Embed Size (px)

DESCRIPTION

Citation preview

DERIVATIVES

DERIVATIVESDERIVATIVES

Derivative Contracts are wasting assets,

which derive their values from an underlying

asset. These underlying can be :

Stocks (Equity) Agri Commodities including grains,

coffee beans, etc. Precious metals like gold and silver. Foreign exchange rate Bonds Short-term debt securities such as

T-bills

TYPES OF DERIVATIVES

Forwards

Futures

Option

“A Forward Contract is a transaction wherein the buyer and the seller agree upon a delivery of a specific quality and quantity of asset usually a commodity at a specified date in future. The price may be agreed on in advance or in future.”

Forward Contract

Risk in Forward Contract

Liquidity Risk:

– Ability of the parties to buy or sell the asset whenever he wants to do

so without any significant price movement.

Other Risks

– Counter party Risk.

– Standardisation Risk

FUTURES CONTRACTFUTURES CONTRACT

It involves an obligation on both the parties i.e the buyer and the seller to fulfill the terms of the contract (i.e. these are pre-determined contracts entered today for a date in the future)

Obligation to buy or sell Stated quantity

At a specific price Stated date (Expiration Date) Marked to Market on a daily basis

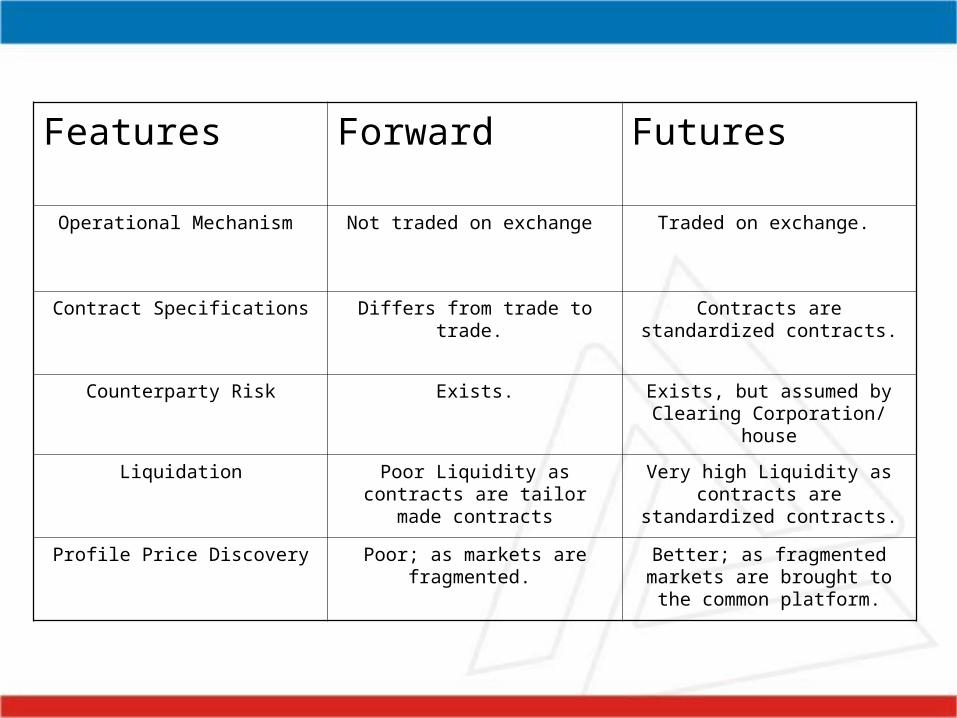

Features Forward Futures

Operational Mechanism Not traded on exchange Traded on exchange.

Contract Specifications Differs from trade to trade. Contracts are standardized contracts.

Counterparty Risk Exists. Exists, but assumed by Clearing Corporation/ house

Liquidation Poor Liquidity as contracts are tailor made contracts

Very high Liquidity as contracts are standardized contracts.

Profile Price Discovery Poor; as markets are fragmented. Better; as fragmented markets are brought to the common platform.

OPTIONS

“An Options contract confers the right but not the obligation to buy (call

option) or sell (put option) a specified underlying instrument or asset at a

specified price – the Strike or Exercised price up until or an specified

future date – the Expiry date. ”

The Price is called Premium and is paid by buyer of the option to the seller

or writer of the option.

Types of option:

Call Option

Put option

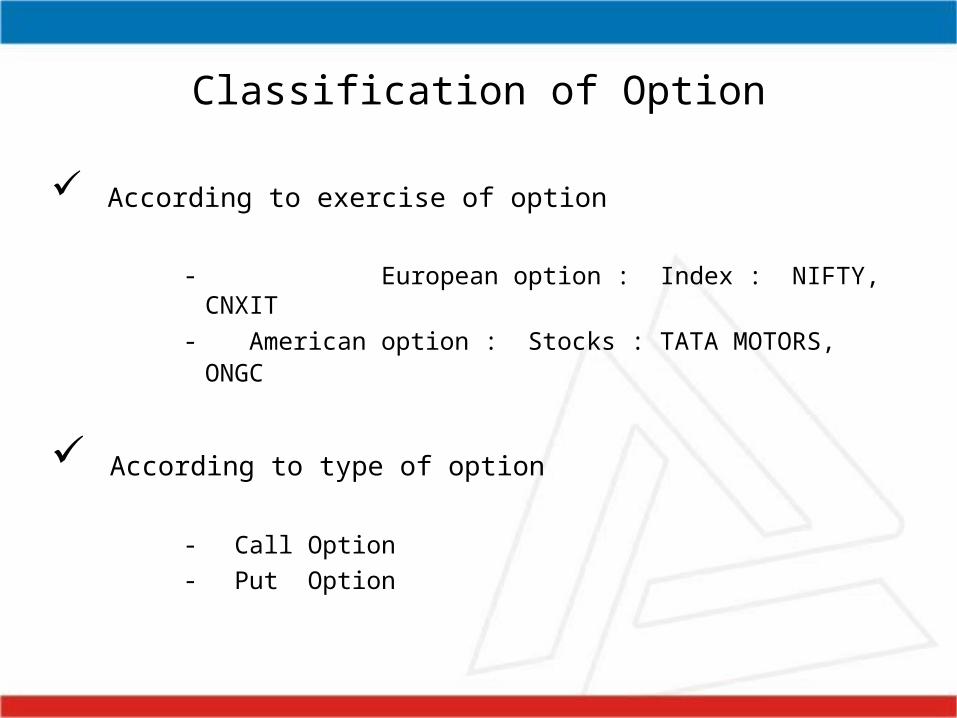

Classification of Option

According to exercise of option

- European option : Index : NIFTY, CNXIT

- American option : Stocks : TATA MOTORS, ONGC

According to type of option

- Call Option

- Put Option

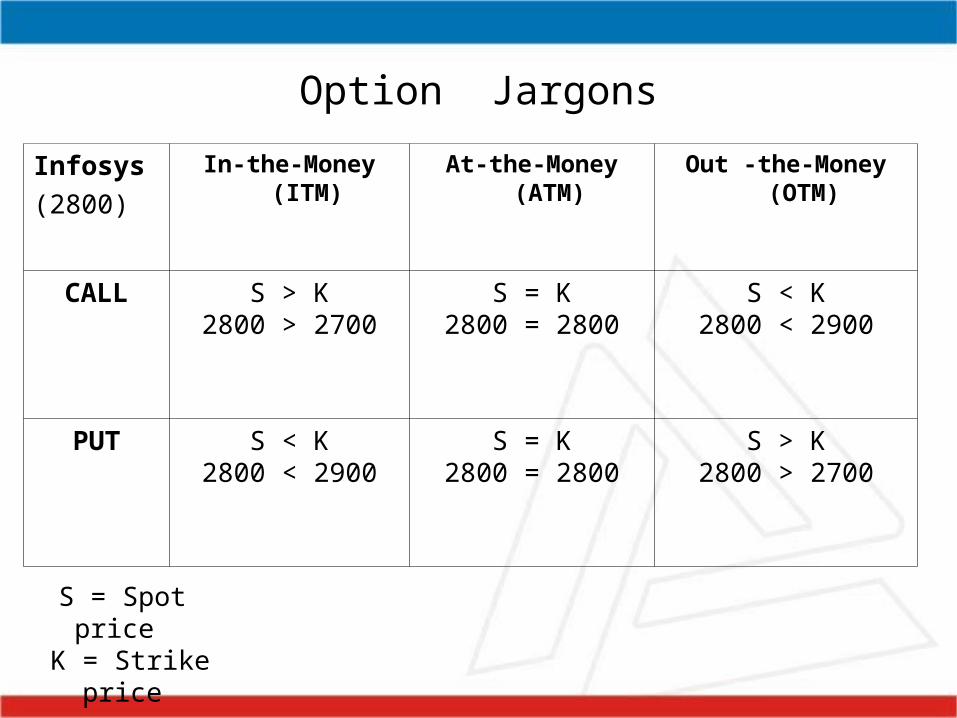

Option Jargons

Infosys

(2800)

In-the-Money (ITM) At-the-Money (ATM) Out -the-Money (OTM)

CALL S > K2800 > 2700

S = K2800 = 2800

S < K2800 < 2900

PUT S < K2800 < 2900

S = K2800 = 2800

S > K2800 > 2700

S = Spot price K = Strike

price

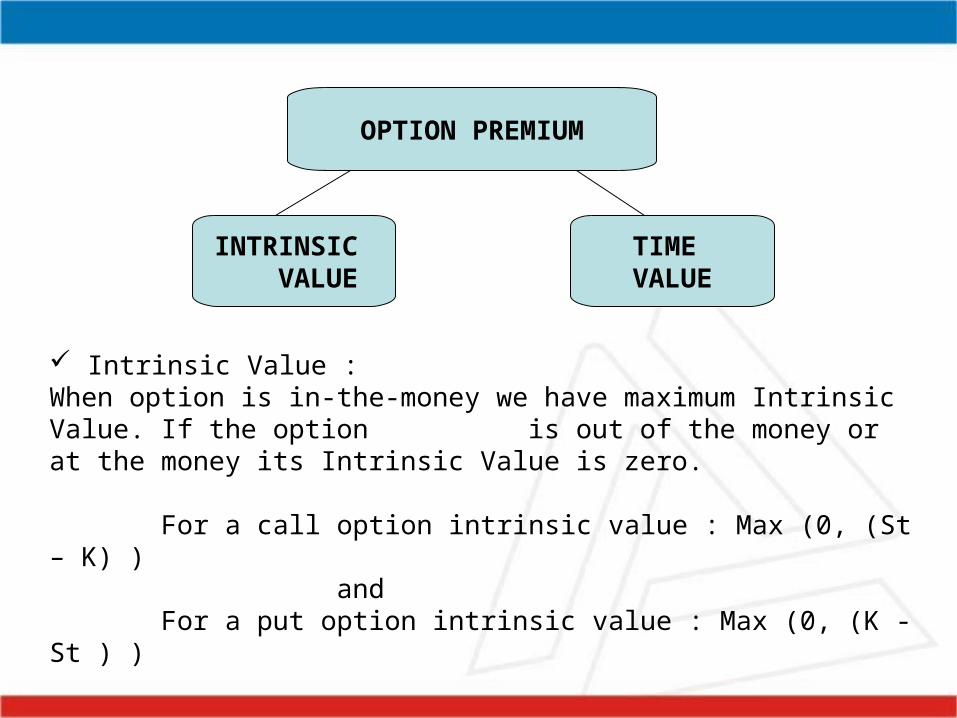

INTRINSIC VALUE

TIME VALUE

Intrinsic Value :When option is in-the-money we have maximum Intrinsic Value. If the option is out of the money or at the money its Intrinsic Value is zero.

