and Global Research

Real Estate Sector

Global Investment House �3 Egypt Economic Review - December 2008

Real Estate

» Robust economic growth in Egypt reaching 7.2% stimulated the growth in the real estate sector.

» Increasing FDI injected in the real estate sector, reaching US$400mn in 2007/08, compared to US$39mn in the previous year.

» The recent decline in raw materials prices could fuel more growth in the sector.

» The real estate market is characterized by a chronic gap because:

• Over-supply in the high-end residential segment. • Low supply of middle and economic properties, where the majority of demand exists.

3.1%

4.2%4.6%

6.9% 7.1% 7.2%

0.8%

3.9%

3.0%

3.8%4.3%

3.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2002/03 2003/04 2004/05 2005/06 2006/07 2007/08

GDP growth Real Estate growth

Source: CBE

�4 Egypt Economic Review - December 2008Global Investment House

Real Estate

Segments Estimated% of population Supply/Demand Outlook

High-End �0% High supply/saturated demand ÚUpper-Middle �5% Good supply/high demand ÒMiddle 35% Moderate supply/very high demand ÒEconomy 40% Low supply/great demand Ò

» Favorable demographic composition with 44% and 36% of population falling in the age-groups of 0-20 and 20-45, respectively.

Residential

Global Investment House �5 Egypt Economic Review - December 2008

Real Estate

» Activation of the mortgage law no.�48, which was issued in 200�, mainly through :

• Establishing the Egyptian Mortgage Refinance Company (EMRC) to be the mortgage market

maker.

• Reduction of property registration fees from �2% to 3% with a cap of LE2,000.

• Slash property tax rate from 46% to �0%.

• Establishing credit bureau to better assess borrowers credit worthiness.

• Establishing “Iskan”, to be the first insurance company concerned with mortgage finance risks.

Residential

�6 Egypt Economic Review - December 2008Global Investment House

Real Estate

Source: Ministry of Investment

» Very low Mortgage lending standing below �% of GDP, compared to 65% in USA, 45% in Europe and �4% in UAE.

14214

355

1,012

2

500

1,014

2,097

16

714

1,369

3,109

-

500

1,000

1,500

2,000

2,500

3,000

3,500

June 2005 June 2006 June 2007 June 2008

Mortgage Co. Banks Total

Residential

Global Investment House �7 Egypt Economic Review - December 2008

Real Estate

» Egypt compares favorable to other countries in the region, in terms of residential sqm prices.

Source: Colliers International

Cairo

Amman

TripoliMuscat

Doha

Riyadh

Khartoum

Dubai

Abu Dhabi

Damascus

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

0 20,000 40,000 60,000 80,000 100,000 120,000

GDP per Capita US$

Avg

. sqm

pri

ce U

S$

0

50

100

150

200

250

300

350

400

450

500

Cai

ro

Am

man

Trip

oli

Mus

cat

Doh

a

Riy

adh

Dam

ascu

s

Dub

ai

Abu

Dha

bi

Kha

rtou

m

Avg

. sqm

pric

e U

S$

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Annual avg. rent/sqm (US$) Rentail yield

Residential

�8 Egypt Economic Review - December 2008Global Investment House

Real Estate

» Higher GDP per capita, on the back of economic growth, leading to growing upper-middle class.

» Reduction in import duties on various items, reaching an average of 6.9%, leading to lower prices in the local market.

» Entrance of international brand names to Egypt.

» Shortage of supply in class “A” retail spaces.

Source: Colliers International

Annual avg. rent/sqm (US$)

867

486 528440

850

470

765

1,200

950

660

-

200

400

600

800

1,000

1,200

1,400

Cairo

Amman

Tripoli

Mus

cat

Doha

Riyadh

Damas

cus

Dubai

Abu D

habi

Kharto

um

Commercial Segment (Retail)

Global Investment House �9 Egypt Economic Review - December 2008

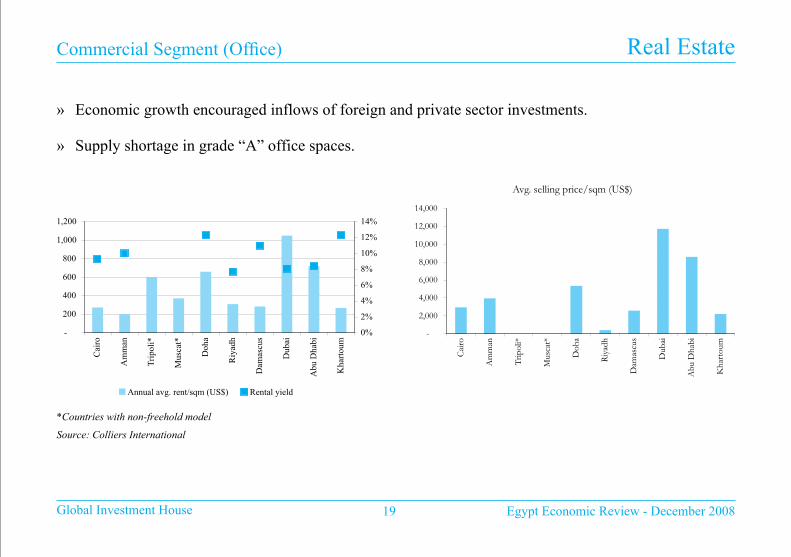

Real Estate

» Economic growth encouraged inflows of foreign and private sector investments. » Supply shortage in grade “A” office spaces.

