Embed Size (px)

Citation preview

Tara Raissa (29014003)

Indriani Rustomo (29014009)

CORPORATE RESTRUCTURING: MERGERS, LBOs, AND DIVESTITURESBrigham-Gapenski Mini Case

Introduction

Case

M&A Decision

M&A in Indonesia: XL & Axis

Outline

The Compumax Company, a regional computer retailer. Due to rich in cash, they consider acquisition as one of the possible uses for the excess funds. A company that may be acquired is Pacific Computer Products Inc., a small mail order hardware and software company that sells nationwide. Pacific’s estimated cash flow (in million dollars)

Introduction

1996 1997 1998 1999

Net Sales $10.0 $20.0 $25.0 $30.0

Cost of goods sold 6.0 12.0 15.0 18.0

Selling/administrative expenses 1.0 1.5 2.0 2.0

Depreciation 2.0 4.0 5.0 6.0

Interest expense 0.5 1.0 1.2 1.5

Cash flow plow-back 1.0 2.5 3.0 4.0

Interest expense

Interest on Pacific’s existing debt

Interest on new debt that CompuMax would issue to help finance the acquisition

Interest on new debt expected to be issued over time to help finance expansion within the Pacific division

Other data

Debt ratio 20.0% Tax rate on consolidated firm

40%

Tax rate 30% Risk-free rate 10.0%

Beta coefficient 1.5 Market Risk Premium

5.0%

Debt ratio after acquisition

50% Growth of cash flow stream after 1999

7%

Among tax considerations, diversification, control, purchase of assets at below replacement cost, breakup value, and synergy, which of the reasons are economically justifiable? And which are not?

Synergy and break-up value are economy justifiable for mergers

Synergy. Because with merger & acquisition, Compumax company can increase their power in the market. And, they can also increase the value from:

Operating economies

Financial economies

Differential management efficiency

Taxes

Break-up value.Assets of Pacific Computer Products Inc. would be more valuable if the company broken up and sold to other companies.

The Case

Below are questionable reasons for mergers

Diversification

Purchase of assets at below replacement cost

Acquire other firms to increase size, thus making it more difficult to be acquired

Synergy and control might be fit as the reasons for the merger of Compumax & Pacific Computer Products Inc.

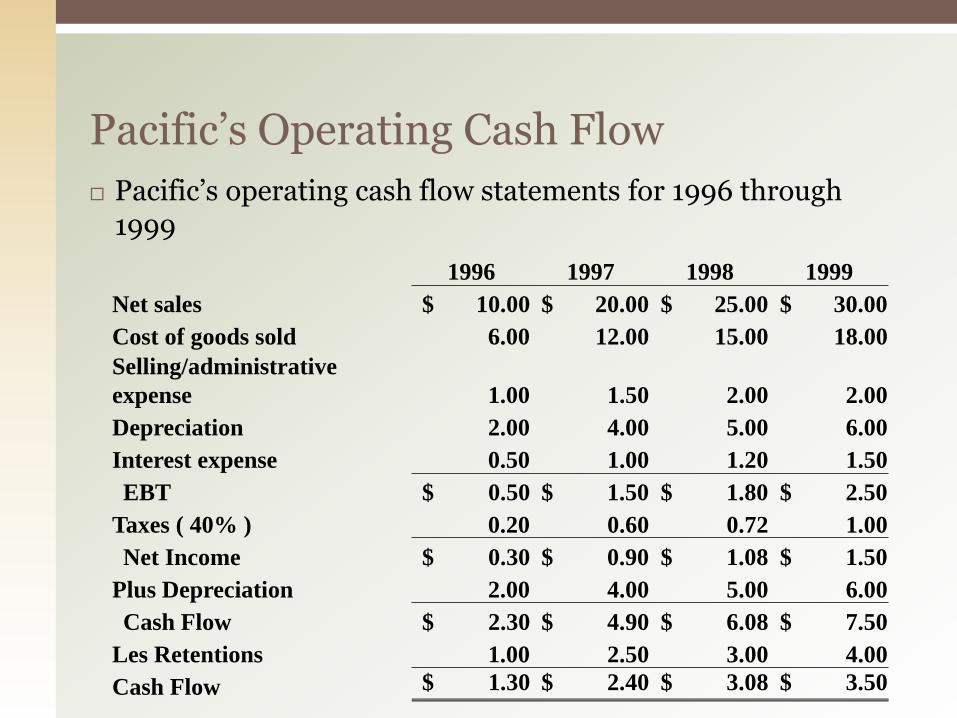

Pacific’s operating cash flow statements for 1996 through 1999

Pacific’s Operating Cash Flow

1996 1997 1998 1999

Net sales $ 10.00 $ 20.00 $ 25.00 $ 30.00

Cost of goods sold 6.00 12.00 15.00 18.00

Selling/administrative

expense 1.00 1.50 2.00 2.00

Depreciation 2.00 4.00 5.00 6.00

Interest expense 0.50 1.00 1.20 1.50

EBT $ 0.50 $ 1.50 $ 1.80 $ 2.50

Taxes ( 40% ) 0.20 0.60 0.72 1.00

Net Income $ 0.30 $ 0.90 $ 1.08 $ 1.50

Plus Depreciation 2.00 4.00 5.00 6.00

Cash Flow $ 2.30 $ 4.90 $ 6.08 $ 7.50

Les Retentions 1.00 2.50 3.00 4.00

Cash Flow $ 1.30 $ 2.40 $ 3.08 $ 3.50

Interest expense deducted in merger cash flow statements because estimated cash flows are residuals that belong to the shareholders of the acquiring firm. Including fixed interest charges increases the volatility.