For a call option intrinsic value : Max (0, (St – K) ) and

For a put option intrinsic value : Max (0, (K - St ) )

OPTION PREMIUM

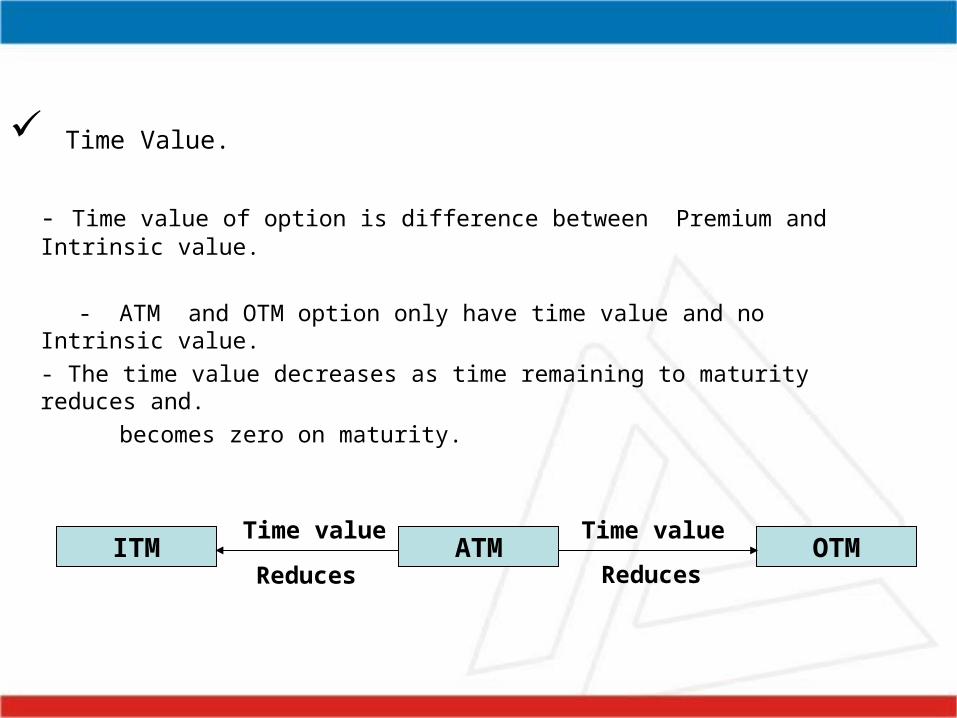

Time Value.

- Time value of option is difference between Premium and Intrinsic value.

- ATM and OTM option only have time value and no Intrinsic value.

- The time value decreases as time remaining to maturity reduces and.

becomes zero on maturity.

ATMITM OTM

Time value

Reduces

Time value

Reduces

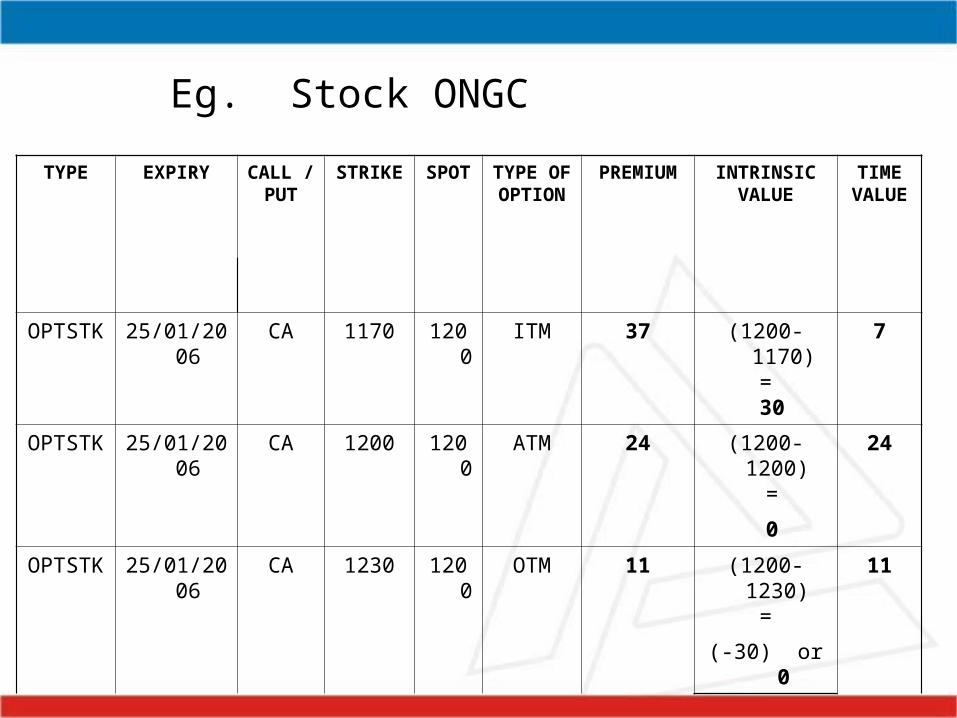

Eg. Stock ONGC

TYPE EXPIRY CALL / PUT

STRIKE SPOT TYPE OFOPTION

PREMIUM INTRINSICVALUE

TIMEVALUE

OPTSTK 25/01/2006 CA 1170 1200 ITM 37 (1200-1170)=

30

7

OPTSTK 25/01/2006 CA 1200 1200 ATM 24 (1200-1200) =

24

0

OPTSTK 25/01/2006 CA 1230 1200 OTM 11 (1200-1230) =

11

(-30) or 0

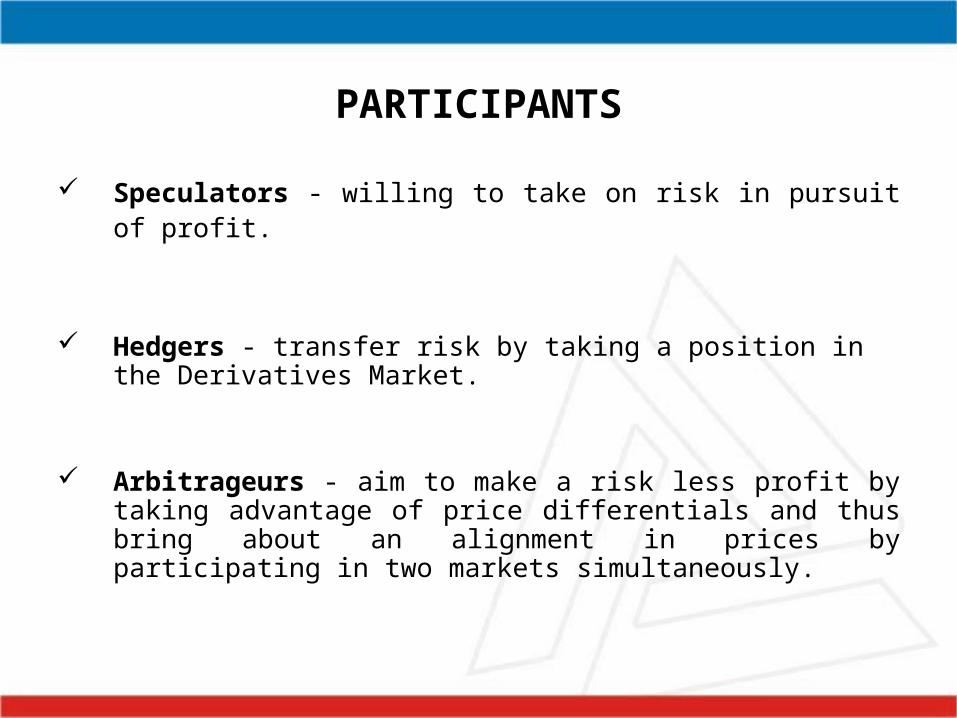

PARTICIPANTS

Speculators - willing to take on risk in pursuit of profit.

Hedgers - transfer risk by taking a position in the Derivatives Market.

Arbitrageurs - aim to make a risk less profit by taking advantage of price differentials and thus bring about an alignment in prices by participating in two markets simultaneously.