-

200

400

600

800

1,000

1,200

Cai

ro

Am

man

Tri

poli*

Mus

cat*

Doh

a

Riy

adh

Dam

ascu

s

Dub

ai

Abu

Dha

bi

Kha

rtou

m0%

2%

4%

6%

8%

10%

12%

14%

Annual avg. rent/sqm (US$) Rental yield

Avg. selling price/sqm (US$)

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Cai

ro

Am

man

Trip

oli*

Mus

cat*

Doh

a

Riy

adh

Dam

ascu

s

Dub

ai

Abu

Dha

bi

Kha

rtou

m

*Countries with non-freehold model

Source: Colliers International

Commercial Segment (Office)

20 Egypt Economic Review - December 2008Global Investment House

Real Estate

» The tourism sector witnessed a strong growth at a CAGR of �6.6% over the past 6 years.

» No. of tourists arrivals reached ��mn in 2007, compared to 9mn in 2006.

» Investment in hotels reached LE5.5bn, against LE3.8bn in 2006/07, growing by 45%.

» The government targets to increase the no. of tourists arrivals to �4mn by the end of 20�2.

» Airports expansions and renovations to accommodate for the increasing no. of arrivals.

» Diversity of touristic activities (historical, recreational, religious).

» Egypt possesses one third of the world’s ancient monuments.

Tourism

Global Investment House 2� Egypt Economic Review - December 2008

Real Estate

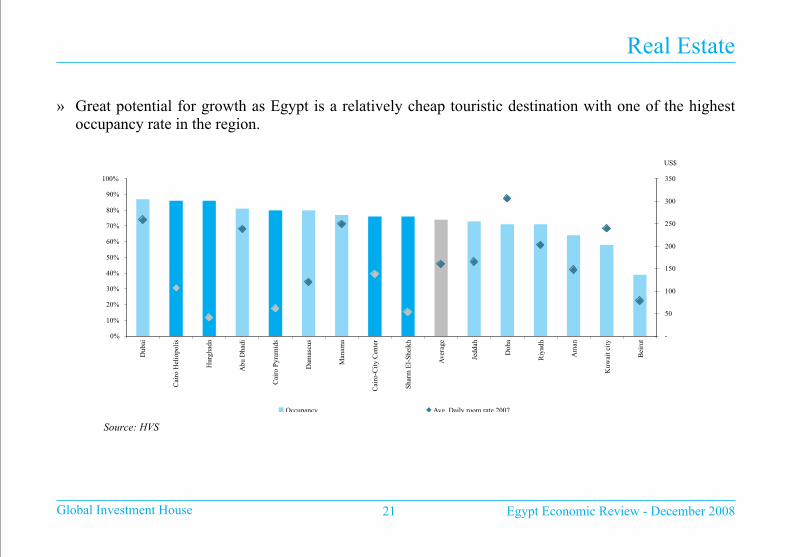

» Great potential for growth as Egypt is a relatively cheap touristic destination with one of the highest occupancy rate in the region.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dub

ai

Cai

ro H

elio

polis

Hur

ghad

a

Abu

Dha

di

Cai

ro P

yram

ids

Dam

ascu

s

Man

ama

Cai

ro-C

ity C

ente

r

Shar

m E

l-Sh

eikh

Ave

rage

Jedd

ah

Doh

a

Riy

adh

Am

an

Kuw

ait c

ity

Bei

rut -

50

100

150

200

250

300

350

US$

Occupancy Avg. Daily room rate 2007

Source: HVS

22 Egypt Economic Review - December 2008Global Investment House

Real Estate

» Generally, positive outlook but at a lower magnitude because of weak expected global economic growth, resulting from the global financial crisis.

Segment Outlook Explanation

Residential Ò • Good potential for growth, especially in the middle and lower income classes.• Mortgage lending is still in its infancy stage • Expected reduction in inflation will relief upward pressure on interest rates, lowering mortgage

rate

Retail Ò • The existing supply shortage will out-weight reduced activity following the global economic expected slowdown.

Office Ò • Under-served segment• Egypt above average expected economic growth at 6%, compared to the average global

economic growth rate of 3%.

