Embed Size (px)

Citation preview

Alpha Construction

Group

Housing Component Products

Demand Forecast

1

Forward

• Many businesses are affected by the cyclical effects of housing and remodeling demand, yet they have not developed formal tools to allow these data to drive their business plans and forecasts.

• Bottom-Line Analytics has significant experience in this and can provide clients with an interactive tool which will help them more accurately forecast and plan their business performance.

• The following is a case using an econometric model to forecast demand for a housing component manufacturer in 2015.

2

Content

• Forecast Model Description• Sales Predictions v. Actuals• Forecast Summary and Assumptions for 2015• Drivers of Growth for 2014• Model Driver Relative Importance• Model Driver Impacts and Sensitivities

– Recurring Seasonality– Housing Starts– Remodeling Spending– Order Backlog– Price to Customer

• Forecast-Simulator Demonstration• Summary

3

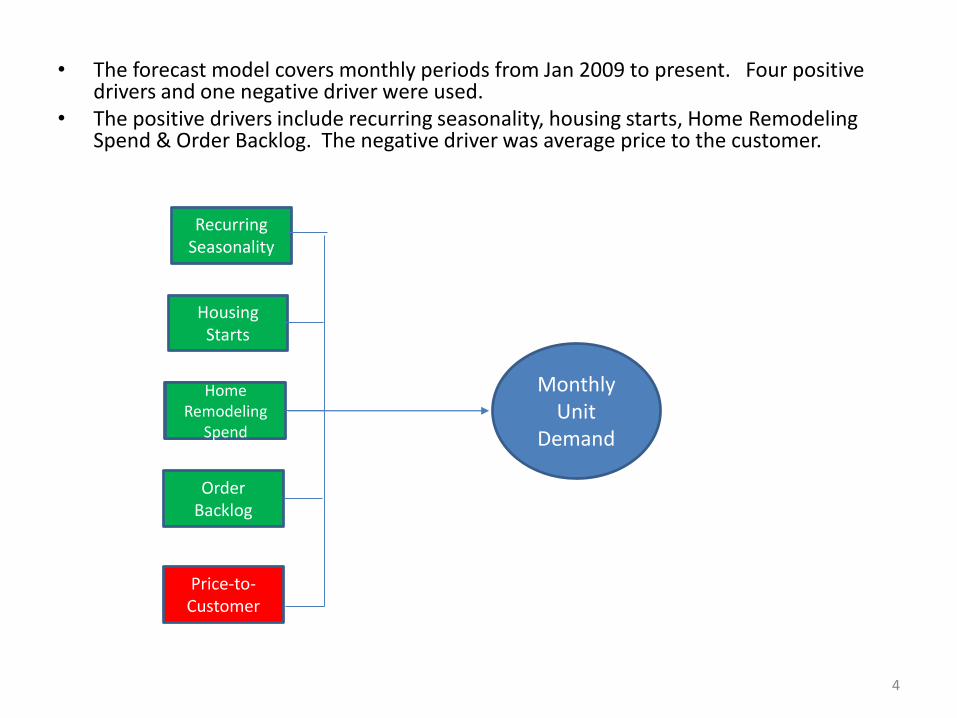

• The forecast model covers monthly periods from Jan 2009 to present. Four positive drivers and one negative driver were used.

• The positive drivers include recurring seasonality, housing starts, Home Remodeling Spend & Order Backlog. The negative driver was average price to the customer.

