Embed Size (px)

Citation preview

1

Financial Planning and Growth

Lecture 3: January 11, 2012

2

Objectives

We will first learn how to use spreadsheets to develop a financial

model that allows us to forecast future funding needs.

We will then make some simplifying assumptions to obtain useful

formulas that allow us to get a feel for what may happen without

doing the detailed financial modeling exercise.

3

Variables definition: based on accounting data for year t

𝐴= total assets (from balance sheet at the end of year t)

𝐷 = total debt (from balance sheet at the end of year t)

𝐸 = total equity (from balance sheet at the end of year t)

𝑁𝑁 = net income (from income statement for year t)

𝑟 = retention ratio =∆ 𝑅𝑅𝑅𝑅𝑅𝑅𝑅𝑅 𝐸𝑅𝐸𝑅𝑅𝑅𝐸𝐸𝑁𝑅𝑅 𝐼𝑅𝐼𝐼𝐼𝑅

=1 − 𝑃𝑃𝑃𝑃𝑃𝑃 𝑟𝑃𝑃𝑟𝑃 = 1 − 𝑑

𝑅𝑅𝐴 = return on assets = 𝑁𝑅𝑅 𝐼𝑅𝐼𝐼𝐼𝑅𝑇𝐼𝑅𝑅𝑇 𝐴𝐸𝐸𝑅𝑅𝐸

𝑅𝑅𝐸 = return on equity = 𝑁𝑅𝑅 𝐼𝑅𝐼𝐼𝐼𝑅𝑇𝐼𝑅𝑅𝑇 𝐸𝐸𝐸𝑅𝑅𝐸

𝑔 = projected sales growth rate (from year t to year t+1)

4

Formal calculation of External Fund Needs (EFN)

Increase in assets =𝐴 ∗ 𝑔 Addition to 𝑅𝐸 = 𝑁𝑁 ∗ 1 + 𝑔 ∗ 𝑟 𝐸𝐸𝑁 = 𝑁𝐼𝐼𝑟𝐼𝑃𝐼𝐼 𝑟𝐼 𝑃𝐼𝐼𝐼𝑃𝐼 − 𝐴𝑑𝑑𝑟𝑃𝑟𝑃𝐼 𝑃𝑃 𝑅𝐸 (∆𝐶𝐶 = 0) 𝐸𝐸𝑁 = 𝐴 ∗ 𝑔 − 𝑁𝑁 ∗ 1 + 𝑔 ∗ 𝑟 = 𝐴 –𝑁𝑁 ∗ 𝑟 𝑔 − 𝑁𝑁 ∗ 𝑟

What is the slope and what is the intercept?

Slope: [𝐴 – 𝑁𝑁 ∗ 𝑟 ] ; Intercept: − 𝑁𝑁 ∗ 𝑟

What are their signs? Slope is + ; Intercept is -

5

EFN & Planned Growth Rate

What happens when g = 0? EFN = -Addition to RE in last year (surplus not invested in assets)

𝑔

𝐸𝐸𝑁

-NI*r

6

The Internal Growth Rate Internal Growth Rate 𝒈𝒊: the rate of growth that can be

supported with no external financing, i.e. EFN = 0.

𝐴 − 𝑁𝑁 ∗ 𝑟 𝑔𝑟 − 𝑁𝑁 ∗ 𝑟 = 0

Solving yields 𝑔𝑟 = 𝑁𝐼∗𝐸[𝐴−𝑁𝐼∗𝐸]

Divide by A & recall 𝑅𝑅𝐴 = 𝑁𝐼𝐴

Then 𝒈𝒊 = 𝑹𝑹𝑹∗ 𝒓(𝟏 – 𝑹𝑹𝑹 ∗ 𝒓)

Make sure you can derive it on your own!