Tourism Ò • Low cost destination to European tourists• Proximity to Europe, reducing travel cost • Expected average annual growth of 5.8%, according to World Travel and Tourism Council

(WTTC).

Outlook

Global Investment House 23 Egypt Economic Review - December 2008

Market Players

Sector/ Company RIC FYE # Shares Free Float CMP MC FC PE PBV DY%

000s as of 20/11/08 LE 000s LE 000s Trailing Forward

30/06/08 LE 2007 2008

Housing & Real Estate

Cairo Housing ELKA Dec. 93,750 95.08% 4.50 42�,875 40�,��9 67.32 55.94 0.86 4.44%

Egyptian Resorts Company EGTS Dec. �,050,000 39.72% �.74 �,827,000 725,684 6.40 6.56 �.72 ��.49%

Nasr City Housing MNHD June �00,000 42.66% 25.84 2,584,000 �,�02,334 29.8� 24.62 9.72 3.�0%

Orascom Hotels & Development ORHD Dec. 22�,962 2.00% 20.00 4,439,246 88,785 ��.09 48.49 �.49 0.00%

SODIC OCDI Dec. 28,4�3 62.28% 4�.�0 �,�67,79� 727,300 3.52 7.75 0.67 0.00%

United Housing UNIT Dec. 42,207 64.�2% 5.�6 2�7,789 �39,647 �4.32 �2.59 4.46 0.00%

Heliopolis Housing HELI June 74,�7� 22.29% 24.00 �,780,��4 396,787 �5.79 �3.36 5.09 5.2�%

Development & Engineering Consultants DAPH Dec. 8,57� 46.82% �3.40 ��4,857 53,776 2.28 5.25 0.83 0.00%

Remco for Touristic Villages Construction RTVC Dec. �04,024 26.40% 5.47 569,0�0 �50,2�9 3.99 2.74 0.58 0.00%

Upper Egypt General Contracting UEGC June 50,000 96.69% 2.�7 �08,500 �04,909 50.97 7.43 0.34 0.00%

Egyptians Housing Development &

ReconstructionEHDR Dec. 75,000 48.26% 3.6� 270,750 �30,664 236.82 27.2� �.68 0.00%

Talaat Mostafa Group Holding TMGH Dec. 2,030,204 4�.90% 3.�6 6,4�5,443 2,688,07� 24.2� 4.�� 0.30 0.00%

Sector Average 26.59 13.03 2.50

Source: EGX and Global Research

Steel Sector

Global Investment House 25 Egypt Economic Review - December 2008

Steel Sector

Source: CBE, Global Research

» Construction and building activities in Egypt have been growing at a �9.9% CAGR from 2004/05 to 2007/08.

» Sales by main Egyptian companies have grown at a CAGR of �2.5% between 2004/05 and 2007/08.

Construction and Building Activities

4.0%

4.1%

4.2%

4.6%

-

5

10

15

20

25

30

35

40

2004/05 2005/06 2006/07 2007/08

LE

bn

3.6%

3.7%

3.8%

3.9%

4.0%

4.1%

4.2%

4.3%

4.4%

4.5%

4.6%

Construction and Building Construction and Building % of GDP

Steel Sales Volume By Main Egyptian Companies

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2001 2002 2003 2004 2005 2006 2007 Jun-08

000

tons

26 Egypt Economic Review - December 2008Global Investment House

Steel Sector

» Forecasts for world steel production indicate a growth of 5.3% in 2008 and 5.4% in 2009, driven by developing economies.

» Even though steel prices decreased from highs of LE7,000/ton to LE5,000/ton in mid-September, profit margins will remain strong as billet prices declined from LE6,000/ton to LE4,000/ton.

» Sustainable growth in construction and mainly infrastructural spending, especially in Upper Egypt.

Egypt Steel Prices

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Oct-07 Nov-07 Dec-07 Jan-08 Feb-08 Mar-08 Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08

LE

/ton

Scraps Billets Steel RebarsSource: IDA and Global Research

Global Investment House 27 Egypt Economic Review - December 2008

Market Players

Sector/ Company RIC FYE # Shares Free Float CMP MC FC PE PBV DY%

000s as of 20/11/08 LE 000s LE 000s Trailing Forward

30/06/08 LE 2007 2008

Iron & Steel

Ezz Steel ESRS Dec. 543,265 34.75% 9.64 5,237,075 �,8�9,884 4.67 2.80 �.22 �0.37%

Ezz - Dekhila Steel - Alex IRAX Dec. �3,364 7.4�% 723.00 9,662,47� 7�5,603 4.28 2.68 2.55 20.06%

Sector Average 4.56 2.77 1.59

Source: EGX and Global Research

Cement Sector

Global Investment House 29 Egypt Economic Review - December 2008

Cement Sector

» Egypt has a comparative advantage in the production and exportation of cement due to the availability of

raw materials, relatively cheap energy and Egypt’s strategic location enabling it to be a major exporter

in the region.

