Embed Size (px)

Citation preview

An Econometric Analysis -and- Replication of Eichengreen, Watson, and Grossman's : Bank Rate Policy Under the Interwar Gold Standard: A Dynamic Probit Model

By: Kabeed Mansur

__________________________________________________________

Introduction

In the paper we analyzed for replication, the authors put forward the following argument - which serves as the main thesis of the study: The author's posit that, that:

"Classical gold standard occupies an almost mystical position in the literature on international finance...[and] is portrayed as a remarkably durable and efficient mechanism for achieving price and exchange rate stability...[However], all to often, scant mention is made of the interwar (1925-1931) gold standard, for it is not evident how interwar experience fits into [this] view....It is clear [as the authors contend] the interwar gold standard was far from durable...The system was anything but conducive to stability". (Eichengreen, Watson, Grossman, 725).

In order to defend this position, the article identifies a number of possible explanations - however, the most prominent of these explanations concerns the role played by central banks during the interwar period. "Perhaps the most popular villains of all are the major central banks...it is alleged, [that] central banks failed to play by the rules of the game ... previously [prior to 1925] seen as intervening through open market operations to amplify the impact on domestic asset supplies of an imbalance in the external accounts, after 1925 they sterilized gold flows instead." (Ibid, 725). To this end:

"...the [case] is made with special force conerning the most visible of central bank instruments: the discount rate (bank Rate)...central banks were compelled to raise their discount rates when confronted by a sustained loss of gold, all to often they refrained from reducing those rates when acquiring reserves...[Thus], by hesitating to act...central banks may have impeded the international adjustment process during the interwar period." (Ibid, 726)

What will follow in our forthcoming analysis will not be an appraisal of this thesis, but rather, our goal will be to partially replicate the empirical results put foreward in the article. The authors specific choice of metrics is motivated by the following questions, which they seek to address and use as their analytical framework:

_____________________

1. First, was the discount rate policy asymmetric in the sense that the bank raised its

discount rate upon losing reserves but failed to lower it upon gaining them?

2. Secondly, was the bank responsive not only to the balance of payments but also to internal conditions when making Bank Rate decisions?

____________________

We will break our analysis into three sections, whereby, we define the variables to be used and the accompanying estimation method as developed the authors in section 1. In section 2 we present the results of our replication and compare it with those published in the article; analyzing and explaining possible causes/reasons for deviation between the two. In the final section, we interpret the empirical results and discuss the implications of these results in the context of the two questions posed above. It is important to quickly note here - before proceeding to our analysis/replication - that the central bank identified herein by the authors and on which the data set is contingent will be: The Bank of England. Moreover, the data used by the authors in their study, and which we will use in our replication was gathered weekly for all variables starting from May 1925 and extending through September 1931. Definition of Variables and Specification of Estimation Method In this section we will define the variables used by the authors - some variables are not listed, this is because either data sets for these are incomplete, unavailable, or not of direct interest to our replication. Therefore, the variables to be defined herein, will be only those strictly considered in our forthcoming replication. After we define our variables, the next task will be to identify the specific estimation method used to investigate and model the variables and their relationships - again, we will only consider a single estimation method insofar as it will be the method used to run our replication, namely: an Ordinary Least Squares(OLS) regression. Table 1- below, presents a definition of variables used in the replication:

____________________________________

Table 1 - Definition of Variables Variable Definition

DBR Change in Bank Rate DGFALL Fall in Gold Reserves DGRISE Rise in Gold Reserves BRHIGH Bank Rate <4% DBRLR (BR - i) DI (London i - NY i)

--------------------------------------------------------------------------------------------------------------- The estimation method we will seek to replicate is an OLS regression:

Since, the authors model DBR as a dependent variable depnding on the following vector of predetermined variables:

DBR = f (DGFall, DGRise, BRHigh, RBRLR, DBRLR, DI).

