Embed Size (px)

Citation preview

Group 13

Sahith an Krishna

Vaashanthiha

Shraddha

Nikhil

Saurav

TERM LOANS

Definition

• In finance a loan is a debt provided by one entity (organization or individual) to another entity at an interest rate, evidenced by a note, which specifies, among other things, the principal amount, rate of interest and date of repayment.

• A term loan is a monetary loan that is repaid in regular repayments over a set period of time.

PURPOSE OF TERM LOANS

Capital Expenditure

New Industrial

Undertaking

Expansion

of

Existing One

Acquisition

of

Movable Assets

PROCEDURES ASSOCIATED WITH TERM

LOANS

• Submission of Loan Application

• Initial Processing of Loan Application

• Appraisal of the Proposed Project

• Issue of Letter of Sanction

• Acceptance of T&Cs

• Execution of Loan Agreement

• Creation of Security

• Disbursement of Loans

• Monitoring

DIFFERENT TYPES OF TERM LOAN

• Long term loans

• Intermediate term loans

• Short term loans

Short term:

• Require repayment in one year or less (On average: between 90 to

120 days)

• Small businesses are more likely to utilize short term loans.

Long term:

• Long term business loans, on average, last from 3-10 years

• Generally, these loans finance assets that are being capitalized

FEATURES OF TERM LOANS

• Currency- Financial Institutions provide both rupee as well as foreign currency term loans.

• Maturity- The maturity period of term loans is typically longer in case of sanctions by financial institutions in the range of 6-10 years in comparison to 3-5 years of bank advances.

• Negotiated- The term loans are negotiated loans between the borrowers and the lender.

• Security- Term loans typically represent secured borrowing

• Interest Payment and Principal Repayment- These are definite obligations that are payable irrespective of the financial situation of the firm

• Restrictive Covenants- In order to protect their interests, FIs impose restrictive conditions on borrowers such as imposing a penalty for defaults.

• Covenants are categorized as : asset related covenats,liability related covenants,cash flow related covenants.

Repayment Schedule

• Term loans by F.I.s are generally repayable in equal semi-annual, quarterly or annual installments

• The interest burden may decline over time but the principal repayment may remain the same