» These promising features of the industry has always made Egypt an attractive investment destination for

foreign suppliers.

» The majority of cement companies in Egypt are dominated by international companies represented by

Holcim, Ciment Francais, Cemex, Vicat, Cimpor and Lafarge.

30 Egypt Economic Review - December 2008Global Investment House

Cement Sector

» Strong performance in line with GDP growth. » The growth in local construction activities ensures demand on cement.

29,1

04

28,7

63

33,5

65

36,2

15

38,4

69

25,7

04

23,5

50

28,5

27

30,2

25

34,4

623,29

9

4,66

1

5,17

3

5,83

8

4,13

2

3.2%

4.1%

4.5%

6.8% 7.1%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2003 2004 2005 2006 2007

000

tons

0%

1%

2%

3%

4%

5%

6%

7%

8%

Supply Demand Exports Egypt GDP Growth Rate

Source: Global Research

Global Investment House 3� Egypt Economic Review - December 2008

Cement Sector

» On November 2007, new cement licenses worth LE�,�38mn were granted to meet the expected demand

from the infrastructure projects, especially in Upper Egypt, where the government announced a mega

project worth LE3,2bn over the period between 2007 to 20�2.

» The new licenses will bring Egypt’s total cement capacities to 55.2mn tons by 20�0, from the current

4�.7mn tons, which reflects the inherent growth in the sector.

» Still the cost per ton is considered low compared to regional and international peers, despite the recent

local increases in energy costs.

» The continuous need for housing in Egypt ensures considerable demand on cement, especially as the

prices will ease, to benefit from low materials costs.

32 Egypt Economic Review - December 2008Global Investment House

Market Players

Sector/ Company RIC FYE # SharesFree Float

CMP MC FC PE PBV DY%

000s as of 20/11/08 LE 000s LE 000s Trailing Forward

30/06/08 LE 2007 2008

Cement

South Valley Cement SVCE Dec. 4�4,055 20.06% 5.�2 2,��9,960 425,264 3.64 3.52 0.90 0.00%

Misr Beni Suef Cement MBSC Dec. 20,000 50.53% 45.60 9�2,000 460,834 4.72 4.59 �.�6 6.58%

Misr Cement - Qena MCQE Dec. 30,000 �2.80% 80.00 2,400,000 307,�52 8.68 7.67 3.0� 6.25%

National Cement Company NCEM June �03,200 �.73% �8.55 �,9�4,360 33,2�2 7.57 �2.�4 2.76 9.97%

Sinai Cement SCEM Dec. 35,000 25.5�% 3�.40 �,099,000 280,345 3.22 3.02 0.82 3.98%

Suez Cement SUCE Dec. �8�,857 �4.00% 20.40 3,709,873 5�9,399 3.78 3.�7 0.64 9.80%

Sector Average 4.69 4.38 1.23

Source: EGX and Global Research

Fertilizers Sector

34 Egypt Economic Review - December 2008Global Investment House

Fertilizers Sectors

Fertilizers demand is secured by robust growth in the agriculture sector in Egypt.

» The agriculture sector is considered one of the significant sectors in Egypt, where it has accounted for

�4% of the country’s GDP in FY 2007/08.

» The local demand on fertilizers is highly strengthened by the continuous growth in the agriculture sector,

which is supported by the following pillars:

• Rapidly growing population.

• Scarcity of arable land.

• Enhanced irrigation systems.

• Providing subsidized fertilizers.

• Adding around �50,000 acres annually to Egypt’s arable land.

• Government awareness campaigns for using the appropriate types and quantities of fertilizers in

order to raise crop yields.

Global Investment House 35 Egypt Economic Review - December 2008

Fertilizers Sectors

» Though the world’s financial crisis has

significantly forced fertilizers prices

downward, squeezing producers margins,

the low cash cost of the fertilizers production

in Egypt ensures strong and sustainable

profit margins.

» Catering to the availability of relatively

cheap raw materials, natural gas and

phosphate rock, more investments are

injected in the fertilizers sector, where local

producers are raising their capacities, and

new joint ventures between local and foreign

fertilizers producers are being established.