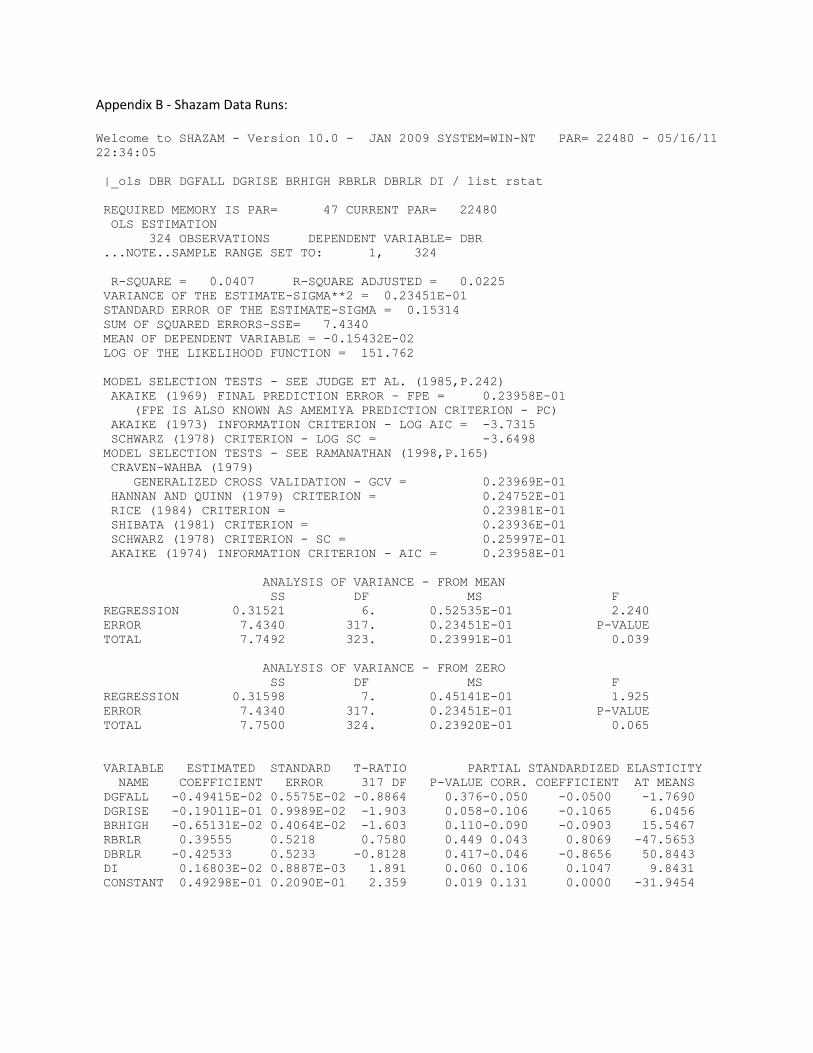

Presentation and Discussion of Replicated OLS v. Actual OLS In this section, we will present a tabular comparison of results obtained from our OLS replication runs in Shazam with those obtained and presented by the authors in the article. We will then analyze and present a possible explanation of causal factors contributing to the observed deviations between the replicated and actual results. Comparison of Replicated OLS v. Actual OLS is found below in table 2.

________________________

Table 2. Replicated OLS v. Actual OLS

Rep. OLS Article OLS

Variable Error Est. Error Est.

DGSFall 0.005 - 0.0049 0.005 -0.0049

DGRise 0.009 0.019 0.009 0.011

BRHigh 0.004 -0.0065 0.004 -0.008

DBRLR 0.034 0.0118 0.034 0.012

DI 0.010 -0.012 0.011 -0.009

Possible reasons for deviation in the OLS replication data from the actual OLS data can e

attributed to two possible causes:

1. Incomplete Data Sets

2. Non Transformed Data Set

We identify these two possible casual factors based on the following disclaimer attached to the data set

by the authors:

________________________________

Data notes on "Bank Rate Policy Under the Interwar Gold Standard: A Dynamic

Probit Model" by Barry Eichengreen, Mark Watson and Richard Grossman, The

Economic Journal, Vol. 95, September 1985, pp 725-745.

These notes were compiled in 1998 and are unfortunately a bit sketchy. The raw data series that I could

find are in the *.txt files. There is a description of the data at the bottom of these files.

The data that were used in the paper (sometimes transformed) are in the *.dat files. Each of these files

contains 328 observations on the relevant variable.

(Source: Readme.txt file attached to Data Set).

________________________________

Discussion and Implications of the Empirical Results

Despite deviations in the replicated v. actual OLS estimates; we do observe that both results

follow a similar trajectory. In this section we discuss what the implications of these results are, in

genereal, in regards to the two questions posed in the introduction. To this end, we see that the:

"OLS are quite plausible: all coefficients (eg, the ones considered in this paper) have

the anticipated signs and are of reasonable magnitudes. For example, the negative

coefficient on DGRall suggests that the bank of England responded to a loss of

reserves by raising Bank Rate, ceteris paribus...The negative coefficient on BRHigh

suggests that the Bank of England did attempt to lower Bank Rate when it exceeded

4%. The negative coefficients on on the difference between the Bank Rate and the

London market rate, suggests that the Bank tended to raise Bank Rate when it fell

short of (exceeded) the market rate in order to insure Bank Rates

effectiveness.....The negative coefficient on [the] London - New York interest

differential (Variable DI), suggests that the Bank felt able to lower Bank Rate when

London rates were rising relative to NY rates, presumably strengthening the capital

account" (Ibid, 738-9).

In conclusion these results indeed reveal an asymmetry, as was conjectured by the authors - in

how the bank of England responded to reserve gains and losses. Our replication of these results,

although deviating somewhat from the actual results arrived at in the article, show further agreement

with the articles thesis. Thus, "such violations of the rules of the game, here adequately documented for

the firs time, may have contributed to the instability of the interwar financial system.". (Ibid, 741).

Bibliography

1). "Bank Rate Policy Under the Interwar Gold Standard: A Dynamic Probit Model" by Barry Eichengreen,

Mark Watson and Richard Grossman, The Economic Journal, Vol. 95, September 1985, pp 725-745.