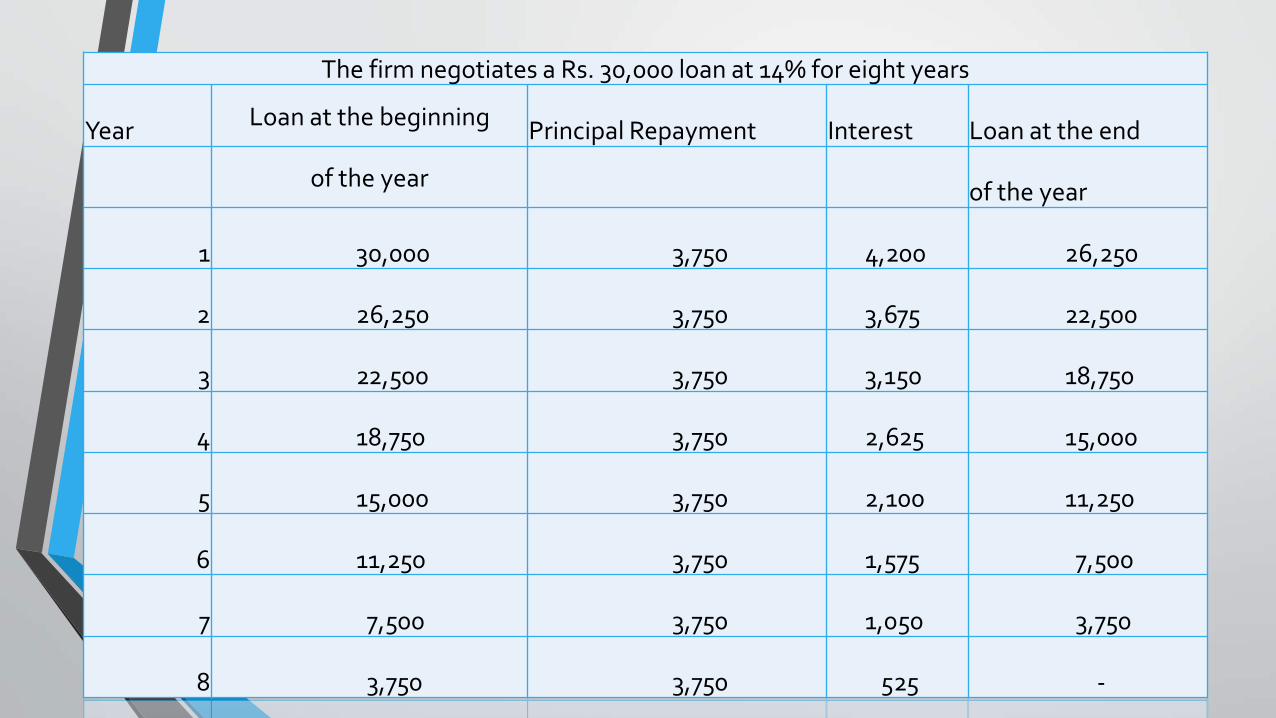

The firm negotiates a Rs. 30,000 loan at 14% for eight years

YearLoan at the beginning

Principal Repayment Interest Loan at the end

of the yearof the year

1 30,000 3,750 4,200 26,250

2 26,250 3,750 3,675 22,500

3 22,500 3,750 3,150 18,750

4 18,750 3,750 2,625 15,000

5 15,000 3,750 2,100 11,250

6 11,250 3,750 1,575 7,500

7 7,500 3,750 1,050 3,750

8 3,750 3,750 525 -

Debentures and Bonds

Contents

•Definition

• Issue of Debentures

• Types

• Features

• Valuation of Debentures

DEBENTURES - Definition

• A debenture is a certificate of loan or a loan bond evidencing the fact that the company is liable to pay a specified amount with interest.

• Issue of a certificate

• Under its seal - Acknowledgment of debt taken by the company.

• Although the money raised by the debentures becomes a part of the company's capital structure, it does not become share capital.

Issue of Debentures

• The procedure of issue of debentures is similar to that of the issue of shares.

• A Prospectus is issued >> applications are invited >> letters of allotment are issued.

• On rejection of applications, application money is refunded. In case of partial allotment, excess application money may be adjusted towards subsequent calls

Issue of Debentures• Issue of Debenture takes various forms which are as under :

1. For cash

2. For consideration other than cash

3. As collateral security.

• Further debentures may be issued at

1. Par

2. Premium

3. Discount

Types

Non Convertible Debentures

These instruments retain the debt character and cannot be converted into equity shares.

Partly Convertible Debentures

A part of these instruments are converted into Equity shares in the future at notice of the issuer. The issuer decides the ratio for conversion. This is normally decided at the time of subscription

Fully convertible Debentures

These are fully convertible into Equity shares at the issuer's notice. The ratio of conversion is decided by the issuer. Upon conversion the investors enjoy the same status as ordinary shareholders of the company.

Types -

Secured DebenturesThese instruments are secured by a charge on the fixed assets of the issuer company. So if the issuer fails on payment of either the principal or interest amount, his assets can be sold to repay the liability to the investors.

Unsecured Debentures

These instrument are unsecured in the sense that if the issuer defaults on payment of the interest or principal amount, the investor has to be along with other unsecured creditors of the company.

Types - Security

Redeemable Debentures

Issued for a fixed period.

The principal amount is paid off to the debenture holders on the expiry of such period.

These can be redeemed by annual drawings or by purchasing from the open market.

Irredeemable Debentures

Not redeemed in the life time of the company.

Paid back only when the company goes into liquidation.

Types -

Redemption

Redemption of debentures can be accomplished either through

• Sinking fund – It is a cash set aside periodically for retiring debentures.

• Buy-back (call) provision – Buy-back provision enable the company to redeem debentures at a specific price before the maturity date.

FEATURES• Face value : For stocks, it is the original cost of the stock shown on the

certificate. For bonds, it is the amount paid to the holder at maturity.

• Coupon rate : The interest rate stated on a bond when it is issued. The coupon is typically paid semi annually.

• Maturity : The tenure of redeemable debentures.

• Tax Benefit: Most important element from the company point of view is that the interest paid is a tax deductible expense. Effectively, the company will get the tax benefit because the taxable income will be reduced by the extent of interest paid. Due to this the effective cost of borrowing gets reduced.

FEATURES

• Credit Rating: Normally, an investor would not go and check the credibility and the risk involved with the debentures. Credit rating agencies are given this task and they rate the debentures and the overall company. Involving a rating agency is compulsory for the issuing company normally in every country.

• Charge on Assets and Profits in case of Default: The debenture holders may have claims over the profits and assets of the company in case the company has defaulted in the payment of either the interest or the capital repayment.

Indenture

An Indenture or Debenture trust deed is a legal agreement between the company issuing debentures and the debenture trustee who represent the debenture holders.

DIFFERENCE BETWEEN BONDS AND DEBENTURES

Both bonds and debentures are instruments available to a company to raise money from the public.

DEBENTURES BONDS

Issued by Companies Generally issued by Government,

Corporations

Not secured by physical assets or collateral Secured

Higher Interest rate Low interest rate when compared to

Debentures

Types of Bonds / Debentures• Bond with maturity

The government and company mostly issued bond that specify the interest rate (coupon rate) with maturity period.

• Pure discount bonds or Zero Coupon bonds

This is a type of bond that makes no coupon payments but instead is issued at a considerable discount to par value

It do not carry an explicit rate of interest. It provides for the payment of a lump sum amount at a maturity date

For example, let's say a zero-coupon bond with a Rs. 1,000 par value and 10 years to maturity is trading at Rs. 600; you'd be paying $600 today for a bond that will be worth Rs. 1,000 in 10 years.

Valuation of Bonds / Debentures

Present value approach

i = contractual interest rate / Coupon rateC = F * i = coupon payment (periodic interest payment)N = number of paymentsi = market interest rate, or required yieldM = value at maturity, usually equals face value

PV of future interest payments PV of maturity value

APPLICATION

ALLOTMENT

CALLS

Thank You CLASS