Source: Fertilizerworks and Global Research

Source: PotashCorp and Global Research

Urea Prices Vs. Natural Gas Prices

200

300

400

500

600

700

800

900

Jan-08 Feb-08 Mar-08 Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08

US$

/M.T

on

4

6

8

10

12

14

16

US$/M

MB

tu

Granular Urea Basket Price (RHS) Middle East Granular Urea (RHS)

Natural Gas Henry Hub Spot Price (LHS)

World Natural Gas Cost (2008 Estimates) 13.00

11.009.95

8.25

3.75 3.50

2.30 2.001.00 0.80 0.60

0

2

4

6

8

10

12

14

Wes

t Eur

ope

USA

Can

ada

Ukr

aine

Chi

na

Arg

entin

a

Rus

sia

Indo

nesi

a

Ven

ezue

la

Mid

dle

Eas

t

Nor

th A

fric

a

US$

/MM

Btu

36 Egypt Economic Review - December 2008Global Investment House

Ammonia/Urea Average Cash Cost

Source: PotashCorp, Yara Fertilizers and Global Research

Ammonia

-

100

200

300

400

500

600

700

800

900

Wes

t Eur

ope

USA

Cana

da

Ukra

ine

Chin

a

Arge

ntin

a

Russi

a

Indo

nesia

Egyp

t

Vene

zuela

Midd

le Ea

st

Nor

th A

frica

US$

/mt

Ammonia Cash Cost

Average Ammonia Cash Cost

Ammonia Current Price (October 2008)

Ammonia Peak Price (August 2008)

Urea

-

100

200

300

400

500

600

700

800

Wes

t Eur

ope

USA

Can

ada

Ukr

aine

Chi

na

Arg

entin

a

Rus

sia

Indo

nesi

a

Egy

pt

Ven

ezue

la

Mid

dle

Eas

t

Nor

th A

fric

a

US$

/mt

Urea Cash Cost

Average Urea Cash Cost

Urea Current Price (October 2008)

Urea Peak Price (August 2008)

Global Investment House 37 Egypt Economic Review - December 2008

Market Players

Sector/ Company RIC FYE # SharesFree

FloatCMP MC FC PE PBV DY%

000s as of 20/11/08 LE 000s LE 000sTrailing Forward

30/06/08 LE 2007 2008

Fertilizers

Abu Kir Fertilizers ABUK June 45,886 �3.00% �66.89 7,657,980 995,537 7.73 8.34 4.�3 6.74%

Egyptian Financial & Industrial Co. EFIC Dec. 69,302 5�.47% 24.�7 �,675,020 862,�33 �4.38 5.93 2.66 4.37%

Sector Average 10.82 7.22 3.45

Source: EGX and Global Research

Telecom Sector

Global Investment House 39 Egypt Economic Review - December 2008

Telecom Sector

» The Communications sector achieved a

growth rate of �4.2% in FY2007/08, on the

back of improved economic conditions.

» Egypt’s expected economic growth of 6%

will ensure the growth of the sector.

» The world financial crisis will have no

effect on the Telecom Sector, due to its

unique nature.

» The low penetration rate in the Egyptian

market will act as a catalyst for the growth

in the sector over the coming years.

Communications Sector

9.4%10.3%

14.1% 14.2%

0

5

10

15

20

25

30

LE bn

2004/05 2005/06 2006/07 2007/08

0%

2%

4%

6%

8%

10%

12%

14%

16%

Communications (LEbn) Growth %

Communicatons Sector Contribution to GDP

2.16% 2.23%

3.25%3.46%

0.0%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2004/05 2005/06 2006/07 2007/08

Source: CBE and Global Research

40 Egypt Economic Review - December 2008Global Investment House

Telecom Sector

Fixed Line

» Telecom Egypt is currently the sole fixed line provider in Egypt.

» Fixed line subscribers grew at a CAGR of 7.7% over the past five years, reaching ��.23mn in 2007.

» Fixed line penetration rate stood at �5.0% in 2007 and �5.�% by the end of September 2008.

» The ARPU of Telecom Egypt reached LE5�.� in September 2008.

» The government postponed a second fixed line license auction to 2009, due to unfavorable market conditions.

11.4%

Fixed Line Subscribers and Penetration Rate

12.6%13.5%

14.5% 14.7% 15.0% 15.1%

-

2

4

6

8

10

12

14Mn

2002 2003 2004 2005 2006 2007 Sep-086%

8%

10%

12%

14%

16%

18%

Fixed Line Subscribers (mn) Fixed Line Penetration %

Teleocm Egypt ARPU

53.5 52.7 55.358.9

54.2 51.1

-

10

20

30

40

50

60

70

2003 2004 2005 2006 2007 Sep-08

LE

Source: Telecom Egypt and Global Research

Global Investment House 4� Egypt Economic Review - December 2008

Telecom Sector

Mobile

» Total mobile subscribers reached 38mn in September 2008, up by 40% compared to September 2007.

» The mobile market has been gradually de-regulated, but NTRA continues to have a major role in controlling competition.