7

The Internal Growth Rate Recall that: 𝒈𝒊 = 𝑹𝑹𝑹∗ 𝒓

(𝟏 – 𝑹𝑹𝑹 ∗ 𝒓)

What happens with gi if the retention ratio (r) increases or equivalently the dividend payout ratio (d) decreases?

Increases! What happens with gi if ROA increases? Increases! Suppose a firm is growing at gi each year. How is the firm’s

debt-to-equity ratio evolving over time? Decreasing!

Is this trend in the debt-to-equity ratio desirable? It depends!

8

Towards the Sustainable Growth Rate

The calculation of gi assumes that the firm cannot access external capital markets (realistic for many firms). And this drives the trend in the D/E of a firm growing at gi.

Can the firm grow faster if it has access to debt markets? Yes! See picture.

If the firm grows by retaining earnings and borrowing, what will

happen to its debt-to-equity ratio over time? Uncertain, D/E can increase or decrease. If the firm cannot raise equity but can borrow, how would you

choose a growth rate that is sustainable in the long run? EEFN=0!

9

The Sustainable Growth Rate

Sustainable Growth Rate g*: the maximum growth rate a firm can

achieve without external equity financing while borrowing to

maintain a constant debt/equity ratio (given its ROE and r).

The gap between a firm’s external financing needs and the

portion that can be covered with new borrowing is called the

External Equity Financing Needed (EEFN).

10

The Sustainable Growth Rate

EEFN = EFN – New Borrowing

= ∆+𝐴𝐼𝐼𝐼𝑃𝐼 – 𝐴𝑑𝑑𝑟𝑃𝑟𝑃𝐼 𝑃𝑃 𝑅𝐸 – 𝑁𝐼𝑁 𝑏𝑃𝑟𝑟𝑃𝑁𝑟𝐼𝑔

But recall this is true under our simplifying assumptions.

Conceptually, g* is the growth rate such that EEFN = 0 !

11

Calculating the Sustainable Growth Rate EEFN = 𝐴 ∗ 𝑔 – 𝑁𝑁 ∗ 𝑟 ∗ 1 + 𝑔 – 𝑵𝑵 ∗ 𝒓 ∗ 𝟏 + 𝒈 ∗ 𝑫

𝑬

What is the last term?

𝑁𝑁 ∗ 𝑟 ∗ 1 + 𝑔 ∗𝐷𝐸

= Δ𝑅𝐸 ∗𝐷𝐸

= Δ𝑅𝐸𝐸

∗ 𝐷

Now solve for g*:

𝐴 ∗ 𝑔∗–𝑁𝑁 ∗ 𝑟 ∗ 1 + 𝑔∗ –𝑁𝑁 ∗ 𝑟 ∗ 1 + 𝑔∗ ∗𝐷𝐸

= 0

12

Calculating the Sustainable Growth Rate

𝐴 ∗ 𝑔∗– 1 +𝐷𝐸

∗ 𝑁𝑁 ∗ 𝑟 ∗ (1 + 𝑔∗) = 0

𝐴 ∗ 𝑔∗– 1 +𝐷𝐸

∗ 𝑁𝑁 ∗ 𝑟– 1 +𝐷𝐸

∗ 𝑁𝑁 ∗ 𝑟 ∗ 𝑔∗ = 0

𝐴– 1 +𝐷𝐸

∗ 𝑁𝑁 ∗ 𝑟 ∗ 𝑔∗= 1 +𝐷𝐸

∗ 𝑁𝑁 ∗ 𝑟

Note that 1 + 𝐷𝐸

= 𝐸+𝐷𝐸

= 𝐴𝐸

13

Calculating the Sustainable Growth Rate

Thus, 1 + 𝐷𝐸∗ 𝑁𝑁 ∗ 𝑟 = 𝐴

𝐸 ∗ 𝑁𝑁 ∗ 𝑟 = 𝐴 ∗ 𝑅𝑅𝐸 ∗ 𝑟

Plug this expression into 𝐴– 1 + 𝐷𝐸

∗ 𝑁𝑁 ∗ 𝑟 ∗ 𝑔∗= 1 + 𝐷𝐸

∗ 𝑁𝑁 ∗ 𝑟

𝐴 –𝐴 ∗ 𝑅𝑅𝐸 ∗ 𝑟 ∗ 𝑔∗ = 𝐴 ∗ 𝑅𝑅𝐸 ∗ 𝑟

Divide by A to get: 1–𝑅𝑅𝐸 ∗ 𝑟 ∗ 𝑔∗ = 𝑅𝑅𝐸 ∗ 𝑟

Thus 𝒈∗ = 𝑹𝑹𝑬∗𝒓[𝟏 – 𝑹𝑹𝑬 × 𝒓]

14

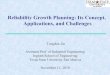

EFN vs. 𝑔,𝑔𝑟, and 𝑔∗

g

EFN

0 gi g*

15

Different Regions of Growth

Case 1 0 < 𝑔 < 𝑔𝑟 : Here RE are more than enough to finance low growth, so you can also pay dividends, accumulate cash, or do something with the money. The D/E is falling. Case 2: 𝑔𝑟 < 𝑔 < 𝑔 ∗ : Here additions to RE are more than the amount raised in debt, and thus the D/E is falling. Would it make sense to grow at g < g* ? If D/E is high, doing this for some time may be desirable

16

Different Regions of Growth Case 3: 𝑔 > 𝑔 ∗

3 choices facing the firm: Grow without issuing equity but issuing debt: D/E

increases because equity increases more slowly than debt. Is this optimal?

Eventually you would reach bankruptcy.

Grow issuing equity and debt. Is this sustainable in the long run?

Yes, provided that D/E stays constant.

Grow raising equity but not debt. D/E would be falling. Is this optimal?

Not in the long run, but maybe in the short run.

17

Back to Sumo: Calculate EFN, gi and g* Using the information for 2009, we see that A=6,000, NI=690,

ROA = 11.5%, ROE = 20.3%, and r = 2/3.

Using our formulas (based on the assumptions on slide 13): EFN (g = 20%) = 6,000 * 20% - 690 * 2/3 * 1.2 = 648 𝑔𝑟 = .115 * 2/3 / [1-.115 * 2/3] = 8.3% 𝑔∗ = .203*2/3 / [1-.203 * 2/3] = 15.6%

Note (of course) that our estimate of EFN differs from our

estimate with more realistic assumptions in slide 10.

How far off it will be depends of how much our simplifying assumptions depart from what is reasonable for the firm.

18

Back to Sumo: Calculate EFN, 𝑔𝑟 and 𝑔∗

Recall our simplifying assumptions:

i) operating expenses grow 20%.

ii) interest expenses grow 20%.

iii) accounts payable do not change.

Use the spreadsheets in Lecture 3.xls to verify that:

If 𝑔 = 20% then EFN = 648.

If 𝑔 = 𝑔𝑟 then EFN = 0 (and thus balance sheet is complete)

If 𝑔 = 𝑔 ∗ then EFN = 406.8. Note that in 2009 D/E = 76.5% and if we cover EFN with debt then in 2010 D/E = 76.5%.

19

20

21

Caveats on Financial Planning Models They do not indicate which financial policies maximize firm

value. In other words, there is no finance theory in them!

They rely on simplifying assumptions that may not be realistic (e.g., not everything grows in proportion to sales).

If you complicate them too much by adding more detail they may became less practical to use.

But they are useful tools to plan investment and financing decisions (just be aware of the assumptions).

You can use them to forecast financial needs and financial statements, which are the basis of cash flow projections!

22

Summary & Conclusions

With some simplifying assumptions we can develop simple

formulas for the internal growth and sustainable growth rates.

Comparing planned growth rates with 𝑔𝑟 and 𝑔∗ provides critical

information about a firm’s future financing needs and trend in

the debt ratio.