Home Remodeling

Spend

Order Backlog

Price-to-Customer

Monthly Unit

Demand

Housing Starts

Recurring Seasonality

4

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

Jan

.20

06

May

.20

06

Sep

.20

06

Jan

.20

07

May

.20

07

Sep

.20

07

Jan

.20

08

May

.20

08

Sep

.20

08

Jan

.20

09

May

.20

09

Sep

.20

09

Jan

.20

10

May

.20

10

Sep

.20

10

Jan

.20

11

May

.20

11

Sep

.20

11

Jan

.20

12

May

.20

12

Sep

.20

12

Jan

.20

13

May

.20

13

Sep

.20

13

Jan

.20

14

May

.20

14

Sep

.20

14

Jan

.20

15

May

.20

15

Sep

.20

15

Forecast/Simulated Sales Actual Sales

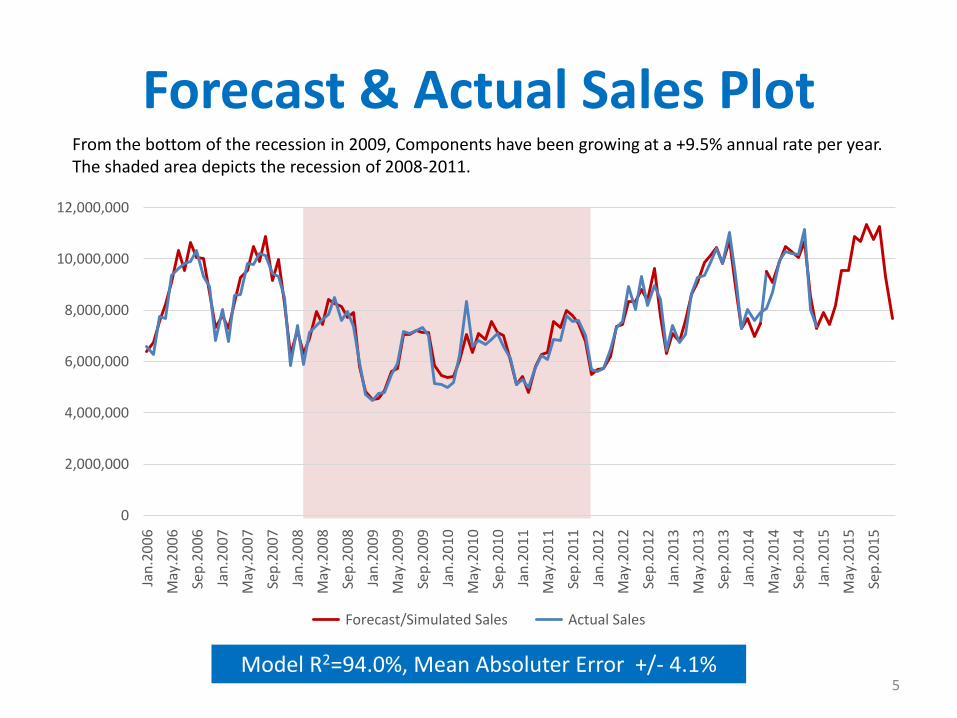

Forecast & Actual Sales Plot

5Model R2=94.0%, Mean Absoluter Error +/- 4.1%

From the bottom of the recession in 2009, Components have been growing at a +9.5% annual rate per year.The shaded area depicts the recession of 2008-2011.