3.4%8.3% 10.8%

19.1%24.8%

40.7%

50.7%

-

5

10

15

20

25

30

35

40Mn

2002 2003 2004 2005 2006 2007 Sep-08

0%

10%

20%

30%

40%

50%

60%

Mobile Subscribers (mn) Mobile Penetration %

Mobile Subscribers and Penetration Rate

Mobinil49.6%

Vodafone43.0%

EtisalatMisr7.5%

Mobile Operators Market Share(September 2008)

Source: Mobinil, Vodafone and Global Research Source: NTRA and Global Research

42 Egypt Economic Review - December 2008Global Investment House

Telecom Sector

Mobile

» The increased competition among the current 3 mobile operators is expected to squeeze their profit margin.

» The pre-paid market is the prominent one, with over 97% of mobile subscribers preferring pre-payment plans.

Mobile Cellular subscribers per 100 inhabitants

176.5150.4

148.3114.7

97.396.3

81.480.5

75.973.1

64.2

31.330.7

21.313.8

39.8

0 20 40 60 80 100 120 140 160 180 200

United Arab EmiratesQatar

BahrainSaudi Arabia

KuwaitOman

AlgeriaJordan

TunisiaLibya

MoroccoEgypt

SyriaLebanon

SudanYemen

Source: ITU

Global Investment House 43 Egypt Economic Review - December 2008

Market Players

Sector/ Company RIC FYE # Shares Free Float CMP Market Free PE PBV DY%

000s as of 20/11/08 Cap Cap Trailing Forward

30/06/08 LE LE 000s LE 000s 2007 2008

Communication

Mobinil EMOB Dec. �00,000 28.58% ��7.00 ��,700,000 3,343,860 6.42 6.�9 5.30 �4.26%

Orascom Telecom Holding ORTE Dec. �,028,�00 37.46% 2�.05 2�,64�,505 8,�06,908 3.22 8.28 2.97 4.75%

Telecom Egypt ETEL Dec. �,707,072 �8.27% �3.20 22,533,345 4,��6,842 8.89 7.70 0.90 7.58%

RAYA RAYA Dec. 56,985 68.76% 4.80 273,527 �88,077 6.75 4.99 0.60 25.63%

Sector Average 5.42 7.64 2.90

Source: EGX and Global Research

Stock Market

Global Investment House 45 Egypt Economic Review - December 2008

Stock Market

» CASE 30 Index still has a positive trend on the long run even after its recent significant losses.

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

Trend line

2-Ja

n-06

2-Fe

b-06

2-M

ar-0

6

2-A

pr-0

6

2-M

ay-0

6

2-Ju

n-06

2-Ju

l-06

2-A

ug-0

6

2-Se

p-06

2-O

ct-0

6

2-N

ov-0

6

2-D

ec-0

6

2-Ja

n-07

2-Fe

b-07

2-M

ar-0

7

2-A

pr-0

7

2-M

ay-0

7

2-Ju

n-07

2-Ju

l-07

2-A

ug-0

7

2-Se

p-07

2-O

ct-0

7

2-N

ov-0

7

2-D

ec-0

7

2-Ja

n-08

2-Fe

b-08

2-M

ar-0

8

2-A

pr-0

8

2-M

ay-0

8

2-Ju

n-08

2-Ju

l-08

2-A

ug-0

8

2-Se

p-08

2-O

ct-0

8

2-N

ov-0

8

Source: EGX and Global Research

46 Egypt Economic Review - December 2008Global Investment House

Stock Market Indicators

Indicators 2003 2004 2005 2006 2007 2008(Jan -Oct)

Volume of listed securities �,20�.6 �,786.3 4,�98.9 7,757.� ��,377.6 �8,686.5 Volume of unlisted securities 220.7 648.4 �,���.6 �,323.4 3,7�2.5 2,52�.8 Total volume (million) 1,422.3 2,434.7 5,310.4 9,080.5 15,090.0 21,208.3 Value traded (listed securities) 23,000.0 36,�4�.7 �50,924.0 27�,�07.8 32�,524.5 447,�54.2 Value traded (unlisted securities) 4,764.0 6,232.6 9,7�0.7 �5,63�.9 4�,�95.9 46,775.9 Total value traded (LE million) 27,764.0 42,374.3 160,634.7 286,739.7 362,720.4 493,930.1 Average monthly value traded (listed securities) �,9�7.0 3,0��.8 �2,577.0 22,592.3 26,793.7 44,7�5.4 Average monthly value traded (unlisted securities) 397.0 5�9.4 809.2 �,302.7 3,433.0 4,677.6 Total (LE million) 2,314.0 3,531.2 13,386.2 23,895.0 30,226.7 49,393.0 Number of transactions (Listed securities) �,205,775 �,675,277 3,922,30� 6,590,�96 8,7�2,584 �0,936,543 Number of transactions (unlisted securities) 23,602 68,287 2�7,79� 23�,244 30�,282 593,376 Total number of transactions 1,229,377 1,743,564 4,210,092 6,821,440 9,013,866 11,529,919 Number of listed companies 978 795 744 595 435 377 Number of traded companies 540 503 44� 407 337 306 Average monthly traded companies 206 200 �86 �83 �99 2�2 Market capitalization end of year (LE bn) �7�.9 233.9 456.3 534.0 768.3 475.4 Turnover Ratio (%) ��.5 �4.2 3�.� 48.7 38.7 90.� Price Earning (P/E) Ratio * 8.8 �5.6 22.0 2�.0 �9.� �2.3 Price to Book (P/B) Ratio * 2.� 4.4 9.� 5.9 8.6 4.8