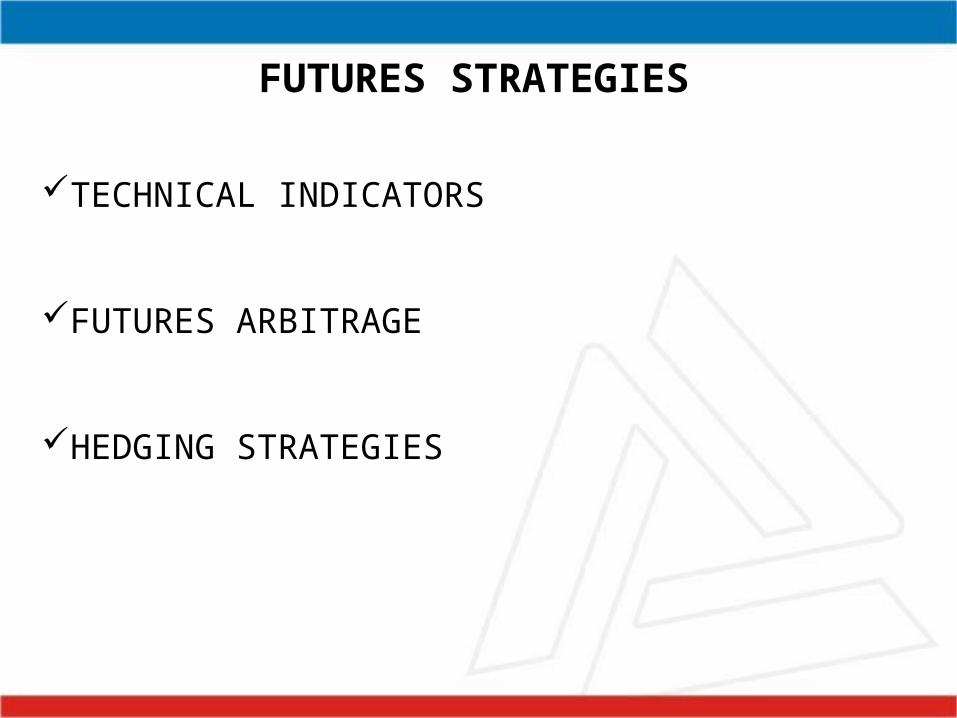

FUTURES STRATEGIES

TECHNICAL INDICATORS

FUTURES ARBITRAGE

HEDGING STRATEGIES

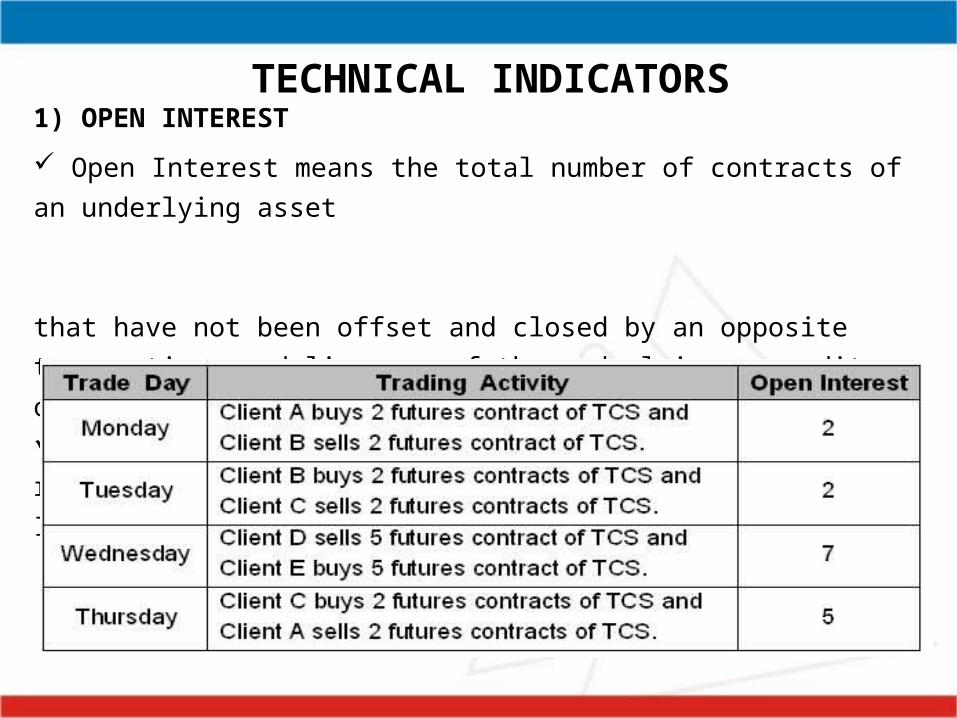

1) OPEN INTEREST

Open Interest means the total number of contracts of an underlying asset

that have not been offset and closed by an opposite transaction or delivery of

the underlying commodity or by cash settlement. Sum of all positions taken by different traders are reflected in the Open

Interest.

TECHNICAL INDICATORS

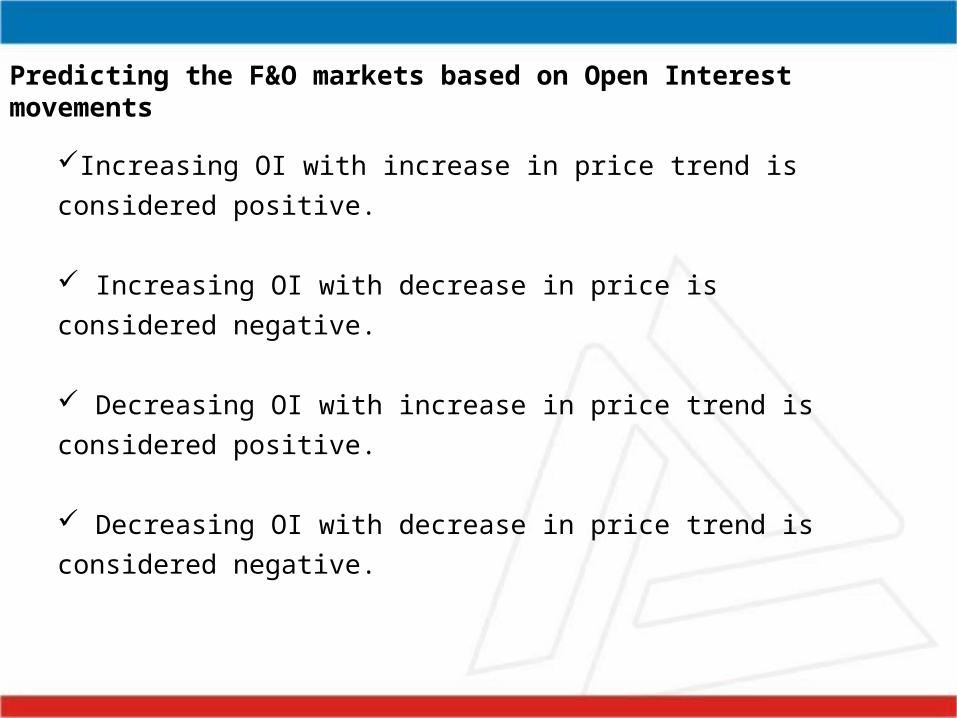

Predicting the F&O markets based on Open Interest movements

Increasing OI with increase in price trend is considered positive.

Increasing OI with decrease in price is considered negative.

Decreasing OI with increase in price trend is considered positive.

Decreasing OI with decrease in price trend is considered negative.

2) PUT CALL RATIO

The Put/Call Ratio is the number of put options contracts traded

divided by the number of call options contracts traded.

If put call ratio is high, it means more put options are trading in

the market which is an indicator of bearishness.

Whereas if the put call ratio is low then it indicates bullishness.

Put call ratio of options shows an inverse relationship with

market.

Volatility

It is a statistical measure of a market or a security's price movements over

a period of time.

Mathematically volatility is often expressed as standard deviation.

There are two types of volatility:

- Historical Volatility.

- Implied Volatility.

Historical Volatility

• Historical volatility is a measure of actual price changes during a specific time

period in the past.

• It is the annualized standard deviation of daily returns during a specific period.

• Historical volatility is also referred to as actual volatility or realized volatility.

• For short-term volatility, generally 5 days, 10 days, 20 days or 30 days time

frame is considered. Whereas for long term volatility, normally 60 day, 180 day

or 360 day time period is considered.

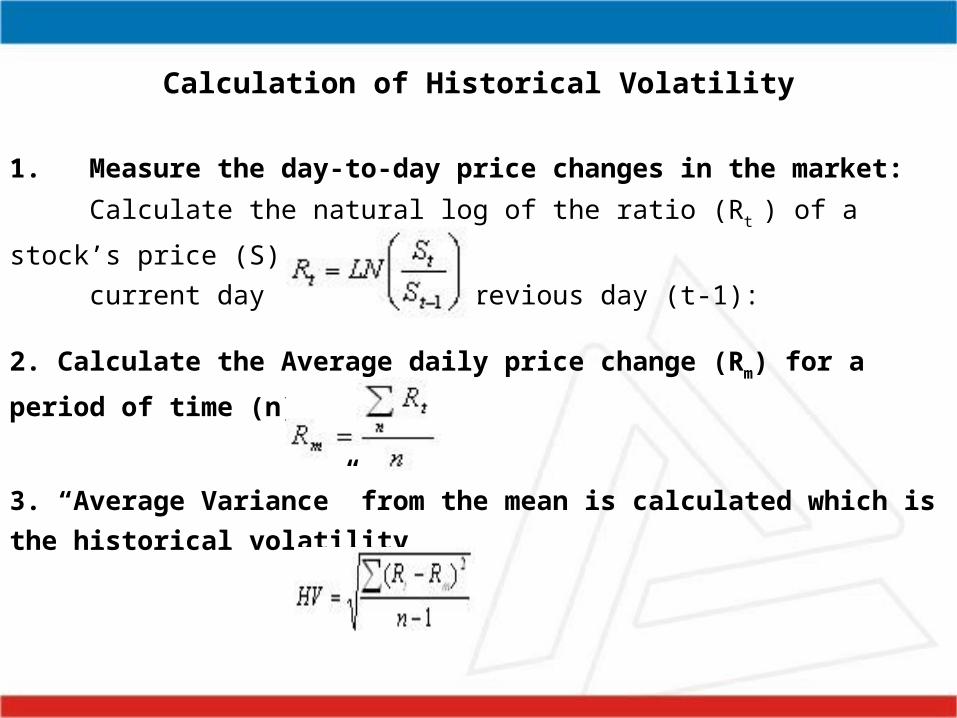

Derivatives’ StrategiesCalculation of Historical Volatility

1. Measure the day-to-day price changes in the market:

Calculate the natural log of the ratio (Rt ) of a stock’s price (S) from the

current day (t) to the previous day (t-1):