2). Data Set Found at: http://www.princeton.edu/~mwatson/publi.html Journal Article #6

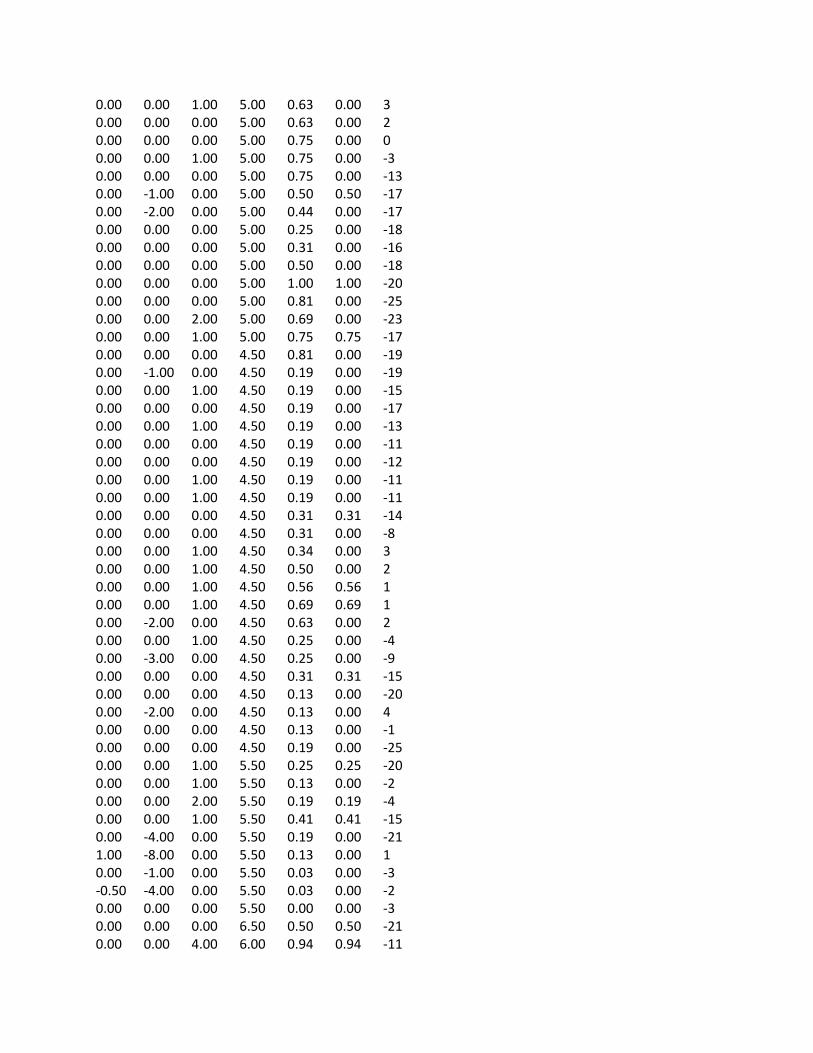

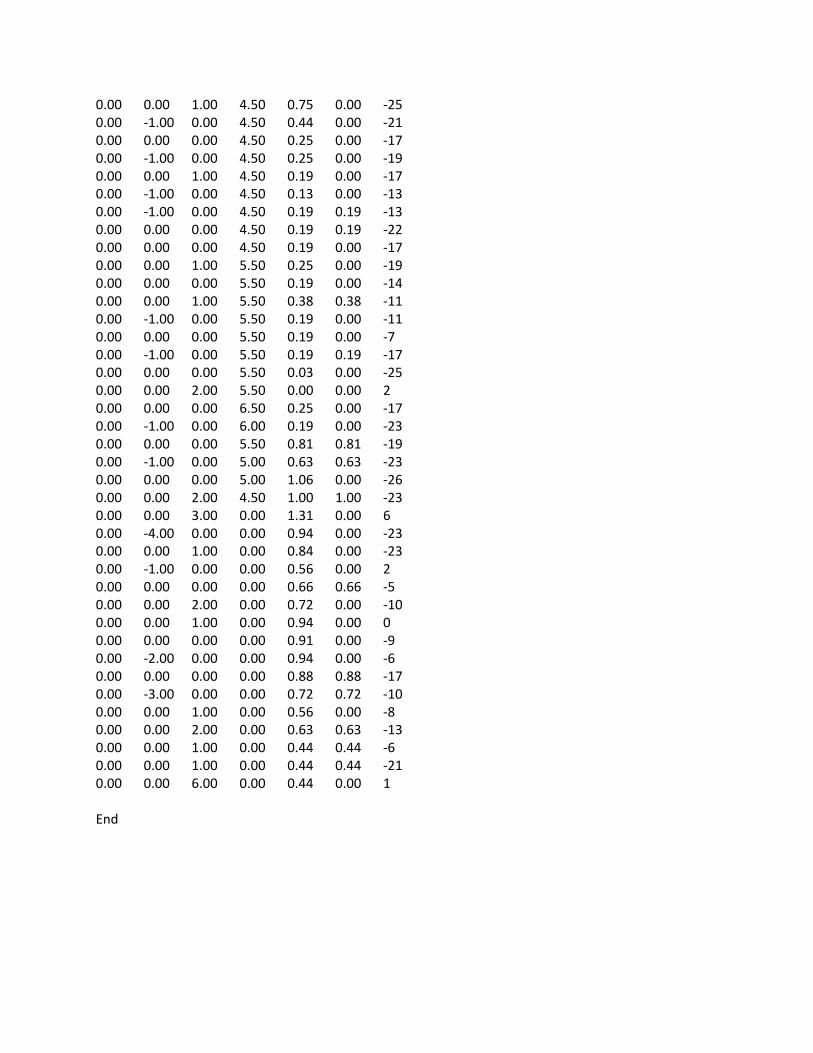

Appendix 1- Data Set:

DBR DGFall DGRise BRHigh RBRLR DBRLR DI 0.00 0.00 0.00 5.00 0.62 1 35 0.00 0.00 0.00 5.00 0.50 0.00 -3 0.00 -1.00 1.00 5.00 0.81 0.00 -6 0.00 -1.00 0.00 4.50 0.69 0.00 -2 0.00 -4.00 0.00 4.50 1.00 1.00 6 0.00 -1.00 0.00 0.00 0.25 0.00 4 0.00 -1.00 0.00 0.00 0.13 0.00 6 0.00 0.00 0.00 5.00 0.13 0.00 2 0.00 0.00 0.00 5.00 0.13 0.00 2 0.00 0.00 0.00 5.00 0.56 0.56 2 0.00 -1.00 1.00 5.00 0.63 0.00 2 0.00 0.00 0.00 5.00 0.69 0.69 2 0.00 0.00 1.00 5.00 0.63 0.00 -23 0.00 0.00 0.00 5.00 0.75 0.00 -21 0.00 0.00 0.00 5.00 0.75 0.00 -19 0.00 0.00 0.00 5.00 0.75 0.00 -15 0.00 0.00 1.00 5.00 0.44 0.00 -21 0.00 0.00 0.00 5.00 0.44 0.00 1 0.00 0.00 0.00 5.00 0.31 0.00 -22 0.00 -1.00 1.00 5.00 0.31 0.31 -18 0.00 0.00 0.00 5.00 0.88 0.88 -12 0.00 -1.00 0.00 5.00 0.75 0.00 -8 0.00 0.00 0.00 5.00 0.88 0.00 -2 0.00 0.00 1.00 5.00 0.69 0.69 2 0.00 -1.00 1.00 5.00 0.06 0.00 -6 0.00 0.00 0.00 4.50 0.81 0.00 -8 0.00 0.00 0.00 4.50 0.19 0.00 -18 0.00 0.00 0.00 4.50 0.19 0.00 -20 0.00 -1.00 0.00 4.50 0.19 0.00 -12 0.00 -1.00 0.00 4.50 0.19 0.00 -10 0.00 0.00 0.00 4.50 0.19 0.00 -12 0.00 0.00 0.00 4.50 0.19 0.00 -24 0.00 0.00 0.00 4.50 0.19 0.00 5 0.00 0.00 0.00 4.50 0.19 0.00 5 0.00 0.00 2.00 4.50 0.22 0.00 -3 0.00 0.00 2.00 4.50 0.31 0.00 1 0.00 -1.00 1.00 4.50 0.34 0.34 -19 0.00 0.00 0.00 4.50 0.50 0.00 -2 0.00 0.00 0.00 4.50 0.50 0.00 -2 0.00 0.00 1.00 4.50 0.63 0.63 -10 0.00 0.00 1.00 4.50 0.63 0.00 -6 0.00 0.00 0.00 4.50 0.44 0.00 -8 0.00 0.00 1.00 4.50 0.25 0.00 2 0.00 0.00 0.00 4.50 0.25 0.00 -24 0.00 -3.00 0.00 4.50 0.13 0.00 0

0.00 -1.00 0.00 4.50 0.13 0.00 -6 1.00 0.00 0.00 4.50 0.19 0.00 -4 0.00 -3.00 1.00 4.50 0.19 0.00 -2 0.00 0.00 0.00 4.50 0.19 0.00 -4 0.00 0.00 0.00 5.50 0.25 0.00 6 0.00 0.00 1.00 5.50 0.16 0.00 -6 0.00 0.00 2.00 5.50 0.38 0.00 -8 0.00 -3.00 0.00 5.50 0.19 0.00 -13 0.00 -5.00 0.00 5.50 0.13 0.00 -2 0.00 -2.00 0.00 5.50 0.06 0.00 -8 0.00 0.00 0.00 5.50 0.03 0.00 -4 0.00 0.00 0.00 5.50 0.03 0.03 -6 -0.50 0.00 1.00 6.50 0.38 0.38 -10 0.00 0.00 1.00 6.00 0.31 0.31 -14 -0.50 0.00 3.00 5.50 0.69 0.00 -16 -0.50 0.00 3.00 5.00 0.94 0.94 -18 0.00 0.00 1.00 5.00 1.09 1.09 -8 -0.50 0.00 1.00 4.50 1.13 1.13 -8 0.00 0.00 1.00 0.00 1.13 0.00 -2 0.00 -1.00 0.00 0.00 1.09 1.09 -6 0.00 0.00 0.00 0.00 0.84 0.00 -4 0.00 -1.00 0.00 0.00 0.75 0.75 0 0.00 0.00 0.00 0.00 0.56 0.00 4 0.00 0.00 1.00 0.00 0.81 0.81 -7 0.00 0.00 0.00 0.00 0.94 0.00 -11 0.00 -1.00 1.00 0.00 0.91 0.00 -13 0.00 -3.00 0.00 0.00 0.75 0.00 -12 0.00 -2.00 0.00 0.00 0.81 0.00 -11 0.00 0.00 0.00 0.00 0.81 0.81 -3 0.00 0.00 1.00 0.00 0.56 0.00 -1 0.00 0.00 0.00 0.00 0.38 0.00 -3 0.00 0.00 0.00 0.00 0.44 0.00 -25 0.00 0.00 0.00 0.00 0.44 0.00 -20 1.00 0.00 1.00 0.00 0.47 0.47 -16 0.00 -15.00 2.00 0.00 0.47 0.47 -20 0.00 0.00 0.00 0.00 0.13 0.00 3 -0.50 0.00 1.00 4.50 0.31 0.31 -26 0.00 0.00 2.00 5.00 0.63 0.00 -26 -0.50 0.00 0.00 5.00 0.50 0.00 -26 0.00 -1.00 0.00 5.00 0.75 0.00 -3 0.00 0.00 0.00 4.50 0.75 0.75 -3 0.00 -2.00 0.00 4.50 0.94 0.00 -15 0.00 -1.00 0.00 0.00 0.25 0.00 -7 0.00 0.00 0.00 0.00 0.06 0.00 -5 0.00 -1.00 0.00 5.00 0.06 0.00 -7 0.00 0.00 1.00 5.00 0.25 0.25 3 0.00 -1.00 0.00 5.00 0.75 0.75 4 0.00 0.00 0.00 5.00 0.56 0.00 2