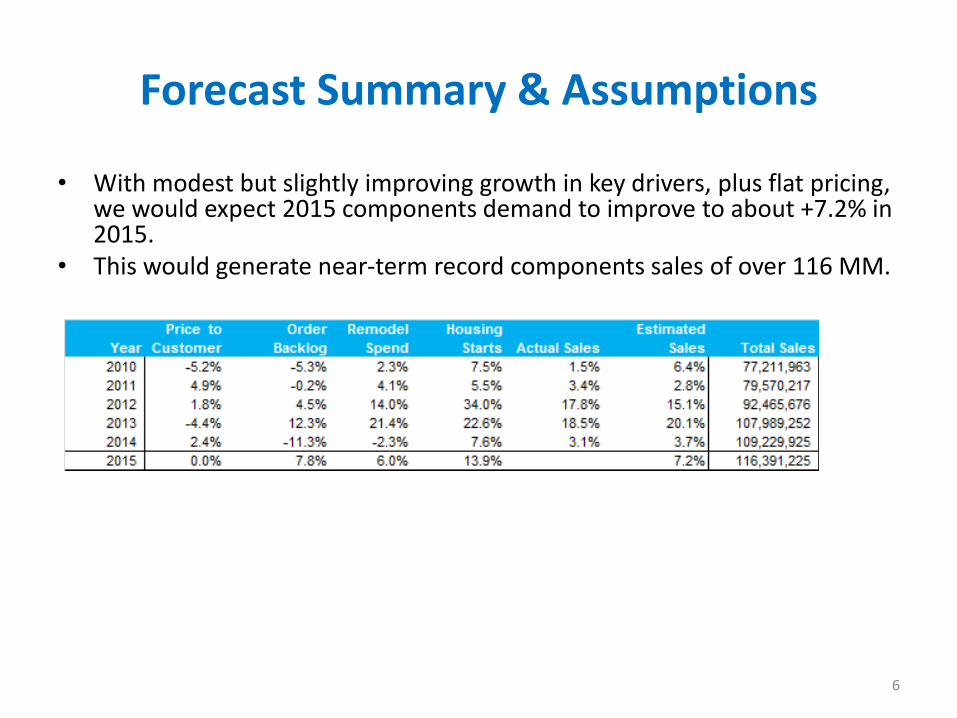

Forecast Summary & Assumptions

• With modest but slightly improving growth in key drivers, plus flat pricing, we would expect 2015 components demand to improve to about +7.2% in 2015.

• This would generate near-term record components sales of over 116 MM.

6

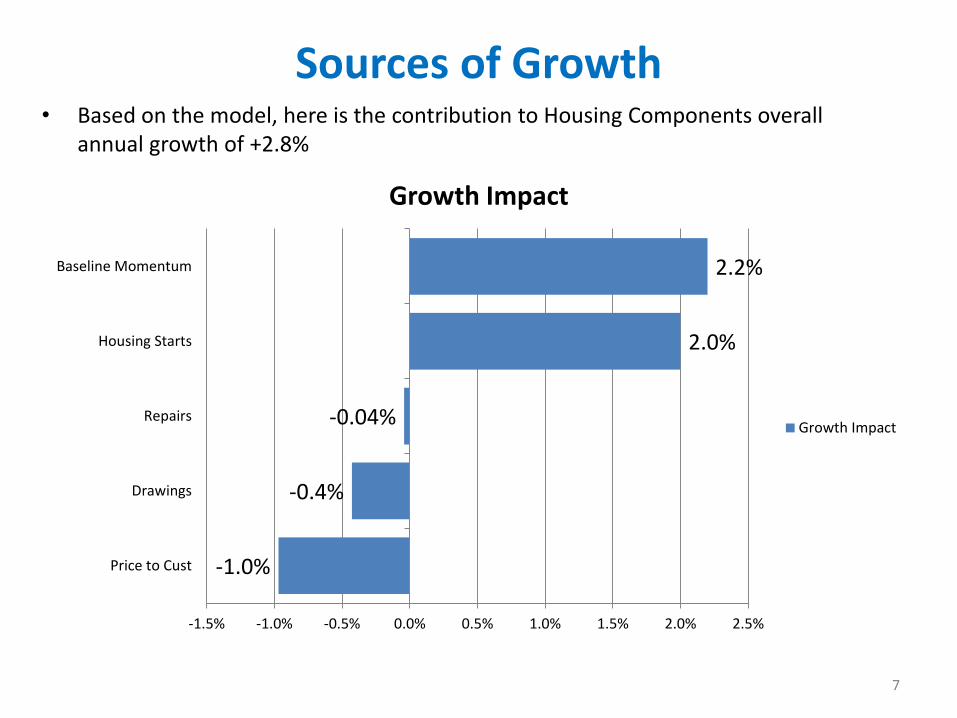

Sources of Growth

-1.0%

-0.4%

-0.04%

2.0%

2.2%

-1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5%

Price to Cust

Drawings

Repairs

Housing Starts

Baseline Momentum

Growth Impact

Growth Impact

7

• Based on the model, here is the contribution to Housing Components overall annual growth of +2.8%