Securities include stocks, bonds and mutual funds * P/E and P/B ratios are based on the most active companies only (Liquid Market) Source: EGX

Global Investment House 47 Egypt Economic Review - December 2008

Stock Market

Source: EGX

» Market cap. vs. number of listed and traded companies

-

200

400

600

800

1,000

2003 2004 2005 2006 2007 2008 (Jan to Oct 2008)

Com

pani

es

-

200

400

600

800

1,000

LE

Bn

Market capitalization end of year (LE bn) Number of listed companies

Number of traded companies

48 Egypt Economic Review - December 2008Global Investment House

Stock Market

» Total volume vs. value traded development

-

5

10

15

20

25

2003 2004 2005 2006 2007 2008 (Jan to Oct 2008)

Bill

ion

Shar

es

-

100

200

300

400

500

600

LE

Bn

Total value traded (LE Bn) Total volume (Bn)

Source: EGX

Global Investment House 49 Egypt Economic Review - December 2008

Stock Currently Traded Below Par Value

Company RIC Par ValueCMP

As of 20/11/08Traded at a

discount to par

Talaat Mostafa Group Holding TMGH �0.00 3.�6 -68%

Media Production City MPRC �0.00 3.85 -62%

NAEEM Holding ($) NAHO �.00 0.42 -58%

Arab Polvara Spining & Weaving APSW 5.00 2.67 -47%

Remco for Touristic Villages Construction RTVC �0.00 5.47 -45%

Arab Cotton Ginning ACGC 5.00 3.23 -35%

SPINALEX SPIN 2.00 �.39 -3�%

Export Development Bank of Egypt EXPA �0.00 8.02 -20%

El Ezz Porcelain (Gemma) ECAP 5.00 4.24 -�5%

Cairo Housing ELKA 5.00 4.50 -�0%

Development & Engineering Consultants DAPH �4.00 �3.40 -4%

RAYA RAYA 5.00 4.80 -4%

Source: EGX and Global Research

50 Egypt Economic Review - December 2008Global Investment House

Stocks Currently Traded Below Book Value

Sector/ Company RIC BV/shareCMP

As of 20/11/08

Traded at a

discount to BVTalaat Mostafa Group Holding TMGH �0.60 3.�6 -70%Upper Egypt General Contracting UEGC 6.35 2.�7 -66%Arab Polvara Spining & Weaving APSW 7.65 2.67 -65%Media Production City MPRC �0.97 3.85 -65%NAEEM Holding ($) NAHO �.�9 0.42 -65%Arab Cotton Ginning ACGC 8.02 3.23 -60%EFG-Hermes Holding HRHO 23.89 �3.56 -43%Remco for Touristic Villages Construction RTVC 9.35 5.47 -42%RAYA RAYA 8.03 4.80 -40%Oriental Weavers Carpets ORWE 33.�3 �9.90 -40%Export Development Bank of Egypt EXPA �2.75 8.02 -37%Suez Cement SUCE 3�.69 20.40 -36%SPINALEX SPIN 2.�� �.39 -34%El Ezz Porcelain (Gemma) ECAP 6.37 4.24 -33%SODIC OCDI 6�.09 4�.�0 -33%East Delta Flour Mills EDFM 30.�4 2�.0� -30%KABO KABO �.53 �.20 -2�%Sinai Cement SCEM 38.20 3�.40 -�8%Alexandria Flour Mills AFMC �4.�6 ��.66 -�8%Development & Engineering Consultants DAPH �6.09 �3.40 -�7%Cairo Housing ELKA 5.23 4.50 -�4%Telecom Egypt ETEL �4.69 �3.20 -�0%South Valley Cement SVCE 5.69 5.�2 -�0%NSGB NSGB �6.82 �5.60 -7%Source: EGX and Global Research