0.00 0.00 1.00 5.00 0.63 0.00 3 0.00 0.00 0.00 5.00 0.63 0.00 2 0.00 0.00 0.00 5.00 0.75 0.00 0 0.00 0.00 1.00 5.00 0.75 0.00 -3 0.00 0.00 0.00 5.00 0.75 0.00 -13 0.00 -1.00 0.00 5.00 0.50 0.50 -17 0.00 -2.00 0.00 5.00 0.44 0.00 -17 0.00 0.00 0.00 5.00 0.25 0.00 -18 0.00 0.00 0.00 5.00 0.31 0.00 -16 0.00 0.00 0.00 5.00 0.50 0.00 -18 0.00 0.00 0.00 5.00 1.00 1.00 -20 0.00 0.00 0.00 5.00 0.81 0.00 -25 0.00 0.00 2.00 5.00 0.69 0.00 -23 0.00 0.00 1.00 5.00 0.75 0.75 -17 0.00 0.00 0.00 4.50 0.81 0.00 -19 0.00 -1.00 0.00 4.50 0.19 0.00 -19 0.00 0.00 1.00 4.50 0.19 0.00 -15 0.00 0.00 0.00 4.50 0.19 0.00 -17 0.00 0.00 1.00 4.50 0.19 0.00 -13 0.00 0.00 0.00 4.50 0.19 0.00 -11 0.00 0.00 0.00 4.50 0.19 0.00 -12 0.00 0.00 1.00 4.50 0.19 0.00 -11 0.00 0.00 1.00 4.50 0.19 0.00 -11 0.00 0.00 0.00 4.50 0.31 0.31 -14 0.00 0.00 0.00 4.50 0.31 0.00 -8 0.00 0.00 1.00 4.50 0.34 0.00 3 0.00 0.00 1.00 4.50 0.50 0.00 2 0.00 0.00 1.00 4.50 0.56 0.56 1 0.00 0.00 1.00 4.50 0.69 0.69 1 0.00 -2.00 0.00 4.50 0.63 0.00 2 0.00 0.00 1.00 4.50 0.25 0.00 -4 0.00 -3.00 0.00 4.50 0.25 0.00 -9 0.00 0.00 0.00 4.50 0.31 0.31 -15 0.00 0.00 0.00 4.50 0.13 0.00 -20 0.00 -2.00 0.00 4.50 0.13 0.00 4 0.00 0.00 0.00 4.50 0.13 0.00 -1 0.00 0.00 0.00 4.50 0.19 0.00 -25 0.00 0.00 1.00 5.50 0.25 0.25 -20 0.00 0.00 1.00 5.50 0.13 0.00 -2 0.00 0.00 2.00 5.50 0.19 0.19 -4 0.00 0.00 1.00 5.50 0.41 0.41 -15 0.00 -4.00 0.00 5.50 0.19 0.00 -21 1.00 -8.00 0.00 5.50 0.13 0.00 1 0.00 -1.00 0.00 5.50 0.03 0.00 -3 -0.50 -4.00 0.00 5.50 0.03 0.00 -2 0.00 0.00 0.00 5.50 0.00 0.00 -3 0.00 0.00 0.00 6.50 0.50 0.50 -21 0.00 0.00 4.00 6.00 0.94 0.94 -11

