Embed Size (px)

Citation preview

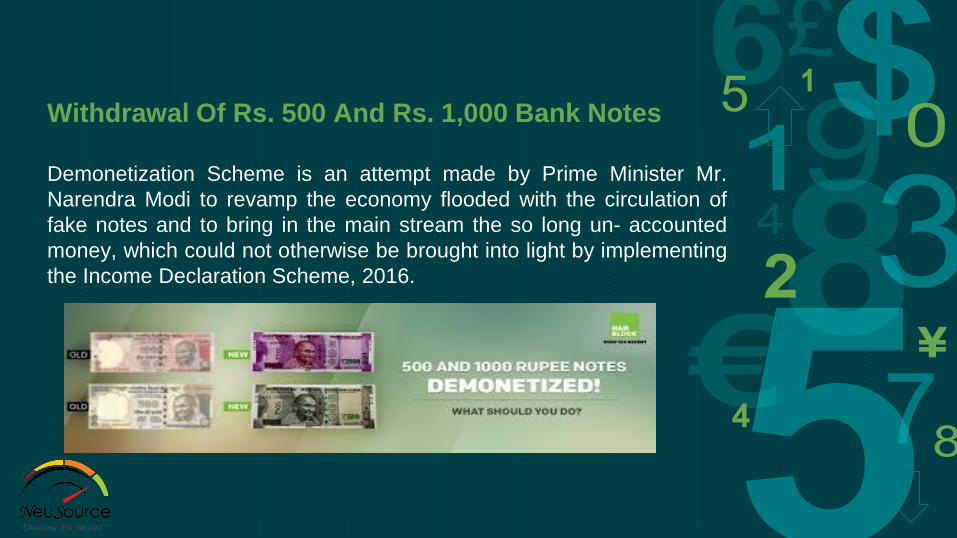

Withdrawal Of Rs. 500 And Rs. 1,000 Bank Notes

Demonetization Scheme is an attempt made by Prime Minister Mr.

Narendra Modi to revamp the economy flooded with the circulation of

fake notes and to bring in the main stream the so long un- accounted

money, which could not otherwise be brought into light by implementing

the Income Declaration Scheme, 2016.

Why Only Higher Denomination Notes?

With effect from midnight 8th Nov, 2016 (for selected areas from

midnight 11th Nov, 2016), Rs. 500 and Rs. 1,000 notes have ceased to

be legal tender. Since, incidence of fake Indian currency notes in higher

denomination has increased and as such High-denomination notes are

thought to be best way to keep unaccounted (black) money, ceasing the

legal character of such notes may prove to be infallible move to combat

such mal practices.

Cash Deposit-whether Any Threshold Or Not?

It cannot be denied that cash deposits over Rs. 2.5 Lakh will be brought

in the checking mechanism by the banks and tax department, but as of

now, there doesn’t exist any threshold for depositing cash in the bank

account.

The chief objective of the scheme is to bring into account the

unaccounted cash and also to promote transactions through banking

channels so as to develop a cashless economy. Thus, a person can

deposit as much cash as he holds in form of OHD notes in the bank

account, fulfilling the guidelines related to verification and KYC norms as

issued by RBI in consultation with the tax department.

What Exactly Bothers You? What You Are Afraid Of? What

You Wonder Of? Why Are You Rushing For Consultations

Prior To Depositing Cash? Why Are You Striving To

Locate Alternatives To Cash Deposit?

Since the time the OHD notes were illegal, the market is full of

unstoppable discussions, leading to a confusing situation which

somehow crashes the mind the common people. The issue touches its

heights when you are having huge amount of OHDs notes. Here, a

person like you wanders to find someone who can suggest you in the

best possible manner.

What Are You Afraid Of?

Depositing huge cash in the bank account will lead to investigation,

inquiries, etc. by the tax department which may also result in the

penalties, tax, etc.

If the cash has not been accounted for earlier, then, the

consequences may even be more drastic , and

Such many more queries.

Real Position And Consequences

One cannot deny the following:

⊸ Depositing cash exceeding Rs. 2.5 lakh (whether accounted or not)

will be reported by the banks to the Income Tax Department, which will

then be reflected on your income tax portal “Under compliance-

Account for cash transactions”

⊸ Depending upon the reply you furnish to the information to above, the

tax department will decide upon whether any further action is necessary

or not

⊸ If an action is considered to be necessary by the department, then,

you may be subjected to inquiries requiring your personal presence and

presentation of documents before the tax officials, assessment of income

and such related results.