2. Calculate the Average daily price change (Rm) for a period of time (n)

3. “Average Variance” from the mean is calculated which is the historical

volatility

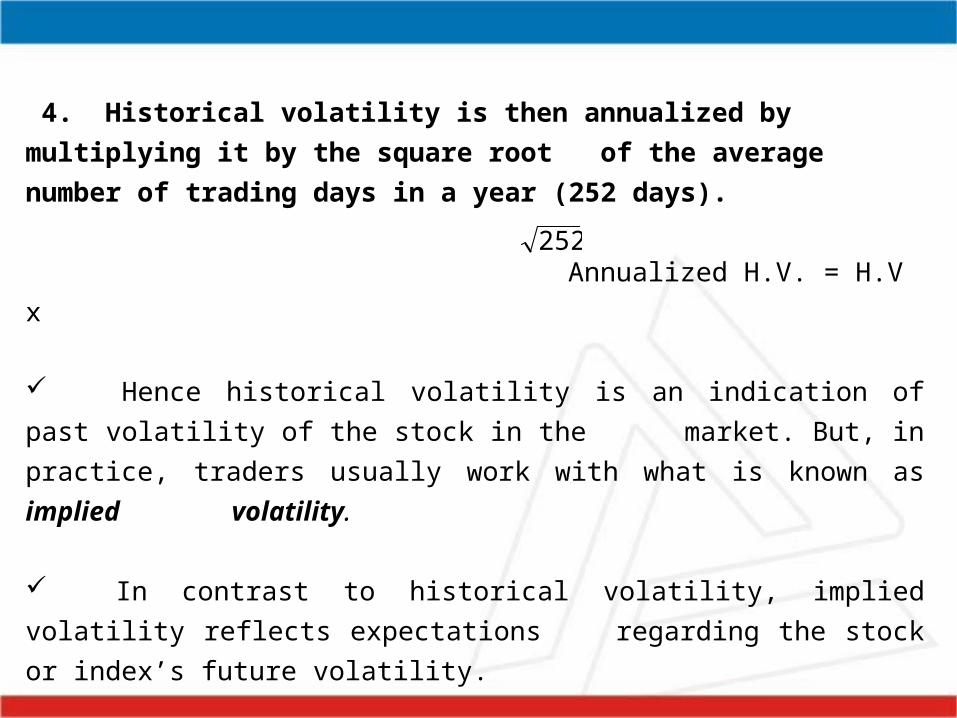

Derivatives’ Strategies 4. Historical volatility is then annualized by multiplying it by the square root

of the average number of trading days in a year (252 days).

Annualized H.V. = H.V x

Hence historical volatility is an indication of past volatility of the stock in the

market. But, in practice, traders usually work with what is known as implied

volatility.

In contrast to historical volatility, implied volatility reflects expectations

regarding the stock or index’s future volatility.

252

Implied Volatility

• Implied volatility of a stock or an index is computed using an option pricing

model such as the Black-Scholes or Binomial.

• Rising implied volatility causes option prices to rise while falling implied

volatility results in lower option premiums.

• The value of an option consists of several components like - strike price, spot

price, expiration date, implied volatility of the stock and prevailing interest rates.

Derivatives’ Strategies• On a given stock, there would generally be a number of calls outstanding,

which may have different exercise prices and expiration dates.

• From each of these we can make an estimate about the standard deviation of

the stock’s rate of return.

• The various standard deviations are then combined on a simple or weighted

average basis and an estimate about the volatility can be made.

• Therefore implied volatility is that level of volatility which is calculated from

the current trading option price.

FUTURES ARBITRAGE

Arbitrage is the act of simultaneously buying and selling assets or commodities in an attempt to exploit a profitable opportunity.

Arbitrage is done between two related instruments which are temporarily mis-priced. For example, the futures price and spot price are related by the interest rate, time to maturity and corporate benefit, if any, in the interregnum.

If the two prices do not move in tandem, then it throws up arbitrage opportunity. An arbitrageur will buy what is cheap and sell what is costly and lock in profits without any risk.

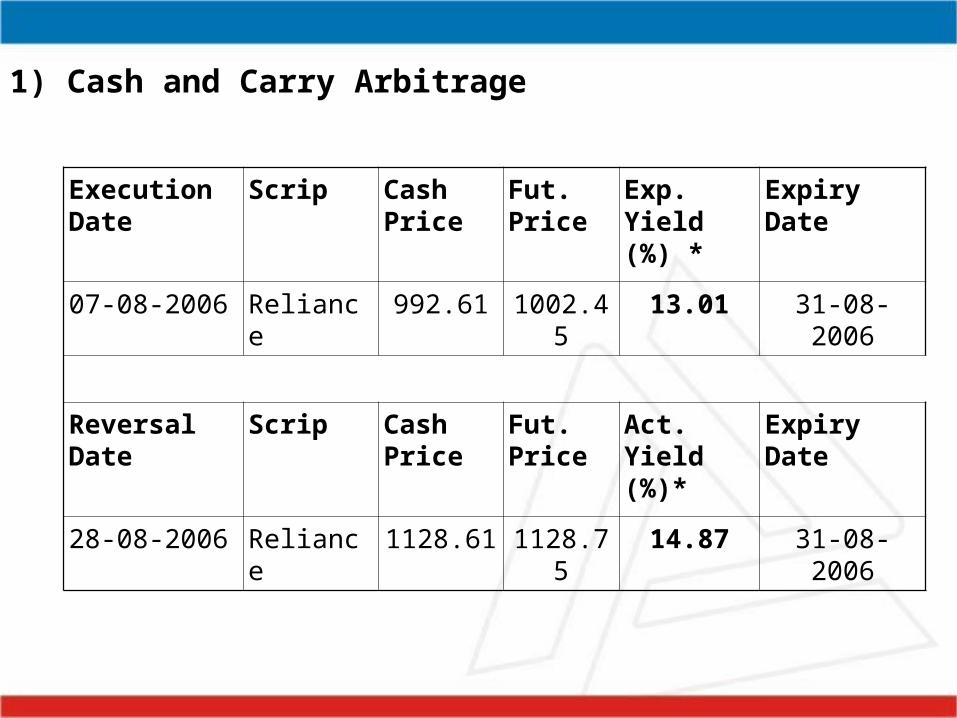

Execution Date

Scrip Cash Price

Fut. Price

Exp. Yield (%) *

Expiry Date

07-08-2006 Reliance 992.61 1002.45 13.01 31-08-2006

Reversal Date Scrip Cash Price

Fut. Price

Act. Yield (%)*

Expiry Date

28-08-2006 Reliance 1128.61 1128.75 14.87 31-08-2006

1) Cash and Carry Arbitrage

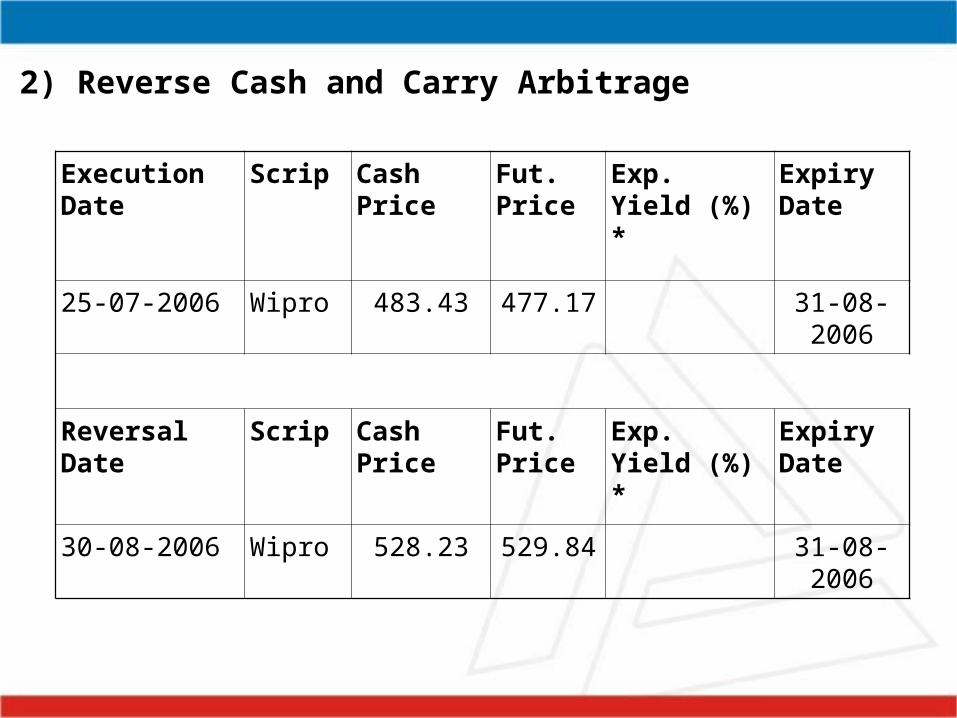

2) Reverse Cash and Carry Arbitrage

Execution Date Scrip Cash Price Fut. Price

Exp. Yield (%) *

Expiry Date

25-07-2006 Wipro 483.43 477.17 31-08-2006

Reversal Date Scrip Cash Price Fut. Price

Exp. Yield (%) *

Expiry Date

30-08-2006 Wipro 528.23 529.84 31-08-2006

Index Arbitrage is the basis between the Index (Nifty) futures and its constituents (Basket).

Nifty future is in discount to Nifty spot – Buy Nifty Futures and Sell Basket.

Nifty future is in premium to Nifty spot – Buy Basket and Sell Nifty Futures.

As we can’t trade in Nifty spot, we have to create Basket of Nifty components either with underlying stock or stock futures.

INDEX ARBITRAGE

If Nifty is in discount (as quite often), then you have to sell basket.

As you cannot short sell in cash, we will be creating basket using stock futures.

Advantage of using stock futures is – only margin money will be deployed.

We will be creating Basket based on the weight of the constituents in the Nifty.(Market Capitalization Method)

We have to make portfolio - “Perfect Hedge”.

PROCESS

Contd…

Minimum exposure of 242 contracts in Nifty (12,100 units) as it will be best hedge. All the stocks will participate according to their actual weights on the exposure of 242 contracts in Nifty.

Once good returns have been observed we will execute the strategy. Execution requires highly skilled arbitrageurs.