0.00 0.00 1.00 5.00 0.19 0.00 -15 0.00 0.00 0.00 5.00 0.88 0.00 -9 0.00 0.00 0.00 4.50 0.59 0.00 1 0.00 0.00 4.00 0.00 0.91 0.00 1 0.00 0.00 1.00 0.00 1.03 0.00 -8 0.00 -1.00 0.00 0.00 0.88 0.00 -17 0.00 -1.00 0.00 0.00 0.84 0.00 -23 0.00 -2.00 0.00 0.00 0.78 0.78 -20 0.00 0.00 1.00 0.00 0.69 0.69 -21 0.00 0.00 0.00 0.00 0.94 0.94 1 0.00 0.00 1.00 0.00 0.97 0.97 2 0.00 -1.00 0.00 0.00 0.94 0.94 -2 0.00 -1.00 0.00 0.00 0.81 0.81 -2 0.00 -1.00 0.00 0.00 0.59 0.00 -4 0.00 0.00 1.00 0.00 0.84 0.84 8 0.00 0.00 0.00 0.00 0.50 0.00 -3 0.00 0.00 2.00 0.00 0.38 0.00 6 0.00 0.00 2.00 0.00 0.38 0.00 0 1.00 0.00 1.00 0.00 0.44 0.00 1 0.00 0.00 0.00 0.00 0.44 0.00 -6 0.00 -17.00 0.00 0.00 0.56 0.56 0 0.00 -1.00 0.00 0.00 0.06 0.00 4 0.00 0.00 0.00 4.50 0.31 0.00 8 0.00 0.00 2.00 5.00 0.63 0.00 -11 0.00 0.00 0.00 5.00 0.63 0.63 -8 1.00 -1.00 0.00 4.50 0.44 0.00 -4 0.00 -2.00 0.00 4.50 0.69 0.00 -13 0.00 -1.00 0.00 0.00 0.69 0.00 -23 0.00 -1.00 0.00 0.00 0.13 0.00 -15 0.00 0.00 0.00 0.00 0.06 0.00 -11 0.00 0.00 1.00 5.00 0.13 0.13 -5 0.00 -1.00 0.00 5.00 0.44 0.44 -3 0.00 0.00 2.00 5.00 0.94 0.94 -3 0.00 0.00 0.00 5.00 0.63 0.63 -3 0.00 0.00 1.00 5.00 0.69 0.69 3 0.00 0.00 1.00 5.00 0.75 0.75 4 0.00 0.00 1.00 5.00 0.75 0.00 -22 0.00 0.00 1.00 5.00 0.69 0.00 -24 0.00 0.00 0.00 5.00 0.69 0.00 -3 0.00 -1.00 0.00 5.00 0.50 0.00 5 0.00 0.00 0.00 5.00 0.44 0.00 5 0.00 0.00 0.00 5.00 0.25 0.00 -22 0.00 -1.00 0.00 5.00 0.38 0.38 -22 -0.50 0.00 0.00 5.00 0.50 0.00 -20 0.00 0.00 0.00 5.00 0.94 0.00 -27 0.00 -1.00 0.00 5.00 0.69 0.00 -1 0.00 0.00 0.00 5.00 0.69 0.00 3 0.00 0.00 1.00 5.00 0.94 0.94 1

0.00 0.00 0.00 4.50 0.81 0.00 -15 0.00 0.00 0.00 4.50 0.19 0.00 -13 0.00 0.00 0.00 4.50 0.19 0.00 1 0.00 0.00 1.00 4.50 0.19 0.00 2 0.00 0.00 0.00 4.50 0.19 0.00 -27 0.00 0.00 0.00 4.50 0.19 0.00 -27 0.00 -1.00 0.00 4.50 0.19 0.00 -22 0.00 0.00 2.00 4.50 0.19 0.00 -1 0.00 0.00 0.00 4.50 0.19 0.00 -8 0.00 0.00 0.00 4.50 0.50 0.50 -5 0.00 0.00 0.00 4.50 0.38 0.38 -5 0.00 0.00 0.00 4.50 0.41 0.41 -1 0.00 0.00 0.00 4.50 0.50 0.00 -8 0.00 0.00 4.00 4.50 0.56 0.00 -9 0.00 0.00 1.00 4.50 0.75 0.75 -7 0.00 0.00 1.00 4.50 0.56 0.00 -2 0.00 0.00 1.00 4.50 0.25 0.00 -7 0.00 -5.00 0.00 4.50 0.25 0.00 -9 0.00 -2.00 0.00 4.50 0.25 0.00 -7 0.00 -2.00 0.00 4.50 0.13 0.00 -5 0.00 -1.00 0.00 4.50 0.13 0.00 -1 0.00 -1.00 0.00 4.50 0.06 0.00 3 0.00 0.00 1.00 4.50 0.19 0.00 -24 0.00 0.00 0.00 5.50 0.25 0.00 5 0.00 0.00 1.00 5.50 0.19 0.19 -26 0.00 0.00 1.00 5.50 0.31 0.31 -21 0.00 0.00 0.00 5.50 0.38 0.00 -23 0.00 -1.00 0.00 5.50 0.25 0.25 -22 -0.50 -1.00 0.00 5.50 0.16 0.16 -24 0.00 0.00 0.00 5.50 0.06 0.06 0 0.00 -3.00 0.00 5.50 0.00 0.00 0 0.00 -1.00 0.00 6.50 0.38 0.38 -5 0.00 0.00 3.00 6.50 0.56 0.56 -5 -0.50 0.00 5.00 5.50 0.69 0.00 3 0.00 0.00 1.00 5.00 0.25 0.25 -19 0.00 0.00 0.00 5.00 1.13 1.13 -22 0.00 0.00 1.00 4.50 0.66 0.66 -22 0.00 0.00 0.00 0.00 1.31 1.31 -21 0.00 -2.00 0.00 0.00 1.00 0.00 -19 0.00 0.00 0.00 0.00 0.88 0.00 -16 0.00 0.00 0.00 0.00 0.75 0.00 0 0.00 0.00 1.00 0.00 0.63 0.00 -19 0.00 -1.00 0.00 0.00 0.75 0.75 -8 0.00 0.00 0.00 0.00 0.94 0.00 -22 0.00 0.00 1.00 0.00 0.91 0.00 -20 0.00 -1.00 0.00 0.00 0.94 0.00 -19 0.00 -3.00 0.00 0.00 0.81 0.00 -21 0.00 -3.00 0.00 0.00 0.63 0.63 -13