But the real question is that whether you really

need to be worried of above results and if yes, then

to what extent, legal position of such actions by the

department and most importantly, the tax and

penalties which you may be subjected to, we thus

produce herewith some of the facts which have a

legal premise which may prove to be a full or partial

solution to these grapevine-structured queries

In Case The Cash Deposit Had Duly Been Returned I.E.

Shown In The Income Tax Return For Earlier Year(s)

Which Is Termed As Accounted Money

If the amount credited in pursuant to this scheme matches with your

income tax return filed for earlier year(s), then, you are saved from the

undesirable action by the department in this scheme. However, if those

returns have any discrepancies or omissions, then, they may be

subjected to assessments otherwise.

In Case The Cash Deposit Had Not Duly Been Returned

I.E. Not Shown In The Income Tax Return For Earlier

Year(s):

If the credited amount had not been shown in the return for previous

years, then, the same may be accounted for in the return for the current

year i.e. F.Y. 2016-17 for which return is due to be filed by 31st July,

2017 (30th Sep in some cases), disclosing the source of income in an

appropriate manner and discharging the tax liabilities (if any) at your end.

However, the source of income should be justifiable as there are bigger

chances of the return being brought into the scrutiny.

Now, the legal premise in this case is explained on Next Slides

Provisions Which You Should Be Knowing (Which May

Prove An Expected Tax Planning To Be Unlawful)

Section 68 & Section 115BBE As per this section, if the Tax official finds any amount being credited in

your books/return, then, he may ask for explaining the nature and

source of income.

Now, whether the explanation regarding nature and source is

satisfactory or not, depends upon the opinion of such officer. For

example, if the person produces before the officer, establishes the

identity of the person from whom the amount had been received and

also assigns such amount a valid nature, then, the explanation may

seem to be satisfactory. However, the official is free to ask the other

person to explain the source in his hand.

Section 68 & Section 115BBE

If, in the above cases, when either of the persons are not able to furnish

satisfactory explanations about the nature and source of amount, so

much of the amount being unexplained shall be deemed to be the

income of such person.

Also, as per section 115BBE, such income shall be taxable at flat rate

of 30% (plus surcharge if any and cess) i.e. no deduction of any expense

or deduction or allowance of loss will be allowed against such deemed

income. Also, no benefit of exemption limit shall be allowed to any

person for such income.

Section 269SS & 269T

Now, in order to convert the unaccounted money into legible one, one

may think of showing the credited money as “Loans or advances

received or repaid in cash”. So, it is important to have a look on the

following provisions:

As per section 269SS, no person can accept any loan or deposit from

any other person by any mode other than account payee cheque or by

use of electronic clearing system through a bank account if the amount

accepted, in aggregate from such person, is Rs. 20,000 or more. This

means if loan is received whether full or in parts of below Rs. 20,000 in

cash, then, also it is against the legal provisions.

Section 269SS & 269T

Also as per Section 269T, nor person can repay any loan or deposit by

any mode other than account payee cheque or by use of electronic

clearing system through a bank account if the amount of such loan or

deposit (together with interest) is Rs. 20,000 or more. This means that

repayment of loan in cash which amounts to Rs. 20,000 or more , either

made at once or in parts, is against the law.

If a person contravenes any of the above sections, then, a penalty

of sum equivalent to such loan accepted or repaid shall be imposed

by the tax official. However, if reasonable justification is provided for

accepting or repaying loan in cash above the threshold, then, the penalty

may not be imposed.

Section 143(3)

If the return is selected for scrutiny, then, the tax official shall pass an

assessment order under section 143(3) determining the amount of tax

payable (along with interest if any).

But before passing order under this section, a notice shall be issued

under section 143(2) either to present before the tax official or to

produce the evidence in support of the return. However, this notice

cannot be issued if the return has not been filed.

Also, time limit for issuing notice under this section is 6 months from the

end of the financial year in which the return is filed.

Section 147 & 148

The provisions of this section may also get attracted if the tax official

believes that for any year, the income has been escaped from

assessment.

Action under this section can be taken till the end of four years from the

end of relevant assessment year. But if the return has not been filed or

the person doesn’t disclose all the material facts fully and truly, then, the

limitation of four years doesn’t apply.

Notice under section 148 shall be first issued for initiating assessment

under this section.

Penalty And Prosecution Resulting From Tax Evasion

Section 270A Now, with a view to prevent from the actions by the tax department, one

may account for the deposited amount in the return for current year

ending on 31st March, 2017.

However, penalty may be imposed in case the income is found to have

been under-reported.

What Is Under-reporting Of Income?

Under-reporting of income shall arise if:

If return has been filed, then, income assessed by the tax official is more

than what has been processed under section 143(1) by CPC, or

If no return has been filed, then, the income was indeed taxable

In the above cases, the, under-reported will be that income which has

not been shown in the return.