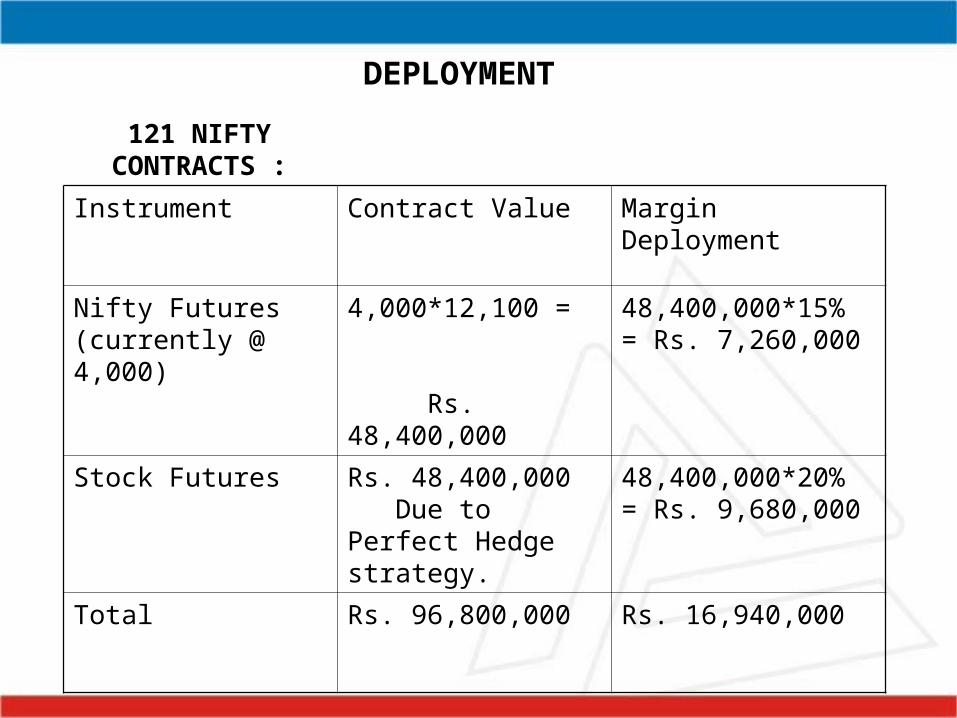

121 NIFTY CONTRACTS :

Instrument Contract Value Margin Deployment

Nifty Futures (currently @ 4,000)

4,000*12,100 = Rs. 48,400,000

48,400,000*15% = Rs. 7,260,000

Stock Futures Rs. 48,400,000 Due to Perfect Hedge strategy.

48,400,000*20% = Rs. 9,680,000

Total Rs. 96,800,000 Rs. 16,940,000

DEPLOYMENT

RETURNS

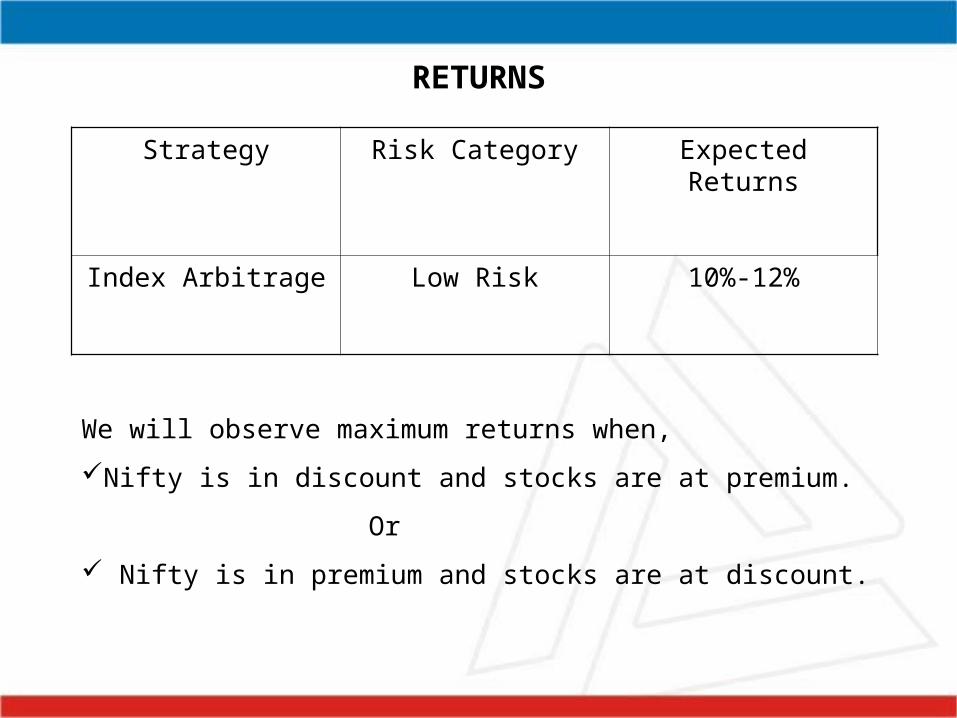

Strategy Risk Category Expected Returns

Index Arbitrage Low Risk 10%-12%

We will observe maximum returns when,

Nifty is in discount and stocks are at premium.

Or

Nifty is in premium and stocks are at discount.

RISKS

Lot size constraint : As we have to buy/sell stocks in lot size in futures, so weights of stocks may differ from actual weights

which may lead to some loss.

Execution risk : As both trades have to be executed simultaneously, there can be slippage costs. As we have to execute

trades at Market Price and due to low liquidity in some of the stocks Bid/Ask spread can be high which may lead to some loss.

MANAGING RISKS

Lot size risk can be minimized by making the portfolio close to “Perfect Hedge”. If we execute the strategy for 242 contracts then the problem will be solved as most of the stocks will participate in their actual weights.

These transactions are very execution intensive and hence require highly skilled dealers and researchers who can explore all the opportunities available in the market and exploit them in the best possible manner.

HEDGINGProtecting the value of an asset against risk arising out of fluctuations in price is known as hedging. Technically hedging means transfer of risk from the asset holder to another person who is willing to carry risk.

When an investor is bearish on market, he can hedge his position by taking countervailing position against his portfolio, say, selling Nifty futures.

If the market falls, the fall in portfolio value will be compensated by the gains on the Nifty futures. But if the market rises, the rise in the portfolio value would be offset against the futures loss.

The same concept can be applied to any stocks which have a presence in futures market. The result of any Perfect Hedge contract is – “No Profit and No Loss”

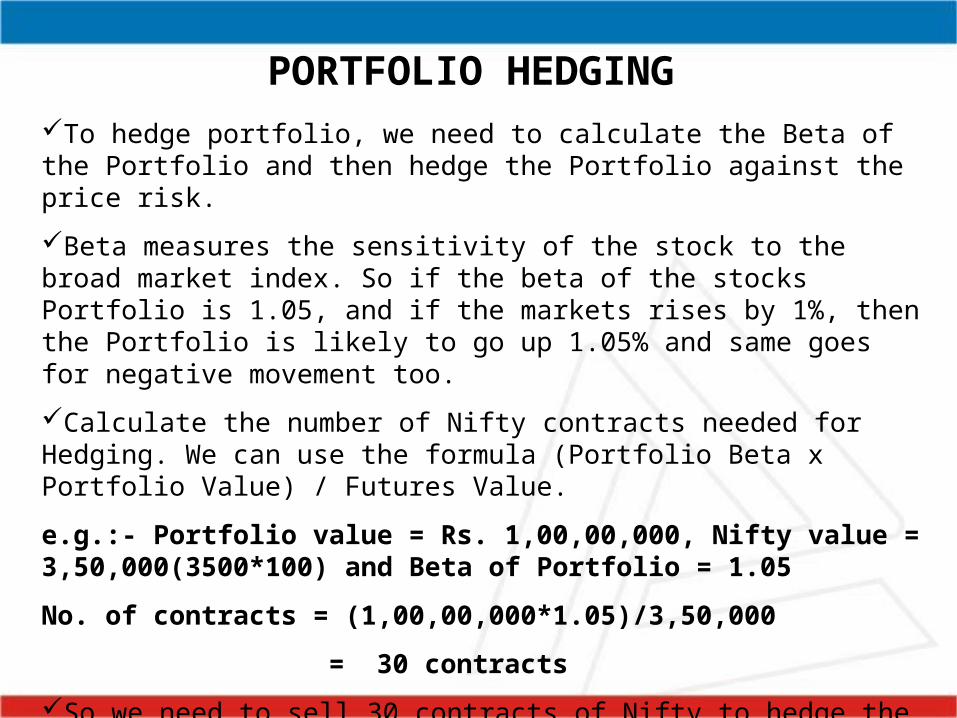

PORTFOLIO HEDGINGTo hedge portfolio, we need to calculate the Beta of the Portfolio and then hedge the Portfolio against the price risk.

Beta measures the sensitivity of the stock to the broad market index. So if the beta of the stocks Portfolio is 1.05, and if the markets rises by 1%, then the Portfolio is likely to go up 1.05% and same goes for negative movement too.

Calculate the number of Nifty contracts needed for Hedging. We can use the formula (Portfolio Beta x Portfolio Value) / Futures Value.

e.g.:- Portfolio value = Rs. 1,00,00,000, Nifty value = 3,50,000(3500*100) and Beta of Portfolio = 1.05

No. of contracts = (1,00,00,000*1.05)/3,50,000

= 30 contracts

So we need to sell 30 contracts of Nifty to hedge the Long Portfolio.