-0.50 -1.00 0.00 0.00 0.78 0.00 -9 0.00 0.00 1.00 0.00 0.44 0.00 -19 0.00 -1.00 0.00 0.00 0.41 0.41 5 0.00 0.00 1.00 0.00 0.41 0.41 2 0.00 0.00 3.00 0.00 0.72 0.72 5 0.00 0.00 2.00 0.00 0.41 0.00 -1 0.00 0.00 2.00 0.00 0.63 0.63 3 0.00 0.00 1.00 4.50 0.19 0.19 7 0.00 0.00 0.00 4.50 0.31 0.00 -23 0.00 0.00 2.00 5.00 0.50 0.00 -12 0.00 0.00 0.00 5.00 0.94 0.94 -13 0.00 0.00 0.00 4.50 0.69 0.69 -7 0.00 -2.00 0.00 4.50 0.81 0.81 -2 0.00 -1.00 0.00 0.00 0.50 0.00 6 0.00 0.00 0.00 0.00 0.13 0.00 6 0.00 0.00 0.00 5.00 0.50 0.50 4 0.00 0.00 0.00 5.00 0.19 0.19 0 0.00 0.00 1.00 5.00 0.50 0.50 -4 0.00 0.00 0.00 5.00 0.69 0.00 -16 0.00 0.00 0.00 5.00 0.63 0.00 -10 0.00 0.00 0.00 5.00 0.75 0.75 -6 0.00 0.00 0.00 5.00 0.75 0.00 -2 0.00 0.00 1.00 5.00 0.75 0.00 -6 0.00 0.00 0.00 5.00 0.75 0.75 0 0.00 0.00 1.00 5.00 0.50 0.00 -23 0.00 0.00 0.00 5.00 0.50 0.00 6 0.00 0.00 0.00 5.00 0.31 0.00 2 0.00 0.00 0.00 5.00 0.25 0.00 5 0.00 0.00 0.00 5.00 0.44 0.44 -22 0.00 0.00 0.00 5.00 0.75 0.75 -19 0.00 0.00 0.00 5.00 0.94 0.00 -20 0.00 0.00 0.00 5.00 0.63 0.00 6 0.00 0.00 1.00 5.00 0.69 0.00 -4 0.00 -3.00 0.00 4.50 0.81 0.00 -9 0.00 0.00 0.00 4.50 0.25 0.00 -11 0.00 0.00 0.00 4.50 0.19 0.00 -16 0.00 0.00 0.00 4.50 0.19 0.00 -24 0.00 -1.00 0.00 4.50 0.19 0.00 -1 0.00 0.00 0.00 4.50 0.19 0.00 1 0.00 0.00 0.00 4.50 0.19 0.00 4 0.00 0.00 0.00 4.50 0.19 0.00 -24 0.00 0.00 0.00 4.50 0.19 0.00 -13 0.00 0.00 0.00 4.50 0.22 0.22 -2 0.00 -1.00 0.00 4.50 0.38 0.00 0 0.00 0.00 0.00 4.50 0.31 0.00 4 0.00 0.00 2.00 4.50 0.50 0.50 -23 0.00 0.00 0.00 4.50 0.50 0.00 -25 0.00 0.00 3.00 4.50 0.50 0.00 -23