However, The Following Shall Not Be Termed As

Under-reported Income:

If the person offers explanation before the tax official which is

satisfactory in his opinion and also presents all the material facts to

substantiate the explanation

Any estimate of income by official, if the accounts are correct and

complete, but the income from accounts cannot be figured out

properly

Any estimate of income by official, if the person has himself on the

basis of material facts made a lower addition

Income on which penalty is imposable by way of search initiated by

the department.

How Much Penalty Can Be Imposed?

⋅50% of tax payable on under-reported income, or

⋅200% of tax payable on under-reported income if under-reporting is due

to misreporting.

Now, what is misreporting of income:

⊸ misrepresentation or suppression of facts

⊸ failure to record investments in the books of account

⊸ claim of expenditure not substantiated by any evidence

⊸ recording of any false entry in the books of account

⊸ failure to record any receipt in books of account having a bearing on

total income

⊸ failure to report any international transaction or any transaction

deemed to be an international transaction or any specified domestic

transaction.

F.Y. 2016-17

The provisions of this section shall apply for years commencing from

F.Y. 2016-17.

Tax payable in this case shall be computed as under:

⊸ Tax payable on such income as if it were the total income in case of

company, firm or local authority; and

⊸ At the rate of 30% of under reported income, in any other case.

Section 271(1)(c)

Now, if the return filed for this year is brought into the net of scrutiny, then, it

may be possible that the tax official claim that such income or any part of

such income pertains to any preceding year and the same had not been

disclosed earlier. In that case, the penalty proceedings if any will be initiated

under section 271(1)(c).

According to this, if the person:

⊸ has concealed the particulars of income, or

⊸ has furnished inaccurate information of such income

then, he shall be liable to a penalty which can be maximum up to 300% of the

tax payable on such concealed income.

However, if the person offers a satisfactory explanation and also produce

material facts to substantiate such explanation, then, no income can be

claimed to have concealed.

Section 275

However, no order of penalty shall be passed under above sections if the

period, later of the following has expired:

⊸ After the expiry of 6 months from the end of the month in which action

for imposition of penalty is initiated , or

⊸ After the expiry of financial year in which the penalty proceedings are

completed and such financial year being that year in which action for

imposition of penalty has been initiated.

Section 271A

In addition to penalties imposable under above sections, the person may

also be liable to a penalty of Rs. 25,000 if he fails to keep and maintain

the books of accounts and other documents in the prescribed manner.

Section 276C

If a person wilfully evades any tax, etc. under this act, then, apart from

any other proceedings which may be imposed (i.e. discussed above), he

shall also be punishable with:

⊸ In a case where the amount evaded exceeds Rs. 25 Lakh, with

rigorous imprisonment for a term which shall not be less than six months

but which may extend to seven years and with fine, or

⊸ In any other case, with rigorous imprisonment for a term which shall

not be less than three months but which may extend to two years and

with fine.

Section 276CC

If a person wilfully fails to furnish return in due time, then he shall be

punishable with:

⊸ In a case where the amount evaded exceeds Rs. 25 Lakh, with

rigorous imprisonment for a term which shall not be less than six months

but which may extend to seven years and with fine, or

⊸ In any other case (amount of tax is Rs. 3,000 or more), with rigorous

imprisonment for a term which shall not be less than three months but

which may extend to two years and with fine.

Section 277A

Now, in the course of finding for alternatives for safe cash deposit, one

may rely upon the aid of any other person who helps the first person to

evade any tax or interest or penalty under Income Tax Act.

It is important to note here that if it is proved that the second person

done such an act, then, he may punishable with rigorous imprisonment

for a term which shall not be less than three months but which may

extend to two years and with fine.

So, the above discussion may prove to be useful

and you may have an introductory knowledge about

the possible repercussions. This may also guide

you about an action to be taken which happens to

be the most feasible and appropriate one.

Lastly, one should also be aware of the fact that in all the above

cases, there shall be reflected on the income tax portal of the person

with whose PAN the bank account has been linked, a summary of

cash transactions and that person will have to submit an online

response by opting for any of the options as under:

transactions are considered to be in ITR

transactions are considered in ITR of another account holder

transactions are not considered for ITR

transactions are partly considered for ITR

transactions are not taxable or exempt (e.g. agricultural income)

transactions do not have a relation with this account

The above response should be genuine as it will, to an extent, lay

down basis for probable action the tax officials.

THANKS!

CA Hemant Gupta

+91-9540003545

www.neusourceindia.com

Click for Fix A Meeting