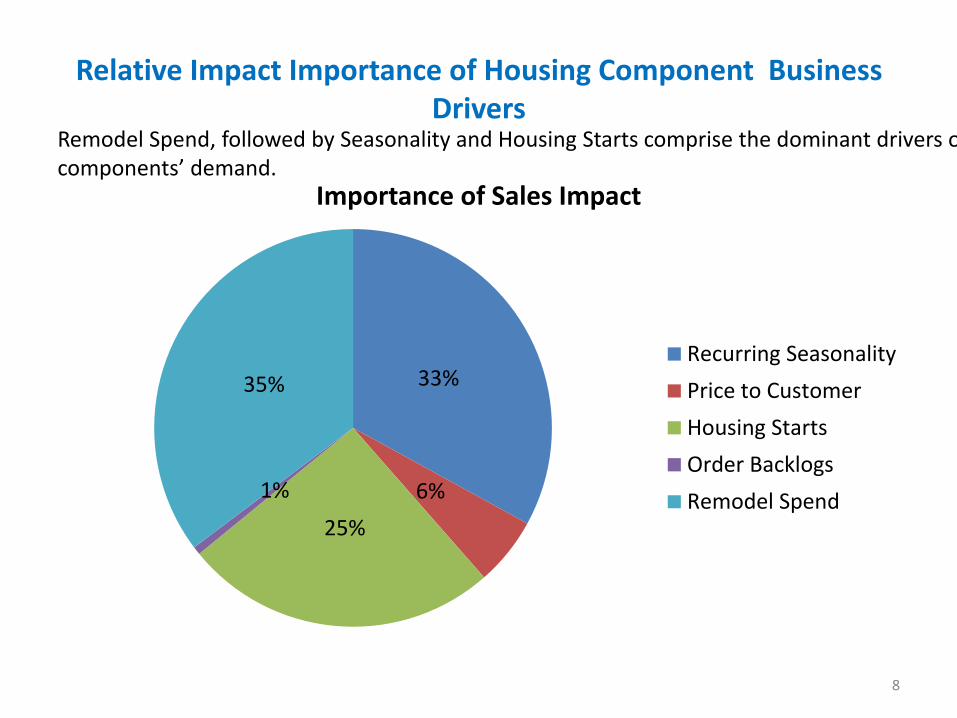

Relative Impact Importance of Housing Component Business Drivers

33%

6%

25%

1%

35%

Importance of Sales Impact

Recurring Seasonality

Price to Customer

Housing Starts

Order Backlogs

Remodel Spend

Remodel Spend, followed by Seasonality and Housing Starts comprise the dominant drivers ofcomponents’ demand.