Global Investment House 5� Egypt Economic Review - December 2008

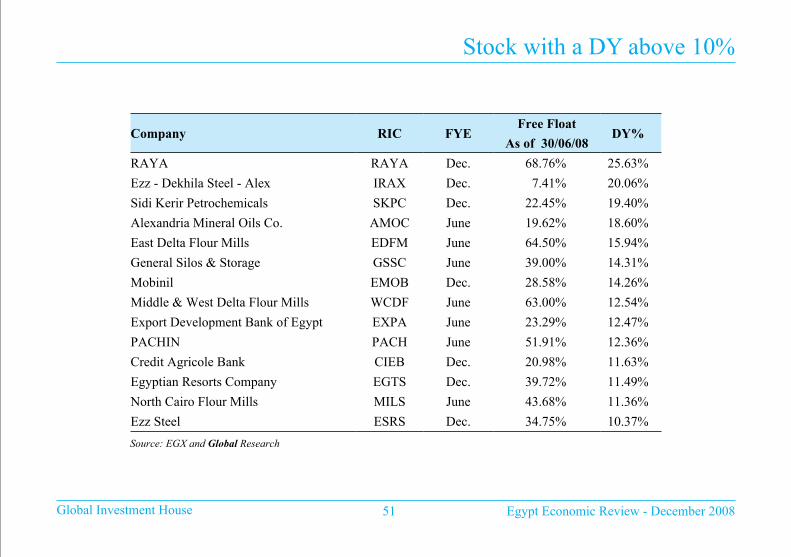

Stock with a DY above �0%

Company RIC FYEFree Float

DY%As of 30/06/08

RAYA RAYA Dec. 68.76% 25.63%

Ezz - Dekhila Steel - Alex IRAX Dec. 7.4�% 20.06%

Sidi Kerir Petrochemicals SKPC Dec. 22.45% �9.40%

Alexandria Mineral Oils Co. AMOC June �9.62% �8.60%

East Delta Flour Mills EDFM June 64.50% �5.94%

General Silos & Storage GSSC June 39.00% �4.3�%

Mobinil EMOB Dec. 28.58% �4.26%

Middle & West Delta Flour Mills WCDF June 63.00% �2.54%

Export Development Bank of Egypt EXPA June 23.29% �2.47%

PACHIN PACH June 5�.9�% �2.36%

Credit Agricole Bank CIEB Dec. 20.98% ��.63%

Egyptian Resorts Company EGTS Dec. 39.72% ��.49%

North Cairo Flour Mills MILS June 43.68% ��.36%

Ezz Steel ESRS Dec. 34.75% �0.37%

Source: EGX and Global Research

52 Egypt Economic Review - December 2008Global Investment House

To Sum Up

» Egypt is a safe investment destination in the coming period.

» The buoyant expected GDP growth of 6% in 2009 ensures considerable FDI inflows to Egypt mostly in

manufacturing sectors, as well as transportation, education and health care.

» Drops in International food and energy prices will save the country’s budget a considerable amount of

the subsidy bill, as well as push inflation rate downward.

» Being mostly on the low cash cost of production per ton of various industries will guarantee relatively

high profit margins for the companies on the Egyptian stock market.

» The strong fundamentals of many traded stocks on the Egyptian stock market and the current low price

levels will be the catalyst for these stocks to rebound to their historical average prices, once the 2009 Q�

results are announced.

This material was produced by Global Investment House KSCC (‘Global’),a firm regulated by the Central Bank of Kuwait. This document is not to be used or consideredas an offer to sell or a solicitation of an offer to buy any securities. Global may, from time to time,to the extent permitted by law, participate or invest in otherfinancing transactions with the issuers of the securities (‘securities’), perform services for or solicit business from such issuer, and/or have a position or effect transactionsin the securities or options thereof. Global may, to the extent permitted by applicable Kuwaiti law or other applicable laws or regulations, effect transactions in thesecurities before this material is published to recipients.Information and opinions contained herein have been compiled or arrived by Global from sources believed to be reliable, but Global has not independently verifiedthe contents of this document. Accordingly, no representation or warranty, express or implied, is made as to and no reliance should be placed on the fairness,accuracy, completeness or correctness of the information and opinions contained in this document. Global accepts no liability for any loss arising from the use ofthis document or its contents or otherwise arising in connection therewith. This document is not to be relied upon or used in substitution for the exercise of independentjudgement. Global shall have no responsibility or liability whatsoever in respect of any inac curacy in or ommission from this or any other document prepared byGlobal for, or sent by Global to any person and any such person shall be responsible for conducting his own investigation and analysis of the information containedor referred to in this document and of evaluating the merits and risks involved in the securities forming the subject matter of this or other such document.Opinions and estimates constitute our judgment and are subject to change without prior notice.Past performance is not indicative of future results. This documentdoes not constitute an offer or invitation to subscribe for or purchase any securities, and neither this document nor anything contained herein shall form the basisof any contract or commitment what so ever. It is being furnished to you solely for your information and may not be reproduced or redistributed to any other person.Neither this report nor any copy hereof may be distributed in any jurisdiction outside Kuwait where its distribution may be restricted by law. Persons who receivethis report should make themselves aware of and adhere to any such restrictions. By accepting this report you agree to be bound by the foregoing limitations.

Global Investment HouseTel: (965) 2295 1000 - Fax: (965) 2295 1299

Global Research