0.00 0.00 1.00 4.50 0.75 0.00 -25 0.00 -1.00 0.00 4.50 0.44 0.00 -21 0.00 0.00 0.00 4.50 0.25 0.00 -17 0.00 -1.00 0.00 4.50 0.25 0.00 -19 0.00 0.00 1.00 4.50 0.19 0.00 -17 0.00 -1.00 0.00 4.50 0.13 0.00 -13 0.00 -1.00 0.00 4.50 0.19 0.19 -13 0.00 0.00 0.00 4.50 0.19 0.19 -22 0.00 0.00 0.00 4.50 0.19 0.00 -17 0.00 0.00 1.00 5.50 0.25 0.00 -19 0.00 0.00 0.00 5.50 0.19 0.00 -14 0.00 0.00 1.00 5.50 0.38 0.38 -11 0.00 -1.00 0.00 5.50 0.19 0.00 -11 0.00 0.00 0.00 5.50 0.19 0.00 -7 0.00 -1.00 0.00 5.50 0.19 0.19 -17 0.00 0.00 0.00 5.50 0.03 0.00 -25 0.00 0.00 2.00 5.50 0.00 0.00 2 0.00 0.00 0.00 6.50 0.25 0.00 -17 0.00 -1.00 0.00 6.00 0.19 0.00 -23 0.00 0.00 0.00 5.50 0.81 0.81 -19 0.00 -1.00 0.00 5.00 0.63 0.63 -23 0.00 0.00 0.00 5.00 1.06 0.00 -26 0.00 0.00 2.00 4.50 1.00 1.00 -23 0.00 0.00 3.00 0.00 1.31 0.00 6 0.00 -4.00 0.00 0.00 0.94 0.00 -23 0.00 0.00 1.00 0.00 0.84 0.00 -23 0.00 -1.00 0.00 0.00 0.56 0.00 2 0.00 0.00 0.00 0.00 0.66 0.66 -5 0.00 0.00 2.00 0.00 0.72 0.00 -10 0.00 0.00 1.00 0.00 0.94 0.00 0 0.00 0.00 0.00 0.00 0.91 0.00 -9 0.00 -2.00 0.00 0.00 0.94 0.00 -6 0.00 0.00 0.00 0.00 0.88 0.88 -17 0.00 -3.00 0.00 0.00 0.72 0.72 -10 0.00 0.00 1.00 0.00 0.56 0.00 -8 0.00 0.00 2.00 0.00 0.63 0.63 -13 0.00 0.00 1.00 0.00 0.44 0.44 -6 0.00 0.00 1.00 0.00 0.44 0.44 -21 0.00 0.00 6.00 0.00 0.44 0.00 1 End

Appendix B - Shazam Data Runs: Welcome to SHAZAM - Version 10.0 - JAN 2009 SYSTEM=WIN-NT PAR= 22480 - 05/16/11

22:34:05

|_ols DBR DGFALL DGRISE BRHIGH RBRLR DBRLR DI / list rstat

REQUIRED MEMORY IS PAR= 47 CURRENT PAR= 22480

OLS ESTIMATION

324 OBSERVATIONS DEPENDENT VARIABLE= DBR

...NOTE..SAMPLE RANGE SET TO: 1, 324

R-SQUARE = 0.0407 R-SQUARE ADJUSTED = 0.0225

VARIANCE OF THE ESTIMATE-SIGMA**2 = 0.23451E-01

STANDARD ERROR OF THE ESTIMATE-SIGMA = 0.15314

SUM OF SQUARED ERRORS-SSE= 7.4340

MEAN OF DEPENDENT VARIABLE = -0.15432E-02

LOG OF THE LIKELIHOOD FUNCTION = 151.762

MODEL SELECTION TESTS - SEE JUDGE ET AL. (1985,P.242)

AKAIKE (1969) FINAL PREDICTION ERROR - FPE = 0.23958E-01

(FPE IS ALSO KNOWN AS AMEMIYA PREDICTION CRITERION - PC)

AKAIKE (1973) INFORMATION CRITERION - LOG AIC = -3.7315

SCHWARZ (1978) CRITERION - LOG SC = -3.6498

MODEL SELECTION TESTS - SEE RAMANATHAN (1998,P.165)

CRAVEN-WAHBA (1979)

GENERALIZED CROSS VALIDATION - GCV = 0.23969E-01

HANNAN AND QUINN (1979) CRITERION = 0.24752E-01

RICE (1984) CRITERION = 0.23981E-01

SHIBATA (1981) CRITERION = 0.23936E-01

SCHWARZ (1978) CRITERION - SC = 0.25997E-01

AKAIKE (1974) INFORMATION CRITERION - AIC = 0.23958E-01

ANALYSIS OF VARIANCE - FROM MEAN

SS DF MS F

REGRESSION 0.31521 6. 0.52535E-01 2.240

ERROR 7.4340 317. 0.23451E-01 P-VALUE

TOTAL 7.7492 323. 0.23991E-01 0.039

ANALYSIS OF VARIANCE - FROM ZERO

SS DF MS F

REGRESSION 0.31598 7. 0.45141E-01 1.925

ERROR 7.4340 317. 0.23451E-01 P-VALUE

TOTAL 7.7500 324. 0.23920E-01 0.065

VARIABLE ESTIMATED STANDARD T-RATIO PARTIAL STANDARDIZED ELASTICITY

NAME COEFFICIENT ERROR 317 DF P-VALUE CORR. COEFFICIENT AT MEANS

DGFALL -0.49415E-02 0.5575E-02 -0.8864 0.376-0.050 -0.0500 -1.7690

DGRISE -0.19011E-01 0.9989E-02 -1.903 0.058-0.106 -0.1065 6.0456

BRHIGH -0.65131E-02 0.4064E-02 -1.603 0.110-0.090 -0.0903 15.5467

RBRLR 0.39555 0.5218 0.7580 0.449 0.043 0.8069 -47.5653

DBRLR -0.42533 0.5233 -0.8128 0.417-0.046 -0.8656 50.8443

DI 0.16803E-02 0.8887E-03 1.891 0.060 0.106 0.1047 9.8431

CONSTANT 0.49298E-01 0.2090E-01 2.359 0.019 0.131 0.0000 -31.9454