8

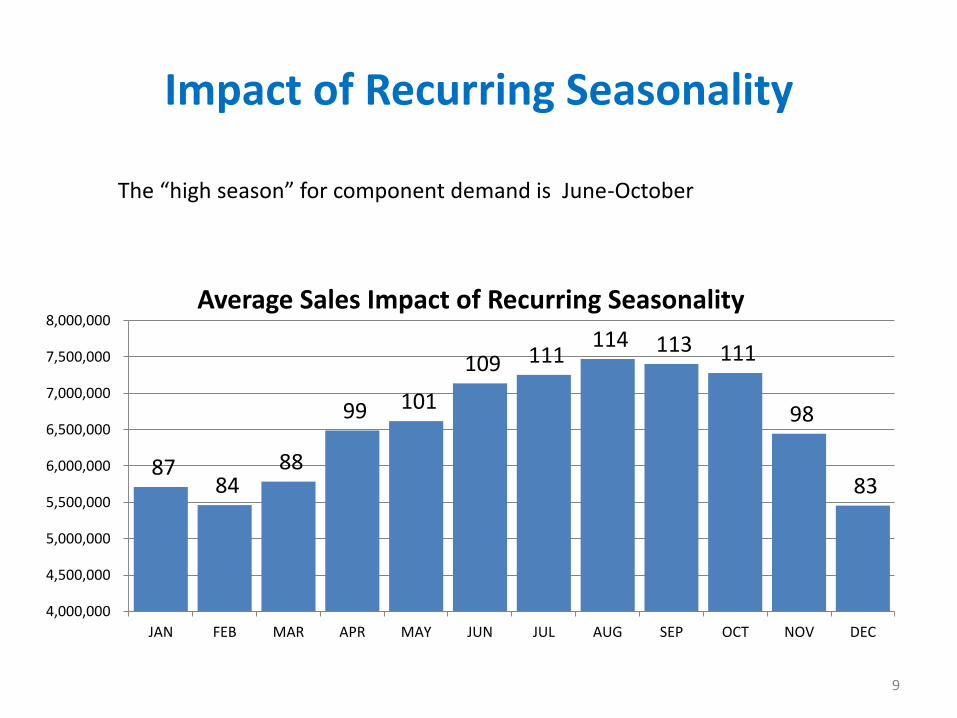

Impact of Recurring Seasonality

8784

88

99 101

109 111114 113 111

98

83

4,000,000

4,500,000

5,000,000

5,500,000

6,000,000

6,500,000

7,000,000

7,500,000

8,000,000

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Average Sales Impact of Recurring Seasonality

The “high season” for component demand is June-October

9

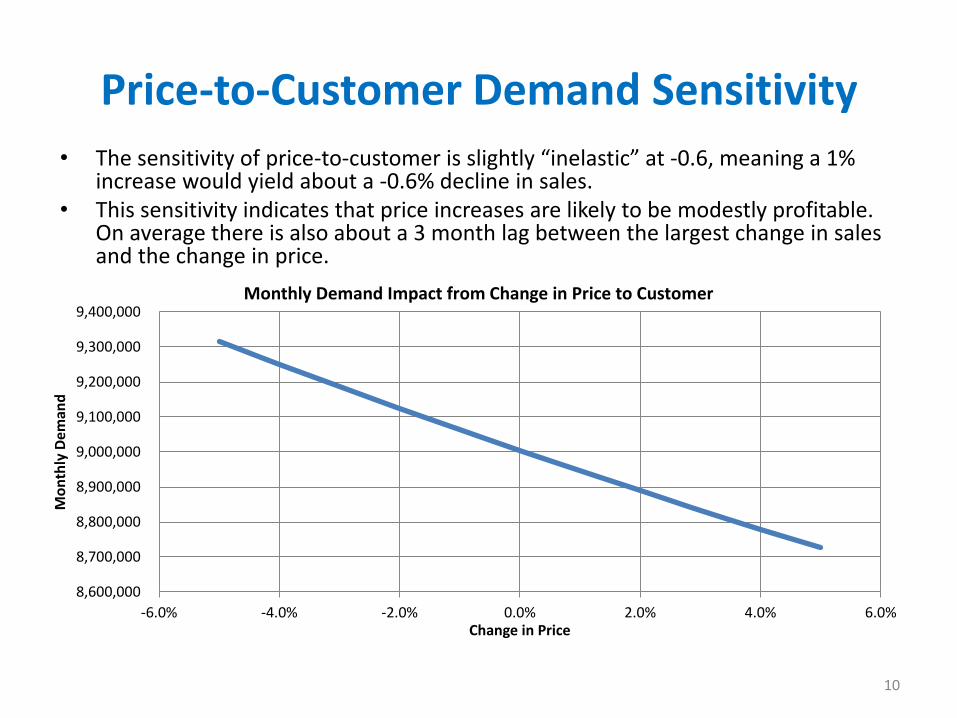

Price-to-Customer Demand Sensitivity

8,600,000

8,700,000

8,800,000

8,900,000

9,000,000

9,100,000

9,200,000

9,300,000

9,400,000

-6.0% -4.0% -2.0% 0.0% 2.0% 4.0% 6.0%

Mo

nth

ly D

eman

d

Change in Price

Monthly Demand Impact from Change in Price to Customer

• The sensitivity of price-to-customer is slightly “inelastic” at -0.6, meaning a 1% increase would yield about a -0.6% decline in sales.