OPTIONS STRATEGIES

HEDGING STRATEGIES

DIRECTIONAL SPREADS

VOLATILITY SPREADS

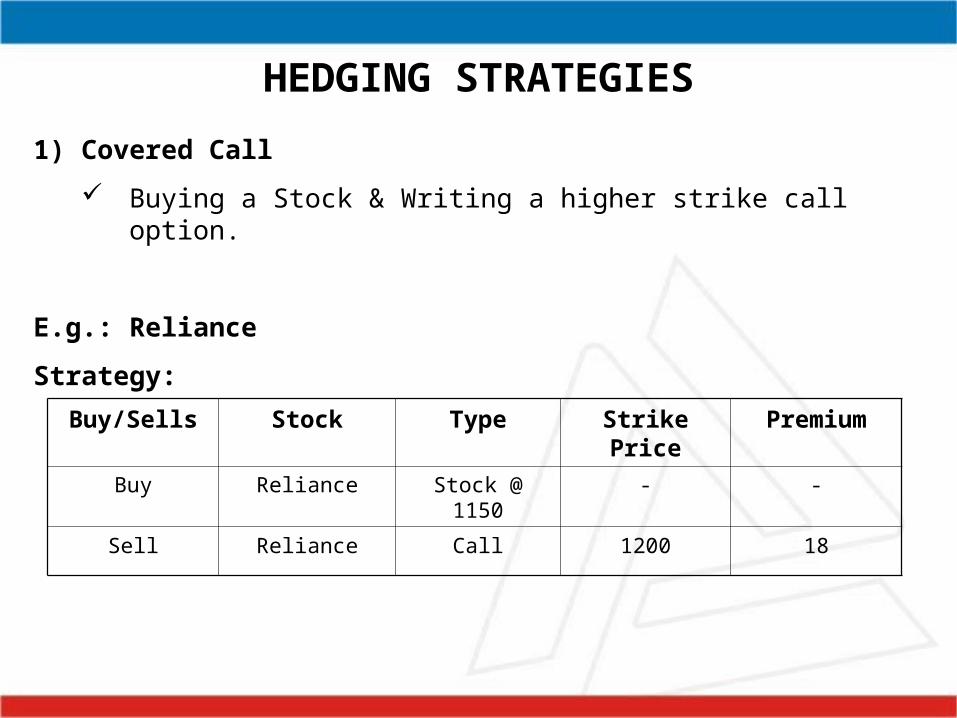

HEDGING STRATEGIES

1) Covered Call

Buying a Stock & Writing a higher strike call option.

E.g.: Reliance

Strategy:

Buy/Sells Stock Type Strike Price Premium

Buy Reliance Stock @ 1150 - -

Sell Reliance Call 1200 18

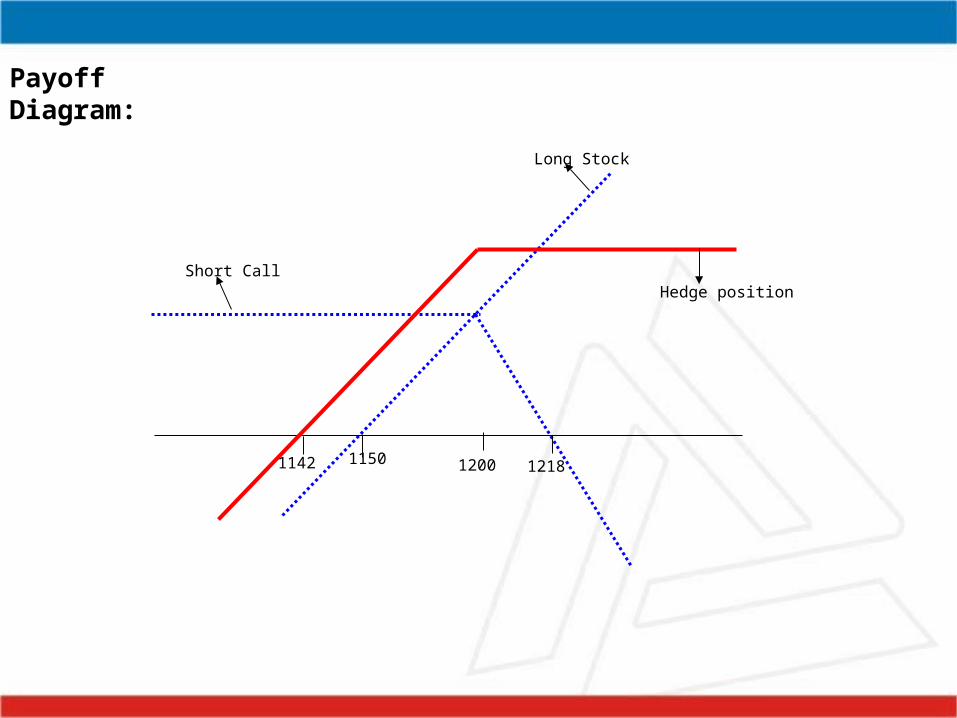

1150 1200

Short Call

Long Stock

Hedge position

1142 1218

Payoff Diagram:

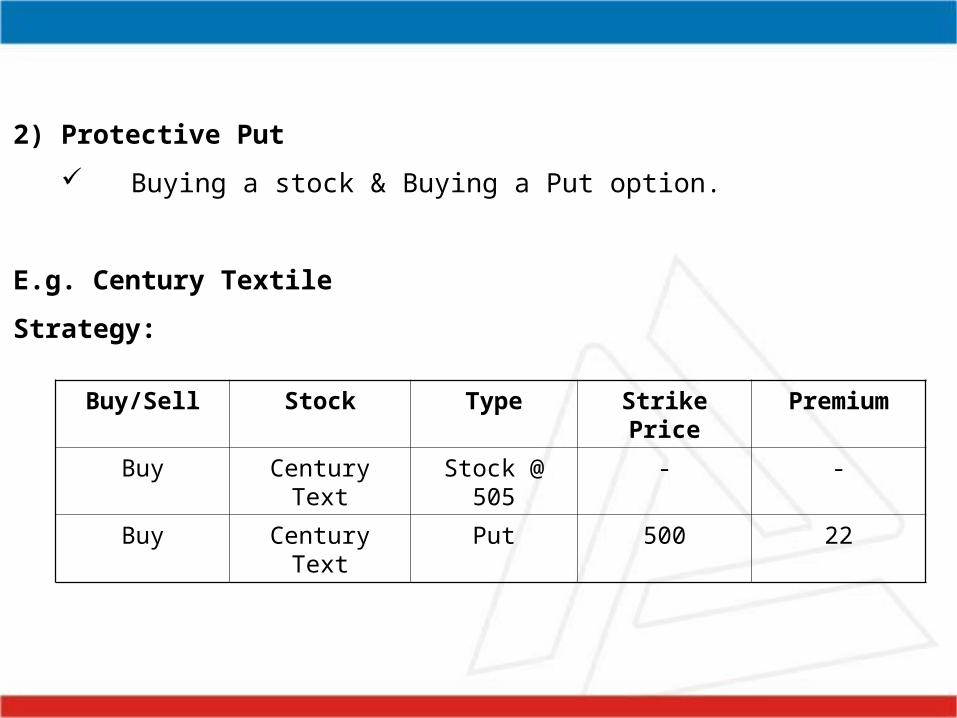

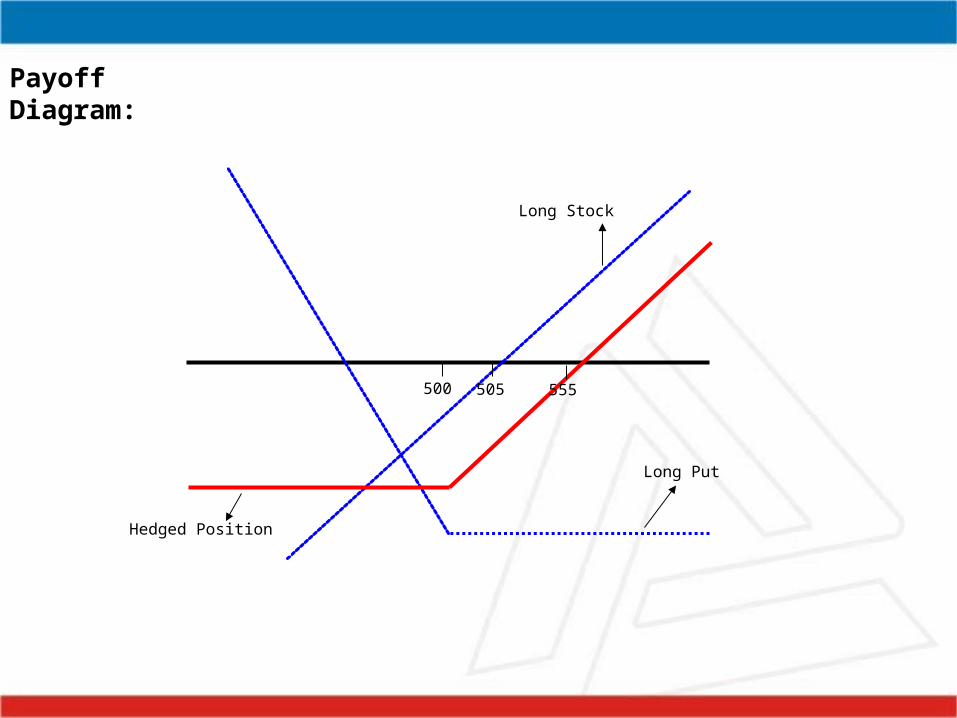

2) Protective Put

Buying a stock & Buying a Put option.