Because the cash flows are equity flows, they should be discounted using a cost of equity rather than overall cost of capital.

Interest Expense & Discount rate

Cost of capital𝑘𝑠(Target) = 𝑘𝑅𝐹 + 𝑘𝑀 − 𝑘𝑅𝐹 𝑏Target

𝑘𝑠(Target) = 10%+ (10% − 5%) x 1.5 = 17.5%

Unlevered 𝑏 calculation

𝑏𝑈 =𝑏𝐿

1 + (1 − 𝑇)(𝐷/𝐸)=

1.5

1 + (1 − 0.3)(0.2)= 1.32

Levered 𝑏 after merger𝑏𝐿(new 50% debt ratio) = 𝑏𝑈 1 + (1 − 𝑇) 𝐷/𝐸= 1.32 1 + (1 − 0.4)(0.5) = 1.32 1.3 = 1.716

Cost of equity of target firm after the merger𝑘𝑠 = 𝑘𝑅𝐹 + 𝑅𝑃𝑀 × 𝑏𝐿 = 10% + 5% × 1.716 = 18.58%

Terminal value

TV =FCF𝑁(1 + 𝑔)

𝑘𝑠 − 𝑔=3.5(1 + 0.07)

18.58% − 7%= $32.34M

The value of Pacific

Net CF to Compumax =CF1

(1 + 𝑘𝑠)1+

CF2(1 + 𝑘𝑠)

2+

CF3(1 + 𝑘𝑠)

3

+TV

(1 + 𝑘𝑠)4

=1.3

(1.1858)1+

2.4

(1.1858)2+

3.08

(1.1858)3+

35.84

(1.1858)4= $21.41M

If another firm were evaluating Pacific as an acquisition candidate, they might not obtain the same value, since the discount rate and forecast they use might be different.

Terminal Value

If Pacific currently has 10 million shares outstanding, with last price $1.00 per share. Then, the market value of Pacific is

V𝑀 = shares outstanding × price = 10,000,000 × $1= $10,000,000

From our last calculation, the value of Pacific is $21.41M, which is greater than the market value of Pacific.

Compumax can offer bid to Pacific at minimum price $1 per share, which is the same as market price. Compumax can also offer higher bid than the market price, with maximum price $2.141 per share.

Bid Price

If mergers create value, the value would be shared to the parties involved. The stockholders of target firm would gain value from the difference between market value and the merger value. And acquiring firm would gain value from the difference between merger value and firm valuation.

Some merger-related activities undertaken by investment bankers

Arranging mergers

Developing defensive tactics

Establishing a fair value

Financing mergers

Raise financing for companies

Mergers

PT XL Axiata Tbk. is one of the major cellular providers in Indonesia. PT XL Axiata Tbk. is 66.5% owned by Axiata Group Berhad through Axiata Investments (Indonesia) SdnBhd and public 33.5%, and is part of Axiata

PT Axis Telekom Indonesia, owned by Saudi Telecom Company.

The acquisition done by entering into a conditional sale and purchase agreement (CSPA) with Saudi Telecom Company (STC) and Teleglobal Investments B.V. (Teleglobal), a subsidiary of STC.

The acquisition announced on September 26 2013 and completed on March 19 2014.

XL Axiata Acquisition on Axis Telekom

Teleglobal will sell (or procure the sale of) a 95% equity stake in AXIS to XL

AXIS is valued at 100% enterprise value of USD 865 million, on a cash free and debt free basis.

The purchase consideration will be utilized towards payment of a nominal value for AXIS equity and redemption of AXIS' indebtedness.

The completion of the transaction is subject to

All applicable regulatory approvals

XL shareholders’ approval at an Extraordinary General Meeting of Shareholders

Spectrum retention

Conditional Sale And Purchase Agreement

Over 65 million customers will immediately benefit from the superior quality of service and wider coverage

Consolidates the industry further and paves the way for more prudent, growth focused expansion with a more efficient capex profile

Supports the government’s national broadband objective

Addresses XL’s current challenges - Provides additional spectrum capacity to XL, subject to regulatory approvals, leading to: Significantly enhanced quality of service and network experience on both

2G and 3G Enhanced asset utilization, particularly on XL's towers and network

equipment, with tangible reduction in capex and opex spends

Further reinforces XL’s leadership position, with sizeable business operations and scale Larger subscriber base and on-net community Stronger and more effective data focus and traction amongst the youth

segment Complementary businesses with multiple areas of revenue and

cost synergies

Key Rationale

XL Stock Price during Acquisition