• This sensitivity indicates that price increases are likely to be modestly profitable. On average there is also about a 3 month lag between the largest change in sales and the change in price.

10

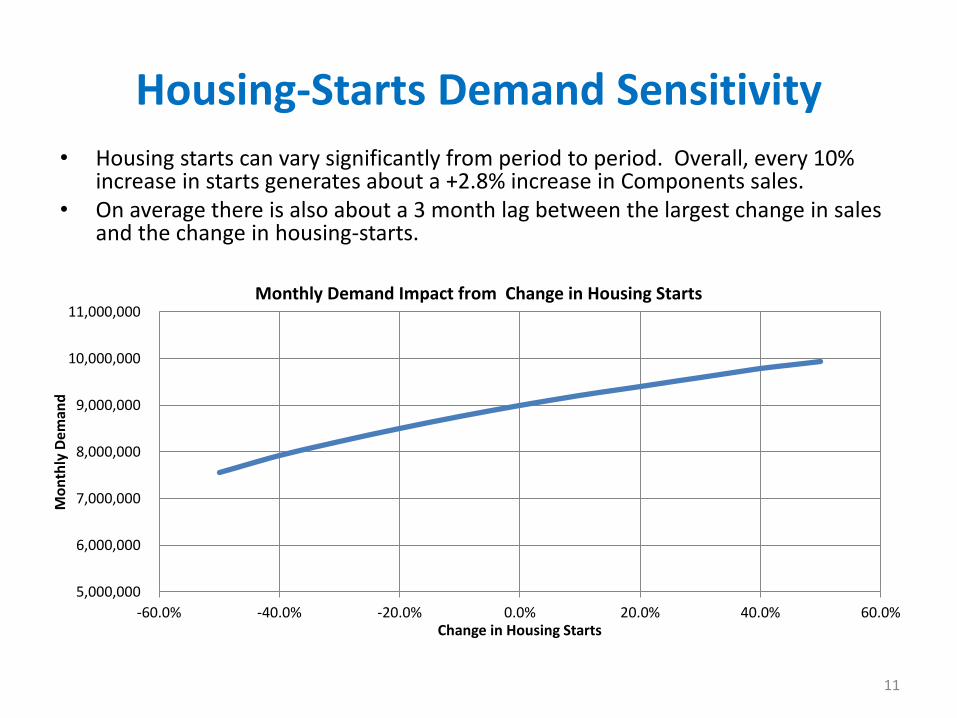

Housing-Starts Demand Sensitivity

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

11,000,000

-60.0% -40.0% -20.0% 0.0% 20.0% 40.0% 60.0%

Mo

nth

ly D

eman

d

Change in Housing Starts

Monthly Demand Impact from Change in Housing Starts

• Housing starts can vary significantly from period to period. Overall, every 10% increase in starts generates about a +2.8% increase in Components sales.

• On average there is also about a 3 month lag between the largest change in sales and the change in housing-starts.