E.g. Century Textile

Strategy:

Buy/Sell Stock Type Strike Price Premium

Buy Century Text Stock @ 505 - -

Buy Century Text Put 500 22

Long Put

Long Stock

Hedged Position

505500 555

Payoff Diagram:

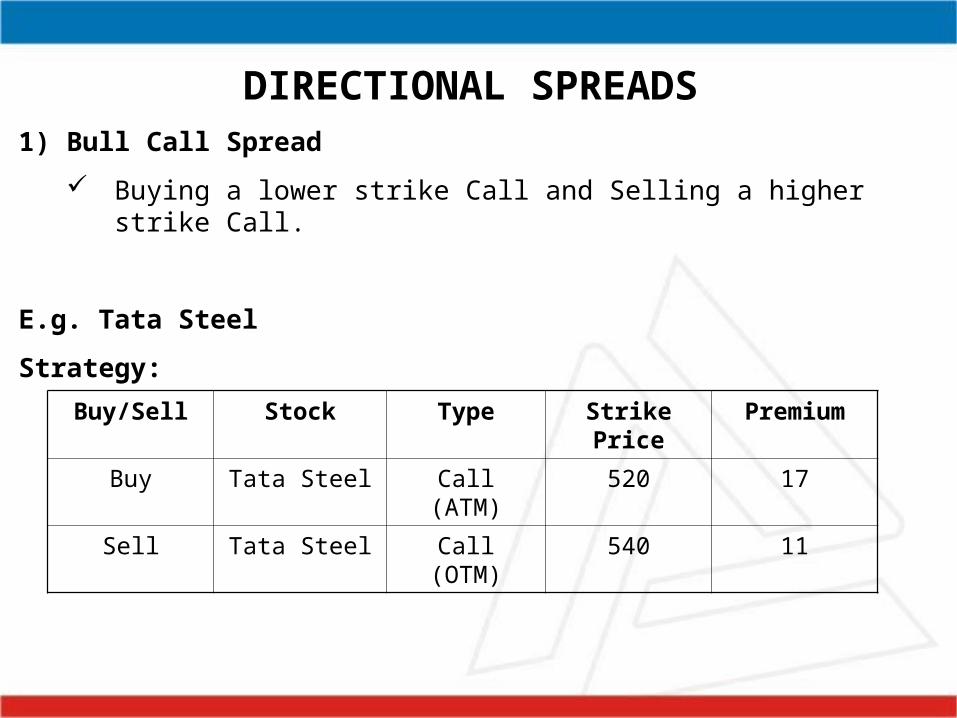

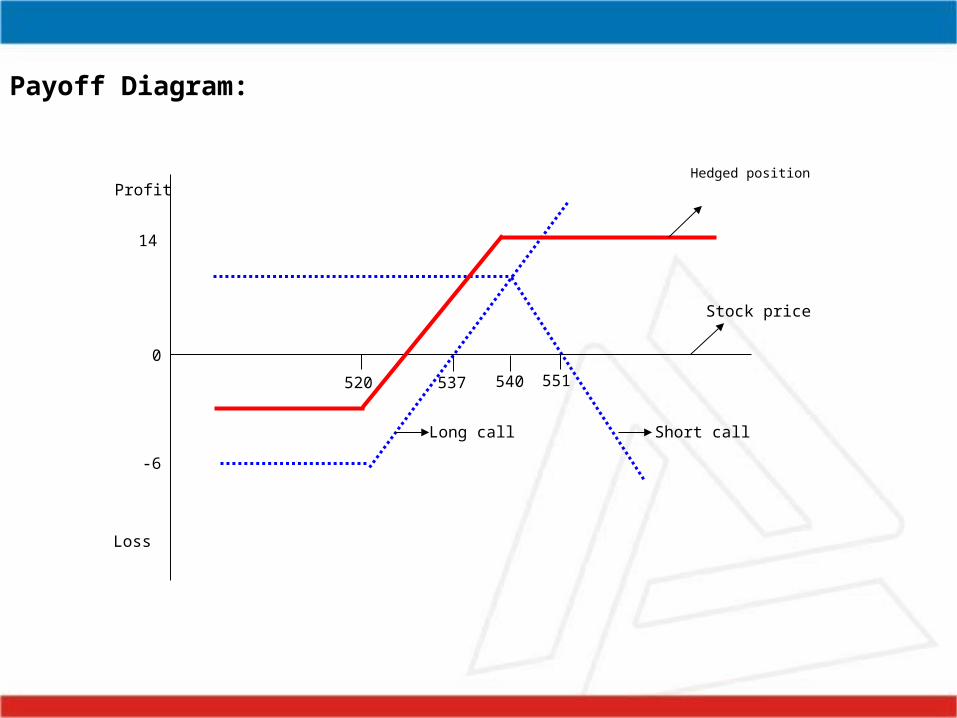

DIRECTIONAL SPREADS1) Bull Call Spread

Buying a lower strike Call and Selling a higher strike Call.

E.g. Tata Steel

Strategy:

Buy/Sell Stock Type Strike Price Premium

Buy Tata Steel Call (ATM) 520 17

Sell Tata Steel Call (OTM) 540 11

Payoff Diagram:

520 540 551537

Long call Short call

Hedged position

Stock price

Profit

Loss

0

14

-6

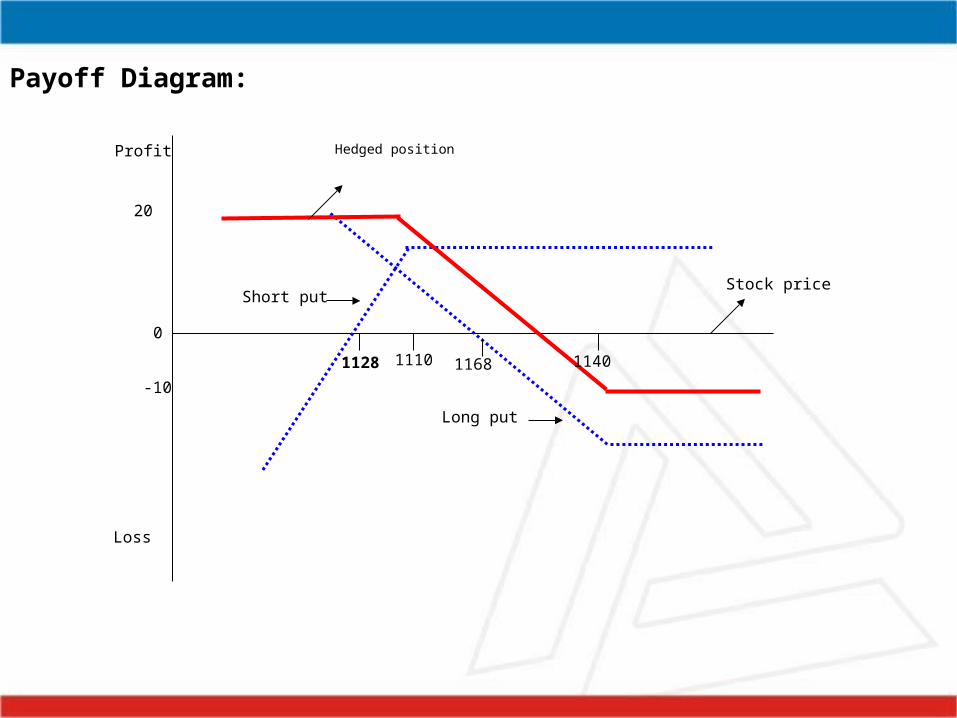

2) Bear Put Spread:

Buying a higher strike Put and Selling a lower strike Put.

E.g. ONGC

Strategy:

Buy/Sell Stock Type Strike Price Premium

Buy ONGC Put (ATM) 1140 28

Sell ONGC Put (OTM) 1110 18

Long put

Short put

Hedged position

Stock price

1128 1168 11401110

Profit

Loss

0

20

-10

Payoff Diagram:

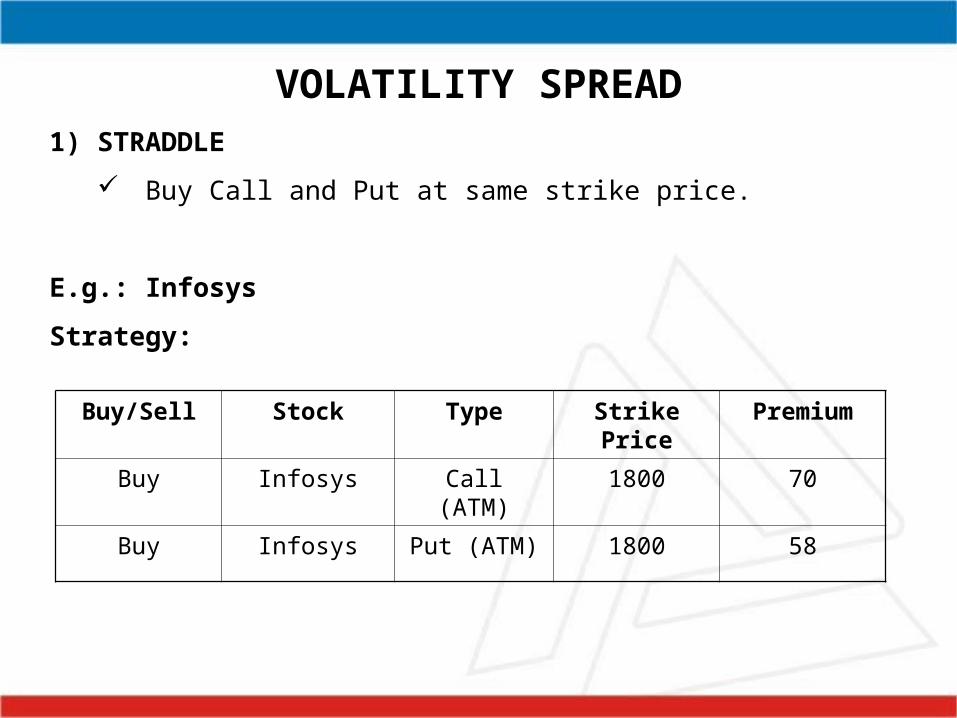

VOLATILITY SPREAD1) STRADDLE

Buy Call and Put at same strike price.

E.g.: Infosys

Strategy:

Buy/Sell Stock Type Strike Price Premium

Buy Infosys Call (ATM) 1800 70

Buy Infosys Put (ATM) 1800 58

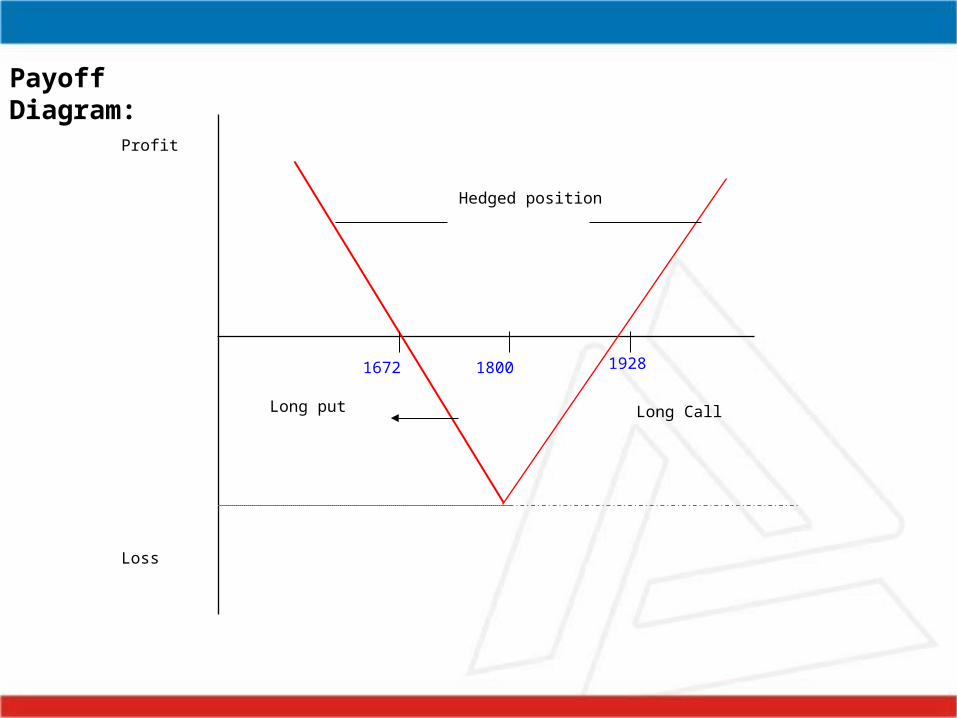

Payoff Diagram:

1672

Hedged position

Long CallLong put

Profit

Loss

1800 1928

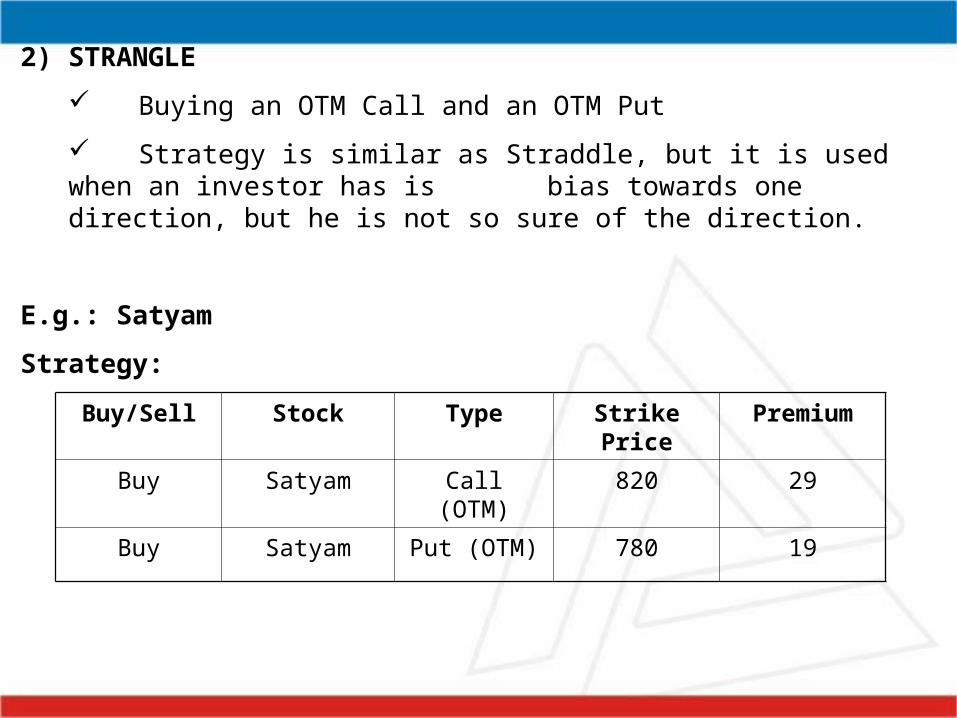

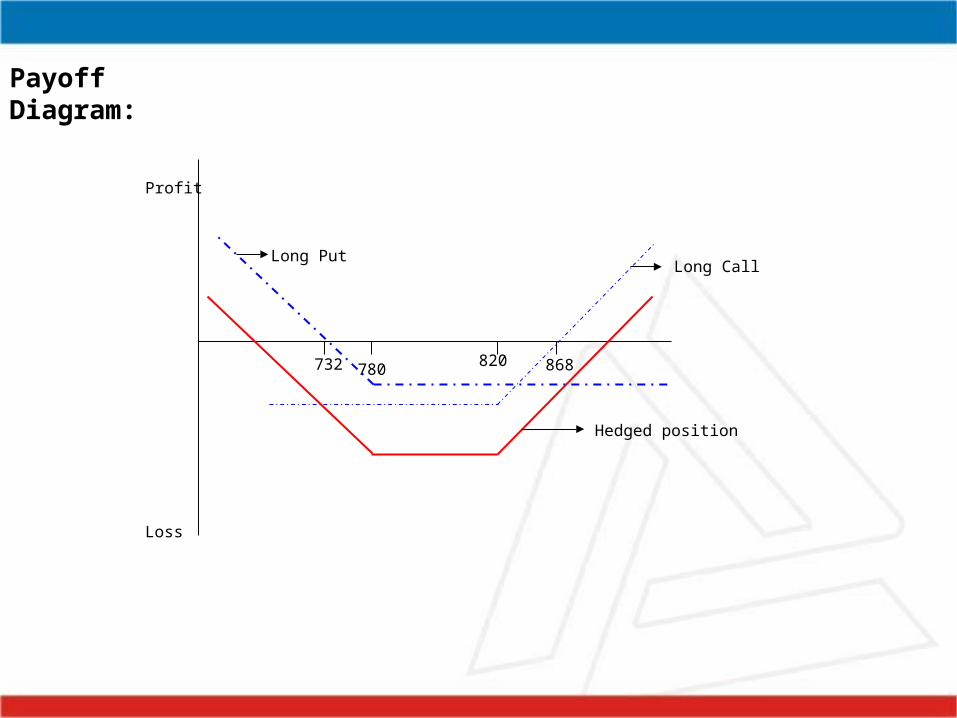

2) STRANGLE

Buying an OTM Call and an OTM Put

Strategy is similar as Straddle, but it is used when an investor has is bias towards one direction, but he is not so sure of the direction.

E.g.: Satyam

Strategy:

Buy/Sell Stock Type Strike Price Premium

Buy Satyam Call (OTM) 820 29

Buy Satyam Put (OTM) 780 19

Payoff Diagram:

780820 868732

Long PutLong Call

Hedged position

Profit

Loss

DERIVATIVES’ GREEKS

GREEKS:

• Greeks are statistical values that show the sensitivity of the price of an option to the factors that determine the value of an option.

• They can be used as indicators to help monitor and analyze the risks associated with portfolios which include options. Greeks include:

· Delta · Gamma · Vega · Theta · Rho

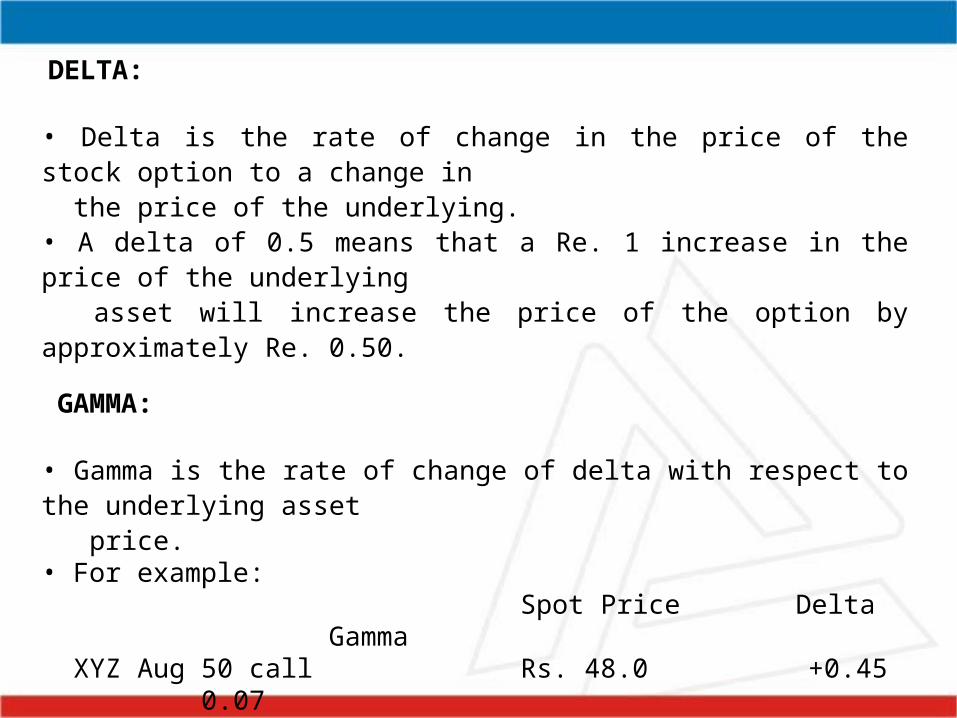

DELTA:

• Delta is the rate of change in the price of the stock option to a change in the price of the underlying.• A delta of 0.5 means that a Re. 1 increase in the price of the underlying asset will increase the price of the option by approximately Re. 0.50. GAMMA:

• Gamma is the rate of change of delta with respect to the underlying asset price. • For example:

Spot Price Delta Gamma XYZ Aug 50 call Rs. 48.0 +0.45 0.07 Rs. 49.0 +0.52

Rs. 47.0 +0.35• If gamma is small, delta changes slowly whereas if gamma is large delta is very sensitive to the price of the underlying

THETA:

• Theta is the rate of change of the value of the portfolio with respect to the passage of time.

• The theta of an option measures the unit change in the option price for a 1- day decrease in the days remaining to option.

• Theta is also referred to as time decay of an option. For a buyer of the option, this decay works against him while for a seller of the option it works in his favour.

VEGA: • Vega is also known as kappa or lambda. • Vega is the rate of change of the value of the portfolio with respect to the change in volatility. • A Vega of 0.12 indicates that an option’s value will increase/decrease by Re.

0.12 with every 1% increase/decrease in volatilityRHO:• Rho is the rate of change of the value of the portfolio with respect to the

interest rate.

DERIVATIVES REPORT

• DERISMART

• DERISTRAT

• DERIWATCH

• PAIR STARTEGY

• ROLLOVER ANALYSIS

MIB (Smart Net)

• Open Interest

• Put Call Ratio

• Implied Volatility

• Cash & Carry Arbitrage Opportunity

• Reverse Cash & Carry

• Bulletin Board

Thank You