11

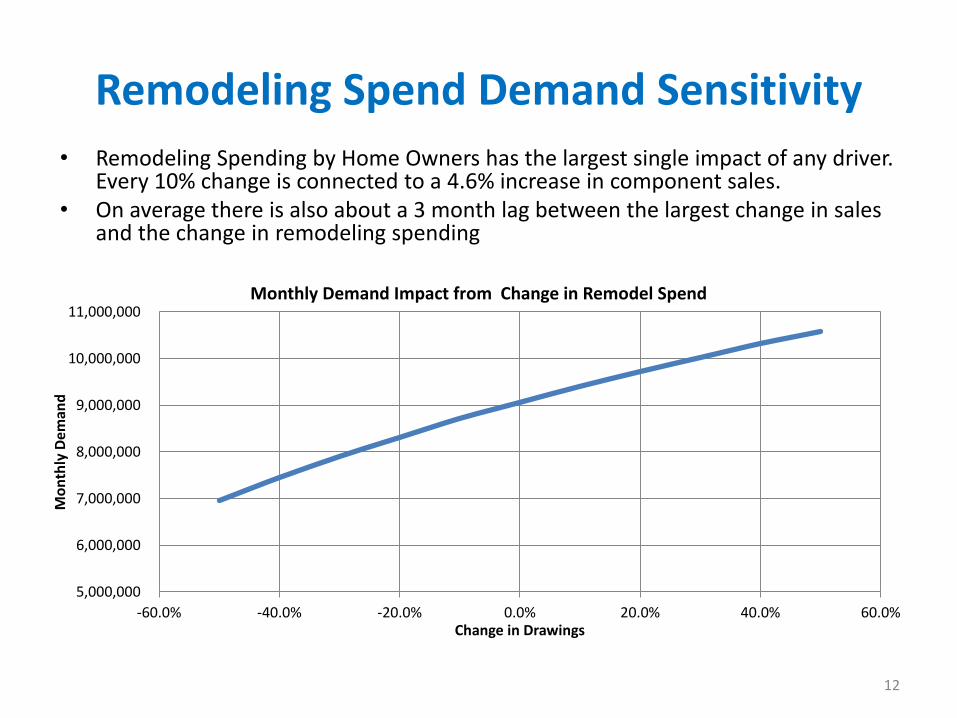

Remodeling Spend Demand Sensitivity

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

11,000,000

-60.0% -40.0% -20.0% 0.0% 20.0% 40.0% 60.0%

Mo

nth

ly D

eman

d

Change in Drawings

Monthly Demand Impact from Change in Remodel Spend

• Remodeling Spending by Home Owners has the largest single impact of any driver. Every 10% change is connected to a 4.6% increase in component sales.

• On average there is also about a 3 month lag between the largest change in sales and the change in remodeling spending

12

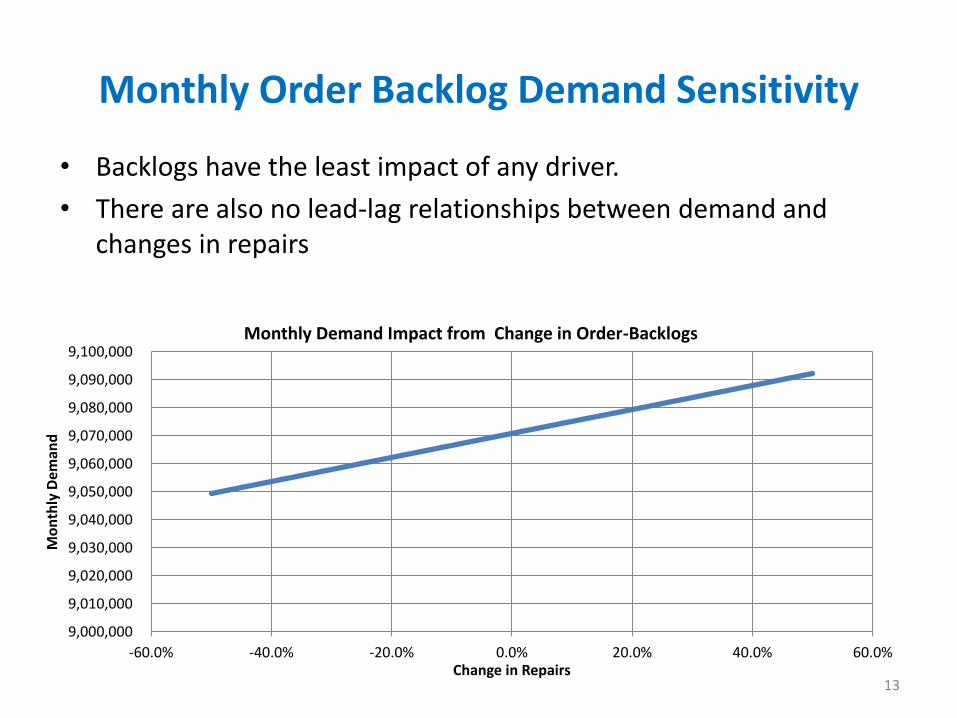

Monthly Order Backlog Demand Sensitivity

9,000,000

9,010,000

9,020,000

9,030,000

9,040,000

9,050,000

9,060,000

9,070,000

9,080,000

9,090,000

9,100,000

-60.0% -40.0% -20.0% 0.0% 20.0% 40.0% 60.0%

Mo

nth

ly D

eman

d

Change in Repairs

Monthly Demand Impact from Change in Order-Backlogs

• Backlogs have the least impact of any driver.

• There are also no lead-lag relationships between demand and changes in repairs

13

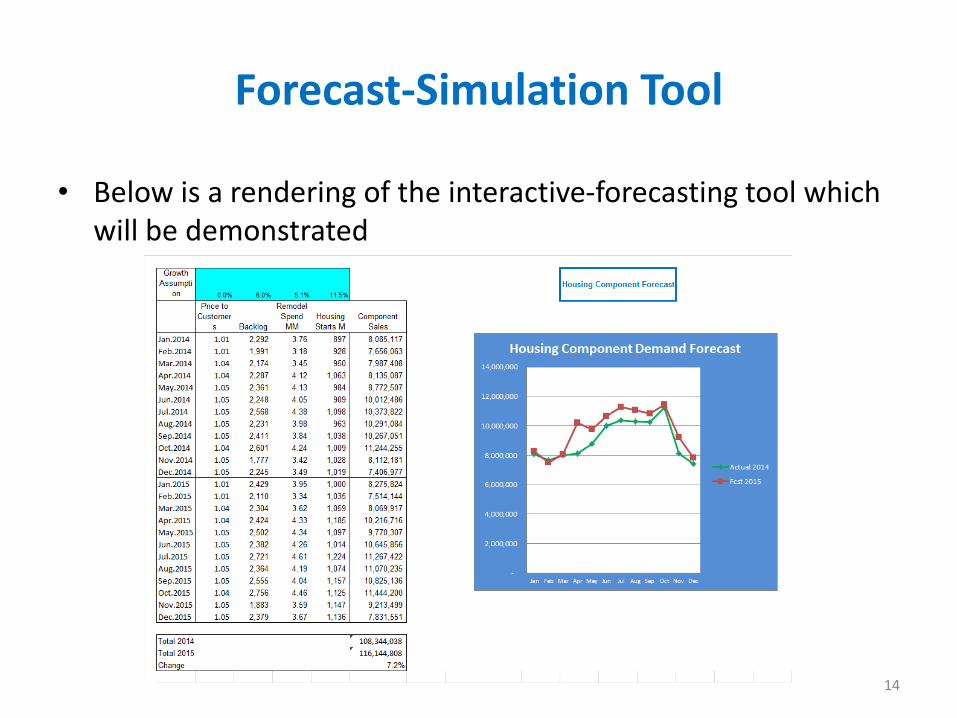

Forecast-Simulation Tool

• Below is a rendering of the interactive-forecasting tool which will be demonstrated

14

Summary

• Across 5 key business drivers, we have derived a model which connects to monthly Components demand with a 93% fit.

• For 2014, prior sales momentum and housing starts are the two leading positive drivers of annual +3.1% sales gain.

• With “modest” assumptions about the growth in key drivers, and flat pricing, for 2015, we expect to see demand growth of about +7.2% versus about +3.1% growth in 2014.

• Drawings, recurring seasonality and housing starts form the most dominant drivers of components monthly demand

15